TLT bull puternweak data for 2 months non farm payrols says us that fed probably will lower the interest rate so it will get us upside in us treasuries

Government bonds

DE30 LONG TREND CHANCESWe set to allow rgis to hit the support level before any entry due to chances with high volume

US 10Y TREASURY: a bit of correction Two weeks ago U.S. Treasury yields were under a strong impact of weaker-than-expected non-farm payrolls data. The market reacted with a strong move toward the level of 4,2%. However, during the previous week some corrections in the level of yields occurred, as expected. The market digested the data and moved yields toward the 4,3%. The 10Y yields are ending the week at 4,28%.

The week ahead is also going to be an interesting one from the perspective of data. The inflation rate for July and the producers price index for July are scheduled for a release. The market will wage this data in a sense of its potential impact on the Fed's decision to cut or postpone rate cuts in September. Inflation data are especially relevant for market participants as it will provide an overview of the spillover effect of implemented tariffs on both inflation and the U.S. real economy.

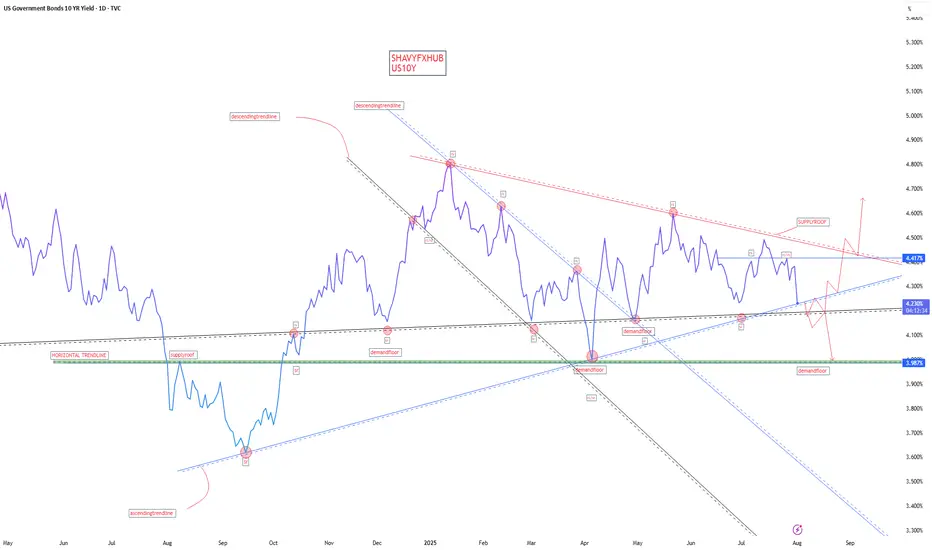

UST 10Y Technical Outlook for the week Aug 11-15 (updated daily)UST 10Y Technical Outlook for the week Aug 11-15 (updated daily)

Overnight

The yield on the US 10-year Treasury note climbed to 4.27% on Friday, marking a fourth consecutive session of increases from a three-month low earlier in the week. This uptick follows market reactions to proposed tariffs on gold bars, President Trump’s nomination of Stephen Miran to the Federal Reserve’s Board of Governors, and concerns over potential politicization of the Fed. Weak economic indicators, including a lackluster jobs report, a subdued ISM Services PMI, and rising jobless claims, have heightened expectations for an interest rate cut next month. Additionally, recent Treasury auctions for 10-year and 30-year notes suggest declining demand for US debt. Investors are now focused on the upcoming CPI report and other economic data for further clarity on the US economy’s trajectory.

