UBER - Use it, don't own it!The charting is difficult for the fledglings, but all of the same. The volume has dropped off a cliff at a new high. Generally not a good sign. I like the service, but it makes no money.

Uber

Uber buy or sell?MMHVW - this is a classic chart showing the second day of Uber going public. They may have picked the wrong time to go public. Wouldn’t it be nice pick up some in single digits?

UBER Move coming, ST Bottom within rangeLooking for Uber to push higher to the top of this range it's currently defining. New indicator I'm using here and there shows a bottom detected earlier today and some strength on the intraday at close.

Hoping we push above the Green line and on to $45.30 area. Still enjoying Uber price movement, IPOs are hard to predict but IP and Ubers expansion into other related industries makes me believe in them LT over other companies like LYFT.

Financials need to catch up to hype and current values but that obviously takes time. Hoping for more PT upgrades before next earnings.

GLTA

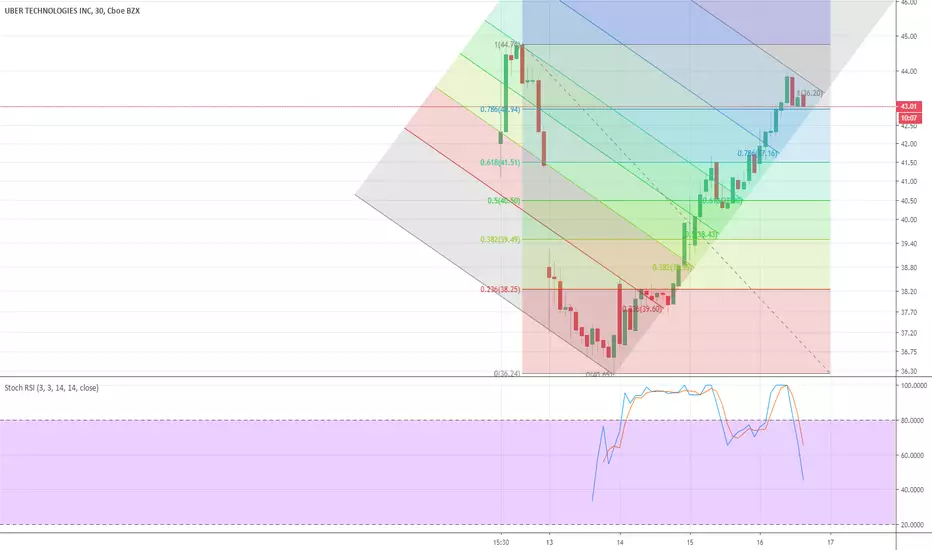

Transportation Clones / LevelsIn name and concept; clones

some people refer to fib levels colloquially as clones as well!

enjoy

manage your own risk

much love

gl hf

xoxo

snoop

Uber ready for a Lyft tomorrow?Not financial advice. I’m not a financial advisor. I’m learning to trade. Learn to trade!

Still on course for a possible breakout of a possible ASC TRI

Lyft breaking important resistance (intraday)If LYFT can stay today above the $63. I would expect it to go higher.

If the candlestick today has a wick on its top (breaking through this $63). I see potentially heavy winds for the stock.

Bitcoin storming highs, ECB warns, & Fed preparesThe BTC cryptocurrency rate for the first time since May 2018 exceeded its highest level. The information Facebook Inc. has signed up more than a dozen companies including Visa Inc., Mastercard Inc., PayPal Holdings Inc., and Uber Technologies Inc. to back the new cryptocurrency that the social-media giant plans to unveil next week and launch next year.

We consider the cryptocurrency market reaction as inadequate and irrelevant to the importance of the event. Well, the news looks impressive, at first glance.: Visa Inc., Mastercard Inc., PayPal Holdings Inc., and Uber Technologies Inc. invested in cryptocurrency. It would seem that it takes CTC market to a new level.

But in fact, it does not. The amount of investment is about $ 10 million from each of the companies. Once again, not billions, but millions (!). On the scale of Visa or Mastercard, this is not even a mathematical error. That is, no revolution has taken place, and the current growth is making such a big deal out of everything. So we do not recommend to take the growth of cryptocurrency at face value. There is the trading proverb: “buy rumours, sell facts.” our advice is acting in accordance with it. So the growth of Bitcoin is a great opportunity for its sales, nothing more.

Meanwhile, The ECB confused euro buyers, saying that the Central Bank is ready to take action at any time. It is about both reducing interest rates and returning to quantitative easing in the Eurozone if it needed to support the economy. For the euro, this is so-so news, but again - these are just words. No actual action has been taken yet.

