$URA Cup and HandleIf you're bullish on Uranium (I am ) , then URA is a great ETF to invest/ trade.

Looks like a buy here to me regardless, nice volume shelf support and breakout retest before all time highs and blue skies

Could I be wrong - Absolutely

Will I be managing my risk - Absolutely

$26.50 stop loss price (I'm trading the 31/36 Debit spreads)

Uranium

#uranium combo. I love these! #HODL 30%+rip incoming! #bullflag$DNN

$CCJ

$UEC

$UUUUU

$URNM

$UEX

Nilce bullflag.- nearly through the traffic!

She Gone! $FIND $BSNEFNot much technical here. They are sitting on billion$ of Uranium. Draw the chart how you want this one is going up!

Uranium Gap FillIt's been written about extensively, but secular growth fundamentals and likelihood quant funds will chase this back to ATM makes it a very appealing long.

URA - GREAT UPSIDE POTENTIAL !!!!URA (Uranium) is one of the best investment in commodities to be consider now and for the future.

It is a strategic buying opportunity calling for huge upside potential first target being :

$ 37.05 ahead of $ 55.68

Yesterday's breakout (see below on related ideas my private analysis written yesterday for detail)

TRUST ME :

BUY ON DIPS

All the best and take care

Ironman8848

$UEC almost there! Almost there!$UEC cup and handle

weirtd bullflag-like structure evolving.

Somewhere between $DNN and $UUUU in terms of progress through it.

$UUUU coming round the #bullflag when she comes!She'll be coming round the bullflag when she comes....

She'll be coming round the bullflag when she comes....

She'll be coming round the bullflag

She'll be coming round the bullflag

She'll be coming round the bullflag when she comes!

A bit behind $DNN

$DNN level up in the bullflag$DNN churning around the flag. Now level-up to the top compartment of the yellow box heading for blue!

UX2! #URANIUM The bottom is NIGH! 34.40 and soon! Then we POP!OK OKOKOKOK

Uranium in a freefall? Is it?

So where is the bottom??

$34.40 - see the chart for explanation. I see a big multi-leaf IH&S. Tricky chart ! But there it is. I have seen no better explanation for this chart.

Tips accepted ;)

PDN - Potential Head and Shoulders - short term shortRecent Uranium price increase has helped raise the PDN much more rapidly to 116% from 1st September (0.52c and touched $1.12 on 16th September)

However the recent sell off from 1.12 to 0.85c has formed the head and shoulders.

This leads to a potential short term opportunity to short the stock.

Today's close: 0.85c

Potential target: 0.535 to 0.485

Disclaimer: This is not a financial advice. DYOR. And stock can react in any way with broader market sentiment. This is just for education or entertainment purpose.

URANIUM - URA - MED/LONG TERM STRAT BUYLooking at the daily picture, we can identify several important information :

1) caught in a $ 23.00 - $ 25.50 trading range

2) mix of a double bottom and double top

3) currently below the Mid Bollinger Band

4) in the middle of the sideways trading range above mentioned.

5) supported by the former uptrend support line (in green)

6) still below the ongoing resistance line (in blue)

Nevertheless, recent price action from the former high @ $ 28.68 towards

$ 23.00 should be seen as an healthy consolidation move and not as a trend reversal.

Therefore, having in mind a med/long term buy strategy, dips should be seen as a good opportunity

to increase the existing long exposure for those who are already long or to initiate new positions for the others.

TRUST ME.. there is a STRONG STORY behind and it is only the beginning of the story...

Have a look at the monthly picture and you will see the upside potential, it is huge !!!

Last but not least, the better vehicle to invest in the URANIUM theme is the following :

Strategy Certificate on U3O8 RENAISSANCE Portfolio

Underlying: U3O8 RENAISSANCE Portfolio

SSPA/EUSIPA Product Type Tracker Certificates (1300)

ISIN: CH0441692628 /Valor: 44169262

Last price (05.10.2021) $ 1'987.05

Best

Ironman8848

#uranium #UX2! cpoming down to the 0.382 fib - may a/c for $UUUULet's see!!!

nice retrace

NMothing goes up in a straight line.

IH&S proceeds

UEC retracement and setup.5 retrace from the high in mid-Sep. This is consistent with the potential inverted H&S printing. I think it not coincidental that the volume profile shows price at the point of control too.

Excellent entry hereThis very stylish, bullish megaphone has some seriously quick upside once Fibonacci 0.618 is penetrated hard.

