Closing (IRA): MJ April 16th 18 Short Put... for .09/contract.

In for .63, (See Post Below), out for .09. .54 ($54) profit per contract. Still have May 21st 18s on.

Shortput

Opening (IRA): IWM May 7th 192.5 Short Put... for a 2.53/contract credit.

Notes: My weekly, ~16 delta, 45 days until expiry short put in the broad market exchange-traded fund with the highest implied volatility . This one's only got 38 days left, but it's this or go out to the monthlies (52 days).

Opening (IRA): XBI May 21st 120 Short Put... for a 2.17/contract credit.

Notes: 30-day at >35% at 40.1%. Selling the 16 delta here. 1.84% ROC at max as a function of notional risk. As usual, will take profit on approaching worthless or, if in the money at expiry, take assignment and sell call against.

Opening (IRA): ICLN May 21st 20 Short Put... for a .53/contract credit.

Notes: 30-day implied at 48.8%. ROC 2.72% at max as a function of notional risk.

Opening (IRA): EWZ May 21st 29 Short Put... for a .57/contract credit.

Notes: Just banging through the underlyings at the top of my high IV list. EWZ's 30-day is at 54.07%. ROC at max 2.00% as a function of notional risk.

Opening (IRA): TAN May 21st 70 Short Put... for a 1.93/contract credit.

Notes: High 30-day at 61.5%. Not as liquid as I would like. In any event, 2.84% ROC at max as a function of notional risk.

Opening (IRA): MJ May 21st 18 Short Put... for a .48/contract credit.

Notes: High 30-day at 64.9%. Selling the 15 delta strike here. 2.74% ROC at max as a function of notional risk. Will take profit on approaching worthless or, if in the money, take assignment and sell call against.

Rolling (IRA): SPY September 17th 205 Short Put to the 275... for a 1.93 credit.

Notes: Another continuation of a longer-dated setup I started around the beginning of the year. (See Post Below). With 178 days to go and more than 50% of extrinsic gone, rolling this up to the 275 strike for a 1.93 credit. Total credits collected of 4.12 versus current short put value of 2.88; realized gain: 1.24 ($124).

Rolling (IRA): SPY May 21st 331 Short Put to May 21st 360... for a 1.87 credit.

Notes: Here, a continuation of a longer term play I established at the beginning of the year. (See Post Below). With the 331 at >50% max and >45 days to go, rolling up to the 360 strike (17 delta) for both a realized gain and a credit. Total credits collected of 8.08 versus current short put value of 3.60; total realized gain: 8.08 - 3.60 = 4.48 ($448).

Closing (IRA): EWZ March 31st 30 Short Put... for an .08/contract debit.

Notes: In for .60/contract (See Post Below); out for .08 with 8 days to go. .52 ($52)/contract profit.

Rolling (IRA): SPY April 16th 349 Short Put to April 30th 367.50... for a 2.16 credit.

Notes: Rather than adding more units, another take profit roll. Although there's .88 of extrinsic still left in this, locking in the realized gain via roll out to the April 30th 16 delta strike at the 367.50 for a 2.17 credit. Total credits collected of 9.07 versus current option value of 3.05 -- i.e., I've locked in 9.07 - 3.05 or 6.01 ($602) or profit so far.

Rolling (IRA): IWM April 1st 200 Short Put to April 30th 207.5... for a 2.28 credit.

Notes: With only .40 of extrinsic left and 16 days to go, rolling this out to around the 16 delta strike in the contract nearest 45 days until expiry for a realized gain of 2.40 ($240) (See Post Below) and a 2.29 credit. Total credits collected of 4.57.

OPENING (IRA): LIT MARCH 19TH 58 SHORT PUT... for a 1.16/contract credit.

Notes: 30-day at 58.6% and expiry-specific at 57.2%. Unfortunately, not the most liquid thing in the world, so expect to do some price discovery or be patient for a fill.

Opening (IRA): AAPL April 16th 107.5 Short Put... for a 1.99 credit.

Notes: With a 30-day implied of 42.8%, expiry-specific at 41.8%, and earnings in the rear view, adding some Dow component high implied underlyings to my wheelhouse. I already have some BA in my portfolio, which has the highest 30-day of Dow components that have already announced earnings, and pretty much have all the high implied exchange-traded-fund bases covered. ROC 1.89% at max as a function of notional risk. I went with the 19-delta 107.5 in lieu of the 105 (15 delta) or the nonstandard 106.25. A little more aggressive than I usually go, but wanted to get at least 1.5% ROC at max out of it.

Rolling (IRA): SPY July 16th 250 to July 16th 306 Short Put... for a 1.89 credit.

Notes: As with my June short put roll, a continuation of a longer-dated setup. Rolling up at 50% max to lock in the realized gain to the strike paying at least 1%. Total credits collected of 4.44.

Rolling (IRA): SPY June 18th 283 Short Put to the 329 Short Put.. for a 1.92 credit.

Notes: Here, a continuation of a longer-dated strategy I started at the beginning of the year, (See Post Below). With the 283 reaching 50% max, I'm rolling it up to the strike paying at least 1% for both a realized gain and a credit. Total credits collected of 5.87; ROC now 1.82% at max.

FXI Short Put (Wheel)Chinese large caps have tumbled over the last couple of weeks and seem to have found support on the rising trendline around $47. The FXI also has a weighted PE ratio of 12.64 which is less than half the SPY's 27. In simple words, you are getting a greater value per dollar in FXI than the SPY.

Trade Idea:

Cash-Secured Put: 45 Strike expiring 4/16 for $0.65 Credit. 75% PoP and $650 BPE for a 10% Max ROC.

