US100 PutsThe price is struggling to break out from the last supply zone and its probably going to reverse and fill the imbalance gap all the way down to $17200.

Us500

S&P Bears are strong but Bulls still have a chanceLast week, sellers firmly controlled the market. Buyers attempted to defend March's low, but the bears left them no chance. Prices consistently declined for six consecutive days, with the futures chart ( CME_MINI:ES1! ) appearing even more bearish.

We are now approaching a critical juncture, which presents a significant opportunity for buyers to take a stand. The daily RSI is nearing an oversold condition, and simultaneously, the price is approaching the SMA100 alongside a horizontal support level ( 490 ) from the February consolidation.

There is no absolute certainty that buyers will seize this opportunity, but we should closely monitor the price action next week. Although sellers have demonstrated their strength, we are still in a weekly uptrend, and trends do not end easily unless there is a radical shift in sentiment. Despite negative news in recent weeks, nothing has emerged as critically detrimental yet. However, this could change, so we must regularly reassess the situation as new information becomes available.

The short-term outlook remains bearish, but this could change depending on how the price reacts to these support levels.

Disclaimer

I don't give trading or investing advice, just sharing my thoughts.

Dow Jones (US30): Pullback From Key Level

After a test of a strong horizontal resistance,

Dow Jones broke and closed below a support line of a rising parallel channel

on a 4h time frame.

We can expect a retracement to 38230 / 38066

❤️Please, support my work with like, thank you!❤️

Earnings season produces wild movesAfter the closing bell on Tuesday, Tesla reported its earnings for the first quarter of 2024. Despite the report showing a 9% YoY decline in total revenue and a staggering 55% YoY drop in net income, along with an increase in operating costs by 37% YoY, shares of the company soared more than 12% in the aftermarket. The price action, however, was not the same for Meta Platforms, which delivered much better results yesterday, with revenue growing by 27% YoY, net income by 117% YoY, and operating costs by 6% YoY; yet, the company’s shares plummeted more than 15% following the announcement.

While trying to wrap our heads around these moves, we would like to point out the double divergence forming on the monthly graph between the price and RSI, shown in Illustration 1.01. In addition to that, we would want to highlight an impending bearish crossover between the 20-day SMA and the 50-day SMA, both of which currently act as crucial resistance levels. If the SPX breaks and maintains ground above them, it will be positive, but if the SPX fails, it will be slightly worrisome. Besides that, another spike in the VIX will also be concerning. Today, there are several important data releases, including jobless claims, GDP growth rate, wholesale inventories, and pending home sales. Furthermore, several big names are reporting their earnings, most notably Alphabet and Microsoft.

Illustration 1.01

Above is the monthly chart of SPX and RSI. Yellow arrows indicate the first and the second divergence between the price and RSI.

Technical analysis gauge

Daily time frame = Bearish

Weekly time frame = Bearish

*The gauge does not necessarily indicate where the market will head. Instead, it reflects the constellation of RSI, MACD, Stochastic, DM+-, ADX, and moving averages.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor or any other entity. Therefore, your own due diligence is highly advised before entering a trade.

S&P500 - Long opportunity ✅Hello traders!

‼️ This is my perspective on S&P500.

Technical analysis: Here we are in a bullish market structure from 4H timeframe perspective, so I look only for long position. My point of interest is if price continue the retracement and then rejects trendline + S/R zone + FIBO 0.618 level.

Like, comment and subscribe to be in touch with my content!

Big earnings this week could pave the way for a reboundThe S&P 500 Index has been edging lower for nearly a month, accompanied by a rise in volatility. From its all-time highs in late March 2024, the SPX has declined about 5.6%, which begs the question of a rebound. Interestingly, this week, several big names, including Alphabet, Meta Platforms, Microsoft, and Tesla, are reporting their earnings for the first quarter of 2024. If these results are generally good, then there is a significant chance that SPX will recover some of the losses. However, if earnings fail to fulfill investors’ expectations and there are notable downgrades to future forecasts, it could spark more fear among investors and rekindle volatility in the market.

