SP500 spx spyThis is my best estimate. While we could possibly already be in the C wave down and finishing up on a minor wave 2....I am thinking that the FED may continue to do the same as before and prop the market up into the FOMC meeting on March 15th. This is just a guess. If that is the case then perhaps we can reach near the 2800 level again before starting a 5 wave drop. GL

UVXY

SP 500 "weekly view"SO obviously we are in the supercycle 5th wave. Inside that, we are in the 3rd wave. Inside that 3rd wave we have just completed the smaller degree 4th wave (even thought it felt big) and are about to trek up for that smaller degree 5th and complete the larger 3rd wave. The drop for the larger 4th should be huge and impulsive just like this last drop. I was expecting an impulsive drop because of the wave 2 corrections being long and slow. So the same goes for this next drop. Timing it is not something I wish to really do right now, except that if the larger cycles are still about correct, then it could start with a September rate hike and end towards the end of the year. GL

VIX √12 = SPX anticipated 30 day move %This is a commonly used calculation that many traders use, I believe it's also part of the CMT.

UVXY - GAP DOWN POSSIBLE BUY STOCH(17) oversold and DMI(17) holding. Gap down in oversold could be quick move to upside.

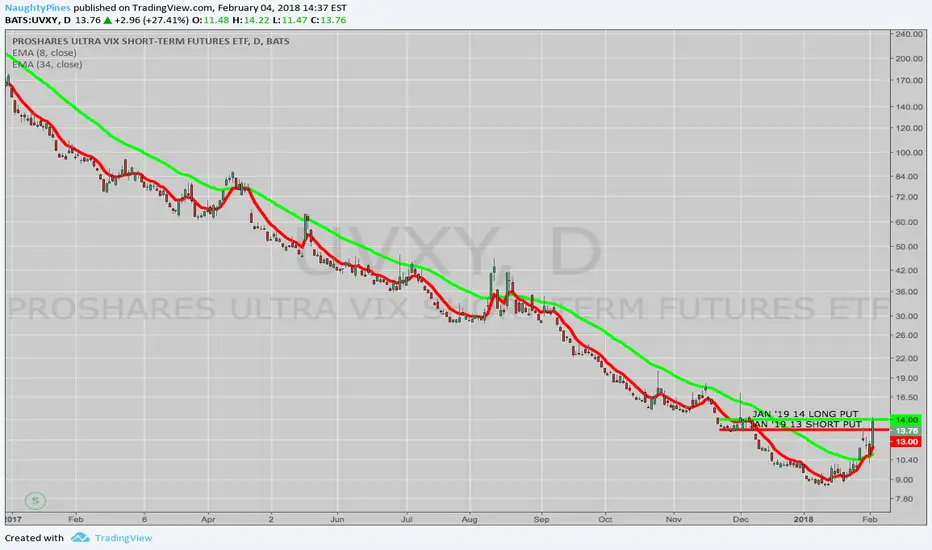

UVXYShort UVXY via long Apr20 put debits for $2.19.

POP: 68%

Max loss: $892 (2.19 x 4)

Max Win: $308

ROC: 34.5% over 66 days

Long 24 put: 36 delta

Short 21 put: 30 delta

I usually let these expire ITM, as my broker TW has cheap exercise fees. In the case that it expires in between strikes, then I will have to manage them by closing on expiration day.

Example Of Shorts CoveringYou can see the company has the biggest volume probably ever, or in a long time at least. It is shorts covering. They revealed the previous day that they would be divesting from their VAR project, which accounted for 93% of revenue. They just diluted shares signifantly, then did a reverse split. They even tried a vote in December, which failed, so had to hold a Special Meeting, in order to cast a re vote. All that trading volume is shorters

DMI(17): DI+ fell out of flag and heading into supportDMI(17): DI+ fell out of flag and heading into support around 20

TRADE IDEA: UVXY -- TIME TO LOOK AT LEAPS?It's not often that I play leaps or think of myself as "playing leaps." In case you're wondering, a "leaps" is a "long term equity anticipation security" -- basically, a long-dated option. My most frequent use of them is in my individual retirement account where I'm working a covered call, want to hold onto the underlying for dividend generation, but also want to use the short call leaps as a capital preservation tool and push it out far out in time to decrease the likelihood of my shares being called away.

