7 MOST IMPORTANT CHARTS TO WATCH RIGHT NOW1. VIX is filling the gap from when the Feb-Mar crash begun. Volatility is getting supressed when things actually look very fragile with Central Banks having nothing under control. A VIX spike (big move down for stocks) wouldn't be a surprise here for reasons I'll explain soon.

2. DXY looking strong here. The 50 DMA has turned up and dollar strength could be a problem here. Watching other charts tells me things are OK, so the weakness comes from specific currencies. Some currencies are doing very well while others very poorly and there is no concrete way to go about it.

3. CNH/CNY however are very clear as to what is going on. They seem to be in agreement with the DXY. The relentless USD downtrend has been broken and the USD is showing signs of life. Despite the QE, despite the massive stimulus... the USD hasn't gone down. That's not a great sign. Sure most currencies are getting devalued, but if the USD is so strong and could begin an uptrend we have a problem...

4. Essentially most of that is attributed to US long term rates going up faster than anywhere else. This could be happening for many reasons, right or wrong. Inflation might be here, inflation might be coming... but it depends on which country you are looking at and in what form you are seeing it. Is it because of supply shocks (i.e low Oil and Copper production), currency debasement, loss of faith in the currency or trade wars etc? It could be many combined, but when we see bonds go down it could the fact that we have a lot of supply coming in and not enough demand. Maybe we had such a big bull market that people are taking profit. However the impact this has on the market is on many different levels and it comes down to how the market is structured, stock valuation models, different investment strategies and so on. So the more yields go up (bonds down), the bigger the problem becomes if it is relentless.

5. Gold has been going down because real yields have been going up and people have been taking more risk. Why hold gold and not other more useful commodities or riskier assets in general? Gold going up isn't a good thing. It means something is not going well. Over the last few days Gold didn't go down along with bonds, which is worrying. It is stuck between and uptrend and a downtrend, however it is clear it is currently in a downtrend as it is below all key MAs (50-200-300 DMAs).

6. Oil has had a massive rally and I can't tell whether it is over for now but it could be. Very high oil prices in the current environment wouldn't be ideal, but hopefully because more oil is being produced, not because demand is down. Low oil demand means low growth and bad things in general going on. High oil demand means growth and go things going on. Oil got above the 2019 highs, swept them, retested them and went down quite a bit. It also crossed above the big diagonal downtrend from the 2008 high all the way down here and then came back down. If it closes like this and goes lower, I can't rule out 52$ or even 42$, but if it starts going above 68 it could quickly accelerate higher.

7. RUA is the index that has the top 3000 US stocks, spot. It is just an index and doesn't track futures but spot, so it isn't open 24/5. Stocks are still in an uptrend, which Japanese and European stocks showing quite a bit of strength. We've seen quite a few US stocks do well, but if the top US stocks struggle because of higher rates... there could be a big problem. If bonds start selling off hard, the borrowing costs for many companies will skyrocket. That is clearly a massive issue right now. So is a 20% like the one we had in 2018 possible? Yes it is. Do I think stocks could still go parabolic? Of course, but it might take some extra time to get there. We need bigger actions from central banks and eventually bonds slowing down and go up slowly. For now we could get another 5-10% correction, test the trendline and go higher. Until I see the market close below I think up is more likely, although I am more cautious.

RUSSELL 2000

Daily Market Update for 3/17Trend lines drawn from the 3/5 low (9d), 3/11 (5d) and today 3/17 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wednesday, March 17, 2021

Facts: +0.40%, Volume higher, Closing range: 78%, Body: 58%

Good: High closing range on slightly higher volume, support at 21d EMA

Bad: Lower high, lower low, dipped below 50d MA

Highs/Lows: Lower high, lower low

Candle: Green body covers most of candle, similar upper and lower wicks

Advance/Decline: About even advancing and declining stocks

Indexes: SPX (+0.29%), DJI (+0.58%), RUT (+0.73%), VIX (-2.83%)

Sectors: Consumer Discretionary (XLY +1.40%) and Industrials (XLI +1.15%) were top. Health (XLV -0.36%) and Utilities (XLU -1.63%) were bottom.

Expectation: Sideways or Higher

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

Happy St. Patrick's Day!

Investors got what they needed to hear from the fed's Jerome Powell. Interest rates will remain untouched and there will be no tapering of bond buying despite a big upgrade in the fed's outlook on the economy. The change in investor sentiment mid-day was clear as the indexes made a rally.

The Nasdaq closed with a +0.4% gain after dipping below the 50d MA and 21d EMA in the morning. The dip came as yields soared and investors worried about what was to come from the Fed meeting. After rallying in the afternoon, the index closed on slightly higher volume with a 78% closing range. The short upper wick above a 58% green body was formed from a small pullback just before close. There were about equal number of advancing and declining stocks.

All indexes ended the day positive with the S&P 500 (SPX) gaining +0.29% and the Dow Jones Industrial (DJI) gaining +0.58%. The Russell 2000 was the top performing index for the day with a +0.73% gain.

The VIX volatility index declined another -2.83% and is at its lowest point since February 2020. It is still above levels before the market crash of 2020.

The improved outlook from the Fed had an impact across several sectors. Consumer Discretionary (XLY +1.40%) and Industrials (XLI +1.15%) were top. The cyclical sectors recovered from losses earlier in the week. Health (XLV -0.36%) and Utilities (XLU -1.63%) were bottom.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) gained -0.46%. The Fed expects inflation to reach around 2.2% which will weaken the dollar in the short term.

The US 30y and 10y treasury bond yields rose for the day, but pulled back from the big increases in the morning. The US 2y treasury bond yield dropped for the day.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both rose today.

Silver (SILVER) and Gold (GOLD) advanced. Crude Oil (CRUDEOIL1!) declined. Timber (WOOD) advanced. Copper (COPPER1!) and Aluminum (ALI1!) advanced. Most commodities are bullish on the improved economic outlook from the fed.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio is at 0.605. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is moving back toward neutral.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

Keeping this update brief during vacation. Mega-caps overall were mixed while the majority of growth stocks benefited from the day's news.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

The weekly initial jobless claims data will be released on Thursday. Better than expected numbers could be a boost to today's optimistic outlook.

Manufacturing data will also be released that will provide insight into how manufacturing is recovering to meet demand.

Nike (NIKE), Accenture (ACN), FedEx (FDX), Dollar General (DG), Weibo Corp (WB), Utz Brands (UTZ) will report earnings.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The index was able to close above the 50d MA showing some support at that level.

The one-day trend line points to a +1.57% gain tomorrow. The trend line from the 3/5 bottom points to a +1.13% gain.

The five-day trends line points to a -0.26% loss.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

The market and the fed have been a bit at odds for the past month. Today the fed won. They gave us a firm stance on interest rates and bond buying while acknowledging the improved outlook for growth in the economy this year. That didn't provide any room for the market to argue. Don't fight the fed.

That can put some more steam into the market rally. Still, many sectors have taken quite a beating in the charts this past few weeks and there is still a ways to go to recover prices. Until then, expect those sectors, stocks and indexes to meet with resistance as overhead supply needs to be shaken out before new highs can be made.

Stay healthy and trade safe!

Daily Market Update for 3/16Trend lines drawn from the 3/5 low (8d), 3/10 (5d) and today 3/16 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Tuesday, March 16, 2021

Facts: +0.09%, Volume lower, Closing range: 33%, Body: 23%

Good: Higher high, higher low, successful test of 50d MA

Bad: Low closing range, longer upper wick, could not hold morning rally

Highs/Lows: Higher high, higher low

Candle: Thin red body underneath a long upper wick

Advance/Decline: Over three declining stocks for every advancing stocks

Indexes: SPX (-0.16%), DJI (-0.39%), RUT (-1.72%), VIX (-1.20%)

Sectors: Communications (XLC +1.05%) and Technology (XLK +0.75%) were top. Industrials (XLI -1.42%) and Energy (XLE -2.85%) were bottom.

Expectation: Sideways or Lower

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

An attempted rally in the morning sold off as investors reacted to disappointing economic data, both for February retails sales and industrial and manufacturing production. Gains were limited to fewer stocks and dominated by mega-caps.

