Narayana Hrudayalaya - Strong Fundamental & TechnicalFundamental plus Technical Analysis on a Financially Strong Company:

Narayana Hrudalaya Ltd is engaged in providing economical healthcare services. It has a network of multispecialty and super specialty hospitals spread across multiple locations.

Focus

Company plans to add 700 plus beds for the next 3-4 years at Bangalore Health City. It intends to invest upto Rs. 1,000 Cr in the West Bengal for setting up a superspecialty hospital.

Capex Plan

Company has planned a total capex of 1136 Cr for FY24 and till Q3 FY24 it has spent 477 Cr.

Stock P/E - 31.7

Industry PE - 56.3

EPS growth 5Years - 67.8 %

Buy Score - 4.56 (Buy Score above 0 for me, is considered very good and above 1, excellent.)

ROCE 5Yr - 19.6 %

Please note that this idea is meant to spread awareness and should NOT be considered a buy recommendation. Do your own research before making any financial commitments.

Technofunda

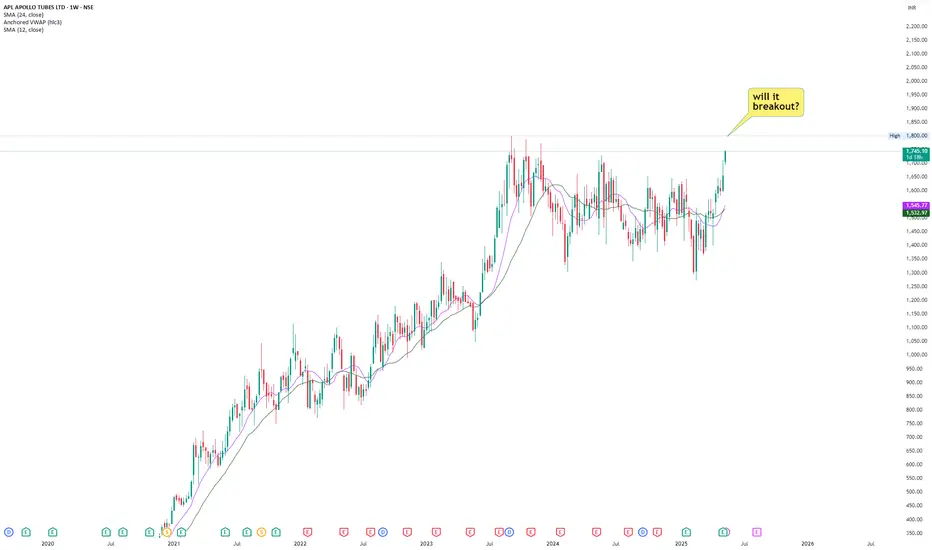

APLAPOLLO- All time high possible!!!APLAPOLLO is nearing its all time high level. Stock is nearing this level with relatively higher volume.

Stock has recorded double digit growth in last consecutive 2 quarters.

Margins have also expanded by roughly 40%.

Company has also expanded its CAPEX budget in coming years.

Overall it's a good technofunda stock to watch. Add to watchlist.

[TechnoFunda]IDFC FIRST BANK – DEEP DIVE INTO MULTI-YEAR SUPPORTTECHNICAL ANALYSIS:

Ascending broadening channel structure

– Since the Aug-20 low (~₹15) price has traced a steady up-sloping trendline, touching in Mar-21, Feb-22 and now Apr-25

– Parallel resistance capped rallies in Feb-18 and Sep-23, defining a ~₹80–100 supply zone

– Channel slope averages ~30% annualized gains from support to resistance

EMA confluence and momentum

– April formed a bullish engulfing candle that closed above the 50 EMA (₹63.8), signalling renewed buyer conviction

Elliott-style wave count

– Wave 1: Aug-20 to Feb-23 advance into channel top (₹100)

– Wave 2: Feb-23 to Apr-25 retrace back to support/200 EMA (₹55)