Here, they serve a different purpose in these particular underlyings (UVXY, VXX) -- namely to take advantage of a short-term pop in volatility (which were infrequent over the past year) without getting caught up in short-term gyrations volatility may experience that may make shorter term setups frustrating because they run out of time for volatility to mean revert and/or experience significant contango erosion or beta slippage (I have a few of those on that are, at best, "troubled" here).

Traditionally, I have seen two approaches to these long-dated setups intended to take advantage of occasional short-term pops: (1) setups that calculate the approximate erosion/beta slippage the underlying will experience on average over the life of the setup and then sells a credit spread or buys a debit spread at or near the strike at which the price of the underlying is likely to settle toward the end of the option's life; and (2) at-the-money setups.

Since a lot of different things can happen during the life of an option such that the average contango erosion or beta slippage is monkeyed with -- making an approximation of where price will potentially settle a less than accurate endeavor, I'm going with the latter type of setup here -- buying an at the money debit spread, with the spread straddling current price (i.e., the long above, the short below). A few tips ... .

(1) Since the UVXY leaps aren't the most liquid things in the world, a fill will require a touch of price discovery, so I will start with trying to get a fill for 50% of the width of the spread (hey, we can all dream, can't we) and then adjust the fill price to see if I can get a fill for no less than one-third the width of the spread.

(2) This isn't a setup for the impatient. It's a set and forget. With that in mind, keep the spread width and/or number of contracts small such that the buying power effect relative to your account size is within your risk parameters and leaves you with plenty of dry powder to take advantage of further pops in volatility (they may have been infrequent over the past year, but they happen).

(3) Give some thought as to how wide you want to go with the spread. Going extremely narrow may, in essence, prevent you from "squeezing in" additional spreads in the particular leaps expiry you're using. If I put on the example shown here, I won't be able to buy 14/15 debit spreads going forward, since selling 14 short legs will close out the 14 longs of the 13/14's, so going wider with the spread and using fewer contracts may give you greater flexibility to use this expiry for further setups going forward. That being said, I can always sell 13/14 short call verticals in the futures without "stepping on" the 13/14 long put verticals, if I choose to go narrow with the debit spread.

(4) Early on, the ride could be "rough." High volatility environments tend to have a short life, but that doesn't mean that higher volatility can't last longer than it's comfortable for you as a trader or that any given period of time doesn't have the potential to do things that aren't "average" in nature of what we've experienced since February of 2016 (winner, winner, chicken dinner for short volatility ... ).

Skewed Strangle on UVXYAfter a brief moment of Backwardation this week in the term structure of the Vix futures, we came back into Contango. To me it looks like there is still some fear and buying protection is not getting cheaper, especially with earnings coming up on some of the big dogs. I believe volatility will start to come off during the next couple of days, so I want to add to my core short volatility trades.

UVXY Implied volatility is still very high so I decided to sell some premium.

I sold the 12/8 Strangle for $2.60.

What can go wrong? If UVXY rises over 35% in the next 42 days I will get assigned 100 Shorts per contract. I don't mind being short volatility since that would just be an addition to my already core shorts (Part of the plan).

Getting long is another ballgame, and one I don't like that much (So I skewed the Strangle to the downside). But for this to happen First UVXY would have to drop over 48% in the next 42 days. If that happens I will be pretty happy making a killing in the rest of my Shorts. On this one, I would take the assignment at the $8 price with a cost basis of effectively $5.40. That is a pretty low price (Most likely would have reverse split by then) and I am sure I can Sell some Calls after to get out of the trade on top.

The trade:

Short 12 CAll

Short 8 PUT

Credit received $2.60

Probability of profit is 63%

WATCHING MONDAYAll converging. Volume and activity dry up, if you see some nice volume in the premarket, could turn into a nice bounce in the open. These are all like, the "blue chips" of bitcoin stocks, the originals with the most volume.

