BARK to List on NYSE Through Merger with STICBARK, A Leading Brand for Dogs, to List on NYSE Through Merger with Northern Star Acquisition Corp.

BARK serves over 1 million dogs monthly through BarkBox and Super Chewer subscriptions and broad retail distribution of its comprehensive suite of best-in-class, proprietary products

projected revenues of approximately $365 million and gross margins of approximately 60% for fiscal year ending March 31, 2021, 179% YoY increase in revenue from new product lines in first half of FY2021, and net revenue CAGR FY2020-FY2023 of over 40%

Transaction values BARK at an enterprise value of approximately $1.6 billion and is expected to provide up to $454 million of gross cash proceeds to invest in the acceleration of new and existing product lines as well as international expansion

Top-tier institutional investors, including Fidelity Management & Research Company LLC, Senator Investment Group, the Federated Hermes Kaufmann Funds, and affiliates of the Santo Domingo Group, among others, are supporting the transaction with an upsized $200 million fully-committed PIPE

The Northern Star and BARK Boards of Directors have unanimously approved the proposed merger and the related transactions, which are expected to be completed early in the second quarter of 2021,

www.prnewswire.com

Stockanalysis

500.com Limited Announces Private Placement500.com Limited Announces Private Placement and Appointment of New Officers

500.com Limited (NYSE: WBAI) ("500.com" or the "Company"), an online sports lottery service provider in China, today announced that it has entered into a definitive share subscription agreement (the "Agreement") with Good Luck Information Technology Co., Limited ("Good Luck Information"), a company incorporated in Hong Kong, for the issuance and sale of newly issued Class A ordinary shares of the Company ("Class A Shares").

Pursuant to the Agreement, Good Luck Information will purchase 85,572,963 newly issued Class A Shares for a total purchase price of approximately US$23 million, to be settled in U.S. dollars or in crypto-currencies, including Bitcoin (BHC), to be determined chosen by the Company within one month of the date of the Agreement. Good Luck Information shall make full payment of the purchase price in currencies determined by the Company within one month of the Company's determination. The per share purchase price of US$0.269 is the closing trading price of the Company's ADSs on December 18, 2020, the last trading day immediately preceding the date of the purchase agreement. as adjusted by a 1-to-10 ADS to ordinary shares ratio.

Good Luck Information has agreed to subject all the shares it or its affiliate will acquire in the transaction to a contractual lock-up restriction for 180 days after the closing. The closing is expected to take place on or before February 20, 2021, upon satisfaction of customary closing conditions.

Good luck Information is controlled by Mr. Man San Vincent Law, a founder of the Company, who currently holds less than 5% of the Company's outstanding share capital. Upon closing, Good Luck Information will hold 16.6% of the Company's issued and outstanding ordinary shares.

finance.yahoo.com

Buy Some BMW Stock here ....XETR:BMW

BMW is on an upward channel on a daily basis, and formed flag pattern

Also it retested the broken channel and is suitable to buy some at the demand zone

Nvidia long position ongoing. Hello traders.

Just wanted to share an ongoing Nvidia trade with opportunity to still enter before market reopen.

Working the H1 time frame here on this stock using a follow trend script.

Nvidia is a great example of how the script I'm using can be used on stocks if you operate on lower time frames to catch the ups and downs needed for working those lower time frames.

On this stock I'm using the script to work to a stop loss and take profit target.

Back test data is show at the bottom of screen on three years worth of data.

For anymore information please drop me a message.

A look at DataDog stock growth.Hello Traders

I've covered the potential of the strategy script I am using on stocks like Tesla and Apple and how the script presented early entry opportunities.

Working the W1 chart on those two stocks mentioned buy signals presented on both at stages in 2019 and have kicked on to some unreal gains.

But now its time to focus on some potential growth stocks. Here I talk about Datadog.

This stock year to date has grown 164% and the strategy I use presented a buy signal back in June which is when I entered this one in to my portfolio. Since then it has gone on to gain 15%. Still loads of potential growth and when working this time frame its all about long term growth.

