MR. COPPER GOES FUN. WITH DONALD TRUMP — IT IS A BULL RUNCopper prices in 2025 are up about 27 percent year-to-date, driven by a complex interplay of technical and fundamental factors, with geopolitical events such as the Trump administration's tariff policies and the escalation of geopolitical tensions in the Middle East having a significant impact.

Fundamental Outlook:

The main driver of copper prices in 2025 is the ongoing global surge in demand driven by the transition to clean energy. Copper is essential for electric vehicles (EVs), renewable energy infrastructure, and grid upgrades, all of which require extensive use of copper due to its superior electrical conductivity.

For example, EVs use about 2-4 times more copper than traditional vehicles, and renewable installations such as wind turbines contain several tons of copper each. This structural growth in demand underpins the optimistic outlook for copper in the medium to long term.

On the supply side, however, copper production is growing. The International Copper Study Group (ICSG) forecasts a global copper surplus of 289,000 tonnes in 2025, more than double the 2024 surplus. This surplus is driven by rising production, particularly from new or expanded operations in the Democratic Republic of Congo, Mongolia, Russia and elsewhere.

Capacity increases in these regions, coupled with smelter growth, could contribute to a supply glut despite strong demand.

Conversely, geopolitical tensions in the Middle East could disrupt bauxite and alumina supply chains, a region that is a strategically important supplier of raw materials.

Impact of Trump Tariffs:

The Trump administration’s threats and actions to impose tariffs on U.S. copper imports have added volatility and complexity to the market. The tariff announcement triggered a sharp sell-off in early April 2025 as concerns about the impact on US manufactured demand and global trade flows grew. London Metal Exchange (LME) copper prices fell to one-month lows following China’s retaliatory tariffs, before partially recovering after some tariff exemptions and reductions were announced.

The tariffs also distorted physical supply chains. Traders rushed to deliver copper to the US ahead of the tariffs, reducing copper availability in other regions such as China. This arbitrage resulted in a significant widening of the price differential between US CME copper contracts and LME copper prices, with US prices trading at a premium of over 10% to London. This premium reflects the tariff risk embedded in the US copper price and expectations of temporary domestic market tensions.

Technical Outlook:

Technically, copper prices have shown resilience despite the tariff shocks. Copper prices sold off after peaking in late March 2025 before the tariffs were announced, but have since begun to recover.

Long-term trendlines and moving averages remain supportive, with the 100-week and 200-week moving averages trending higher and forming a bullish crossover earlier in the year.

Long-term copper prices are once again attacking the 18-year resistance around $4.50/lb ($10/kg) that capped the upside in 2008 and again in the 2010s and first half of the 2020s, with a 1.5x rally in the next 1 to 3 years.

The technical main chart of the COMEX December 2025 copper futures contract COMEX:HGZ2025

points to the possibility of an upside move, all the way to the $7 mark (around $15/kg) as early as H2 2025.

Conclusion

Going forward, copper prices are expected to remain volatile but supported by long-term structural demand growth, with the impact of tariffs likely to cause episodic disruptions rather than a sustained suppression of increasingly hot prices.

--

Best wishes,

@PandorraResearch Team😎

Recessionwatch

Bull in a China Shop. The S&P 500 Index After 100 Days of TrumpPresident Donald Trump's first 100 days in office were the worst for the stock market in any postwar four-year U.S. presidential cycle since the 1970s.

The S&P 500's 7.9% drop from Trump's inauguration on Jan. 20 to the close on April 25 is the second-worst first 100 days since President Richard Nixon's second term.

Nixon, after taking office as President of the United States (for the second time) on January 20, 1973, witnessed the S&P 500 index fall by 9.9% in his first 100 days in office, due to the unsuccessful economic measures he took to combat inflation, which led to the recession of 1973-1975 when the S&P 500 index losses of nearly to 50 percent.

It all started in January 1973 in the best soap opera traditions of Wall Street, at the historical peaks of the S&P 500 index..

..But less than two years later it quickly grew into a Western with a good dose of Horror, because the scenario of a 2-fold reduction of the S&P 500 index was unheard those times for financial tycoons and ordinary onlookers on the street, since the Great Depression of the 1930s, that is, for the entire post-war time span since World War II ended, or almost for forty years.

Nixon later resigned in 1974 amid the Watergate scandal.

On average, the S&P 500 rises 2.1% in the first 100 days of any president's term, according to CFRA, based on data from election years 1944 through 2020.

The severity of the stock market slide early in Trump's presidency stands in stark contrast to the initial "The Future is Bright as Never" euphoria following his election victory in November, when the S&P 500 jumped to all-time highs on the belief that Mr. Trump would shake off the clouds, end the war in Ukraine overnight, and deliver long-awaited tax cuts and deregulation.

Growth slowed and then, alas, plummeted as Trump used his first days in office to push other campaign promises that investors took less seriously, notably an aggressive approach to trade that many fear will fuel inflation and push the U.S. into recession.

The S&P 500 fell sharply in April, losing 10% in just two days and briefly entering a bear market after Trump announced “reciprocal” tariffs, amid a national emergency that gave him free rein to push through tariffs without congressional oversight.

Then Trump began yanking the tariff switch back and forth, reversing part of that tariff decision and giving countries a 90-day window to renegotiate, calming some investor fears.

Many fear more downside is ahead.

Everyone is looking for a bottom. But it could just be a bear market rally, a short-term bounce of sorts.

And it's not certain that we're out of the woods yet, given the lack of clarity and ongoing uncertainty in Washington.

Time will tell only...

--

Best 'China shop' wishes,

@PandorraResearch Team

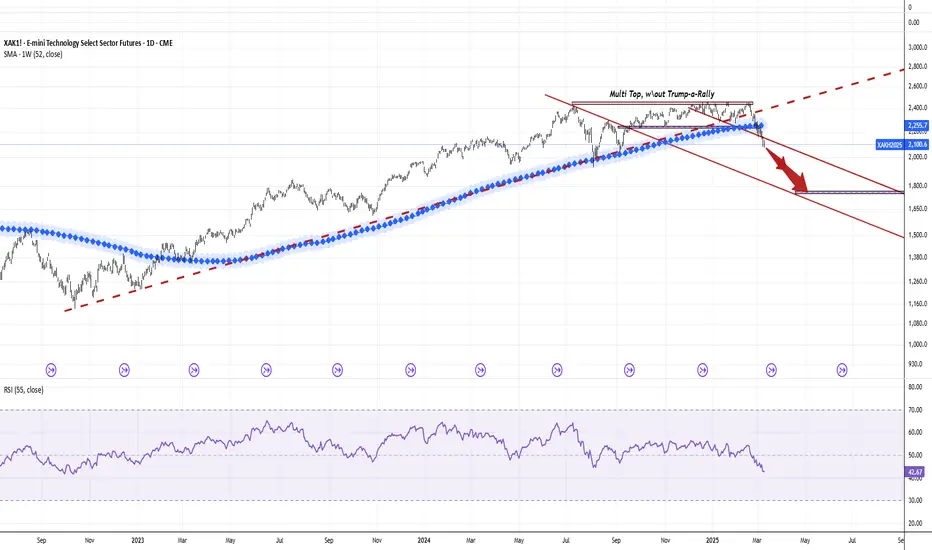

US Technology Sector Futures. The Heartbreak HotelPresident Donald Trump's tariffs on imported tech goods, targeting China, the EU, Canada, and Mexico, are reshaping the U.S. technology sector through higher costs, supply chain disruptions, and retaliatory trade risks. While intended to boost domestic manufacturing and reduce trade deficits, these measures are creating immediate economic strain across critical industries. Below is an analysis of their key negative impacts:

Rising Consumer Prices and Hardware Costs

The 25% tariff on EU semiconductors, 10% levy on Chinese goods, and 25% duties on Canadian/Mexican imports are projected to add $50 billion in new costs to North American tech supply chains. This directly affects consumer electronics:

Smartphones and laptops. Apple’s iPhone production in China exposes it to 10% tariffs, likely forcing U.S. price hikes.

Semiconductors. The U.S. relies on China and Taiwan for 80% of 20-45nm chips and 70% of 50-180nm chips, with tariffs disrupting access to essential components.

Cloud/AI infrastructure. Steel and aluminum tariffs (25%) increase data center construction costs, potentially raising prices for AWS, Google Cloud, and Microsoft Azure services.

