FRSHThis is a very pre-mature chart here I'm doing for you @ALYWLAM

I can expect Frshworks to stay bullish in long run. Although we may be witnessing the start of a shakeout on the stock since it's fairly new into the market.

We've seen an instance like AFRM where it dropped in half from open price all the way down to the 40's before forming a cup and handle and exploding to the upside, which I hope happens with FRSH.

Continue to buy up the stock at any given lvl in the 20's or even low 30's iMO.

I'm bullish on the long term existance of this stock.

SAAS

China's SaaS: An 'Open Ocean' Up Ahead (4/4)China's cloud computing industry is still gradually developing, which implies infinite opportunities. When it comes to SaaS, the potential is even larger. This article is an overview of the country's cloud computing industry featuring the key players in the market, including Kingdee, Kingsoft, Youzan and Weimob.

Server device

In China, public cloud services have been increasingly popular, along with a number of existing customers showing desires to extend and customize the providers' offerings at their own expense. The country's cloud service value chain possesses enormous investment value at different levels. One reason is that the high cost of data migration generates solid user stickiness; the other reason is the relative independence of the sector from macroeconomic fluctuations. As projected by IDC, the cloud computing penetration among enterprises will increase to 15.8% by 2024 in China. By then, the market size will reach CNY 563.3 billion.

Currently, China's cloud market is at an early stage of development, with a lower market penetration rate compared with that in the United States. As per R&D World, China's spending on research and development (R&D) is expected to top with USD 621.5 billion in 2021, denoting a 25.5% share of the global R&D spending that year. In contrast, China's spending on cloud computing services only accounts for 6.2% of the global figure. It points to the fact that there is a great potential for the cloud computing market within China along with the continuing technological development.

11 out of the 20 most prominent tech companies in the US have been intensively engaged in the software-as-a-service (SaaS) business, which accounts for 40% of the value of those 20 companies. On the contrary, only 6 out of the 20 major tech players in China have SaaS business, occupying slightly 3% of the total value of those 20 largest Chinese techs. The industry's key players in China are the local SaaS providers such as Kingdee and foreign players that charge exorbitant prices in exchange for customized services.

Considering China's strict regulation on foreign companies, especially in various technology-related fields, the local companies are more likely to get the upper hand in the competition.

Weimob (02013:HK)

Weimob was founded in 2013 and currently has over 5,700 employees, 1,600 channel partners, and 3 million registered merchants. Providing cloud-based commerce and marketing solutions, it leverages Tencent’s social networking service platforms for SMBs in China. The company provides SaaS and other software for e-commerce, retail, catering, hotel, local life and other industries, enabling merchants to carry out traffic management, obtain public domain traffic, and supports them to achieve digital transformation.

In view of the recent trend of more enterprise customers maintaining direct connections with users through WeChat, Weimob will see strong momentum in digital commerce revenue growth and continue to expand its scope from the SaaS area to more extended services.

China's SaaS: An 'Open Ocean' Up Ahead (3/4)China's cloud computing industry is still gradually developing, which implies infinite opportunities. When it comes to SaaS, the potential is even larger. This article is an overview of the country's cloud computing industry featuring the key players in the market, including Kingdee, Kingsoft, Youzan and Weimob.

Server device

In China, public cloud services have been increasingly popular, along with a number of existing customers showing desires to extend and customize the providers' offerings at their own expense. The country's cloud service value chain possesses enormous investment value at different levels. One reason is that the high cost of data migration generates solid user stickiness; the other reason is the relative independence of the sector from macroeconomic fluctuations. As projected by IDC, the cloud computing penetration among enterprises will increase to 15.8% by 2024 in China. By then, the market size will reach CNY 563.3 billion.

Currently, China's cloud market is at an early stage of development, with a lower market penetration rate compared with that in the United States. As per R&D World, China's spending on research and development (R&D) is expected to top with USD 621.5 billion in 2021, denoting a 25.5% share of the global R&D spending that year. In contrast, China's spending on cloud computing services only accounts for 6.2% of the global figure. It points to the fact that there is a great potential for the cloud computing market within China along with the continuing technological development.

11 out of the 20 most prominent tech companies in the US have been intensively engaged in the software-as-a-service (SaaS) business, which accounts for 40% of the value of those 20 companies. On the contrary, only 6 out of the 20 major tech players in China have SaaS business, occupying slightly 3% of the total value of those 20 largest Chinese techs. The industry's key players in China are the local SaaS providers such as Kingdee and foreign players that charge exorbitant prices in exchange for customized services.

