Silicon Valley Bank / SIVBSVB Financial Group stock tumbled more than 42% in premarket trades Friday on fears of a run on the bank, as analysts downgraded the company and reports surfaced of funds advising clients to pull their money from the parent company of Silicon Valley Bank.

Founders Fund, the San Francisco-based venture-capital fund co-founded by Peter Thiel, has advised companies to pull their money, according to a Bloomberg News report citing people familiar with the matter.In a separate development, The Wall Street Journal reported that SVB Financial Group took out $15 billion of loans from the Federal Home Loan Bank of San Francisco at the end of 2022, compared to zero in the year-ago period, to assure liquidity.

The bank pledged collateral of about three times what it borrowed to back the advances, the WSJ reported, around the same time it sustained a 13%, or $25 billion decline in deposits in the final three quarters of 2022, the WSJ reported.

The steep losses Friday came after SVB Financial SIVB, ended down 60% in the regular trading day after it disclosed large losses from securities sales and announcing a dilutive stock offering along with a profit warning. The bank was unprepared for rising interest rates which have hit its net interest income and net interest margin

the troubles at SVB seemed unlikely to spread widely throughout the banking system. Morgan Stanley said in a note to clients that SVB’s issues were “highly idiosyncratic.”

Also on Wednesday, SVB announced it sold $21 billion worth of securities to raise cash and reposition its balance sheet toward assets with a shorter duration, which are less exposed to rising interest rates. SVB estimated that it took a $1.8 billion loss on that sale.

SVB

USDC & SVBIn the past 24 hours, the trading volume of the Bybit USDC/USDT perpetual contract pair exceeded an astonishing $380 million, and the annualized funding rate was as high as 740%

After Friday's stunning collapse of Silicon Valley Bank, questions swirled around the exposure of one of crypto's top firms, Circle, the issuer of the second-largest stablecoin, USDC.

In its March attestation, Circle had revealed that part of its $9.88 billion in cash reserves was held at SVB, although it did not disclose the total amount. Following the collapse of SVB, withdrawals from USDC mounted, with the crypto intelligence platform Nansen showing over $1 billion in redemptions from the stablecoin since SVB's shutdown. USDC has a market cap just north of $40 billion.

As USDC lost its $1 peg across different crypto exchanges amid withdrawals, Circle sought to instill confidence, with the company tweeting at 6:50 pm ET that it would continue to operate normally, sharing that SVB was one of the six banking partners it uses for the 25% of its reserves that it keeps in cash, although still not disclosing the amount held at SVB.

As investors continued to move out of USDC, Binance announced it would be temporarily suspending its auto-conversion policy of USDC to its BUSD stablecoin, citing "market conditions" and describing the action as a "normal risk-management procedural step." At 10:11 PM ET, Circle offered more clarity, tweeting that $3.3 billion—or around 8%—of its reserves remained at SVB, revealing that wires initiated on Thursday to remove balances from the bank had not been processed. Dante Disparte, Circle's chief strategy officer, tweeted soon after that Circle was protecting USDC "from a black swan failure in the banking system."

Meanwhile, USDC's peg continued to weaken, with the token trading at $0.92 against tether on Kraken as of 10:40 pm ET. Coinbase announced it would be temporarily pausing conversions from USDC to USD over the weekend while banks are closed, adding that during periods of heightened activity, conversions rely on USD transfers from banks that clear during normal banking hours. Coinbase worked with Circle to create USDC, launching the token in 2018.

After the FDIC placed SVB into receivership on Friday, the weekend will prove an uncertain time as the financial world waits to see if the U.S. government is able to find a buyer for the failed bank or will otherwise backstop losses, with insured deposits only backed up to $250,000. Former Treasury Secretary Lawrence Summers called for depositors to be paid back in full.

While the crypto industry seems to be safe from SVB contagion for now, with much of the sector moving to Signature Bank and other partners in the wake of Wednesday's voluntary liquidation of Silvergate, Circle could prove the exception. The firm is a fundamental cog in the crypto ecosystem, with USDC serving as a crucial on-ramp into crypto for investors globally.

Some onlookers expressed confidence that Circle would be able to weather the storm. The investor Adam Cochran tweeted that Circle could cover a possible $3.3 billion gap from the interest it collects from reserves, a sale share, or other venture debt. "This is a non-issue in my mind," he wrote.

The hedge fund North Rock Digital CEO Hal Press said that they has continued to buy more USDC at $0.88, having previously bought at $0.935; he believes that USDC will end up fully repegging, a worst case 70% of the cash via asset sales USDC would still be worth 93c.

Yields are mixed but all point higher, history repeating?🚨🚨🚨

Going to make a stink about #yield again.

Short term #interestrates have been creeping higher.

Let's👀@ #bond Yields.

6M = holding steady, trading slightly higher.

BUT,

1Yr = BROKE RECENT HIGHS. It's at resistance but shows momentum.

2Yr = Closing in on TSX:SVB closure high. This is where #banks began to break down.

10Yr TVC:TNX @ current downtrend is being tested. Break through is good.

HUH?

Higher = good short term for #stocks. Markets have a history of breaking AFTER rates begin to trade lower and yield curve normalizes. This can take a year or so.

Not saying markets will be pumping for a year. Just saying this is historical. We could be setting up for much more upside but with RISK.

We posted on the 2008 yield crisis some time ago.

Despite bank run, why is the market higher? • First, the bank run APPEARS to have stabilized

• Second, the inflation SEEMS to be taming

Do not be complacent, keep on keeping track of the coming market developments. Just like what Jerome Powell said on the 3rd May after the latest interest rate hike, in the meeting conference, he said “We will take a data-dependent approach, our future policy will depend how events unfold … meeting by meeting.”

I totally agree with him! As a retail investor, we can study into the price behavioural movement and I did quite a few videos on that (see below), market will usually give us early signal and we should be able to tell before the next crisis hits again.

Trading & Hedging in Nasdaq -

E-mini Nasdaq Futures & Options:

Minimum fluctuation

0.25 index points = $5.00

Micro E-mini Nasdaq Futures & Options:

Minimum fluctuation

0.25 index points = $0.50

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Why Russell Index the most Reflective for Bank Run Crisis?Russell represents the true economy of United States.