The Nasdaq closed with a +0.09% gain, but that was down from a 1.19% gain earlier in the day. After testing the 50d MA, the index bounced back up to close a bit below where it opened and leaving behind a 23% red body. The 33% closing range is not great, but the volume was lower than the previous day and lower than average. There were over three declining stocks for every advancing stock.

The other major indexes all lost. The S&P 500 (SPX) lost -0.16%. The Dow Jones Industrial Average (DJI) lost -0.39%. The Russell 2000 (RUT) was the worst performer with a -1.72% decline.

The VIX volatility index declined -1.20%.

Communications (XLC +1.05%) and Technology (XLK +0.75%) were top. Industrials (XLI -1.42%) and Energy (XLE -2.85%) were bottom. All of the cyclicals (Energy, Financials, Industrials and Materials) lost as well as Consumer Discretionary. These sectors were impacted by the disappointing economic data in the morning.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) gained +0.09%.

The US 30y and 10y treasury bond yields rose slightly, but seem to be leveling off. US 2y bond yields remained flat.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both declined today. The spread between corporate and treasury bonds remain about the same.

Silver (SILVER) declined while Gold (GOLD) advanced. Crude Oil (CRUDEOIL1!) declined. Timber (WOOD) advanced. Copper (COPPER1!) and Aluminum (ALI1!) declined.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio is at 0.644. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is moving back toward neutral.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

Keeping this update brief during vacation, but keep an eye on the mega-caps as they influence the indexes. The mega-caps overall did well today with the majority ending the day with gains.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

On Wednesday, we'll get news on Building Permits and Housing Starts before the market opens. After the opening bell, Crude Oil Inventories will be released.

The FOMC will meeting tomorrow. In the afternoon, their economic projections and interest rate projections will be released. This will be the biggest economic news of the day and set the stage for the next moves in both bonds and equity markets. Will the Fed make investors more or less confident in the stability of yields and the US dollar.

Wednesday's earnings reports will include Pinduoduo (PDD), BMW ADR (BMWYY), Cintas (CTAS), Five Below (FIVE).

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The index was able to stay above the 50d MA showing some support at that level. The support only really matters, if news from the FOMC meeting remains positive and confident.

The trend line from the 3/5 bottom points to a +1.51% gain while the five-day points to a +0.93% advance.

The trend from today is downward and if it continues, the one-day trends line points to a -1.23% loss.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

This morning's economic news was a bit of a shock for investors who were expecting better numbers pointing to the economic recovery. Instead it showed the recovery slowing in speed and raising some alarms. The reaction was negative but also showed some caution from overreacting as there is more to come this week with the FOMC meeting.

Despite the economic data, yields did not move much. One might have expected them to come down a bit more given the perception the economic recovery is not overheating and inflation may not accelerate. But all eyes really are going to be on the Fed. What adjustments will they make to the outlook for economic growth this year? Will they even hint at changes in monetary policy? Will this be the start of the next "Taper Tantrum"?

Tomorrow we will have a lot to digest.

Stay healthy and trade safe!

Daily Market Update for 3/15Trend lines drawn from the 3/5 low (7d), 3/9 (5d) and today 3/15 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Monday, March 15, 2021

Facts: +1.05%, Volume higher, Closing range: 100%, Body: 73%

Good: Close above last week's high and back above 50d MA

Bad: Nothing

Highs/Lows: Higher high, higher low

Candle: No upper wick, most green body over lower wick

Advance/Decline: About even advancing and declining stocks

Indexes: SPX (+0.65%), DJI (+0.53%), RUT (+0.31%), VIX (-3.19%)

Sectors: Consumer Discretionary (XLY +1.34%) and Utilities (XLU +1.28%) were top. Financials (XLF -0.58%) and Energy (XLE -1.14%)

Expectation: Sideways or Higher

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

It was a relatively smooth start to the week as bond yields stayed fairly tame compared to previous weeks. That allowed the tech heavy Nasdaq to continue a rally to catch up with the other indexes. There is still more catchup to do as the S&P 500, Dow Jones Industrial average and Russell 2000 set new all-time highs.

After a brief test of the 21d EMA line, the Nasdaq rallied into close for a +1.05% gain on higher volume. The volume increased as the index moved up in the last 30 minutes of trading to end the day with a 100% closing range. The 73% green body is above a lower wick formed from some selling before noon. There were about the same number of advancing stocks as declining stocks.

The S&P 500 (SPX) gained +0.65%. The Dow Jones Industrial (DJI) had an early morning rally that sold off, but then was able to recover and close the day with +0.53% gains. The Russell 2000 (RUT) closed the day with a +0.31% advance, but only after visiting intraday lows twice in a choppy session

The VIX volatility index declined -3.19%.

Consumer Discretionary (XLY +1.34%) and Utilities (XLU +1.28%) were the top sectors. Utilities (XLU) was near the top of the sector list last week during the back and forth rotation. Financials (XLF -0.58%) and Energy (XLE -1.14%) were at the bottom of the list for today.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) gained +0.16%.

We will continue to watch treasury bond yields today. The US 30y and 10y treasury bond yields declined slightly while the 2y yield increased, helping to flatten the curve a bit. However the yield curve remains steep.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both increased for another day.

Silver (SILVER) and Gold (GOLD) advanced. Crude Oil (CRUDEOIL1!) declined. Timber (WOOD) pulled back from highs. Copper (COPPER1!) declined while Aluminum (ALI1!) advanced.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio is at 0.523. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is moving back toward the greed level.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

Keeping this update brief during vacation, but keep an eye on the mega-caps as they influence the indexes.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

Retail Sales data will be released Tuesday before market open. Industrial Production data will also be released, both indicating the pace at which economic activity is recovering.

Volkswagen (VWAGY) will report earnings on Tuesday. In addition, FUTU Holdings (FUTU), Coupa Software (COUP), Jabil Circuit (JBL), Eastman Kodak (KODK) will report.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The index moved back above the 50d MA which should provide some support.

The trend line from the 3/5 bottom points to a +0.97% gain while the five-day and one-day trends lines point to a +0.26% gain.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

Bond investors have calmed a bit, allowing the longer term bond yields to settle a big. I'll be keeping a close eye on the yields for the coming week at they are having a big influence on tech and growth stocks, which impacts the Nasdaq.

The expectation for tomorrow is for sideways or higher. If the index can follow-through with the expectation, it can start to work toward the all-time high.

Stay healthy and trade safe!

Small Caps approaching measured move target for wedgeWill likely overshoot to upside and sell near 2400-2500

Market Week In Review - 3/8/2021 - 3/12/2021The Market Week in Review is my weekend homework where I look over what happened in the previous week and what might come in the next week. It helps me evaluate my observations, recognize new data points, and create a plan for possible scenarios in the future.

I do occasionally have some errors or typos and will correct them in my blog or in the comments on TradingView. I do not have an editor and do this in my free time.

If you find this helpful, please let me know in the comments. I am also more than happy to add new perspectives and data points if you have ideas.

The structure is the following:

A recap of the daily updates that I do here on TradingView.

The Meaning of Life, a view on the past week

What's coming in the next week

The Bullish View, The Bearish View

Key index levels to watch out for

Wrap-up

If you have been following my daily updates, you can skip down to the “The Meaning of Life”. If not, then this first part is a great play-by-play recap for the week. Click the original charts for more detail each day.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Monday, March 8, 2021

Facts: -2.41%, Volume lower, Closing range: 2%, Body: 73%

Good: Held above 12,600 as market closed

Bad: Could not hold short rally in morning, selling the rest of afternoon

Highs/Lows: Higher high, higher low

Candle: Short upper wick over a thick red body, no lower wick

Advance/Decline: More than one declining stock for every advancing stock

Indexes: SPX (-0.54%), DJI (+0.97%), RUT (+0.49%), VIX (+3.28%)

Sectors: Utilities (XLU +1.41%) and Materials (XLB +1.34%) were the top sectors. Communications (XLC -1.34%) and Technology (XLK -2.42%) were bottom.

Expectation: Lower

The rotation continues. It's not often that a rotation is so clearly seen, with the Dow Jones ending the day up nearly 1% and the Nasdaq ending the day down 2.41%. Nine sectors outperformed the broader S&P 500 index, while the other two sectors lost enough to bring down the index for a loss by the end of the day.

