Valuation

6B Swing Short Swing short, COT - Valuation - Supply and Demand.

Been waiting a long time to short the pound..

HEG Limited Stock Analysis [Fundamental+Technical]Company Overview:

Industry: Graphite Electrodes (used in Electric Arc Furnaces for steel production)

Parent Group: LNJ Bhilwara Group

Location: Largest graphite plant at a single location near Bhopal, MP

Global Reach: 67% export-based; presence in 35+ countries

Business Highlights

Products: UHP & HP Graphite Electrodes

Customers: Top 25 global steel companies

Capacity: Increased to 100,000 TPA in Nov 2023

Utilization: 81% (despite global slowdown)

Revenue from Operations: ₹2,394.90 Cr

Net Profit: ₹231.54 Cr (down 49% YoY)

EBITDA: ₹525.63 Cr (down 28% YoY)

EPS: ₹59.99

Net Cash Flow from Operations: ₹615 Cr (up from ₹114 Cr)

ROCE: ~7.2%

Return on Net Worth (RoNW): 5.63%

📈 Technical Insights:

Current Price: ₹474.60

50 EMA: ₹431.44 (support zone)

200 EMA: ₹429.40 (support zone)

Price is trading above both EMAs, indicating a bullish trend reversal.

Golden Cross formation (50 EMA crossing 200 EMA) recently occurred — a classic long-term bullish signal.

The stock bounced from ₹400 zone and now forming higher highs.

Key Strengths

One of the lowest-cost graphite electrode producers globally

Among top 5 global players (ex-China)

Strong relationships with major steelmakers

Backward integrated captive power: 76.5 MW

State-of-the-art technology and high R&D focus

Key Risks

Highly dependent on steel sector demand

Pricing pressure due to global oversupply and China's export surplus

Needle coke (key raw material) cost volatility

Current underutilization of capacity

Growth Triggers

Green Steel Push: EAF-based steel production expected to grow globally

Anode Powder Plant: ₹1,800 Cr investment in 20,000 TPA facility for EV battery anode materials; revenue expected from FY27

India’s EV & Steel Boom: Growing steel consumption (8.2% CAGR) and EV transition are long-term positives

SWOT Summary

Strengths:

Global presence, high export revenue, low-cost structure

Technological leadership

Weaknesses:

Profitability linked closely to global steel demand

Volatility in raw material prices

Opportunities:

EV market and EAF steel expansion

Threats

Competition from China, diversion of raw material to battery sector

Future Outlook

Near-term challenges due to soft steel demand

Medium to long-term outlook is strong, driven by:

Increasing EAF penetration

Global decarbonization policies

Strategic expansion into EV-grade graphite anodes

Analysis Based on Valuation + Chart

CMP:₹474.60

Fair Price Range: ₹600 – ₹1200(Using a conservative P/E range of 10 to 20)

Fair Value (DCF):₹1100+ (Based on 10% projected EPS growth over 5 years and a 12% discount rate.)

Support Levels:₹430 (EMA), ₹400 (price action)

Resistance Zones:₹490-500 (near-term), ₹600 (supply zone)

Disclaimer

The information provided in this report is for educational and informational purposes only and should not be construed as financial or investment advice. While every effort has been made to ensure the accuracy of data and analysis, no guarantees are made regarding future performance. Stock market investments are subject to market risks, including potential loss of capital. Please consult your financial advisor or conduct your own due diligence before making any investment decisions.

Is it going to happen again? My view to the markets right now...CBOT_MINI:YM1!

Is the Dow Jones breaking the downtrend again?

I believe there's a strong chance the markets are setting up for another move higher. From a fundamental standpoint, the recent pause in tariffs is a big deal. It removes an immediate layer of uncertainty that’s been hanging over the global economy, especially for exporters and multinational companies. On top of that, the fact that key tech products have been left out of the latest tariff actions is boosting confidence in the sector that has been leading market strength for years.

Economically, we’re still seeing resilience in key indicators. Unemployment remains low, consumer spending is steady, and central banks are staying cautious with tightening. The environment still leans more towards slow growth than recession, which supports equities over the medium term.

More importantly, my own criteria for a favorable market setup are lining up. Whether it’s sentiment, intermarket signals, or trend conditions—this looks like a solid spot for a bullish stance.

You can see my chart to check out my current viewpoint on the Dow Jones and how I’m positioning based on all this.

