Closed (IRA): EFA November 18th 50 Short Puts... for a .23/contract debit.

Comments: Opened these for .52/contract. (See Post Below). Closed here for a smidge greater than 50% max with 31 days to go. .29 ($29) profit per contract.

Premiumselling

Closed (Margin): /ES November 18th 2400 Short Put... for a 1.30 debit.

Comments: Filled this for a 3.10 credit. (See Post Below). Out here for 1.30. (3.10 - 1.30)/2 = .90 ($90) profit. Will look to add back in rungs on weakness/higher IV, assuming I can get into strikes lower than what I have on currently.

Closed (Margin): ARKK November 18th 29/50 Short Strangle... for an .83 debit.

Comments: Filled this for a 1.33 credit. (See Post Below). Out today for a .50 ($50) profit.

Opened (Margin): IWM 144/154/182/192 Iron Condor... for a 3.34 credit.

Comments: (Late Post). Another "synthetic short strangle" I put on on Friday, with the short legs set up around the 25 delta, the longs out from there to obtain a 50% ROC at max metric. 3.34 credit on buying power effect of 6.66; 50.2% at max; 25.1% at 50% max.

Will primarily look to roll paired legs (short call/long put, short put/long call) to delta balance. For example, the short call finished the day in .52/$52 worth of profit, the long put .43/$43, so I would look to roll the short call and long put down simultaneously to lock in that realized gain and to delta balance.

Opening (Margin): /ES January 20th 1600 Short Put... for a 3.20 credit.

Comments: Adding a rung out in January after taking off higher rungs in November ... . Targeting the <75% of current price strike paying around 3.00. 1.60 max on BPE of 12.42; 12.9% ROC as a function of buying power effect; 6.4% at 50% max. A basic bet that we either (a) don't see 1600 by January opex; or (b) the contract reaches >50% max before then.

Opening (IRA): QQQ December 2nd 225 Short Put... for a 2.37 credit.

Comments: My weekly, broad market exchange-traded fund short put in the symbol with the highest 30-day, targeting the <16 strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

Closed (Margin): /ES November 18th 2300 Short Put... for a 1.20 debit.

Comments: Taking off some risk/drying out some powder here for "the next one." Filled this for a 3.30 credit. (See Post Below). Taking it off here for 1.20. (3.30 - 1.20)/2 = 1.05 ($105) profit.

Closed (Margin): /ES November 18th 2200 Short Put... for a 1.05 debit.

Comments: Filled this for a 3.10 credit. (See Post Below). Closing here for 1.05. (3.10 - 1.05)/2 = 1.025 ($102.50) profit.

Opening (Margin): SPY November 18th 320/338/388/406 Iron Condor... for a 6.13 credit.

Comments: Putzing a bit with these so-called "synthetic short strangles" ... . Selling the 25's on both sides and erecting long wings out from there. I had to go oddball width with the wings (18.00) to keep the setup symmetrical, since there's only 5-wides on the put side.

6.13 credit on buying power effect of 11.87; 51.6% ROC as a function of buying power effect at max; 25.8% at 50% max. As with my QQQ setup (See Post Below), will look to roll the pairs of sides (long put/short call, long call, short put) for a realized gain and to delta balance.

Rolling (Margin): XOP October 21st Short Straddle to November 18... for a 6.93 credit.

Comments: Rolling this out "as is," betting that this weakens ... eventually. Total credits collected of 17.94. Resulting delta/theta of -46.61/22.04 with break evens of 109.06 on the put side; 144.94 on the call side.

Opened (IRA): SPY Jan/Feb/March 270/250/230 Short Put LadderOpened another tranche in this weakness, targeting successive <16 delta strikes paying around 1% of the strike price in credit.

Paid 2.72 for the January 20th 270, 2.58 for the February 17th 250, and 2.41 for the March 17th 230. Will generally take profit at 50% max or take assignment, sell call against if that occurs.

Opening (IRA): QQQ November 25th 235 Short Put... for a 2.80 credit.

Comments: My weekly, broad market short put in the exchange-traded fund with the highest 30-day IV, targeting the <16 delta strike paying around 1% of the strike price in credit.

Opening (Margin): /ES December 30th 1900 Short Put... for a 3.15 credit.

Comments: Adding a smidge back in, after taking off a couple of my higher risk rungs in October. 1.575 ($157.50) max on BPE of 13.75 ($1375); 11.5% ROC (50.0% annualized) as a function of buying power effect; 5.7% at 50% max (25.0% annualized). A basic bet that the S&P doesn't lose 50% of its value by year end.

Closed (Margin): /ES October 31st 2700 Short Put.. for a 1.55 debit.

Comments: Filled this for a 3.10 credit. (See Post Below). Hit 50% max today. Drying out some powder for the next bout of weakness. (3.10-1.55)/2 = .775 ($77.50) profit.

