S&P500: Channel Up ready to explode to 6,175S&P500 is bullish on its 1D technical outlook (RSI = 63.112, MACD = 49.220, ADX = 50.110) as it is extending August's Channel Up. The 4H RSI is forming an Arc pattern that is much like the below 4H MA50 consolidation of October 1st - 8th. After that was completed, the price rallied to the 1.786 Fibonacci extension to form a HH on the Channel Up. The 1.786 Fib was the target of the next bullish wave as well. Consequently, we are long on SPX, aiming again for that Fib (TP = 6,175).

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

Us500

Deep short for SPY? My target is at 510, here why!Christmas Eve Rally? - Not quite.

Trump Trade? - Hardly.

So, what’s driving the market higher, and where is SPY headed next?

Investor sentiment surrounding the upcoming U.S. presidential elections seems to echo the euphoria of 2016, raising hopes for a similar post-election rally. Themes like tax cuts, protectionism, and trade wars are fueling optimism for U.S. equities.

But let’s not get carried away. The economic and geopolitical landscapes today are vastly different, and so is the narrative. The “Superman” Trump of 2016 no longer holds the same sway over markets.

The post-COVID stock market rally was buoyed by an unprecedented flood of liquidity. Based on our analysis, those excess dollars are nearly spent. Furthermore, the global economic outlook bears little resemblance to the relatively stable environment of 2016.

While the Democrats’ recent performance metrics provide Powell with ample material to champion a “resilient economy,” the bigger question remains: Is the U.S. stock market truly worth its current valuations?

We’ll delve into the overvaluation of the #SPY and #SPX indices in greater detail in the coming updates.

For now, you can pay close attention to technical analysis, identifying key peaks and potential correction levels.

S&P is Shaping a Bull Flag While Awaiting the FED DecisionLast week was characterized by increasing selling pressure that hindered upward price progression but failed to trigger any substantial pullback. The market has not even retested the previous consolidation zone ( 598-601 ), which highlights the weakness of the sellers.

Looking at the daily chart, the recent price action resembles a bull flag, favoring a continuation of the upward trend. For sellers to demonstrate their strength, they must not only break this pattern to the downside but also breach the 598 support level and drive the price further down to 594 .

Much will depend on the Federal Reserve's interest rate decision this week, alongside the release of key economic data. The most favorable outcome for the bulls would be a 0.25% rate cut. Any other scenario could spark concerns—either about an impending recession (if the cut is larger) or about a prolonged high-interest-rate environment (if the cut is absent).

The market outlook remains bullish; however, the current price level is not ideal for new long positions. Buyers would be better served by waiting for a more meaningful pullback (e.g., to the 600 level), provided it is not driven by a negative shift in economic sentiment.

US500 Is Very Bullish! Long!

Take a look at our analysis for US500.

Time Frame: 8h

Current Trend: Bullish

Sentiment: Oversold (based on 7-period RSI)

Forecast: Bullish

The market is approaching a significant support area 6,060.5.

The underlined horizontal cluster clearly indicates a highly probable bullish movement with target 6,114.4 level.

P.S

We determine oversold/overbought condition with RSI indicator.

When it drops below 30 - the market is considered to be oversold.

When it bounces above 70 - the market is considered to be overbought.

Like and subscribe and comment my ideas if you enjoy them!

S&P500 Is Approaching the Daily TrendHey Traders, in today's trading session we are monitoring US500 for a buying opportunity around 5940 zone, S&P500 is trading in an uptrend and currently is in a correction phase in which it is approaching the trend at 5940 support and resistance area.

Trade safe, Joe.

Bullish momentum to extend?S&P500 (US500) is falling towards the pivot which has been identified as a pullback support and could bounce to the 1st resistance.

Pivot: 6,006.92

1st Support: 5,866.31

1st Resistance: 6,157.58

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

SPX Long in Long term to $5050, the up to $6060On the basis of previous cycles analysis.

S&P 500 index is now in the 1st wave of the new growth cycle. Technically and fundamentally now I expect the downside to $4200, but not for long.

After this SPX is going to reach the $5050 price level.

Then after 2nd wave correction (10%) 6 month before US President election SPX starts its 3rd wave up to $6060.

S&P500 What will happen in 2025 and 2026 based on this pattern?The S&P500 index (SPX) has had an excellent run since the time (August 28, see chart below) we introduced the following piece of analysis on the similarities between the 2015 - 2017 fractal and today's 2022 - 2024:

As you see, the index rose by around +8.50% from 5625 to 6100 in only 3.5 months. We are still expecting a local top just below the 3.0 Fibonacci extension, with our Target in tact at 6500.