Considering China's strict regulation on foreign companies, especially in various technology-related fields, the local companies are more likely to get the upper hand in the competition.

China Youzan (08083:HK)

Youzan provides merchants with social network-based SaaS systems with omnichannel operations and integrated new retail solutions, applying PaaS cloud services to create business customization options while providing extended services, such as Youzan Guarantee, Youzan Distribution and Youzan Promotion.

Within Youzan's ecosystem, merchants can sell items via social networks, managing their own omnichannel retail through the company's SaaS solutions. The firm also offers a variety of cloud-based commerce services to merchants through a suite of SaaS products such as Youzan WeiMall, Youzan Retail, Youzan Chain, Youzan Beauty and Youzan Education. In addition, Youzan specializes in the SaaS business that supports SME merchants and facilitates retail transactions. Across industries, management teams lacking a technical background can easily open a customized online store on Youzan.

Youzan's gross merchandise volume (GMV) in 2020 was CNY 103.7 billion, a 61% increase compared to 2019's figure. In the same year, the gross profit margin of its SaaS products increased by 11.8%, reaching 76.0%.

China's SaaS: An 'Open Ocean' Up Ahead (2/4)China's cloud computing industry is still gradually developing, which implies infinite opportunities. When it comes to SaaS, the potential is even larger. This article is an overview of the country's cloud computing industry featuring the key players in the market, including Kingdee, Kingsoft, Youzan and Weimob.

Server device

In China, public cloud services have been increasingly popular, along with a number of existing customers showing desires to extend and customize the providers' offerings at their own expense. The country's cloud service value chain possesses enormous investment value at different levels. One reason is that the high cost of data migration generates solid user stickiness; the other reason is the relative independence of the sector from macroeconomic fluctuations. As projected by IDC, the cloud computing penetration among enterprises will increase to 15.8% by 2024 in China. By then, the market size will reach CNY 563.3 billion.

Currently, China's cloud market is at an early stage of development, with a lower market penetration rate compared with that in the United States. As per R&D World, China's spending on research and development (R&D) is expected to top with USD 621.5 billion in 2021, denoting a 25.5% share of the global R&D spending that year. In contrast, China's spending on cloud computing services only accounts for 6.2% of the global figure. It points to the fact that there is a great potential for the cloud computing market within China along with the continuing technological development.

11 out of the 20 most prominent tech companies in the US have been intensively engaged in the software-as-a-service (SaaS) business, which accounts for 40% of the value of those 20 companies. On the contrary, only 6 out of the 20 major tech players in China have SaaS business, occupying slightly 3% of the total value of those 20 largest Chinese techs. The industry's key players in China are the local SaaS providers such as Kingdee and foreign players that charge exorbitant prices in exchange for customized services.

Considering China's strict regulation on foreign companies, especially in various technology-related fields, the local companies are more likely to get the upper hand in the competition.

Kingsoft Cloud Holdings (KC:NASDAQ)

Kingsoft Cloud is the largest independent cloud service provider in China. Unlike many others in the space who tend to be narrowly segmented, it has extended from its original infrastructure-as-a-service (IaaS) model to platform-as-a-service (PaaS) to SaaS, forming a complete closed-loop that covers the entire cloud computing market to achieve cross-functional expansion as the scale grows. Kingsoft Cloud has built a comprehensive cloud platform consisting of extensive Cloud infrastructure, diverse products and industry-specific solutions across public cloud, enterprise cloud and AIoT cloud services. Powered by Kingsoft Group's enterprise service capabilities, Kingsoft Cloud is widely trusted in China and has inherited a huge customer base.

In the midst of fierce competition in the cloud service market, Kingsoft Cloud raised a total of USD 720 million in six rounds of funding in 2017-2018 and went public in May 2020. With sufficient cash reserves and the support from consumer electronics giant Xiaomi, Kingsoft has been able to survive and thrive. Its customer are, however, so concentrated now that the three largest of them account for 53% of its revenue.

Kingsoft Cloud's focused approach has made it a prime force in a few cloud industry subfields, such as games, video streaming, live streaming and finance. It is now expected to further boost its presence in various new verticals, where the main potential of the cloud market is mainly distributed. For example, Kingsoft Cloud recently shifted to the financial and government fields, enabling it to open up new business fulcrums beyond the public cloud business. In 2019, Kingsoft Cloud entered the field of Artificial Intelligence of Things (AIoT), which happens to be one of the key investment areas in China's 'new infrastructure' course.