The Nasdaq closed the day with a -2.41% loss on lower volume. The closing range of 2% followed an afternoon of selling that formed the 73% red body underneath a small upper wick from the short morning rally. There were more declining stocks than advancing stocks.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Tuesday, March 9, 2021

Facts: +3.69%, Volume higher, Closing range: 71%, Body: 56%

Good: Good gain on higher volume, higher high, higher low, above 13k

Bad: Selling in last hour of day

Highs/Lows: Higher high, higher low

Candle: Slightly longer upper wick with a thick green body

Advance/Decline: Two advancing stocks for every declining stock

Indexes: SPX (+1.42%), DJI (+0.10%), RUT (+1.91%), VIX (-5.65%)

Sectors: Consumer Discretionary (XLY +3.78%) and Technology (XLK +3.40%) were the top sectors. Financials (XLF -0.91%) and Energy (XLE -1.75%) were bottom.

Expectation: Sideways or Higher

The rotation reverses. Today saw a reversal of the past several days rotation as money flooded back into big tech, consumer discretionary, and growth stocks. Treasury bond yields seemed to stabilize a bit allowing investors to turn their eyes on the stimulus and the impact it will have on performance in the near term.

The Nasdaq closed with +3.69% gain on higher volume. The closing range of 72% came after some selling in the final hour of trading, forming the upper wick. The green body covers 56% of the candle and represents a day that was dominated by the bulls. There were two advancing stocks for every declining stock.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wednesday, March 10, 2021

Facts: -0.04%, Volume lower, Closing range: 14%, Body: 69%

Good: Higher high, higher low, support above 13,000

Bad: Rejection off 21d EMA in morning led to selling and close near low

Highs/Lows: Higher high, higher low

Candle: Thick red body with small upper and lower wicks, low closing range

Advance/Decline: More advancing stocks than declining stocks

Indexes: SPX (+0.60%), DJI (+1.46%), RUT (+1.81%), VIX (-6.12%)

Sectors: Energy (XLE +2.53%) and Financials (XLF +2.04%) were back on top. Technology (XLK -0.40%) was bottom.

Expectation: Sideways or Lower

The rotation settles. There was still signs of rotation in the market today, with the sector list flipping once again. But the effect is much more subdued than the past week. The passing of the stimulus has investors eyes wide open while they sent the Dow Jones Industrial to all-time highs.

The Nasdaq was not able to benefit from the enthusiasm as it declined -0.04%. A sideways move, but still a day marked by selling after a morning gap-up. The closing range of 14% is underneath a thick red body of 69% and slightly longer upper wick formed just after the market opened. There were more advancing stocks than declining stocks, however volume on declining stocks was higher.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Thursday, March 11, 2021

Facts: +2.52%, Volume lower, Closing range: 81%, Body: 67%

Good: Another higher high and higher low, back above 21d EMA and 50d MA

Bad: Not much, resistance at 13,400

Highs/Lows: Higher high, higher low

Candle: Thick red body with small upper and lower wicks, low closing range

Advance/Decline: Almost three advancing stocks for every declining stock

Indexes: SPX (+1.04%), DJI (+0.58%), RUT (+2.31%), VIX (-2.88%)

Sectors: Technology (XLK +2.14%) and Communications (XLC +1.89%) were top. Utilities (XLU -0.26%) and Financials (XLF -0.29%) were bottom.

Expectation: Sideways or Higher

The back and forth continues as the Nasdaq and technology stocks rise again. The sector list has flipped back and forth the last several days as investors rotate in and out of big tech and growth stocks. Today, the market rallied as jobs reports showed positive gains in the labor market and the stimulus is proceeding to Biden's signature. Technology was back on top while Financials moved to the bottom.

The Nasdaq closed with a +2.52% gain on lower volume. The 67% green body was formed in the morning as the index quickly rose to intraday highs around 13,400 and stayed there the rest of the day. The short upper wick is above an 81% closing range. There were almost three advancing stocks for every declining stock.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Friday, March 12, 2021

Facts: -0.59%, Volume lower, Closing range: 97%, Body: 58%

Good: Bulls bought back the morning lows to bring index back above 21d EMA

Bad: Lower high and lower low

Highs/Lows: Lower high, lower low

Candle: Green body above a lower wick with very small upper wick

Advance/Decline: About even advancing and declining stocks

Indexes: SPX (+0.10%), DJI (+0.90%), RUT (+0.61%), VIX (-5.57%)

Sectors: Real Estate (XLRE +1.72%) and Utilities (XLU +1.35%) were top. Communications (XLC -0.28%) and Technology (XLK -0.72%) were bottom.

Expectation: Sideways or Higher

Are you dizzy yet? This rotation just won't end. Every day this week the Technology sector flipped from the bottom of the sector list to the top and then the next day to the bottom. Yesterday it was at the top. Today it's back at the bottom. As long term bond yields are reaching for pre-pandemic highs, investors are still trying to determine the impact on valuations of big tech and growth stocks.

The Nasdaq closed the week with a green candle, but ended the day with a -0.59% decline. Volume was lower but the bulls bought up a morning dip to bring the index back above the 21d EMA in the afternoon. A closing range of 97% means a very small upper wick. The longer lower wick rests underneath a 58% green body. There were about the same number of advancing and declining stocks.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Meaning of Life (View on the Week)

It was a wild week of rotation instigated by volatility in the treasury bond markets. Economists and investors weighed the impact of stimulus on inflation, currencies, bonds and equities. The outcomes could have opposite effects on different sectors. Technology and Communications, that have growth mega-caps, could be negatively impacted by higher yields, raising the costs of borrowing money to drive growth. Financials could benefit from the higher yields driving interest rates and additional revenue on both mortgages and commercial borrowing.

The winners from the stimulus bill will be industrials and materials as the economy returns to pre-pandemic levels and these sectors benefit. The market made that clear as the Dow Jones Industrial gained 1% on Monday while the Nasdaq declined -2.41%. Utilities, Industrials and Materials were top sectors along with Financials. All cyclicals, but as the first three would remain steady throughout the week, Financials was up and down depending on bond performance.

But it also seemed no one was quite ready to give up on big tech and growth stocks. Tuesday was "buy the dip" day, sending the Technology sector back to the top of the list. Growth companies like Tesla (TSLA) gained 20%, rebounding off recent lows. The four big mega-caps all closed the day with gains. Financials and Energy moved to the bottom of the sector list. The 3y note auction brought some optimism back to the bond market, bringing yields back down from recent gains.

The 10y auction on Wednesday also brought some confidence back to the bonds market. Yields on treasury bonds pulled back a little. But even as yields came down, the yield curve steepened. A steep yield curve forecasts higher interest rates and could mean other monetary policy changes from the Fed. That's where the fear is focused. Technology moved back to the bottom of the sector list on Wednesday.

A quick refresh on the yield curve. The yield of a treasury bond can be viewed as the level of risk investors see in the bond. Shorter term bonds are paid back quickly and therefore investors usually assign lower risk and therefore require lower yields. Longer term bonds are viewed with higher risk, there's more time between now and the maturity date of the bond for something happening that will impact the value, so yields are higher. Risk/reward.

The yield curve is a plotting of the interest rates from short term to long term.

When the yield curve is normal, there should be an upward sloping curve. From the shortest term bonds to the middle term, yields will accelerate. As you move past the middle, the longer the maturity date moves out the difference in yields level off. An inverted yield curve shows the opposite and means that there is much more risk in the short term than the long term, so yields are higher on short term bonds.

What we are seeing this week is normal in that short term yields are lower than long term, but the curve is unusually steep. It's at its steepest slope since 2015/16. Investors see short term bonds as much safer than long term bonds, likely on the optimism of the short term economic recovery this year. Longer term, investors are more uncertain. What will happen to the dollar? When will the fed stop its easy money policy? So there is less demand for long term bonds, investors selling, bond prices drop, and yields go up.

If the fed wants to get revenues from selling 10y, 20y, 30y bonds, what do they need to do? They need to entice bond investors by covering the risk with greater reward. They need to either stop injecting money into the economy which is devaluing the dollar (and making long term bonds risky), increase purchases of longer term bonds to control the yield curve, or they need to raise interest rates. Regardless of comments from the fed that they are not concerned with the increasing yields, it has investors spooked, sending them back and forth between fear and greed.