SP500 " This is not the big one yet"This is only the 5% drop that I was talking about. I was hoping it started a week or two later but oh well.

sp500 a little moreI think I can see it.. Yes this has been very tricky. When I see it bust through then I wait to see what the market wants to show me and adjust. As you can see,....IT APPEARS...LOL....like we are if the final wave 5. Today was a small wave 4 and we should move up in the next day or two. Since the larger wave 1 was the longest, wave 5 cant be longer than wave 3. So there is the FIB measurement for wave 3 and as you can see, there is a nice 2900 number just below the 100% wave 3 measurement. Can this be it finally? I think so. This correction (once it get started) should be a good one. But I really think the first part down could be only 5% for the A wave. Then of course the annoying B wave. And that should take us into March or possibly all the way to April before the much bigger 10 - 15% wave C. Ill try me best to time it based on the B wave back up.

Volatility to return in 2018!SuperTrend buy signal triggered.

We have crossed the rubicon and are now at market levels where retail investors and permabear "professionals" who have been sitting on the sidelines during this most hated bull market in history are compelled to throw in the towel.

As they finally re-enter the market, it will lead to increased volatility and I expect up to a 10% correction in the major US indexes in the first half of 2018.

Additionally the short volatility trade is extremely lopsided and will not take much of an uptick to unravel.

While I do expect volatility to increase significantly from major lows this year, it doesn't mean the major US stock indexes will be negative at year end. To the contrary, I expect more all time highs as the year progresses alongside an uptick volatility which will be a scenario most have not seen often.

SP500 "Very long term projection" Weekly ChartSO please do not mind the messiness of this chart as I had to go to the weekly view and zoom way out which squishes everything together. I made a long term chart about a month or so ago and realized that my topping date was incorrect. You see, I truly believe that Trump will not get re-elected for a second term and I am using that as the trigger date. Just my guess on that. I originally, mistakenly thought that the election date was November 2019, but it is really 2020. So I had to move the election line and have two channels for two possible target areas. (obviously this is just a guess but lets have some fun shall we). The first black lined channel is narrowing as you can see. This is the line that hits the tops of this long bull run that started in 2009. If we only maintained that channel then the top of that channel by election time is around SP500 4300 - 4400 which should equate to DOW 38,000 - 40,000. (Not too shabby if you ask me). BUT. Does that really look like a parabolic bubble phase that has been spoken so much about. No it does not. SO what is the market capable of. I went back to the 1990's and mapped out the trajectory of price for that 5th wave of the large 3rd wave. That is what a bubble parabolic looks like. So first I took the bottom line of the channel and copy/pasted it to make an alternate upper channel that is parrellel. Then I took the 1990's price action and placed it to cover the next 3 years. And what do you know, that looks like a very good parabolic bubble phase and coincidently reaches the top of that upper channel around election time. Wild guess, I know. But why not. If, as you can see, we happen to reach that area then that would equate to DOW 48,000 - 50,000. And that is how these people have come up with Dow 50,000.

At that point Gold should be bottoming at that point and everything should be in a bubble. I would be selling my house around that time if this transpires and buying a ton a physical gold and silver. GL

Dow 30 000The VIX has never been this low, ever.

The Dow's daily trading volume has never had so many massive monthly volume bars in such a short time period, unless it was a big sell off, or dip buying after a massive recession.

The only risks are war, disease, or Trump getting impeached. This shutdown will cause a little pull back, but the trend will continue

SP500I think we will get a little more of a drop early next week before we push up. This consolidation is taking a long time so I have to adjust the target accordingly. I read a very brief but probably very true tweet about end of year profit selling. This guy said that there will be minimal selling for the end of 2017 because people are probably going to hold off until January 2018 to take advantage of the tax cuts. Well that makes sense. There is a small short term bullish divergence forming. We still have not resolved the long term very large bearish divergence but that might happen in January like that guy said. Time will tell. Be ready.

THINKING AHEAD TO (YET ANOTHER) UVXY REVERSE SPLITAs I thumb twiddle a bit here waiting for another VXX weekly expiry to open up and for a UVXY reverse split, I'm pondering potential long-dated plays in UVXY I can put on immediately post-split that are basically "set and forget" plays.