But in the United States, these actions could be committed on Wednesday, when the decision of the Federal Open Market Committee will be announced. So far, the markets are on the side of the unchanged rate, but there is a probability of decline, besides, comments are possible with instructions in favor of a rate reduction in July. But we will write more about it and what to do with the dollar tomorrow, that is, on the eve of the announcement of the Fed's verdict.

Our trading preferences for today: we will look for points for selling the US dollar primarily against the Japanese yen, as well as the euro and the pound, sell oil and the Russian ruble, and also buy gold.

LYFT Inverse H&S bullish breakoutPattern: Bullish breakout of inverse Head and Shoulders

Edge: No outside edge since this stock just IPO'd a few weeks ago. We are just trading the pattern.

Risk Management: Bought at $62.92. Stop below $58.52 (below the 20 day moving average). PT1 is $73, PT2 is $78 (gap fill), then open target for the remainder of the shares.

Uber, PayPal, Visa to Back Facebook’s GlobalCoin CryptocurrencyVisa, Mastercard, PayPal and Uber are all backing Facebook’s new cryptocurrency, according to a new report.

The Wall Street Journal reported Thursday that the social media giant has signed on more than a dozen backers for its GlobalCoin cryptocurrency, a stablecoin that has been developed in secrecy for more than six months. Each of the new backers will invest roughly $10 million in the project as part of a governing consortium for the cryptocurrency.

Stripe, Booking.com and MercadoLibre are part of the project, according to the Journal, though the report does not specify what their roles are.

Facebook announced it was launching GlobalCoin last December, though the company indicated that it was looking at cryptocurrency as far back as the end of 2017. The crypto is expected to be a stablecoin that will operate within the company’s messaging infrastructure – WhatsApp, Instagram and Facebook Messenger.

However, Facebook has been tight-lipped about what exactly GlobalCoin will be used for, though the BBC suggested that Facebook may look to retailers, allowing its users to purchase discounted goods using the cryptocurrency. The cryptocurrency would be used to transfer value directly from Facebook to the retailer, cutting out credit card companies in the middle, which BBC suggests would help the retailers’ profits.

GlobalCoin is now expected to be unveiled on June 18.

Uber right angle triangle?Not financial advice. I’m not a financial advisor. I’m learning to trade. LEARN TO TRADE.

100% risk. 100% shot in the dark. 25% trade max. Not enough history on this chart, 1 month old.

Target of $53+ by June 27th if there is a chart pattern. “Good luck trading”

How to Trade the Uber slump, with a hedge in case it rallies NYSE:UBER Technically speaking UBER has been trading with a more positive than negative bias since its inception.

There are many risks for this company going forward and for that reason we would like to explore options trades that benefit in prices dropping. (or even rising)

I have designed this trade to benefit more from a plunge (40% or more) in UBER's underlying stock through the use of options.

There is one segment on the right side of the chart that shows a hypothetical gain if uber should drop roughly 41% from its IPO open price.

The strike prices are laid out in terms of other long put option targets as well as their intended time frame.

For the sake of this exercise we won't be quoting the exact figure because the fast changes in the options premiums, but if all of the targets are hit before or around the time of its earnings call we could see appreciation in the underlying option from 100 - 300% (estimation)

Granted this trade is slightly neutral because we are paying for any loss in the call options value if the stock does drop but what we suggest is pyramiding the position where more put options are accumulated as time passes and the earnings date approaches..

The put dates are set for July, August and September where we are getting long puts for these periods in weighted sizes:

We would keep buying 10 puts , 7 puts , 5 puts , 2 puts , 1 put at these strike prices : 40, 35, 30, 25 and when the strike prices are hit we would roll forward the put options into lower strikes with a heavier quantity- if successful a portion of the 10 puts at the 40 strike price would be liquidated and a remainder would be rolled into 35 and 30 strike prices for the following month thereby synthetically being short 1000 shares of UBER .... the more momentum in the decline would results in a greater velocity of leverage we'd have on the position (A MUCH BIGGER SHORT)

Profiting along the way

When such huge drops occur it leads to a lot of competition among buyers, and our concern is that there will be institutions buying up UBER along the way down and for that reason when the goals are met (40, 37, 35) we would cautiously liquidate those puts just to raise cash and protect the overall short position

So that being said if there are any comments about why the stock should go up we would like to continue writing about this as it progresses, there are still another 2-3 months for the plan to work, and even though this is a bearish trade we would still be open to protecting against all losses, and even ride the stock to maybe even a $100 valuation in the future.

It is early to tell, but from what I have heard, the company is not growing and they have been losing money for 9 years, any price shock would put pressure on management to change vital aspects of the business model and improve performance...

best,

Damian Richardson

Who is shorting UBER?Anybody shorting #Uber tech.

I have not heard or read anything positive on the company so decided to be on the short side.

I see this trend judging by the chart.

Anybody has same views?