Economic Release for the week www.myfxbook.com

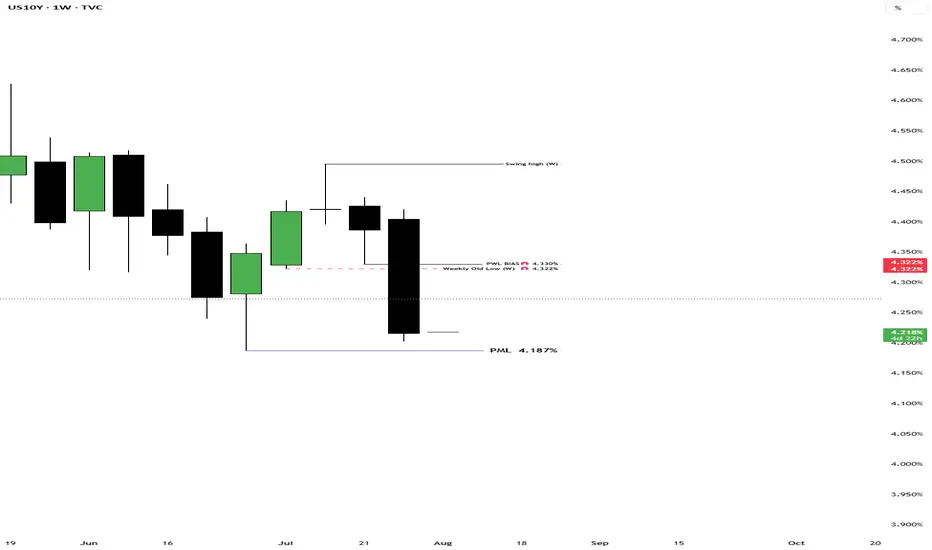

Weekly Bias

Based on last week's market activity, the market tested the prior week's low and the previous month's low before rallying strongly to close within the prior week's range. For the upcoming week, I anticipate the market may target last week's high of 4.42%. Key economic data, including CPI and inflation figures, are scheduled for release on Tuesday. These figures are likely to introduce significant volatility, so close monitoring is advised.

**Disclaimer:**

The technical analyses provided herein are based solely on my personal analysis and are intended for my own study and reference. They do not constitute a recommendation or solicitation to buy or sell any financial instruments. Any decision made by individuals based on this analysis is their own responsibility, and I assume no liability for any losses or damages incurred as a result of using this information. It is advisable to conduct thorough research and consult with a qualified financial advisor before making any investment decisions.

US10Y & T-Bond Future - Weekly AnalysisBias For The Week:

US10Y - Bullish Up to 4.341%

T-Bond - Bearish Down To 113.25

LMACD of the US02Y has just dipped bellow 0!In the past while rates have been elevated for a period of time things have gone bad for risk markets once the LMACD dipped bellow 0. Could be this time different?

US 10-year yield threatening to breach key supportAfter Friday’s US jobs report, US Treasury yields fell across the curve. This caused the benchmark 10-year yield to retest the area below the 6M resistance level at 4.417% and settle at the 3M support from 4.211%. The mentioned support level has acted as a familiar floor since May this year. Therefore, a rejection of this base could refocus attention on 4.417% as an upside target, while a breakout might open the possibility for price to decline towards a 1Y support at 4.038%.

Written by the FP Markets Research Team

US 10Y TREASURY: NFP sank yields Although the previous week was full of important US macroeconomic data, including the FOMC meeting, still the weaker than expected NFP data impacted significantly the US Treasuries market. The 10Y US benchmark yields were holding around the 4,3% level during the week, however, weak NFP data pushed yields strongly to the downside, closing the week at the level of 4,22%. The support line at 4,2% was also tested at Friday's trading session. As per current sentiment, investors are now anticipating two rate cuts till the end of this year, one in September and another one in December by 25bps. Odds for September rate cut stand at 85% since Friday.

The week ahead will be a reflective one on financial markets, as there are no important data to be released. In this sense, markets will digest both this week's posted economic data as well as macro projections from the latest FOMC meeting. Some upward corrections are possible, at least till the level of 4,3%.

US10Y Technical Analysis & Mortgage Rate Outlook Weekly. Aug. 4US10Y Technical Analysis & Mortgage Rate Outlook

(Based on Weekly Chart & Current Economic Context)

Technical View (Weekly Timeframe)

The US10Y yield is sitting around 4.21%, in the middle of a wide consolidation range that’s been developing since late 2023. This range is bounded by strong resistance near 4.62%–4.80% (purple supply zone) and support near 3.86%–4.00%.

* Trend Structure:

* We are still in a macro uptrend from the 2020 lows, but recent action has been sideways-to-lower since late 2023.