There are 2,000 medium size companies with each value between $300m to $2b. The index includes a diverse range of companies from various sectors, including financials, healthcare, consumer goods, industrials, and technology. In my opinion Russell represents the true economy of united states.

If the bank run crisis deepens, it is possible that 2,000 companies will not hold up well. The reasons for this are stated in the video. This could affect the other major indices, with the Russell 2000 potentially leading the pack. The Russell 2000 is considered more reflective of the US economy compared to the other major indices with big names like Apple, Amazon, and Microsoft.

E-mini Russell 2000 Index Futures & Option

Outright:

0.10 index points = $5.00

Micro E-mini Russell 2000 Index Futures

Outright:

0.10 index points = $0.50

Micro E-mini S&P 500 Index Futures & Option

Outright:

0.25 index points = $1.25

Micro E-mini Nasdaq Index Futures & Option

Outright:

0.25 index points = $0.50

Micro E-mini Dow Jones Industrial Average Index Futures

Outright:

1.0 index points = $0.50

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Regional Banks Leading Market to Hell?Regional Banks have always led our economy during booms and during busts. You will note from this simple chart that one key trend line has measured our current secular bull market. Regional banks have remained above this trend line since it was first touched in 2009. Excluding March 2020 (Covid19), which is not valid data, regional banks have never dipped below with confirmation. My best guess is that if they do, it will spell the beginning of the end for the U.S. macroeconomy in its current secular bull run. Watch closely as regional banks are really flushing the toilets today. If not careful, they may also need a savior. Enter JPOW and the Fed for a surprised pause/pivot ...if so.

PacWest, NASDAQ:PACW : -36%

Western Alliance, NYSE:WAL : -31%

Metropolitan Bank, NYSE:MCB : -27%

HomeStreet, NASDAQ:HMST : -23%

Zions Bank, NASDAQ:ZION : -15%

KeyCorp, NYSE:KEY : -9%

HarborOne, NASDAQ:HONE : -10%

Citizens Financial, NYSE:CFG : -12%

Remember, of our four largest bank failures to date: Washington Mutual (-386 billion), First Republic (-$233 billion), SVB (-209 billion), and Signature Bank (-118 billion) ...three of these have occurred in the last 2 months ...and we ain't done yet, folks.

The true shitcoins are large centralized corporate banks. We must be ready to transition to an alternative currency solution. Enter Bitcoin/crypto. Be ready.

Best,

Stew

Bank Wars: 1st Republic, 1st Citizens, Silicon Valley, BitcoinAs First Republic Bank continues to slide down the charts (still ongoing at the publishing of this idea), talks about another bank run happening is starting to resurface again. How valid is the claim that people will flee to crypto as things get worse in the banking system? (Especially with people like Balaji, that claims that Bitcoin will hit HKEX:1 ,000,000 by the end of June.) A closer look at some of the facts.

Balaji's 1M Bitcoin Thread:

twitter.com

When Fear Reigns Banking Majors GainIn times of crisis, investors rush to safety. When risk shows in places of safety, bank runs begin. One's pain is someone else's gain. Silicon Valley Bank (SVB) & Signature Banks' combined assets at $300 billion is witnessing a flight to safety.

At $300 billion, it is trivial relative to $23 trillion within the American banking system. Remember that the FDIC only insures deposits up to USD 250k. Both institutional and individual clients holding large deposits in regional banks are rushing to move their funds from regional to major banks.

Between 2020 and 2022, regional bank index outperformed the broader bank index. Regional banks business was designed to be lean - collect deposits and extend loans to home buyers and local businesses.

This was meant to be less risky relative to banking majors whose businesses were sophisticated and inherently risky. Hence the banking relief law passed in 2018, made regulations less onerous to banks with domestic assets of less than $250 billion.

As a result, by end of 2022, US had 2,100 banks with $19.8 trillion in assets. Only ten out of these 2,100 banks had domestic assets more than $250 billion.

Lax regulations led some regional banks astray with concentrated bets on customer segments and risk management of asset and liability maturity risk. With rates rising, tides receding, banks that were swimming naked became obvious.

Chart below contrasts the impact of unrealised losses on select US bank's tier 1 capital ratio. It is little surprise that SVB imploded with such an adverse capital situation when unrealised losses were accounted for.

Now as crisis of confidence in banking spreads across both sides of the Atlantic, depositors are rushing to move their money to larger safer bank and money markets.

FT reported on March 15th that large US banks are getting flooded with fund transfer requests from regional banks. SVB has triggered a tectonic shift in deposits unseen in more than a decade. Veteran hands know well that anxiety created by small shocks make larger crises less likely.

JPM, Citigroup are among the beneficiaries of regional bank pains. To aid customers to move deposits swiftly, these banks are taking extra steps to speed up client onboarding. It is reported that these banks are reassigning employees to account opening linked jobs to handle workload and to hasten the process.

HNI’s Shifting to Large Banks

Despite the liquidity backstop promise extended by US Fed and US Treasury, depositors are moving funds into larger banks such as JPM, Citi and Bank of America. This phenomenon is more so for accounts holding >$250k (the limit up to which is guaranteed by FDIC).

The 25 biggest US banks gained $120B in deposits in the days following the collapse of SVB and Signature while smaller banks saw a net outflow of $108B during that period. This has been the largest weekly decline in deposits at small banks and poses the risk of inciting more financial instability.

Citi’s private bank servicing wealthy individuals is opening accounts within a day compared to usual timeline of one to two weeks. Citi is reported to open accounts & initiate fund transfers even as new clients are under compliance checks.

Larger banks are subject to significantly tougher regulatory scrutiny as a result they become attractive destinations for shell-shocked depositors.

Portfolio diversification is not new. Long shadow cast by the debacle of three sizeable banks within a space of a week has exposed the fragility in the system. This has prompted depositors to diversify not only their portfolios but also their banks.

Moreover, comparing the actual assets held by large banks to mid-sized banks:

SVB and Silvergate, both of which collapsed had their assets largely held in bonds held to maturity or available for sale. For SVB, the maturity date was in the far future, posing liquidity concerns when a bank run ensued.