China's SaaS: An 'Open Ocean' Up Ahead (1/4)China's cloud computing industry is still gradually developing, which implies infinite opportunities. When it comes to SaaS, the potential is even larger. This article is an overview of the country's cloud computing industry featuring the key players in the market, including Kingdee, Kingsoft, Youzan and Weimob.

Server device

In China, public cloud services have been increasingly popular, along with a number of existing customers showing desires to extend and customize the providers' offerings at their own expense. The country's cloud service value chain possesses enormous investment value at different levels. One reason is that the high cost of data migration generates solid user stickiness; the other reason is the relative independence of the sector from macroeconomic fluctuations. As projected by IDC, the cloud computing penetration among enterprises will increase to 15.8% by 2024 in China. By then, the market size will reach CNY 563.3 billion.

Currently, China's cloud market is at an early stage of development, with a lower market penetration rate compared with that in the United States. As per R&D World, China's spending on research and development (R&D) is expected to top with USD 621.5 billion in 2021, denoting a 25.5% share of the global R&D spending that year. In contrast, China's spending on cloud computing services only accounts for 6.2% of the global figure. It points to the fact that there is a great potential for the cloud computing market within China along with the continuing technological development.

11 out of the 20 most prominent tech companies in the US have been intensively engaged in the software-as-a-service (SaaS) business, which accounts for 40% of the value of those 20 companies. On the contrary, only 6 out of the 20 major tech players in China have SaaS business, occupying slightly 3% of the total value of those 20 largest Chinese techs. The industry's key players in China are the local SaaS providers such as Kingdee and foreign players that charge exorbitant prices in exchange for customized services.

Considering China's strict regulation on foreign companies, especially in various technology-related fields, the local companies are more likely to get the upper hand in the competition. Four companies discussed below are those positioned exceptionally well to benefit from the country's cloud upgrade:

Kingdee (00268:HK)

Holding 6.8% of China's cloud market, per EqualOcean data, Kingdee has maintained the largest share in enterprise SaaS cloud services for two consecutive years, while its enterprise-grade SaaS ERM (cloud ERP) and 'Financial Cloud' services have taken this position for 4 consecutive years. Kingdee is also one of the largest ERP software providers in China.

In 2020, Kingdee continued to redirect resources to the SaaS business, leveraging its large corporate customer pool, in an attempt to gradually alienate itself from the ERP software business by focusing on the development and promotion of subscription-based cloud products. As a result, the SaaS business reached 57% of the total revenue in the 2020 fiscal year, surpassing the ERP business (43%) for the first time. After cultivating a solid customer base in its ERP segment, Kingdee would be able to convert many of them into buyers of the other services.

$CRWD flag - long to 300 extended target, 250 initial$CRWD showing a beautiful symmetrical triangle setup. If you missed my $BNTX callout this is next to run hard and fast.

$PANW in their last ER admitted they are losing business to $CRWD which is growing at record pace.

Positions: 240/250c 6/18; 250/260c 7/16

IBM breaking 8 year downtrendIBM is beginning to break out on the weekly chart from a trend line that was acting as strong resistance for over 8 years.

Recently the company has unveiled the world's first 2nm chip and announced previously that it will begin focusing on Cloud and AI which will serve the company well as those are two large secular growth stories. Go Long IBM. Trades at 9.79 EV/EBITDA ratio, well run company financially with a long growth path ahead of it.

I expect IBM and INTC to be some of the main beneficiaries of the bill that just passed in the senate today that okayed $54 billion dollars for the Semiconductor Industry to focus production on American soil and improve research efforts. INTC and IBM have long been the American blue-chip players in the space and are currently collaborating in advanced semiconductor research. This is a timely partnership as INTC is building two new fabs in Arizona and IBM just released its 2nm chip but does not manufacture its own chips (ahem ahem INTC).

Long-term Price Target: $250

Daily Chart w/ Golden Cross:

CARDSTACK - A "Clean No Comment" Series Entry #3Entry number three of

a "Clean No Comment" chart.

Viewer inference advised.

ADBE over 475.00Cloud/SaaS were some of the growth leaders pre and post-COVID but have significantly cooled off since the peak in August/September and did not rally to the degree other names did in November - February. ADBE is forming a flag on the weekly viewing shown here on the daily, entry provided at 475.00 over VPOC, price action resistance which also serves as a "round number" psych level.

ASAN over 40.20This software name recently IPOed in 2020 and is breaking ATH. Trend based fib extensions above as potential resistance levels.