* Yields remain above the long-term uptrend line but have failed to sustain breakouts above 4.80% multiple times — showing sellers are defending that zone heavily.

* Support Levels:

* 4.00%–4.10% → First key demand zone.

* 3.86% → Major floor; losing this could trigger a larger downside move toward 3.50%–3.60%.

* Resistance Levels:

* 4.50% → First overhead supply.

* 4.62%–4.80% → Strong long-term resistance. A breakout here could signal a push toward 5.0%+ yields.

Economic & Labor Market Context

The latest labor market report showed slowing job growth but still relatively low unemployment. Wage pressures have eased slightly, hinting that labor-driven inflation is cooling. However:

* Inflation remains above the Fed’s 2% target, making the central bank reluctant to cut rates aggressively.

* The bond market is pricing in fewer rate cuts in 2025 than previously expected, keeping yields elevated.

* The Fed’s tone remains “higher for longer” until inflation shows more decisive softening.

Mortgage Rate Implications

Mortgage rates tend to follow the 10-year Treasury yield plus a spread of roughly 1.8%–2.0%.

* If 10Y Stays Near 4.20% → 30-year fixed mortgage rates likely hover around 6.0%–6.2%.

* If 10Y Tests 4.80% Resistance → Mortgage rates could climb toward 6.8%–7.0%.

* If 10Y Breaks Below 4.0% → Mortgage rates could fall into the 5.8%–5.9% range.

Given the Fed’s cautious stance and sticky inflation, a sustained drop below 6% mortgage rates in the near term looks unlikely unless we get a meaningful deterioration in economic growth.

My Thoughts

* Short-term (1–2 months): Likely range-bound between 4.0% and 4.62% until a major macro catalyst (CPI, Fed policy shift) forces a breakout.

* Medium-term (3–6 months): If economic data continues to soften, yields could drift toward 4.0% and help mortgage rates ease modestly. If data surprises to the upside, a retest of 4.80% is likely.

* Mortgage Rate Forecast: Expect 30-year fixed rates to stay between 6.0% and 6.6% for the rest of summer, with downside limited unless the Fed signals an earlier pivot.

UST 10Y Technical Outlook for the week Aug 4-8 updated dailyUS Treasury 10Y Technical Outlook for the week Aug 4-8 (updated daily)

Overnight

The yield on the US 10-year Treasury note dropped sharply by nearly 20 basis points to 4.25% on Friday, hitting a three-month low, driven by revised labor market data indicating significant weakness. Nonfarm payrolls for July increased by only 73,000, far below the expected 110,000, with prior data revised downward by 258,000 jobs for the previous two months. These figures highlighted the adverse effects of tariff threats and economic policy uncertainty, challenging earlier perceptions of a strong US labor market. As a result, market expectations shifted, reducing the likelihood of a Federal Reserve rate cut in September and limiting anticipated cuts to two for the year. Additionally, President Trump’s imposition of 39% tariffs on Switzerland, effective next week, and new tariffs on the EU, Japan, and Korea, effective immediately, further pressured yields. The Treasury’s announcement of increased buybacks for notes, bonds, and TIPS also contributed to the decline in yields.

Economic Release Aug 4 to 8 www.myfxbook.com

Weekly Outlook

Last week’s market has been very volatile. Yield has closed below prior week’s low and may continue to reach the previous month’s low of 4.187% . There are lots of noise in Trump’s administration from firing of the National statistician to fed governor Adriana Kuger resignation and Nuclear talks. These might affect the market in the coming days.

**Disclaimer:**

The technical analyses provided herein are based solely on my personal analysis and are intended for my own study and reference. They do not constitute a recommendation or solicitation to buy or sell any financial instruments. Any decision made by individuals based on this analysis is their own responsibility, and I assume no liability for any losses or damages incurred as a result of using this information. It is advisable to conduct thorough research and consult with a qualified financial advisor before making any investment decisions.

US02Y LongUS02Y Long on the regression break.

I am considering the other bond markets as this has already moved a long way.

