Time to buy short duration treasury bonds?The Fed funds rate is higher than the 30 year treasury interest rate.

The last time that happened was in 2000 and 2008.

What happened back then was that the stock market and the 2 year treasury interest rate both dropped significantly.

Will history repeat itself?

Treasuryyield

US inflation - US treasury Rate compared with the seventiesHi All

This fraction of seventies is already for 1 year identical.

US inflation rate minus US treasury rate

230112- Relation (1) interest rate, (2) Treasury Yield, (3) oil U.S. INTEREST RATES vs TREASURY YIELD vs OIL PRICE

Timeframe: 1 month. start: 1972

Blue line: interest rates (USINT)

Orange area: 10-year U.S. Treasury Bond Yield (IRLTLT01USM156N)

Green Line: oil (scale on the left)

(A) WHEN INTEREST RATES ARE ABOVE BOND YIELD,

(1) it sparks a financial crisis: 1990, 2000, 2008, 2019

(2) it is followed by a spike in oil price.

(3) on smaller timescale, oil price rises and falls with increases and decreases in Treasury Yields.

(B) OBSERVATIONS ON INTEREST RATE:

(1) Interest Rates have been falling since 1980

(2) Treasury Yields have been declining since 1980

(3) It appears, the Federal Reserves strives for a 5% interest rate. It drops interest rates FAST when the market is too hot, and builds up slowly again, attempting to meat the 5% arbitrary target.

(4) As time goes on the Federal Reserve is more cautious in raising interest rates.

BUT MOST RECENT RAISES IN INTEREST RATE ARE ALL BUT SLOW.

s3.tradingview.com

T10-2Y Treasury Yield - Monthly ChartI tried to predict Treasury yield cycle using Trent lines.

I would like to see if the treasury yield follow the cycle along the trend lines.

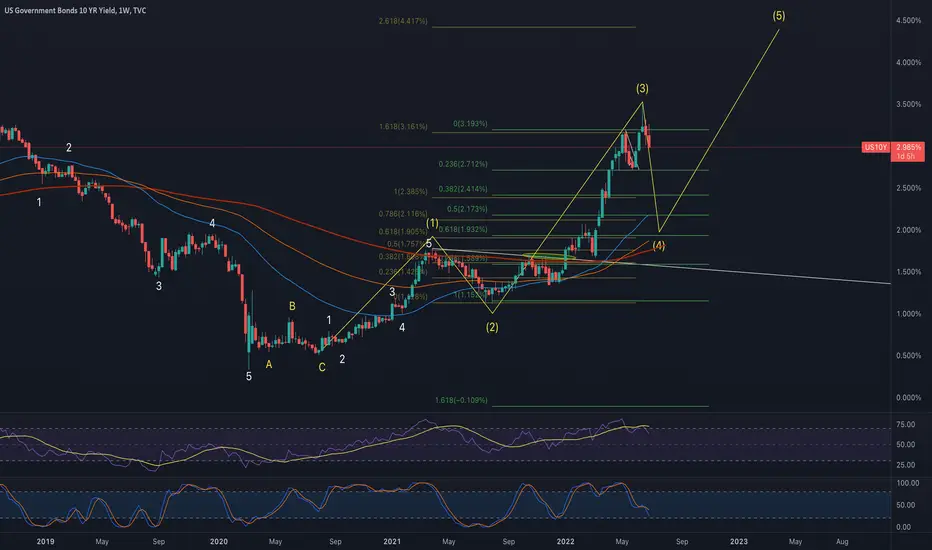

long short term bonds bullish cypher forming elliott wave 4-5looking at short term bonds over the next 3-4yrs and take the monthly dividend. From the 4th Elliott wave to the 5th, then I'll likely convert over to the 20yr treasury in 2years to try to buy the D leg of the cypher pattern on the 20yr. see charts. In this chart, notice how the price action retrace back to the 3rd wave, this movement was a very big bearish cypher pattern... I'm a buyer of the dips

Treasuries accelerating their decline from oversold conditionsTreasuries accelerating their decline today free falling from already historic oversold conditions on multiple time-frames.