If it continues to replicate the past pattern into the 2018 fractal as well, then we may experience the last correction of the Bull Cycle around March 2025 towards the 1W MA50 (blue trend-line) as it happened in February - March 2018 and then the final rally to a new All Time High (ATH) towards the end of the year (October - December 2025).

What this pattern shows, and what we've presented to you as a possible scenario on previous analyses, is for a new Bear Cycle to begin in 2026, four years after the Inflation Crisis of 2022, that will once more test the 1W MA200 (orange trend-line), which is the market's long-term Support.

As a side-note to investors, it is important to understand that corrections are cyclical and crises systemic. Long-term, multi-year patterns like this, help us understand with a certain degree of efficiency, when to enter and when to exit. Timing is at times (especially on such long-term horizons), more important than pricing.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Potential bullish bounce off pullback resistance?S&P500 (US500) is falling towards the pivot and could bounce to the 1st resistance which has been identified as a pullback resistance.

Pivot: 6,026.51

1st Support: 5,871.75

1st Resistance: 6,099.49

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

S&P500: Crossed under the 4H MA50. Bearish.S&P500 is headed towards a neutral 1D technical outlook (RSI = 59.952, MACD = 52.430, ADX = 39.810) as today the price hit the 4H MA50 after more than 2 weeks. Every time the index crossed under the 4H MA50 since October 21st, it declined more to the 4H MA200. The long term pattern remains a Channel Up but short term the strenght behind the 4H RSI drop favors going short. Target a potential contact point with the 4H MA200 (TP = 5,960).

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

S&P 500: Riding the Wave of OptimismS&P 500: Riding the Wave of Optimism Amid Economic and Political Dynamics

The S&P 500 continues its upward trajectory, buoyed by tech-driven gains and investor optimism, even as mixed economic data and geopolitical uncertainties loom. Here’s a deep dive into the current market landscape and what it means for the benchmark index.

---

Economic and Market Drivers

Tech-Led Rally and AI Optimism

The S&P 500's performance has been significantly influenced by gains in the technology and AI sectors. Investors are betting on the transformative potential of AI, propelling stocks like Microsoft and Meta to the forefront. However, regulatory scrutiny, such as the FTC's probe into Microsoft's AI software sales, introduces a layer of uncertainty.

Resilient Labor Market

While the Challenger Layoffs report showed a slight uptick, JOLTS job openings rose to 7.744 million in October, indicating a stable labor market. This balance supports the Federal Reserve’s cautious approach to monetary policy, as Chair Jerome Powell reiterated the economy’s strength and gradual progress in reducing inflation.

Mixed Economic Indicators

- **ISM Services PMI** fell to 52.1, below expectations of 55.7, suggesting a slowdown in service sector growth.

- **Durable goods orders** increased by 0.3%, meeting expectations and reinforcing the narrative of economic stability.

- **Construction spending** rose 0.4%, signaling robust investment activity.

- **University of Michigan 1-Year Inflation Prelim** came in at 2.9% (forecast: 2.7%, previous: 2.6%), showing slightly higher inflation expectations.

- **University of Michigan Sentiment Prelim** reached 74 (forecast: 73.2, previous: 71.8), reflecting improved consumer confidence.

These data points reflect a U.S. economy navigating challenges while avoiding a hard landing—a scenario that fuels investor confidence.

---

Federal Reserve Policy: A Turning Point?

Fed officials, including John Williams and Christopher Waller, have hinted at the potential for a December rate cut, with futures markets now pricing in an **85% likelihood of a 25-basis-point reduction**, up from **67%** before the recent jobs report. Inflation progress appears to have stalled, with Fed Governor Michelle Bowman cautioning that more robust measures may be necessary to meet the 2% target by 2025.

The November jobs report further influenced expectations:

- US Nonfarm Payrolls rose to 227k (forecast: 220k, previous: 12k, revised to 36k).

- US Unemployment Rate ticked up to 4.2% (forecast: 4.1%, previous: 4.1%).

- US Average Earnings YoY remained steady at 4% (forecast: 3.9%, previous: 4.0%).

These figures reflect a labor market resilient enough to accommodate rate cuts, which could provide an additional boost to equity markets.

---

Corporate Highlights:

- Salesforce reported Q3 revenue of $9.44 billion, exceeding estimates, but missed on adjusted EPS, reflecting mixed investor sentiment.

- Meta (Facebook) is aligning its strategies with evolving political landscapes, as CEO Mark Zuckerberg seeks to navigate regulatory and policy shifts.

