Energy (D): GasolineThere are three if/else statements with this trade.

If price fills the gap set on December 2nd and shows signs of buying, go long.

Else, stay flat and wait.

If price reaches purple region as indicated in chart, go short.

Else, stay flat.

If price reaches "Buy Here" level, buy there.

- Odds are we will see some action in this trade as long as price does not gap beyond forecasted prices. Gas and oil essentially have a 1-1 positive correlation, so follow this asset for some clues/ indication on energy trajectory.

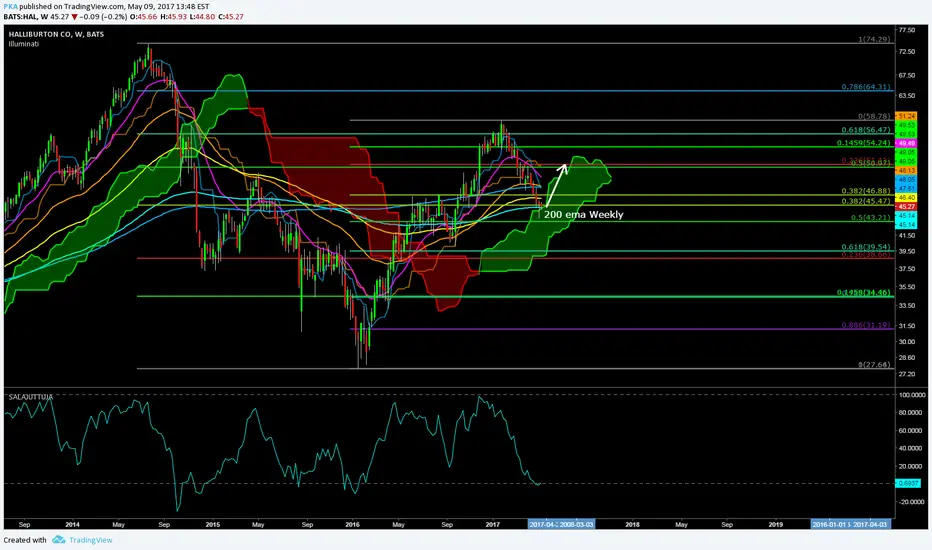

XLE

USOIL trade idea.....Going long on USOIL by using GUSH. USOIL just completed a 3 drive to a bottom pattern. We can expect a turn here. Panic selling this morning is tough to go long into but the rewards should be there. Set a stop just below $43.

THE WEEK AHEAD: XOP/OIH/XLE, COSTPremium Selling

For the umpteenth week in a row, there is little in the market for high quality premium selling plays. Screening for 52-week >70 implied volatility rank, you'll basically get one quality hit at the moment, and that is COST, which has dipped significantly on AMZN/WFM merger news. A few names are approaching that 70 mark, but they have earnings three to four weeks out; you might as well wait to put on volatility contraction plays around earnings announcements in those cases. I previously set out a nondirectional play in COST (see Post below) that I didn't enter, having been distracted by something or other; I may reconsider that play now that the market's had an opportunity to digest the AMZN news.

Other names, such as NBR (petro, part of whose operations are deep water),* RAD (pharmacy in merger and acquisition with WBA), and BBRY (a kind of WTF, why are they still around) are too small in dollar value to be worth playing unless you dive in and go straight-on covered call or near-to-the-money short put.

Directionals

I've been waiting for several weeks to put on a bullish XOP, OIH, and XLE play. Each time I look at them, it appears that oil has trundled lower on rising rig count, total stock build, lackluster inventory draw, or a combination thereof.

I've been primarily watching oil prices around the supposed average shale production break even at $40 to go long in one of these underlyings. We may be close enough for me to make a play, but I'll probably continue watching. Lower is better for either a net credit put diagonal or a Poor Man's Covered Call in these guys.

Low Volatility Plays

With VIX continuing on its sub-12 bender, there probably isn't a better time to go put-side low volatility strategy in broad index underlyings (SPY, IWM, QQQ, DIA) using either calendars, net credit put diagonals, or debit diagonals. These capitalize on volatility expansion and movement of the underlying toward the put side, ideally allowing you to exit the short put aspect of the setup at worthless and recapture any value left in the long at the expiry of the front-month short. Heck, the dam has to break at some point ... .