#btc #bitcoin $btc #dogecoin #dogearmy #DogecoinToTheMoon #doge #ether #ethereum #litecoin #gold #silver #platinum #xrp #ripple #tether $coin $mstr

Lotus Resources backtesting breakoutLotus Resources is backtesting its breakout for a significant move higher

URANIUM is filling the gaps on a long-term bullish trendThis is an update to my April 2021 idea on the Uranium ETF:

As you see, the price rallied following March's Golden Cross on the 1W chart and so far the 1W MA50 (blue trend-line) has been holding as Support (which was my biggest concern back then), offering a great dip buy opportunity on August 16.

What's even more interesting is that the asset has been filling gap after gap on the Lower Highs of last decade's bear trend. The next one is at 39.00. Be ready to take advantage of the next 1W MA50 dip.

** Please support this idea with your likes and comments, it is the best way to keep it relevant and support me. **

--------------------------------------------------------------------------------------------------------

!! Donations via TradingView coins also help me a great deal at posting more free trading content and signals here !!

🎉 👍 Shout-out to TradingShot's 💰 top TradingView Coin donor 💰 this week ==> Vergnes

--------------------------------------------------------------------------------------------------------

$PDN uranium bullflag in evolutionBottom at 77? bullflag atop LT gradient

Haven't changed chart since Friday, just wanted to emphasise the gradients and add on the extension of the gradient line from previous channel up

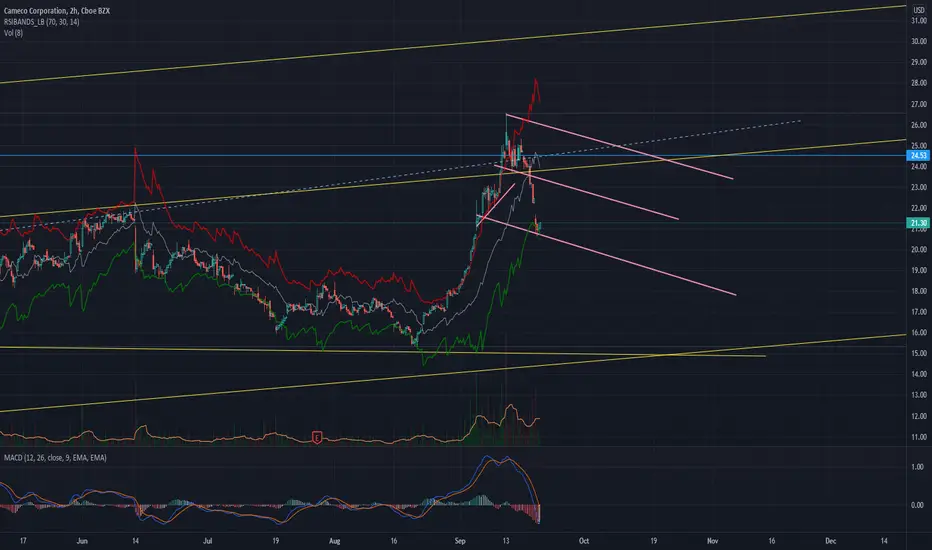

CcjAre we there yet? Not sure. Got the make off a bullflag though. Falling wedge and a little o bearflag dropping her to 19.5 and see then….

Most bullflags have a waistline that’s midway between top and bottom rails so if you acan see the waistline, you can project a floor. Ccj is tricky but that’s my best guess for now.

$AEEBit pumpy-dumpy. A colourful FA story.

OIt's dropped ito a ?symm wedge or desceending triangle on the 1-15min time scales

BUt zooming out, may dosome more dumping/retesting, but those VWAPs should be a floor even if it pulls back lower at 21-22c.

$CCJ Vs Uranium UX2!rapid backtest has sent the RSI70 SOARING

Backtest back to the VPVR and wasteline of the bullflag

See the UX price arcing up with teh CCJ: UX

Nice entry? If you look at the chart, I'd think so.. just want a smidge more conirmation of current local stucture.

I'm LT HODL CCJ LEAPS so...

CCJNice ledges there and setup for a bullflag on the BO line.

gaps down nice and bullish. Clearing teh decks of sellers so FOMO can take over again.

$URNM channel definedChannel defined.

Now we're pulling back. ?how far. BUt there are a few ledges there tha are likely seeds for a bullflag/h&s to sprout from.

Expect a pullback to the mid-channel line.

$UUUU #uranium timber!!!breaking down, bounced off the cup and handle rim.

Now putting a handle on a local cup. Bouncing between a core of VWAPs and the rim.

Another 10-15% to shed.

Est ~6-10 weeks of bullflag, depending on the U price.