By contrast, Silvergate largely had bonds available for sale but selling them all at once would have caused huge realized losses.

Another interesting takeaway is the way in which each regional mid-sized bank adopts a different portfolio tailored for their specific clientele and their needs. Although, this allows them to fine-tune their operations and holdings, it comes with the downside of financial instability during periods of aggressive rate hikes and economic uncertainty.

By contrast, Citigroup, JP Morgan, BoA, and PNC have portfolios that are well diversified with a healthy mix of cash & interbank loans, loans, bonds to maturity, and bonds available for sale. Crucially, their significant cash holdings allow them to weather the storm far better and eases any liquidity concerns for depositors.

Capital Flow Towards Asset Managers

Large asset managers are also witnessing an influx of funds. Seemingly the money is moving away from regional banks and into majors and asset managers offering access to money market funds. Money market funds which hold US Government Debt are considered the safest destination for large amounts of fund given the overwhelming uncertainty in the banking sector. They also have the added advantage of offering investors seniority in case of bankruptcy proceedings.

Certain MMF’s are currently offering yields as high as 5.02% compared to a paltry 0.23% average for bank deposits, making the shift towards MMF’s a no-brainer for many.

More than $300B has flown into money market funds in March taking the overall assets in money market funds to a record $5.1T. This also represents the largest month of inflows for asset managers since the start of the COVID-19 pandemic. Goldman, Fidelity, and JPM are the biggest beneficiaries from these inflows.

Goldman’s US money market funds have increased by $52B or 13% since the beginning of the banking crisis on March 9th. JPM’s funds received $46B while Fidelity saw $37B of inflows according to data from iMoneyNet.

Capital Flow into Gold

Gold is one of the most prominent safe haven assets that investors look to in times of economic uncertainty and instability. This capital flow was seen during the 2008 financial crisis when bank deposits plummeted and Gold price skyrocketed.

The same can now be seen on an even larger scale. Commercial bank deposits have plummeted well below even 2008 levels while the price of gold is teetering around $2,000/ounce, the highest price ever.

Although, some gold investors choose to buy physical gold or jewellery, larger investors often opt for other instruments that are more cost effective such as ETF’s or Futures. This too offers the larger banks a huge opportunity to benefit from the inflow of capital into gold-linked products through their investment banking divisions.

GLD, or SPDR gold trust is the largest Gold ETF. It saw a net inflow of $915M in March. The same can be seen in CME’s GC futures which saw managed money traders increase their net long positions by 5x or 83k contracts ~$16B.

Trade Setup

This case study illustrates potential gains to be harvested from spread trades as funds move from regional banks to majors. With rates remaining elevated the majors enjoy a comfortable Net Interest Margin. Rising deposit base by cherry picking high credit quality customers will enable banking majors to vastly outperform the regional banks.

Therefore, this case study sets for three spread trades -

(a) Long JPM and Short KBWR (1:3)

(b) Long COF and Short KBWR (1:2)

(c) Long C and Short KBWR (1:1)

A spread trade requires that the notional values of each leg of the trade to be identical. Accordingly, the ratios above have been provided based on the closing prices as of April 3rd. Table below sets out entry, target, stop and reward-to-risk ratio for each of these trades.

Long JP Morgan & Short KBWR

● Entry: 2.82

● Target: 3.17

● Stop: 2.62

● Profit at Target: $16

● Loss at Stop: $9.5

● Reward-to-Risk Ratio: 1.7x

Long Capital One Financial & Short KBWR

● Entry: 2.08

● Target: 2.54

● Stop: 1.9

● Profit at Target: $21

● Loss at Stop: $8.5

● Reward-to-Risk Ratio: 2.5x

Long Citibank & Short KBWR

● Entry: 1.01

● Target: 1.19

● Stop: 0.937

● Profit at Target: $8

● Loss at Stop: $3.5

● Reward-to-Risk Ratio: 2.2x

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com cme /.

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

Bank Run to Gold Rush Gold rush up accordingly to each major news during the bank run crisis in March.

Problem seems to subside for now. We will explore the possibility of a contagion effect to a wider bank run in this video.

A story of having too much money problem

• It is a bank – need to pay interest to depositors

• During pandemic - invested 10yrs bonds yield average 1.79%

• Before Feb 2022 Fed fund rate at 0.25%

• Mar 2023 Fed fund rate at 5%

How about the other banks, will they also have a similar problem in time to come? With uncertainty still lingering I am seeing opportunities in Gold, other precious metals and commodities.

3 types of gold for trading:

• COMEX Gold

0.10 per troy ounce = $10.00

• E-mini Gold

0.25 per troy ounce = $12.50

• Micro Gold

0.10 per troy ounce = $1.00

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Banking crisis + War Provocation = Haiiyaaa! More money printing. More banks facing liquidity shortage. More bank runs as panic and fear kicks in. As mentioned before, Q2 will be bank run galore.

Entire 2 year's QT effort by Jerome Powell, is now being reversed in less than a month.

Did Credit Suisse got bailout by SNB and UBS recently for almost $105B Swiss Francs? Hmm today $CS is trading at less than $1.

Did SVB got liquidity injection by several banks and the government to avoid collapse? Hmm a week ago, SVB just filed chapter 11 for bankruptcy protection.

Good read here: lnkd.in

Early this week Deutsche Bank is knee weak and now the latest one, Schwab is flying a kite outside during a monsoon storm. Awesome read here:

lnkd.in

Yo, at the end of the day, I am forecasting that only a handful of banks, like less than 5, will be standing in the coming years.

To usher in CBDC, you must herd the sheeps into a smaller ranch to make control and compliance, easier.

To usher in CBDC, competition is BAD. Very bad. Competition is antithesis of monopoly. Therefore, Bitcorn? Ethereum? And the other cryptos? Hmm

And US is getting more aggressive in provoking war with China and Russia.

What has the world got to now....

I remember an old saying, "When all else fail, go to war"

By Sifu Steve @ XeroAcademy

Eurozone banks now caught the coldAs I mentioned before, the contagion will spread like wildfire because the banking system are so intertwined.

We now see Deutsche Bank potentially get caught in the onslaught. Their share tanked by approximately 15% last Friday.

