Aemulus Turtle Strategy BOB Type 2 + BOD Type 1MYX:AEMULUS

Resistance turn Support

Fast Turtle Buy

FiFT BOD

MCDX + Banker 38%

Atom Turn Green

Technology

ELSOFT Turtle BOD Type 1 StrategyMYX:ELSOFT

Fast Turtle Buy

FiFT BOD Star

Banker 39%

Atom turn green

Microsoft - $400 2021 Price TargetAt the time of this post:

$AMZN | $3,479

$GOOG | $2,916

$TEAM | $371

$MSFT | $301

Facebook Ponzied - Algorithms for Profits - Large Cap Stonks*valuation matters in *rising rates environment.

The echochamber is closing for good. Bad for advertising revenues. Poggers. Libra coin #feevulture #failarmy

Amazon Ponzied - Made in China - Small Biz Killer*valuation matters in *rising rates environment. Go small caps!! #MSOgang

Large cap stonks & crypto Ponzi Pogs collapse.

Apple Ponzied - Made in China - Ponzi Pogs & StonksHold for Broke. *valuations matter in *rising rates environment.

Google Ponzied - Algorithm Crackdown - Ponzi Pogs"only buys fam". The chants of neverending gluttony. #echochambers in the #metaverse.

Algorithms get busted. HODL ponzi pogs & stonks for broke. *valuation matters

Go Small Caps!! #MSOgang #cannabisreform Jobs & Justice!!!!!!

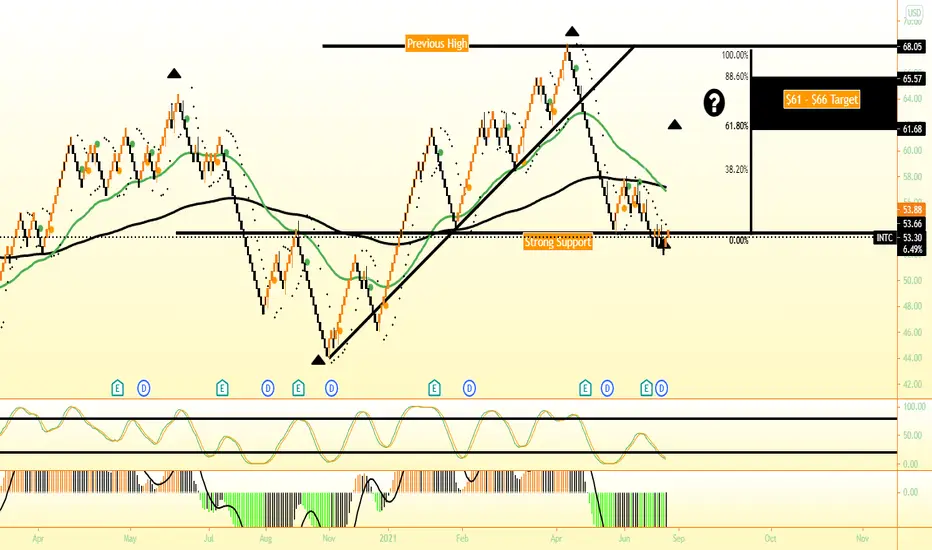

Intel Corp.Company Description:

Intel Corporation is one of the world's largest semiconductor chip maker. The Company develops advanced integrated digital technology products, primarily integrated circuits, for industries such as computing and communications. It also develops platforms, which it defines as integrated suites of digital computing technologies that are designed and configured to work together to provide an optimized user computing solution compared to components that are used separately. Intel designs and manufactures computing and communications components, such as microprocessors, chipsets, motherboards, and wireless and wired connectivity products, as well as platforms that incorporate these components. The Company sells its products primarily to original equipment manufacturers, original design manufacturers, PC and network communications products users, and other manufacturers of industrial and communications equipment. Intel Corporation is based in Santa Clara, California.

Analysis:

When taking a look at the 4 hour chart, I see a few indicators that give me bullish sentiment:

1. Candles near strong support.

2. RSI Oversold.

3. Mac D on it's down side.

4. High before the most recent previous high was broken.

5. 200/50 EMA Cross w/ 2 Orange Renkos.

Looking for a price target of $57 and up! Not Financial Advice. Always Do Research Before Decision!

GM - The Tesla Crusher - EV Push - Valuation & Sales*rising rates environment will smash the Dogefathers Ponzi Pogs. Forward P/E is a NOGO from now on. *valuation & PROFITS NOW matter most.

I'd enter with a 50% stack. DCA if need be. I doubt you get a chance at anything meaningful. The chip play for EVs and others.

#checkmate STORYTELLERS

#investingnfts

Go Small Cap Gems!

VMWARE MONTHLY AMAZING HEAD AND SHOULDERSVMware, Inc. is an American cloud computing and virtualization technology company headquartered in California. VMware was the first commercially successful company to virtualize the x86 architecture. Excellent bullish break of a head and shoulders on a monthly timeframe that can be used as an entry point on this asset.