US10YTHE non farm employment data report has given us a reason to sell of US10Y.the lower than forecast of 73K was a big shock ,the slower job growth reflects caution amongst employers amid uncertainties related to tariff, trade and immigration policies. Wages grew with average hourly earnings increasing about 0.3% month over month. overall, the labor market shows signs of cooling but remains fundamentally resilient with payroll gains still keeping pace with working age population growth.

the US10Y COULD SLIP DOWN MORE ON ECENONOMIC OUTLOOK,IF THEY DONT DEFEND THE DEMAND FLOOR .

#US10Y #BONDS #YIELD

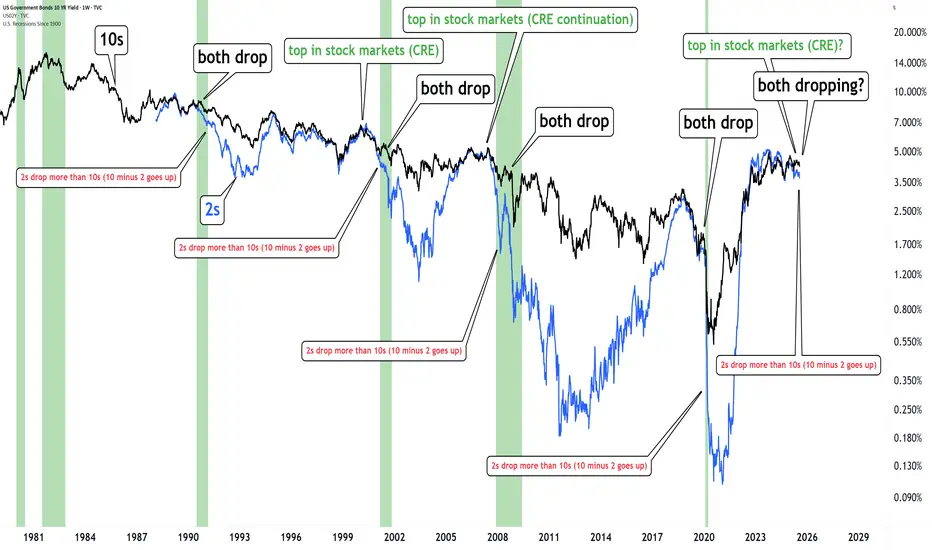

The bond market is warning us.When both 2s & 10s drop together and the yield curve steepens (10–2 rises)... It’s historically followed by important market turmoil

Happened in 2000, 2008 and 2020.

It's possibly happening again.

The bond market is warning us.

US10Y1. Labor Market Data

Average Hourly Earnings m/m:

Actual: 0.3%

Forecast: 0.3%

Previous: 0.2%

Interpretation: In-line with forecast and slightly above the prior period, indicating stable wage growth. This suggests inflationary pressures from labor costs remain steady, not accelerating unexpectedly.

Non-Farm Employment Change:

Actual: 73,000

Forecast: 106,000

Previous: 14,000

Interpretation: A clear downside surprise; job gains are well below expectations, and while up from a low previous period, this points to softening labor demand—an early sign of slack in the job market.

Unemployment Rate:

Actual: 4.2%

Forecast: 4.2%

Previous: 4.1%

Interpretation: Matches the forecast but marks a slight uptick, reinforcing mild labor market weakness.

Fed View: The Fed will interpret softer than expected job growth and a higher unemployment rate as evidence of easing labor market pressures—a dovish signal that could support future policy easing if the trend continues.

2. Manufacturing and Industry

Final Manufacturing PMI (S&P Global):

Actual: 49.8

Forecast: 49.7

Previous: 49.5

Interpretation: Slightly above forecast but still below the 50 threshold, indicating contraction persists but is less severe.

ISM Manufacturing PMI:

Actual: 48.0

Forecast: 49.5

Previous: 49.0

Interpretation: Below both forecast and prior; contraction in the manufacturing sector is deepening.

ISM Manufacturing Prices:

Actual: 64.8

Forecast: 69.9

Previous: 69.7

Interpretation: Lower than both forecast and previous, signaling input price pressures are easing—positive for the Fed’s inflation outlook.

