Breakout Setup: $EL !🚨 🚨

📈 Price cracked key resistance at $78.85

🔁 Breakout + Retest confirmed

🎯 Targeting: $83.94

🛡️ Stop Loss: $76.85

📐 Risk/Reward: ~2.5R

🔥 Bullish structure, strong momentum, and volume behind the move.

Is this the start of a bigger reversal? 👀

#EL #BreakoutTrade #SwingSetup #NYSEStocks #ProfittoPath #TechnicalAnalysis

Breakout Alert: $TRUP!🚨 🚨

📈 Clean breakout above resistance at $56.40

🔁 Retest ✅

🎯 Target: $59.10

🛡️ Stop: $55.46

🧠 RR: ~2.6R — textbook setup!

👀 Watching for momentum continuation in this quiet climber...

Will it surprise the market next? 👇

#TRUP #BreakoutTrade #SwingTrading #PriceAction #ProfittoPath

Coin base breakout on high volume Coin base is at the entry on the daily. With positive news in the market gives up bullish sentiment. Targeting TP3

$RDDT Long Setup – Bullish BreakoutReddit ( NYSE:RDDT ) has broken out above the Ichimoku Cloud on the daily chart, signaling a potential shift in trend. Momentum is building with MACD pushing higher and no signs of divergence, showing continued strength. While this trade offers a solid 2.1 risk/reward setup (entry at $134.14, stop at $108.80, target at $188.34), the current entry is not ideal—price is extended from support, and the breakout has already moved significantly. However, the structure still points to bullish continuation. If RDDT can hold above the $130–$135 zone, there’s room to run into the $180s and potentially beyond. A pullback toward the breakout zone would offer a stronger entry, but the upside here remains attractive for a swing trade. This setup is best approached with smaller size or added confirmation if chasing.

Bearish Elliot Triangle Wave $250 targetObserving Tesla Chart, I noticed a bearish 4hr Elliot Wave A-E. The flow is also bearish and lines up with the bear sentiment. Looking for a bearish Apex Breakout..

$NVDA 6/27 exp week; $150 calls. Quick ChartHello. Market is moving up off the “news” of “ceasefire” from Trump. Take what is given I suppose. NASDAQ:NVDA could see a beautiful upside towards the psych level of $150 in just one session (Tuesday, 6/24) which is just a “small” move of 3%. Could break out of its rising wedge. This name has been lackluster as of late (kinda sorta). $150 calls will be entered at open (6/24) and my first target will be $148.98. There are multiple rejections at these levels. Good luck!

WSL

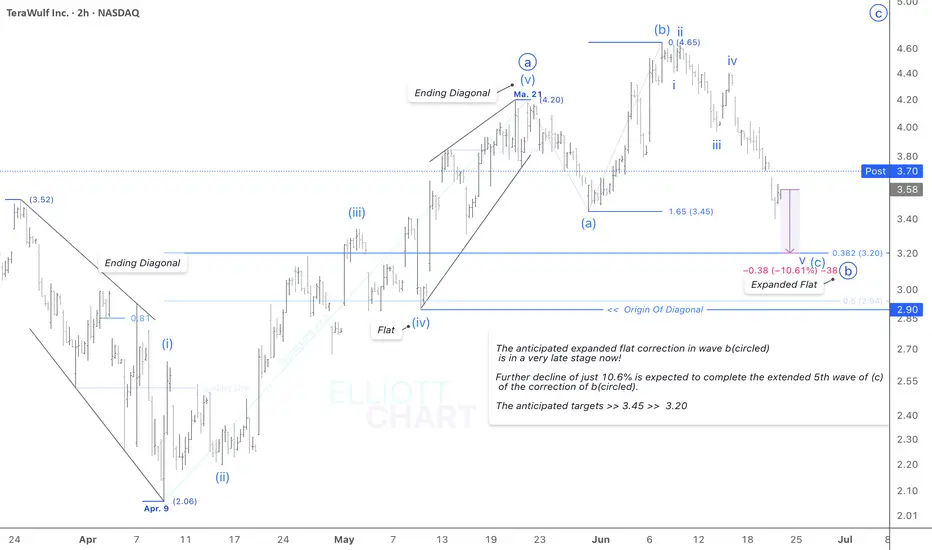

WULF / 2hAccording to the prior analysis, NASDAQ:WULF reached the first target >> 3.45, extending its correction by a 9% intraday decline in the 5th subdivision of wave (c), as anticipated. A final decline of just 10.6% will conclude the entire correction in wave b(circled) in an expanded flat formation very soon!

