SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2955.8 where it could potentially bounce further to 3027.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPXU

SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2955.8 where it could potentially bounce further to 3027.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2955.8 where it could potentially bounce further to 3027.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2955.8 where it could potentially bounce further to 3027.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX potential reversal!

SPX expected to rise up to 1st resistance at 2955.8 where it could potentially react off and drop down to 2841.3.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX potential reversal!

SPX expected to rise up to 1st resistance at 2955.8 where it could potentially react off and drop down to 2841.3.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX potential reversal!

SPX expected to rise up to 1st resistance at 2955.8 where it could potentially react off and drop down to 1st support at 2847.2.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX bounced from support, potential for a further rise!

SPX bounced off 2841.3 where it could potentially rise further to 2955.8.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPXU LONG SETUPSPXU price possibly changed the trend and price breakout daily down trend line. hope will go long and wait for 200 ma crossover for entry confirmation. I also watching this one .

SPX bounced from support, potential for a further rise!

SPX bounced off 2841.3 where it could potentially rise further to 2955.8.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX bounced from support, potential for a further rise!

SPX bounced off 2841.3 where it could potentially rise further to 2955.8.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

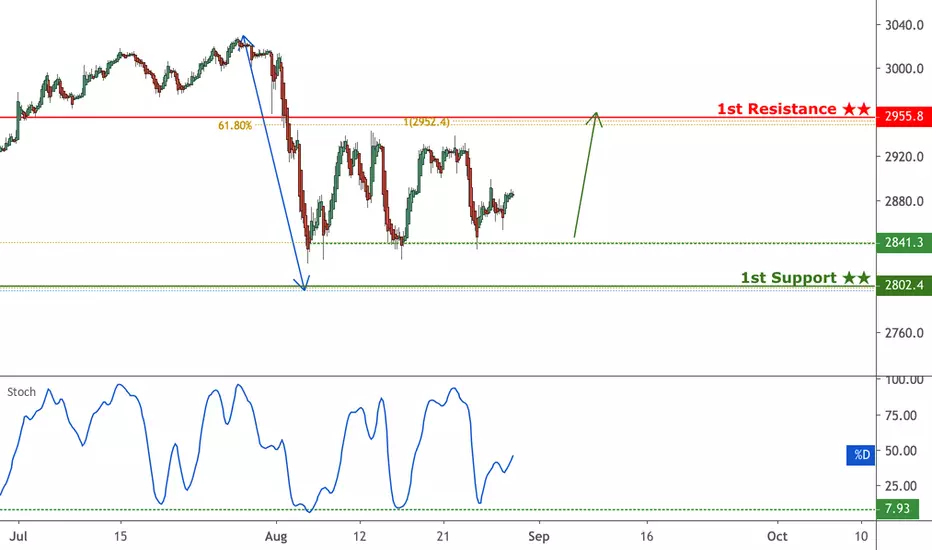

SPX approaching resistance, look out for potential reversal!

SPX is approaching its resistance at 2955.8 where it is could reverse down to its support at 2802.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX reversed from resistance, potential drop!

SPX reversed off 2955.8 where it could potentially drop further to 2802.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX potential reversal!

SPX expected to rise up to 1st resistance at 2955.8 where it could potentially react off and drop down to 1st support at 2802.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX potential for a further rise!

SPX bounced off at 2841.3 where it could potentially rise further to 2955.8.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2900.6 where it could potentially bounce further to 2964.0.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX to climb from upside confirmation, potential bounce!

SPX to climb from its upside confirmation at 2900.6 where it could potentially bounce further to 2964.0.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

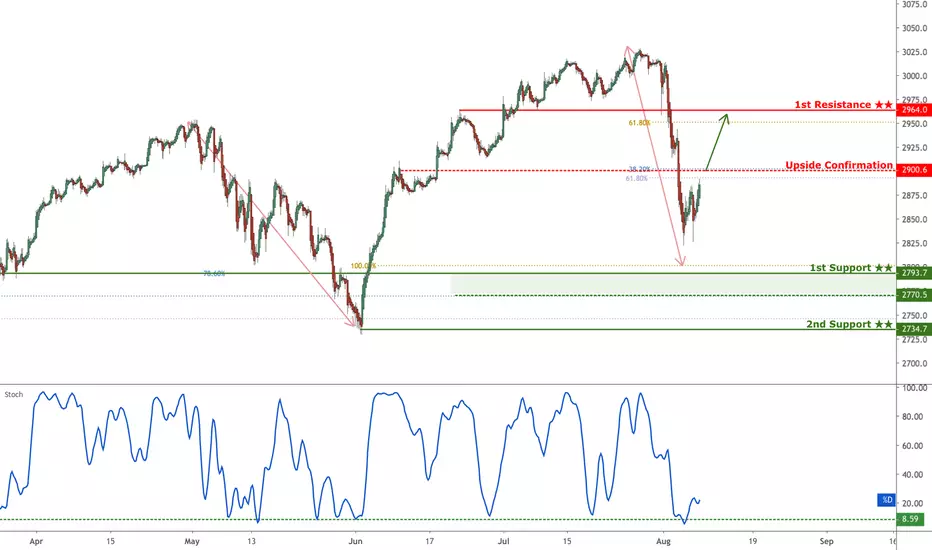

SPX approaching support, potential for a bounce!