- *Microsoft faces FTC scrutiny, underscoring increasing regulatory challenges in the tech sector.

Despite these challenges, corporate earnings have largely supported market valuations, adding another layer of support for the S&P 500.

---

Seasonality and Sentiment:

December has historically been a strong month for the S&P 500, driven by:

- Holiday-driven consumer spending.

- Portfolio rebalancing.

- End-of-year tax considerations.

snapshot

The Fear & Greed Index, currently at 53, indicates a greed-driven sentiment. This optimism aligns with traders pricing in a higher likelihood of Fed rate cuts, reflecting a favorable market environment.

---

Outlook: Optimism with Caution

The S&P 500’s upward momentum is underpinned by strong tech-sector performance, resilient economic data, and seasonal tailwinds. However, challenges such as geopolitical risks, regulatory scrutiny, and uneven progress in disinflation could temper gains.

The Fed's flexibility and potential rate cuts are positive signals for the market, bolstering growth-oriented sectors. Nonetheless, investors should remain vigilant, monitoring corporate earnings, economic releases, and geopolitical developments.

In the near term, the S&P 500 appears poised to end the year on a strong note. However, with inflationary pressures, mixed economic indicators, and geopolitical uncertainties still in play, the path forward will require a delicate balance between economic stability and investor confidence.

US500 Potential UpsidesHey Traders, in today's trading session we are monitoring US500 for a buying opportunity around 6060 zone, US500 is trading in an uptrend and currently is in a correction phase in which it is approaching the trend at 6060 support and resistance area.

Trade safe, Joe.

S&P 500: Riding the Wave of OptimismS&P 500: Riding the Wave of Optimism Amid Economic and Political Dynamics

The S&P 500 continues its upward trajectory, buoyed by tech-driven gains and investor optimism, even as mixed economic data and geopolitical uncertainties loom. Here’s a deep dive into the current market landscape and what it means for the benchmark index.

---

Economic and Market Drivers

Tech-Led Rally and AI Optimism

The S&P 500's performance has been significantly influenced by gains in the technology and AI sectors. Investors are betting on the transformative potential of AI, propelling stocks like Microsoft and Meta to the forefront. However, regulatory scrutiny, such as the FTC's probe into Microsoft's AI software sales, introduces a layer of uncertainty.

Resilient Labor Market

While the Challenger Layoffs report showed a slight uptick, JOLTS job openings rose to 7.744 million in October, indicating a stable labor market. This balance supports the Federal Reserve’s cautious approach to monetary policy, as Chair Jerome Powell reiterated the economy’s strength and gradual progress in reducing inflation.

Mixed Economic Indicators

- **ISM Services PMI** fell to 52.1, below expectations of 55.7, suggesting a slowdown in service sector growth.

- **Durable goods orders** increased by 0.3%, meeting expectations and reinforcing the narrative of economic stability.

- **Construction spending** rose 0.4%, signaling robust investment activity.

- **University of Michigan 1-Year Inflation Prelim** came in at 2.9% (forecast: 2.7%, previous: 2.6%), showing slightly higher inflation expectations.

- **University of Michigan Sentiment Prelim** reached 74 (forecast: 73.2, previous: 71.8), reflecting improved consumer confidence.

These data points reflect a U.S. economy navigating challenges while avoiding a hard landing—a scenario that fuels investor confidence.

---

Federal Reserve Policy: A Turning Point?

Fed officials, including John Williams and Christopher Waller, have hinted at the potential for a December rate cut, with futures markets now pricing in an **85% likelihood of a 25-basis-point reduction**, up from **67%** before the recent jobs report. Inflation progress appears to have stalled, with Fed Governor Michelle Bowman cautioning that more robust measures may be necessary to meet the 2% target by 2025.

The November jobs report further influenced expectations:

- US Nonfarm Payrolls rose to 227k (forecast: 220k, previous: 12k, revised to 36k).

- US Unemployment Rate ticked up to 4.2% (forecast: 4.1%, previous: 4.1%).

- US Average Earnings YoY remained steady at 4% (forecast: 3.9%, previous: 4.0%).

These figures reflect a labor market resilient enough to accommodate rate cuts, which could provide an additional boost to equity markets.

---

Corporate Highlights

- Salesforce reported Q3 revenue of $9.44 billion, exceeding estimates, but missed on adjusted EPS, reflecting mixed investor sentiment.

- Meta (Facebook) is aligning its strategies with evolving political landscapes, as CEO Mark Zuckerberg seeks to navigate regulatory and policy shifts.

- *Microsoft faces FTC scrutiny, underscoring increasing regulatory challenges in the tech sector.