Technology was back on top on Thursday. Long term yields were higher, but seemed under control. Friday Technology was back to the bottom, but after a morning dip, buyers brought the Nasdaq back up to close near an intraday high. Despite the yield curve steepening again with the 30y and 10y yields hitting their highest since early 2020, inflation numbers and consumer sentiment were better than expected. That was enough to give bullish investors optimism and end the week with the DJI and RUT at all time-highs and the SPX knocking on the door.

Despite all the turmoil, the Nasdaq closed the week with a +3.09% gain on slightly lower volume. The closing range of 86% is far better than the previous weeks. The index had a higher low but a lower high, making this an inside week.

I've redrawn the channel from the March bottom. If the index can stay in this channel, then it would seem the economic outlook has been priced into big tech and growth stocks, and the index can start to follow along with the gains we've seen in the Dow Jones Industrial and Russell 2000.

The S&P 500 (SPX) advanced +2.64%. The Dow Jones Industrial average (DJI) gained 4.07%. The Russell 2000 (RUT) gained 7.32% for the week.

The VIX volatility index closed the week with a -16.10% decline.

It was a wild week for the sectors as investors rotated in and out of Technology and Communications stocks. All sectors ended the week with gains.

Consumer Discretionary ( XLY ) was the big winner. Large stimulus checks will be delivered soon that are expected to be poured into the economy via consumer spending on both needs and wants.

Technology ( XLK ) and Communications ( XLC ) spent Monday at the bottom of the sector list, Tuesday at the top, Wednesday at the bottom, Thursday at the top, and Friday at the bottom. In the end, the two sectors landed just behind the SPX in performance, but did have gains for the day.

Financials ( XLF ) was also one to watch. It flipped back and forth as investors followed closely what was happening in the bond markets. The increase in yields could be a boon for Financials. The increased yields would have the opposite impact on big technology and communications companies and smaller growth companies. As yields went back and forth, so did the performance of these sectors.

Energy ( XLE ) ended the week as the worst sector. Although it had a big gain on Wednesday, it wasn't enough to cover the losses on Monday and Tuesday.

Utilities ( XLU ) and Real Estate ( XLRE ) did not have any big days, but were on a steady rise throughout the week. They ended the week in 2nd and 3rd place on the list. The two sectors are often used as defensive plays.

Steep yield curve. You can see the spread between the US 10y and 2y treasury bond yields in the top chart, also marked with a green horizontal line so you can see just how long since the spread has been that wide. Also note that US 30y and 10y yields are back to pre-pandemic levels. Inflation and the possibility of a weakening US dollar means long term bonds are out of vogue.

High Yields Corporate Bonds (HYG) and Investment Grade (LQD) corporate bond prices both declined for the week. The spread between corporate bonds and short term treasury bonds remain about the same.

The US Dollar (DXY) pulled back from the recent gains, declining -0.32% for the week.

Silver (SILVER) and Gold (GOLD) both advanced for the week.

Crude Oil Futures (CRUDEOIL1!) declined just slightly from its highest point since 2018.

Timber (WOOD) advanced and is trading at all-time highs. Copper (COPPER1!) and Aluminum (ALI1!) both declined but are still in upward trending channels.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Big Four Mega-caps

The four big mega-caps had mixed results for the week. Microsoft (MSFT) and Amazon (AMZN) closed the week with +1.79% and 2.97% gains. Amazon likely got a boost from the stimulus checks expected to increase consumer spending while people are still nervous to shop at brick-and-mortar stores. Apple (AAPL) lost -0.32% for the week. Alphabet (GOOGL) was down-2.24%. Microsoft and Alphabet are trading above 10w and 40w moving average lines. Apple is trading below the 10w MA line and Amazon is trading below both the 10w and 40w moving average liens.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Four Recovery Stocks

I picked four recovery stocks to track against the indexes and other indicators in this report. This week all four had gains. Carnival Cruise Lines (CCL) gained over 9% this week. Delta Airlines (DAL) advanced +7.83%. Marriott International (MAR) gained +2.23%. Exxon Mobil gained +1.71%.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio (PCCE) ended the week at 0.606, showing investors getting a little more bullish. A contrarian indicator, when the put/call ratio is below 0.7, it signals overly bullish sentiment which typically proceeds a pullback in the market.

The CNN Fear & Greed index moved toward the greed side.

The surprise was seeing the NAAIM exposure index go down to 0.48. That's a fairly low level and indicates nervousness from institutional investors. If exposure to equities by money managers is below 50%, then what is driving prices higher?

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Week Ahead

Monday's TIC Net Long-Term Transactions data will give an idea of how much investor money is flowing in and our of US markets. More inflows means foreign investors are buying US equities and as a proxy, buying the US dollar to buy those equities. On the other side, US investors may be buying more foreign equities, using those markets currencies.

Retail Sales data will be released Tuesday before market open. Industrial Production data will also be released, both indicating the pace at which economic activity is recovering.

On Wednesday, we'll get news on Building Permits and Housing Starts before the market opens. After the opening bell, Crude Oil Inventories will be released. In the afternoon, FOMC economic projections and interest rate projections will be released.

The weekly initial jobless claims data will be released on Thursday. Manufacturing data will also be released that will provide insight into how manufacturing is recovering to meet demand.

Monday's earning reports will include a couple interesting small-caps: Vuzix (VUZI) and Desktop Metal (DM).

Volkswagen (VWAGY) will report on Tuesday. In addition, FUTU Holdings (FUTU), Coupa Software (COUP), Jabil Circuit (JBL), Eastman Kodak (KODK) will report.

Wednesday will include Pinduoduo (PDD), BMW ADR (BMWYY), Cintas (CTAS), Five Below (FIVE).

On Thursday, Nike (NIKE), Accenture (ACN), FedEx (FDX), Dollar General (DG), Weibo Corp (WB), Utz Brands (UTZ) will report.

Be sure to check your portfolio for upcoming earnings reports.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Bullish Side

Did you see the Dow Jones Industrial average index? Six consecutive days of gains to set a new all-time high to close the week! The stimulus, passed through congress and signed by President Biden, is a huge amount of support to the economic recovery. Industrial stocks and small-caps are going to lead the charge and eventually the economics will be priced into big tech and growth stocks and they will join the rally.

Never fight the fed. The Fed is continuing easy monetary policy that is fueling massive liquidity in the market.

Many weekly charts look good. It's always important to take a step back and look beyond the daily turmoil.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

The Bearish Side

Treasury bonds continue to have unusual volatility. Bond investors don't like volatility. Note only does it make it harder to use in hedging strategies, but popular trading strategies using multiple maturities of bonds become more difficult.

The steepening curve Is an indicator of future interest rate increases, that will continue to worry equity investors away from the tech mega-caps and growth stocks. That will have an overweight influence on indexes and impact investor sentiment.

The NAAIM exposure index doesn't represent all institutional investors, but it is an indicator of professional portfolio managers sentiment toward the market. At less than 50% exposure, one must question what is driving prices higher. It could be retail traders and passive indexation that is driving the current rally. That may be a recipe for disaster.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Key Nasdaq Levels to Watch

Although the broader market is clearly not in correction, the Nasdaq is still lagging behind the other indexes. To build confidence in big tech and growth stocks traded on the Nasdaq, some gains on higher volume is required. If key levels on the downside breakdown, we can expect the big players in the Nasdaq to also pull down the other indexes.

On the positive side:

The Nasdaq closed above the 21d EMA on Friday, but below the 50d MA. That's the first key level to pass for next week. That level is at 13,367.48.

Last week's high is at 13,601.33. This week could not make a new high, so having the index make that milestone next week will be important.

14,000 will be the next area of resistance.

The all-time high is at 14,175.12. That might be a stretch to get there this week, but keep it in our sites.

On the downside, there are several key levels to raise caution flags:

Stay above the 21d EMA which is a currently at 13,290.28.

The 10d MA is at 13,105.93. Going below this line will be a red flag.

If the index has a pull back, the 13,000 is a support area that must hold.

12,599.23 is the low from this week. Stay above that level to make a higher low.

The next support area is 12,500-12,550.