– Wave 3 (projected): expected to carry price toward channel top again, targeting ₹95–100

Measured-move & targets

– Channel height (~₹85–15 = ₹70) added to support gives a potential target near ₹125 – bullish scenario only on a clean break above channel resistance

– Shorter-term target zone: ₹75 (minor swing highs) → ₹85 (channel midline)

Risk management

– Invalidation: monthly close below ₹55 erodes the uptrend and negates wave-count

– Use a stop 1.5× ATR below the Apr-25 low (₹50) for defined risk

FUNDAMENTAL ANALYSIS:

Revenue & earnings trajectory

– Quarterly revenue up from ~₹40 B in 2020 to ₹113 B in Q1 ’25, reflecting strong loan book growth and fee income diversification

– Net income swung from losses in 2018–19 to a peak of ~₹12 B in 2023, and stays positive at ₹3 B in the latest quarter

Asset-quality improvement

– GNPA ratio down from ~2.2% in 2020 to ~1.3% in Q1 ’25; PCR steadily rising above 75%

– Slippages have trended lower quarter-on-quarter, supporting margin stability

Margin & capital metrics

– Net interest margin at ~4.2%, above industry average, driven by retail and SME lending

– CET-1 ratio comfortably above 13% with Tier-1 capital buffer, enabling healthy credit growth

Valuation & catalysts

– Trades at ~0.4× book value and 10× trailing P/E vs sector averages of 1.5× and 15× respectively

– Potential rerating catalysts: continued NIM expansion, sustained reduction in credit cost, digital customer growth

MACRO & SENTIMENT CONTEXT:

- RBI rate cycle poised for cuts in H2 ’25, which could support credit demand

- Bank Nifty outperforming broader markets; institutional flows have rotated into midcap banks

- Relative strength vs Nifty: RSI on a monthly sits near 50, rising from oversold – room to run before overbought

TRADING PLAN:

- Enter partial long near current price (₹66–70)

- Add on break above ₹75 with conviction

- Targets: ₹75 → ₹85 → ₹95–100 (channel top)

- Stop-loss: ₹50–55 zone (monthly close basis)

- Trail stops above each new swing low to lock in profits as price advances

HEG Limited Stock Analysis [Fundamental+Technical]Company Overview:

Industry: Graphite Electrodes (used in Electric Arc Furnaces for steel production)

Parent Group: LNJ Bhilwara Group

Location: Largest graphite plant at a single location near Bhopal, MP

Global Reach: 67% export-based; presence in 35+ countries

Business Highlights

Products: UHP & HP Graphite Electrodes

Customers: Top 25 global steel companies

Capacity: Increased to 100,000 TPA in Nov 2023

Utilization: 81% (despite global slowdown)

Revenue from Operations: ₹2,394.90 Cr

Net Profit: ₹231.54 Cr (down 49% YoY)

EBITDA: ₹525.63 Cr (down 28% YoY)

EPS: ₹59.99

Net Cash Flow from Operations: ₹615 Cr (up from ₹114 Cr)

ROCE: ~7.2%

Return on Net Worth (RoNW): 5.63%

📈 Technical Insights:

Current Price: ₹474.60

50 EMA: ₹431.44 (support zone)

200 EMA: ₹429.40 (support zone)

Price is trading above both EMAs, indicating a bullish trend reversal.

Golden Cross formation (50 EMA crossing 200 EMA) recently occurred — a classic long-term bullish signal.

The stock bounced from ₹400 zone and now forming higher highs.