Feels pretty broken to me, but that doesn't mean we can't break further.

On watch for a true dislocation/break down/panic on further weakness.

10 year notes broke out of the bullish wedge as expected10 year notes broke out of the bullish wedge as expected.

Bulls have a setup for a large five wave up rally in T-notes (meaning decline in 10 year yield)

Bonds Rise On WeeklyMonthly chart looks like we are topping on the US10Y. Weekly chart tells a different story. I believe the Weekly US10Y is telling us that fed is going to have to be more hawkish with interest rates on 21st September. We will see if i am right.

Why Corporate Bonds are not a good option for Retail InvestorsCorporate bonds or tradeable debt instruments issued by corporations are a type of fixed income security. Given the recent media attention and the rising demand for fixed income investments among retail investors, it may come as a surprise that they are not suitable for all investors. Corporate bonds have different risks associated with them than other fixed income investments like savings accounts, money market funds, and even municipal bonds. If you are considering investing in corporate bonds or are already holding some in your portfolio, here is why you should avoid them as a retail investor

What is a Corporate Bond?

A corporate bond is a debt instrument issued by a corporation to raise money. Corporate bonds typically have a set maturity date after which the outstanding principal will be repaid. There are many kinds of corporate bonds, including investment grade and high yield, government and non-government, and they can be issued in local or foreign currencies. Corporate bonds are often traded on the secondary market, which means they are liquid and can be bought and sold easily. Investors earn a return on corporate bonds by receiving interest payments and by the increase in the bond’s value as it matures. The interest rate on a corporate bond is based on factors like the company’s credit rating, the length of time the bond is outstanding, and the bond yield in the market at that time. Corporate bonds are typically less liquid than stocks, and may have shorter holding periods, especially if you purchase them on the secondary market.

Risks of investing in Corporate Bonds

Corporate bonds are considered a form of debt financing, and as such, there are risks associated with holding them. The main ones are default, liquidity, and interest rate risk. - Default risk - Investing in corporate bonds entails the risk that the issuing company will default on the payment of interest or the repayment of principal. However, since corporate bonds are issued by companies in different industries, there is a low probability that they will all default at the same time. - Liquidity risk - The risk that you will not be able to sell the investment in a timely fashion at a price that is attractive to you. - Interest rate risk - The risk that if you hold the investment until maturity, you will earn a lower rate of return because interest rates will have risen in the meantime.

Why you should avoid Corporate Bonds as a Retail Investor

While corporate bonds may be suitable for institutional investors, they are not a good option for the average retail investor. For one, you will have to educate yourself on the various types of corporate bonds, their risks and returns, and what kind of companies you should be investing in. Even if you are successful at taking this on, you are likely to end up with a very concentrated portfolio, which brings us to the next problem. The other issue is that retail investors typically hold a small number of bonds and these bonds are often concentrated in a few issuers. This is not a good strategy because if a company defaults, you could lose a large portion of your capital. This is clearly a bad strategy.

So, How about Investment grade debt ETFs?

LQD, In a rising interest-rate scenario. The bonds' tenure is clearly working against them, especially since unemployment continues to fall at an astonishing rate. This is not the time to invest in this ETF if the Fed raises interest rates to combat inflation.

In order to completely comprehend this analysis we must know how important the duration is, while investing in bonds.

Duration is an important topic. It is the bond's effective maturity, which means it is oriented to something lesser than the time of the bond's final payment since part of the bond's value, generally from coupons, happens earlier in the bond's existence. If a bond has a longer effective maturity at a fixed interest rate, it indicates that investors are tied to an interest rate that was once market for a longer period of time, and if rates increase as they are currently, you will be bound to an uneconomical rate for a longer period of time. Simply put, longer term bonds lose value more severely when interest rates increase.