12,397.05 is the current bottom of the correction on the Nasdaq.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

This was a week that reminded us to take a step back and look at the weekly charts. The Nasdaq chopped back and forth, that seems like losses. But on the weekly chart, the index had a good gain with a great closing range.

At the same time, the choppiness may continue into the coming week and cause investors to get overly nervous. Although the other major indexes are performing well, eventually the big players in the Nasdaq could pull down those indexes as well.

It's important to avoid predictions. Instead, set some expectations for what you might think will happen. Watch those key levels in the Nasdaq, and follow the price action of the index and your favorite stocks. Keep stop losses up to date to protect from a sudden turn to the downside. But lets hope for upside.

The report is a bit brief this week since I'm heading out to vacation. I hope you have a great week ahead! I'll be trading from the beach. :)

Good luck, stay healthy and trade safe!

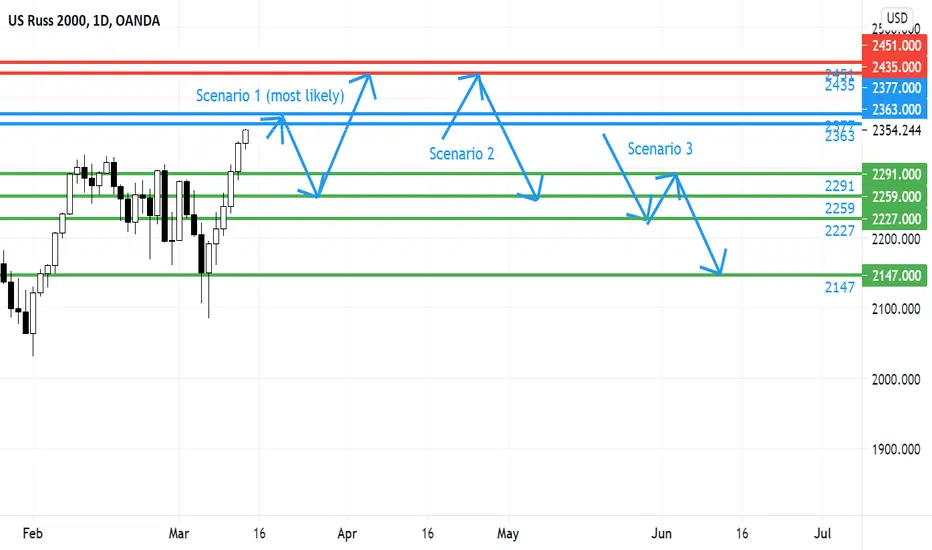

Weekly Analysis for #RUT for 15-19 March 2021Trend: Daily/Weekly/Monthly: Up/Up/Up

RUT is strongest of the 3 US indices. Expect rotation to continue and RUT to lead. I don’t and can’t call tops. But some signs point to pullbacks.

3 possible scenarios:

1) As long as 2363-77 resistance zone holds, look for shorts targeting 2259-91 support zone. This zone should hold for a next leg up, to 2435-51.

2) We have a fast rally from open to 2435-51 resistance zone, by Tuesday or Wednesday, where we see a sharp rejection for a strong move down to 2259-91.

3) We open in Globex and sell off start, targeting 2227 before a bounce to 2259-91 and further selling to 2147

IMO, scenario 1 is most likely.

Daily Market Update for 3/12Trend lines drawn from the 2/16 ATH (19d), 3/8 (5d) and today 3/12 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Friday, March 12, 2021

Facts: -0.59%, Volume lower, Closing range: 97%, Body: 58%

Good: Bulls bought back the morning lows to bring index back above 21d EMA

Bad: Lower high and lower low

Highs/Lows: Lower high, lower low

Candle: Green body above a lower wick with very small upper wick

Advance/Decline: About even advancing and declining stocks

Indexes: SPX (+0.10%), DJI (+0.90%), RUT (+0.61%), VIX (-5.57%)

Sectors: Real Estate (XLRE +1.72%) and Utilities (XLU +1.35%) were top. Communications (XLC -0.28%) and Technology (XLK -0.72%) were bottom.

Expectation: Sideways or Higher

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

Are you dizzy yet? This rotation just won't end. Every day this week the Technology sector flipped from the bottom of the sector list to the top and then the next day to the bottom. Yesterday it was at the top. Today it's back at the bottom. As long term bond yields are reaching for pre-pandemic highs, investors are still trying to determine the impact on valuations of big tech and growth stocks.

The Nasdaq closed the week with a green candle, but ended the day with a -0.59% decline. Volume was lower but the bulls bought up a morning dip to bring the index back above the 21d EMA in the afternoon. A closing range of 97% means a very small upper wick. The longer lower wick rests underneath a 58% green body. There were about the same number of advancing and declining stocks.

The Dow Jones Industrial average (DJI) and Russell 2000 (RUT) both made new all-time highs. The big industrial stocks of the DJI and small-caps of the RUT are likely to benefit the most from the new stimulus and recovering economy. The DJI closed with a 0.90% gain while the RUT advanced +0.61%. The S&P 500 (SPX) ended the day with a 0.10% gain.

The VIX volatility index declined -5.57%.

Real Estate (XLRE +1.72%) tops the sector list despite rising yields. With consumer sentiment on the rise, it could be a boon for real estate. Utilities (XLU +1.35%) and Industrials (XLI +1.34%) are also at the top. Communications (XLC -0.28%) and Technology (XLK -0.72%) moved back to the bottom.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) gained +0.27%.

Yields on the 30y and 10y treasury bonds both rose to new recent highs. The 30y yield is at its highest point since January 2020, while the 10y is at its highest point since early February 2020. The 2y yield rose modestly for the day. The yield curve is at its steepest since 2016. A steep yield curve means rising interest rates in the future.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both declined for another day.

Silver (SILVER) declined while and Gold (GOLD) advanced. Crude Oil (CRUDEOIL1!) remained about even. Timber (WOOD) continues to advance. Copper (COPPER1!) and Aluminum (ALI1!) declined.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio rose to 0.606. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is moving back toward the greed level.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

The four big mega-caps have been back and forth all week. Today they all declined. Microsoft (MSFT) and Alphabet (GOOGL) declined -0.58% and -2.41%, but remain above their key moving average lines. Apple (AAPL) and Amazon (AMZN) declined -0.76% and -0.77% and are below their 21d EMA and 50d MA lines.

New Oriental Ed (EDU) was the top mega-cap stock of the day with a +4.55% gain. Bank of America (BAC), Home Depot (HD) and Walmart (WMT) round out the top four, each with gains greater than 1.51%. Alibaba (BABA), Alphabet, and Facebook (FB) were at the bottom of the list with 2% or more declines.

Some growth stocks did well. SNAP (SNAP) had a great day with a +5.15% gain. Ehang Holdings (EH), Palantir (PLTR) and Grow Generation (GRWG) all had gains, albeit modest compared to recent history, at around 0.5% to 0.75%. DataDog (DDOG) , Okta (OKTA), Peloton (PTON) and JD.com (JD) were at the bottom of the growth list.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

The short-term 3 month and 6 month bill auctions will be on Monday. Late in the after TIC Net Long-Term Transactions will show how much investors are trading in foreign securities markets (both inbound and outbound to the US). The number is directly linked to currencies since the investors first need to buy the local currency before investing.

Monday's earning reports will include a couple interesting small-caps: Vuzix (VUZI) and Desktop Metal (DM).

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The index dipped back below the 21d EMA and 50d MA lines, but was able to close above the 21d EMA.

The five-day trend line points to a +1.51% advance while the one-day trend line points toa a +0.63% advance. Both would be moves back above the 50d MA.

The longer trend-line from the 2/16 ATH points to a -3.72% decline, moving the index back below the 13,000 area.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

It's been a wild week and I'm glad the weekend is here. The up and down of Technology and Growth stocks left investors not sure whether to be in or out of the action. If you found other plays in industrials or cyclical stocks, you might have had a great week.

I used the Nasdaq as the basis for the daily update because it represents most closely the stocks I invest in. But keep in mind that the Dow Jones Industrial average and the Russell 2000 are hitting new all-time highs. The S&P 500 index is also near new all-time highs. Once the rotation settles, we should see the Nasdaq start to move along more closely with the other indexes.