Not Financial Advice

Promising Breakout Setup Ahead! Chart 1W CBOT_MINI:YM1! BLACKBULL:US30

Promising Breakout Setup Ahead!

The chart highlights RSI and Williams %R trendline breakout plays. My strategy? Identify trendlines on the chart, monitor RSI and Williams %R, and target breakouts on these momentum indicators.

Current Situation:

All key signals have already triggered.

Strong bullish seasonality

Favorable COT data (small specs bearish, commercials bullish)

Low open interest

This setup aligns with high-probability breakout criteria.

Chart Indicator

SMA 1W 52 (red)

SMA 1W 18 (green)

Bottom Indicators

WilVal

Williams R% 9 length

RSI 9 length

Not Financial Advice

for more questions ask in the comments or

check my X @valuebuffet

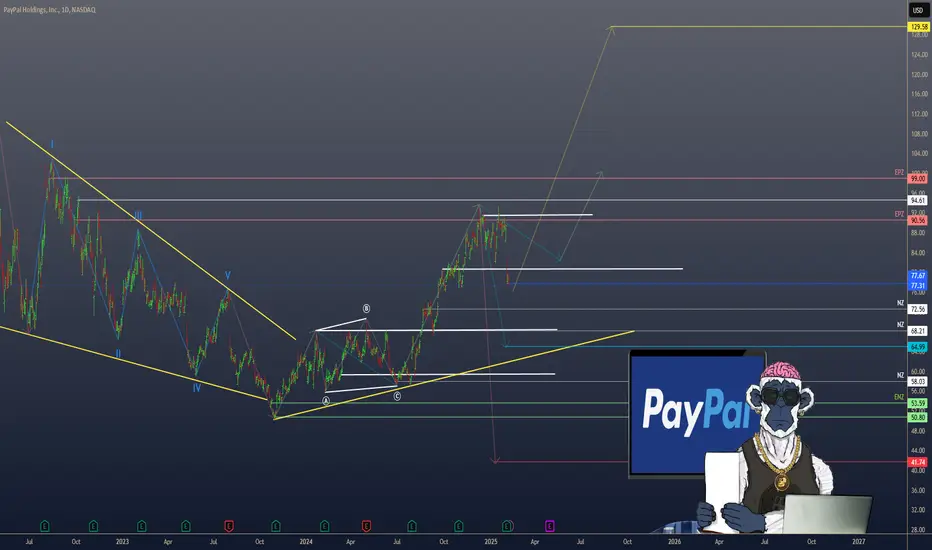

$PYPL PAYPAL’S FINANCIAL LANDSCAPE: VALUATION & OPPORTUNITIESPAYPAL’S FINANCIAL LANDSCAPE: VALUATION & OPPORTUNITIES

1/8

PayPal ( NASDAQ:PYPL ) has been on the move lately—announcing a FWB:15B buyback and posting mixed but intriguing earnings results. Let’s dive into what’s making this fintech giant tick! 💳💡

2/8 – Recent Revenue Growth

PayPal’s revenue soared during the digital payment boom but has moderated recently.

Although the exact figures aren’t in the latest posts, growth since 2017 is substantial.

Stabilization might indicate a new normal in digital payments.

3/8 – Earnings & Guidance

Some quarters saw EPS pop by 61%—pretty impressive! 🚀

Mixed guidance ahead: margin expansion concerns and flat-to-down cash flow.

The FWB:15B buyback suggests management sees long-term potential.

4/8 – Valuation vs. Peers

Forward P/E near 10, PEG ratio of 0.52—that’s cheap compared to Visa/Mastercard.

PayPal straddles fintech + payments, competing with everyone from Square ( SET:SQ ) to Apple Pay.

Lower growth vs. some peers, but strong operating margins help PayPal stay ahead.

5/8 – Risk Factors

1️⃣ Regulatory: New rules could cramp expansion.

2️⃣ Market Saturation: Need emerging markets to fuel next leg of growth.

3️⃣ Competition: Stripe, Apple Pay, & countless fintech upstarts.

4️⃣ Tech Disruption: Blockchain, AI, or next-gen payments could reshape the landscape.

6/8 What’s PayPal’s biggest near-term challenge?