How maturity of a these bonds (Duration) is affecting LQD

Unemployment has gone down despite the increased rates, which has surprised many analysts. The Phillips Curve is back in force, where low unemployment yields high inflation if inflation is kept down, and contrary to common perception, Consumer spending has declined, but unemployment is so low that it might rise again unless the Federal Reserve, which is committed to lowering inflation, continues its anti-inflation campaign. The Federal Reserve has raised rates as well as given gloomy recession predictions, and more banks are following its lead, including the Bank of England. LQD, which has dropped 14% this year, have long-duration bonds, majority of fixed-rate, which is concering for this ETF.

Credit Spread

Global Cooperate Bonds in general

Corporate bonds continuing their strong performance in July, producing $80 million (+76% year on year). July was the most profitable month of the year for CBs . Their revenues in 2022 have exceeded from 2021 ($512 million). Average balances increased by 9.8% year on year, average costs increased by 59% year on year, and usage have increased by 27% year on year. Spreads on non-investment grade and high yield bonds continue to widen as corporate prospects deteriorate owing to weakening consumer demand and stricter financial conditions. In-turns , asset values fall, yields rises, and borrower demand increases. However, CG Debt funds have seen the highest monthly outflows in May and June (-$73.7 billion)

In July, High Yield Bonds enjoyed the relieve rally.

Interest rates vs Corporate Bonds comparison

Alternatives to Corporate Bonds for retail investors

For retail investors, the most advisable option is to go with government bonds. Government bonds have historically offered a lower risk profile compared to corporate bonds. The best way to go about investing in government bonds is to go for a diversified bond fund. Using a bond fund reduces the risk associated with investing in bonds further as the fund manager may hold a large number of different bonds. If you are looking at a short-term investment horizon (less than 10 years), then you could also opt for short-term government bonds. If you have a long-term horizon, then you could consider a long-term government bond fund. Savings accounts, money market funds, and short-term government bonds are very liquid forms of low risk investment options.

Conclusion

It is important to understand that the corporate bond market is not risk-free. When interest rates are rising, corporate bonds are generally falling in price as they are competing against government bonds with lower interest rates. In times of economic uncertainty or when interest rates are rising, the risk of default is generally higher for companies issuing corporate bonds. Thus, it is advisable to invest in corporate bonds only when the economy is growing steadily. For retail investors, the best options are to go with government bonds or short-term government bonds. These are low risk, liquid investments and will help you achieve your financial goals.

Intensified recession mood as US bond yield curve remains invertEUR/USD 🔼

GBP/USD 🔼

AUD/USD 🔼

USD/CAD 🔽

XAU 🔽

WTI 🔼

Almost three weeks of an inverted US bond yield curve has led investors all but confirm the recession, and sluggish GDP data on Thursday could be the nail in the coffin. The latest price to yield readings of the two- and ten-year Treasury notes were at 3.0081 and 2.785, respectively, which remained inverted since 6 July.

Meanwhile, major currencies have retrieved lost ground against the greenback. EUR/USD has a minor uptick to 1.022, despite Monday's Germany IFO business climate index declining to 88.6, falling short of the 90.2 forecasts. GBP/USD returned above the 1.2000 level to close at 1.2042.

AUD/USD rose and stabilized at 0.6950 level, reaching a closing price of 0.6953. The Australia Consumer Price Index will be available on Wednesday morning to reveal recent price level changes. USD/CAD slumped to 1.2848, after slowing at the 1.2850 level.

The jury is still out on gold being the proper hedge option for the possible recession, gold futures retreated from a high of 1,733.3 to 1,719.1. WTI oil futures gained $2 to $96.7 a barrel, lower than expected gas demand in the ongoing US driving season has eased the supply shock impacts.

More information on Mitrade website.

10-Year Treasury Yield Trendline Breakout Faces Next TestThe 10-year Treasury yield confirmed a breakout under a near-term rising trendline from March, opening the door to reversing the uptrend since then.