After Credit Suisse got obliterated and UBS come to pick up the remains with assistance from SNB ($100 Billion Swiss Franc), their share price now trade below $1.

Liquidity injection did nothing to help Credit Suisse. I see this bailout as helping the top 10% to rescue their money and let the rest die.

It is always the case. Silicon Valley Bank just gap down and declining more, Signature Bank not showing signs of recovery at all and the regulators/leaders of US still say everything is okay.

One thing to bare in mind is that, all the country's leaders have a fiduciary duty to not cause public panic, even though they have a gun to their head.

So, what ever you read right now in the mass media by Janet Yellen, Jerome Powell, Bank CEOs and other Central Bank chairperson, is deemed untrustworthy.

As mentioned before, the next sector that might get hit will be real estate, in particular commercial real estate.

White collar layoffs on-going + high inflation + high cost of borrowing + tightening lending requirement + high delinquency in rental/mortgage payments

+ work from home/hybrid preference = commercial real estate crash. If this crash happens, Commercial Mortgage Backed Securities will come crashing down too, which will bring down the Big Banks.

There will be flight to safety. Gold and silver will continue to rise, no doubt about that. US Stock market will like rally short term as Eurozone and Switzerland is on shaky grounds.

US Dollar may see a short term bullishness as sentiment on Euro bloc is hitting the headlines. Massive riots in France due to Macro increasing retirement age, will also be priced-in and act as catalyst.

APAC region could potentially see great alternative to store value and protect capital. APAC markets, as I always said, is more conservative and resilient.

By Sifu Steve @ XeroAcademy

DXY Potential Forecast| Pre FOMC | 23rd March 2023Fundamental Backdrop

1. Plenty of instability in the market due to the SVB crisis and other banks being heavily affected by it.

2. The Fed is incentivised to either pause rates or maintain at 25bps due to the current instability in the market.

Technical Confluences

1. Price is currently in a bearish trend.

2. Price is near the H4 support area at 102.65.

3. Well below the ichimoku cloud, signifying bearish intent.

Idea

Looking for price to form a new lower low at 100.821.

NOT FINANCIAL ADVICE DISCLAIMER

The trading related ideas posted by OlympusLabs are for educational and informational purposes only and should not be considered as financial advice. Trading in financial markets involves a high degree of risk, and individuals should carefully consider their investment objectives, financial situation, and risk tolerance before making any trading decisions based on our ideas.

We are not a licensed financial advisor or professional, and the information we are providing is based on our personal experience and research. We make no guarantees or promises regarding the accuracy, completeness, or reliability of the information provided, and users should do their own research and analysis before making any trades.

Users should be aware that trading involves significant risk, and there is no guarantee of profit. Any trading strategy may result in losses, and individuals should be prepared to accept those risks.

OlympusLabs and its affiliates are not responsible for any losses or damages that may result from the use of our trading related ideas or the information provided on our platform. Users should seek the advice of a licensed financial advisor or professional if they have any doubts or concerns about their investment strategies.

XAUUSD Potential Forecast | 21st March 2023Fundamental Backdrop

1. Plenty of instability in the market due to the SVB crisis and other banks being heavily affected by it.

2. GOLD, as a safe haven asset, flew to the highs to 2000 and is currently rejecting.

3. This is fuelled by the instability with the USD.

Technical Confluences

1. Price could potentially retrace back to the H4 support level at 1959.24 before heading back up.

2. Price went parabolic to the 2000 regions.

3. Bullish pressure is still intact and will be looking for longs.

Idea

Looking for price to break new highs beyond 2065 and this is just the beginning.

NOT FINANCIAL ADVICE DISCLAIMER

The trading related ideas posted by OlympusLabs are for educational and informational purposes only and should not be considered as financial advice. Trading in financial markets involves a high degree of risk, and individuals should carefully consider their investment objectives, financial situation, and risk tolerance before making any trading decisions based on our ideas.

We are not a licensed financial advisor or professional, and the information we are providing is based on our personal experience and research. We make no guarantees or promises regarding the accuracy, completeness, or reliability of the information provided, and users should do their own research and analysis before making any trades.

Users should be aware that trading involves significant risk, and there is no guarantee of profit. Any trading strategy may result in losses, and individuals should be prepared to accept those risks.

OlympusLabs and its affiliates are not responsible for any losses or damages that may result from the use of our trading related ideas or the information provided on our platform. Users should seek the advice of a licensed financial advisor or professional if they have any doubts or concerns about their investment strategies.

USD Hangs in the Balance: Bank Chaos vs. Inflation The US Federal Reserve is about to begin its two-day policy meeting and will announce its latest interest rate decision 48 hours later. During the meeting, officials will weigh the possibility of raising interest rates due to inflation, which is still considered high, or whether the current turmoil in financial markets should be given more weight. Unfortunately, the pre-meeting blackout period prohibits officials from commenting on the situation.

UBS shares, which had dropped over 14%, managed to recover by closing 1.2% higher after the bank provided a 3 billion Swiss franc ($3.2 billion) emergency rescue package for its troubled domestic rival, Credit Suisse. The large size of Credit Suisse's balance sheet, which stands at around 530 billion Swiss francs as of the end of 2022, is a concern for the global banking system, as it is twice the size of Lehman Brothers' when it collapsed in 2008.

The Federal Reserve, in response to the Credit Suisse crisis and the failures of a few US regional banks, has begun offering daily currency swaps to central banks in Canada, Britain, Japan, Switzerland, and the euro zone in order to ease funding stress in global markets.

With all this going on, traders are uncertain whether the Federal Reserve will raise its benchmark policy rate on Wednesday (US time). The dollar index fell below 103.5 on Monday for the third session in a row as investors anticipate that the Federal Reserve might not increase rates as much as previously expected due to the banking crises.

Fed funds futures reflect a 70% probability of a quarter-percentage point rate hike, with a 30% chance of no change. A significant drop in near-term inflation expectations is also contributing to the expectation of the Fed pausing its rate hikes, as expectation for the near-term inflation reached nearly a two-year low last month.

