Rate Cut Incoming. Buckle Up"What the Yield Curve and Fed Moves Mean for Your Next Trade."

Historically, when the Federal Reserve lowers the federal funds rate while the yield spread is negative (also known as an inverted yield curve), it has often been an indicator of an impending market correction or recession.

Let’s break this down:

Historically, the bond market is a key indicator. Typically, long-term bonds offer higher yields than short-term bonds; This a healthy sign. When that flips and short-term yields surpass long-term ones, we get what’s called an inverted yield curve. This inversion signals that investors are getting nervous about the near-term economy. When the Fed then steps in to lower rates, they’re trying to stimulate growth, but it often comes too late.

Looking back at past events:

The dot-com crash of 2000: The yield curve inverted, the Fed cut rates, and a 35% market correction followed.

The 2008 financial crisis: Again, the yield curve inverted, rates were cut, and the market saw a major downturn exceeding 50%.

Going back even further, the same pattern held in the 1970s and 1980s.

The big questions are:

Why does this combination signal trouble?

Will this pattern repeat itself again?

While history tends to repeat itself, the data shows that when the Fed cuts rates with a negative yield spread, market corrections often follow. The inverted curve suggests tighter credit conditions, reduced lending, and lack of confidence, all piling on top of one another creating a recipe for disaster.

Stepping back even further, we see that investor sentiment and the bond market tend to lead the way. Credit tightens, and companies cut back on spending. Another a perfect recipe for an economic slowdown and market drop.

It's a familiar cycle. So lets buckle up.

Yeildcurve

Macro Monday 58 - Recession Warning Charts Worth Watching Macro Monday 58

Recession Charts Worth Watching

If you follow me on Trading view, you can revisit these charts at any time and press play to get the up to date data and see if we have hit any recessionary trigger levels. They are very handy to have at a glance.

CHART 1

10 - 2 year treasury yield spread vs U.S. Unemployment Rate

Subject chart above

Summary

▫️ The chart demonstrates how the inversion of the Yield Curve (a fall below 0 for the blue area) coincides with U.S. Unemployment Rate bottoming (green area) prior to recession onset (red areas).

▫️ The yellow box on the chart gives us timelines on how many months passed, historically, before a confirmed economic recession after the yield curves first definitive turn back up towards the 0% level (also see circled numbers showing connecting bottoming unemployment rate).

▫️ Using this approach, you can see that the average time frame prior to recession onset is 13 months (April 2024) and the max timeframe is 22 months (Jan 2025).

▫️ This is only a consideration based on historical data and does not guarantee a recession or a recession timeline however it significantly raises the probability of a recession, and the longer into the timeframe we are the higher that recession probability.

▫️ We typically we have a recession (red zones) either during or immediately after the yield curve moves back above the zero level. At present we are at -0.08 and fast approaching the zero level which is one of the most concerning data points of this week.

▫️ The unemployment rate moved from a low of 3.4 in April 2023 to 4.3 in July 2024. This is a significant increase and is typical prior to recession onset.

Conclusion

▫️ If both the 10 - 2 year treasury yield spread and the U.S. Unemployment Rate continue in their upwards trajectory in coming weeks and months, this is a significant risk off signal and recession imminent warning.

▫️ The Sahm Rule triggered this week which has been one of the most accurate indicators of a recession starting. It is triggered when the three-month moving average of the U.S Unemployment Rate above rises by 0.50 percentage points or more, relative to its low over the previous 12 months. The Sahm rule triggering adds to recession concerns, however the designer of the rule has stated that I may not be accurate factoring in recent events like COVID-19 which has thrown unemployment and economic data to extremes.

What is the 10-2 year Treasury yield spread?

The 10-2 year Treasury yield spread represents the difference between the yield on 10-year U.S. Treasury bonds and 2-year U.S. Treasury bonds. It’s calculated by subtracting the 2-year yield from the 10-year yield. When this spread turns negative (inverts), it’s significant because it often precedes economic downturns. An inversion suggests that investors expect lower future interest rates, which can signal concerns about economic growth and potential recession. In essence, it’s a barometer of market sentiment and interest rate expectations

What is the U.S. Unemployment Rate

The unemployment rate is calculated by dividing the number of unemployed people by the total labor force in the U.S (which includes both employed and unemployed individuals).