Fed View: Ongoing contraction in manufacturing and lower input prices support the argument that inflation risks are cooling from the supply side, allowing for a more dovish stance.

3. Consumer and Construction

Revised UoM Consumer Sentiment:

Actual: 61.7

Forecast: 62.0

Previous: 61.8

Interpretation: Slightly below forecast, little change—consumer confidence remains relatively subdued.

Construction Spending m/m:

Actual: -0.4%

Forecast: 0.0%

Previous: -0.4%

Interpretation: Same as previous, misses forecast—ongoing weakness in construction and real estate investment.

Fed View: Weak consumer sentiment and persistent soft construction data reinforce slower demand-side dynamics, an argument in favor of pausing or even cutting rates.

4. Inflation Expectations

Revised UoM Inflation Expectations:

Actual: 4.5%

Forecast: Not directly listed (prior 4.4%)

Interpretation: Ticks up slightly, indicating that consumers expect inflation to remain higher. This could temper the Fed’s willingness to cut rates too soon—if expectations become unanchored, the Fed may have to stay hawkish.

Overall Fed Interpretation

Labor market: Softer than forecast, unemployment up—dovish for rates.

Manufacturing/industry: Slight improvement in PMI, but ISM shows contraction; input prices are easing—dovish.

Consumer/construction: Little improvement, still weak—dovish.

Inflation expectations: Up slightly—potential hawkish caution.

Net result: The data is mostly dovish—except for the higher inflation expectation which remains a concern. The Fed will likely see this data as supporting a “watchful pause” and adopt a more flexible stance: no immediate rate cut, but the case for easing is growing unless inflation expectations keep drifting higher. Sustained weak jobs or further easing in prices would increase the chances of a rate cut in coming months. Elevated inflation expectations will keep the Fed cautious about acting too quickly.

#DOLLAR #US10Y #STOCKS #BONDS #YIELD

US Treasury 10Y Technical Outlook for the week July 28-Aug 1 US Treasury 10Y Technical Outlook for the week July 28-Aug 1 (updated daily)

Overnight

Overnight, U.S. Treasury yields reversed their upward trend and traded lower as investors awaited key developments from the Federal Reserve’s upcoming policy meeting and ongoing U.S.-China trade talks. The benchmark 10-year Treasury note yield fell to 4.35%, a decrease of 2 basis points, while the 30-year bond yield dropped to 4.92%, down 3 basis points. This shift followed a period of elevated yields driven by concerns over potential inflationary pressures from proposed U.S. tariffs. Market participants were particularly focused on the Federal Reserve’s stance on interest rates, with futures markets indicating a likely rate cut in September. Additionally, trade negotiations in London between U.S. and Chinese officials added uncertainty, as economists anticipated that tariff-related disruptions could push the Consumer Price Index higher, potentially impacting future Fed decisions. The market’s cautious mood was reflected in a light economic data calendar, leaving room for yields to react to trade and Fed-related headlines.

Economic Release for the Week www.myfxbook.com

Weekly Bias

As expected last Monday we were anticipated that 4.395% will be mitigated. Basing on how the market moved last week and the week closing through below previous week low I am anticipating a continuation to target 4.33% to 4.322%. Bear in mind though that this week’s FOMC meeting could generate a significant volatility and become a catalyst to our projection.

Daily Bias UST 10y July 29

Overnight

The yield on the 10-year US Treasury note remained steady at approximately 4.39% for the third consecutive session as investors awaited a critical week of monetary policy and economic data. The Federal Reserve is expected to maintain current interest rates at its Wednesday meeting, with markets keenly observing for indications of a potential rate cut in September. Investors are also focused on the upcoming Personal Consumption Expenditures report, the Fed’s preferred inflation measure, which may reveal the impact of tariffs on price dynamics. Additionally, a series of labor market data releases, culminating in Friday’s closely watched monthly jobs report, will draw significant attention. On the trade front, a recent US-EU agreement has reduced tariffs on most EU exports to 15%, down from a previously threatened 30%, alleviating some trade-related uncertainty.