1️⃣ Regulatory Hurdles

2️⃣ Competition

3️⃣ Market Saturation

4️⃣ Tech Disruption

Vote below! 🗳️👇

7/8 – SWOT/SCOT

Strengths: Massive user base, recognizable brand, buyback confidence.

Weaknesses: Slowing user growth, uncertain future margins.

Opportunities: Emerging markets, strategic partnerships, AI integration.

Threats: Fierce competition, cyber risks, evolving payment tech.

8/8 – Your Next Move?

PayPal’s at a pivot—undervalued or a value trap? 💰

Let’s see if NASDAQ:PYPL can keep up the momentum!

#PayPal #Fintech #DigitalPayments #PYPL #Investing #Earnings #Valuation #Finance

$NKE Nike, Inc is finally back to CHEAP-ENOUGH levelsMany years ago I had drawn this 1.7-1.3 level in the PSR (or Price-to-Sales Ratio) for NYSE:NKE and the recent smack down for NYSE:NKE stock has put it within reach of the 1.7-1.3 X Sales zone.

The RETURN for shareholders has been negative for the last 7 years in NYSE:NKE when adjusted for inflation. The stock is basically unchanged back to 2018 here (not factoring dividends).

What is the point of this?

When a stock gets sold down on bad news, there is an underlying level of value which will support it from that point forward. There are always portfolio managers looking to invest in stocks that have had solid long term fundamentals with rising sales and earnings and a nearly recession-proof business model.

The opposite is also true that there are NO BUYERS for a stock once it gets ridiculously overpriced and no one can justify buying shares are high prices. The only hope you have at that point is for momentum to attract new buyers who aren't paying attention to valuation and because of tax laws that encourage people to hold on for long term capital gains tax rates to kick in for holding periods greater than 1 year.

Thanks to TradingView for providing all of this high quality fundamental information AND for the ability to graph this data so we can visualize and see where the value is in the marketplace.

The value is down here in NYSE:NKE shares so it is a good time to start buying.

Cheers,

Tim

3:47PM July 1, 2024 76.67 last +1.30 +1.72%

Wave of the day: Visa

5 good reasons for NYSE:V stock

1. Bounce from the value zone

2. Rising MACD histogram

3. Buying Volume coming in

4. Pocket Pivot on the last day

5. Analysts have set a mean price target forecast of 160.17. This target is 20.33% above the current price.

What's your take on Visa?Comment below

Legal Disclaimer: The information presented in this analysis is solely for informational and educational purposes only and does not serve as financial advice.

Soft landing calls for tough choices2023 has been a tough year for stock pickers. The gap between equity factor styles has been vast over H1. Growth, riskier in nature, posted the best performance up 24% year-to-date (YTD) followed closely behind by quality up 20% YTD1. The excitement around artificial intelligence (AI) reached a fever pitch in H1 2023, supporting growth-oriented technology stocks.

As we enter H2 2023, we remain constructive on select areas of global equity markets. The resilience of the US economy has defied all odds. The strength of the US consumer (accounting for 70% of GDP), alongside the fiscal impulse, has been the cornerstone of the US’ extraordinary resilience. While inflation has shown encouraging signs of decline in the US, strong economic momentum alongside a rebound in commodities raises the risk of a re-acceleration of inflation. In turn, rates could remain higher for longer, resulting in Federal Reserve (Fed) rate cuts being delayed until Q1 2024. In such an environment, an enhanced equity income approach could fit well. Even if the earnings outlook weakens in China, proactive policy support via rate cuts could support its stock multiples.

In Europe, where we are likely to witness a mild recession, we believe adopting a more cautious and defensive approach is warranted. Earnings revision ratios remain the strongest in Japan while they are the weakest in emerging markets.

US equities are the belle of the ball

It was the narrowest market in history, with just 25% of stocks outperforming the S&P 500. Expectations of cooling inflation aiding the Fed to end its current tightening cycle supported the performance of higher-duration growth stocks. For investors calling for a soft landing, rates are likely to remain at current levels or higher for a longer duration of time. A tight US labour market, with unemployment at historic lows and rising wages, is likely to slow the downward pricing momentum in the service sector. As the market regime transitions, it should provide a ripe opportunity for market breadth2 to improve. Markets may begin to favour value and dividend-paying stocks. History has shown us that breadth tends to improve as the economy recovers from a downturn.