Experts warn companies may pass 60-100% of tariff costs to consumers rather than absorb profit losses.

Supply Chain Disruptions and North American Integration

The tariffs jeopardize tightly integrated North American production networks:

Cross-border dependencies. Components often cross U.S.-Mexico or U.S.-Canada borders multiple times during manufacturing. Christine McDaniel of the Mercatus Center notes this integration means tariffs “hurt the pricing power of the U.S.” by inflating domestic costs.

Critical material shortages. Canada supplies nickel and cobalt for batteries, while Mexico handles assembly for firms like Foxconn. Tariffs risk delays and renegotiations with suppliers.

Retaliatory measures. The EU may respond with fines or trade barriers against U.S. tech giants like Apple and Google, escalating tensions.

Sector-Specific Challenges

Semiconductors and Hardware

Chip shortages. With limited domestic foundry capacity, tariffs on EU semiconductors threaten AI development and device manufacturing.

Networking equipment. Proposed 10% tariffs on Chinese-made routers and modems could disrupt cloud providers reliant on these components.

Data Centers and AI

Construction delays. Steel/aluminum tariffs increase costs for server racks and cooling systems, potentially delaying $80 billion in planned U.S. data center investments.

AI infrastructure. Projects like the $500 billion Stargate initiative face higher expenses for imported components, slowing AI adoption.

Macroeconomic Risks

Trade deficit growth. Despite tariffs aiming to reduce the $1 trillion U.S. goods trade deficit, S&P Global warns retaliatory Chinese tariffs could worsen imbalances.

Job losses. Economic modeling suggests tariffs may cost 125,000+ U.S. tech jobs through reduced consumer spending and IT budget cuts.

Innovation slowdown. While firms like TSMC and Intel accelerate U.S. fab construction, short-term supply chain reallocations divert R&D funding.

Corporate Responses and Limitations

Some companies are attempting mitigation strategies:

Stockpiling. NVIDIA and AMD are urging partners to increase pre-tariff production.

Domestic shifts. Apple plans $500 billion in U.S. manufacturing, while TSMC pledged $160 billion for stateside fabs.

However, these efforts face scalability issues. Building advanced chip foundries takes 3-5 years, leaving gaps in critical components. Meanwhile, 65% of IT firms report difficulty finding tariff-free alternatives for Chinese inputs.

Technical challenge

The main technical graph for US Technology Select Sector Futures CME_MINI:XAK1! (CME Group mode of AMEX:XLK - SPDR Select Sector Fund - S&P500 Technology ETF) indicates on further Bearish market in development since major support of 52-week SMA has been broken already, with possible upcoming Bearish cascade effects in the future.

It is also important to note the almost complete absence of a Trump-a-rally in the 2024 holiday quarter, which contributed to the formation of a multi-resistance top.

Conclusion

While the tariffs aim to strengthen U.S. tech autonomy, their immediate effects—higher prices, supply instability, and strained international relations—outweigh potential long-term benefits. With global IT spending still projected to grow 9% in 2025, the sector’s resilience is being tested by policy-driven headwinds that threaten America’s competitive edge in semiconductors, AI, and consumer electronics.

Investing in S&P500 Technology Sector Futures / ETFs seeks to provide precise exposure to companies from technology hardware, storage and peripherals; software; communications equipment; semiconductors and semiconductor equipment; IT services; and electronic equipment, instruments and components industries; allows investors to take strategic or tactical positions at a more targeted level than traditional wide style based investing.

S&P500 Technology Sector Futures / ETFs are designed for investing at a more targeted Technology level, since nearly 50 percent of holdings weight just a five well-known names:

Name Weight

APPLE INC NASDAQ:AAPL 15.61%

MICROSOFT CORP 12.83%

NVIDIA CORP NASDAQ:NVDA 11.91%

BROADCOM INC NASDAQ:AVGO 5.18%

SALESFORCE INC NYSE:CRM 3.11%

--

Best 'Heartbreaking' wishes,

@PandorraResearch Team 😎

One Chart to Rule them All ~ 10Y/2Y and 10Y/3M Yield Spreads10Y/2Y and 10Y/3M Yield Spread

One chart to rule them all. I have combined the 10Y/2Y Yield Spread (purple line) and the 10Y/3M Yield Spread (blue line) onto one chart. You can get updated readings on it at anytime on my TradingView page (link in bio above)

I have measured the historic timeframe from un-inversion to recession for both datasets. Un-inversion occurs when the yield spread rises back above the 0 level.

Given the 10Y/2Y Yield Spread has just un-inverted (moved above 0), I thought this a worthy exercise. The findings are interesting and useful.

Main Findings / Trigger Levels

The findings are based on the last 4 recessions (this as far back as the 10Y/3M Yield Spread chart will go);

▫️ Before all four recessions both yield spreads un-inverted (only one has to date);

- At present only the 10Y/2Y yield spread has un-inverted (2nd Sept 2024), thus we can watch for the next warning signal which is an un-inversion of the 10Y/3M yield spread. Without both yield spreads un-inverting the probability of recession is reduced.

▫️ The 10Y/2Y typically un-inverts first and the 10Y/3M un-inverts second.

-Historically the delay between the 10Y/2Y and the 10Y/3M un-inversion is between 3 to 10 weeks (23rd Sept – 11th Nov). This is the date window that we can watch for a 10Y/3M un-inversion (based on historic norms).

-If we move outside this window beyond the 18th Nov with no 10Y/3M un-inversion, then we are outside the historic norms and something different is happening. Nonetheless watching for the un-inversion of the 10Y/3M after this date could be consequential.

▫️ On the chart I have used the last four 10Y/2Y yield spread un-inversion timeframes to recession and created a purple area to forecast these from the recent the inversion on the 2nd Sept 2024 forward (Labelled 1 - 4). This creates a nice visual on the

chart. Based on these historic timeframes and subject to the follow up 10Y/3M un-inversion confirming in coming weeks, the potential recession dates are as follows (also marked on chart);

1.28th Oct 2024 (based on 2000 10Y/2Y un-inversion to recession timeframe)

2.03rd Feb 2025 (based on 2020 10Y/2Y un-inversion to recession timeframe)

3.12th May 2025 (based on 2007 10Y/2Y un-inversion to recession timeframe)

4.25th August 2025 (based on 1990 10Y/2Y un-inversion to recession timeframe)

✅ Remember, you can check in on this chart and press play to get updated data at any time by clicking the link in the comments below or by following me on TradingView👍

▫️ I will include a table in the comments which outlines all of the above metrics with dates. I will also share a chart with a zoomed in version of present day so that all the above trigger dates can be more closely monitored.

Finally, it’s important to recognize that these findings and trigger levels are based on the last four recessions. There is no guarantee that a recession will occur or occur within the set trigger levels. What we have is a probabilistic guide based on historic patterns. This time could play out very differently or not play out at all. Regardless, all of the above findings help us gauge the probability of a recession with historic timeframes to watch. It leaves us better armed to make the necessary risk adjustments, particularly if the 10Y/3M yield curve un-inverts.

Price is king, and at present, prices are pressing higher on most relevant market assets. From the above findings and the current positive market price action, it appears we have a little more time before being hauled into a longer-term correction or recession. I lean towards the later dates (2, 3, and 4 above) for this reason. Interestingly, many of my historic charts from months ago and last year suggested Jan/Feb 2025 (also option 2 above) as a very high-risk period. You can view these charts under the above specific chart on TradingView.

This chart is your one-stop shop for checking recession trigger levels based on historic timeframes for both yield spreads. You can update this chart data anytime on my TradingView page with just one click. Be sure to follow me there to access a range of charts that will help you assess the direction of the economy and the market. Thanks again for coming along!

Remember, you can check in on this chart and press play to get updated data at any time by clicking the link in the comments below or by following me on TradingView.

Thanks

PUKA

ISM Manufacturing & ISM Services PMI Combined show trigger levelISM Manufacturing and ISM Services PMI Combined 🪢

This week the ISM PMI's were released as follows:

🚨ISM Manufacturing PMI = 47.2 (contractionary)

✅ISM Services PMI = 51.5 (expansionary)

With both metrics offering mixed signals, I decided to make a chart that combines the ISM Manufacturing and ISM Services PMI into one dataset on the chart.

Interestingly it provided a clean chart with many patterns to observe, and useful forward looking trigger levels to keep an eye on. Don't forget you can update on this chart data anytime on my TradingView page with one click.