Rising concerns about a recession in the United States, also amid a general slowdown in global growth expectations, are pressuring bond yields lower.

Ahead, the 10-year rate is facing the May low at 2.705 where the 100-day Simple Moving Average is fast approaching. The latter could still reinstate the dominant upside focus.

Otherwise, more pain may be in store. Below is the 61.8% Fibonacci extension at 2.3667. Resuming the uptrend entails a push back above the current 2022 high at 3.497.

TVC:US10Y

10 yr My W4 on weekly HTF chart is looking likely. If the Fed & ECB are in the debt market trying to stabilize the system via repo swaps then this dump is going to be a normalization process and the markets will chop around in some f**ked up range until W4 is complete around 1.9%-2.2% during this normalization period bullish momo will fizzle out and bears will short all pumps and win , but the greedy bears will get squeezed as all big dumps in markets will get bought up quick and change the direction b4 most traders know what even happened. I suggest only buying your core positions until w4 is finally done projected to finish July-Sept 2022. This would be a good move for the patient investors here to hold and add because once the W4 finishes and markets stabilize (if the fed pivots like I am saying above) W5 will line up on the 10 yr with W5 for stocks & crypto. Conversely If W4 becomes a fear trade (inflation narrative grows momo, war in Ukraine gets worst possibly nuclear war, china invades Taiwan or anything else unforeseeable) then W4 will decimate markets and 3200 SP500 is possible and $12K BTC.

10 year We must see how the markets react to this dump to the 10 yr, my gut thinks this could be a fear trade which causes money to leave risk and head into USA gov bonds. I would assume that at some point around 2.4% (618% golden ratio) a bottom will be found and the inflation narrative will be silenced for at least some time while Oil has a decent pull back to $60. Then the W5 will kick in and maybe intitially seem bullish while rates climb in a structured manor till around 3% or 3.2%. After rates hit that level inflation may start to appear again in the MSM. Once w5 really kicks in and heads towards 3.5%-4% plus this will likely be the debt market melt down. So watching DXY, stocks and crypto how this all plays out

New Zealand dollar sliding, GDP nextNZD/USD has extended its losses today. In the North American session, NZD/USD is trading at 0.6222, down 0.59% on the day.

The New Zealand dollar continues to fall, and fast. The currency has slumped 1.93% this week and is trading just above 0.6216, a 2-year low.

There is plenty of hand-wringing ahead of the FOMC meeting on Wednesday, as the financial markets nervously await the next rate increase. The meeting is live, with the Fed most likely to raise rates by 0.50% for a second straight meeting. However, there are voices calling for a massive 0.75% hike, notably, the chief economist at Goldman Sachs. It would be a shock if the Fed delivered a 0.75% increase, given the turbulent economic environment. The recent US inflation report shows inflation continues to accelerate, raising doubts that an aggressive Fed can guide the economy to a soft landing and the inversion of US Treasury yields is adding to these concerns. A 0.75% salvo from the Fed could lead to a sharp backlash from the markets, which the Fed will be keen to avoid.

The US dollar enjoyed a spectacular day on Monday against most major currencies, and the dollar index surged above resistance at 105. US 10-year yields rose as high as 3.38% earlier in the day, and the upward movement continues to support the US dollar. Risk-correlated currencies like the New Zealand dollar were pummelled, with NZD/USD falling by 1.49%.

New Zealand releases first-quarter GDP later today, with the markets bracing for a modest gain of 0.6% QoQ. This follows a 3.0% gain in Q4. The Reserve Bank of New Zealand will be keeping a close eye on the strength of economy, as the Bank tries to steer the economy to a soft landing while raising interest rates.

NZD/USD is testing support at 0.6244. Below, there is support at 0.6099

There is resistance at 0.6288 and 0.6413

#TNX #US10Y 10 year yield at a top?So the 10 year yield has run hard on interest rate hike expectations.

However, as can be seen from the chart, the yield is currently about 93% above its 50 month moving average, the highest it has ever been...by far.