Despite these challenges, corporate earnings have largely supported market valuations, adding another layer of support for the S&P 500.

---

Seasonality and Sentiment

December has historically been a strong month for the S&P 500, driven by:

- Holiday-driven consumer spending.

- Portfolio rebalancing.

- End-of-year tax considerations.

The Fear & Greed Index, currently at 53, indicates a greed-driven sentiment. This optimism aligns with traders pricing in a higher likelihood of Fed rate cuts, reflecting a favorable market environment.

---

Outlook: Optimism with Caution

The S&P 500’s upward momentum is underpinned by strong tech-sector performance, resilient economic data, and seasonal tailwinds. However, challenges such as geopolitical risks, regulatory scrutiny, and uneven progress in disinflation could temper gains.

The Fed's flexibility and potential rate cuts are positive signals for the market, bolstering growth-oriented sectors. Nonetheless, investors should remain vigilant, monitoring corporate earnings, economic releases, and geopolitical developments.

In the near term, the S&P 500 appears poised to end the year on a strong note. However, with inflationary pressures, mixed economic indicators, and geopolitical uncertainties still in play, the path forward will require a delicate balance between economic stability and investor confidence.

Bearish drop?S&P500 (US500) is reacting off the pivot and could drop to the 23.6% Fibonacci support.

Pivot: 6,083.37

1st Support: 6,027.94

1st Resistance: 6,107.21

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

S&P 500: Riding the Wave of OptimismS&P 500: Riding the Wave of Optimism Amid Economic and Political Dynamics

The S&P 500 continues its upward trajectory, buoyed by tech-driven gains and investor optimism, even as mixed economic data and geopolitical uncertainties loom. Here’s a deep dive into the current market landscape and what it means for the benchmark index.

---

Economic and Market Drivers

Tech-Led Rally and AI Optimism

The S&P 500's performance has been significantly influenced by gains in the technology and AI sectors. Investors are betting on the transformative potential of AI, propelling stocks like Microsoft and Meta to the forefront. However, regulatory scrutiny, such as the FTC's probe into Microsoft's AI software sales, introduces a layer of uncertainty.

Resilient Labor Market

While the Challenger Layoffs report showed a slight uptick, JOLTS job openings rose to 7.744 million in October, indicating a stable labor market. This balance supports the Federal Reserve’s cautious approach to monetary policy, as Chair Jerome Powell reiterated the economy’s strength and gradual progress in reducing inflation.

Mixed Economic Indicators

- ISM Services PMI** fell to 52.1, below expectations of 55.7, suggesting a slowdown in service sector growth.

- Durable goods orders increased by 0.3%, meeting expectations and reinforcing the narrative of economic stability.

- Construction spending rose 0.4%, signaling robust investment activity.

These data points reflect a U.S. economy navigating challenges while avoiding a hard landing—a scenario that fuels investor confidence.

---

Federal Reserve Policy: A Turning Point?

Fed officials, including John Williams and Christopher Waller, have hinted at the potential for a December rate cut, with futures markets pricing in a 74% likelihood of a 25-basis-point reduction. Inflation is expected to ease gradually, targeting 2% by 2025, but progress remains uneven. The Fed’s Beige Book also reported modest price increases and slightly higher economic activity, aligning with the central bank’s cautious optimism.

This pivot towards monetary easing, coupled with balanced labor market conditions, is a positive signal for equities, particularly growth-oriented sectors.

---

Corporate Highlights

- Salesforce reported Q3 revenue of $9.44 billion, exceeding estimates, but missed on adjusted EPS, reflecting mixed investor sentiment.

- Meta (Facebook) is aligning its strategies with evolving political landscapes, as CEO Mark Zuckerberg seeks to navigate regulatory and policy shifts.

- Microsoft faces FTC scrutiny, a development that underscores the increasing regulatory challenges in the tech sector.

Despite these challenges, corporate earnings have largely supported market valuations, adding another layer of support for the S&P 500.

---

Seasonality and Sentiment

December has historically been a strong month for the S&P 500, driven by:

- Holiday-driven consumer spending.

- Portfolio rebalancing.

- End-of-year tax considerations.

This seasonal strength aligns with the **Fear & Greed Index**, which currently stands at 56, indicating a greed-driven sentiment. Such sentiment often paves the way for further market upside, as investors are inclined to take on more risk in anticipation of future gains.

---

Outlook: Optimism with Caution

The S&P 500’s upward momentum is underpinned by strong tech-sector performance, resilient economic data, and seasonal tailwinds. However, challenges such as geopolitical risks, regulatory scrutiny, and uneven progress in disinflation could temper gains.