At present you can see that the data is compressed into a something resembling a "Darvas Box". I understand this not price but data, however this economic data is clearly in a compressed channel and appears uncertain in terms of a definitive direction. It has also never been in a pattern like this for this long in the past, which could mean a break out up or down is closer than it is further away.

Prior patterns have demonstrated that break throughs of both diagonal and horizontal support lines has resulted in significant downward movements. This is evident on the chart and this is something we can watch out for should we break below the box.

Consistent with past recession's the Combined PMI dropped below the 50 level (🔴red circles) way back in Dec 2022. Since then we have oscillated around the 50 level in the compressed box in indecisive fashion.

Never has the data behaved specifically this way in the past, specifically for this long. There are no other compressed boxes of data lasting this long. At some stage the ISM Data will push the its way out of this box I have drawn and it could be a good indicator to observe for early signals of the direction of the economy in the U.S. as a whole (both services and manufacturing combined)

As always, this chart in on my TradingView page, and you can click on it at any stage to get an updated reading on the chart so you can quickly get a visual update on the direction of the U.S. Economy via combined ISM PMI's.

Enjoy

PUKA

Federal Reserve is Behind the Curve, Recession is 100% CONFIRMEDHello everyone,

The federal reserve has kept interest rates at near zero and printed the MOST money in US history back in 2020 and this has caused one of the worst inflation in 40 years. Jerome Powell decided to fight inflation by giving us the fastest rate raising campaign in history. He has kept rates too high for too long and we are now guaranteed a recession. Jerome Powell will find himself in a position to cut rates very fast due to the cracks in the job market. It is already too late we will be witnessing a huge spike in unemployment. Who knows how high this can go, back in 1929 unemployment hit 24.9%.

Macro Monday 60 ~ Japanese Yen Recession Signal Macro Monday 60

Japanese Yen Recession Signal

If you follow me on Trading view, you can revisit this chart at any time and press play to get the up to date data and see if we have hit any Yen recessionary trigger levels. Very handy to have at a glance.

The Chart

The chart illustrates how the Japanese Yen / U.S. Dollar has followed a similar trajectory as the U.S. Unemployment Rate. The chart demonstrates that the Yen price has behaved in a particular way prior to recessions (red areas). You might be wondering how the Yen can offer insights into economic recessions and how they are linked;

1. Historically, the yen has strengthened during recessions due to the reduction of U.S. interest rates that typically coincides with recessions. When the U.S. Federal Reserve lowers rates, it makes the yen relatively more attractive to investors. With rate cuts highly likely in September 2024 the Japanese Yen is likely to see positive price action against the U.S. dollar.

2. The BOJ has historically intervened to prevent the Yen from becoming too strong. A strong yen negatively impacts Japan’s export-reliant economy. However, this trend shifted in 2022 when Tokyo stepped in to defend the Yen’s value. The BOJ bought Yen after expectations that other central banks would raise rates while the BOJ kept rates ultra-low.

3. In July 2024, the BOJ raised interest rates and signaled further policy tightening. Concerns about the historically weak yen also played a role (evident on the chart by the 30 year low in June 2024). This move, along with U.S. growth concerns, triggered an unwinding of carry trades (where investors borrow cheaply in yen to invest in higher-yielding assets), causing the yen to rebound against the dollar.

The chart along with the above three points are suggesting the Yen may be about to rise significantly in coming months versus USD. This direction of price for the Yen is consistent with the early signs of recession onset, in particular if the Yen increases in value by 22% to 42% (see below).

Japanese Yen vs U.S. Unemployment Rate

The blue numbers and corresponding blue box on the chart suggests that a sudden 22% – 42% increase in the Japanese Yen / U.S. Dollar (from below the 0.008200 level) typically precedes recessions. This 22 – 42% increase in the yen is something we can look out for in combination with other recession charts we have in our current armory. See my most recent charts.

▫️ Above we discussed some macro-economic factors that suggest a high probability of the Yen ascending higher. The yen price also made a 30 year low in June 2024 and now appears to be breaking higher.

▫️ We now have levels on the chart to watch; the 22% level and the 42% level. In the event the Yen rises to these levels alongside the U.S. Unemployment Rate continuing to increase, this would significantly raise the probability of recession in subsequent months.

Summary

▫️ The chart captures how the Japanese Yen has followed a similar trajectory as the U.S. Unemployment Rate. When both move in unison up and to the right it typically isn’t a good sign for the economy.

▫️ A number of macro-economic factors suggest the Yen is about to increase e.g. Likely lowering of interest rates in the U.S will make the dollar more affordable to borrow and increase its supply weakening its strength whilst increasing the strength/value of the Yen.

▫️ The chart demonstrates that increases in Yen from below 0.008200 by 22% - 42% typically precede recessions. Theses levels are etched on the chart for you to monitor.

▫️ As the Yen price made a 30 year low in June 2024 and now appears to be breaking higher and with the addition of macro-economic events suggest a higher Yen, its now more important than ever to monitor the Yen and its historic recession trigger levels at 22% and 42%. These are on the chart for your convenience. You can revisit this chart at any time and press play to get the up to date data and see if we have hit any JPY recessionary trigger levels.

Japan Trade Opportunities

Given the higher probability that the Yen is increasing, this heightens the probability of recession, however it also means some Japanese stocks might offer a nice back end currency benefit over coming two years. Do you know any good Japanese Value stocks? If you do, be sure to share them below for some recession proof, back end currency promising trades.

As always, its been a pleasure

PUKA

Buyback Watch for Swing TradingEarnings are over so buybacks are back in the mix. The market is likely to continue to be volatile and choppy until all the ETF investors who want to sell have done so. Then, the uptrend is likely to resume because there are not enough barometers warning of a recession AND we just had one 3 years ago.

Buybacks tend to drive price up, so they are a good swing and momentum trading strategy. Notice how neatly the support from previous highs halted the run down. Reversal points at strong support levels are one area to watch for buyback patterns.

Euro Area Interest Rate Reduction a signal? Euro Area Interest Rate

◻️Reduced from 4.5% to 4.25% as expected

◻️We can acknowledge the pattern & recognize its significance without jumping to any immediate conclusions

◻️Chart will need to be combined with others to make assertions, such as the 10Y/2Y Yield Spread

U.S. 10Y/2Y Yield Spread with U.S. Unemployment rate

The amount of months that have passed prior to recession initiation after the yield curve makes its first turn back up towards 0% level

◻️ Historical Average timeframe is April 2024

◻️ Historical Maximum timeframe would be Jan 2025

No guarantee that history will repeat. Again, just a chart and some data that is worth keeping an eye on. Some people state the bond market is now broken and manipulated, we should know within 12 - 18 months, or sooner.

PUKA

Macro Monday 13~Purchase Managers IndexMacro Monday 13

ISM Purchasing Managers Index

The ISM Purchasers Managers Index (PMI) measures month over month change in economic activity within the manufacturing sector.

The PMI is a survey-based indicator that is compiled and released each month by the Institute for Supply Management (ISM). The survey is sent to senior executives at more than 400 companies in 19 primary industries, which are weighted by their contribution to U.S. Gross Domestic Product (GDP).

A PMI above 50 represents an expansion in manufacturing when compared with the previous month. A PMI reading under 50 represents a contraction while a reading at 50 indicates no change. The further away from 50, the greater the level of change.

According to Investopedia "ISM data is considered to be a leading indicator of economic trends. Not only does the ISM Manufacturing Index report information on the prior two months, it outlines long-term trends that have been building over time based on prevailing economic conditions".

The ISM reports are released on the first business day of each month for the month that has previously closed. Thus, they are some of the earliest indicators of current economic activity that investors and business leaders get regularly. Something to look out for next Monday 2nd October 2023.

The PMI focuses mainly on the five major survey areas;

1. Employment (20%)

2. New orders (30%) Covered in Macro Monday 6

3. Production/Output (25%)

4. Inventory levels (10%)

5. Supplier deliveries (15%)

We covered the ISM New Orders Index in Macro Monday 6 as it is the largest component of the Purchaser Managers Index making up 30% of the overall index. I will leave a link to the chart.

The Chart

The chart outlines the last 12 recessions (shaded red zones) with the PMI readings over the same period. As we are already aware above 50 on the PMI reading is expansionary and below 50 is contractionary (red thick line).

