Innotek: the company stay optimistic abt its long-term prospectsInnoTek

InnoTek, trading at \$0.43, has been navigating a transformative journey since selling its core disk-drive components business over 15 years ago. The precision components manufacturer pivoted to grow its small stamping business and has since diversified into promising sectors such as electric vehicles (EVs) and graphics processing unit (GPU) servers, which are riding the artificial intelligence (AI) wave. These efforts are now bearing fruit, with revenue for the first half of 2024 rising 30.9% year-on-year to S\$121.6 million.

The diversification strategy has been driven by growth in GPU server-related projects for AI applications, which now account for about 27% of InnoTek’s revenue, up from 14% a year earlier. The automotive segment remains its largest contributor, accounting for 33% of revenue, bolstered by the strong EV market in China. Other segments, including office automation, TVs and displays, also contribute significantly to its topline.

However, profitability has taken a hit, with net profit for H1 2024 slipping 8.3% to S\$3.2 million. This was attributed to extraordinary costs linked to shifting business strategies and geopolitical tensions driving the “China+1” manufacturing strategy. InnoTek has been strategically expanding its footprint in ASEAN countries, with facilities in Thailand and Vietnam, and plans to further invest in Malaysia due to its favorable infrastructure and skilled workforce.

Despite short-term challenges, the company remains optimistic about its long-term prospects. With a market capitalization of \$100 million, InnoTek trades at 0.6x its book value of 76 cents. Its strong balance sheet, featuring net cash of \$56 million, supports a sustainable dividend payout of 2 cents per share, translating to a yield of 4.6%. Analysts recommend an “Accumulate on Weakness” strategy, citing the company’s strong positioning for longer-term growth.

Stocksignals

NVDA Technical analysis and my view on the stockIn my opinion, NVDA is still robust and is establishing a low on the 200 MA.In spite of the current dispute with Deepseek, NVDA remains a robust stock and business.

Currect support $120 + 200 EMA.

PFE looking higher with +10% profit potential PFE has finished strong correction and is finding a bottom near $25.

I anticipate that within the next three months, the stock, which I purchased at $26.5, will reach $30.

Blue line entry

Red stop

Green lines are target.

Looking for a breakup descending trend line & price action aboveLooking for a breakup descending trend line and consistent price action above. If so, a Long position will be opened. Later on, the position parameteres will be updated.

Supply and Demand Trading Made Simple With Astrazeneca StockIn the ever-evolving world of stock trading, where news headlines can shift markets in a heartbeat, savvy investors often turn to the age-old principles of supply and demand to find clarity. Enter AstraZeneca stock (NASDAQ: AZN) — a biopharmaceutical titan that has played a pivotal role in global health. It is a beacon for traders seeking to unlock the secrets hidden within its price movements.

There is a monthly demand level at $66 per share, which took control last November 2024. It's the end of January 2025, and the stock is rallying as expected.

AMD Channel Down bottomed on RSI Bullish Divergence.Advanced Micro Devices (AMD) have been trading within a Channel Down pattern since the March 08 2024 All Time High (ATH). The pattern is currently on its 3rd Bullish Leg and is below its 1D MA50 (blue trend-line) for exactly the past 3 months.

This Bearish Leg has however most likely come to an end as the 1D RSI is on Higher Lows against the price's Lower Lows, showcasing a Bullish Divergence similar to May 01 2024. As a result, we can expect the new Bullish Leg to start, with the previous minimum being +32.85%. Target $148.00.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

NVIDIA hit its 1W MA50 after 2 years! One last rally left?NVIDIA Corporation (NVDA) opened significantly lower on Monday following the DeepSeek news on more efficient and lower cost A.I. competition and by doing so, the price hit its 1W MA50 (blue trend-line) for the first time in 2 years, resulting in Tuesday's very strong rebound.

We have to go back to the week of January 23 2023 to see NVDA trading again on the 1W MA50, which became the major Support of the Channel Up pattern that took it off the 2022 Inflation Crisis bottom.