With the Federal Reserve signaling flexibility and potential rate cuts, the market sentiment remains favorable. However, investors should remain vigilant, monitoring corporate earnings, economic releases, and geopolitical developments.

In the near term, the S&P 500 appears poised to end the year on a strong note, but the path forward will depend on a delicate balance of economic stability and investor confidence.

S&P500: No corrections possibly for the whole 2025.S&P500 is on excellent bullish levels on the 1D timeframe (RSI = 64.149, MACD = 44.390, ADX = 33.789) as it is extending the strong rise since the U.S. elections. Going back even more, this uptrend has been nothing but sustainable ever since the August 5th bottom that almost hit the 1W MA50. In fact that MA level is intact since October 2023. The index has been following a similar path with the December 2018 - December 2021 Bull Cycle that topped after a +105% rise. You can see that following the COVID correction recovery after leg (6), the index crossed over the 1W MA50 and never broke it up until after the January 2022 High in 574 days.

Consequently, we expect a continuation of the current uptrend for as long as the 1W MA50 stays intact. We are targeting a +105% rise yet again (TP = 7,150) near the end of 2025.

See how our prior idea has worked out:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

S&P 500 – Solid Foundation Amid Positive Economic DataS&P 500 – Solid Foundation Amid Positive Economic Data

The S&P 500 index continues to find support from favorable economic data and a stable macroeconomic outlook for the United States. Despite ongoing challenges, the market reflects optimism fueled by a mix of improving manufacturing indicators, resilient consumer spending, and a potential softening in Federal Reserve policy. Additionally, seasonal trends strongly favor the S&P 500, as December is historically one of the best months for equities.

---

Key Economic Drivers Supporting the S&P 500

1. ISM Manufacturing PMI – Signs of Stabilization

- The **ISM Manufacturing PMI** for November rose to 48.4, beating expectations, although still indicating contraction. This suggests the U.S. manufacturing sector is moving closer to stabilization.

- Input costs showed the slowest inflation in a year, and renewed job creation added to the optimism. Challenges such as weaker international demand and reduced production remain, but improved business confidence is a positive signal.

2. Construction Spending Growth

- Construction spending increased by 0.4% in October, highlighting resilience in the housing and infrastructure sectors. This reflects ongoing consumer and government investment, contributing to economic stability.

3. ISM Manufacturing Prices Paid – Easing Inflationary Pressures

- The ISM Manufacturing Prices Paid index dropped to 50.3, well below forecasts of 55.2. This is a significant development for inflation control, signaling moderating cost pressures within the manufacturing sector.

- Implications:

- Positive for equities: Lower inflation reduces the risk of aggressive Federal Reserve rate hikes.

- Stable monetary outlook: This supports expectations of a gradual shift toward easing monetary policy.

4. Fed Officials’ Support for Gradual Easing

- Recent comments from Fed officials indicate a balanced approach toward monetary policy:

- Christopher Waller highlighted the likelihood of a rate cut in December, citing a balanced labor market and gradual progress on inflation.

- John Williams reaffirmed that inflation is expected to decline toward the 2% target while projecting GDP growth of 2.5% in 2024.

- A potential rate cut could provide a further boost to equities as borrowing costs decrease, encouraging corporate investment.

5. Consumer and Business Optimism

- The S&P Global U.S. Manufacturing PMI pointed to renewed job creation and improving confidence, though challenges such as weaker international demand persist. This mix of cautious optimism and moderating inflation supports steady market sentiment.

---

Seasonality and Market Sentiment

Seasonality is a key supporting factor for the S&P 500 at this time. December has historically been a strong month for equity markets due to holiday-driven consumer spending, portfolio rebalancing, and end-of-year tax considerations. This seasonal strength aligns with the Fear & Greed Index, which currently stands at 64, indicating a **greed-driven sentiment** that tends to favor further market upside.

---

S&P 500 Outlook

The S&P 500 is well-positioned to benefit from these positive economic indicators:

- Lower inflationary pressures reduce the likelihood of aggressive Federal Reserve action, which is supportive of equity markets.

- Steady GDP growth and a resilient labor market provide a strong foundation for corporate earnings.

- Improved manufacturing confidence and spending on infrastructure create additional momentum for sectors like industrials and materials.

- Strong seasonality and a favorable market sentiment further reinforce the potential for continued gains.

While global uncertainties and weaker international demand could weigh on certain sectors, the overall outlook for the S&P 500 remains bullish, with near-term support from seasonal trends, improving economic data, and the potential for a more accommodative Fed policy stance.

