#GLENMARK #SANOFI #PFIZER #BPLPHARMA #MARKSANS #BIOCON #GRANULES#GLENMARK

NSE: GLENMARK

CMP: 440

TP: 515

SL: 400

TF: <6m

RR > 2 times

Return > 17%

THYROCARE CNXPHARMA LUPIN NSE:CIPLA SUNPHARMA SPARC DIVISLAB DRREDDY AUROPHARMA BALPHARMA GLENMARK SANOFI PFIZER BPLPHARMA MARKSANS BIOCON GRANULES IPCALAB LAURUSLABS NATCOPHARM GLAND ALKEM ZYDUSLIFE

Factors:

BULLISH WEDGE BREAKOUT

Trend Following

Rising Volume with rising Prices.

Flag pattern breakout.

Pennant Pattern Breakout with Bullish Candle.

Retest Successful.

Higher Highs & Higher Lows.

Broken above RESISTANCE levels

Trading at SUPPORT levels

Earnings are strong.

Bullish Wedge Breakout

Risk Return Ratio is healthy.

And

Rising from Double Bottom Pattern to Flag Pattern forming.

If you like my work KINDLY LIKE SHARE & FOLLOW this page for free Stock Recommendations.

With 💚 from Rachit Sethia

PFIZER

#CIPLA #BALPHARMA #GLENMARK #SANOFI #PFIZER #AUROPHARMA #NIFTY50#CIPLA

NSE: CIPLA

CMP: 1128

TP: 1250

SL: 1080

TF: <6m

RR > 2.5 times

Return > 11%

THYROCARE CNXPHARMA LUPIN NSE: CIPLA SUNPHARMA SPARC DIVISLAB DRREDDY AUROPHARMA BALPHARMA GLENMARK SANOFI PFIZER

Factors:

BULLISH WEDGE BREAKOUT

Trend Following

Rising Volume with rising Prices.

Flag pattern breakout.

Pennant Pattern Breakout with Bullish Candle.

Retest Successful.

Higher Highs & Higher Lows.

Broken above RESISTANCE levels

Trading at SUPPORT levels

Earnings are strong.

Bullish Wedge Breakout

Risk Return Ratio is healthy.

And

Rising from Double Bottom Pattern to Flag Pattern forming.

If you like my work KINDLY LIKE SHARE & FOLLOW this page for free Stock Recommendations.

With 💚 from Rachit Sethia

Pfizer in a bull flag.Pfizer - 30d expiry - We look to Buy a break of 48.31 (stop at 46.56)

Short term bias has turned positive.

Posted a bullish Flag formation.

A break of 48.26 is needed to confirm the outlook.

A break of the recent high at 48.26 should result in a further move higher.

Short term momentum is bullish.

This stock has seen good sales growth.

The bias is to break to the upside.

Our profit targets will be 52.69 and 53.69

Resistance: 48.00 / 49.70 / 52.00

Support: 46.70 / 46.00 / 44.70

Disclaimer – Saxo Bank Group.

Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis , like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis , as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