Peak pessimism towards China

China’s reopening rebound has faded. The transition to a less debt-fuelled, less property-reliant and more consumer-driven economy is an important adjustment. We expect government stimulus policies to be aimed at enhancing the efficiency of the private sector. Further iterations of policy rate cuts by the People’s Bank of China (PBOC) are likely to follow; however, outright quantitative easing won’t be on the cards, as it is likely to further weaken the yuan, which the PBOC would like to avoid. With a low correlation to US equities (at 20x P/E)3 coupled with a high valuation discount, pockets of China continue to provide good investment prospects.

Pockets of opportunity in non-state-owned enterprises

Non-state-owned enterprises, particularly within the Technology, Communication Services and Health Care sectors, faced the brunt of China’s regulatory crackdown. These regulatory interventions stifled growth in key sectors such as e-commerce, mobile payment, ride-hailing, and online education. It also resulted in the suspension of initial public offerings (IPOs) and delisting of Chinese internet companies. Growing political frictions in supply chains are incentivising China to regain independence in the semiconductor and hardware space. Chinese technology companies are trading at a significant discount compared to US peers, offering plenty of room to catch up.

Prefer defensives over cyclicals as Europe runs out of steam

Nearly six months back, investors marvelled at how the euro-area economy had emerged from the energy crisis. That momentum appears to be fading as China’s recovery slows down, consumer confidence declines, and the impact of tighter monetary policy gains a stronghold on the economy. Higher inflation over the past year is holding back demand from households, which is hurting growth.

The monetary tightening over the past year not only triggered an increase in real rates, it also impacted borrowers’ credit metrics. Owing to this, eurozone banks have tightened their lending standards.4 Banks remain the primary source of corporate funding in Europe. The credit impulse—that is, the annual change in the growth of credit relative to GDP—in the euro area reached its lowest point since 2010.

TINA is alive in Japan

There is no alternative (TINA) to equities is still alive in Japan. This is evident from higher equity risk premiums of 2.97% for Japan compared to 0.41% in the US.5 While the rest of the world has been busy trying to quell the inflation fires, Japan has emerged from the COVID-19 lockdowns with a faster pace of growth and higher inflation. A combination of higher equity risk premiums, a weaker yen supportive of the Japanese export market, corporate reforms, and attractive valuations have been important catalysts for equities.

Policy shift still remains loose

The Bank of Japan (BOJ) took a significant step towards normalisation in July by announcing a further adjustment to its yield curve control (YCC) regime. The BOJ formally changing its course constitutes an acknowledgement that inflation is returning to the Japanese economy. Yet the BOJ lowered its (median) inflation forecast for fiscal year (FY) 2024 to +1.9% and left its FY 2025 projection unchanged at +1.6%, in effect justifying ongoing easing by the BOJ. With Japan’s nominal growth rising over the coming years, the revised policy by the BOJ still remains loose, supporting the case for Japanese equities. Historically, a weaker yen has benefitted the performance of Japanese exporters as it enhances their competitive advantage. Adopting a tilt towards dividend-paying Japanese equities is likely to reap the benefits of not only a weaker yen but also corporate governance reforms.

Conclusion

As we progress into year-end, the outlook remains more nuanced. In the US, we favour value and dividend stocks as equity market breadth improves. While China’s problems in the housing sector are likely to remain a drag on domestic demand, we do see pockets of opportunity in undervalued sectors – technology and healthcare. Given the strong manufacturing headwinds facing Europe, we expect weak growth in the eurozone for the remainder of 2023, potentially favouring a tilt towards defensive stocks.

Sources

1 Bloomberg as of 11 October 2023.

2 Breadth is measured by comparing the equal weighted performance versus the market cap-weighted performance of the US stocks listed on the S&P 500 Index.

3 P/E = price to earnings ratio.

4 Euro area Bank Lending Survey (BLS), April 2023.

5 Bloomberg, WisdomTree, as of 29 September 2023. Equity risk premium is the difference between the earnings yield and the respective 10-Year Government Bond Yield.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

SkyWest (SKYW), Valuation Chart for InvestingLooking at the average analyst target and Anchor for NASDAQ:SKYW I see some potential downside in the near future that could present some buying opportunities. The company has been one of the only Airlines that I am willing to invest in at the moment.

Overall, SkyWest has had a mixed earnings growth trend over the past 4 quarters. The company has reported both positive and negative earnings growth during this time period. The company's earnings growth trend is likely to be affected by a number of factors, including the overall economic environment, the performance of the airline industry, and the company's own operational performance.