S&P: Weekly Recap and OutlookLast week, the market opened with a gap up that was quickly filled, after which price hovered near the previous all-time high. Bolstered by new economic data, which delivered no negative surprises, bulls pushed the price out of the trading range, establishing a new all-time high.

While this is undoubtedly a positive development that reinforces the bullish thesis, a few warning signs warrant closer attention:

1. Low Breakout Volume: The breakout occurred on significantly low volume. While volume is less critical in indices and ETFs compared to individual stocks, observing below-average volume during such an important event raises concerns about the breakout’s sustainability.

2. Relative Weakness in the Tech Sector (XLK): This deviation signals hesitancy among growth investors, which could potentially ripple through to other market participants.

Additionally, concerns highlighted in my previous review remain unresolved and continue to be relevant.

At this stage, there is no concrete evidence of a sentiment shift or technical signals pointing to a broad trend reversal. However, there is a growing impression that the rally may be nearing temporary exhaustion, which could lead to a significant pullback.

Key Focus for the Upcoming Week

Investors will be closely watching the employment data, which has already hinted at labor market weakness. If new data further support this trend, it could heighten bearish sentiment.

Price action this week will likely provide important clues:

• Bullish Confirmation: If the breakout is followed by a swift continuation, this will confirm buyers’ conviction and overall market strength.

• Bearish Signals: Conversely, if the price pulls back below 600 or oscillates indecisively around this level, it may signal uncertainty among buyers, creating an opportunity for short sellers to capitalize.

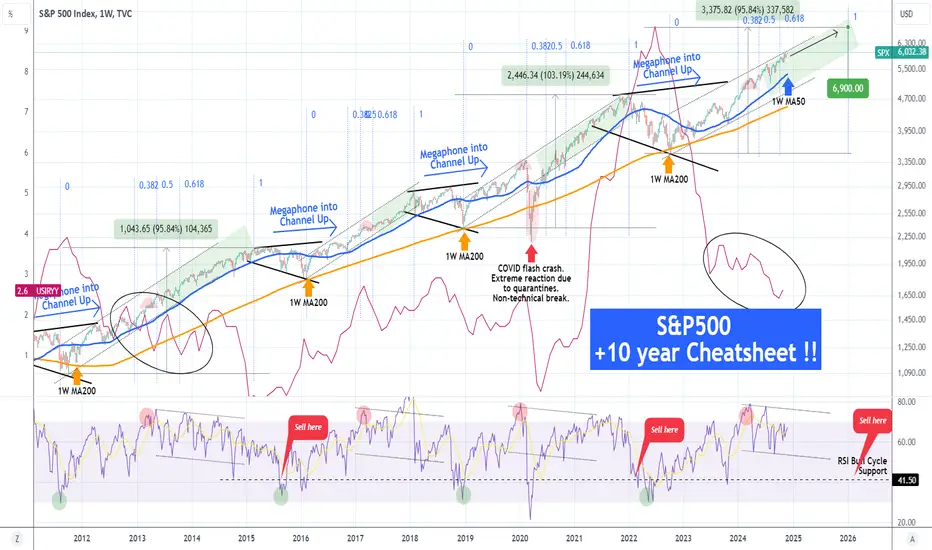

S&P500 This Inflation Cheatsheet shows no correction in 2025.This is a chart we first posted almost 4 months ago (August 14, see chart below) at the time of a CPI date release, where we viewed the S&P500 index (SPX) against Inflation (red trend-line) and calling for an immediate buy:

** The 1W MA50 as the ultimate Support **

Well the price jumped +11% since then from 5440 to over 6000. The first principle of this chart is that as long as the 1W MA50 (blue trend-line) is supporting, investors should stay bullish. This is because all previous multi-year rallies since August 2011 that started within a Channel Up, ended upon a 1W candle close below the 1W MA50 and transitioned into a Megaphone pattern for the new Bear Phase.

** Declining Inflation fueling stocks **

Right now we are still on a declining Inflation trend, very similar to early 2014 (ellipse shape on Inflation), while the 1W RSI of SPX is declining inside a Channel Down. This is a Bearish Divergence, which during all previous SPX Channel Up patterns, didn't make the index top until the RSI broke below its 41.50 Support (notable exception of course the March 2020 COVID flash crash which was a one in 100 years Black Swan event).

** SPX Target and timing **

As a result, while the 1W RSI trades within its Channel Down and above 41.50 and all price candles close above the 1W MA50, we expect the index to extend the multi-year uptrend to 6900, which would represent a +95.84% rise from the October 2022 bottom, similar to the February 2015 High. Notice that the December 2021 top was also of a similar magnitude (+103%).