Even with the choppy week, the Nasdaq does close the week with gains over last week. Check your watch lists and find stocks that are acting pretty well compared to their peers and the market. I found the DELL chart recently and it seems DELL didn't get the memo for the tech correction.

Stay healthy and trade safe!

Daily Market Update for 3/11Trend lines drawn from the 2/16 ATH (17d), 3/4 (5d) and today 3/10 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Thursday, March 11, 2021

Facts: +2.52%, Volume lower, Closing range: 81%, Body: 67%

Good: Another higher high and higher low, back above 21d EMA and 50d MA

Bad: Not much, resistance at 13,400

Highs/Lows: Higher high, higher low

Candle: Thick red body with small upper and lower wicks, low closing range

Advance/Decline: Almost three advancing stocks for every declining stock

Indexes: SPX (+1.04%), DJI (+0.58%), RUT (+2.31%), VIX (-2.88%)

Sectors: Technology (XLK +2.14%) and Communications (XLC +1.89%) were top. Utilities (XLU -0.26%) and Financials (XLF -0.29%) were bottom.

Expectation: Sideways or Higher

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

The back and forth continues as the Nasdaq and technology stocks rise again. The sector list has flipped back and forth the last several days as investors rotate in and out of big tech and growth stocks. Today, the market rallied as jobs reports showed positive gains in the labor market and the stimulus is proceeding to Biden's signature. Technology was back on top while Financials moved to the bottom.

The Nasdaq closed with a +2.52% gain on lower volume. The 67% green body was formed in the morning as the index quickly rose to intraday highs around 13,400 and stayed there the rest of the day. The short upper wick is above an 81% closing range. There were almost three advancing stocks for every declining stock.

All four major indexes gained for the day with the Russell 2000 (RUT) advancing 2.31%, just behind the Nasdaq performance. The S&P 500 gained +1.04%. The Dow Jones Industrial gained +0.58%.

The VIX volatility index declined -2.88%.

The sector list flipped once again with Technology (XLK +2.14%) moving to the top, followed by Communications (XLC +1.89%) and Consumer Discretionary (XLY +1.53%). Financials (XLF -0.29%) moved to the bottom.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) declined -0.44%.

Yields on the US 30y and 10y treasury bonds rose. The 2y bond yields dropped.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both gained for another day.

Silver (SILVER) and Gold (GOLD) declined just slightly. Crude Oil (CRUDEOIL1!) gained. Timber (WOOD) continues to advance. Copper (COPPER1!) advanced while Aluminum (ALI1!) advanced.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio declined to 0.571 as investors get more bullish. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is moving back toward the greed level.

The NAAIM exposure index moved all the way down to 0.48. That's the lowest exposure since April of 2020 and brings up the question of what is driving prices higher if investment managers are reducing positions.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

All four big mega-caps advanced for the day. Alphabet (GOOGL) had the biggest advance with a +3.16% gain. Microsoft (MSFT) advanced +2.03%. Both Alphabet and Microsoft are trading above their 21d EMA and 50d MA lines. Apple (AAPL) and Amazon (AMZN) had gains of +1.65% and +1.83% but remain under their 21d EMA and 50d MA lines.

Taiwan Semiconductor (TSM), New Oriental Ed (EDU), PayPal (PYPL) and Tesla (TSLA) were the top four mega-caps. AT&T (T) and Verizon (VZ) were at the bottom of the list despite Communications ending near the top of the sector list.

Almost all the growth stocks in the daily update list had gains. UP Fintech (TIGR), Ehang Holdings (EH) and Digital Turbine (APPS) topped the list with more than 14% gains. SUMO Logic declined 13.51% after beating earnings but offering soft sales guidance.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

Friday's producer price index data will complement the consumer price data earlier in the week. In addition, the inflation expectation and consumer sentiment numbers released after the market opens will be watched closely.

Sharp (SHCAY) will report earnings on Friday before market open.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The Nasdaq moved above the 21d EMA and 50d MA lines today and met resistance around 13,400.

The five-day and one-day trend lines both point to another gain tomorrow that will be a +1.29% advance.

The longer trend-line from the 2/16 ATH points to a -4.60% decline, moving the index back below the 13,000 area.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

Having the index close above the 21d EMA and 50d MA is a great positive sign for the rally. Another advance on higher volume would solidify the rally in my opinion and I'd mark the bottom as 2/5 and update the trend-lines.

Still, I have a few concerns. The NAAIM exposure index moving to less than 50% while the market rallies is a mystery. What is driving prices higher if positions are being reduced by money managers. The answer could be the record amount of retail trading and the popularity of options trading.

Another indicator I've started to watch, but haven't been including here is the TRIN.NQ ARMS Trading Index. This index measures the Advance/Decline ratio against the Advancing Volume / Declining Volume ratio. A number of 1.00 indicates a balance of volume between advancing and declining stocks. A low number under 0.5 would mean there is a larger amount of volume going to advancing stocks and could indicate panic buying as investors buy the dip.

Nonetheless, an advance past the 21d EMA tells me there's reason to look at opportunities for entry with controlled risk. I'd be selective about what stocks are setting up with proper bases vs which are rebounding and may turn back around in the coming week as rally buying fades.

Stay healthy and trade safe!

Daily Market Update for 3/10Trend lines drawn from the 2/16 ATH (16d), 3/3 (5d) and today 3/9 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wednesday, March 10, 2021

Facts: -0.04%, Volume lower, Closing range: 14%, Body: 69%

Good: Higher high, higher low, support above 13,000

Bad: Rejection off 21d EMA in morning led to selling and close near low

Highs/Lows: Higher high, higher low

Candle: Thick red body with small upper and lower wicks, low closing range

Advance/Decline: More advancing stocks than declining stocks

Indexes: SPX (+0.60%), DJI (+1.46%), RUT (+1.81%), VIX (-6.12%)

Sectors: Energy (XLE +2.53%) and Financials (XLF +2.04%) were back on top. Technology (XLK -0.40%) was bottom.

Expectation: Sideways or Lower

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

The rotation settles. There was still signs of rotation in the market today, with the sector list flipping once again. But the effect is much more subdued than the past week. The passing of the stimulus has investors eyes wide open while they sent the Dow Jones Industrial to all-time highs.

The Nasdaq was not able to benefit from the enthusiasm as it declined -0.04%. A sideways move, but still a day marked by selling after a morning gap-up. The closing range of 14% is underneath a thick red body of 69% and slightly longer upper wick formed just after the market opened. There were more advancing stocks than declining stocks, however volume on declining stocks was higher.

The other three major indexes all gained for the day. The Russell 2000 (RUT) had the biggest gains with a +1.81% advance. The Dow Jones Industrial (DJI) gained +1.46% while the S&P 500 (SPX) gained +0.60%. The Dow Jones Industrial has a very bullish candle that closed at an all-time high.

The VIX volatility index declined another -6.12%.

The sector list flipped back and forth the past three days with the top and bottom trading positions. Energy (XLE +2.53%) and Financials (XLF +2.04%) were back on top. Technology (XLK -0.40%) was on the bottom and the only losing sector for the day.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) declined -0.15%.

Yields on the US 30y bond rose for the day while the 10y and 2y yields declined.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both gained for another day, showing investors' confidence in US corporations as the stimulus bill is passed.

Silver (SILVER) and Gold (GOLD) both advanced for another day. Crude Oil (CRUDEOIL1!) declined. Timber (WOOD) advanced. Copper (COPPER1!) advanced while Aluminum (ALI1!) declined.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio declined to 0.594 as investors get more bullish. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index remains near neutral.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

All four big mega-caps declined for the day. Microsoft (MSFT) declined -0.58% and moved back below its 21d EMA. Alphabet (GOOGL) declined -0.20% but closed above the key moving average lines. Apple (AAPL) and Amazon (AMZN) declined and remain below both key moving average lines.

Exxon Mobil (XOM) was the leading mega-cap of the day, gaining +3.07% on optimism over economic activity picking up in sectors that depend on oil.Comcast (CMCSA), Bank of America (BAC), and Walmart (WMT) were other winners at the top of the mega-cap list. New Oriental Ed (EDU) lost 14%. Alibaba (BABA), Taiwan Semiconductor (TSM) and ASML Holding (ASML), all mega-caps with foreign HQ.