SPX is expected to drop to 1st support at 2793.7 where it could potentially react off and up to 1st resistance at 2910.8..

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX bounced from support, potential for a further rise!

SPX bounced off its support at 2907.8 where it could potentially rise further to 3030.4.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

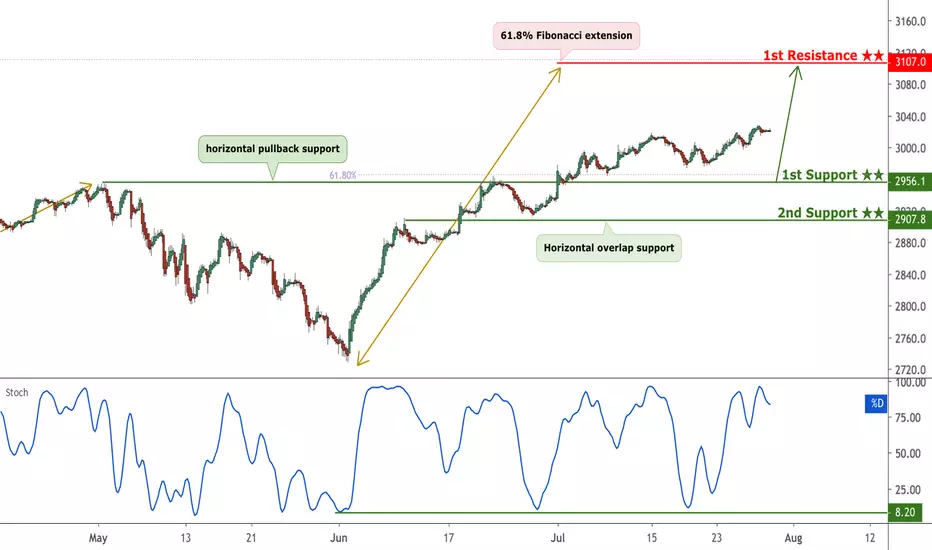

SPX bounced from support, potential for a further rise!

SPX bounced off its support at 2956.1 where it could potentially rise further to 3107.0.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX approaching support, potential for a bounce!

SPX is expected to drop to 1st support at 2956.1 where it could potentially react off and up to 1st resistance at 3107.0.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPX approaching support, potential for a bounce!

SPX is expected to approach first support at 2956.1 where it could potentially react off and up to 1st resistance at 3107.0.

Trading CFDs on margin carries high risk.

Losses can exceed the initial investment so please ensure you fully

understand the risks.

SPXU - Crash courseOutline of SPXU versus the S&P500 as a means to shorting the US equities market.

Outline

------------

I fully believe that there will be a serious correction if not outright crash in the near future as many companies are trading with significantly inflated values relatives to their fundamentals and of course the general state of the world economy.

I have been examining and experimenting with various different ways to short the market since 2015/16 when I made my last serious speculative attacks upon equities. Being a UK citizen I am still able to use OTC derivatives such as CFD's and these have been my traditional angle of attack as they permit me to trade on-margin using various configurations of leverage without the hassle of having to offload assets onto an unwilling market at a later date.

As such I recently discovered SPXU and one of the things which struck me about it was it's raw potential for profit when combined with CFD derivatives. Because derivatives are generally based around contracts with brokers which can be closed at specific pre-set times or even arbitrarily at point of maximum benefit, then of course this overrides the problem of trying to sell an asset which will only ever decrease in value after a ginormous rally during a serious crash.

A lot of the other downsides of SPXU are also minimised by holding derivatives based on the SPXU index rather than any de facto form of the ETF.

SPXU vs. S&P500 Price Action

---------------------------------------

Now one of the reasons I am attracted to SPXU is because if you look carefully at it then it moves in a non-linear exponential fashion.

For instance compare the curve of the S&P500 to the curve of SPXU in the chart above.

The S&P is moving in a linear fashion, while SPXY, by contrast is moving in an exponential fashion.

(I tried to post diagrams for your benefit but trading view is a pile of crap and wouldn't let me)

You'll see immediately that SPXU, while it does indeed derive its value from the underlying swaps based on the S&P500, moves in a very different way. The S&P500 is effectively linear, while SPXU is exponential.

Let me explain why this occurs.