For any more information on the strategy I utilize please drop me a message.

If only I had this script years ago! Apple review. Afternoon traders

I just want to demonstrate the possibilities of the script I'm using on trading stocks.

I've used Tesla as an example before on the potential of using this strategy for long term investments.

Today I will show Apple quickly as an example of when the strategy presented a buy signal on the 1W chart all the way back in August 2019 and has since gone on to gain 144% in value. A stop loss parameter is set and now its a case of following the trend until a next signal presents.

No one had this script at the time but now we do I'll go over some potential long term growth stocks over the course of the next few days on my profile. I'll be using the 1W chart to present possible ideas of investing in stocks with long term growth potential.

For any information on the script I am using please drop me a message.

Bft spac company and Paysafe Announce MergerFoley Trasimene Acquisition Corp. II and Paysafe, A Leading Global Payments Provider Focused on Digital Commerce and iGaming, Announce Merger

Transaction values Paysafe at pro-forma enterprise value of $9 billion upon consummation of transaction ~

~ Transaction Includes a $2.0 Billion Fully Committed PIPE from Investors including a $500 million investment from Fidelity National Title Insurance Co., Chicago Title Insurance Co., Commonwealth Land Title Insurance Co. and Fidelity & Guaranty Life Insurance Co., and a $350 million investment from Cannae Holdings, Inc. Other institutional investors include Third Point LLC, Suvretta Capital Management, Hedosophia and the Federated Hermes Kaufmann Funds ~

- Upon closing of the transaction, the newly combined company (the "Company") will operate as Paysafe and plans to list on the New York Stock Exchange (NYSE) under the symbol PSFE.

- The balance of the consideration will consist of equity in the combined company. Existing Paysafe equity holders, including Blackstone, CVC and management, will remain the largest investors in the Company.

- The transaction is expected to close in the first half of 2021.

www.businesswire.com stock

Docu Free Package Docu will either crawl up before dropping or even drop now. Looks like the letter is most likely. Remember to buy low and sell high.

BlackBerry (BB) Stock Soars on AWS Deal for Smart Vehicle DataAWS and BlackBerry Join Forces to Accelerate Innovation with New Intelligent Vehicle Data Platform

• BlackBerry IVY will help automakers create personalized driver and passenger experiences and improve operations of cloud-connected vehicles with new BlackBerry QNX and AWS technology

• AWS, AMZN, and BlackBerry Limited (NYSE: BB, TSX: BB), a worldwide leader in intelligent security software and services, announced a multi-year, global agreement to develop and market BlackBerry's Intelligent Vehicle Data Platform, IVY.

• BlackBerry IVY is a scalable, cloud-connected software platform that will allow automakers to provide a consistent and secure way to read vehicle sensor data, normalize it, and create actionable insights from that data both locally in the vehicle and in the cloud.

• Automakers can use this information to create responsive in-vehicle services that enhance driver and passenger experiences.

• BlackBerry IVY will solve data challenges by applying machine learning to that data to generate predictive insights and inferences, making it possible for automakers to offer in-vehicle experiences that are highly personalized and able to take action based on those insights.

• Automakers will gain greater visibility into vehicle data, control over who can access it, and edge computing capabilities to optimize how quickly and efficiently the data is processed.

• With BlackBerry IVY’s integrated capabilities, automakers will be able to deliver new features, functionality, and performance to customers over the lifetime of their cloud-connected vehicles, as well as unlock new revenue streams and business models built on vehicle data.

• BlackBerry IVY could leverage vehicle data to recognize driver behavior and hazardous conditions such as icy roads or heavy traffic and then recommend that a driver enable relevant vehicle safety features such as traction control, lane-keeping assist, or adaptive cruise control.

• BlackBerry IVY will enable automakers to compress the timeline to build, deploy, and monetize new in-vehicle applications and connected services across multiple vehicle brands and models.