Three Main Findings

1. In 11 out of 12 recessions a PMI reading at or below 42 was established. This means if the PMI falls to 42 there is a 92% probability of a recession. At present we have not reached that level, we are currently at 47.6.

2. The PMI has bottomed 10 out of 12 times in Quarter 1 (between Jan – March) with the remaining two bottoms happening in Quarter 2 (both in May). This means that 83% of the time the PMI cycle appears to bottom in Quarter 1 with the most bottoms in January (6) with Feb(2) and May(2) in close second place.

- It’s worth noting that the bottom of the PMI cycle

may not be the bottom of a stock market cycle. If

we are forward looking then a rising PMI is positive

for the economy and markets but ideally a move

above 50 is the true signal of economic expansion

from a manufacturing standpoint.

3. The average PMI bottom to bottom cycle timeframe over the past 6 cycles is 58 months with the shortest being 37 months and the longest being 86 months. We are currently at month 38 and the average month of 58 is Jan 2025 with the max of 86 months being May 2027.

- How interesting is it that both these potential PMI

bottom dates line up with our two most frequent

PMI bottom months indicated in point 2 (January

and May).

- Interestingly according to U.S. government

research, since WWII the business cycle in America

takes, on average, around 5.5 years which closely

aligns with our 58 month (or roughly 5 year)

indication for the PMI chart. The business cycle

incorporates an aggregate of economic data such

as the ISM data, GDP and income/employment

metrics. We might cover the business cycle in more

detail on a future Macro Monday.

The ISM New Orders Index (30% of the PMI)

Similar to the ISM New Orders Index Chart (covered in Macro Monday 6) which makes up 30% of the PMI, we have not reached below the 42 level on this chart either which has provided a 100% confirmation of recession when we have had a definitive move below the 42 level historically.

For ISM New Orders if we stay below a sub 50 level on the ISM New Orders Chart for greater than 7 months it has resulted in a recession every time except for 1966 and 1995 (8 out of 10 times). We are currently 14 months below the 50 level which is unprecedented, with the new orders index nudging a little lower on the August reading from 47.3 down to 46.8.

ISM Data Release 2nd October 2023

When we receive our next ISM Data release next Monday 2nd October 2023 we can refer back to the PMI chart and the New Orders Index Chart and see how things have progressed and if we have reached and critical levels.

These charts and the others I have completed on Macro Mondays are all designed so that you can revisit them at any point and press play on TradingView and see if we are breaking new into higher or lower risk territory.

I hope they all help towards your investing and trading decisions.

Have a great Monday guys, Lets get after it!

PUKA

ISM Manufacturing New Order IndexMacro Monday (6)

United States ISM Manufacturing New Order Index - ECONOMICS:USMNO

This week I have honed in on the Institute of Supply Management Manufacturing New Orders Index (ISM New Orders Index) as it is the largest component of the headline Purchaser Managers Index(PMI) making up 30% of that index. I also make the case below for how it can act as leading indicator of demand by way of trend projection.

The ISM New Orders Index is an indicator of U.S. economic activity based on a survey of more than 300 purchasing managers at manufacturing firms advising if orders have increased, decreased or stayed the same. Survey responses reflect the change, if any, in the current month compared to the previous month.

A reading above 50 indicates the expansion in the manufacturing sector which is interpreted as a positive indicator of economic growth. A reading below 50 indicates a contraction in the manufacturing sector which suggests a slowing economy.

According to Investopedia "ISM data is considered to be a leading indicator of economic trends. Not only does the ISM Manufacturing Index report information on the prior two months, it outlines long-term trends that have been building over time based on prevailing economic conditions".

The ISM reports are released on the first business day of each month for the month that has previously closed. Thus, they are some of the earliest indicators of current economic activity that investors and business people get regularly.

ISM New orders provide an indication of current consumer demand. Utilizing a chart of New Orders readings we can attempt to understand the trend of consumer demand forward. ISM New Orders could be considered an additional gauge of consumer sentiment because if businesses are reporting increases in orders month over month, this demonstrates consumers have the consistently had the resources and the desire to spend. If this continues over months a trend can form and we can capture this direction on a chart.

To support the ISM predictive argument I include a chart that illustrates a correlation between the ISM Manufacturing New Orders Index and the University of Michigan Consumer Sentiment Index, the latter of which is considered one of thee leading indicators for predicting future consumer spending/demand. This will be posted in the comments.

According to the University of Michigan, the Consumer Sentiment Surveys "have proven to be an accurate indicator of the future course of the national economy."

Based on the above correlation I postulate that we can use the ISM New Orders Index as an additional leading/predictive indicator to establish what direction consumer demand is trending.

The ISM New Orders Chart

Focusing on the ISM Manufacturing New Orders Index Chart you can see that a breach below the sub 50 level can act as a leading or affirming indicator of a slowing economy, lowering consumer demand/sentiment and ultimately recession.

Orange Zone

Historically If we enter into the orange area and stay there for greater than 7 months it has resulted in a recession every time except for 1966 and 1995 (8 out of 10 times). Some analysts have recognised and compared the similarities of the current period to the 1995/96 period. The similarities are evident on this chart with two touches or bounces from the red zone which appears to be happening at present. The August and September ISM New Orders reading will ultimately tell us if this will play out similar to 1995/96 or not. We know what to expect if it doesn’t.

Red Zone

Anytime we have entered into the red zone we have confirmed a recession. Its key to realise that recessions are typically assigned 8 months after they have started and this could mean we are already in one... Interestingly we have toe dipped into the red zone twice, in Feb and May 2023 however I do not see this as a definitive move into the red zone, I see these as bounces from this level as noted above.

Moment of Truth for ISM New Orders

What is clear from looking at the chart is that we are at a critical juncture as we have been 13 months in the orange zone which is a historic first. The coming months readings for August (released Sept) and September (released Oct) will be vitally important for providing an indication of the direction of the economy.

A drop down into the red zone and you know what to expect. A rise out of the orange area and above the 50 level would be positive however we have been rejected from areas above 50 in the past (see red lines on chart). I have included some rough fractals from periods in the past (arrows in grey) where we were previously rejected from the 52 and 54 level only to be dumped back into the red and into recession. It’s great that we are aware of these potential false flags so that we don’t get ahead of ourselves. It’s important to note that these fractal examples from 1980, 1990 & 1967 are not projections, just observations from past readings on what may be possible. It only highlights that we need to be cautious, even if we rise above the 50 level, we can be rejected into recession from the 52 and the 54 level. This is why we need help from other charts and indicators to help gauge the likelihood of a continuation higher or rejection lower.

Here on Macro Mondays we have been and will continue to build a portfolio of leading market charts/indicators that you can check for free on my Trading View and see how they are all progressing. These charts will include trigger events and will be updated as matters progress. The charts can help inform you of the direction of the economy, the market and help you anticipate or time any potential looming recession.

Some prior charts and their indications to date (all linked under this article);

Concerning Charts:

o Macro Monday 2 – The 2/10 year Treasury Spread FRED:T10Y2Y : The current yield curve inversion on the 2/10 year Treasury Spread historically provided an advance warning of recession/capitulation in 2000, 2007 & 2020 however it provided us a wide 6 - 22 month window of time from the time the yield curve made its first definitive turn back up to the 0% level. September will be month 6 of that 6 – 22 month window and thus we are clearly entering dangerous territory.

o Macro Monday 6 – ISM Manufacturing New Orders Index ECONOMICS:USMNO : Its clear from our chart shared today that the ISM New Orders Index is also entering into dangerous territory having been below the sub 50 level and in the orange zone for 13 months. This has never happened before without a recession, bar a lessor 12 month timeframe in the orange zone in 1995/96. The ISM Manufacturing New Orders readings for August and September will be vital indicators for the direction of the economy.

o Macro Monday 4 – Global Net Liquidity Vs S&P 500 NYSE:GNL : We shared this chart on the 3rd July as an advance warning of an imminent and expected pull back in the $SPX500. A negative divergence was evident on the chart as Global Net liquidity was decreasing for 6 months from Jan – July 2023 and the S&P 500 increased over the same period. Please review the chart press play and see how accurate this call has been. GNL is currently signalling at minimum a continued correction over the months of Aug and Sept.