In other news, oil prices declined to their lowest point in 15 months on Monday due to concerns that the risks in the global banking sector may lead to a recession. Gold prices, which had surged 6.4% in the previous week, fell to $1,980 an ounce on Monday but remained close to the one-year high of $2,009 hit earlier in the session.

Gold Shines amid Global Financial DistressCOMEX: Micro Gold Futures ( COMEX_MINI:MGC1! )

Gold prices surged Friday as a wave of banking crises shook global financial markets. Spot gold climbed 3.1% to $1,977.89 per ounce, its highest level since April 2022. Gold price is now within $100 of its all-time high of $2,074.88.

In the futures market, the nearby April contract of COMEX gold futures settled at $1,973.5, where the far-month June 2024 contract closed at $2,076.9.

The year-long Fed rate hikes cracked the US banking system. Within two weeks, we have witnessed the collapses of Silvergate Bank and Silicon Valley Bank in California and Signature Bank in New York. First Republic Bank, a mid-sized bank in California, received $30 billion emergency injection from 11 largest American banks, led by JP Morgan.

Interestingly, it was J.P. Morgan who organized a $30 million rescue plan to avert the collapse of Wall Street in 1907. That crisis led to the creation of Federal Reserve System.

A century later, the cost of bank bailout increases by 1,000 folds. However, bank runs have already spread. Credit Suisse, a prestigious investment bank, is under distress. On Sunday evening, fellow Swiss bank UBS announced that it is acquiring Credit Suisse.

Gold Price Rises in Times of Major Crises

In the past two decades, gold price peaked in times of market turbulence.

• The 2008 financial crisis

• The 2010 European debt crisis

• The 2018-19 US-China trade conflict

• The outbreak of COVID pandemic

• The Russia-Ukraine conflict

• The March 2023 bank run

Gold price is also negatively correlated with the US dollar. Last year, when Dollar rose on the back of Fed tightening, gold took a beating. Now, as investors expect the Fed to slow rate hikes, gold shines through the chaos.

Investing in Gold: what in there for you?

• Diversification: Gold helps reduce the overall risk of your portfolio by providing a hedge against inflation and currency devaluation

• Tax efficiency: Long-term capital gains on gold investments are taxed at a maximum rate of 28%, which is lower than 37% for other long-term capital gains

• Protection against rising prices: Gold has historically been a good hedge against inflation, and it can help protect your purchasing power

• Liquidity: Gold ETFs and Gold Futures are highly liquid financial instruments. Many brokers also buy and sell gold bars and gold coins, with a commission.

• Hedge against difficult economic conditions: Gold is a global store of value, and it can provide financial cover during geopolitical and economic uncertainty

• Portfolio diversifier: Gold can act as a hedge against inflation and deflation alike, as well as a good portfolio diversifier

In a previous writing, I showed that gold did not work well as a hedge against inflation.

However, gold holds up extremely well during major crises where other assets lost value.

Hedging against Known and Unknown Risks

Risk on, gold goes up. Risk off, gold declines. Some risks are expected, while others come as a surprise.

Fed rate actions are scheduled events and can be considered known or expected risk. CME FedWatch Tool shows the likelihood that the Fed will change the Federal target rate at upcoming FOMC meetings. It analyzes the probabilities of changes to the Fed rate and U.S. monetary policy, as implied by 30-Day Fed Funds futures pricing data.

As of March 19th, FedWatch estimates a 38% chance of Fed keeping the current rate unchanged at 450-475 bp, and 62% odds of increasing 25 bp to 475-500 bp.

By providing $300 billion in emergency lending to member banks, the Fed has effectively put Quantitative Easing at work. In my opinion, the Fed has switched its priority from fighting inflation to crisis management. Managing the systemic risk in the US banking system outweighs the battle against inflation at this time. It’s a matter of priority.

What’s unknown is the potential failure of any bank not yet exposed in the news. US banks are estimated to sit on unrealized loss in hundreds of billions of dollars in their bond portfolio, largely consisted of Treasury and US agency bonds. As the “held-to-maturity” asset will be sold or marked down, these banks could run into trouble by a run of depositors and investors. In this unusual time, no news is good news.

Short-term Trading Strategies

The upcoming FOMC meeting on March 22nd make a compelling reason for event-driven trades on Micro Gold Futures.

Here is my logic:

• If the Fed keeps the rate unchanged, stock market would rally. As a major risk is removed from the financial system, gold price would fall

• If the Fed raises 25 bps, stock market would fall, and gold price would rally, potentially breaking the current record high

Micro Gold Futures (MGC) contract has a notional value of 10 troy ounces. At $1,993.4, an April 2023 contract (MGCJ3) is valued at $19,934. Initiating a long or short position requires a margin of $800. This is approximately 4% of contract notional value.

If gold price moves up to $2,050, a long futures position would gain $566. Relative to the initial margin, this would equate to a return of +70.8%, excluding commissions.

If gold price moves down to $1,900, a short futures position would gain $934, a theoretical return of +116.8%.

Unexpected market event could be a trigger for gold price to rally. An event-driven trade idea could be constructed around it. In my opinion, comparing to the distress of regional banks, the systematic risks triggered by a Big Bank failure could send global market in shock at ten times the magnitude. If the Fed raises rate next week, I expect more bank failures to coming in the next few months.

Happy Trading.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trading set-ups and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

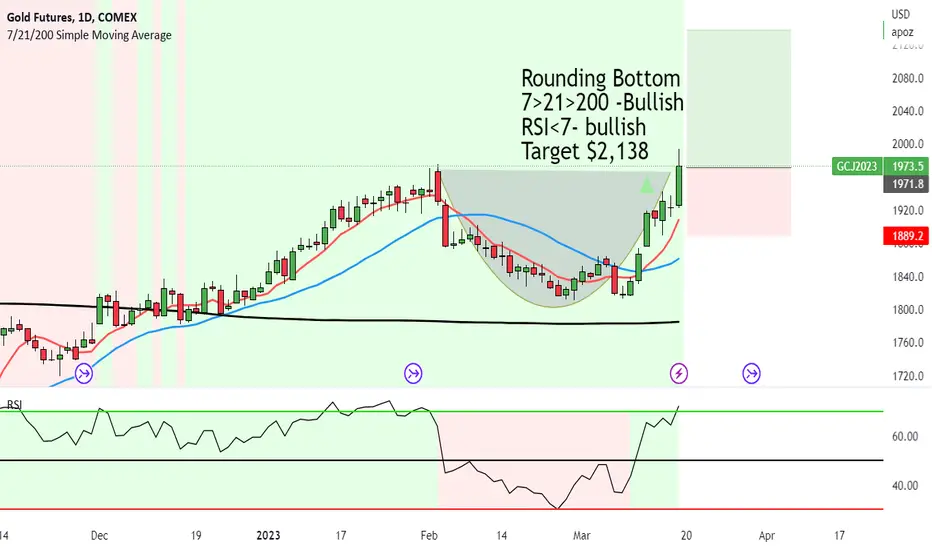

Gold pumping up to $2,138 due to the banking collapse in AmericaRounding Bottom has formed on the daily.