This also should provide great opportunities to buy in... Fundamentals are looking good.

Valuation Chart for AMD, Average Analyst Targets and ForecastsFor those that believe that some how AMD will magically stay at these levels, please keep in mind, the average analyst target is $103.43. On top of that, I believe the company is Anchored at lower prices based on projected earnings growth and cost of equity. This stock will revisit lower levels once again.

Inflection PointBKI caught my attention for a few reasons.

1. Held by Scion Asset Mngt- if you haven't heard of them or Michael Burry, check it out. Crazy returns off the financial Crisis.

2. SP sitting at an inflection point at bottom of long term demand zone and near lowest long term demand zone.

3. BKI's shiller PE ratio range over the past 10 years is from 36.26-43.09 and currently sitting at 37.37 implying that it is near its lowest valuation in 10 years.

4. Mornings Star Fair Value market valuation sitting at $61.1. My own target of $77.5 is based on a Fibonacci retrace of 61.8% of 2020 highs.

Applying Warren Buffett and Peter Lynch valuations : SNAP stockWhen I was new, I traded just the picture of prices.

Later after living through a full cycles, I learned stocks were actually businesses.

Business sell stuff to customers and generate revenue each year.

Businesses have cash flows and earnings.

Thats why when we look book 10 to 20 years, most businesses are more valuable today then back then.

Valuation looks at what things are worth today and also looks at future potential.

Financial math is discounting the the future growth to make sure you get the best deal you can.

Valuation keeps you grounded.

You can still day trade, swing trade, and option trade all you want. Valuation just helps you know the true value inside the business so you avoid some losers and pick more winners.

Cheers and good luck on your journey!

#snap #warrenbuffett #peterlynch

Momentum vs Business Valuation"The momentum guys take it up to the moon,

the value guys pick it up off the floor.

Just watch out for the space between the two."

-Confucius the trader

have been reading up on the Turtle Traders and their momentum strategy. They would have bought anything as long as it meets their break out rules. Fascinating statistical strategy based on both 20 period price action and 55 day price action. Im sure they love the action in NVDA right now.

However, in the valuation books. The oldies but goodies books (Intelligent Investor by Benjamin Graham, Beating the Street by Peter Lynch) they would be less enthusiastic about the current valuation. Most useful would be Peter Lynchs PEG ratio, where growth rate is used to allow paying a higher price than normal for growth stocks.

The roughly 30% growth rate annual expectation in this case would mean if NVDA falls below 30pe, it would be attractive. Its almost twice that now. Thats not necessarily a reason to sell a quality stock. it just means that investors have already market up the stock and are buying it ahead of the future growth being expected. In this case, 2026s future growth.

Traders gonna trade. They dont care about the future value of a stock. they care about Profit this week or this month and then on to the next one.

however the investors do care. They are looking for getting a deal on something that can swell up with earnings and juicy future value dividends. Investors want a discounted price today, and 20 years of accumulated earnings so they can milk the future dividend payouts.

Any who, just watch out and be aware. Its a fast horse, its also a popular one.

Robert Kiyosaki & Peter Schiff right -Hard times make strong menXLF financials, Stocks to GDP and stocks to gold, all tell the story.

Our debt based system is bottlenecked. More money is 'needed'.

Valuation is the light when the stock market is full of darknessthe market only goes 2 ways, up and down, and yet it can still be difficult to see through the noise.

I used to just look at charts, and trade off of the pictures. boy was I a fool.

turns out stocks are businesses. if you knew that, you should have told me sooner :D

valuation changed my life.

on dark days like today, the market is falling and its feels scary and red and bad and scary and omg.

but it has to be this way.

this is how you get the 10 baggers or the 100 baggers the grow over the next decades.

yeah the market can go down 50%.

guess what, the storm will pass.

and then business and life will go on.

and companies will grow a little bit every month and every quarter.

whats 20% compounding for 10 years? do you even math bro?

its hard.

learn.

you can do it.

kthanxbye

Grab stock future value in 2031 using crayons and binocularsStocks are businesses. most of them anyways. some are expensive hobbies until the money runs out.

Its a good exercise to value opportunities as you see them. useful to weigh it and make notes in your files.