Key Strengths

One of the lowest-cost graphite electrode producers globally

Among top 5 global players (ex-China)

Strong relationships with major steelmakers

Backward integrated captive power: 76.5 MW

State-of-the-art technology and high R&D focus

Key Risks

Highly dependent on steel sector demand

Pricing pressure due to global oversupply and China's export surplus

Needle coke (key raw material) cost volatility

Current underutilization of capacity

Growth Triggers

Green Steel Push: EAF-based steel production expected to grow globally

Anode Powder Plant: ₹1,800 Cr investment in 20,000 TPA facility for EV battery anode materials; revenue expected from FY27

India’s EV & Steel Boom: Growing steel consumption (8.2% CAGR) and EV transition are long-term positives

SWOT Summary

Strengths:

Global presence, high export revenue, low-cost structure

Technological leadership

Weaknesses:

Profitability linked closely to global steel demand

Volatility in raw material prices

Opportunities:

EV market and EAF steel expansion

Threats

Competition from China, diversion of raw material to battery sector

Future Outlook

Near-term challenges due to soft steel demand

Medium to long-term outlook is strong, driven by:

Increasing EAF penetration

Global decarbonization policies

Strategic expansion into EV-grade graphite anodes

Analysis Based on Valuation + Chart

CMP:₹474.60

Fair Price Range: ₹600 – ₹1200(Using a conservative P/E range of 10 to 20)

Fair Value (DCF):₹1100+ (Based on 10% projected EPS growth over 5 years and a 12% discount rate.)

Support Levels:₹430 (EMA), ₹400 (price action)

Resistance Zones:₹490-500 (near-term), ₹600 (supply zone)

Disclaimer

The information provided in this report is for educational and informational purposes only and should not be construed as financial or investment advice. While every effort has been made to ensure the accuracy of data and analysis, no guarantees are made regarding future performance. Stock market investments are subject to market risks, including potential loss of capital. Please consult your financial advisor or conduct your own due diligence before making any investment decisions.

NSE:GODFRYPHLP - 🚬 ➕🏪➕🍭 can it create a magicThis evergreen stock from the FMCG Sector listed in India is not just on the verge of a breakout after seven years but also building optionalities that can surprise us on the upside.

👍

✅ Weekly Closing close to 52-Week High

✅ Stock up close to 40% in the last couple of weeks

✅ Verge of the multi-year breakout

✅ FMCG sector

🤞~ Every green sector

🤞- Optionalities - Cloud kitchen (ready to eat)

🤞- Optionalities - Convenience store's growth

👎 💣

❎Promoter's credibility

❎ Sin Stocks

❎ Not in explosive growth

BSE:GODFRYPHLP

39% Lying on the Table in BPCL chartsThe fundamental situation, BPCL is in, I can not see it not going ahead and achieving the 39% technical targets.

Disclaimer: I am holding since 355 and have targets of almost 100% from current levels, i.e. of around 1150.

Trade/ make financial commitments at your own risk. This is to spread awareness and not intended as a buy/sell call. Always, do your own research and/or seek expert financial help.

SUPRAJIT Stock showing momentum with good volume technical showing stock in upward trend 📈 but this is a analysis not a recommendation so always remember Stop 🛑 loss and risk management

This watch-maker company's time has come!The company is an engineering firm engaged in the manufacturing of watch components, precision stamped components and progressive tools for various applications.

• Business is spread across retail and manufacturing of watch components and precision- engineered tools

Key Financials:

• Total Revenue for latest quarter increased ~34% YoY

• Net Profit for latest quarter increased by >67% YoY

• TTM Net Profit margin remained stable at ~5%

Red Flag Check:

• Promoter holding in the company has increased by 1.1% and is at ~51% with insignificant pledging

• Debt:Equity ratio is ~0.5 with ~5.5x interest coverage

• Stock is not under any exchange surveillance lists

Key Technicals:

• Stock has broken out of short term consolidation zone with heavy volumes into all time high territory

• Stock is steadily moving into higher price zones supported by volume

• Stock is showing higher relative strength compared to benchmark index

Disclaimer:

This is for informational purposes only. It is not intended to be a solicitation or an offer to buy or sell any security or instrument or to participate in any particular trading strategy. The views and opinions expressed here are personal. The information contained here has been obtained from sources believed to be reliable but is not necessarily complete, and its accuracy cannot be guaranteed. I may have positions in the securities or instruments shared as ideas. Do your own research OR consult a financial advisor for personalized investment advice.