The next retracement target >> 3.20

Trend Analysis >> The trend will turn upward soon! to a Minute degree impulsive wave c(circled) after completion of correcting down in the same degree wave b(circled).

#CryptoStocks #WULF #BTCMining #Bitcoin #BTC

RIOT / 2hAs anticipated in the prior NASDAQ:RIOT 's analysis, the expected decline(7.3% intraday) as the last subdivision of the leading diagonal wave A, is quite well done.

Wave Analysis >> The leading expanding diagonal in Minor degree wave A, as the first subdivision of the ongoing correction in wave (2), indicates that a relatively deep correction in wave (2) might be thoroughly developed.

Trend Analysis >> The trend is correcting down in the Intermediate degree wave (2), which will take a few weeks to develop.

The retracement targets >> 8.76 >> 8.20 >> 7.93 >> 7.67

#CryptoStocks #RIOT #BTCMining #Bitcoin #BTC

Nvidia - New all time highs!Nvidia - NASDAQ:NVDA - breaks out now:

(click chart above to see the in depth analysis👆🏻)

Within two and a half months, Nvidia rallied more than +70%. Following this recent bullish strength, a retest of the previous highs was totally expected. But this does not seem to be the end at all. There is a much higher chance that we will see new all time highs soon.

Levels to watch: $150

Keep your long term vision🙏🙏

Philip (BasicTrading)

My RKLB for the rest of 2025 before sell offI believe we are going through these 2 scenario drawn out on my chart

1) we have a head and shoulder sell off. target $48-55

2) we go higher following the orange line neutron and really good news. target $95-124

good luck to all may u have success in all your trading setup

Meta Platforms - This stock tastes sooo good!Meta Platforms - NASDAQ:META - will print a new all time high:

(click chart above to see the in depth analysis👆🏻)

Over the course of the past two months, Meta has been rallying +40%. This recent behaviour was not unexpected at all but rather the consequence of the all time high break and retest. Now - back at the previous all time high - Meta will most likely break out higher again.

Levels to watch: $700, $900

Keep your long term vision!

Philip (BasicTrading)

$IREN Long Setup – Ichimoku Cloud Breakout with MACD Momentum IREN is setting up for a strong long opportunity on the daily chart, showing clear bullish structure and momentum. Price has broken above the Ichimoku Cloud with confirmation from both Tenkan-sen and Kijun-sen alignment, and the future cloud remains bullish. This breakout has held for several weeks now, with consistent higher highs and higher lows forming since the April bottom. The MACD is also supporting the move, with both the MACD line and histogram in bullish territory and no immediate signs of bearish divergence. The setup presents a clean risk/reward profile: entry at $10.67, stop at $9.09 just below recent support and Tenkan-sen, and a target at $16.25, which aligns with the R2.5 pivot zone and historical resistance from mid-2023. That’s a risk/reward ratio of 3.53. Volume has been steadily building on up days, suggesting institutional accumulation. If price breaks and holds above the $11.25 pivot (R1), expect continuation toward the next resistance levels at $16.25 and potentially $19+. I’m viewing this as a 2–6 week swing trade based on the daily chart structure and overall trend.

Will PLTR Push Through the Gamma Wall? Jun 24🔍 Overview:

Palantir Technologies (PLTR) is trading at $139.92 (+1.91%) as of June 23 close. After days of range-bound action, bulls are trying to reclaim critical levels while battling overhead gamma resistance. With Smart Money Concepts showing both BOS and CHoCH, the next move could be explosive.

🔩 Market Structure (SMC View):

* 15m Chart:

* Clear Break of Structure (BOS) upward in morning session.

* Followed by Change of Character (CHoCH) bearish in the afternoon.

* Price tapped into a green demand zone and reacted with a bounce near $137.

* A re-test of the red CHoCH supply zone around $140.50–$141.30 is in progress.

* Trendlines suggest a tightening wedge, with the top of the channel converging near $144.

🧠 GEX and Options Sentiment:

* Gamma Wall (Call Resistance):

🔼 $142–143 zone – Highest net GEX (CALL wall), where market makers may start shorting gamma, creating resistance.

* Major Call Walls:

* $145 (12.37% GEX)

* $149–150 (Strongest 2nd layer walls)

* PUT Wall Support:

* $130 major PUT support (7.49% wall)

* $134 is minor soft support area.

* IV & Sentiment:

* 📉 IV Rank (IVR): 17.3 – low, indicating cheap premiums.

* Call Buying Strength: 38.4% – moderately bullish.