As far as timing is concerned, we have calculated a model based on the 1W RSI top and the start of its Channel Down. As you see at that point, SPX always makes a medium-term pull-back (red Arc). This tends to be within the 0.382 - 0.618 time Fibonacci levels and on the 2011 - 2014 Bull Cycle, that was within the 0.382 - 0.5 Fib zone. As a result, applying this principle on the current Bull Cycle, the trend is now just 2 months past the 0.618 time Fib and we can expect a Cycle Top around December 2025.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

S&P 500 is climbing upwardsS&P 500 is climbing upwards

The market’s move reflects ongoing digestion of mixed US economic data, supportive seasonality, and cautious optimism among investors.

US Economic Data Highlights

Data provided a mixed snapshot of the US economy, contributing to the market’s recent fluctuations:

- **Chicago Fed National Activity Index (Oct):** Fell to -0.40, below the expected -0.2.

- **Dallas Fed Manufacturing Index (Nov):** Came in at -2.7, worse than the forecast of -2.4.

- **New Home Sales (Oct):** Declined to 0.61M, significantly missing expectations of 0.73M.

- **Richmond Fed Manufacturing Index (Nov):** Plunged to -14, below the forecast of -10.

- **Durable Goods Orders (Oct):** Increased by just 0.2%, underperforming the 0.5% forecast.

- **Initial Jobless Claims (Nov 23):** Reported at 213K, slightly better than expected (216K), but still pointing to a resilient labor market.

- **Chicago PMI (Nov):** Dropped to 40.2, well below the anticipated 44, highlighting weakness in manufacturing.

Market Sentiment and Seasonality

Seasonality continues to work in favor of the S&P 500, as historical trends during this period often support equities. The **Fear & Greed Index**, currently at **64 points**, reflects moderate optimism and a "Greed" sentiment, which typically aligns with risk-on behavior in the markets.

Rate Cut Expectations

Markets remain focused on the Federal Reserve’s upcoming meeting on **December 18th**, with a **66,3%% probability** currently priced in for a **25 basis-point rate cut**. Such a move could provide additional support for equities by easing financial conditions, though its long-term impact remains uncertain.

Geopolitical Risks

While market sentiment has improved slightly, risks remain in the background. The ongoing war in Ukraine continues to pose threats to global stability, with potential knock-on effects on energy prices, supply chains, and economic performance.

Long-Term Trend Intact, but Volatility Likely

The S&P 500’s long-term upward trend remains intact, bolstered by supportive seasonality, stable GDP growth, and investor optimism. However, the current environment of mixed economic data and rising policy uncertainty suggests that market volatility could persist in the short term.

Broader Context

27.11 data underscored a steady but moderating US economy, while forward-looking risks remain:

- **Global Economic Outlook:** The S&P Global forecast anticipates global GDP growth of approximately 3% by 2025, with US growth slowing to below 2% next year and China toward 4%.

- **US Policy Risks:** Potential policy shifts under the new administration could elevate inflation pressures and tighten financial conditions, introducing further uncertainty for equity markets.

Implications for S&P 500

Today’s modest gain shows resilience in the face of mixed signals from economic data and global risks. With supportive seasonality and a strong likelihood of a December rate cut, the S&P 500 may find short-term support. However, investors should remain vigilant, as volatility is likely to persist amid policy uncertainties and geopolitical risks.

What’s your outlook for the S&P 500 after today’s rebound? Can the market sustain its gains, or will headwinds from mixed data and global risks take over? Share your thoughts in the comments!

S&P 500: A +0.2% Gain Following a Day of DeclineS&P 500: A +0.2% Gain Following a Day of Decline

The S&P 500 rebounded with a modest 0.2% gain today, recovering some ground after yesterday’s 0.5% decline. The market’s move reflects ongoing digestion of mixed US economic data, supportive seasonality, and cautious optimism among investors.

US Economic Data Highlights

Yesterday’s data provided a mixed snapshot of the US economy, contributing to the market’s recent fluctuations:

- **EIA Crude Oil Inventories:** Fell by -1.844M barrels, exceeding the forecast of -1M, signaling tighter supply conditions.

- **US GDP Growth (Q3, Second Estimate):** Steady at 2.8%, unchanged from the previous estimate, highlighting consistent economic expansion.

- **Personal Consumption and Spending:** October’s real personal consumption rose by just 0.1% (forecast: 0.2%), while consumer spending grew by 0.4%, meeting expectations but showing a slowdown from revised data of 0.6%.