CHART 2

Interest Rate Historic Timelines and impact on S&P500

Summary

▫️ This chart aims to illustrate the relationship between the Federal Reserve’s Interest rate hike policy and the S&P500’s price movements.

▫️ This is obviously pertinent factoring in the expectations of a rate cut in Sept 2024. This chart which I shared in Sept 2023 may have accurately predicted this likely Sept 2023 interest rate cut but is this positive for the market?

▫️ Interest Rate increases have resulted in positive S&P500 price action

▫️ Interest rate pauses are the first cautionary signal of potential negative S&P500 price action however 2 out of 3 pauses have resulted in positive price action. The higher the rate the higher the chance of a market decline during the pause period.

▫️ Interest rate pauses have ranged from 6 to 16 months (avg. of 11 months).

▫️ Interest rate reductions have been the major, often advanced warning signal for significant and continued market decline (red circles on chart)

▫️ Interest rates can decrease for 2 to 6 months before the market eventually capitulates.

▫️ In 2020 rates decreased for 6 months as the market continued its ascent and in 2007 rates decreased for 2 months as the market continued its ascent. This tells us that rates can go down as prices go up but that it rarely lasts with any gains completely wiped out within months.

Conclusion:

▫️ Rate cuts should signal significant concern as most are followed immediately by recession or followed by a recession within 2 to 6 months of the initial cut. This is high risk territory.

▫️ During the week I seen the 2 year treasury bill which matches closely the Federal Reserve interest rate cycle. The spread developing between the two suggests rate cuts are imminent. Remember point one above. The chart below:

CHART 3

Relationship between 2 Year Bonds and Interest Rate

▫️ Very briefly, you can see the red areas where gaps formed when the Federal Reserve interest rate was lagging behind the 2 year treasury bonds declines.

▫️ Currently there is a large gap of 1.74% between the two data sets. The last time we had gaps like this were prior to the 2000 and 2007 recessions. Even prior to COVID-19 you can see the Federal reserve was playing catch up.

What to watch for in coming weeks and months?

▫️ If both the 10 - 2 year treasury yield spread and the U.S. Unemployment Rate continue in their upwards trajectory in coming weeks and months, this is a significant risk off signal and recession imminent warning.

▫️ Since 1999 the Federal reserve interest pauses have averaged at 11 months. July 2024 is the 11th month. This suggests rate cuts are imminent.

▫️ The 2 year bond yield which provides a lead on interest rate direction is suggesting that rates are set to decline in the immediate future and that the Fed might lagging in their rate cuts. Furthermore, rate cuts are anticipated in Sept 2024 by market participant's.

▫️ Finally, rate cuts should signal significant concern as most are followed immediately by recession or followed by a recession within 2 to 6 months of the initial cut. Yet the market appears to be calling out for this. This is high risk territory. Combine this with a treasury yield curve rising above the 0 level and an increasing U.S. unemployment rate and things look increasingly concerning.

We can keep any eye on these charts for a lead on what might happen next. I will be reviewing some other charts over coming days around jobless claims and ISM figures to see how positive and negative we are looking.

PUKA

RECESSION PROABILITY SIGNIFICANTLY INCREASES JAN - JUN 202410Y/2Y Yield Spread & Unemployment Rate

Originally shared back in July 2023 (see below charts)

Its interesting to see that the yield curve is rising fast (up towards the 0 level)

We are reaching into dangerous recessionary territory. No guarantees, just a significantly increased probability.

Continuous jobless claims are reaching pre-recession warning levels in both time and volume. Meaning more and more people are becoming unemployed and remaining unemployed for longer. More info in links below.

The average interest rate pause timeframe is closing in fast at June 2024 also(Contained in Charts below also).

Its time to pay very close attention. The initial 6 months of this year

Stay safe out there

PUKA

Update on the Yield Curve Inversion Battleplan Background

My first idea where I lay out a yield curve battle plan was published 13 months ago. It was by no means perfect but I found it quite useful. I used it to buy the dip the market was experiencing and then when I was not seeing the follow through to a new all-time high I went back into safer assets (except for my crypto play money). The last idea looked at the spread between the 10 and 2year US Government Bond and this one will be looking at the 30 and the two year. The spread on 30 versus 2 years isa lot more stable than the 10 and 30 and right now I find it is the more usefulmeasure.