CSCO Log Chart AnalysisGood reclaim of important monthly level, I'd prefer to see a nice retrace back to 57s but the opportunity cost may outweigh the better entry. We're entering peak euphoria ranges from the internet bubble... if we escape this range, north of $82 the fun really starts. All time highs are a mere 40% away, with 50%+ upside from there.

Take profit levels marked using fib retracement of the internet bubble top and bottom. I expect this to run from this spot, good R:R with scaled stops under the monthly level.

Considering this analysis was done at high time frame, it may take a while to play out. Below 53.41, I think this trade is invalidated.

AMAT running out of steamNASDAQ:AMAT has been seriously testing its dynamic support through last weeks earnings report, but has not yet posted a full daily candle beneath. Still, that support has been functionally invalidated by 4 successive candles poking through. In my opinion, a new technical structure is therefore forming. How price action respects the MA200 and/or key supports in the 115-120 range will help define the new channel and pattern.

The largest potential drop (excluding external catalysts) could be to the 118 level, i.e. at the confluence of the MA200 and 19MAY low.

Longer term, NASDAQ:AMAT will continue to post blowout earnings, which should lead to new ATH in late 2021/early 2022. In the meantime, we may see it continuing to trade on the lower side of FMV with a weak upward trend.

Salesforce Ponzied - Double Top - Large Cap Stonksvaluation matters. Seems to have caught the $doge buzz. Buy Buy Buy. lol

NO.

Profit TODAY matters most in *rising rates environment.

McDonalds Ponzied - Rising Rates Environment - Volume MIAAlways up. Buys only. Bla Bla. The MCD in our town just upgraded to a double lane drive thru. Is that a clue? Large caps gobbled up all the smalls. I liked our mom n pops too. Shame. MCD ate them all. So sad. Time to pay their fair share! Corporate tax rates will get the hike they deserve.

*Revenues from abroad. Shipped from abroad. Expenses abroad. wow. Milkshakes on backorder from where??? Shame.

Large cap Stonks. Hold for broke in a rising rate environment.

Go small Caps!! #MSOgang

$GOGO: 33% Short Interest Heading Into Holiday Season$GOGO getting a pop today one day after the White House announced mask mandates through the holiday season, should we buy the news or will this be a holiday humbug?

Bursa Technology Index predicts to Rally if able to break ATHBursa Tech Index shown a good example of compliance to Fibo Extension.

2nd High/ATH is at Fibo extension of 1.618 and retrace to Lower High. this HL is well supported (2x double bottom)

If the index break 93.9 (ATH) - Technology Index and its counters should rally together with Bursa Index.

Observer the STO cross, which shows an early rally indicator.

Ford Lightning - Upcoming Best EV Sellers - Prove it!EVS have been hyped forever now. Lets see if Ford's supply chain can hold up and beat out the goofy Ponzied Cyber Truck. Gross. Anyway.... everything rally is up. Find quality with profits TODAY, not 20 years from now!

*valuation matters

NOMO FOMO

Stop Pogging! Learn to Invest. You'll do great.

Growing Stocks to Watch in the Chinese Market: (WIMI:NASDAQ)The regulatory and other uncertainties in the Chinese market directly impact sectors like fintech, gaming, and education. Winners will be companies that have benefited from the regulatory change or captured the newly emerging opportunities.

WiMi Hologram Cloud (WIMI:NASDAQ)

WiMi Hologram Cloud is one of China's top holographic Cloud technical solution providers that focuses on AR automotive HUD software, 3D holographic pulse LiDAR and holographic microelectronics. Frost & Sullivan, for instance, described WiMi's holographic AR application platform as one covering the most comprehensive set of AR products in China.

WiMi reported a 140% year-over-year increase in revenue from CNY 319 million in 2019 to CNY 766 million in 2020. The net income before the impact of stock compensation expenses was CNY 40.3 million in 2020, presenting a decreasing trend mainly due to a 362.8% increase in R&D expenditure.

Also, with the increasing application solutions demand on the 3D vision-related semiconductors, WiMi broke into the market. WiMi's 56% of the 2020 revenue was contributed by its semiconductor business, which was just launched in July of that year. Along with the rise in the Chinese semiconductor industry that is vigorously supported by the state, the business is going to build a new growth curve for WiMi.

For the full article with the charts, please visit the original link.

Nvidia - Double Top - Large Cap Stonks - Rising RatesAlways overbought. Run! *valuation matters

Great company though.

$ARKK: Cathie vs Burry, Which Side Will You Choose?The 120 level on ARKK continues to act as a very prominent level. What would you do?

ARKK 120 features a prominent low volume node and now we have a chance to meet this level with the falling trendline that starts from the Feb high to the June 2021 lower high. Together these forces will meet and ultimately decision in the coming weeks. I'll let time tell me which way I'll play this one but will the Russell 2000 be a canary in the coal mine or will it successfully squeeze bears like it's been known to do. You may also look to the Fed and forex markets to see how the dollars role may play apart. Good luck traders!