- **Durable Goods Orders:** Increased by 0.2%, falling short of the 0.5% forecast, reflecting weaker demand for long-term goods.

- **PCE Price Index (YoY):** Increased to 2.3%, matching expectations but higher than the prior 2.1%, indicating persistent inflationary pressures.

Market Sentiment and Seasonality

Seasonality continues to work in favor of the S&P 500, as historical trends during this period often support equities. The **Fear & Greed Index**, currently at **64 points**, reflects moderate optimism and a "Greed" sentiment, which typically aligns with risk-on behavior in the markets.

Rate Cut Expectations

Markets remain focused on the Federal Reserve’s upcoming meeting on **December 18th**, with a **66,3%% probability** currently priced in for a **25 basis-point rate cut**. Such a move could provide additional support for equities by easing financial conditions, though its long-term impact remains uncertain.

Geopolitical Risks

While market sentiment has improved slightly, risks remain in the background. The ongoing war in Ukraine continues to pose threats to global stability, with potential knock-on effects on energy prices, supply chains, and economic performance.

Long-Term Trend Intact, but Volatility Likely

The S&P 500’s long-term upward trend remains intact, bolstered by supportive seasonality, stable GDP growth, and investor optimism. However, the current environment of mixed economic data and rising policy uncertainty suggests that market volatility could persist in the short term.

Broader Context

Yesterday’s data underscored a steady but moderating US economy, while forward-looking risks remain:

- **Global Economic Outlook:** The S&P Global forecast anticipates global GDP growth of approximately 3% by 2025, with US growth slowing to below 2% next year and China toward 4%.

- **US Policy Risks:** Potential policy shifts under the new administration could elevate inflation pressures and tighten financial conditions, introducing further uncertainty for equity markets.

Implications for S&P 500

Today’s modest gain shows resilience in the face of mixed signals from economic data and global risks. With supportive seasonality and a strong likelihood of a December rate cut, the S&P 500 may find short-term support. However, investors should remain vigilant, as volatility is likely to persist amid policy uncertainties and geopolitical risks.

What’s your outlook for the S&P 500 after today’s rebound? Can the market sustain its gains, or will headwinds from mixed data and global risks take over? Share your thoughts in the comments!

SPX500 / US500 Index Market Money Heist Plan on Bullish SideHallo! My Dear Robbers / Money Makers & Losers, 🤑 💰

This is our master plan to Heist SPX500 / US500 Index Market Market based on Thief Trading style Technical Analysis.. kindly please follow the plan I have mentioned in the chart focus on Long entry. Our target is Red Zone that is High risk Dangerous level, market is overbought / Consolidation / Trend Reversal / Trap at the level Bearish Robbers / Traders gain the strength. Be safe and be careful and Be rich.

Entry 📈 : Can be taken Anywhere, What I suggest you to Place Buy Limit Orders in 15mins Timeframe Recent / Nearest Low Point take entry in pullback.

Stop Loss 🛑 : Recent Swing Low using 2h timeframe

Attention for Scalpers : Focus to scalp only on Long side, If you've got a lot of money you can get out right away otherwise you can join with a swing trade robbers and continue the heist plan, Use Trailing SL to protect our money 💰.

Warning : Fundamental Analysis news 📰 🗞️ comes against our robbery plan. our plan will be ruined smash the Stop Loss 🚫🚏. Don't Enter the market at the news update.

Loot and escape on the target 🎯 Swing Traders Plz Book the partial sum of money and wait for next breakout of dynamic level / Order block, Once it is cleared we can continue our heist plan to next new target.

💖Support our Robbery plan we can easily make money & take money 💰💵 Follow, Like & Share with your friends and Lovers. Make our Robbery Team Very Strong Join Ur hands with US. Loot Everything in this market everyday make money easily with Thief Trading Style.

Stay tuned with me and see you again with another Heist Plan..... 🫂

S&P500 Don't expect the rally to stop now.Our last S&P500 (SPX) analysis (November 18, see chart below) gave us the ideal buy entry on the 0.5 Fibonacci retracement level, with the price immediately responding with a rebound:

The rebound took place on the 4H MA200 (orange trend-line) and we are now even past the 4H MA50 (blue trend-line). Despite the strong uptrend, this rally is far from over technically, as not only is the 4H RSI below the (70.00) overbought barrier where it has given the first bearish signs near the two previous Higher Highs, but also significantly lower than the top (Higher Highs trend-line) of the September 06 Channel Up.

As a result we expect a continuation of the current Bullish Leg. The previous one peaked on the 1.786 Fibonacci extension, so our Target is now just below it at 6150.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