Side Note: I am very aware of the Halloween effect in which markets rally into the months of October – December thus a pull back in Aug/Sept could end up being short term with a surge in the markets in October. The ISM reading for August (released in Sept) and September (released October) should help us gauge what outcome is more likely. Any increase/decrease in GNL will also offer insight over those months. Aside from this we should be aware of any Fiscal Stimulus that is announced as this would likely have a significant impact. I hope to cover Fiscal Stimulus in coming Macro Mondays, it’s a work in progress.

Charts Demonstrating Strength:

o Macro Monday 1 - Dow Jones Transportation Index ( DJ:DJT ): The transportation sector acts as a leading indicator as it is further up the value chain ahead of the final products being sold by companies in Dow Jones Industrial Average $DJI. It is similar to ISM Manufacturing New orders in this regard, ahead of or at point of sale execution. When the Dow Jones Industrial Average TVC:DJI is climbing higher while the DJT is falling (Negative Divergence), it can be a signal of economic weakness ahead, this occurred prior to March 2020 capitulation, making this a very valuable tool to have in our arsenal.

- In our chart recently shared a positive weekly MACD cross gave us a heads up that price might break through strong resistance levels, which it in fact did. If we can make the prior resistance level support and bounce off the support, price could stretch to all-time highs at which point we can reassess.

o Macro Monday 3 – SPDR Homebuilder Index AMEX:XHB : The Chart can be used as a leading indicator for the US housing market as the stocks in the XHB comprise of companies that provide the materials and products to build new houses and renovate homes. These products are higher up the supply chain and sold before construction commences or during. In the past the XHB chart provided a significant advance 12 month+ warning of the 2007 Great Financial Crisis which is illustrated in red on that chart.

- Since sharing the chart price appears to be on course to testing its all time high and has a bullish MACD Cross on the monthly. This could also be a double top however historic positive MACD Cross performance suggests we have higher to go. Its looking positive.

o Macro Monday 5 – Arca Major Markets Index (XMI): The XMI has proven itself as a leading indicator as it provided an advanced 9 month warning of the follow up recession/capitulation price action that initiated in Sept 2000 on the S&P 500.

- Since we shared this chart it has broken above its all time highs and is currently resting on support. A bounce higher here would be confirmation of the uptrend, however this could be a false breakout which would be confirmed if we lost the support. This chart will be important to watch for the August – September period also, again highlighting just how important these 2 months are.

Conclusion

Its clear from all of the above charts that the price and readings for the months of August and September 2023 will be critical to determining the potentiality of a recession / market capitulation or for letting us know will there be continuation of climbing the wall of worry. Its clear that we are at an inflection point over the next 60 days. Based solely on the charts shared to date the fact that the DJT, XMI and XHB are still leaning bullish, I remain long term long until these charts break down or the GNL and ISM Manufacturing Index confirms to the downside. That does not mean that we can’t get a 10% ,15% or 20% pullback in the S&P over the next 60 days, this would not surprise me, however based on some of the charts I have shared previously I think it is probably that this will be a temporary pull back. This leans me towards thinking that if there is a hard landing, it will come later in 2024 or even 2025. If that view changes and the above positive charts pull back, ill be the first to let you know.

Stay Nimble folks, August and September are decision time.

PUKA

Continuous Jobless Claims Continues to IncreaseU.S. Continuous Jobless Claims

Rep: 1,895 🚨 20k HIGHER THAN EXPECTED🚨

Exp: 1,875K

Prev: 1,865k (revised down from 1,871k)

20,000 higher continuous claims than expected. This is keeping the long term trend rising and remains one of thee most concerning charts out there.

Chart Trend

Since Sept 2022 continuing claims increased from 1.302m to 1.895m (593k+).

This is significantly concerning trend and suggests that an increasing number of people that have become unemployed are remaining unemployed for longer.

Recession Watch

For the last 6 Recessions the 2.86m level was surpassed confirming or coinciding with recession initiation (see red dashed line). This is noted as the “Last 6 Recessions Threshold” on the chart. This is a level that was surpassed on confirmation of recession commencement (recessions are in red). The blue levels are pre-recession increases which are the warnings we are trying to interpret to get a lead.

The above chart above has min, avg and max levels on the bottom right to illustrate the levels we would need to hit for increased the pre recession risk. Right now this chart demonstrates we are at max timeframe and close to max levels for an advance recession warning.

PUKA

Macro Monday 35~Richmond Fed Manufacturing and Services IndexMacro Monday 35

Richmond Fed Manufacturing and Services Index

(Released Tuesday 27th Feb 2024 @ 15:00 GMT or 9:00 CT)

The Richmond Manufacturing and Services Indexes measures the conditions of each respective industry for the 5th Federal Reserve District which covers the District of Columbia (Washington DC), Maryland, North Carolina, South Carolina, Virginia, and most of West Virginia. Both the indexes are derived from surveys conducted each month of relevant businesses in each respective industry.

▫️ The Richmond Manufacturing Index survey focuses on questions related to production, new orders, employment, prices, capacity utilization, and future expectations within the manufacturing sector.

▫️ The Richmond Services Index survey, on the other hand, asks questions about business activity, new business, employment, prices, inventory, capital expenditures, and future expectations within the service sector.

While the specific questions and data points might differ between the surveys, the basic structure and methodology for calculating the diffusion indices remain consistent;

The Chart

You can see that the green zone is expansionary and the red zone is contractionary.

At present Manufacturing (blue line) is in fairly deep contraction at -15 and whilst Services (red line) has recovered from -22 (Apr 2023) to +4 (Jan 2024).

Reading the Chart:

🟢Above 0 is expansionary (green zone)

🔴Below 0 is contractionary (red zone)

Historic Recession Patterns

I have highlighted some patterns on the chart (orange) which demonstrate that historically when Services and Manufacturing declined for a period of between 27 and 45 months a recession can follow such declines. Importantly there was a period of decline in from Apr 2010 – Dec 2013(45 months) which did not result in a recession. During this period Services remained elevated and only fell marginally into contractionary territory for brief spells (which could be a tell of some buoyancy in the market during this period). At present we are 32 months into a general decline in both manufacturing and services. Services have been on the incline since Apr 2023 and recently moved into expansionary territory at +4 in Jan 2024 which is promising and may indicate the beginning of a trend change, however until manufacturing follows this trajectory I believe we are still at risk of repeating history. Manufacturing is down at -15 at present and needs to start as sustainable recovery into expansionary territory. It has remained more a less in contractionary territory since Apr 2022.

Why even consider the Richmond Fed index?

I think the best way to outline the utility of the Richmond Fed is to compare it to the Dallas Fed Index which will be released later today (Monday). I have covered the Dallas Fed on a previous Macro Monday (link will be in the comments) and I will update you on this index when it is released later today also.

Both the Richmond Manufacturing Index and the Dallas Fed Manufacturing Index are valuable indicators of regional manufacturing activity, each offering unique insights.

Dallas Fed Index focuses on a major economic manufacturing hub – Texas

(An estimated 14.4 million people are employed in the state of Texas)

The Dallas Fed Manufacturing Index covers manufacturing activity mainly in the state of Texas. The state of Texas ranks 2nd only to California in factory production & comes in at 1st as an exporter of manufactured goods, thus Texas is an important state for gauging manufacturing & production in the U.S. economy (not services is not included here). Texas also contributes an incredible c.10% towards the U.S. Manufacturing gross domestic product making the index an important metric to consider towards potential GDP trends in the U.S. So, the Dallas Fed is very good at gauging manufacturing in the U.S. simply because of the volume of manufactured goods from the region. Whilst the Dallas Fed Index focuses on a high volume of manufacturing activity and production within the state of Texas, it also specifically focuses on durable goods industries like aerospace, energy, and technology whilst the Richmond Index below is much more diversified in terms of its manufacturing industries, its services sector and regionally diverse.

Richmond Index focuses on more economically diverse regions (inclusive of a large services sector)

(An estimated 23 - 25 million people are employed in the fifth federal reserve district)

This Richmond Index covers the Fifth Federal Reserve District, encompassing an incredibly diverse range of industries across six states. Its difficult to portray the expansive array of various manufacturing and services within these regions but I will try. This index goes far beyond the specific performance of durable goods in an isolated state like Texas and reflects manufacturing and services health across various sectors and regions. It offers economists a broader picture of manufacturing health in the U.S. compared to indices focused on specific industries or regions.