Main Chart

The main assumption is that the process of the yield curve inverting is has extraordinarily complex ramification for the global financial system…. That are simply ultimately bearish. The complexity initially drives prices up and then when the curve reasserts prices are driven down. You could get lost in the weeds and look at the repo market, or how DXY pumping may affect trade balances and rotations int markets and all that. Which is fine.

But I am looking for something simpler. The most important thing to recognize is that the classic blowoff top and bull trap formation performed with a lot of fidelity to a ABC correction. A zoom in and view of the weekly chart shows a lot of strong buying right at the 2.618 level

The 1989 and 2006 inversion did not have clear topping structures like we see from the dotcom pop and the current double top (which putting in its lower high) Compared to the dotcom pop those were baby crashes in time and intensity. A zoom in on the current price action of NDX and the bond spread shows that we have had bearish reversal candles on NDX and growing green candles on the bond spread. It almost looks like the spread pair is in a W pattern and the ratio should be getting close to 2%-ish again.

Double Tops

Double tops have a take-off, a first high, a valley that links the first high to a second high, and then a sell off. Often the sell off returns price to the take off point. The tops do not need to be symmetrical. They can be “Eve and Adam” or “Eve and Eve” tops. Right now it isn’t clear that type of double top we are in. It could be a Eve and Adam or a Eve and Eve. Even more formally, until price returns to the neckline we don’t even have a confirmed double top and we are just in early pattern recognition. The whole process of a double top can take a long time.

Here is a bitcoin double top from last bear market on the 12-hour time frame. It took 60 days to return from the take off point. If I am right about being in the middle or beginning of the second top, then this pattern is only halfway or so to getting to target and over-performance is another matter.

Conclusion

If this idea is accurate once we see the 30- and 2-year US government Bond spread turn positive again we can expect a bear market/recession. We already had two quarters of GDP declining which for the longest time was a technical definition of a recession until “for some reason” people decided that wasn’t the definition anymore. Now also have numbers coming out of government agencies that people don’t trust because they don’t trust the Administratum and we are looking at chart formations and the yield curve for a real view of what is happening in the economy.

And it is pretty bearish.

Recession Timeframe Horizon Macro Monday (2)

Potential Recession Time Horizon

Below you will find a breakdown of how many months pass before a confirmed Economic Recession (shaded grey areas) after the yield curves first definitive turn back up towards the 0% level:

1) 13 Months (Dec 1978 – Jan 1980)

2) 9 Months (Nov 1980 – July 1981)

3) 16 Months (Mar 1989 – Jul 1990)

4) 12 Months (Mar 2000 – Mar 2001)

5) 22 Months (Feb 2006 – Dec 2007)

6) 6 Months (Aug 2019 – Mar 2020)

7) 4 Months so far (Mar 2023 - ????)

Average Time frame: 13 months (reasonable time horizon would be 6 – 18 months).

I consider the first definitive turn up towards the 0% level as no. 7 on the chart (March 2023). Since this date we have rolled over below the -1% level (see additional chart in comments). March 2023 appears similar to the bounce in Dec 1978 (No. 1 in the chart), it also rolled over to the lower sub -1% level. If we assumed a similar 13 month timeframe to recession commencement as in Dec 1978 of 13 months, which also aligns with our 13 month average above, we would be looking at April 2024 for a recession to commence. Interestingly 1978 - 1980 was a similar peak inflationary period known as the Great Inflation, a defining macroeconomic period of high inflation.

You might be wondering, has a recession ever occurred in the month of April before? I personally thought this was a strange month but it has occurred in the past.

In April 1960 a recession commenced and lasted 10 months to February 1961. The 1960 recession was mainly a result of an over-tight monetary policy whereby the Federal Reserve raised interest rates from 1.75% in mid-1958 to 4% by the end of 1959 and maintained them at that level until June 1960. The Federal Reserves motive for raising interest rates and maintaining them was fear of high inflation (as in early 1951 inflation soared to +9.5%). Is it just me or is this all starting to sound a little too familiar?