AYX - Break out of Triangle patternAlteryx, Inc. provides self-service data analytics software platform. They have beaten 4th quarter earnings for past 3 years and Im looking for them to beat again. They have just broken out of triangle pattern on daily chart (could also be double bottom pattern). The Feb options put call ratio is high at .97, so risky to hold thru earnings. $130 calls and $130 puts have the highest OI.

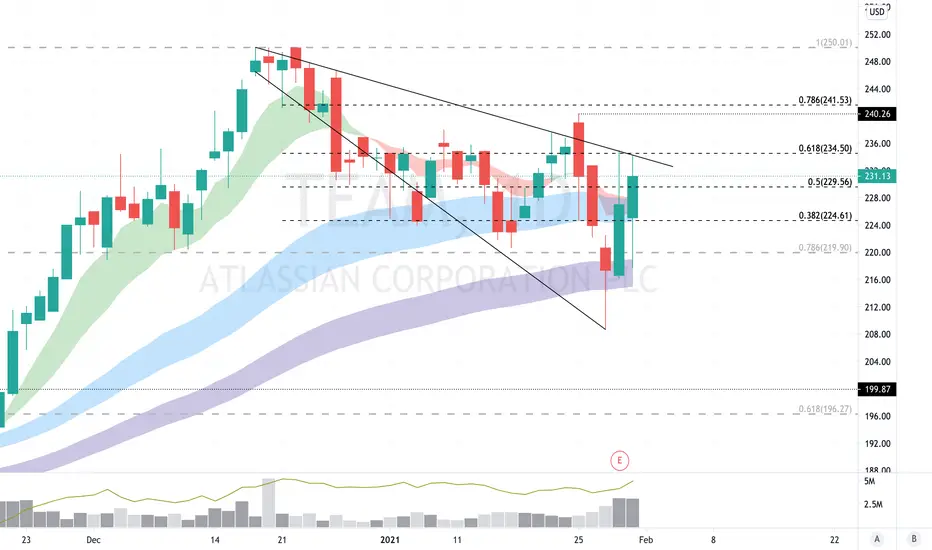

TEAM over 240.26Relative strength on last week's market weakness, can break higher out of this descending broadening formation. Cloud/software/cyber security names looking strong into this week, we'll see if this sector gets rotation.

SNOW READY FOR A BLIZZARD !1! Snow on the daily is getting squeezed by a bullish pennant . MACD is looking ready to flip along with squeeze momentum finally finishing its sell off. With declining sell volume as well and SNOW consistently holding up its long term support line we could see SNOW gap up to its first price target of $330. Along with the trend analysis as seen we also have to take into account NASDAQ:MSFT earnings report released today stating that they had a 17% revenue increase because of cloud business. The future is SaaS and SNOW is looking ready to snow some cash !

AYX - Triangle patternAlteryx, Inc. provides self-service data analytics software platform. Recorded bad earnings last quarter and has wild 15-20% swings. Short interest is 8.7 %. I like this triangle pattern to breakout, as in my last post MSFT will post good earnings and benefit tech stocks next week.

GDRX - Bullish pennant forming on dailyGoodrx is in the cloud software healthcare sector. Nice looking bullish pennant (lower highs , higher lows) on daily with over 28% short interest. Finviz has a $48 price target. Microsoft has earnings next week, so they should push all SaaS/Cloud stocks next week. Good luck!

DBX watch breakout from previous MA cross over areas NASDAQ:DBX

Watch out for area b/t 2 red line, previous heavily traded area, if price can stay in b/t for another 20-30 days, all MAs will be aligned for a huge run-up.

If rush up too much, then maybe a false break out since 200MA still huge resistance to the price

Sentimental :

lots of youtubers pumping it. SAAS overall high value VS DBX "poor" P/E ( due to its poor profitability ( maybe a take over? )

DDOG over 99.61ConThis has moved well and been a nice trade up from the 90s and looks to continue beyond the psych level of 100.Confluence at the fib and VPOC at the 103.50 area can serve as a first target, second above at 110.92.

FEYE over 15.29Nice IH&S setup with a big move that didn't hold, may need to find support before trying again.

Cup and handle, primed for a big moveA strong name recently that has consolidated over the past week and a half with some sharp moves up that were not held. A break should yield a large move. Major and minor fibs marked above.

Another IPO bounce playAfter a disappointing post-IPO performance, this may be finding bottom, tightening price action may lead to a large upside move.

Support of a volume shelf with a clear path upwardAfter consolidating, ADSK has the potential for a technical-based move upward to the top of this trend line.