Illustration 1.01

The picture above shows the daily graph of SPX and two simple moving averages, the 20-day SMA and the 50-day SMA. The yellow arrow indicates an impending bearish crossover between these two moving averages, which represent resistance levels to watch out for in the case of a stock market rebound.

Technical analysis gauge

Daily time frame = Bearish

Weekly time frame = Bearish

*The gauge does not necessarily indicate where the market will head. Instead, it reflects the constellation of RSI, MACD, Stochastic, DM+-, ADX, and moving averages.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor or any other entity. Therefore, your own due diligence is highly advised before entering a trade.

S&P500: 1D MA100 hit. Short term rebound at least to be expectedS&P500 is bearish on its 1D technical outlook (RSI = 37.601, MACD = -44.800, ADX = 58.528) as it touched the 1D MA100 on Friday after more than 5 months. This calls for a short term rebound at least as every previous corrective wave inside the multi month Channel Up that approached the 1D MA100, it rebounded to at least the 0.618 Fibonacci level. Following our last short call, we are now turning long again (TP = 5,115).

See how our prior idea has worked out:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

S&P 500 set to advance after a bout of selling on FridayEfforts are underway to head off a full-blown Middle East war.

What’s Happening Now:

A tense calm prevailed in the Middle East after Iran’s missile and drone attack on Israel. Global markets showed signs of stability on speculation the conflict will remain contained.

Iran said there wouldn’t be further attacks as long as Israel didn’t react aggressively, but Benjamin Netanyahu warned, “Whoever strikes Israel, we will strike him.”

A diplomatic race is underway to help ensure any retaliation doesn’t raise the stakes too high.

“It’s right to price more geopolitical risk premia into assets, but at the end of the day equity markets are still only about 2% off all-time highs,” said Timothy Graf, head of EMEA macro strategy at State Street. “This was a well-telegraphed geopolitical development. A lot of the bad news is in the price already.”

As we can see on the chart, the index is still trading in the tight diagonal canal which once broken a higher liquidity impulse can be expected. With the current situation of repricing rate cuts, higher inflation, and war tensions rising I am strongly expecting a quick 3-7% test to the previous lows.

A Traders’ Week Ahead Playbook: Buy the dip or sell the rip?We move on from a week where strong momentum markets (AI names, NAS100, JPN225, Mexican peso) were sold down hard, with traders better buyers of the VIX, US30, gold, CHF, USD, and defensive equities (utilities).

Notably, the NAS100 recorded its worst week since November 2022, driven in part by market players part-liquidating an incredibly extended position in Nvidia, with 87m shares traded on Friday alone. Tesla and Super Micro Computers also seeing steep declines on the week, with Tesla remaining front and centre with Q124 earnings due after-market on Tuesday – many ask whether we see a fifth consecutive quarter where shares closed lower on the day of reporting?

Long US30 / short NAS100 positions have worked well and remain a tactical play I like into the new week - although with so many heavyweight tech names reporting through the week, NAS100 shorts will watch the reaction to earnings closely and will be prepared to react if the market likes what they see from the respective outlooks.

While sentiment has turned more negative, there is absolutely no panic at all and I’d to see if the buyer’s step in and support the S&P500 a little lower into 4935. That said, the price action and technical set-up suggests selling rallies in the US500 and NAS100 is the play – and if one is compelled to ‘buy dips’, then waiting for the rip after early traders buy the dip seems the higher probability play.

Geopolitical headlines remain fluid and have been a key reason for keeping buyers of risk at bay – many will remain focused on these developments as we roll into the new week. The news flow was certainly a key reason why gold closed higher for a fifth straight week and at a new all-time closing high on Friday, as it was why the CHF was the star currency on the week.