If we wanted to cater for all time scenarios in the chart and noted above (no. 1 - 6) we could argue that the start of a recession is possible at the earliest within 6 months (Sept 2023) and at the latest 22 months (Jan 2025). Also, the month of April 2024 has some eerie similarities to two prior recessions, the 1978 and 1960 Recessions.

Lucky 13

Since World War 2 bear markets have on average taken about 13 months to reach their bottom and a further 26 months to recover their losses. Our average time before a recession would start is 13 months. It’s worth remembering that it could take an additional 13 months before a bottom is established and then 2 years or 26 months (2 x 13) of price action below the pre-recession price highs. Over 3 years is a long time to wait to recover losses. It would be pertinent to start deleveraging or increasing your hedge from the 6 month mark (Sept 2023 in this case) as subsequently the likelihood of a 3 year period below the Sept 2023 price levels increase as each month passes. For reference the S&P 500 index has fallen an average of 33% during bear markets over the avg. timeframe of 13 months to the bottom.

I actually find it very hard to accept that a recession is possible in the near term (within 6 - 12 months) and I would in fact argue against it, however I cannot explain away the data in the chart which speaks for itself and warrants at least some consideration & caution. Nothing is a guarantee and maybe this time it will be different, especially factoring in the amount of unprecedented liquidity added to the market in recent years, sticky inflation and financial supports provided to systemically important banks.

All the chart really indicates is a probable window for a recession to start some time between Sept 2023 – Jan 2025 and no guarantees.

The rule of 13 is worth remembering, simply from a timing perspective (before and during a recession) as it may help your timing. Based on two similar periods in history, the 1978 and 1960 recessions suggest the month of April 2024 may be a key date. Again, no guarantees.

It is also worth noting that for the last six recessions, on average, the announcement of when a recession started was up to 8 months after the fact…meaning we will have no direct indication when a recession starts, however the un-inversion of the yield curve (back above the 0% level) and a rise in unemployment will be the early tells, so these are worth paying attention too. We will keep you posted on any sudden changes in these metrics.

I hope the chart is helpful, provides one perspective of which there are many, and can help time and frame the situation we currently find ourselves in. NO GAURANTEES, just probable timeframes that may be worth paying attention too.

PUKA

List of Recessions:

1. COVID-19 Recession (February - April 2020)

2. The Great Recession of 2008 (December 2007 - June 2009)

3. The September 11 Recession (March - November 2001)

4. The Gulf War Recession (July 1990 - March 1991)

5. The Iran/Energy Crisis Recession (July 1981 - November 1982)

6. The Energy Crisis Recession (January - July 1980)

7. The Nixon Recession (December 1969 - November 1970)

8. The “Rolling Adjustment” Recession (April 1960 - February 1961)

9. The Eisenhower Recession (August 1957 - April 1958)

10. The Post-Korean War Recession (July 1953 - May 1954)

Is the Worst OVER? This is the differential of 10yr vs 1yr US bond which represents long term against short term yield on sovereign debt, and those you don't know, short term bonds are used by central banks to control interest rates(amazing uh? the FED does not actually print money) therefore they do use bonds as a tool to control interest rates which then controls the S&D of capital.

As you can see, we are back at a differential which is extremely low, back to energy crisis levels. However, we seem to be already at very low levels, does that mean THE WORST HAS COME? What is going to happen to the stock market?

A very quick and personal thought to sum everything up as I do not consider myself an expert macroeconomist: the market is efficient, meaning that the current price on every single security is traded at all the current public information that is available and if something keeps going up, it means that expectation are in favor of it moving higher.

Hope that explains what I wanted to say,

Feel free to ask question, be safe!