• BlackBerry IVY will make it easier for automakers to collaborate with a wider pool of developers to accelerate creation of new offerings that deliver improved vehicle performance, reduced costs for maintenance and repairs, and added convenience.

finance.yahoo.com

CRM Buy Set UpIts dropping fast now. but I am seeing a reversal very soon base on my analysis. A good time to go LONG.

SLP - daily point with potencial >15%Simulations Plus, Inc. provides modeling and simulation software and consulting services supporting drug discovery, development research, and regulatory submissions.

The financial side of the company is in good shape, according to my rating 4+ .

Technically, it is an excellent daily point in the demand zone after a false breakdown.

The potential is bombing - 15% and more.

I take now with a stop of 50 and at 48.50, if they fall there and give confirmation.

Operations in financial markets can bring both large potential profits and are associated with potential risks associated, among other things, with the effect of leverage and high volatility of instruments used in trading in financial markets.

The provided forecast is a subjective analytical assessment of the situation in the financial market and in no way is it a recommendation for opening deals, investing and developing your own trading strategy.

Roku growth over last 18 months!Evening traders

Ive been using a follow trend based strategy for the last six months mainly for Forex trading.

This strategy script works with Forex pairs, indices, stocks and crypto.

It's not until recently I've discovered the potential for using this script on stocks for potentially building long term stock portfolios via following the trend based script. Another great example to my earlier Tesla idea and review is this Roku stock growth via following the the stock on the one week time frame.

As you will see the strategy presented a 'buy' signal in March 2019 and Roku stock has since gone on to grow by 300%

For any further information on the strategy I'm using please feel free to message me.

SWKS - strong company near good supportSkyworks Solutions, Inc. is engaged in the design, development and manufacture of proprietary semiconductor products.

Fundamental rating - 4+,

strong financial company, stable profit, revenue growth, good margins, very little debt, and assets are many times greater than liabilities.

Technically - currently in the downtrend on the h1, but good daily support zone below. I will watch the reaction at the 133.85-134.50 area. If they don't go further or if there is a bullish initiative, I will take it. If they breakdown his area , then I will consider 131.27 for long. Below 131 - cancel the scenario.

The targets are 139.65 (+4%) and 148.39 (+10%). Investment for 1-3 months.

When there is a signal to enter, I will additionally write.

Operations in financial markets can bring both large potential profits and are associated with potential risks associated, among other things, with the effect of leverage and high volatility of instruments used in trading in financial markets.

The provided forecast is a subjective analytical assessment of the situation in the financial market and in no way is it a recommendation for opening deals, investing and developing your own trading strategy.

Trivago CEO: 'We do expect a strong demand for travelTrivago CEO: 'We do expect a strong demand for travel because it will be a long winter'

finance.yahoo.com

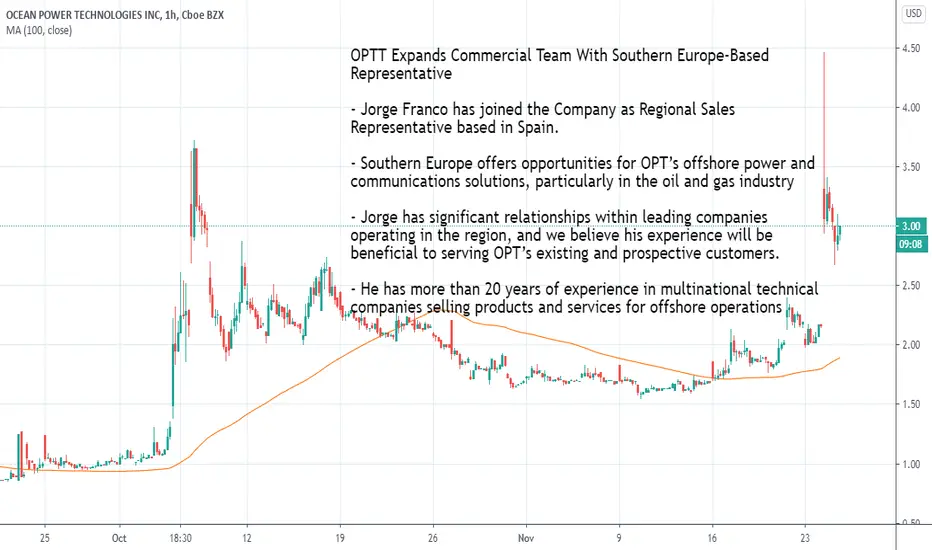

OPTT Expands Commercial Team With Southern Europe-Based RepOPTT Expands Commercial Team With Southern Europe-Based Representative