🔄 Key Zones:

* 🔴 Supply Zone (CHoCH): $140.50–$141.30

* 🟢 Demand Zone (CHoCH): $135.97–$137.30

* ⚠️ Trap Range: Between $137 and $141 — liquidity likely to be swept in both directions before a move.

📈 Trade Setups:

Bullish Scenario:

* Entry: On break and close above $141.50 with retest confirmation.

* Targets:

* $143 → Minor profit-taking zone

* $145 → Next GEX wall

* $149–$150 → High GEX squeeze potential

* Stop: Below $137.30 or mid-channel around $136.50

📌 Ideal if price reclaims above the CHoCH zone and builds volume support near $141.

Bearish Scenario:

* Entry: Rejection from $141.30 supply or breakdown under $137.

* Targets:

* $135.97 → First reaction zone

* $134 → Secondary support

* $130 → Strong GEX-supported PUT level

* Stop: Above $141.60 or structure high of $142.15

📌 Watch for reversal signs inside supply zone or heavy selling into demand.

🔮 Bias:

Neutral-to-Bullish → ⚔️ Battle at $141 CHoCH zone. Gamma resistance is real, but if broken, it could fuel a gamma squeeze toward $145+.

💡 Actionable Advice:

* Scalpers: Fade resistance near $141.30 unless it breaks clean.

* Swing Traders: Wait for break and retest of $141.50 → target $145+.

* Options Traders:

* Low IVR = Great time to buy CALLS if bullish.

* If expecting chop, long straddle at $140 may work before the move.

📌 Conclusion:

PLTR is consolidating right beneath a major gamma wall and previous SMC CHoCH level. If bulls can break through $141.50 with strength, we could see a momentum move to $145 and even $150 this week. Until then, volatility traps remain likely within $137–$141.

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and trade responsibly.

TSLA Breaking Out! Is This Just the Beginning or a Trap? Jun 24 🔥Price Action Overview:

TSLA had a powerful move, jumping +8.23% to $348.68. It cleared key resistance and now consolidates near $349–350. Volume surged, but we’re seeing a bull flag structure with some internal weakness forming.

🧠 Smart Money Market Structure (15-min Chart)

* CHoCH occurred before the breakout, showing smart money accumulation.

* Break of Structure (BOS) confirms bullish intent.

* Price is now ranging in a supply zone, rejecting upper levels with signs of compression.

* Consolidation wedge suggests a possible breakout or fakeout setup.

🔮 Gamma Exposure (GEX) Breakdown (1h Chart)

* Current Price: $348.68

* Gamma Resistance (Call Wall):

* $357.53 → 1st resistance

* $365.00 → heavy resistance

* $367.5 → Extreme Call Wall / GEXY8

* Gamma Support:

* $340 → strong support

* $320 → HVL (High Volume Level) and PUT defense

* $315 / 312.5 → 2nd PUT Wall (if breakdown)

Interpretation:

Price is trapped between GEX compression levels. A breakout above $350 could trigger a gamma squeeze toward $357–360+. A breakdown below $340 targets $320 fast.

📈 Indicators Snapshot

* Volume: High on the breakout, but tapering off during consolidation.

* RSI/MACD (not shown): Likely cooling off — favoring a pullback or re-accumulation.

* CHoCH & OB Zones: Indicate smart money watching $340-$345 for support retest.

⚖️ Scalping vs Swing Outlook

✅ Bullish Case

* Break above $350 → Watch $357.50 and $365 targets.

* Above $367 = gamma squeeze zone unlocked.

Entry: Break and hold $350

Target: $357.50, then $365

Stop: Below $345

⚠️ Bearish Case

* Break below $340 → Flush to $320 and possibly $315

* GEX puts will dominate under $320

Entry: Break and hold below $340

Target: $320, $315

Stop: Above $345

🧭 Trade Strategy Summary

* ⚔️ Inflection Zone: $340–$350 = Decision zone

* 🚀 Watch for gamma squeeze if $350+ holds

* 🛑 Breakdown below $340 flips bias bearish

* 🔄 Volume confirmation is key

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk carefully.

NFLX She got away #3Ahh yes the 3rd stock/idea/position I sold out of in order to go all in on $TSLA. I will stay the course with my plan, but when it hits I'm going to Diversify. You should only make mistakes once, if you repeat them you should cut your left nut. IDK, just have a real consequence so you don't F up again.