Economic Release July 29 www.myfxbook.com

Daily Bias

Basing on price action I am anticipating market to test the previous day high of 4.42%. Market is also waiting for the start of the FED meeting which could contribute to low volatility for the meantime. Although market is expecting no move but any deviation from policy expectation could create high volatility.

Daily Bias UST 10y July 30

Overnight

Overnight, U.S. stock markets experienced a downturn, with major indices like the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite declining ahead of anticipated Federal Reserve announcements. The drop was primarily driven by uncertainty surrounding potential interest rate decisions and ongoing trade tensions, particularly following President Trump’s recent tariff policies. Concurrently, U.S. Treasury yields, including the 10-year note, fell to 4.28% from 4.35% the previous day, reflecting investor caution and a shift toward safer assets amid economic concerns. This market reaction underscores heightened sensitivity to Federal Reserve actions and the broader implications of trade disruptions on global economic growth.

Economic release July 30 www.myfxbook.com

Daily Bias

Cautious positioning kicks in and all our anticipated targets were all missed instead market moved to our weekly bias of 4.33% and old week low of 4.322%. This is expected on an FOMC week due on Thursday morning. With how the market moved yesterday I am anticipating a further test on the low side of previous day range but don’t discount any volatility with GDP due to be released later tonight . www.tradingview.com

Daily Bias UST 10y July 31

Overnight

The yield on the 10-year US Treasury note rose to 4.35% on Wednesday, rebounding from a near-one-month low of 4.32%, as markets evaluated the Federal Reserve’s decision to maintain interest rates and its neutral stance on future policy moves. Strong US GDP growth of 3% in Q2, exceeding market expectations, was tempered by distortions from net foreign demand due to import front-loading. Volatile trade data reflected new tariffs imposed by President Trump on India and Brazil. The Treasury announced stable issuance volumes for notes and bonds but plans to double long-end nominal buybacks and increase TIPS buybacks, aligning with efforts to manage long-end yields, as outlined by Secretary Bessent.

Economic Release July 31 www.myfxbook.com

Daily Bias

Prior to FOMC decision the yield moved higher (price lower) and retraced to the 50% range of the prior day’s range (Tuesday). Today I would like to wait if the market would continue the bullish move of Tuesday. We are on an inside candle pattern so I would like more confirmation for the next move.

**Disclaimer:**

The technical analyses provided herein are based solely on my personal analysis and are intended for my own study and reference. They do not constitute a recommendation or solicitation to buy or sell any financial instruments. Any decision made by individuals based on this analysis is their own responsibility, and I assume no liability for any losses or damages incurred as a result of using this information. It is advisable to conduct thorough research and consult with a qualified financial advisor before making any investment decisions.

U.S. homebuilders tumble as rate cut bets decrease after Powell'** Shares of U.S. homebuilders slide on Weds after Fed chair Powell says no decision yet on rate cuts

** Markets now pointing to odds dropping below 50% that the Fed will cut rates at its next meeting in Sept, as benchmark U.S. 10-year yield

US10Y

extends rise

** Rising yields can potentially lead to higher mortgage rates, which could negatively impact homebuilders by making homes less affordable for consumers

** PHLX Housing Index

HGX

dropping >2% on the session

** Among biggest HGX fallers are: LGI Homes

LGIH

5%, DR Horton

DHI

>2%, Lennar

LEN

nearly 3%, Pultegroup

PHM

>3%

** In S&P 500

SPX

, building products maker Builders FirstSource

BLDR

down 5%, and home improvement retailers Home Depot

HD

and Lowe's

LOW

both off nearly 2%

** With moves on Weds, HGX down ~2% YTD vs 8% advance in SPX

T-Bond Futures & US10Y Yields Weekly BiasUS10Y: 4.288% - 4.240%

T-Bonds: 115.11 - 115.24

Bullish t-bond, bearish US10Y

Crude Oil Spikes - Russia / Ukraine / USA sanction? Concerns about the possibility of tighter global oil supplies are supporting crude prices after President Trump warned of "secondary sanctions" if Russia fails to reach a ceasefire in Ukraine within 10 to 12 days.

These sanctions have absolutely burned the shorts in oil and can cause a 3 bar surge on the daily chart if crude breaks this channel.