To give you an idea of the diverse ranges here:

In Washington DC you have a major corporate & services hub; think Accenture, Deloitte, KPMG, Capital One) combined with tech and comms center with the likes of Amazon web services, Verizon Communications & General Dynamics. You obviously have a strong political and legal presence in this region also.

Maryland, Virginia and North Carolina appear to have a very strong healthcare dynamic with the likes of Bon Secours Mercy Health System, VCU Health System, Duke University Health System and Atrium Health. Baltimore in Maryland has the Johns Hopkins Hospital and Health System employing over 40,000 employees. All these states appear to have strong university presences also (offering education employment and services) which likely supply the necessary expertise for the medical manufacturing and services that are present across these states.

South Carolina is known for having one of the major three Boeing aircraft manufacturing facilities and is also known the manufacturing of Michelin tires.

Across all six states you have a rich and diverse farming and forestry industry, food production facilities and waste productions plants.

Walmart, Home Depot, Target and Amazon are also present across all these states.

You can clearly see why the Richmond Fed offers a more nuanced and complex picture of the U.S. manufacturing and services economy. This diversity in sectors, regions and employment demographic gives us a different insight against the more centralized manufacturing hub contained in Texas under Dallas Fed Index. Furthermore, in terms of employment the six states included in the Richmond Fed Index is approx. 24 million versus the approx. 14.4 million employed in the state of Texas (under the Dallas fed Index). Both indexes are very valuable and should both be equally considered in our assessments of the U.S. economy.

Thanks for coming along and learning about the chart history on the Richmond Fed Index, the historic trends and the combined utility of both the Dallas and Richmond Fed Index .

PUKA

KOLD Natural Gas Pivots Again LONGKOLD on the 15 minute chart has reversed and swung upside. The the anchored VWAP price

dropped through the mean VWAP and is now in the deep undervalued territory of the second

lower VWAP band line. This is an oversold zone for buying. On the chart, a green arrow is a buy

while a red arrow is a sell. New share buys are funded with profits from BOIL positions

now closed. Relative volatility and volume indicators support the analysis.

I will add further to the position whenever there is an entry provided by a correction found

on a lower time frame of 3-10 minutes.

Macro Monday 20 ~ The Philly Fed IndexMacro Monday 20

Philadelphia Fed Manufacturing Index

While the Philly Fed Manufacturing Index (PFMI) is a regional report generated from surveys in Philadelphia, New Jersey, and Delaware by the Federal Reserve Bank, it is particularly useful as it provides an advance indication of the Purchasing Managers’ Index (PMI) report which is released up to a week after the PFMI (the PMI surveys the entire US whilst the PFMI only surveys the regions mentioned above).

The Philly Fed Index is released this Thursday 16th November 2023 and will provide an advance indication as to what to expect from the PMI released Friday 24th November 2023. Both are a review the prior months survey data, October 2023.

The PFMI index dates back to 1968 and is similar to the PMI, the Federal Reserve completes surveys and asks businesses about new orders, shipments, employment, inventories and general business activity, prices paid, prices received, capital expenditures as well as future expectations for business.

A reading= 0 is stagnation

<0 = contraction

>0 = expansion

The current reading is -9 so we are contractionary territory. We did fall as low as -31.3 on the April 2023 release.

The Chart

The main indications from the chart are as follows:

The Orange Zone

▫️ When the PFMI remains in the orange zone for >10 months it has always coincided with a Recession

- We are in presently in this zone 16 months with 2 brief monthly jumps out of it. I think its safe to say we are 10 months+ in the orange zone which historically has always coincided with a recession.

The Red Zone

▫️All Recessions confirmed a reading below -22 on the PFMI (this is below the red line into the red zone on the chart)

- In April 2023 we hit a low of -31.3 which is well into the red zone (sub -22). We have since risen above the neutral 0 level to high of +12 in Aug 2023 however we have since fallen back down into the -13.5 (Sept) and -9 (Oct). The Nov Release is due this Thursday 16th Nov (and is actually the reading for Oct - released in Nov)

Are we already in a mild Recession?

You can see that in March 1970 we reached a similar PFMI level of -31.3, the same level as in April 2023 (there is a dashed red line to illustrate this on the chart). March 1970 was the middle of the 1969-70 Recession which was a mild recession that ran for 11 months from Dec 1969 – Nov 1970. Whilst it was a mild recession as to its impact on the general economy, there was till a 34% decline in the S&P500.

The 1969-70 Recession has many similarities to some of our current economic predicaments, with the main factors leading to the 1970 recession being tighter monetary policy, rising oil prices, rising inflation, and slowing growth in Europe and Asia. Sound familiar?

From Jan – Apr 2023 the Unemployment Rate was at the lowest levels seen since back in 1969 (at 3.4%). For 8 months (Sept 1968 – May 1969) the unemployment rate was down at 3.4%. We reached this level in January 2023 and oscillated there until April 2023 (only 4 months). Since then the Unemployment rate has risen sharply from 3.5% to 3.9% (July – Oct 2023). Interestingly, this move in the unemployment rate from 3.5% to 3.9% also happened from Dec 1969 to Jan 1970 and marked the start of the recession. Could this be an indicator that we stepped into a recession In July 2023? The orange zone and red zone on the chart are triggering a confirmation nod of a recession. During the recession of 1969-70 the unemployment rate topped at 6.08% in Nov 1970, this is something we have not seen yet however we seem to be trending upwards in that direction. Queue the 8th Dec 2023, the next Bureau of Labor Statistics Unemployment date release.

The 1968-70 period was also burdened with high inflation with YOY CPI increasing from 2% - 6% in the 26 month period from Oct 1967 – Dec 1969. Similarly over a 25 month period from May 2020 – June 2022 CPI increased from 0% to 9.08%. The timeline of the 1969-70 inflation is quite similar, not exactly the same rate increase or timeline but similar all the same. Since June 2022 the CPI has come down to 3.7% as of Sept 2023.

There are some broader similarities between the late 1960’s and early 1970’s to present day, the Vietnam war was raging and was receiving significant funding from the US government with many bills passed in support of the war effort. There was also significant poverty issues in the states as the war dragged on, and the awareness of money being spent on it was creating social discourse on the topic. Whilst the current situation of funding towards the Ukraine and Palestine conflicts is obviously very different, a similar awareness and disapproval is present as many domestic states are suffering with poverty. US President Johnson summarised the late 60’s quiet well in a 1966 speech stating that the nation could afford to spend heavily on both national security and social welfare — “both guns and butter”, as the old saying goes. Only in today’s circumstances only one of these seem to still be taking priority and it isn’t butter.

I believe todays chart and post demonstrates a few things, that there is a high probability that we are already in a recession as of July 2023, however on a positive note the period we find ourselves in has many similarities to 1969-70 period, where the recession was a very bearable and mild one. With some luck, unemployment might top at 6.08% within 9 or 10 months like in 1970 and we will see a correction no greater than -34% on the S&P500 eventually. We already survived a 25% S&P500 decline from Dec 21 – Sept 2022. Minus 34% from our recent $4,580 high would put the S&P500 at approx. $3,000.

Obviously there are no guarantees of any of these scenarios playing out, but at present we are certainly playing to the same tune as the 1969-70 period.

PUKA

U.S. Continuing Jobless Claims (Updated Chart & Release)U.S. Continuing Jobless Claims

Rep: 1,806k ✅Lower Than Expected ✅

Exp: 1,845k

Prev: 1,832k (revised down from 1,834)

Whilst the short term lower than expected continuous jobless claims are welcomed the long term trend is one of thee most concerning charts out there.

Chart Trend

Since Sept 2022 continuing claims increased from 1.302m to 1.806m (500k+). This is significantly concerning trend and suggests that an increasing number of people that become unemployed are remaining unemployed for longer.

Recession Watch

The chart below has min, avg and max levels on the bottom right to illustrate the levels we would need to hit for increased recession risk. Right now this chart demonstrates we are at max timeframe and close to max levels for an advance recession warning.

What are Initial and Continuous claims?

Initial Jobless Claims account for only the people that claimed their first week of unemployment benefit whilst Continued Jobless Claims accounts for people who continued to seek their unemployment benefit into week 2 and subsequent weeks.

Next up, Philly Fed Manufacturing Index 💪🏻

Macro Monday 22 - ISM Services Vs PMI US ISM Non-Manufacturing Index (ISM Services)

Next Release: 5th December 2023 (released on third business day of each month)

The U.S. Institute for Supply Management (ISM) Non-Manufacturing Index (“ISM Services”) encompasses a wide range of services across various industries.