Currently it's overextended and needs a correction to 1100-1000....but what happens if they announce a stock split? oh yeah, this could moon..... again. fml

GOOGL at a Make-or-Break Zone! Will 165 Hold or Fold? Jun 24🔍 Market Structure:

GOOGL has been in a clear downtrend, printing multiple BOS (Break of Structure) on the 15-min and 1H charts. However, today we’ve seen a CHoCH (Change of Character) after price bounced from the key 162 zone. This signals a potential short-term reversal or at least a relief rally.

🧭 Key Zones (Price Action + SMC):

* Support (Demand Zone):

* 162.00 → Major liquidity zone & 3rd PUT Wall

* 160.00 → Highest Put Wall, strong support

* Resistance (Supply Zone):

* 165.20–166.00 → Minor supply & CHoCH test zone

* 167.34–167.65 → Major Supply & 2nd Call Wall

* 170.00–172.5 → Critical resistance stack w/ 3rd Call Wall

🧠 GEX + Options Sentiment:

* GEX Zones:

* Strongest Put Wall: 160 (–52.5%)

* Highest NET GEX (Support): 165

* Call Resistance Wall: 175 (52.91%)

* IVX avg: 34.4

* IVR: 31

* Calls Interest: 17.2% (moderate bullish positioning)

This tells us that 165 is acting as a magnet and bounce zone, while 175 is where market makers are likely to keep a lid on the rally.

📊 Indicators & Volume:

* Volume on the bounce was decent—indicating some real buyer interest.

* If price consolidates above 165 and holds into tomorrow, it could trigger a push toward 167.5 and 170.

* A breakdown back below 162 would invalidate this bounce and resume bearish flow toward 160.

🎯 Trade Scenarios:

🔼 Bullish Case (Relief Rally Setup):

* Trigger: Hold above 165 + reclaim 167.5

* Targets: 170 → 172.5 → 175

* Stop: <162 (invalidates the structure)

🔽 Bearish Case (Fade Setup):

* Trigger: Reject at 167.5 or 165 and break below 162

* Targets: 160 → 155

* Stop: >168 (if breakout traps)

🧩 Scalping Setup:

* Above 165.20: Quick scalp to 166.64 / 167.34

* Below 162.50: Breakdown scalp to 160.00

⚠️ Final Thoughts:

GOOGL is in the early stages of a potential reversal — but it’s still fighting under multiple resistance layers. Unless 167.5 breaks clean, this may still be a sell-the-rip environment. Watch how it behaves at the HVL (165) — it’s the pivot for both bulls and bears.

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk properly before trading.

NVDA GEX Zones + Price Setup: Big Move Loading? Jun 24

🔍 Market Structure Overview (15m + 1h Combo)

* NVDA showed bullish BOS and CHoCH structure earlier today, reclaiming mid-range after tapping demand.

* The current CHoCH (purple box) is forming just under the $145 rejection area.

* A strong bounce off the green OB demand box around 142.00–142.04, holding this zone keeps upside potential alive.

* The upward trendline still valid unless we break under the green demand zone.

📊 GEX + Options Sentiment (1H Chart)

* Highest Net GEX / Call Resistance: $147 — strong resistance area.

* Second Call Wall: $148

* Gamma Wall Confluence: $146.20–147 zone –> expect rejection or a squeeze trigger.

* Put Walls: 140 / 139 / 138 — stacked gamma support.

* IVX avg: 37.4 (low volatility), IVR: 0.4 → cheap premium environment.

* CALL bias: 7.2%, 3 Green Dots = Bullish Bias w/ room to run.

🧠 Smart Money Concepts (15m)

* BOS to upside already confirmed.

* New CHoCH forming within a micro consolidation zone between $144–$145.

* Price is currently dancing around mid-supply zone.

* Liquidity still resting above 146.20, creating fuel if breakout sustains.

📌 Trade Scenarios

Bullish Case:

* Trigger: Break and hold above 145.00

* Target 1: $146.20 (first resistance)

* Target 2: $147–$148 (Call Wall + Net GEX)

* Invalidation: Break below 143.00

* Optional Call entry: Above 145, SL below 143.80

Bearish Case:

* Trigger: Rejection at $145 + CHoCH breakdown confirmation

* Target 1: $142.00 (Demand OB)

* Target 2: $140 (PUT Wall)

* Put entry: below $143.50, with volume surge and failed retest of 144

🎯 Final Thoughts:

NVDA is building energy in a tight CHoCH range. A push above $145 opens the gate to a gamma squeeze into $147+. Watch the reaction at 144.78 and 145 zone closely — it’s make or break. Under 143.00 and this flips bearish fast.

This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage your risk before trading.