SPXU and S&P500 Movement

-------------------------------------

SPXU is leveraged x3 to return an inverse of the daily movement of the S&P500 and is rebalanced daily to reflect this.

For instance if the S&P500 moves upwards by 1% on a day, SPXU will move down by 3%. And vice-versa.

In practice what happens over a very long timeframe (e.g. the current bull market) is that the actual raw dollar values on SPXU get smaller as the native S&P500 appreciates. Yet the SPXU has to keep returning 3x the inverse of the S&P's daily change.

Per se, as the SPXU's value shrinks, it's rate of decline shrings in raw dollar form.

As the SPXU devalues, the raw dollar figures returned by this equation get smaller as a result, the losses shrink in raw dollar value vs. the S&P500.

Let me elaborate further with some examples using some rough figures..

Examples Pt. 1

---------------------

- At the moment a 1% move on the S&P500 (lets assume a $3k price point) is worth $30.

- Thus, on the SPXU after triple-leveraging, a 3% move at the $26 price point is equivalent to just $0.78

- We can go further than this and calculate out, for our price point, what a $1 move on the S&P500 is worth on the SPXU in raw dollar value.

- Thus, $1 is 0.033% of the S&P500's $3000 price point.

- Comparing this to SPXU, then this, after the ETF's triple-leveraging comes into play, gives us a raw figure of 0.099% which the SPXU will return in relation to it's present value - it's about $0.02.

- So, for roughly the current point in time, every $1 on the S&P500 moves the SPXU by about 2 cents.

What's the benefit from this?

------------------------------------------

We have to look to a different point in time to see the benefits.

Back in 2009 when equity markets were on their knees, the SPXU and the S&P500 had a very different relationship.

The S&P at this point in time was at around $900 and the SPXU, by contrast was at over $4000.

Rounding down, the price action here was *very* different. Here are some further examples.

Examples Pt. 2

--------------------------

- A 1% move on the S&P at the $900 price point was worth just $9.

- After triple-leveraging then the SPXU was returning $120 per 1% move on the S&P500.

As such, the way the SPXU leveraged S&P500 moves in raw dollar values was radically different because of the sheer difference in valuations.

- $1 on the S&P500 at this price-point represented 0.1111111% of it's value

- Thus, moving the SPXU by about $13 USD after the ETF's triple-leveraging comes into play.

Summary

---------------

We can divide the price action of SPXU into two zones versus the S&P500.

- A "shallow zone" where your long position on SPXU will return under $1 per $1 of movement on the S&P500 (ATH to $1800 on the S&P500)

- A "deep zone" where your long position on SPXU will return more than $1 per $1 of price movement on the S&P500 ($1800 to $0 on the S&P500).

Practical Application & Usefulness Of This

------------------------------------------------------

This is useful for 3 main reasons:

A: Your downside is limited by the factor of ever shrinking loss ratios. The more raw $ value the SPXU loses, the less it actually loses in the future. You lose about 2cents per dollar of upside on the S&P500 at present. Presuming that, worst case scenario of another 30% upside on the S&P500 is possible, then this would translate to a max possible loss of $200 excluding trading fees. I consider this an acceptable amount of risk given the profit potential of a position on this ETF.

B: Your upside has an ever increasing gains ratio similar to a leverage gradient applied to it meaning that once you pass the equilibrium point of about $1800 USD on the S&P500 / $250 on the SPXU (rough figures for where the markets will have to sit for $1 on the S&P500 to be equivalent to $1 on SPXU) then for every $1 lost on the S&P500. SPXU will return MORE than $1.

Again, by way of example, $1 on the S&P500 in 2009 was moving the SPXU by about $30.

C: THE MAIN REASON.... why this is useful, is because the factor of ever-decreasing losses as the S&P500 gains ground will help defend you from losses.... and of course should the S&P500 ever crash to below $1800 you will find yourself in the position of holding something which will move in a very similar fashion to an extremely highly leveraged short against the S&P500 but without having to bear the upside risks associating with consolidating such a position at entry.

D: THE ULTIMATE REASON... why I think going long on SPXU has a lot of potential is because the sheer profit potential in it's upside if we see any sort of equities rout which takes the S&P500 to the equilibrium point. A $200 position on SPXU during the 2007 crisis could easily have made hundreds of thousands of dollars worth of profit.

In short (pun intended) my theory is that playing SPXU against the S&P500 via an instrument with reasonable trading fees will offer you a more defensive entry, and a potentially more profitable exit.

Disclaimer

---------------

I should point out that the SPXU swap fund is not designed to be long-held in it's de facto form and I trade it using CFD derivatives. There's lots of slippage and all sorts of issues because the fund is rebalanced daily. Bottom line there are lots of issues which you will need to factor into your trade however I considered them acceptable risks and hiccups versus the advantages outlined.