The big winners in growth stocks were Draft Kings (DKNG) and Penn Gaming (PENN) with 11.40% and 6.65% gains. Digital Turbine (APPS) continues to reverse from recent lows with a +6.13% gain today. Still, the list of growth stocks tracked by the daily update has more losers than winners. MongoDb (MDB) , SUMO Logic (SUMO) and Peloton (PTON) all had losses of more than 4%.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

Thursday will bring an update to Initial Jobless Claims and the JOLTs Job Openings report. Both are expected to improve over previous numbers.

JD.com (JD) is the big mega-cap reporting on Thursday before market opens. DocuSign (DOCU) and Celsius (CELH) will also report Thursday.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The Nasdaq was able to stay above 13,000 today. It tested but was not able to move above the 21d EMA.

The five-day trend line points to a positive gain of +1.25% for Thursday.

The one-day trend line is pointing to a -0.90% loss that would break back below the 13,000 area.

The longer trend-line from the 2/16 ATH points to a -2.76% decline for tomorrow.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

I am still waiting for a positive gain on higher volume, and ideally a move back above the 21d EMA. That will show more support in the Nasdaq and in our favorite tech and growth stocks.

It's also a good time to look out beyond the stocks that were working so well in 2020 and discover the stocks that are likely to benefit from the economic recovery.

The good news is that the swings in bond yields and fears of inflation seem to be subsiding which will bring a little more predictability to the market.

Stay healthy and trade safe!

Daily Market Update for 3/9Trend lines drawn from the 2/16 ATH (16d), 3/3 (5d) and today 3/9 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Tuesday, March 9, 2021

Facts: +3.69%, Volume higher, Closing range: 71%, Body: 56%

Good: Good gain on higher volume, higher high, higher low, above 13k

Bad: Selling in last hour of day

Highs/Lows: Higher high, higher low

Candle: Slightly longer upper wick with a thick green body

Advance/Decline: Two advancing stocks for every declining stock

Indexes: SPX (+1.42%), DJI (+0.10%), RUT (+1.91%), VIX (-5.65%)

Sectors: Consumer Discretionary (XLY +3.78%) and Technology (XLK +3.40%) were the top sectors. Financials (XLF -0.91%) and Energy (XLE -1.75%) were bottom.

Expectation: Sideways or Higher

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

The rotation reverses. Today saw a reversal of the past several days rotation as money flooded back into big tech, consumer discretionary, and growth stocks. Treasury bond yields seemed to stabilize a bit allowing investors to turn their eyes on the stimulus and the impact it will have on performance in the near term.

The Nasdaq closed with +3.69% gain on higher volume. The closing range of 72% came after some selling in the final hour of trading, forming the upper wick. The green body covers 56% of the candle and represents a day that was dominated by the bulls. There were two advancing stocks for every declining stock.

All major indexes had gains for the day with the Dow Jones Industrial average (DJI) having the smallest gain in contrast to the past several days. The S&P 500 (SPX) gained +1.42% while the Russell 2000 gained +1.91%.

The VIX volatility index declined -5.65%.

Consumer Discretionary (XLY +3.78%) and Technology (XLK +3.40%) were the top sectors as investors rushed in for buying opportunities. Financials (XLF -0.91%) and Energy (XLE -1.75%) were bottom.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) pulled back -0.38% after several days of gains.

Yields on the US 30y, 10y and 2y treasury bonds all declined for the day. That was a welcome change for investors nervous about the impact of higher yields on big tech and growth stocks.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) both gained after several days of declines.

Silver (SILVER) and Gold (GOLD) both advanced for the day. Crude Oil (CRUDEOIL1!) declined. Timber (WOOD) advanced. Copper (COPPER1!) and Aluminum (ALI1!) declined.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio rose to 0.661. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index is neutral.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

All four big mega-caps advanced for the day. Apple (AAPL) and Amazon (AMZN) had the biggest gains with +4.06% and 3.76% advances. Microsoft (MSFT) gained +2.81% and Alphabet (GOOGL) gained +1.64%. Microsoft and Alphabet closed back above their 21d EMA. Apple and Amazon remain below the 21d EMA and 50d MA lines.

Tesla (TSLA) made a huge upside reversal with a 19.65% gain. Nvdia (NVDA), ASML Holding (ASML) and PayPal (PYPL) all gained more than 6%. Walt Disney (DIS) dropped -3.66% after a big gain the previous day. Bank of America (BAC) and Exxon Mobil (XOM) led their respective sectors lower with declines of over 2% each.

Sixteen of the growth stocks tracked for the daily update had gains over 10%. Another eighteen had gains between 5% and 10%. Looking at the extended list of growth stocks, the number of stocks with big gains just keeps going. Only Dr Horton (DHI) had a loss, but that was after two days of gains despite the market dipping. Ehang Holdings (EH) was the big winner with a 31% gain. FUTU Holdings (FUTU) and UP Fintech (TIGR) were also Chinese stocks at the top of the growth stock list. Grow Generation (GRWG) had an 18% gain.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

There are two significant economic events for Wednesday. First, I had anticipated the stimulus vote being today, but Nancy Pelosi announced shortly after my update that it would likely happen Wednesday.

The second big event will be the 10y note auction by the US Treasury. Today's 3y note auction had an average response, alleviating some fears by investors.

Another look at inflation will come on Wednesday with the release of consumer price index data in the morning. Crude Oil Inventories data will come after the market opens.

Oracle (ORCL) will report on Wednesday. Joining Oracle, will be Campbell Soup (CPB), Cloudera (CLDR) and Sumo Logic (SUMO).

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The Nasdaq was able to get back above 13,000 today. It paused slightly in that area before moving higher, showing it's still both a support and resistance line.

If today's rebound continues, the one-day trend line points to a +1.92% gain for tomorrow that would take the index back above the 21d EMA. Another higher volume gain that restores the index above the 21d EMA would be a confidence booster.

The five-day trend line points to a -1.75% loss, back below the 13,000 area. The trend line from the 2/16 ATH is pointing to a -2.94% decline for tomorrow.

I'll remove the head and shoulders pattern from the discussion since we moved back above the neckline. If we decline again, then we'll revisit the levels in the pattern.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

It was a positive expectation breaker today. Monday's selling seemed the index wanted to go lower, but the market does what it wants to do. The rotation back into big tech obviously helps the tech-heavy Nasdaq to have huge gains.

Remember that rotations swing back and forth before the right level is discovered in the market. There's plenty of evidence of panic buying in today's bullish results. That panic buying can easily turn into profit taking, especially as these stocks with massive gains hit overhead supply and investors take the chance to get out of what was a losing position.

So proceed with caution. The expectation tomorrow is set for sideways or higher. Keep an eye on your favorite stocks and see how they perform over the next few days before overcommitting.

Stay healthy and trade safe!

Daily Market Update for 3/8Trend lines drawn from the 2/16 ATH (15d), 3/2 (5d) and today 3/8 (1d).

Ideas always welcome in the comments. Errors will be amended as comments on TradingView or corrected inline in my blog.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Monday, March 8, 2021

Facts: -2.41%, Volume lower, Closing range: 2%, Body: 73%

Good: Held above 12,600 as market closed

Bad: Could not hold short rally in morning, selling the rest of afternoon

Highs/Lows: Higher high, higher low

Candle: Short upper wick over a thick red body, no lower wick

Advance/Decline: More than one declining stock for every advancing stock

Indexes: SPX (-0.54%), DJI (+0.97%), RUT (+0.49%), VIX (+3.28%)

Sectors: Utilities (XLU +1.41%) and Materials (XLB +1.34%) were the top sectors. Communications (XLC -1.34%) and Technology (XLK -2.42%) were bottom.

Expectation: Lower

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Overview

The rotation continues. It's not often that a rotation is so clearly seen, with the Dow Jones ending the day up nearly 1% and the Nasdaq ending the day down 2.41%. Nine sectors outperformed the broader S&P 500 index, while the other two sectors lost enough to bring down the index for a loss by the end of the day.

The Nasdaq closed the day with a -2.41% loss on lower volume. The closing range of 2% followed an afternoon of selling that formed the 73% red body underneath a small upper wick from the short morning rally. There were more declining stocks than advancing stocks.