Maybe not now, but later, your pitch with be thrown, and you might be ready to swing at it.

Don't trust stock charts aloneValuation change my life. I was blind and now I see. not kidding.

I love technical analysis. I love it more when combined with valuation.

Stocks are actual businesses. Charts only track transactions. its like receipts in the trash outside the store :D

Warren Buffett used to collect bottle caps as a kid. Then would sort them to find out what drinks were most popular. He sold Coca Colas from his grandfathers grocery store based on this info and also later in life became a Coke Stock investor.

so what?

Maybe not you, but definitely me, Ive made the mistake of JUST LOOKING AT CHARTS and forgetting whats behind the charts. Actual businesses, people, and world governments acting out their motivations, resulting in what we see in the charts.

There is so much more information, that when combined with charts, makes for better decisions.

Shout out to trading view. Trading view allows for make fundamental data easy to overlay onto charts. gamechanger!

Macro/fed, accounting fundamentals, charts/trends, social sentiment/behavior, options pricing, all of this and more is out there for investors to consider.

Any who.

The video is about the market multiple on earnings which results in prices. Thats what prices are. Prices are a derivative on business earnings. Earning x multiple = price.

When I was noob young monkey, I wish I knew all of these concepts. So here I am trying to share.

Hope you dig it.

Cheers!

TSLA: The ReversalAbout a month ago, everything had turned around for Tesla. The company was being mercilessly mocked as wave after wave of bad news came out & the selling pushed prices down further and further. However, it was not to last. Now, after that (apparently) temporary scare, we are all the way back near $200.

In 2021, I did not like Tesla very much. The reason was because the valuation was something like 300 P/E. Running some sort of standard cash flow analysis gave a value far lower than the stock price.

I was astonished to find that now, the value is closer to $150 a share. The valuation of the stock has improved dramatically as it has fallen. Of course, $200 is above $150, but it is much closer to being fairly valued than it once was. This means it may not be permanently doomed.

The thing is that a reversal this strong likely needs some sort of strong signal/pattern if it were to be pushed back down again - e.g. a false break above $200 to trap anyone who believes too much in Tesla. It is up about 90% from its lows and has created a substantial bullish formation as a result.

I am not sure it has enough momentum to go too far further at the moment. It has shown a lot of strength & may become more bullish due to the better valuation, so it could be worth it to buy any sort of decline that is coming up.

I would also caution against calling one side against the other at the moment. Tesla stock is highly volatile (obviously) and the market could either toss it out the window or enshrine it in the throne of the new paradigm. You should make sure not to be too emotional if you dare to buy (or short) this stock.

Chat GPT Ai stocks list for 2023Is chat gpt and Artificial Intelligence the next boom theme?

Why are so many people talking about it recently?

How long can this new trend create opportunity for , years, decades?

How do we value the opportunity and avoid paying too much?

Dont get ripped off and caught up in the hype, use math and valuation to price the reward and risk in a balanced logical way.

The legends of investing have given us they formulas through lifetimes of trial and error. We just need to apply them.

Benjamin Graham, Peter Lynch, Warren Buffett, Phil Fisher, these guys used simple math to make fantastic decisions.

Concepts like Price to Earnings vs growth, and balance sheet valuation concepts.

Stick to the valuation math principles and make better logic decisions in these uncertain markets.

Cheers!

Overlaying stock valuation levels vs picture trading #gtbifI used stare at charts and colored bars and tried to find shapes to figure out the next move. Guess what, I missed out on a lot of easy opportunities to hold and ran scared out of good stocks because I didnt understand growth valuation.

Stocks will do things that dont make sense on the charts. Stocks are businesses.

We really need to understand the companies behind the charts. Its just lazy and a missed opportunity not to do so.

In this this video, I create some valuation assumptions and overlay them on the charts for insights.

Bear case valuations and bull case valuations.

Hope you enjoy it. Cheers.

SPX 17-18 PE above median average, and over 25 PE w/inflation what recession? what inflation? what rising discount rates?

"Stonks always go up". "What me worry?"

Just because stocks have come down in nominal price, it doesn't mean all these things are priced in.

Buying low means buying below historical median PE and having healthy growth prospects.

Buying low could also mean paying median PE with following years having healthy growth.

What we probably have now is the expectation that inflation raises revenue for nominal growth but not 'real' growth.

As in inflation adjusted, the growth my be less exciting.