MSFT setup for June 241H Chart + GEX (Options Sentiment) Overview

* Current Price: $485.99

* Strong Resistance Zone:

* 490 → 492.5 = Highest positive GEX zone / CALL Wall resistance

* Multiple GEX levels stacked:

* GEX7: 45.76%

* GEX8: 43.68%

* GEX9: 34.16%

* Support Zone:

* 477.5 → 482.5 = Key gamma support + previous demand cluster

* HVL (Highest Volume Level): $472.5 = major downside magnet if pullback strengthens

💡 GEX Bias:

* Very strong CALL side pressure.

* Implied volatility rank (IVR): 8.7 (very low) — ideal for debit spreads or long calls.

* GEX bars taper off past 492.5, showing limited bullish gamma fuel after that level — expect a fade or chop above 492.5.

💼 Options Trade Recommendation:

🔹 Strategy: Call Debit Spread

* Buy: 485C

* Sell: 490C

* Target: $489–$492 (highest GEX zone)

* Stop: Close below $482.5

* Rationale: IV is low, bullish trend, but heavy GEX wall at 490 could stall the rally. Safer to limit upside with spreads.

🕒 15-Min Chart Breakdown (Intraday SMC Price Action)

* Structure:

* BOS (Break of Structure) confirmed on upward move

* CHoCH (Change of Character) just below 486, minor pullback zone forming

* Current range forming inside a small red zone (15M supply) → watch for reaction here

* Support Areas:

* 483.88 = previous resistance → flipped support

* 482.50 = key EMA + demand zone base

* 477.40 = strong confluence with previous BOS and volume base

* Trendline Support: Still intact from earlier LTF rally — buyers still in control unless 482 breaks.

🛠️ Intraday Trade Plan

🔹 Bullish Scenario (preferred)

* Entry: 484.50–485.00 on pullback and confirmation

* Target: 487.50 → 490.00

* Stop: Below 483.50

🔹 Bearish Rejection Play (if rejection at red supply box holds)

* Entry: 486.50–487.00 (only on clear rejection + CHoCH)

* Target: 483.80 → 482.00

* Stop: Above 487.50

📌 Final Thoughts:

* Call Buyers clearly in control, but 490–492.5 is where the option market starts resisting price.

* IV is low → long premium trades make sense.

* Watch CHoCH zones intraday for any early weakness if market shifts risk tone.

📉 Disclaimer:

This analysis is for educational purposes only and does not constitute financial advice. Always manage risk and use proper sizing in trades.

CLSK / 2hNASDAQ:CLSK had a 6% intraday decline today, completing the second wave of an expanded flat correction in wave b upward.

Wave Analysis >> The leading expanding diagonal as wave a is correcting up in wave b, which should have remained in the last subdivision upward that 7.4% advance now is left.

The retracing up target remains intact >> 9.51

An impending decline by 17.6% as the last subdivision >> wave c of (y) would lie ahead that finally will conclude the entire correction in Minute degree wave ii(circled).

The retracing down targets >> 7.93 >> 7.84

Trend Analysis >> After the completion of the entire correction in the Minute degree wave ii(circled), the trend will turn upward to an impulsive third wave in the same degree.

#CryptoStocks #CLSK #BTCMining #Bitcoin #BTC

HOOD Got away #2I swear man, I said anything under 10 and I was loading up..... I did start but then I went all in on NASDAQ:TSLA and here she is another 10 bagger has come and gone. Lesson is Diversify, well sorta. If there's not catalyst for other stonks making big moves then put some here and there. I'm going to buy into this again in the future it's growing like a mofo.

RBLX. Buying for a long term hold. Huge levels of support we must hold on roblox. I will be buying for a long term position.

HIMS puked up its Wegovy today!Hims & Hers Health

HIMS

shares were down more than 34.63% in Monday trading, while Novo Nordisk

NVO stock was down over 5% after Novo Nordisk said it has halted its collaboration with Hims & Hers on the sale of weight loss drugs, including Wegovy.

The two companies launched a collaboration in April to bundle Wegovy through Hims & Hers' telehealth platform.

Novo Nordisk said direct access to the drug would no longer be available through Hims & Hers Health because the company "has failed to adhere to the law which prohibits mass sales of compounded drugs under the false guise of 'personalization' and are disseminating deceptive marketing that put patient safety at risk."

This stock failed to catch a bid despite the equity markets strong.

AMPX may breakout soonNice triangle after a run off the bottom. Inverse head and shoulder (working right shoulder)

If it breaks that would be a wave 3 so fib targets are shown.