- Jorge Franco has joined the Company as Regional Sales Representative based in Spain.

- Southern Europe offers opportunities for OPT’s offshore power and communications solutions, particularly in the oil and gas industry

- Jorge has significant relationships within leading companies operating in the region, and we believe his experience will be beneficial to serving OPT’s existing and prospective customers.

- He has more than 20 years of experience in multinational technical companies selling products and services for offshore operations

finance.yahoo.com

Luminar has struck a deal with Mobileye, an Intel company!Luminar Technologies, Inc. (“Luminar”), the global leader in automotive lidar hardware and software technology, which is currently in the process of becoming a public company through its expected merger with Gores Metropoulos, Inc. (Nasdaq: GMHI, GMHIU, GMHIW), a special purpose acquisition company, has struck a deal with Mobileye, an Intel company, to supply Luminar lidar for the company’s Autonomous Vehicle (AV) Series solution in its next phase of driverless car development and testing.

As part of the agreement, Mobileye will collaborate with Luminar to use its lidar for the first generation of its level 4 Mobility-as-a-Service (MaaS) pilot and driverless fleet in key markets around the world

Luminar’s technology will be used to enable Mobileye’s TRUE REDUNDANCY™ solution which is uniquely comprised of multiple self-contained sensor systems to enable uncompromised safety and validation for level 4 driving. By processing completely independent streams of data from 360-surround view cameras, lidar, and radar, the solution ensures significantly greater perception accuracy and eliminates the impact of disruptions to an individual sensor.

Austin Russell, Founder and CEO of Luminar Technologies said that“Mobileye disrupted the auto industry to become the undisputed king of ADAS, and with the right partner is uniquely positioned to enable autonomy at an unprecedented scale.” “After collaborating with Mobileye for over a year, we’re excited to formalize this deal and work towards a shared vision of making autonomy safe and ubiquitous.”

Luminar has secured a total of 50 commercial partners across passenger vehicle, trucking, and robo-taxi verticals, representing approximately 75% of major players in the targeted customer ecosystem. Luminar’s accelerating commercial traction has resulted in opportunities to convert 12 of its OEM programs and engagements from development stage into production.

Key 2020 achievements across its three key verticals include:

Passenger Vehicle – Luminar has secured the industry’s first series production deal for consumer vehicles starting in 2022. Luminar remains on schedule with the first Iris sensors now running live on vehicles. Luminar is partnered with seven of the top 10 largest automakers at various development stages, with timelines to series production landing between 2022-2025.

Trucking – Luminar is partnered with the largest global truck OEM to commercialize Level 4 autonomous trucks for long-haul highway use cases; Luminar is now also powering all other major autonomous trucking programs globally.

Mobility-as-a-service – Luminar is now working with a number of major next-generation autonomous robo-taxi programs, with particular focus on those closer to series production, including Mobileye’s internal Mobility-as-a-Service program.

www.businesswire.com

Good opportunity for long Swing Good swing opportunity rise in Adobe stock. The price is below its Fair value by around 52$. It will be nice for swing trade from its position right now until it hit its fair value.

PALANTIR stock $20 Long-Term Price Target 🔥🚀News are good for Palantir (Q3).

This chart show a possible scenario for the stock next week.

$20 Long-Term Price Target (and more in the coming months).

This is not precise of course, but the trend would be this (growth).

Your comments are welcome.