This was a shock to technical analysts as we saw a struggle with gold over the last 2 months to $1,818.

7>21>200 -Bullish

The price failed to break below 200MA showing strong demand and buying.

RSI<7- bullish

Target $2,138

Now we've seen a number of banks collapse from SVB, Silvergate (crypto) Credit Suisse and Republic Bank. And there are now signs that there is contagion which could lead to another 10 - 100 banks to fail as well.

There are a couple of reasons I can think of for the push up for gold.

#1: Confidence in the financial system

If big banks in America collapse, it can shake confidence in the financial system, leading investors to look for a safe haven asset like gold.

#2: Inflation

The collapse of big banks can lead to inflation as the government may print more money to support the economy.

This can increase the demand for gold as a hedge against inflation.

#3: Economic uncertainty

The collapse of big banks can create economic uncertainty.

This can cause investors to seek the stability and security of gold.

#4: Panic buying and protection

The collapse of big banks can lead to panic buying of gold as investors rush to protect their assets.

Once again this leads to gold being the safe haven asset to go to, which will push the price up.

banks are on fire again...The banking system is bursting at the seams again. It all started with the recent series of bankruptcies of several American banks at once and it happened in just a week, which was an echo of the problems of the 2007 crisis, which, as people hoped, we were able to solve.

The main signal of the disaster was a sudden failure in the Silicon Valley bank. On March 9, people's deposits disappeared, losses totaled an incredible $42 billion, which brought out an underestimated risk in the system.

The problem was hidden in long-term bonds, in which the bank invested during a period of low interest rates and high asset prices, and when the Federal Reserve System sharply raised rates, the bank began to have problems. As a result, the bank was left with huge losses that were not previously recognized due to the fact that American capital rules do not require most banks to report a drop in the price of bonds that they plan to hold to maturity.

620 billion dollars – that's how many unrecognized losses were in the entire banking system of America at the end of 2022. To understand how much it is: this amount is equal to about a third of the total capital stock of American banks.

The pandemic has brought even more problems to the economy, and the banking system has become even more shaky. A large volume of new deposits poured into banks, and the Federal Reserve's stimulus measures pumped cash into the system. These deposits were directed by banks to purchase long-term bonds and government-guaranteed mortgage-backed securities, and all this increased the risk of ruin in the event of an increase in interest rates.

Having bought bonds with depositors' funds, the bank essentially used other people's funds, but the problem was not that, but that holding bonds to maturity requires matching them with deposits, and as rates rise, competition for deposits increases. At large banks, such as JPMorgan Chase or Bank of America, rising rates tend to increase their earnings thanks to floating-rate loans. However, in about 4,700 small and medium-sized banks with total assets of $10.5 trillion, rising rates tend to reduce their margins, which helps explain why stock prices of some banks have fallen.

Another problem for banks is the risk that depositors will start withdrawing their deposits during the crisis, which will force the bank to cover the outflow of deposits by selling assets. If this happens, the bank's losses loom, and its capital stock may look comforting today, but most of its filling will suddenly become an accounting fiction. That is why the Federal Reserve System acted this way last weekend, being ready to provide loans secured by bank bonds. By providing loans with good collateral to stop the flight, the Fed is right, but such easy conditions come with certain costs. By creating the expectation that the Fed will take on the risks of interest rate changes in a crisis, they encourage banks to behave recklessly.

The coming year requires regulators to make the system safer and less risky for the people. It is necessary to abolish some strange rules that do not require reporting and answers for increased risks that relate to small and medium-sized banks,

Now the government has announced its intention to rescue depositors of the Silicon Valley Bank, which indicates that such banks carry a systemic risk and they need to be rescued in order not to destroy the entire economy of the country. But saving depositors is only half the job, in order to eliminate the repetition of today's and past problems, it is necessary to introduce the same accounting and liquidity rules that big banks follow, as is the case in Europe, and will have to submit plans to the Fed for their orderly resolution if they fail.

These decisions and actions concern not only the United States, these rules should require the entire banking sector to recognize the risks associated with an increase in interest rates. Unrealized losses carry the risk of bankruptcy and banks with such losses should be confirmed by more thorough control and verification than those who do not have such losses.

Timely testing will help to avoid bankruptcy, which would simulate a situation in which the bank's bond portfolio is released to the market, while rates rise even more. After that, it would be possible to determine whether the system has sufficient capital to avoid bankruptcy or not.

Banks, of course, will resist additional control, increasing capital reserves, but all this will help to improve the quality of system security.

Depositors and taxpayers around the world face intense fear, and they should not live with the fear and fragility that they thought had gone down in history many years ago.

Gold gets a safe-haven bid as banks shake confidenceFinancial markets were sent into a tailspin on the news of Silicon Valley Bank (SVB) imploding. Despite the decisive moves by the Federal Deposit Insurance Corporation (FDIC)1 and the Federal Reserve (Fed)2, market confidence has been shaken and we have witnessed a flight to safety. Demand for government bonds have risen sharply, driving the yields on 10-year US Treasuries down from 4.0% on 9/3/2023 to 3.4% (16/03/2023). In tandem, gold prices have risen 6.6% in the past week (9/3/2023 to 16/03/2023). The speed of gold’s moves indicates that the flight to safety has not been obstructed by any broad-based liquidity issues. Very often in the initial phases of financial market stress, investors sell gold to raise cash to meet margins calls on futures positions in other assets or for other liquidity needs. The current crisis appears different in that there are no visible signs of panic gold selling and that could be indicative that the stress in certain parts of the banking sector are idiosyncratic. Nevertheless, investors have been reminded that unexpected events occur with greater frequency than they hoped and have sought to rebuild defensive positions that will help to hedge against further turbulence.