* -- I regard most companies that rely substantially on deep water operations as largely doomed here. Most deep water operations require high per barrel prices that we haven't seen for a substantial period of time and aren't going to see in the short- to medium-term.

USOIL ready to reverse upI went long on 2 light sweet crude oil futures last night at $44.30. Now $44.81. Good support in the low $44 area. This morning I will enter a position in ERX and a smaller position in GUSH in my 401k. See also chartwatchers idea on this.

Neutral trade on XLE (Iron Condor)With IVR at 26 sold the Iron condor 70/73/66/62.5 on XLE with 37 Days to expiration

The Trade:

Short 70 Call

Long 73 Call

Short 66 Put

Long 62.5 Put

Credit = $1.11

55% probability of profit

TRADE IDEA: XLE SEPT 15TH 57/JULY 21ST 67 PMCC** -- Poor Man's Covered Call.

One of the few sectors that hasn't benefited from the post- November election run-up is XLE, so I'm looking to get into a bullish play here where price of the underlying is comparatively low.

Here, I'm basically looking to emulate a full-on covered call using a deep in the money call in September to stand in for stock, 100 shares of which would be somewhat pricey here, comparatively speaking. A covered call with the same short call would cost 64.56 to put on; the Poor Man's shown here is far less than that. Additionally, if you're looking to acquire XLE shares at some point, the setup gives you the flexibility to reduce some cost basis up front before acquiring the shares, after which you can exercise the long call instead of being stuck with shares with a cost basis of 64.56/share here, as you would be with a covered call here.

Unfortunately, as a form of diagonal, there aren't many metrics to look at, but this is what we do know about the setup:

Max Loss/Buying Power Effect: 7.21

Delta: 61.59

Theta: .75

Generally, you work it like a covered call, rolling the short call out to reduce cost basis in the long aspect of the position. However, on break of the short call, your long call won't be subject to "call away" as it would be with stock; in that event, look to exit the trade profitably and redeploy or roll the short call up and out for a credit if you want to continue to reduce cost basis in the long through expiry.

Notes: The pricing of the setup will probably be different during the regular NY session. I'm working with off hours quotes here, and the bid/ask on the back month is particularly wide here, so overall pricing of the setup may be inaccurate.

THE WEEK AHEAD: PIVOT TO NON-HIGH VOLATILITY STRATEGIESWith this quarter's earnings season all but over and with VIX trundling along at sub-10 levels, there is a paucity of high implied volatility plays in the market for premium selling, so I'm looking at deploying something in either low volatility strategies (diagonals) or in directional plays that I've been eyeing.

Screening for underlyings with greater than 70% implied volatility rank over the past 52 weeks, greater than 50% background implied volatility, and relatively high options liquidity yields a few names -- P, HTZ, and NBR, but it'll be tough to squeeze good premium out of these because they're all <$10 underlyings. I would be willing to get into exchange-traded funds if only there was one with >70% implied volatility rank and >35% implied volatility; there currently isn't.

With the individual underlyings, a P 9 short straddle in the July 21st expiry yields 1.84 at the mid with BE's at 7.16 and 10.84 (put side, below expected move; call side, at expected move); a HTZ July 21st 10 short straddle yields 2.03 with BE's at 7.97 and 12.03 (both sides clear of the expected move); and the NBR July 21st 9 short straddle, 1.54, with BE's at the expected move on the put side and above it on the call (7.46/10.54).

Alternatively, NBR is a petro play,* so I can see taking a bullish assumption on the underlying and short putting it, even though it won't pay all that much (the July 21st 8 put brings in .40 with a BE of 7.60).

Directionally, I've got my eye on two sector exchange-traded funds: XLE and XRT. Out of all the sectors, energy and retail have been the most downtrodden, so this may be an opportunity to go long with comparatively "cheap" setups that have oodles of time to work out -- Poor Man's Covered Calls -- with long-dated back months several cycles out. I'll post setups on those separately; however, each time I look to pull the trigger on a bullish XLE setup, oil seems to trundle lower and XLE with it ... .