That said, with Brent crude closing the week 3.1% lower, one could argue it was the move higher in US bond yields – with the US 10yr Treasury pushing above 4.6% - that was really the big kicker that promoted rotation out of tech/AI names and supported the USD.

Short GBPUSD and long USDMXN on any retracement remains a compelling trade on my radar.

Watch US PCE inflation on Friday as the marquee risk on the data front – for a playbook, we could see outsized market moves on a US core PCE print above 0.4% m/m (USD up, gold, NAS100 down) or below 0.25% m/m (USD down, NAS100 and gold higher). A read above 0.4% m/m and the idea of a cut before the US Presidential election would be further dialled back.

There will be a focus on the BoJ meeting, but it is too soon for them to alter policy, and the market gives a change in rates no chance at all. If we get a move in the JPY, it will likely come from any changes to the bank’s inflation forecasts and the post-meeting conference call. We remain on JPY intervention watch, and signs that we are getting closer to the point where Japanese authorities look to step up the fight against JPY's weakness.

PMIs are due in the UK, EU, and US and they could move markets, notably if the service’s PMI outcome misses/beats expectations by a wide margin. Australia Q1 CPI poses a risk to AUD exposures, although, with such little priced into Aussie interest rate futures, it would need to big surprise to have a lasting effect on AUD pairs.

Bitcoin moves past the highly anticipated halving and while we predictably didn’t get any kneejerk reaction in price, the set-up on the higher timeframes is starting to look more compelling from the long side. There was clear support from the market to buy on the move below $60k and this is a level many are guiding for stops on longs. An upside break of $66k could be the trigger for a push into the top of the range of $72k.

Key event risk for traders to navigate:

Monday

• China 1 & 5-year Loan Prime Rate decision (11:15 AEST / 14:15 BST) – No change expected with the 1-year rate left at 3.45% and the 5-year rate at 3.95%.

Earnings – SAP (Germany) – one to watch for clients trading the GER40, with SAP holding a 10% weight on the index.

Central bank speeches – BoE’s Benjamin speaks (19:05 AEST / 10:05 BST)

Tuesday

• EU HCOB manufacturing and services PMI (18:00 AEST / 09:00 BST) – Service PMI eyed at 51.8 (from 51.5 in the prior read) & manufacturing at 46.5 (from 46.1)

• UK S&P manufacturing and services PMI (18:30 AEST / 09:30 BST) - Services at 53.0 (53.1) & manufacturing at 50.4 (50.3)

• US S&P Global manufacturing and services PMI (23:45 AEST / 14:45 BST) - Services at 52.0 (51.7) & manufacturing at 52.0 (51.9)

Earnings – Tesla (after-market), Visa (after-market)

Central bank speeches – BoE Haskel (18:00 AEST), BoE Huw Pill (21:15 AEST), ECB Nagel (22:30 AEST)

Wednesday

• Australia Q1 CPI (11:30 AEST / 02:30 BST) – The economist consensus looks for headline CPI at 0.8% QoQ / 3.5% YoY (4.1%), and the trimmed mean CPI measure eyed at 3.8% YoY (from 4.2%). With Aussie interest rate futures pricing in just one rate cut in 2024, it would take a big beat/miss vs consensus to drive significant volatility in the AUD, with the AUD more sensitive to geopolitical headlines and broad market sentiment.

• Mexico Bi-weekly CPI (22:00 AEST / 13:00 BST) – the consensus is for headline CPI to come in at 4.49% (4.37%) and core CPI at 4.38% (4.41%)

Earnings – Lloyds (UK), Boeing (before-market), IBM (after-market), Meta (after-market)

Thursday

Anzac Day – ASX200 closed.