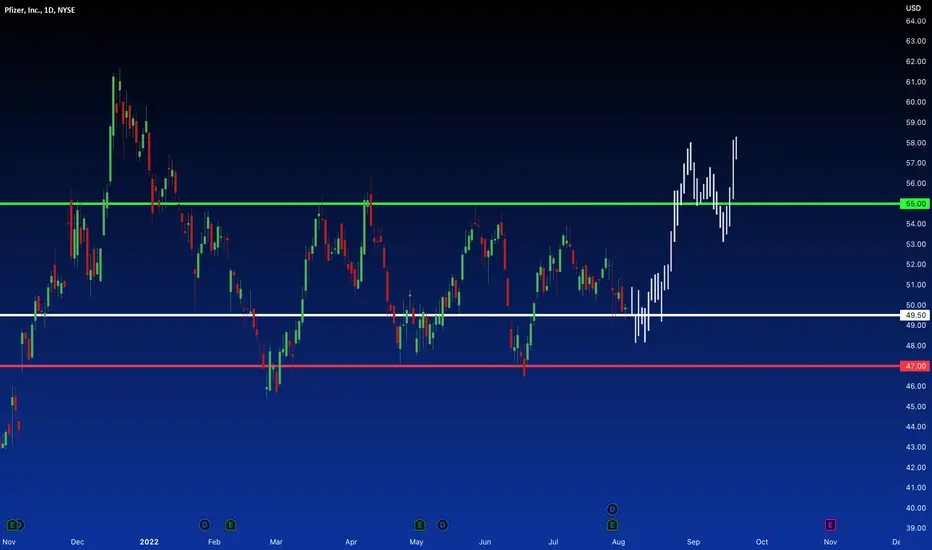

PFIZER Broke above its 2022 Bear Channel!Pfizer (PFE) broke and closed today above the Channel Down that has been dominating the 2022 Bear Market since the January 11 High. At the same time the 1D RSI has been ranging and while the 1D MA200 (orange trend-line) held successfully last time, we do expect one last test or for an even more comfortable long-term buy, the 1D MA50 (blue trend-line).

As you may notice, the Fibonacci retracement levels since the All Time High, formed solid Resistance and Support levels during the downtrend, so after the next pull-back our target will by the 0.786 Fib at 57.35.

-------------------------------------------------------------------------------

** Please LIKE 👍, SUBSCRIBE ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support me, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

You may also TELL ME 🙋♀️🙋♂️ in the comments section which symbol you want me to analyze next and on which time-frame. The one with the most posts will be published tomorrow! 👏🎁

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

PFENot financial advice. The essence of investing & trading is the intelligent and patient preying on the greed, fear, impatience, addiction and ignorance of the majority. It's definitionally Darwinian.

2X $PFE PUTS SET TO PRINT !????? Possible -10% FALL Pfizer is forming a head and shoulders pattern on the 2HR timeframe it has broken the right shoulder trendline and we will look to enter short and puts and play pfizer stock down to the next key levels!

PFENot financial advice.

The essence of investing & trading is the intelligent and patient preying on the greed, fear, impatience, addiction and ignorance of the majority. It's definitionally Darwinian.

Accumulating PFE from $46.00 - $47.50 This is one of the stocks I hold indefinitely for dividends.

we're at the bottom of our current channel and a double bottom is forming in a major area of support.

In my previous post I stated my accumulation sections are in the lower end of the channel, so this is prime real estate to enter.

Momentum downwards has come to a halt and I believe we will retest the center channel line from this point.

I am diversifying a portion of profits I made from the last 2 trade set ups I've posted into PFE. A fundamentally sound entity in our current market economy.

I'm sure you could assume why.

pfizer is ready to see $53 pfizer is ready to see $53 , it's in G diametric pattern and it's ready to compete it to make b of flat

PFE: Triangle break!Pfizer

Short Term - We look to Sell at 50.48 (stop at 52.47)

Our outlook is bearish. Broken out of the triangle formation to the downside. This is negative for sentiment and the downtrend has potential to return. Further downside is expected although we prefer to sell into rallies close to the 51.00 level.

Our profit targets will be 45.49 and 42.00

Resistance: 50.00 / 54.00 / 62.00

Support: 45.00 / 40.00 / 34.00

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Signal Centre’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Signal Centre.

Pfizer | Fundamental Analysis | Must ReadSo far this year has not been kind to stock markets. And while many drug makers have avoided a selloff, Pfizer is not one of them. The pharmaceutical giant has performed more or less on par with the broader market to date. Fortunately, Pfizer's latest quarterly report showed some very encouraging signs.

However, there are also reasons to be concerned about the future of this medical company. Let's look at one earnings-related reason why Pfizer might be a buy and one reason why it might not be.

Pfizer has made a fortune over the past couple of years through its work on coronaviruses. The company continues to benefit greatly from these efforts. In Q2, the company's revenues rose 53% year over year to $27.7 billion. According to company executives, Pfizer recorded the largest quarterly sales in its history during the period, and that was primarily due to its COVID-19 product line.