So the question is, does NVIDIA have fuel left in the tank for one more rally? Technically the answer is yes and it can be found on the stock's price action since July 2015. As you can see, the price has gone through 3 similar eras of Bull Cycles through Channel Up patterns and subsequent Bear Cycles of strong corrections that touched the 1W MA200 (orange trend-line) before initiating the new Bull.

From the Bear Cycle bottom to the Bull Cycle's top, NVIDIA took around 1100 days (1162 during the 2015 - 2018 Cycle and 1071 during the 2019 - 2021 Cycle). Assuming the current Cycle will be at least as long as the last one (1071 days), the stock's Top is expected to be around September 2015.

It was in fact around this time during the last Cycle (Feb 2021) when NVIDIA touched again its 1W MA50, resulting into a new rally phase, the last one of the Cycle. This historic price action shows that during its last year, the stock always makes a January - Oct/Nov rally. When the 1W MA50 gets hit again, it is when the new Bear Cycle is confirmed.

As a result, based on this data set, we've entered NVIDIA's final rally of the Cycle, assuming of course it doesn't close a candle below the 1W MA50 and also that the 1M RSI recovers its MA trend-line (yellow), which also happened again during its previous Cycle.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

RTX Bullish Momentum – Move Toward $131.00 ExpectedNYSE:RTX is demonstrating strong bullish momentum, supported by moving averages and consistent upward strength in price action. The recent push above $125 confirms that buyers are in control, and suggests a likely continuation toward the $131.00 level.

A pullback toward $125–126 could provide an opportunity for buyers to step in, maintaining the rally's trajectory.

This setup aligns with the expectation of a bullish continuation, offering a potential long opportunity if pullbacks or consolidations occur near current levels.

DeepSeek AI | TechStocks Crash | NVIDIA down -17%On Monday (yesterday), Wall Street reacted wildly with the release of Chinese AI app DeepSeek.

Throughout the day, roughly 1 Trillion US Dollars was wiped from the stock market, largely from chip and tech stocks suck as Nvidia which caused a larger sell-off.

OpenAI CEO Sam Altman called it an "impressive model" and POTUS Donald Trump said that it should be a "wakeup call for our industries".

The bright side of this, is that there can be some excellent entry points found across the market after the sell-off.

_______________

NASDAQ:NVDA

APPLE Strong buy on the 1D MA200 targeting $260.Apple Inc. (AAPL) has been trading within a 2-year Channel Up and the recent correction since the December 26 All Time High (ATH) is its technical Bearish Leg. The price posted a strong rebound yesterday following a test of the 1D MA200 (orange trend-line), the first such contact since May 08 2024.

With the 1D RSI touching the oversold barrier (30.000) and rebounding, this is technically a strong buy opportunity at least for the medium-term, as it's not a direct Higher Low of the Channel Up.

Since December already completed a +59% rise from the April 19 2024 Low, we might be having technically a medium-term rebound similar to the October 26 2023 one that re-tested the High's Resistance (at the time). As you can see both corrections have hit the 0.618 Fibonacci level.

As a result, we treat this as a solid buy opportunity to target $260.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

ANANT RAJ Ltd 38% in 5 Days!!!ANANT RAJ Ltd Stock - Short Trade in 15m timeframe

The Risological Options Trading Indicator crossover to the bearish side happened on 23 Jan, 2024 at 11:30 am, where I entered the short trade (spot).

Wanted to close it today, however, the stock hit lower circuit.

Hopefully I will get a chance to exit tomorrow, wish me good luck!

Micron (MU) Stock Update: Correction or Collapse?Morning Trading Family

Here's what's up with Micron (MU): If it bounces back at 92, cool. But if it keeps going down, it might hit 89-90 before it stops. If it drops past that, we might see it go to 84 or even 80. This could be a big moment for MU, so keep watching!