The Dow Jones Industrial average (DJI) gained +0.97% for the day. The Russell 2000 (RUT) advanced +0.49%. The S&P 500 declined -0.54%.

The VIX volatility index rose +3.28%.

Utilities (XLU +1.41%) and Materials (XLB +1.34%) were the top sectors for the day, with 8 out of the 11 SPDR sectors advancing for the day. Communications (XLC -1.34%) and Technology (XLK -2.42%) were the bottom, weighted down by losses from large mega-caps that dominate the two sectors.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Economic Indicators

The US Dollar (DXY) continues to advance with a +0.45% gain today. It has now regained a support area from the second half of 2020.

Yields on the US 30y and 10y treasury bonds rose for the day. The 2y yield spiked above 1.5 again with a 16% increase to 0.169.

High Yield Corporate Bonds (HYG) and Investment Grade Corporate Bond (LQD) prices both dropped.

Silver (SILVER) and Gold (GOLD) both declined for the day. Crude Oil (CRUDEOIL1!) pulled a bit back from its recent advance. Timber (WOOD) advanced. Copper (COPPER1!) advanced while Aluminum (ALI1!) declined.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Investor Sentiment

The put/call ratio dropped to 0.633. The put/call ratio (PCCE) is a contrarian indicator that shows overly bullish or overly bearish investor behavior. The 0.7 level is considered normal. As it approaches 0.60 (overly bullish) and below, watch for a possible pullback in the market.

The CNN Fear & Greed index moved toward the greed side.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Market Leaders

All four big mega-caps declined for the day. Alphabet (GOOGL) and Apple (AAPL) had the biggest losses with -4.27% and -4.17% declines. Microsoft (MSFT) declined -1.82%. Amazon (AMZN) declined for -1.62%. All four are trading below their 21d EMA and 50d MA. They continue to weigh down the indexes and their respective sectors as they have an overweight impact due to their size.

Several mega-caps did very well for the day. Walt Disney (DIS) gained +6.27% for the day. Roche Holding (RHHBF) gained 5%. Oracle (ORCL) and Cisco Systems (CSCO) proved not all is bad for mega-cap tech stocks with gains of around 3% each. Mastercard (MA) and Visa (V) also appeared at the top of the mega-cap list. PayPal (PYPL), Taiwan Semiconductor (TSM), Tesla (TSLA), and Nvidia (NVDA) occupied the bottom of the list with over 5% losses each.

Growth stocks tracked by the daily update were mostly down for the day. Dr Horton (DHI), Draft Kings (DKNG), Ehang Holdings (EH) and Penn National Gaming (PENN) all had gains for the day. FUTU Holdings (FUTU), UP Fintech (TIGR) both were hit with greater than 10% declines. Digital Turbine (APPS) declined a huge 16.32% and is nearly 40% below its all-time high set less than a week ago.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Looking ahead

The EIA Short-Term energy outlook will be released before market opens on Tuesday. After market close, the API Weekly Crude Oil stock numbers will be released. The house is expected to vote on the stimulus bill on Tuesday.

MongoDb (MDB) and Open Lending (LPRO) will report earnings tomorrow.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Trends, Support and Resistance

The trend line from the 2/16 ATH is pointing to a +0.60% gain for tomorrow that would be a nice bounce the 12,600 area.

The one-day trend line is pointing to a -1.63% which would test the 12,400 low from Friday. The five-day trend line points to a -2.19% loss, breaking thru the 12,400 mark.

We've been keeping an eye on a head and shoulders pattern. This pattern represents an attempt to move back to new highs that was rejected at a previous resistance point. Typically the height of the head is measured to determine the potential move downward that will occur as the price breaks below the neck line, which occurred last week.

I've also been cautioning that the drop would not happen in a straight line. Expect some back-and-forth as the index looks for a bottom. The target low from the pattern is 6.3% below Monday's close. Of course, the index could move lower than that point.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wrap-up

Although the expectation set for today was sideways or higher based on Friday's candle, I also noted the weak volume in the rebound on Friday that gave me concern about holding the gains into Monday. Today's sell-off was also at low volume, so it did not really set a decisive direction for the index. Nonetheless, buyers of Nasdaq mega-cap stocks were missing even as the index dipped to a lower close.

Given the thick red bodied candle, the expectation for tomorrow is lower. The passing of the stimulus may provide some support to some segments of stocks but it may also stoke more fears of inflation and rising interest rates that have pulled down big tech and growth stocks.

Keep an eye out for stocks that are preforming well relative to the indexes and put them on your watch list.

Stay healthy and trade safe!

Market Week In Review - 3/1/2021 - 3/5/2021The Market Week in Review is my weekend homework where I look over what happened in the previous week and what might come in the next week. It helps me evaluate my observations, recognize new data points, and create a plan for possible scenarios in the future.

I do occasionally have some errors or typos and will correct them in my blog or in the comments on TradingView. I do not have an editor and do this in my free time.

If you find this helpful, please let me know in the comments. I am also more than happy to add new perspectives and data points if you have ideas.

The structure is the following:

A recap of the daily updates that I do here on TradingView.

The Meaning of Life, a view on the past week

What's coming in the next week

The Bullish View, The Bearish View

Key index levels to watch out for

Wrap-up

If you have been following my daily updates, you can skip down to the “The Meaning of Life”. If not, then this first part is a great play-by-play recap for the week. Click the original charts for more detail each day.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Monday, March 1, 2021

Facts: +3.01%, Volume lower, Closing range: 97%, Body: 78%

Good: Strong buying throughout day, close above 21d EMA

Bad: Nothing

Highs/Lows: Higher high, higher low

Candle: Thick green body with short upper/lower wicks, slightly longer lower wick

Advance/Decline: More than three advancing stocks for every declining stock

Indexes: SPX (+2.38%), DJI (+1.95%), RUT (+3.37%), VIX (-16.46%)

Sectors: Technology (XLK +3.22%) and Financials (XLF +3.13%) were top. Consumer Staples (XLP +1.01%) and Real Estate (XLRE +0.11%) were bottom.

Expectation: Higher

Monday kicked off the week with an upside reversal from last week's downtrend. A small gap up was closed early in the session that was dominated by buying the rest of the day. The gains were large and broad across the market as manufacturing data released in the morning was better than expected.

The Nasdaq closed the day with a +3.01% gain. Volume was lower than Friday. The closing range of 97% represented the buying that continued into close after gains throughout the day created a 78% green body. More than three stocks gained for every declining stock.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Tuesday, March 2, 2021

Facts: -1.69%, Volume lower, Closing range: 3%, Body: 97%

Good: Stayed above 50d MA

Bad: All red body, no visible upper/lower wicks, back below 21d EMA

Highs/Lows: Higher high, lower low

Candle: Marubozu black candle with no wicks, all red body, outside day

Advance/Decline: More than three declining stocks for every advancing stock

Indexes: SPX (-0.81%), DJI (-0.46%), RUT (-1.93%), VIX (+3.21%)

Sectors: Materials (XLB +0.56%) only gaining sector. Consumer Discretionary (XLY -1.15%) and Technology (XLK -1.59%) were bottom.

Expectation: Sideways or Lower

The market gave up half of yesterday's gains in a continuation of two weeks of choppiness as investors await a stimulus bill that will have both positive and negative impacts on equities. Today's expectation breaker after yesterday's session requires a deeper look to understand. Investment has been rotating in and out of Consumer Discretionary and Technology for the past two weeks.

The Nasdaq closed the day with a -1.69% decline on lower volume. The 97% red body with no visible upper and lower wick forms a Marubozu (shaven head) candlestick. The 3% of lower wick was formed in just the last few minutes of trading as most of the day was dominated by selling. There were three declining stocks for every advancing stock.

-=x=-=x=-=x=-=x=-=x=-=x=-=x=-

Wednesday, March 3, 2021

Facts: -2.7%, Volume higher, Closing range: 1%, Body: 90%

Good: 13,000 just barely holding on

Bad: Higher volume selling day shows institutional distribution

Highs/Lows: Lower high, lower low

Candle: Tiny upper wick created at open, thick red body with no lower wick

Advance/Decline: More than two declining stocks for every advancing stock

Indexes: SPX (-1.31%), DJI (-0.39%), RUT (-1.06%), VIX (+10.66%)