Sales of the coronavirus vaccine totaled $8.8 billion, up 20% from last year. Sales of the coronavirus drug Paxlovid were $8.1 billion (no year-over-year comparison here, since the drug received approval in December). These two drugs alone accounted for more than half of Pfizer's total revenue.

While Pfizer's line of drugs against coronaviruses is currently unparalleled, the rest of the company's portfolio is not as impressive. The non-coronavirus drug maker's revenues grew a paltry 1% year-over-year in Q2. Pfizer's line of drugs faces a number of challenges, including adverse events related to its immunologic drug Xeljanz. Xeljanz belongs to a class of drugs known as JAK inhibitors.

Last year, Pfizer published data from a post-marketing study that showed Xeljanz was associated with higher rates of cardiovascular events and cancer than TNF inhibitors, a drug category that includes AbbVie's Humira.

The results of this study, combined with a regulatory decision to add a warning about these risks to the label of Xeljanz (and other JAK inhibitors), are holding back sales of the drug. In Q2, sales of Xeljanz declined 24% year over year to $430 million. Revenues for the immunosuppressant Enbrel also fell 10% year over year to $257 million, probably because of tougher competition, which also affected its sales in Q1.

Pfizer has some good non-coronavirus numbers, including its drug Eliquis. In Q2, sales of that anticoagulant rose 23% year over year to $1.7 billion. But overall, the company has barely been able to increase sales outside of its line of coronavirus drugs. This could be a problem if sales of COVID-19 products fall sharply after this year.

In my opinion, the market is still underestimating Pfizer. First, the company will continue to make profits from Paclovid and Comirnati. COVID-19 will not (unfortunately) suddenly disappear out of thin air after this year. Even if the demand for drugs to prevent or treat the disease declines, Paxlovid and Komirnati can continue to make significant contributions to Pfizer's top-line revenue for a long time to come.

Second, while the rest of the drug line is unimpressive, pharmaceutical companies sometimes face this problem because of growing competition, patent breaks, or other factors. But drug makers generally don't have the advantage of growing sales at the rate that Pfizer does when they face such obstacles.

What matters is whether the company in question can meet these challenges. Having a solid portfolio and plenty of money to devote to research and development helps - and Pfizer has both. Thanks to the company's success in the coronavirus market, its cash balance has skyrocketed.

Pfizer has been active in acquisitions and plans to continue on that path. This should help bolster its already solid line of drugs, which has more than 90 clinical trials. Pfizer expects up to 15 new approvals over the next 18 months. Some of the current programs could go wrong. But the company has all the tools it needs to launch several new potential blockbuster drugs in the next five years. That's why investors should siphon off the company's stock before it rises in price.

PFE not making it through the trendline againPFE is touching the diagonal trendline to the upside again. Can't wait for the breakout. LT holding with nice dividend.

Pfizer: to complete the recovery journeyPfizer stock

He is about to complete the recovery journey he started from the bottom of last June 17

Its recent decline received strong support from the $50.50 barrier

And it is testing a resistance between the average 100 and 51.48 by breaching it, while reaping the momentum with a higher trading volume that increases the chances of the rise

Pfizer: Playing the range againPfizer

Short Term

We look to Sell at 54.06 (stop at 56.08)

Bespoke resistance is located at 54.50. A move higher faces tough resistance and we remain cautious on upside potential. Selling spikes offers good risk/reward. Further downside is expected although we prefer to sell into rallies close to the 54.60 level. We are trading at overbought extremes.

Our profit targets will be 46.80 and 44.60

Resistance: 54.50 / 56.32 / 61.71

Support: 50.00 / 46.50 / 40.94

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

$PFE took long profits, now shortPfizer was a good long for me $$$ now at trend line resistance and as of now showing signs of weakness IMO

At the least I think you can scalp a quick retracement here as an idea or reversion to the mean trade back down to the 10MA.

I'm long PFE 54 Put for next week, nothing major as it's short time frame and just looking for the pullback/ rejection of this resistance line here.