Closed (Margin): /GC November 22nd 1380 Short Put... for a .70 debit.

Comments: Filled this for a 1.40 credit. (See Post Below). Out at 50% max today; .70 ($70) winner.

Closed (Margin): SMH October 21st 190C/205P Short Strangle... for a 22.80 credit.

Comments: Collected a total of 22.93 for this. (See Post Below). Took the opportunity to take it off for a minuscule winner (.13/$13) in this up move.

Closed (Margin): /ES October 21st 2850 Short Put... for a 1.45 debit.

Comments: Filled this for 3.05. (See Post Below). Closing out my most at risk strike here with 18 days to go, resulting in a (3.05 - 1.45)/2 = 1.60 ($160) profit.

Opening (Margin): QQQ November 18th 240/260/314/334 Iron Condor... for a 6.31 credit.

Comments: Moving out to November, which is still a bit long-dated ... . Selling the 23's on both sides for my short legs, erecting longs 20 strikes out from there. 6.31 on BPE of 13.74; 45.9% ROC at max; 23.0% at 50% max.

Here, I'm looking to manage just the short strangle aspect of the setup to delta balance if necessary, leaving the longs alone to safety tape off max loss as well as keep the buying power effect somewhat fixed. As I adjust the short options, however, the spread on one side or the other will widen, thereby increasing buying power effect, since that is attributable to the widest wing. For example, if I roll the short call down by one strike (1.00) and I get a .75 credit for doing that, the buying power effect will increase to 21.00 (since I've widened the wing to 21). However, I will have received a .75 credit for doing that, so my BPE will increase by 1.00 - the credit received or .25 ($25).

As with a naked short strangle, I'll look to adjust just the short strangle aspect of the setup at a delta/theta ratio of >1.00. It's currently .01/17.93.

Opening (Margin): /ES December 16th 1800 Short Put... for a 3.10 credit.

Comments: Adding a rung in the December monthly at a lower strike than what I currently have on, targeting the <75% of current price strike paying around 3.00. 1.55 max on buying power effect of 18.38; 8.4% ROC at max as a function of buying power effect; 4.2% at 50% max.

Opened (Margin): ARKK November 18th 29/50 Short Strangle... for a 1.33 credit.

Comments: (Late Post; Filled on Friday). High IVR/IV at 62.9/68.6%.

Opening (IRA): EFA November 18th 50 Short Put... for a .52/contract credit.

Comments: Slowly building an EFA (ex. Canada/U.S.) position here on weakness. Targeting the <16 delta strike paying around 1% of the strike price in credit.

Opening (IRA): QQQ November 11th 235 Short Put... for a 2.57 credit.

Comments: My weekly, broad market short put in the exchange-traded fund with the highest 30-day, targeting the <16 delta strike in the shortest duration expiry that pays around 1% of the strike price in credit.

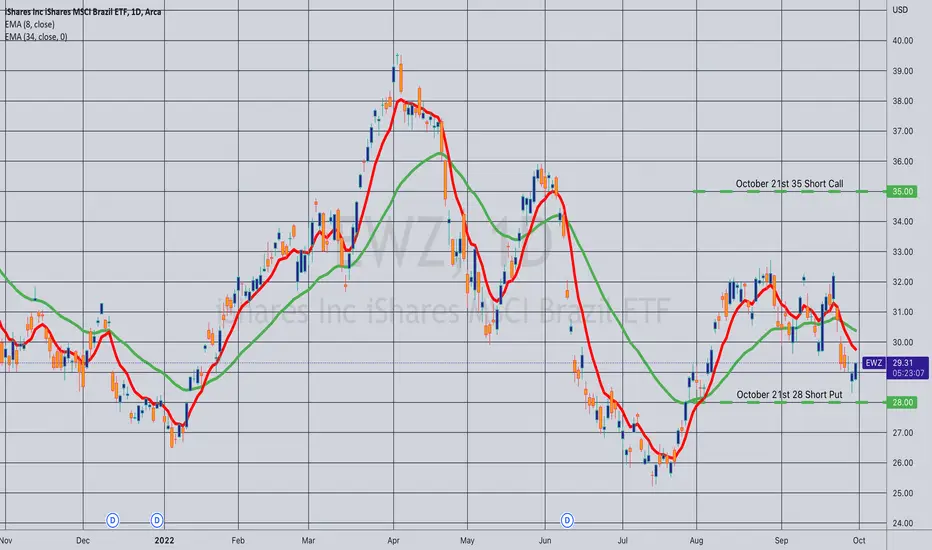

Closing (Margin): EWZ October 21st 28/35 Short Strangle... for a 1.25 credit.

Comments: Closing out at 21 days for a small loss (.07/$7). With this volatility expansion here, I want to redeploy into the biggest bang for my buck, which may or may not be in EWZ.