Kris/Mindbloome Exchange

Trade What You See

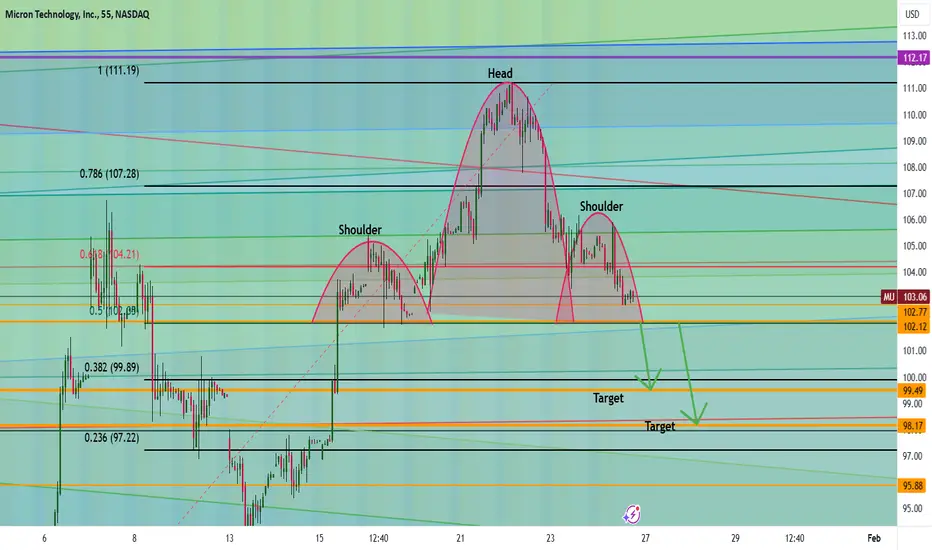

Micron's Next Move: Will $102 Trigger a Drop to $98?Micron (MU) is showing a head and shoulders pattern, and it’s at a critical level. If it breaks below $102, I think we could see it drop to $99.50 or even $98.

This could be a big move, so keep an eye on it!

If this helps, I’d love to hear your thoughts—drop a comment, like, or share. Let’s trade smarter and live better! 💡

Kris/Mindbloome Exchange

Trade What You See

Oracle Soars on USA AI Deal – Is $238 Next?Good morning, trading family!

Here’s what I’m seeing for Oracle (ORCL) right now:

If it can break above $191, we might see it push up to $199–$200. If it clears that, $230–$238 could be the next big move, especially with all the excitement around its role in the $100B U.S. AI project.

But let’s stay cautious—if it drops, $179 could be the next level to watch, and if that doesn’t hold, $166 might be in play.

If this analysis helped you, drop a comment below! A like, boost, or share would mean the world and help others join the conversation. Let’s crush it this week!

Kris/Mindbloome Exchange

Trade What You See

NVIDIA This is the final call for $240.NVIDIA corporation (NVDA) has been trading within a Channel Up for the past 2 years and just last Monday it made contact with its bottom (Higher Lows trend-line). As long as the 1D MA200 (orange trend-line) remains intact, the bullish trend will be maintained.

On top of that, the price action has just completed a pattern, which in the last two times we saw it (Q3 2024 and Q4 2023), it initiated a rally. With the Channel's Bullish Legs being at least of a +86.50% increase, we expect NVIDIA to target at least $240 by May.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

NVIDIA's Momentum A Breakout Story in Progress1. Trend and Structure

The chart showcases an upward momentum, breaking out of a prior resistance level, indicating bullish pressure. The breakout aligns with the upward-sloping trendline, which serves as a strong support structure.

2.Breakout Confirmation

The price has successfully broken through a resistance level, confirming a bullish breakout. This signals potential continuation toward the marked target zone.

3.Entry Point

The entry appears to have been taken near the breakout point, at approximately $141.60, aligning with the bullish momentum.

4. Target (Take Profit)

The take-profit level is marked at $152.94, representing a reasonable upward move from the breakout point. This target aligns with the continuation of the trend.

5. Stop Loss

The stop-loss level is placed at $133.46, below the recent support and trendline. This level ensures protection in case the breakout fails.