$SIGA BULLISH as Monkeypox is spreading around the worldNice breakout from that bullish pennant flag🔥

Monkeypox might be the next Pandemic (according to WHO) and $SIGA might be the next $MRNA (5000% up since the beginning of Covid)🚀📈

PFE, KO - Very Strong Monthly ChoicesFor anyone looking for a long position in their portfolio (Monthly) Pfizer and Coca-Cola Hodl great potential in their current state

Pfizer has formed a bullflag above the Gaussian Channel

Coca-Cola is very similar above the Channel, however lacking the bullflag

For Coca-Cola check out my previous post below

Pfizer at resistancePfizer

Short Term - We look to Sell at 54.62 (stop at 56.31)

Bespoke resistance is located at 54.70. A move higher faces tough resistance and we remain cautious on upside potential. Selling spikes offers good risk/reward. Further downside is expected although we prefer to sell into rallies close to the 54.60 level. Trading has been mixed and volatile.

Our profit targets will be 49.84 and 46.85

Resistance: 54.70 / 56.32 / 61.71

Support: 50.00 / 47.50 / 40.94

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

Pfizer:Pure Technical Play!Pfizer

Short Term - We look to Sell at 53.30 (stop at 55.53)

Price continues to trade within the triangle formation. A move higher faces tough resistance and we remain cautious on upside potential. Selling spikes offers good risk/reward. Further downside is expected although we prefer to sell into rallies close to the 53.56 level.

Our profit targets will be 48.29 and 43.36

Resistance: 53.56 / 56.32 / 61.71

Support: 47.50 / 45.44 / 40.94

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Signal Centre’) . Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Signal Centre.

Will the Moderna share price ever recover?The Moderna share price has fallen from its pandemic peak amid uncertain demand for its lifesaving mRNA vaccine. But will it ever recover?

Moderna (NASDAQ:MRNA) shares traded for more than $450 last summer. But today the stock is trading at $136 – less than a third of its pandemic peak. The vaccine-maker stock gained massively during the pandemic. Its mRNA vaccine was favoured by governments around the world, including in the US and EU. In fact, its shot was famously touted as the Rolls-Royce of vaccines, although it was also linked with very rare cases of myocarditis that perhaps caused it to be less popular than the Pfizer vaccine by those being vaccinated. Prior to the pandemic, the Massachusetts-based firm was trading for less than $15 a share.

But what comes next for Moderna? Will it return to its 2021-highs, or will it continue to fall?

Why is the share price falling?

Moderna only has one commercial product and that’s its lifesaving Covid-19 vaccine, Spikevax. The shot received emergency approval around the world in 2020 and 2021 and is considered one of the most effective vaccines in the fight against Covid-19. Like other vaccines, Spikevax was developed and approved on an accelerated schedule. While it is normal for vaccine development to take a decade from discovery to rollout, Spikevax was created and rolled out within a year.

These exceptional circumstances propelled Moderna from a company that most people had never heard of, to a household name worldwide. Its shot was one of the first four vaccines approved for use against the virus in the West. The other vaccines included the AstraZeneca shot that was sold for cost-price by the Anglo-Swedish drugs company. However, the Moderna vaccine was sold, and continues to be, for around $20-25 a dose.

In turn, this saw Moderna generate $18,4bn in 2021. The figure represents an enormous 2191% jump from 2020. In 2020, the vaccine maker saw revenues of $803m. This figure also represented a huge 1234% increase from the $60m generated in 2019. As such, we can see how the pandemic generated revenue growth in a way which is not likely to be repeated.

Moderna has strong forecasts for 2022, but the future is uncertain after that. The firm, which currently has a market cap of $55bn, says it is on track to deliver $21bn in revenue in 2022. However, forecasts from then on are mixed. While the general forecast is steeply downwards. Some analysts have predicted that Moderna’s vaccine sales will dip as low as $2bn in 2024.

So, investors are clearly concerned about revenue generation in years to come. And I think as we look around us, we can see that demand for Covid-19 vaccines is dropping. Not only among governments, but among normal citizens. Only elderly members of the British public are being offered fourth jabs right now and I’m not sure whether younger members of the population will be given free Covid-19 shots again.

What could send the share price upwards?