VISA HUGE BUY OPPORTUNITY

#invest #investment #money #investing #bitcoin #business #realestate #forex #investor #entrepreneur #trading #cryptocurrency #success #wealth #finance #crypto #trader #motivation #stocks #forextrader #stockmarket #financialfreedom #realtor #blockchain #forextrading #binaryoptions #bitcoinmining #btc #luxury #bhfyp #stocks #stockmarket #investing #trading #money #forex #finance #investment #business #investor #bitcoin #invest #wallstreet #entrepreneur #trader #wealth #cryptocurrency #daytrader #success #financialfreedom #daytrading #motivation #forextrader #forextrading #crypto #stock #millionaire #forexsignals #passiveincome #bhfyp #rich #blockchain #cash #technicalanalysis #nasdaq #entrepreneurship #profit #forexlifestyle #market #investments #swingtrading #fx #sharemarket #stocktrading #binaryoptions #realestate #options #nifty #makemoney #optionstrading #hustle #gold #lifestyle #dividends #luxury #shares #btc #ethereum #warrenbuffet #markets #stockstobuy2020

Leave a like and comment giving us your opinion about this coca cola stock analysis

AMC LONG SET UP (AMC to reopen eight theaters in California) TITLE : BUY AMC

ASSETS : STOCK

SYMBOL : AMC

PLATFORM: WeBull or Robinhood

ORDER TYPE : (EP1) Market (1/2) position size (partial low lot entry)

(EP2) BUY LIMIT ORDER (2/2) (Now enter rest of position)

TF : Week

ENTRY PRICE 1: $2.68

ENTRY PRICE 2: $2.08

STOP LOSS : $1.18 (15 PIPs)

TAKE PROFIT 1- $3.86

TAKE PROFIT 2- $4.86

TAKE PROFIT 3 $5.86

STATUS : ACTIVE

AMC to reopen eight theaters in California

Oct 27 (Reuters) - AMC Entertainment Holdings Inc AMC said on Tuesday it plans to reopen eight theaters in California, one of its key markets, providing some much needed hope to an industry that has been hammered by the COVID-19 pandemic.

AMC said that it would reopen theaters in Northern California, including San Francisco and the greater Bay Area.

The world's largest theater chain expects to have about 540 of its 600-theatre circuit open by the end of this month.

While big theater chains such as AMC Entertainment and Cineworld Group CINE have reopened many locations, audiences have been thin due to virus fears and delays in major releases by studios.

Small and mid-sized theater companies have said they may not survive the impact of the pandemic.

Shares of AMC, which have fallen 62% this year, were up 4.3% in premarket trading.

AMC to Reopen Seven Theater Locations in Northern California

AMC Entertainment (AMC) said Tuesday it will resume operations at seven theaters in Northern California on Oct. 30, and open a new location in the area as well.

As a result of the openings, AMC said it expects to have approximately 540 of its 600-theatre circuit open by the end of October.

AMC Entertainment to Reopen Dozen Locations in New York on Friday; Shares Rise 6% Pre-Bell

AMC Entertainment Holdings (AMC) reported that approximately 12 AMC locations throughout New York state, except for New York City, will resume operations Friday.

AMC said it expects to have approximately 530 of its 600-theatre circuit open and serving guests by the end of October. Beginning Friday, AMC will open in 44 of the 45 states where it has theaters.

"We continue to work closely with state and local authorities about the reopening of New York City, which we now hope with increasing confidence is not far away," said CEO Adam Aron.

Shares of AMC are up more than 6% in premarket trading.

The company said it is in discussions with local authorities about resuming operations in its remaining theaters.

AMC Entertainment Holdings Offers Private Screenings

AMC Entertainment Holdings (AMC) is offering private screenings for up to 20 people, with auditorium available at a starting price of $99 plus tax, according to a post on the company's website.

NXE Setup 1 Buy Order @1.82 This is a nice Setup 1 long setup

Buy order above the current AIMS Box High:

Stop Loss Risk Management: 1.70

Take Profit level 1: Highs to the left and Round Figure $2.00 (close half here let the rest run)