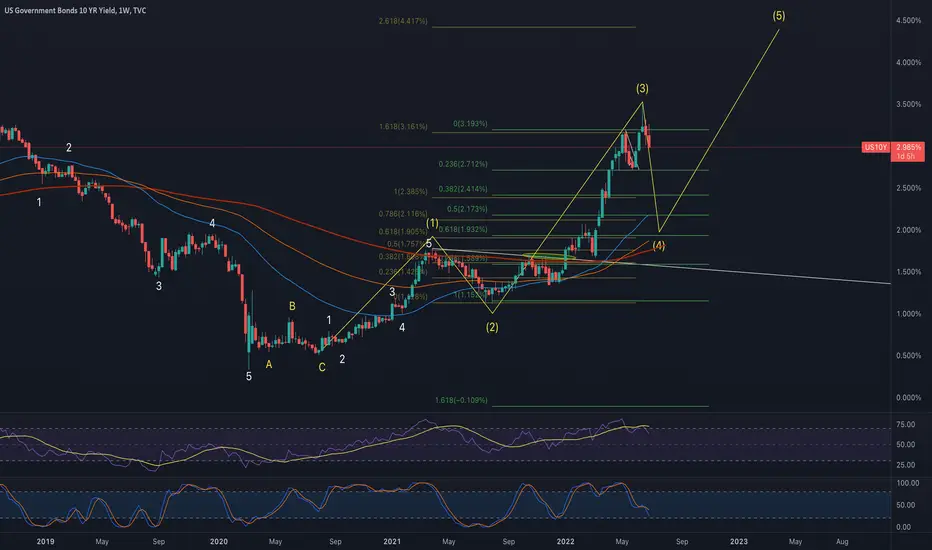

10 yr My W4 on weekly HTF chart is looking likely. If the Fed & ECB are in the debt market trying to stabilize the system via repo swaps then this dump is going to be a normalization process and the markets will chop around in some f**ked up range until W4 is complete around 1.9%-2.2% during this normalization period bullish momo will fizzle out and bears will short all pumps and win , but the greedy bears will get squeezed as all big dumps in markets will get bought up quick and change the direction b4 most traders know what even happened. I suggest only buying your core positions until w4 is finally done projected to finish July-Sept 2022. This would be a good move for the patient investors here to hold and add because once the W4 finishes and markets stabilize (if the fed pivots like I am saying above) W5 will line up on the 10 yr with W5 for stocks & crypto. Conversely If W4 becomes a fear trade (inflation narrative grows momo, war in Ukraine gets worst possibly nuclear war, china invades Taiwan or anything else unforeseeable) then W4 will decimate markets and 3200 SP500 is possible and $12K BTC.

10 year We must see how the markets react to this dump to the 10 yr, my gut thinks this could be a fear trade which causes money to leave risk and head into USA gov bonds. I would assume that at some point around 2.4% (618% golden ratio) a bottom will be found and the inflation narrative will be silenced for at least some time while Oil has a decent pull back to $60. Then the W5 will kick in and maybe intitially seem bullish while rates climb in a structured manor till around 3% or 3.2%. After rates hit that level inflation may start to appear again in the MSM. Once w5 really kicks in and heads towards 3.5%-4% plus this will likely be the debt market melt down. So watching DXY, stocks and crypto how this all plays out

TLT is about to resume the down-trendDown-trend on TLT is about to resume with a target around 122, so I am excepting long side of a yield curve to go event further up and eventually exceed 3%. I like Lacy Hunt's arguments for deflation/not inflation in the long term. But as he also mentioned, it is a norm at the moment to expect a short term inflation pressure.

I believe a 5 wave structure is unwinding since 5th of April, 2020 on TLT chart, with 4th wave potentially just completed. Wave 2 had triangle structure, so wave 4 is expected to form a zig-zag , exactly is it actually happened. So it is ready for the next move down towards 122.

Watch TLT/JNK chart which I found very interesting, it gives an idea about a turning point when market is going to turn from risk to save assets. Most likely it will be in sync with completion of DXY correction (started in 2017), so both $ and bond will go up after then.

10 yrIH&S pattern broke up the 200 weekly ema. Bond yields will most likely be testing around 1.66% and as long as the markets stay up I think we will enter a blow off top.

I can see 1.66% on the 10 yr or maybe even higher with sp500 making a monster run blow off top to 4200 plus B4 any larger correction.

$BAC could Mind the Gap! or Head for $30 Watch for YCC!How would the BANKS react if the Fed

institutes yield curve control (YCC)??

Do we see $30 or go back and fill the GAP!