Earnings – Barclays (UK), Caterpillar (before-market), Alphabet (after-market), Intel (after-market), Microsoft (after-market)

Central bank speeches – ECB’s Schnabel speaks (00:00 AEST and 17:00 AEST)

Friday

• Tokyo CPI (09:30 AEST / 00:30 BST) – headline CPI is eyed at 2.5% (2.6%) and core CPI at 2.2% (2.4%) – shouldn’t be a volatility event for the JPY or JPN225

• Bank of Japan meeting with updated GDP and inflation forecasts (no set time but likely between 12:00 and 15:00 AEST / 03:00 to 06:00 BST) – no change in policy expected, so the focus falls on the bank's inflation projections and the post-meeting conference call.

• ECB 1- & 3-year CPI expectations (18:00 AEST / 09:00 BST)

• US core PCE inflation (22:30 AEST / 13:30 BST) – headline PCE inflation is expected at 0.3% m/m and 2.6% y/y (from 2.5%) and core PCE at 0.3% m/m and 2.7% y/y (2.8%).

Earnings – Exxon (Before market), Chevron

S&P weekly consolidation in progressAt the end of last week, sellers confirmed weekly consolidation by closing below the previous week's low. From now on, bears have control over the price on the weekly timeframe. We should monitor the progression of weekly lows and highs to see when things start to shift, but until then, we should trust the sellers.

It is also notable that if we look at the futures chart ( CME_MINI:ES1! ), we can see that buyers were unable to close above the previous day's high for the last 10 trading days. If buyers want to regain control, this will be their first objective.

Please note that the price is currently positioned near the previous month's low, which can provide an intermediate support level. If you’re planning to short the market, it is better to wait for a pullback or for a breakout with retest.

Finally, if weekly consolidation will convert into monthly consolidation it will be a major win for bears.

Disclaimer

I don't give trading or investing advice, just sharing my thoughts.

Here is What to Know Beyond Why Pfizer Inc. (PFE) is a Trending

Despite short-term challenges like revenue and earnings declines in the current quarter, Pfizer (PFE) maintains a positive long-term growth trajectory. With optimistic earnings estimates for the full fiscal year, consistent EPS beats, and a discounted valuation relative to peers, Pfizer represents an attractive investment opportunity.

Trade Idea: Buy Pfizer (PFE)

Long-term growth potential remains strong despite short-term setbacks.

Positive earnings outlook for the full fiscal year indicates resilience.

Consistent EPS beats highlight Pfizer's ability to manage its bottom line effectively.

Discounted valuation compared to industry peers suggests potential for stock price appreciation.

Consider a medium to long-term investment horizon to capture Pfizer's growth prospects and maximize returns.

S&P500 Dead-cat-bounce before one last bottom?Our last call on the S&P500 (SPX) couldn't have gone better as the Bearish Megaphone pattern we expected (April 05, see chart below) was eventually materialized and easily hit on Tuesday our 5050 Target:

At the moment the index is below the 1D MA50 (blue trend-line), which has been the main Support since November 03 2023 and is headed towards the 1D MA100 (green trend-line) above which the last two main Bearish Legs of the 19-month Channel Up made their first Dead-cat-bounce (March 02 and August 18 2023).

As long as this dead-cat-bounce is contained below the 0.786 Fibonacci retracement level, we see more likely one last corrective wave towards Support 1 and close to the 1D MA200 (orange trend-line). As long as at the time the 1D RSI is on its Support Zone, we will buy for the long-term and target the top of the 19-month Channel Up at 5400.

If the price breaks above the 0.786, we will have a pattern invalidation and buy the break-out instead, targeting again 5400.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

NASDAQ INDEX (US100): Technical Outlook & Trading Plan

Daily/4h time frames analysis for US100.

Price action & key levels.

Directional bias.

Thoughts.

Trading plan.