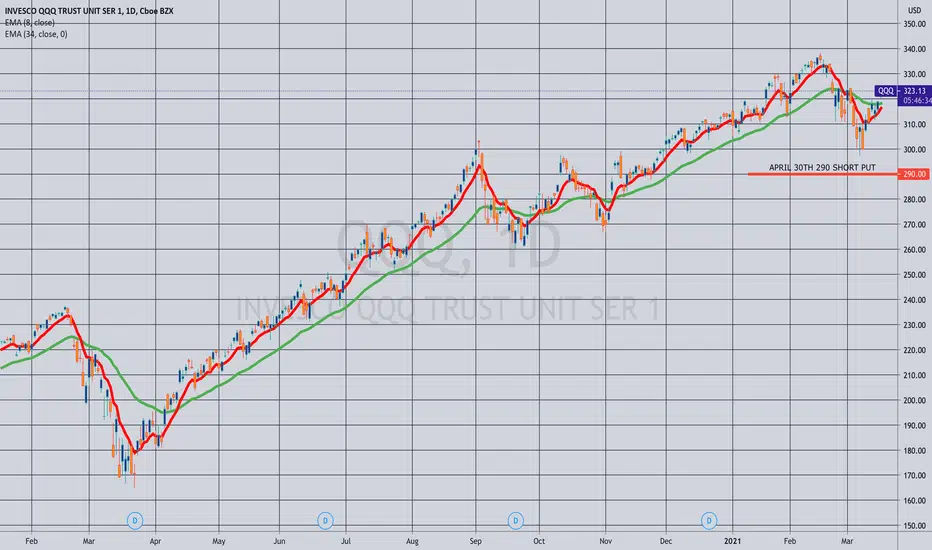

Opening (IRA): QQQ April 30th 290 Short Put... for a 3.51 credit.

Notes: My weekly, 16 delta strike short put in broad market in the contract nearest 45 days until expiry. IWM implied is actually slightly higher here, but the Q's are weaker.

OPENING (IRA): XBI MARCH 19TH 135 SHORT PUT... for a 2.11/contract credit.

Notes: With 30-day at 37.5% and expiry-specific at 38.3%, selling a 16 delta in the March cycle (52 days). 1.59% ROC at max as a function of notional risk.

EWZ Short PutEWZ is trading near its rising trendline support. Assuming that it could break below it, going with a neutral to bullish strat like a short put or a put credit spread would work to your favor even if the ETF breaks below, or trades flat.

Trade Idea:

Short Put: 28 Strike expiring 4/16 for $0.72 Credit. 72.5% Prob. OTM. and only $285 BP used for a max 25% ROC.

SNAP Wheel Strategy Short PutSnapchat is down 25% from its highs, and while it has bounced up a little bit from the highs, it still remains oversold. Now might be the right time to sell a put into weakness and collect premium.

Trade Idea:

Medium Risk: The 44 Put expiring 4/16 for $1 credit . It has a 81.5% Prob. OTM and if you do get assigned, your cost-basis per share will be $43 and it is a good place to own as you will be in the middle of the volume profile for the last 6 months meaning that you won't be buying at the top but at the same time the bottom.

Aggressive: The 47 Put expiring 4/16 for $1.5 credit . It is right below support and has a higher 75% Prob. OTM. While you have a higher chance of getting assigned with this one, considering the support level that hasn't been breached for months, you still have high odds of collecting the premium and not get assigned. Even if you do get assigned, your cost-basis per share will be $45.5.

For both of these trade ideas, if you believe in Snapchat's fundamentals, which are pretty modest, you can hold on to the stock and sell covered calls (70-80% OTM) and collect premium until you get assigned. Once you do get assigned, you can come back to selling cash-secured puts again.

PLTR at support and has high bullish sentimentShort Put : 18-strike expiring 4/16 for $0.69. Short 16 delta and has a 75% POP. It is also very cheap at $400 BPE for a solid 17.5% ROC.

This is a neutral to bullish play with a modest room to the downside and still profit from the trade. This will give you the highest possibility to win and the best part is that you don't need to predict the direction as long as it stays above $18. Close this at 50%-75% profit, 150%-200% loss or 20DTE, whichever comes first.

SFIX Short PutSFIX gap down following disappointing earnings and not-so-bright forecast for the next quarter. Same thing happened with INTC twice over the last year and we saw how it was just an over-reactionary sell-off as it quickly rallied up after a continuation sell-off for a week or so. SFIX's fundamentals are solid assuming that shipping problems don't disrupt the business too much. It will most likely close the gap at around 42. It might also pull down a little bit more, but hopefully it won't go below $34. It gives us a decent range from $34-$42 to accumulate the stock. There is also heavy support around the $41.5 area with both a supply/demand zone along with the 200-day SMA.

Trade Ideas:

Shares: Accumulate between $34-$42 . SL below that if it does continue to fall further, which is unlikely but make sure the SL isn't too close to the bottom support. We should see a push up to $53.75, $65 and $72.5+.

Short Put: Medium Risk: 35 Strike for $0.85-$1 Cr. Aggressive: 40 Strike for $1.65 Cr. This can help you reduce your cost basis by at least $0.85 to $1.65 per share if you do get assigned. If you don't get assigned or the stock never dips that low, you get to keep the premium. It also only requires $385/$425 Buying Power which should yield a nice 22%/38% max ROC.

In either case, assuming you have at least 1 lot of shares, you can always sell 70%-80% OTM covered calls for more passive income while your stock appreciates.