* -- NBR is deepwater; if they're not in trouble now with oil sub-$50/bbl., they will be in trouble in short order if prices hang around here for long. Generally, BE for deepwater oil exploration and production is well above this year's $55/bbl. high, so I'm hesitant to take a bullish assumption on deep water anything. Frankly, I'd rather put my buying power to work on something like XOP, where I'm not exposed to single name risk in this area, given the fact that there are so many troubled companies in this sector.

Bearish harmonic pattern near 2K tech bubble levelsXLK has been one of the main forces behind the U.S stocks market rally since Trump was elected.

XLK is up almost 20% since the U.S elections and it is now approaching the 2K tech bubble levels.

Bearish Bat pattern will be complete just below 60$

Interesting price zone to watch in near future.

Are we near the end?

Read more in this week's newsletter

#WeeklyMarketsAnlaysis on Twitter

Long ESVStop below the large uptrend channel dating back to the early 90's. Target the 250/300 ema on the monthly.

Oil reached target zone and now testing strong daily resistance 49-50$ was the weekly resistance zone I mentioned in this week's newsletter (subscribe on my website)

The focus was on the MA lines (200 and 50) that, for now, hold Oil from advancing higher.

Stop loss for bearish swing trades should be at least above 51$

First target zone - 48$

XLE/ERX - Trend line attackI'm not satisfied with the performance of our XLE and ERX position. Sooner or later the rally will start here also... The more time we spend below the purple trend line the bigger breakout will come. On the 4th of April we broke above the trend line but lost it in a week. On the 4th of May we printed a new low in this decline on very high volume. Most probably that day was the bottom. If stocks are printing a correction during the next 2 weeks - unlikely - we might test back 65.82$...

I think when we break above the purple trendline again that will be a valid breakout and the great rally in oil stocks will start finally.

I will try to trade some individual stocks also. There will be stocks which will print 4-500% rally in the next 3-4 months.

I think ERX also has a good chance of printing a 200-300% rally.

All the indicators (MACD, TSI, SlowStoch) are showing a divergence. I'M preparing for 2 scenarios:

1. We are churning around the trendline for a few more days and breaking out

2. we test back the lows at 65.82$ and a monster rally is coming out of the double bottom.

Nasdaq, S&P, Dow Jones at all time highs. I see zero chance that oil stocks will miss this rally.

Long XLE by Selling Jade Lizard June 65put, 68.5/69.5caXLE started to bounce back from bottom. I expect it to be going up and then start side way. So I would setup a Jade Lizard position.

Position:

Sell 1 June 65 Put

Sell 1 June 68.5/69.5 Call Spread

Total Premium: 1.04$

Break Even: $63.96,

Profit area: $63.96 $69.54. No upside risk.

Pop %: 84%

Low Energy In Energy SectorThe Energy Sector SPDR Fund XLE has been in a defined bearish trend for all of 2017. Due to this bearish movement, the 100 day moving average (DMA) is about to cross below the 150 DMA. This actual event has occurred 15 times in the history of the fund and has a minimal drop of 0.263%. It has a median drop of 2.067% and maximum drop of 38.054% over the following 16 trading days. Although I typically write on events that have occurred, this event is likely and greater benefit could be gained by making moves earlier.

When we take a look at other technical indicators, the relative strength index (RSI) is at 40.2699. RSI tends to determine trends, overbought and oversold levels as well as likelihood of price swings. I personally use anything above 75 as overbought and anything under 25 as oversold. The current reading declares the fund has been moving lower. The RSI has been trending lower since May 2016. Even though the RSI typically cycles between overbought and oversold levels, that has not necessarily been the case with this fund. Overall the RSI is failing to make newer highs which is another significant signal of downward movement. Only once over the past year has the RSI broke above this trend before immediately following suit and heading down. This overall downtrend should continue as long as the RSI stays below this trendline.

The true strength index (TSI) is currently -19.3683. The TSI determines overbought/oversold levels and/or current trend. I solely use this as an indicator of trend as overbought and oversold levels vary. The TSI is double smoothed in its calculation and is a great indicator of upward and downward movement. The current reading declares the fund is down.