❤️Please, support this video with like and comment!❤️

S&P500: First 4H Death Cross since August 14th 2023!S&P500 has formed today a Death Cross on the 4H timeframe after 8 months (August 14th 2023), turning bearish on the 1D technical outlook as well (RSI = 37.122, MACD = -81.00, ADX = 53.782) as yesterday it crossed under the 1D MA50 for the first time since November 3rd 2023. Both are technically very bearish developments and according to the last 4H Death Cross, we remain bearish until we complete at least a -5.87% decline (TP = 4,980). Observe how the symmetry among the two fractals is very strong, both the Death Cross and the 1D MA50 breakout were done around the same Fibonacci levels.

See how our prior idea has worked out:

## If you like our free content follow our profile to get more daily ideas. ##

## Comments and likes are greatly appreciated. ##

S&P500(US500):🔴Is it Bearish...?!🔴(Details on caption)By examining the ES1! 4-hour chart (S&P), we can figure out that, the market structure is bearish, so we looking for a sell position.

In that case, the price had a bearish reaction to all of the bearish Pd Array, so we can expect a bearish reaction on the balance price range (BPR).

In my perspective, sell-side liquidity is a draw on liquidity. Until this sell-side is not purging I don't think about buy position.

💡Wait for the update!

🗓️15/04/2024

🔎 DYOR

💌It is my honor to share your comments with me💌

NASDAQ INDEX (US100): Correction Continues

After quite a long consolidation within a wide horizontal range

on a daily, US100 index violated its support.

That violation is an important sign of strength of the sellers.

It may trigger a correction lower, at least to 17500.

❤️Please, support my work with like, thank you!❤️

Trader Thoughts – defence the play of the day The markets have come alive with the sound of derisking, deleveraging, hedging and broad managing of risk exposures. Friday was about managing risk going into the weekend, but today was different and the move could have legs - where for many playing defence has been the order of the day, while we have also seen traders getting aggressive, with shorting activity in equity picking up, notably in Tesla.

On a cross-asset basis, there has been migration to buy equity volatility (the VIX sits at 19.2%), while there has been a further move into the USD, CHF, and gold, although the flight to quality was not broad-based with US 10-year Treasuries +10bp.

While US bond yields were already moving higher into the US retail sales report (+0.7% vs 0.4% eyed), the stronger outcome of the data set off a further sell-off in US Treasuries, with US 10-year yields pushing into 4.66%. The equity market was initially fine with the rise in yields, but as headlines rolled in that Israel had vowed a new response the sellers gained full control – it was when S&P500 futures traded through Friday’s low (5150) and then the 50-day MA (5142) that the floors lit up with more indiscriminate selling in equity.

The moves were then compounded by a rush to hedge risk, with funds buying volatility, where noticeable we saw the VIX index trade through 18% and into 19.46%. On the day 1.31m VIX call options traded vs 573k puts, so traders have been positioning for higher volatility and hedging portfolios accordingly. It’s no surprise that we’ve seen a sizeable 149k VIX futures traded, again well above average – higher market volatility leads to a whole range of selling activity from systematic players, and pension funds who target levels of volatility to determine their equity allocation. In these uncertain times high volatility begets higher volatility.

We’ve been left with the S&P500 tracking its highest high-low trading range since March 2023 (119 points), with price closing near the lows of the day. Plenty for the day traders to work with, and this sort of price action, with the various indices seeing a strong high-to-low trend day, will not have gone unnoticed, and to many, these are ideal trading conditions.

Momentum monitor – markets on the move

We see higher FX volatility playing through, with the USD ripping vs all currencies. There has been a solid unwind of carry positions, with the higher-yielding plays – BRL, COP, CLP, and ZAR – all seeing big percentage changes. The USD is king, and while overbought it is not at a stage where mean reversion players are just yet seeing a higher probability of a snapback. There are too many tailwinds for the greenback right now – haven appeal, momentum, relative interest rate settings and relative economic data trends. Pullbacks, it seems, will be shallow and well-supported.