This specialty packaging co. looks to be moving to Stage 2!The company is a producer of plastic packaging material in the form of multilayer collapsible tubes and laminates used primarily for packaging of toothpaste, personal care, cosmetics, pharmaceuticals, household and industrial products.

• World's largest global specialty packaging company, manufacturing laminated plastic tubes catering to the FMCG and Pharma

space with units in ~10 countries.

Key Financials:

• Total Revenue for latest quarter increased ~13% YoY

• Net Profit for latest quarter increased by >73% YoY

• TTM Net Profit margin increased from ~5% to ~8%

Red Flag Check:

• Promoter holding in the company has almost stayed constant at ~52% with insignificant pledging

• Debt:Equity ratio is <0.5 with ~5x interest coverage

• Stock is not under any exchange surveillance lists

Key Technicals:

• Stock has broken out of 1-year stage 1 consolidation zone with heavy volumes

• Stock has broken out of a cup-and-handle formation

• Stock is showing higher relative strength compared to benchmark index

Disclaimer:

This is for informational purposes only. It is not intended to be a solicitation or an offer to buy or sell any security or instrument or to participate in any particular trading strategy. The views and opinions expressed here are personal. The information contained here has been obtained from sources believed to be reliable but is not necessarily complete, and its accuracy cannot be guaranteed. I may have positions in the securities or instruments shared as ideas. Do your own research OR consult a financial advisor for personalized investment advice.

This auto components company is in the breakout zone!The company has over 6 decades of experience in auto components manufacturing

• Business is diversified across Two Wheelers, PVs, CVs Off-Highway and Farm Equipments

• Also supplies to Major EV OEM’s globally

• Has diversified Product Portfolio – Gasket & Heat Shields, Forgings, Suspension Systems, Anti-vibration Products & Hoses

Key Financials:

• Total Revenue for latest quarter increased ~18% YoY

• Net Profit for latest quarter increased by >34% YoY

• TTM Net Profit margin increased from ~16% to ~17%

Red Flag Check:

• Promoter holding is decent at almost ~58%

• Debt:Equity is good at about 0.27 with sufficient interest coverage of ~7x

• Stock is not in any of the exchange surveillance lists

Key Technicals:

• Price is in a steady uptrend and has broken out of a cup and handle formation with heavy volumes

• Strong relative strength compared to benchmark index

• Price is nearing its all-time high zone

Disclaimer:

This is for informational purposes only. It is not intended to be a solicitation or an offer to buy or sell any security or instrument or to participate in any particular trading strategy. The views and opinions expressed here are personal. The information contained here has been obtained from sources believed to be reliable but is not necessarily complete, and its accuracy cannot be guaranteed. I may have positions in the securities or instruments shared as ideas. Do your own research OR consult a financial advisor for personalized investment advice.

This PPE and safety equipment manufacturer is nearing ATH!The company is one of the largest manufacturers and distributors of PPE products in India, with 90%+ orders coming from repeat customers, and provides the widest range of head-to-toe PPE products from helmets, eyewear, ear protection, face masks, safety garments, and gloves, to shoes, etc.

• Company has posted highest ever turnover and PAT in latest quarter

• Company is re-investing profits in fixed assets for future growth

Key Financials:

• Total Revenue for latest quarter increased ~9% YoY

• Net Profit for latest quarter increased by >46% YoY

• TTM Net Profit margin increased from ~8% to ~10%

Red Flag Check:

• Promoter holding is pretty high at almost ~75%

• Debt:Equity is not a concern with decent interest coverage

• Stock is not in any of the exchange surveillance lists

Key Technicals:

• Price is in a steady uptrend and looks to breach its listing week high

• Strong relative strength compared to benchmark index

• Price broke out of a small consolidation zone with heavy volumes

Disclaimer:

This is for informational purposes only. It is not intended to be a solicitation or an offer to buy or sell any security or instrument or to participate in any particular trading strategy. The views and opinions expressed here are personal. The information contained here has been obtained from sources believed to be reliable but is not necessarily complete, and its accuracy cannot be guaranteed. I may have positions in the securities or instruments shared as ideas. Do your own research OR consult a financial advisor for personalized investment advice.