The index is designed to measure the economic activity and health of the services sector in the United States some of which are professional services (accounting, legal, etc.), healthcare (hospitals, clinics & other practitioners), accommodation, leisure and food services.

Similar to the ISM Manufacturing Index (aka as the Purchasers Managers Index) which surveys producers and manufacturers which we covered in Macro Monday 13, the ISM Services index is also based on surveys conducted on participants in the relevant services sectors noted above. Also similar to the ISM Manufacturing index, the ISM Services is reported as a diffusion index, where values above 50 indicate expansion or growth in the sector, while values below 50 suggest contraction.

This makes both the ISM Manufacturing Index and ISM Services Index easy to compile onto a chart for comparison purposes.

The ISM Services Vs ISM Manufacturing Chart

The chart demonstrates the following:

▫️ At present ISM Services has been more resilient and is in expansionary territory at 51.8 (above 50) whilst ISM Manufacturing is in contractionary territory below the 50 level at 46.7.

▫️ Both the ISM Services Index and the ISM Manufacturing Index have been in a downward trajectory since 2021.

- You can clearly see that since March 2021 the

Manufacturing Index has declined from 64.5 down

to 46.7 today (Red Line).

- Thereafter from November 2021 the ISM Services

Index declined from 67.5 down to 51.8 today (Blue

Line).

▫️ As you can see on the chart a steep manufacturing decline can often provide advance an warning of a subsequent services decline (grey areas on chart).

It’s important to acknowledge that the Manufacturing Index can lead the ISM Services Index. It is important because we discovered in Macro Monday 13 that the Manufacturing Index (AKA Purchaser Managers Index) reading below 42 can provide an advance/confirmation warning of recession, thus more weight could be assigned to the Manufacturing Index than Services Index in predicting a recession (as it appears to lead services direction). For this reason we will review the ISM Manufacturing Index (PMI) indications below.

The ISM Manufacturing Chart

The main findings of the ISM Manufacturing Index (AKA Purchaser Managers Index)

From a Recession Perspective

▫️ 11 of the 12 recessions on the chart coincided with a PMI of less than 42.

▫️ 1 recession occurred that did not breach below the 42 level (No. 9 on the chart)

From a PMI Perspective

▫️ 12 of the 13 times that the PMI moved below the 42 level, this coincided with a recession.

▫️ 1 time we have had a sub 42 PMI reading without a recession (Between 11 & 12 on the chart).

At present we are at a level of 46.7 so we do not currently have a trigger event for a recession but we know exactly what to look for.

Based on both historical perspectives, there is an c.92% probability of a recession should a sub 42 PMI level be established, or vice versa, in the event of a recession confirmation there is a c. 92% probability it would coincide with the sub 42 PMI level.

Timing ISM Manufacturing Bottoms

o 10 out of 12 PMI Bottoms occurred in Q1 and the remaining two bottoms were in Q2. 83% of the time the PMI bottoms occur in Q1 which is good to know and watch for with Q1 2024 approaching swiftly.

o The average PMI Bottom to bottom timeframe over the past 6 cycles is 58 months (Min 37 – Max 86). We are presently at month 44 and month 58 is Jan 2025 (Q1)

The ISM New Orders Index (30% of the PMI)

Similar to the ISM New Orders Index Chart (covered in Macro Monday 6) which makes up 30% of the Purchaser Managers Index or Manufacturers Index (PMI), we have not reached below the 42 level on this chart either which has provided a 100% confirmation of recession when we have had a definitive move below the 42 level historically. At present we are at 45.5 on this chart and we seem to have a downward trajectory at present unless something changes upon the next data release.

In summary, we now know now that the Manufacturers Index (PMI) often leads the Services Index, and we need to pay close attention to the 42 level on both the New orders Index (Makes up 30% of PMI) and the Manufacturing Index (PMI) as a breach below this level on these charts increases the probability of a recession upwards of 92%. We are also now aware that there is a high incidence of the PMI bottoming in Q1 (83% of the time) and occasionally in Q2. These are quarters we can be on high alert for a sub 42 level.

The ISM Services PMI is released on the third business day of each month at 10:00 a.m. (EST) or 15:00 GMT. The next release will be on the Tuesday the 5th December 2023. Most of the ISM data releases commence within the first 5 working days of the month.

As always folks, I will watch the numbers and keep you informed. All of the above charts are updated on TradingView as data is released.

PUKA

MACRO MONDAY 15 ~ Gold Performance During RecessionsMacro Monday 15

Gold Performance During Recessions vs S&P500

With the U.S. Treasury Yield Curve being inverted since July 2022, many leading analysts believe that the U.S. economy is headed toward a recession in coming months. Many of the charts covered on our Macro Monday releases are signaling some recession concerns (not confirmations). With this in mind, we will start looking at assets that perform well during recessions. This starts with non-other than the obvious, Gold.

The aim of this Gold chart is to establish if gold is a good asset to hold during recession periods versus holding general market indices such as the S&P500. The obvious thought would be that it would offer a hedge of sorts but we want to back that up with the data and a visual.

We are parking any preconceived notions that gold is a safe haven risk free asset and we will focus purely on the data from the last 8 recessions. Lets see how Gold fares.

The Chart

The chart measures golds price movement from the beginning of each recession period to what the price was when Gold exited the recession period. The recession periods are the green and red shaded areas on the chart.

The measurement for the S&P500 price decline during the recession periods (in the table provided) is measured from the S&P500 entry price at the beginning of each recession period to the lowest price point during the recession period (not the exit value from the recession period as used for Gold). I used the lowest price during the recession periods as a measurement for the S&P500 as it illustrates the maximum damage to a portfolio holding the S&P500 index within a recession period.

Chart – Main Findings

1. The average length of the 8 recessions on the chart is c.11 months during which:

- The average return for Gold was +7.3% and,

- the S&P500 declined by an average of -35.6%

2. Based on the above figures in 6 out of the last 8 recessions Gold outperformed the S&P500 by 42.7% on average.

3. Recession 6 and 4 are the outliers which show that Gold decreased in value during these recession periods by -9.3% & -6.3% respectively, however Gold still performed better than the S&P500 in both cases (S&P500 declined by -12.7% & -16.3%).

Overall Golds performance during the last 8 recessions certainly provides an argument for its inclusion in investors’ portfolios. During these periods of market uncertainty and volatility it is highly probable that your Gold position will perform better than the S&P500 and afford your portfolio some protection from the potential average S&P500 price declines of 35.6%. It appears that you could expect an average return 7.3% for holding gold through a recession period (which is an average of 11 months). Whilst this is a very small gain, it is a relatively risk averse gain for these periods of great uncertainty.

It’s important to note that there are other assets to consider such as the Cash and Government Bonds both of which can pay a yield. If these yields are providing a higher real return (yield being paid minus current inflation) then they could be more attractive than an asset like Gold which is not providing a yield and which could decrease in value over the same period (such as in No. 6 and 4 above). There are also other commodities and value stocks to consider during recessionary periods. We will have a look at these alternatives in coming Macro Mondays to compare their performance to Golds during recessions.

Gold has established itself as popular among investors because it can be used as a hedge against currency devaluation, inflation, or deflation. Thus investors seek safety in the precious metals like Gold when they are concerned about losing real value from otherwise safe assets like cash and US government bonds.

I believe this chart demonstrates Gold is worth holding in any investors portfolio during periods of recession and uncertainty.

PUKA

Macro Monday 14~Unemployment Rate Rise Macro Monday 14

US Employment Rate Pre-Recession Indications

The Unemployment Rate tells us how many people in the United States are currently without a job and actively looking for one. The U.S. Bureau of Labor Statistics calculates and reports the unemployment rate. In basic terms it consists of the following;

Survey: The Bureau of Labor Statistics conducts a regular survey of a sample of households across the country. They ask people whether they are working or actively trying to find work.

Calculation: Based on the survey results, the Bureau calculates the percentage of people who are unemployed (those without jobs but actively seeking employment) compared to the total number of people in the labor force (those who are either employed or actively looking for work).

Reporting: This percentage is then reported as the unemployment rate. For example, if 5 out of every 100 people in the labor force are unemployed, the unemployment rate would be 5%. At present the Unemployment rate is 3.8%.

