Opening (IRA): QQQ August 16th 380 Short Put... for a 4.00 credit.

Comments: Starting to round out my Q3 rungs here on weakness and higher IV, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

Shortput

Opening (IRA): IWM July 19th 190 Short Put... for a 2.33 credit.

Comments: Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. (This is actually at the 18 delta, but it was either the 190 or the 185 where I wanted to pitch my tent from a delta standpoint).

Starting to slowly deploy third quarter rungs here in broad market (IWM, QQQ, SPY) while I piddle around with shorter duration higher IV sector ETF stuff.

Opening (IRA): IWM Sept/Oct 160/150 Short PutsComments: Going ahead and rounding out Q3 rungs here with IVR at 82.7.

September 20th 160: filled for a 1.99 credit

October 18th 150: filled for a 1.61 credit

Will look to manage shorter duration rungs as I come to them ... .

Opening (IRA): TLT July 19th 86 Short Put... for a .98 credit.

Comments: Adding to my TLT position on weakness here, targeting the strike paying around 1% of the strike price in credit.

I already have rungs on in April/May/June, so am adding a smidge out in July.

With QQQ and SPY knocking on ATH's, holding off on my usual broad market plays to await weakness and/or higher IV.

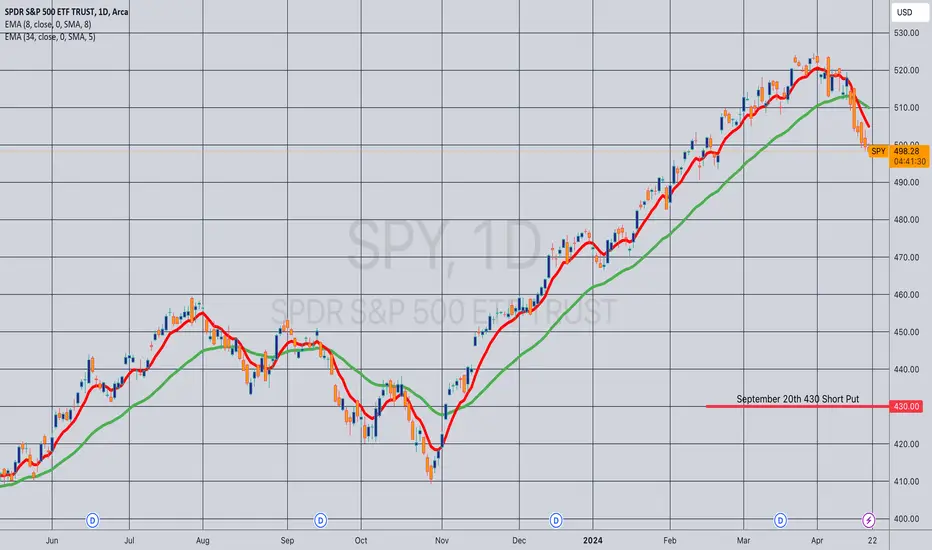

Opening (IRA): QQQ September 20th 430 Short Put... for a 4.34 credit.

Comments: Adding a rung out in Sept at the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging Into the Q's. I already have rungs on in June, July, and August ... .

Will naturally back-track into shorter duration if I can get in at strikes better than what I currently have on.

Opening (IRA): QQQ August 16th 370 Short Put... for a 4.30 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the Q's.

Adding at a strike better than what I currently have on in August ... .

Opening (IRA): IWM August 16th 170 Short Put... for a 1.78 credit.

Comments: Starting to round out my Q3 rungs here on weakness and higher IV, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. Already have June and July rungs on, so going out to August here.

Opened (IRA): IWM June/July 182/180 Short PutsComments: Added at strikes better than what I currently have on in weakness, targeting the <16 delta strikes in the respective expiries paying around 1% of the strike price in credit to emulate dollar cost averaging into the small cap ETF.

June 21st 182: Filled for 1.89

July 19th 180: Filled for 2.22

I also briefly looked at QQQ and SPY, but couldn't get in at strikes better than what I currently have on, so am leaving those positions alone for now.

Opening (IRA): IWM June 21st 175/July 19th 170 Short PutsComments: Targeting the <16 delta strikes paying around 1% of the strike price in credit to emulate dollar cost averaging into the small caps ETF.

Adding here on weakness, better strikes than what I currently have on in those expires.

Filled the June 21st for a 1.75 credit; the July 21st 170 for 1.76.

Opening (IRA): IWM June 21st 185 Short Put... for a 1.87 credit.