The less virulent nature of the Omicron strain has made vaccinations less vital. While Omicron is considerably more contagious than previous variants, it causes less severe symptoms. One thing that would send the Moderna share price soaring is the emergence of a more virulent strain, which would incentivise more vaccination. However, viruses don’t tend to evolve to become more deadly. The most successful viruses are the ones that spread, not the ones that kill their hosts.

The second thing that could reverse the negative trend in the share price is the development or launch of new products with commercial potential. mRNA technology has been lauded as having the capacity to be more easily manufactured to take on diseases such as cancer. However, the majority of Moderna’s vaccines in development concern Covid-19 and other respiratory viruses.

Moderna has two combined respiratory-virus vaccine candidates in its pipeline. One targets influenza and Covid-19. The other targets flu, Covid-19, and respiratory syncytial virus (RSV). Both candidates are in preclinical development. This sort of product could enhance the firm’s revenue generation capability, but it seems unlikely that such vaccines would be rolled out to whole populations. Instead, it would be targeted at the most vulnerable, probably just in time for the winter months. However, competitor Novavax is slightly closer to commercialising a similar product.

Moderna also has a Cytomegalovirus (CMV) vaccine in phase three trials. CMV is related to the herpes virus that causes cold sores and chickenpox. However, once you have the virus, you retain it for life. It can cause serious health problems in some babies who get the virus before birth and in adults with weakened immune systems.

The biotech firm is also developing a Zika vaccine and a personalized cancer vaccine (PCV). The PCV is in phase two trials and such vaccines, if successful, are likely to be very lucrative. The disease is one of the biggest killers worldwide and treatment can be very costly. Moderna is also working on a HIV vaccine. However, many of Moderna’s vaccines are still some distance from commercialisation. Reaching commercialisation can take a decade or longer.

Valuation

Because of the uncertain future, Moderna looks very cheap by some metrics. The biotech firm has a price-to-earnings (P/E) ratio of just four, based on its profits over the past 12 months. It also has a price-to-sales ratio of just 2.4. Moderna’s valuation is quite unique in many respects. Growth stocks tend to be expensive as they’re partially valued on future revenue potential rather than their current earnings. However, Moderna growth appears to have been short-lived, and it seems unlikely that such revenue growth can be repeated in the future.

With peak demand for Covid-19 vaccines likely past, an increase in the share price, at least in the short term, seems unlikely. However, I don’t see the stock’s share price falling much further. One forecast suggests that Moderna’s profits could fall to $2bn in 2024. If the market cap remained the same as it is today, $2bn in profit would give Moderna a P/E ratio of around 27 in 2024. That’s still expensive by some metrics, but biotech firms tend to trade at a premium given their valuation reflects future earnings potential. And Moderna clearly has some potential beyond its current Covid jab.

$PFE Call Sweeps and ER next week hmmmPfizer has ER next week and 5/20 calls sweeping today

Technically it looks like we can get a run up to ER , as PFE is at trendline support and possible "fill out" of the triangle pattern

Any run up will capture some gains, will trim position and leave a few runners for ER.

Sweeps were 55.5 and 57 strike which are pretty far out the money, worth noting. Could just be a traders Lotto on $37K of premium (must be nice haha)

Cheers

$PFE: Big weekly trend setting up...I think $PFE offers a tremendous opportunity here, good setup to enter a position with low risk vs reward potential. Could be a long term position as well, depending on how it evolves.

I'm long 12.07% here, risking a 3 times the daily ATR move against me for a 1% loss if it drops that much. Valuation is attractive and long term charts have a huge setup in $PFE, the big correction as of late seems to be over, and it's ready to go steadily up again.

Best of luck,

Ivan Labrie.

PFE: Sell Zone is 58-60Pfizer's W-4 bottomed right in our "Buy Zone" and has bounced 10% since. I expect Pfizer to continue to climb up to the $58-60 level over the coming 2 weeks or so. After that, Pfizer will pull back for it's larger degree W-2, which should bring price back to about the $50 level. We will have more clarity on pullback targets once W-5 tops, most likely in our "selling zone". The point is, this is not an idea time to start a position. I will be selling covered calls against my shares of Pfizer when we reach the selling zone, and will be looking to add shares for about $50 sometime in Late May/Early June.