In simple terms, the unemployment rate is a way to gauge how many people are struggling to find jobs in the United States. In this respect it is an important economic indicator that helps us and policy makers understand the health of the job market.

The Chart

In today’s chart I will be analysing the history of the Unemployment Rate and how it has behaved both before and during recessions. The aim of the analysis is to help us understand the distinct pre-recession patterns and levels that occur prior to recession so that we can prepare ourselves should these levels be breached or these patterns play out again. These historic levels will be placed on the chart for you to monitor from today forward.

Chart Outline:

1. Recessions are the red zones (also numbered & labelled 1 – 12 and on the chart itself)

2. Increases in the Unemployment Rate prior to recession are in blue.

- These blue zones start at the lowest level the Unemployment Rate established prior to the

recession periods in red.

- Basis points (bps) have been used to show the change in the value within the blue zones

(pre-recession zones) e.g. recession No. 2 The Great Financial Crisis had a pre-recession

Unemployment Rate increase from 4.39% - 5.00% which is a 0.61% increase in the

unemployment rate or a 61 bps increase.

- Peaks: I have also included peak bps increases within these pre-recession periods (within

the blue zones). These are times that the Unemployment Rate peaked higher but reduced

thereafter but a recession still followed.

Chart Findings:

1. In 10 out of 12 of the recessions outlined the Unemployment Rate increased in advance of the on-coming recession (in the blue zones) demonstrating that initial early increases to the Unemployment Rate can act as an early recession warning signal:

- An average increase of 33.5 bps over an average timeframe of 7.3 months is observed pre-recession.

- The maximum increase in the pre-recession blue zones was 71bps over 8 months. This max increase was observed prior to 1980 Volcker/Energy Recession no. 6 on the chart (this increase was from 5.59% to 6.30% in the Unemployment Rate itself – a 71bps increase). This recession was induced by Fed Chair Paul Volcker’s sudden increase to interest rates much like those that have been imposed by Jerome Powell over recent months (Volcker was appointed in Aug 1979 and got to work quick).

- The max timeframe for a rising Unemployment Rate prior to recession was 16 months. This was prior to the The Gulf War Recession, no. 4 on the chart (which was considered a short 8 month softer recession). This max 16 month pre-recession timeframe has been marked on the chart to May 2024 in correspondence with today’s pre-recession blue zone timeline – so we know where a max timeline would put us (not a prediction).

- 2 out of 12 times the Unemployment Rate did not increase prior to recession however it did not decrease either, it based at 0 bps or no change (No.1 COVID-19 Crash and No. 5 The Iran/Energy Crisis Recession). Whilst the Unemployment Rate did not increase, they did temporarily peak higher within the blue zones by 10 bps (No. 1) and 31 bps (No.5) demonstrating the importance of peaks and bases formed prior to an Unemployment rate ramp up and recession.

I found the peak increases interesting to include because they illustrate that the Unemployment Rate can oscillate peaking higher temporarily only to form a higher low or return to its starting point, but a peak, if significant enough could be a telling indicator. The most notable peaks are the following; 62 bps (no. 12), 61 bps (no. 9), 60 bps (no. 10), 30 bps (No. 8), 31bps (No. 5) and only 10 bps (No. 2) for the COVID Crash. All of these peaks reduced thereafter within their pre-recession blue zones but a recession still ensued. A sudden increase in the unemployment rate should be taken seriously. I will include a subsequent data table chart that outlines these peaks and all other data utilized for Chart 1’s illustration and findings.

We are currently in dangerous territory as we have passed the average timeframe of 7.3 months of increases to the Unemployment Rate and the Unemployment Rate increased by 40 bps over that period which is higher than the historical average of 33.5bps. We have surpassed both averages. The max historical pre-recession increase is 71 bps (No. 6) so this is a level to watch going forward. This translates to a level of 4.11% in the Unemployment Rate (marked on the chart).

Similar to today’s Unemployment Rate level, there are two very similar instances in the past where the Unemployment Rate increased from c.3.4% to c.3.8% prior to recession (See RED ARROWS on chart). These both took 7 – 10 months to play out with a 10 – 42 bps increase to be established before recession hit. This is very similar to today’s levels which are at 7 months and 40bps of an increase with the 8th month being released this Friday 6th October 2023 which should be very revealing.

We are now well armed with an historical chart as a reference point for any upcoming Unemployment Rate figures released in coming months. We know we have surpassed the averages in terms of timeframe (7 months) and the 40 bps increase is above the avg. 33.5 bps. We can refer back to this chart using Trading View, press play and see if we are breaching the max pre-recession level of 4.11% (the 71bps move) or other extreme pre-recession levels such as the dot.com and GFC Unemployment Rates (both marked on the chart). And if you don’t frequent the chart on trading view I will update you here regardless.

Lets see what Friday brings….

PUKA

MACRO MONDAY 10~ Interest Rate & S&P500MACRO MONDAY 10 – Historical Interest Rate hike Impact on S&P500

This chart aims to illustrate the relationship between the Federal Reserve’s Interest rate hike policy and the S&P500’s price movements.

At a glance the chart highlights the lagging effects of the Federal Reserves Interest Rate hikes on the S&P500 (the “Market”). In all four of the interest rate hikes over the past 24 years the S&P500 did not start to decline until 3 months into an interest the rate pause period (at the earliest) and in 3 out of 4 of the interest rate pauses there was a 6 – 16 month wait before the market begun to turn over. The move to reducing interest rates (after a pause period) has been the major warning signal for the beginning or continuation of a major market decline/capitulation. We might have to wait if we are betting on a major market decline.

In the chart we look particularly at the time patterns of the last two major interest rate hike cycles of 2000 and 2007 as they offer us a framework as to what to expect in this current similar hike cycle. Why is this cycle similar to 2000 & 2007?.. because rates increased to 6.5% in 2000, 5.25% in 2007 and we are currently at 5.50% in 2023 (sandwiched between the two). These are the three highest and closely aligned rate cycles over the past 24 years. The COVID-19 crash is included in this analysis but has not been given the same attention as the three larger and similar hike cycles 2000,2007 & 2023.

The Chart

We can simplify the chart down to FIVE key points (also summarised hereunder):

1. Previously when the Federal Reserve increased interest rates the S&P500 made significant

price gains with a 20% increase in 2000 and a 23% increase in 2007.

- Since rates started increasing in February 2022 we have seen the S&P500 price make a

sharp decline and then recover all those losses to establish an increase of 5% at present

since the hiking started.

- This means all three major interest hike cycles resulted in positive S&P500 price action.

- For reference, a more gradual rate hike pre COVID-19 also resulted in 20%+ positive price

action.

2. When the Federal Reserve paused interest rates in 2000 it led to a 15% decline in the

S&P500 and then in 2007 it led to a 28% increase in the S&P500. It is worth noting that a

lower interest rate was established in 2007 at 5.25% versus 6.5% in 2000. This might

indicate that this 1.25% difference may have led to an earlier negative impact to the

market in 2000 causing a decline during the pause phase. Higher rate, higher risk of

market decline during a pause.

- At present we are holding at 5.5% (between the 6.5% of 2000 and the 5.25% of 2007).

3. In the event that the Federal Reserve is pausing rates from hereon in, historic timelines of

major hike cycles suggest a 7 month pause like in 2000 or a 16 month pause in line with

2007 (avg. of both c.11 months). For reference COVID-19’s rate pause was for 6 months.

- 6 - 7 months from now would be March/April 2024 and 16 months from now would be

Nov 2024 (avg. of both Jun 2024 as indicated on chart).

4. As you can see from the red circles in the chart the initiation of Interest rate reductions

have been the major and often advanced warning signals for significant market declines,

including for COVID-19.

5. It is worth considering that before the COVID-19 crash, the interest rate pause was for 6

months from Dec 2018 – Jun 2019. Thereafter from July 2019 rates begun to reduce (THE

WARNING SIGNAL from point 4 above)…conversely the market rallied hard by 20% from

$2.8k to $3.4k topping in Feb 2020 at which point a major 35% capitulation cascaded over

6 weeks pushing the S&P500 down to $2,200. Similarly in 2007 the rates began to decline

in Aug 2007 in advance of market top in Oct 2007. A 53% decline followed. The lesson here

is, no matter how high the market goes, once interest rates are decreasing it’s time to be

on the defensive.

Summary

1. Interest Rate increases have resulted in positive S&P500 price action