I have seen evidence in both open interest and volume of people playing both ends of the stick at split when the price of the underlying -- in all likelihood -- will be at a high point, after which contango erosion and/or beta slippage will ensue: (1) buy long-dated (as long as you can go) at-the-money or deep-in-the-money puts; or (2) buy long-dated out-of-the-money puts for about the price you would pay to put on your standard 3-wide long put vertical (or less; some folks literally buy the most out-of-the-money, cheapest long puts they can lay their grubbies on). Because I'm literally not made of money, option (1) is out -- deep-in-the-money is just plain ass pricey on a per contract basis, and I question the usefulness of paying more than you have to in intrinsic and/or extrinsic value when the play is that the underlying is going to erode from that point forward over longer time frames -- just being deeper in the money doesn't necessarily pay more in that event unless you are paying less extrinsic by going that way.*

Consequently, the play I'm going to put on immediately post-split is out-of-the-money long puts in a strike where I'm paying around 2.25 or less per contract (obviously, the less, the better) in the longest dated expiry that exists at the time of the split.** Naturally, it's difficult to price these out at the moment, so I'll just wait for the split and price them out then ... .

* -- The general rule with most underlyings is that the deeper you go in the money, the less extrinsic you should pay. However, if you want to buy a Jan '20 35 long put at the moment (an extreme example, I know), it'll cost you 29.95 at the mid. 35 (the strike) minus 9.67 (current price of the underlying) = 25.33; 29.95 (the price you'd pay for the long put) minus 25.33 = 4.62. That 4.62's extrinsic value you're paying for up front, and that will decay over time.

** -- I can also see the potential in just buying deep out of the money long put verticals instead "on the cheap." Having a short put aspect as part of the play will naturally offset some of the extrinsic you're paying for the long. To a certain extent, it's a matter of how much you want to stick out there for how long ... .

THE WEEK, MONTHS AHEAD: VIX, VXX, UVXY, SVXYAs 2017 comes to a close as one of -- if not the -- lowest volatility years ever on record for the S&P and Nasdaq, I'm not hopeful that this low volatility won't continue for some time to come. To be honest, though, no one really has any way of knowing or predicting volatility going forward, except in the most obtuse of ways, such as forecasting market performance over a given time period or pointing out exogenous risks, which can in turn drive the volatility environment. Since predicting volatility going forward is a total crap shoot to me, I feel it's best to play the ball "from where it lies" and to adapt when the environment changes, rather than trying to predict when and how much it's going to change.

With this in mind, I plan to continue to keep doing what appears to be working (and, really, what has always worked, albeit with some periodic bumps in the road): shorting volatility products that have been the gift that kept giving in 2017, as much as being bullish broad market (short puts, short put verts, long call verts, long calls) was pretty much the gift that kept on giving in the same time period. At some point, this strategy will in all likelihood cease to work so well; until that time, it's just a plain time saver not to worry about checking the high implied volatility screener on a daily basis, since -- in all likelihood -- I'm not going to find anything there that meets my basic premium-selling criteria until things change their tune in substantial fashion from a volatility perspective. Previously, I religiously checked that screener on a daily basis (I probably still will; old habits die hard), but my guess is that the markets will continue to make that mechanical approach to premium selling in this market very short work, as that process has repetitively yielded very few worthwhile candidates for premium selling for weeks (if not months) on end in the stuff I like to trade -- broad market and sector exchange traded funds.*

This week, I foresee only doing my weekly VXX long put vertical trade; the way it's looking, it'll be the Feb 9th** 27/30's or 27.5/30.5's given where VXX is at now. As previously pointed out, I'm hesitant to wade into UVXY here given its lowness to the deck and the likelihood it'll reverse split soon. The reverse split is not a "deal killer," but rather just a choice not to be in some funky, non-standard options contracts post-split. As always, I'll keep an eye out for any VXST/VIX >1.00 or VVIX >110 pops; it's possible that we could get one as investors opt for taking tax losses in their crap piles before the year's done and/or reposition anew in 2018 ... .

* -- Naturally, I'm way more picky than some as to when sell premium. I expect certain things out of premium selling setups profit-wise relative to accompanying risk, and if those things aren't there, I'm just not going to play the market that way. The alternative approach is to take what the market gives you, regardless of implied volatility; this approach has its merits (cash flow, for one). After all, having no premium selling plays on in this market generates "nothing" cash flow; having something on generates something; and something is always greater than nothing.

** -- Feb 9th should open up on Thursday, if I'm not mistaken.