Credit Suisse concerns add to investors desire for defensive hedges

The Credit Suisse debacle unfolding quickly on the heels of SVB highlights that when confidence is shaken in one part of the banking sector it can easily spread. All banks, deposit takers, brokers and lending institutions with weak metrics are under the microscope. A liquidity life-line offered by the Swiss National Bank on 16/03/2023 has allayed markets fears for now, but we believe that investors are likely to continue to seek defensive assets in this time of uncertainty.

Either tightening or losing monetary policy could be interpreted as a policy mistake. Gold is there as a hedge.

The European Central Bank (ECB) raised interest rates by 50 basis points on 16/03/2023, marking a bold move given the fragile state of market confidence. However, blended with dovish commentary, markets are expecting less rate rises in the future and believe the 50 bps hike was delivered only because the ECB felt like it had pre-committed and any smaller hike would signal conditions are worse than what the market has priced in. The Euro appreciated against the dollar and the Dollar basket depreciated, providing further support for gold in Dollar terms.

While the jury is out on whether the Federal Reserve will pivot its monetary policy early (note the Federal Open Committee meeting is on 21st and 22nd March), investors are seeking to protect themselves with hard assets. If the Fed doesn’t soften its hawkish stance, it risks transforming a bank liquidity issue into a recession as risk appetite and confidence has been shaken. If the Fed does act either by terminating quantitative tightening or prematurely ending the hike cycle, the central bank’s monetary largess will linger for longer. Either way, gold is likely to benefit. Gold tends to do well in recessions and is seen as the antithesis to central bank created fiat currencies.

Gold gains are well supported

We therefore expect gold to hold onto the past week’s gains in the is time of turbulence. The key short-term risk for gold at this stage is not market confidence recovering quickly, but a broader market meltdown that could drive gold selling to raise liquidity for meeting other obligations (such as margin calls). In that scenario, gold is likely to recover in time as other investors will buy the metal to shore up their defensive hedges.

Sources

1 The FDIC provided more than its usual $250,000 insurance on deposits.

2 The Fed created a new liquidity tool - Bank Term Funding Program (BTFP) - offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral.

GBPUSD Potential Forecast | 17th March 2023Fundamental Backdrop

1. Inflation in GBP continues to be heightened.

2. A lot of instability in the US due to the Silicon Valley Bank crisis triggering a chain reaction to many other banks involved.

Technical Confluences

1. Price has broken the uptrend as seen by the trendline.

2. Price can potentially retrace back to the trendline or the H4 support level at 1.1961 before heading up.

3. Structure has been broken to the upside.

4. Price is resting well above the ichimoku cloud.

Idea

GBPUSD can create a new higher high on the larger timeframe and given the instability surrounding the USD, GBPUSD have potential to continue heading up.

NOT FINANCIAL ADVICE DISCLAIMER

The trading related ideas posted by OlympusLabs are for educational and informational purposes only and should not be considered as financial advice. Trading in financial markets involves a high degree of risk, and individuals should carefully consider their investment objectives, financial situation, and risk tolerance before making any trading decisions based on our ideas.

We are not a licensed financial advisor or professional, and the information we are providing is based on our personal experience and research. We make no guarantees or promises regarding the accuracy, completeness, or reliability of the information provided, and users should do their own research and analysis before making any trades.

Users should be aware that trading involves significant risk, and there is no guarantee of profit. Any trading strategy may result in losses, and individuals should be prepared to accept those risks.

OlympusLabs and its affiliates are not responsible for any losses or damages that may result from the use of our trading related ideas or the information provided on our platform. Users should seek the advice of a licensed financial advisor or professional if they have any doubts or concerns about their investment strategies.

Backfiring BondsTwo financial institutions, Silvergate Capital and Silicon Valley Bank (SVB), collapsed early last week due to a series of ill-fated investment decisions which were exposed by global interest rate tightening. The collapses came after the institutions invested large amounts of capital in long-dated US government bonds, which were considered relatively low risk. However, as interest rates rose rapidly to combat spiralling inflation, bond portfolios started to lose significant value. As a result, when cash demands got high enough, Silvergate and SVB had to sell those backing assets at substantial losses. Silvergate announced a $1 billion loss on the sale of assets in the fourth quarter of last year, while SVB lost $1.8 billion. In both cases, US Treasury bonds comprised large portions of the liquidations. SVB, once the 16th largest bank in the US, then announced a $1.75bn capital raising to plug the hole caused by the sale of its bond portfolio. As one would anticipate, this news resulted in a run on the bank's reserves, and two days later, the bank collapsed, marking the largest bank failure in the US since the global financial crisis. The US government has since guaranteed all deposits of the bank's customers, which has attempted to address concerns of widespread contagion and further runs on other banks' reserves. After the collapse of these institutions, the Federal Reserve announced the Bank Term Funding Program (BTFP), which will provide banks and other depository institutions with emergency loans. However, JPMorgan has since stated this program could inject as much as $2 trillion into the American banking system, which would nullify all hope of inflationary pressures easing.

All of the talk in recent years has been about protecting the banking system from crypto. However, ironically, we had a situation where a digital asset had to be protected from the banking system. The SVB debacle caused USDC to temporarily lose its peg after it was revealed that its issuer, Circle, had $3.3bn wrapped up in a SVB bank account. The stablecoin fell to as low as $0.88 over the weekend before recovering after the US government's deposit guarantee was announced.

These events have highlighted an underappreciated problem with increasing interest rates to reign in inflation. The issuance of new Treasury bonds with higher yields causes the market value of existing bonds with lower yields to decrease. As a result, all banks that hold a significant amount of Treasurys as legally required collateral are vulnerable to the same risk that has affected banks like Silvergate and Silicon Valley Bank. Recently, it looked as if the contagion effects had spread to Swiss banking giant Credit Suisse when their stock began to plummet after questions were raised about the banks' stability. However, since then, the bank has secured a £44.5bn lifeline from the Swiss central bank. The importance of this should not be underestimated. Credit Suisse manages assets in the region of $1.6 trillion. If the bank collapses, it could trigger a domino effect, bringing about a 2008-like crisis.