Ismt Ltd ISMT manufactures seamless tubes ranging from an outer diameter of 6 mm to 273 mm for a wide variety of applications. Typical uses include:

Stabilizer bars

Air bag canisters

Front wheel drive shafts

Anti-roll bars

Piston pins

Collapsible steering columns

Steering linkages

Transmission shafts or Propeller shafts

Trailer axles

Stub axles

Gear shafts

Common rails (Diesel engines)

Clutch parts

CV cages

Now it can break it's upper trendline and can head for 70rs tgt wait for breakout

Ask your financial advisor before buying

Only for educational purposes

USDCHF short ideagiven the fact that SNB Policy Rate release was slightly higher than last month's.

this is the short scenario I consider to USDCHF

(ONSE:RHIM) RHI Magnestia India Capital Cycle Play?RHIMagnestia India ltd earlier known as Orient Refractories Limited (ORL) is in the business of manufacturing and marketing special refractory products, systems

and services to the steel industry in India and Globally. It is a market leader for special refractories in India and has many global customers for its international quality products.

KEY POINTS

Revenue Breakup

Presently, the company earns 74% of its revenues from manufacturing of refractories and 22% from trading of refractory items.

Dependent Industries

Demand for refractory is primarily dependent on steel industry, which accounts for 75% of total sales. Refractory products are also used glass, cement, non-ferrous, petrochemicals, etc.

Manufacturing Facilities

The company has 2 manufacturing facilities located in Bhiwadi, Rajasthan and Tangi, Odisha for its manufacutring operations.

Capacity Expansion & Investment

In FY20, The company purchased certain assets of Manishri Refractories & Ceramics Pvt Ltd's plant situated at Cuttack, Odisha for ~44 crores. The plant has capacity of 10,000 tonnes of MGU bricks which will be increased to 18,000 tonnes post capex.

It also acquired 100% stake in Intermetal Engineers India Pvt Ltd for 10 crores for manufacturing of steel plant equipments which are exported to its customers in Gulf and African Region and caters to 400 plant customers in India.

Merger Scheme

The company proposed a merger scheme to merge RHIIndia and RHIClasil (promoter group entities) with the company.

The merger would issue ~4 crore equity shares to the shareholders of RHIIndia and RHIClasil which would have increased the equity capital of the company to 16 crores.

The scheme was rejected by the NCLT in March 2020. However, the NCLAT directed NCLT to approve the scheme without any delays January, 2021.

Acquisition by RHIMagnesita

RHIMagnesita acquired 43.6% stake in the company from the core shareholders in March, 2013.

It further acquired 26% stake through an open offer in April 2013.

RHIMagnesita is a global leader in refractories with largest number of manufacturing locations around the world.

Disc: Not invested as yet , might add a tracking position next week.

NSE: AMBIKCO - Doubler already 💪 - Next Target Updated chartsNSE:AMBIKCO

sharing updating chart in quick video

please refer to my old updates , posted here.

Nasdaq:RBLX-Roblox Corporation - Let's play some game???Been tracking this stock for some time ..

Now time to take some entry

Share my details as blog beofe

Disc: Not invested, will next week as first trance or tracking position.

ADA/USDT Fibonacci As u see in the chart We Are in 0.618 Fib-Retraces and expected To Move on Above 1.9 Again

In the second Place Hawskinson Is going To help Musk For Upgrading and coding the elements Of doge

So iT would be a Good chance To have This

Private Blockchain Coin In ur basket For A short time

Buy IG Petrochemical : CMP 765, CBSL 679, Targets 820-840-860

* Swing Trading

* Flag Breakout

* Fundamentally good Company

* Highest Monthly Close

* Good Volumes