LYFT Inverse H&S $75 6/21 PTThe Right shoulder is formed now on this pattern and it has room to run especially if the market runs as well.

NKN Head And Shoulders and Listing/Development NewsBITTREX:NKNBTC is completing a head and shoulders pattern on the daily chart and creating a new uptrend line. This all aligns with the Mainnet launch at the end of June and also the possibility of being listed on Huobi by it's FastTrack program. NKN is being touted as trying to "Uberize" the internet. They are also partnered with several very successful blockchain teams, I'm very bullish on NKN at the moment.

Huobi Tweet June 5:

Huobi FastTrack will hold its inaugural vote on June 13th at 8pm (GMT+8) w/ Atlas Protocol ( $ATP ), Fusion ( $FSN ), New Kind of Network ( $NKN ), Origo Network ( $OGO ), and Skrumble Network ( $SKM ).

Details: (link: bit.ly) bit.ly/31jtuxQ

#FastTrack

twitter.com

WHY TO GO LONG WITH UBERThere is reverse Shoulder Head Shoulder pattern. Simple moving average (3) is above the neck level. In addition to that OBV volume level is above the resistance level at SHS pattern zone. Target: 44.00, Stop level 41.00, ROI(Return on Investment) = 1.5 usd profit per share / 1.50 risk per share = 1 that means the return on investment of this share has neutral risk level.

Pullback expected before next move higherStrength on UBER recently has me interested. 10K still doesn't add up to what this trades at but I do like the intrinsic value they have built. I'm a small buyer sub 42 right now but think this moves higher in the coming months - assuming the market can be calm. Hard company for me to pull the trigger on and be confident with in the short-term. More earnings calls & More data.

GLTA

UBER Breakout Imminent UBER is about to make a large movement.

I don’t usually operate on 1h candles, but with Uber we don’t have much history to look at. In the three weeks since its IPO, Uber has been surprisingly boring to watch. This is mostly due to the unfortunate timing of its launch. In the week of Uber’s IPO the market experienced its highest volatility since the Christmas massacre. We have yet to decide whether 2019’s party is over, but Uber will likely trade as an amplified version of market’s decision.

Uber has been forming a small flag since its debut, unsure of which direction it should breakout. Options expiring in two weeks currently hold a 5% premium in both directions, anticipating the coming move, but split on the direction it will take. Since before its launch I have felt that, should the market have another significant leg to its bull run, UBER could potentially be a significant bubble of 2019 in similar fashion to the cannabis industry in 2018 and cryptocurrency in 2017. Whenever enough attention is focused on the future, anticipation surpasses reality without fail. With markets this creates bubbles as the integral variable of time falls from calculations.

While there is a large upside to UBER at the moment, it will be entirely subject to prevailing market sentiment, which is currently a jittery mix of trepidation and ambition. It wants to go all in on one more hand, but it also knows that it’s drunk and should head on home to recover.

Relevant indicators:

1. As mentioned, we have a flag forming. Volume has been drying up as market players place their bets over the last few weeks, and when the dice roll soon, the price will either break above 45 or below 35, the current high and low created by the first two trading days.

2. Bloomberg recently reported that 70% of available shares for shorting are lent out. This high amount indicates a strong belief in the downside, but it also shows a saturation of the position that hasn’t yet managed to materialize, indicating that it may not be strong enough to dissuade investors who want in on UBER.

2. Uber is not a profitable company, which means any investments made currently will require a large amount of time to bring a return from the company itself. The only way to profit off of a company like this is if someone else is more excited about the investment than you. Netflix (NFLX) is an example of this. These companies are expanding rapidly, and all returns are reinvested immediately in a battle to grab future market share. Due to time being such an unknown variable for the return, there is a natural inclination to the downside caused by reality that can only be countered by an increasing amount of hype regarding the potential returns of the future. This factor is largely dependent on overall market sentiment, but high-profile companies like Uber are the ones that best achieve this.

1. Lyft had its IPO shortly before Uber, and with the stock’s premier going a way similar to Facebook’s initial launch, this seems a simple instinctive guess to the direction due to LYFT being the closest comparison on the surface. But Uber is not Lyft, and its image and scope can be argued to place it in a different class than Lyft, rendering the comparison flawed. If investments in the future of self-driving cars are going to operate similarly to that of media and entertainment like Netflix, then Uber is the obvious choice for an investment in this future.

Note: Bottom trend line may be entirely accurate due to such limited information. While This movement is expected imminently, there is no accurate way to determine the exact timing for this.

Uber, young chart, first patternTriangle pattern for the young Uber! 0.50 Fibonacci level testifies a strong support for that 40$ price level. First Target will be 44$.

#Uber and a bullish wave targeting $ 50Uber and a bullish wave to form a possible Deep bearish Crab pattern targeting $ 50