6.Risk-Reward Ratio

The setup demonstrates a healthy risk-to-reward ratio, with potential gains outweighing the risks. This indicates a well-calculated trade.

7. Technical Indicators

The momentum of the candles breaking the resistance shows strong bullish interest. No immediate signs of bearish divergence or reversal are visible in the chart.

The chart reflects a bullish breakout setup in NVIDIA's stock price. With strong momentum and a clear trendline breakout, the trade aligns well with the current upward movement. The target and stop-loss levels are well-placed, adhering to a disciplined trading strategy.

NETFLIX New Bullish Leg to $1140 has started.Netflix (NFLX) has been trading within a long-term Channel Up since the October 18 2023 Low. Every time that the price broke below and later recovered the 1D MA50 (blue trend-line), it was the most efficient buy signal of the pattern.

This is what took place yesterday, we had the first recovery above the 1D MA50 since the break below it on Jan 10. Along with the inevitable Bullish Cross below the 0.0 level on the 1D MACD (which again has been the best buy signal all these years), we expect the new technical Bullish Leg of the Channel Up to start.

So far we've had 5 core Bullish Legs and as you can see the tend to rise by roughly the same amount two at a time. The first two have been roughly +40%, then the next two +25% and the one before +38.71%. It is fair to assume that the one that has just started will be of around +38.71% too. As a result, we can place our Target a little lower for less risk and aim at $1100.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Inverse head and shoulder pattern monthly chart Just for education purpuse

Its look like inverse head and shoulder patern on monthly chart

thanks

From Market Underdog to Tech Titan| AppLovin’s Explosive Growth AppLovin: Making Ads Great Again, One Algorithm at a Time

AppLovin Corp, a prominent software company valued at $57 billion, offers an advanced mobile marketing platform. Over the past year, its stock price has surged by an impressive 500%, far outpacing the S&P 500’s 39% increase. The company’s financial growth is equally remarkable, with a year over year revenue boost of 40%, a 188% jump in operating profits, and a 300% surge in net income in its latest quarterly report

With 40% of the company held by insiders and a shareholder friendly stance that includes share buybacks, AppLovin presents a compelling investment opportunity. Additionally, its valuation remains competitive relative to other software companies, supporting my "buy" rating.

From Ad Nerds to Tech Lords, AppLovin’s Secret to Winning Over Wall Street

AppLovin operates a comprehensive software platform that helps clients achieve crucial KPIs, such as revenue growth and business expansion. Leveraging AI, its software platform stands out as a powerful tool for advertisers, providing capabilities like automated marketing, customer engagement, and monetization. It’s built to optimize targeted content delivery to the most suitable audience, supported by analytics and monetization features that drive maximum value.

At the core of AppLovin’s technology is AXON, an AI engine that powers AppDiscovery. This feature matches advertiser demand with publishing opportunities through a sophisticated real-time auction algorithm, shifting from traditional waterfall systems to an intelligent, programmatic approach.

AppLovin has positioned itself as a leader in the future of advertising, driven by its cutting-edge AI capabilities. I believe there’s immense growth potential here that the company is just beginning to explore.

Performance

In the third quarter, AppLovin reported a 39% year-over-year revenue increase, moving from $864 million to $1.2 billion. This marks its highest-ever quarterly revenue and extends its streak of sequential topline gains to seven quarters. For the first nine months of 2024, AppLovin saw a 43% year-to-date revenue increase, largely fueled by a 76% rise in software platform revenue. This growth was driven by AppDiscovery, whose installations surged by 39% in Q3, underscoring its strong appeal to advertisers.

Beyond software platform growth, AppLovin’s in-app purchases and advertising revenues also increased modestly by 3% and 7%, respectively, despite challenging comparisons, supported by a 53% boost in advertising impressions.

The company achieved record operating cash flows of over $550 million in Q3, alongside significant margin improvements across gross, operating, and EBITDA levels. These gains highlight the company’s explosive growth and underscore the stock’s 500% rise over the past year.