Gold has been the classic geopolitical hedge, although we could have seen an even more pronounced move and a possible upside break of $2400 if crude (+0.2%) had participated. The fact that XAUUSD rallied 1.7% despite the move in the USD, and the 5bp rise in US 10YR real rates cements gold as perhaps the primary portfolio hedge given unfolding news flow. Conversely, there is a risk that gold could find a solid sell-down should Israel refrain from escalating, but for many the headlines suggest an increase in conflict is more likely than not and gold can offer defense in the portfolio.

Asia faces another tough day at the office, with the JPN225 called -1.4%, HK50 cash -1.2% and the ASX200 -0.7%. There is certainly not much in the news flow to inspire risk-taking and there is a growing list of factors to refrain from buying and to manage exposures, which of course, can see the buy side of the order book dry up, which means we get more exaggerated price moves.

China gets focus, not just because it performed admirably yesterday and we watch to see if the index can outperform, but also, we get Q1 GDP (consensus +4.8%), industrial production, retail sales and fixed asset investment.

Aggressive rate cuts are off the tableThe SPX retreated nearly 3% from its all-time highs following last week’s print showing a higher-than-anticipated Consumer Price Index (CPI) for March 2024. This marks a second consecutive month of accelerating CPI in the United States, which presents an obstacle for the FED in its more than two-year-long battle against inflation. Plus, it makes it increasingly unlikely that the central bank will engage in aggressive rate cutting as is still widely expected. Not only is it improbable that the FED will ease its monetary policy during the FOMC meeting between 30th April and 1st May 2024, but the latest print puts future rate cuts in jeopardy as well.

Since the start of the hiking cycle, we have believed that it will be challenging for the FED to lower rates quickly. Thus far, this opinion has been supported by elevated and sticky inflation. Furthermore, rising prices of commodities make an arguably good case for this to stay true also in the upcoming months, tying FED’s hands for a little longer. In turn, this raises the chances of the central bank constricting the economy too much, leading to an economic accident.

Illustration 1.01

Illustration 1.01 shows the daily chart of VIX. Yellow arrows indicate important technical developments in the past month. As the reality of no aggressive rate cuts is starting to sink in, there is a good chance that volatility will stay elevated in the near future.

Illustration 1.02

The price of WTI crude oil rose nearly 20% this year. The geopolitical tensions in the Middle East have been playing an important role in influencing its price over the past few months. If there is a broader conflict between Israel and Iran (which is at the highest odds in the past ten years), then oil could rise in the upper range between $90 and $100, putting further pressure on inflation.

Illustration 1.03

The image above shows the SPX in the ascending channel. The yellow arrow indicates a bearish breakout below the upper bound of the channel.

Technical analysis gauge

Daily time frame = Bearish

Weekly time frame = Bullish (stalling)

*The gauge does not necessarily indicate where the market will head. Instead, it reflects the constellation of RSI, MACD, Stochastic, DM+-, ADX, and moving averages.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor or any other entity. Therefore, your own due diligence is highly advised before entering a trade.

Resumption of the bullish momentum?The S&P 500 (US500) has made a bullish reaction off the pivot and could potentially rise towards the 1st resistance.

Pivot: 5,117.40

1st Support: 4,956.50

1st Resistance: 5,263.47

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

US500 Will Go Up! Long!

Here is our detailed technical review for US500.

Time Frame: 1D

Current Trend: Bullish

Sentiment: Oversold (based on 7-period RSI)

Forecast: Bullish

The market is testing a major horizontal structure 5122.2.

Taking into consideration the structure & trend analysis, I believe that the market will reach 5315.3 level soon.

P.S

Overbought describes a period of time where there has been a significant and consistent upward move in price over a period of time without much pullback.

Like and subscribe and comment my ideas if you enjoy them!

US500 is under the pressure of a strong dollarHey Traders, in the coming week we are monitoring US500 for a selling opportunity around 5200 zone, US500 is trading in a downtrend and currently is in a correction phase in which it is approaching the trend at 5200 support and resistance area.