Using the TD indicator one can also see that the yields are potentially topping this month.

As can be seen from the Stochastic and RSI below, both are at major tops.

The yields and DXY priced in a more hawkish FED the last couple of days since we got the higher than expected CPI reading on 10 June.

Chances are that the FED will not be able to continue with higher interest rate hikes as this will crash the market.

So, the yields and DXY might have been running based on expectations but might revert quite a bit on actual release of FED interest rate decisions tomorrow.

10 year treasury yieldspotential double top around 3.23% on 10 year treasury rate, coincides with resistance of multi decade down trend (yellow). on a logarithmic price chart.. or do we break out of a multi decade trend and see rates go higher? even if we did break out, could the Fed respond with YCC to stop long end rates going up, which could break the financial system..? thoughts and comments welcome.

T10Y2Y Yield curve inversion potential crucial pointWhenever this chart crosses 0 it means the yield curve for the 2 and 10 year bond yields has inverted. Historically a significant economic downturn followed. It's not perfect but nonetheless I wanted to put this out there for feedback.

Thanks

Other countries' wars are good for US interest ratesWhen a nation with a safe-haven currency uses other nations as war proxies, where do you think the money will flow?

30Y Fixed Mortgage Rates (US Avg.) vs 30Y Treasury RateTop section is average 30-year fixed mortgage rates minus US 30Y treasury, and the bottom is them separated. Average US mortgage rates (blue) started to move ahead of treasury rate and expect 30Y treasury to move above 3% this year

Aussie rises ahead of key employment dataThe Australian dollar has reversed directions and pushed above the 72 line. In the North American session, AUD/USD is trading at 0.7224, up 0.54% on the day.

Australia will release December employment numbers in Thursday's Asian session. The economy is expected to have created 43 thousand new jobs, which would be a modest gain compared to the monster spike of 366 thousand in November. The market is also projecting that the unemployment rate will tick lower to 4.5%, from the 4.6% beforehand. A strong release would likely give a boost to the Australian dollar.

Earlier today, Australia's Westpac Consumer Sentiment for January disappointed with a reading of -2.0%, marking a second straight decline. Consumers are wary that the spike in Omicron cases could trigger further lockdowns. The number of hospital cases has swelled and on Tuesday, Australia recorded 77 deaths from Covid, the highest one-day total since the pandemic began.

An ANZ report last week noted that the Australian consumer is suffering from an "Omicron malaise in spending" and that could mean trouble for the Australian economy, as consumer spending is a key driver of growth. The major banks are planning to revise downward their growth forecasts and Commbank has already lowered its Q1 forecast QoQ from 2.3% to just 1.0%.

In the US, there are growing concerns that the Federal Reserve will accelerate the tightening of its policy. This has been reflected in an upswing in US Treasury yields. The 10-year rate climbed above 1.80% on Tuesday, a 2-year high, and hit 1.90% earlier today, but has retreated to 1.83%. The 10-year rate hasn't been above the symbolic 2% level since July 2019 but could reach that line shortly. Most analysts are projecting three or four rate hikes in 2022, but the Fed may have more in store - Jamie Dimon, CEO of JP Morgan, made headlines last week when he projected the Fed could hike up to six or seven times this year.

There is resistance at 0.7304 and 0.7392

AUD/USD has support at 0.7139 and 0.7062

US treasury yields yeeting, decoupling from btcTreasury yields have followed btc for the first time this whole cycle compared to previous cycles, but now with them mooning, are they decoupling or is this a sign of things to come for btc, especially if dxy continues to plummet which it most likely will as the Fed does what the Fed does?

Yield will hit above 2% in couple of weeksMomentum: Stochastic still goes up

Pattern: Inverted Head and Shoulder

Price: 2.03%

Time: Q1 - Q2 2022

10-YEAR YIELD ANALOGUEPossible analogue from the lead up to the last financial crisis. Potential catalysts still taking shape. Continued central bank NIRP would support this scenario.