Given AppLovin’s strategic success and positive advertiser response, I anticipate ongoing improvements in cash flow and profit margins. With over $3.3 billion spent on share buybacks since 2022—$980 million in 2024 alone—the company continues to reward its shareholders while capitalizing on its profitable AI-driven platform.

Valuation

Although APP’s trailing P/E ratio of 74.52 and PS ratio of 19.33 might appear high compared to the IT sector averages, a comparison with peers in the Application Software industry reveals a different perspective.

In a peer group of large software companies, APP ranks third in EV/Sales ratio at 18.65 but also boasts a forward topline growth rate of over 24.1%, placing it among the top performers. This high growth potential appears to justify the stock’s premium, positioning it attractively in terms of PS ratio relative to anticipated growth.

Despite recent heavy buying, APP remains an appealing value investment. As long as it maintains its relative positioning, I continue to view the stock favorably.

Risks

Despite my optimism, I recognize that AppLovin’s momentum could be part of a broader AI-driven market surge, raising concerns about a potential AI bubble. If the market faces a downturn similar to the dot-com bubble, APP could experience a sharper decline than its peers, especially given its relatively weak balance sheet.

Additionally, with an RSI of 96 signaling heavy overbuying, there may be potential for a future correction. While APP’s 500% rise is impressive, it could be vulnerable if the market undergoes a broader correction

Conclusion

Advertising is on the cusp of an AI driven transformation, and AppLovin is well-positioned to capitalize on this shift with its powerful AI-enabled platform. Despite the stock’s impressive 12-month performance, there’s still significant growth potential

COSTCO New uptrend about to begin.Costco (COST) gave us the most optimal buy signal on our previous analysis (October 07 2024, see chart below) right at the bottom of the Channel Up, and easily hit our 1000 Target:

Yet again, we are ahead of a strong bullish break-out and the only Resistance level that remains is the 1D MA50 (blue trend-line). The 1D RSI has already given a buy signal right on its oversold barrier (30.00) on January 02 2025.

Once the 1D MA50 breaks, we will have a confirmed break-out buy signal. The previous tree Bullish Legs have been of at least +16.08%, so our new Target as of today is 1045.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

GREAT LONG?!"START OF A TREND WHERE THE EMA STARTED TO BALLOON.

QUESTIONS TO ASK YOURSELF:

How does the company look fundamentally?

Has the stock shown full respect for the 50 EMA?

Has the stock created a bottom and a breakout?

Are we holding above the 20 EMA?

Trail the stop approximately 8%.

Sell 50% at overbought levels (RSI).

Jyoti CNC Trying to make a comeback. Jyoti CNC Automation Ltd. engages in the provision of manufacturing solutions for computerized machine cutting tools. It operates under the Within India and Outside India geographical segments.

Jyoti CNC Automation Ltd. CMP is 1273.05. The Positive aspects of the company are Company with Low Debt, Company able to generate Net Cash - Improving Net Cash Flow for last 2 years and Companies with rising net profit margins. The Negative aspects of the company are extremely high Valuation (P.E. = 105.5), High promoter stock pledges, Increasing Trend in Non-Core Income and Companies with growing costs YoY for long term projects.

Entry can be taken after closing above 1293Targets in the stock will be 1337, 1368 and 1406. The long-term target in the stock will be 1434, 1463 and 1513. Stop loss in the stock should be maintained at Closing below 1157 or 1079 depending on your risk taking ability.

Disclaimer: The above information is provided for educational purpose, analysis and paper trading only. Please don't treat this as a buy or sell recommendation for the stock or index. We do not guarantee any success in highly volatile market or otherwise. Stock market investment is subject to market risks which include global and regional risks. I or my clients might have positions in the stocks that we mention in our posts. We will not be responsible for any Profit or loss that may occur due to any financial decision taken based on any data provided in this message. Do consult your investment advisor before taking any financial decisions. Stop losses should be an important part of any investment in equity.