All in all, it would be ironic if increasing interest rates failed to lower inflation but instead resulted in a number of banks collapsing as a result of their bad bets on treasuries. Despite this market turmoil, yesterday, the European Central Bank stuck to its plan and went with a 50bps rate hike meaning that Credit Suisse may not be out of the woods yet. In recent weeks, the market had been pricing in a 50bps rate hike from the Fed. However, the collapse of SVB and broader risks to the financial system may lead the Fed to raise interest rates by no more than a quarter percentage point next week, with some institutions such as Barclays expecting the Fed to pause all rate increases.

Despite these events, in recent days Bitcoin has significantly outperformed markets. Since the 11th of March, Bitcoin is up over 20% whilst other asset classes are up between 0-2% with 10Y US Yields down around 4%. The key reasons for this most likely come down to the dampening of US CPI data along with the decreased likelihood of future rate hikes as a consequence of the events of the past week. Ironically, while inflation and bank crisis now look more likely, the expectation of more liquidity has provided risk-on assets, such as Bitcoin, bullish momentum.

Australian dollar climbs on strong employment dataThe Australian dollar has taken investors on a roller-coaster ride this week, reflective of the gyrations we're seeing in the financial markets. In the North American session, AUD/USD is trading at 0.6656, up 0.56%.

Australia's employment report for February was stronger than expected. The economy produced 64,600 news jobs, after a decline of 10,900 in January. This beat the estimate of 48,500. What was especially encouraging was that full-time jobs rose by 74,900, with part-time positions declining by 10,300. The unemployment rate fell to 3.5%, its lowest level in almost 50 years, down from 3.7% and below the estimate of 3.6%.

The tightness in the labour market has allowed the RBA to aggressively tighten, with ten straight rate hikes since April 2022. Inflation slowed to 7.4% in January, down from 8.4% in December, so the rate hikes are having an effect on curbing inflation. Still, it will be a long road back to the inflation target of around 2%. The central bank is leaning to taking a pause at the April meeting and leaving the cash rate at 3.60%. Major central banks are moving away from continued tightening and the RBA will have to take that into account, as well as the Silicon Valley Bank crisis which has investors on edge about contagion spreading. Central banks have to be cautious with all the market turmoil, for fear that additional tightening would make a global recession more likely.

Market pricing of rate moves has been gyrating like a yo-yo, and currently there is a 10% chance that the RBA will cut rates by 25 basis points at the April meeting. Just a month ago, the markets expected rates to peak at 4.1% in August. The SVB crisis has completely shifted pricing and the markets are currently expecting rates to fall to 3.35% by August.On

There was more good news as Australian consumer inflation expectations for March ticked lower to 5.0%, down from 5.1% and below the forecast of 5.4%.

AUD/USD is testing support at 0.6639. Below, there is support at 0.6508

0.6713 and 0.6844 are the next resistance lines

Robert Kiyosaki and now Larry Fink on Credit Suisse's demiseThis 2 charts reminds me of a James Bond movie, Skyfall.

There is a claim by many that, these companies are too big to fail. Oh yeah?

7th largest investment bank in the world is get steamrolled. Yesterday about 6pm Malaysia time, Credit Suisse ($CSGN) got halted due to excessive selling.

Robert Kiyosaki predicts this bank will be next. Today, Larry Fink of Blackrock is echoing Rich Dad Poor Dad author.

2nd largest Swiss bank is going under real soon and this will rock Eurozone badly.

On to US banks, Moody's have place 5-6 banks under watch for downgrading due to contagion following SVB, Silvergate and Signature bank's catastrophe.

The pack leader is First Republic Bank ($FRC). Since last week Thurs, already down 80%. Holy moly!

Others will be Western Alliance Bancorp ($WAL), Intrust Financial Corp, UMB Financial Corp ($UMBF), Zion Bancorp ($ZION) and Comerica Inc ($CMA). This year will be crazy.

Will Jerome Powell finally pivot? He got 2 options, raise rates and crush the economy OR pivot and deal with rising inflation again.

What I think is, you will keep printing money. Like you always do and that's all you can do, dear central banks.

Stop covering up simple stuff with euphemism such as Bank Term Funding Program (BTFP) to cover up for money printing.

As if Quantitative Easing is not euphemistic enough.

By Sifu Steve @ XeroAcademy

VIX: MICRO VOLATILITY CYCLES / POINTS OF CONTROL / MACD & RSI DESCRIPTION: In the chart above I have provided a MICRO ANALYSIS of the VIX INDEX which represents volatility in the overall US MARKET. This is a short term play for this week based on micro volatility cycles.

POINTS:

1. Deviation in critical thresholds is 4 points a small adjustment from previous VIX charts published as volatility adheres to this more often.

2. 23 Point serves as critical support for VIX.

3. Current Trend = Symmetrical Triangle Formation 2nd Phase

4. Overlapping Green Dotted Lines = Market Open

5. Overlapping Red Dotted Lines = Market Close

IMO: In my opinion whether or not current setup becomes invalidated I do not see current price action falling below 23 POINTS is the POINT OF CONTROL TO THE DOWNSIDE while 31 POINTS is the POINT OF CONTROL TO THE UPSIDE.

MACD: Current MACD levels continue to fall and are bound to flip into negative territory further confirming current setup that needs some pullback for VIX.

RSI: Current RSI levels are dropping and no current signs of DIVERGENCE that would indicate a sudden flip to positive territory.

SCENARIO #1: VIX price action agrees with current setup & respects symmetrical triangle setup and bounces off 25 in coming session & precedes to the upside to break 29.

SCENARIO #2: VIX price action disagrees with current symmetrical triangle setup and breaks below 25 & faces possible bounce at 23 instead.

FULL CHART LINK:https://www.tradingview.com/chart/UUCv2fGk/

TVC:VIX

AMEX:UVXY