We would also like to consider the current bullish momentum on the dollar, due to the negative correlation a strong dollar usually put pressure on indices like S&P500.

Trade safe, Joe.

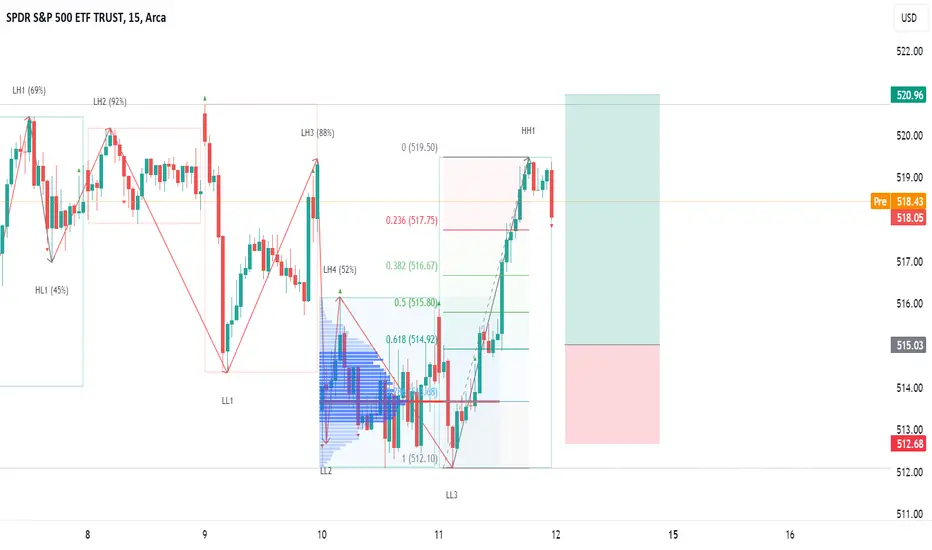

SPY LONG: scout for hourly higher lowBulls defended the weekly low and made a convincing breakout yesterday. This is a powerful statement, although buyers have not yet proven their control. To do that, they must first establish a weekly higher low, which is likely to happen next week (of course, we need to monitor how things develop). This presents a great opportunity for a long play, but buyers should wait for a pullback and scout for an hourly higher low. Ideally, this should occur near the previous Volume Area High (VAH). An example of the trade is shown on the chart.

You can read full analysis of the market below

Disclaimer

I don't give trading or investing advice, just sharing my thoughts.

S&P bears attack, bulls still holdLast week was marked by the aggressiveness of sellers and the resilience of buyers. On Monday Buyers were ideally positioned for another break out but they didn’t have enough steam to accomplish it. Sellers, long awaiting their opportunity, pushed the price down, breaking the weekly support. However, they couldn’t develop this into something more significant, as the bulls returned with a firm "no". The rest of the week continued in the same tug-of-war fashion.

The most confusing days were Thursday and Friday. Thursday started very bullish but ended with a dramatic bearish turn. Friday, expected to be bearish, unfolded under the bulls' control.

This was a story. Now, let’s now review all the signals more formally:

Bearish Signals

• Confirmed downtrend on the daily chart, indicated by a lower high and lower low.

• Weekly consolidation has begun.

Bullish Signals

• The week closed right at the previous week's low after price shaped hourly higher low

• Friday’s value zone is within the value zone of the previous four days.

The context remains very bullish – price is in a strong weekly uptrend, last month closed very strong. Overall, it is a very ambiguous case with neither side having a clear advantage. Buyers are exhausted, yet not willing to capitulate. Bears are attempting to play their game but lack sufficient strength.

The short-term outlook is neutral. From this position market can go in any direction. We need additional signs of one side gaining an upper hand. Until then, it is not advisable to place big bets on either side.

Wednesday is a very important day, with both the release of inflation data and the FOMC meeting

Disclaimer

I don't give trading or investing advice, just sharing my thoughts.