Comments: Targeting the <16 delta strike in the shortest duration that pays around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

The ROC %-age isn't tremendously sexy here, so primarily doing this to keep theta on and burning while I work shorter duration, higher IV underlyings (e.g., SMH, XBI, GDX/GDXJ, etc.).

Opening (IRA): XBI June 21st 82 Short Put... for a 1.90 credit.

Comments: Selling a put here, since the resulting cost basis if assigned shares would be lower than the cost basis of the position I've currently got on now. The full position is now a June 21st 82/88 covered strangle (i.e., short put, stock, short call).

Will look to take profit at 50% max.

Metrics:

Buying Power Effect/Break Even/Cost Basis in Shares if Assigned: 80.10

ROC at Max as a Function of Buying Power Effect: 2.37%

ROC at 50% Max as a Function of Buying Power Effect: 1.19%

Delta/Theta: 23.36/2.42

Opening (IRA): SPY September 20th 430 Short Put... for a 4.34 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into S&P 500 ETF, adding at a strike better than what I currently have on.

As with my other broad market, will look to generally take profit at 50% max or -- if assigned -- sell call against at the strike price my short put was at.

Opening (IRA): SPY August 16th 450 Short Put... for a 4.50 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the S&P 500 ETF.

Here, adding a strike better than what I currently have on in the August expiry.

Will generally look to take profit at 50% max.

Opening (IRA): QQQ July 21st 380 Short Put... for a 3.90 credit.

Comments: Starting to tip-toe into Q3 (July/August/September) contracts in broad market (IWM, SPY, QQQ). Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

As usual, will look to sell in shorter duration on weakness, assuming I can get in at strikes better than what I currently have on.

Opening (IRA): QQQ June 21st 395 Short Put... for a 4.09 credit.

Comments: Finally, a bit of weakness ... . Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging in without actually being in stock.

Opening (IRA): SMH June 21st 180 Short Put... for a 2.01 credit.

Comments: High IVR/IV at 75.1/35.1. Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the semiconductor ETF.

I may look to ladder out at intervals if premium remains decent.

Opening (IRA): SMH July 19th 165 Short Put... for a 1.69 credit.

Comments: High IVR/IV at 78.9/34.5. Adding a rung out in July to my SMH position, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the semiconductor ETF.

Generally, will look to take profit on the short put at 50% max.

Opened (IRA): BITO May 17th 24 Short Put... for a 1.74 credit.

Comments: Adding a rung at strikes better than what I currently have on. Will generally look to take profit at 50% max or take assignment of shares should that occur and proceed to sell call against.

Metrics:

Buying Power Effect/Break Even/Cost Basis in Shares (If Assigned): 22.26

Max Profit: 1.74 ($174)

ROC %-age at Max: 7.82%

ROC %-age at 50% Max: 3.91%

Opening (IRA): IWM June 21st 180 Short Put... for a 1.82 credit.

Comments: Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. There is no July contract yet, but June is still paying at <16 delta ... .

Opening (IRA): BITO April 19th 26 Short Put... for a 1.23 credit.

Comments: Adding to my covered call position (See Post Below) on weakness, converting the covered call into a covered strangle (i.e., short put + stock + short call). I went with April, since May appeared to be shit illiquid at where I'd want to pitch my tent.

I'm fine with being assigned additional stock here at the 26 strike, since my cost basis in my shares is currently 27.54, with the cost basis in any shares assigned via the 26 at 24.77, although my preference would be just to take profit on the covered call aspect at 50% max and the short put at 50% max and move on.

Naturally, if I also manage to grab the April dividend, that would be additionally bueno.

As a standalone trade:

Break Even/Buying Power Effect/Cost Basis in Any Assigned Shares: 24.77

Max Profit: 1.23 ($123)

ROC at Max: 4.97%

ROC at 50% Max: 2.48%

Opening (IRA): TQQQ April 19th 52 Short Put... for a 1.54 credit.

Comments: Adding a short put component to my TQQQ covered call (See Post Below) here on weakness.

Metrics:

Break Even/Buying Power Effect/Resulting Cost Basis In Stock: 50.46

Max Profit: 1.53/$153

ROC at Max: 3.03%

ROC at 50% Max: 1.52%

Will generally look to take profit on the covered call component at 50% max and the short put component at 50% max.

Opening (IRA): TLT May 17th 88 Short Put... for a 1.08 credit.

Comments: Laddering out on weakness, targeting the strike paying around 1% of the strike price in credit at or below the cost basis of the shares I've currently got.

Opening (IRA): IWM June 21st 169 Short Put... for a 1.63 credit.

Comments: Laddering out at intervals, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

Will start looking at adding in shorter duration if I can get in at strikes better than what I currently have on.