Keep you eye on the daily 200 MA...if it holds above we should push higher on crude.

FOMC RATE DECISION TOMORROW - Tune into our live stream.

US05Y Bullish ideaWe can see we had rejection after taking out our sell side liquidity and balancing our daily fair value gap. We are still showing strength in the bond market as well with the dollar index. Our DOL is to the upside in the form of buyside liquidity and our daily volume imbalance at 4.073%.

* Fundamentals: We are having a rise in inflation and a stronger interest rate of the dollar against most of the major basket currency pairs, which in the longer term should potentially see us get a stronger dollar and an increase in our bond yields.

US 10Y TREASURY: FOMC week During the previous week investors were digesting the latest macro data aiming to set expectations for the forthcoming FOMC meeting, which is scheduled for Wednesday, July 30th. The 10Y Treasury yields were moving between 4,32% and 4,44%, closing the week at 4,38%. The drop in yields during the second half of the week was impacted with a trade deal between the US and Japan. Negotiations with the EU are taking place during the weekend in Scotland, whose outcome will be known at the start of the week ahead.

Regardless of trade negotiations, the week ahead will bring a lot of currently important US macro data, as well as the FOMC meeting. Current expectations with 95% odds is that the Fed will keep interest rates unchanged in July. Also, it is expected that Fed Chair Powell will inform the public about the latest Feds members view on the US economic developments. In case of any information that the market still has not priced, the higher volatility will take place. For the week ahead, there is both probability for a further modest relaxation in yields, at least till the level of 4,35%, and also potential for testing of 4,4% for one more time.

Bond Bulls Smell Blood: 20-Year Yields Likely to Fall🧩 Fundamental Bear Case for 20-Year Yields

1. Recession Risk and Slowing Growth

Leading economic indicators (e.g., ISM Manufacturing, Conference Board LEI) continue to suggest softening demand across key sectors.

A recession or significant slowdown would drive capital into long-duration Treasuries, causing yields to fall as bond prices rise.

Historically, 20-year yields fall 200–300bps from cycle peaks during recessions. With yields near 5%, there is ample downside room.

2. Federal Reserve Policy Pivot

The Fed’s hiking cycle appears to be at or near its terminal point. Rate cuts in 2025 are increasingly priced in, especially as inflation moderates.

If inflation continues to decelerate toward the Fed’s 2% target while growth slows, the Fed may be forced to ease sooner or more aggressively than expected.

Long-duration bonds, including the 20Y, are highly sensitive to forward rate expectations and would benefit from a dovish pivot.

3. Disinflationary Trends

Core inflation metrics (e.g., Core PCE, Core CPI) are in year-over-year decline.

Key disinflationary forces:

Wage pressures have eased as labor markets normalize.

Housing costs, which lag in CPI data, are projected to fall further.

Supply chain normalization continues post-COVID.

These factors reduce the need for elevated long-term yields, especially with inflation expectations anchored.

4. Supply-Demand Dynamics Favor Treasuries

Despite large Treasury issuance, global demand remains strong:

Foreign buyers (e.g., Japan, EU) seek higher yields as their home rates remain low or negative.

U.S. institutions (pensions, insurance funds) are rebalancing into risk-free long bonds amid equity volatility.

A risk-off rotation or broader de-leveraging cycle would only accelerate this demand.

🔍 Technical Summary

Rising wedge pattern is nearing a potential breakdown — a bearish structure signaling exhaustion.

Price is failing to reclaim the previous uptrend channel, now acting as resistance.

A completed harmonic AB=CD pattern near recent highs suggests a mean-reverting move could be imminent.

Closest technical targets include:

4.33% (23.6% Fib)

3.68% (38.2% Fib)

Possibly even 3.16% (50% retracement) over the next 6–12 months if macro weakness persists.

📌 Bottom Line

The combination of:

Cooling inflation

A Fed pivot on the horizon

Rising recession risk

And technical exhaustion signals

Supports a bearish outlook for 20-year yields, meaning bond prices (especially long-duration instruments like TMF or TLT) could appreciate meaningfully from here.