The positive vortex indicator (VI) is at 0.7572 and the negative is at 1.0678. When the positive level is higher than 1 and higher than the negative indicator, the overall price action is moving upward. When the negative level is higher than 1 and higher than the positive indicator, the overall price action is moving downward. The current reading declares the fund slightly moving up recently, but should begin its downtrend again.

The stochastic oscillator K value is 21.2870 and D value is 19.7285. This is a cyclical oscillator that is highly accurate and can be used to identify overbought/oversold levels as well as pending reversals and short-term activity. I personally use anything above 80 as overbought and below 20 as oversold. When the K value is higher than the D value, the stock is trending up. When the D value is higher that the K value the stock is trending down. The current reading declares the fund has been flirting with oversold territory for at least two weeks. Most likely one of two things will occur. The fund will continue to slowly move down with up days causing the stochastic to stabilize and rise even though the fund continues its downward bias. The second possibility would have the fund rise up and out of the downtrend either temporarily or permanently.

Considering the moving average crossover, RSI, TSI, VI and stochastic levels, the overall direction appears to be pointing down. Based on historical movement compared to current levels and the current position, the stock could drop at least 3% over the next 26 trading days.

THE WEEK AHEAD: EWY, FEZ, FXE, AND OIH/XOP/XLEWith VIX in another ebb and a paucity of high quality premium selling earnings plays in the making for next week with both high implied volatility rank and high implied volatility, I'm looking at exchange traded funds instead for potential plays.

For instance, EWY, the South Korea exchange traded fund, makes sense in the current geopolitical environment, and its implied volatility rank and implied volatility reflect this, coming in at 55/22. It doesn't meet my usually standards of >70 and >35, but sometimes the market doesn't allow you to be picky. The June 16th 56/59/65/68 iron condor brings in .81 at the mid (not quite up to my usual 1/3rd the width of the wings snuff); alternatively, the June 16th 57/62/62/67 iron fly brings in 2.76. A drawback is that this instrument only has monthlies, a situation I'm not fond of ... .

With French election finals on the horizon on May 7th, another play that makes sense against the backdrop of "news," is FEZ (Euro Stoxx 50) (49/21). However, I previously attempted to get a fill of an iron fly before the primaries, and it was quite pesky, particularly on the call side. Currently, I'm unable to get a mid price quote for the June 9th 34.5/37.5/37.5/40.5 iron fly or a similar setup in the June 16th expiry due to the fact that the long calls where I want to set up are no bid.

With FXE (the Euro proxy), which I tend to play as I would play EURUSD, I would go directionally short. The background implied volatility is so low that it just doesn't make sense as a straightforward premium selling play since the contraction that's usually a feature of these plays is likely to be minor; moreover, I have a directional assumption in a tightening Fed environment versus a loose to easing ECB environment (bearish).

There are a couple of ways to play it: (a) ATM short call verts where the break even is around 106 (e.g., the June 16th 105/108 short call vert; 1.20 cr; BPE 1.80; BE at 106.20), legging in small in the event it rips higher on a Macron win (currently, the likely outcome); (b) a call diagonal that gives you some flexibility on the short call side of things (e.g., a June 16th 107 short call; Sept 15th 110 long call; .07 cr; 2.93 BPE) without exposing you to downside risk in the event that the Euro caves in at some point on dollar strength or Euro weakness.

Lastly, I've got eyeballs on oil. It's dipped somewhat dramatically off highs, so I'm looking at various bullish plays in OIH, XOP, and/or XLE, all of which track oil prices somewhat religiously. Currently, I'm still working an XOP put diagonal, but am amenable to getting into another XOP play. (Put diagonal: XOP June 16th 33 short put; Dec 15th 27 long put; .10 credit at the mid; 5.90/contract BPE; PMCC: XOP June 16th 37 short call/Dec 15th 24 long call; 10.82 db).

Neutral trade on XLE (Straddle)Looking for a neutral play on XLE (I think we are starting to have 2 way action). IVR is not that high at 26, so doing less contracts (I don't have any other position right now on XLE).

I sold the 69 Straddle for $2.78. Our break evens are just above the expected move, and this is close to a 54% probability trade.