Amazon update Hi traders this is how Amazon trending as you can see it's already breakout n retest previous high 189.00 we are now sitting at 225 my suggestion is to buy more until 300.00 atleast,some said stocks is slow i really don't see that cz there is no hurry for anything in the market,what is matter is directions n patience n rewards it doesnt matter if you trade forex or crypto or commodities are you making profits or looses this is what matters if you are winning,find what is good for you n stick to the plan,make sure you are notin hurry to be rich without knowledge you might quit unnecessary cz you are competing with really really smart people's who are trying to take.money from you as you are trying to take it from them,soo you must learn how to be objective n not to be greedy n take profits consistently as they come then you can enjoy the journey,i wiah all profitable week n choose any pairs in my post n follow the trend n simple make profits no pain no gain.

Netflix Faces Rising Volatility and Bearish Technicals Ahead of Netflix (NASDAQ: NFLX) will announce its results after the close of trading in New York on Thursday, 17 July. Analysts forecast the NASDAQ-listed streaming media company to report second-quarter earnings growth of 45%, reaching $7.08 per share, while revenue is expected to increase by 15.6%, amounting to $11.1 billion. Net subscriber additions are predicted to decrease by 42.9%, falling to 4.6 million.

For the third quarter, analysts forecast guidance for revenue of $11.3 billion, up 14.7%, and earnings of $6.68 per share, reflecting growth of 23.6%. The options market is pricing in a 6.4% move, either up or down, in Netflix shares following the earnings report.

The significant expected move in the stock is driven by implied volatility levels for options expiring on 18 July, which were high at nearly 70% as of the 13 July close and are likely to increase further as results approach. Options positioning in Netflix also appears notably bullish, with call delta values surpassing put delta values. This indicates that once the company reports its results and options begin to decrease in value due to the decay of implied volatility, market makers might find themselves overly hedged on the long side, potentially forcing them to sell shares. This scenario could exert downward pressure on the stock if it fails to breach the $1,300 level, which acts as the gamma call wall.

Additionally, technical analysis shows a downside risk for the shares both before and after the results. The Relative Strength Index (RSI) for Netflix has been trending lower and recently dropped below 50, signalling a shift in momentum from bullish to bearish. Furthermore, the stock has broken down from a rising broadening wedge pattern, which is traditionally seen as a bearish reversal signal, indicating a possible decline back towards the pattern’s origin, around $1,100.

Written by Michael J. Kramer, founder of Mott Capital Management.

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed.

No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction, or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.

time to buy HLFBouncing off new support, after a very long descent, this company is still profitble and looks severely oversold. Not to mention what looks like a new uptrend, looks like buy and hold for me.

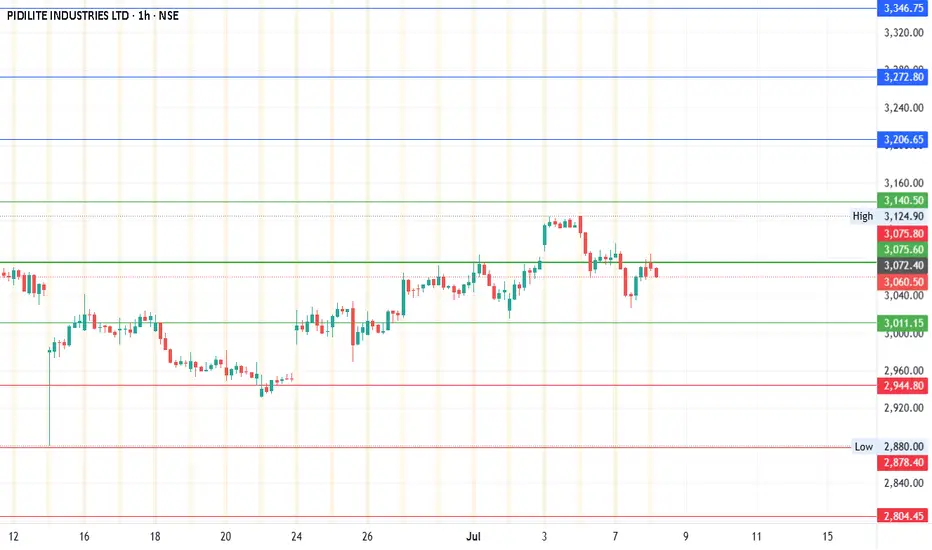

#PIDILITINDDate: 08-07-2025

#PIDILITIND Current Price: 3066

Pivot Point: 3075.60 Support: 3011.17 Resistance: 3140.52

#PIDILITIND Upside Targets:

Target 1: 3206.66

Target 2: 3272.80

Target 3: 3346.75

#PIDILITIND Downside Targets:

Target 1: 2944.78

Target 2: 2878.40

Target 3: 2804.45

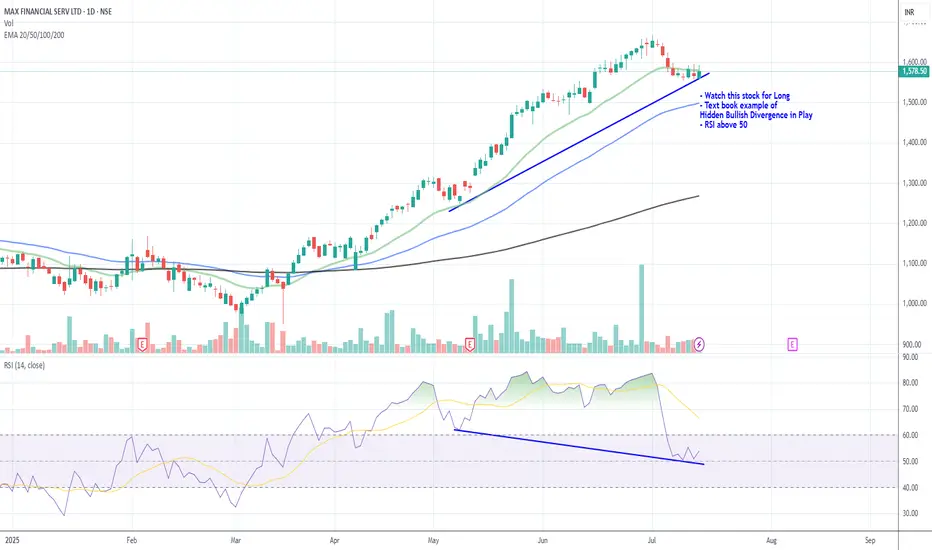

Watch MFSL for Long- Watch this stock for Long

- Text book example of

Hidden Bullish Divergence in Play

- RSI above 50

GADT – BUY SIGNAL (THIRD STRIKE) | 14 JULY 2025 | 1H TIME FRAMEGADT – BUY SIGNAL (THIRD STRIKE) | 14 JULY 2025 | 1H TIME FRAME

After breaking out of a slightly upsloping trading range (marked in light blue) and achieving a high of Rs. 570, GADT pulled back. With the pullback nearly complete, we expect a bounce and a run toward multiple quantified displacement targets.

Fortis Healthcare Long:Fortis Healthcare Long:

- Price takes support @ 20 DEMA

- Near All time high

- Hidden Bullish Divergence

- Earnings call in next month

KEI Industries Long_Support @ 20 DEMAKEI Industries Long:

- Price takes support at 20/50 & 200 Daily EMA

- Hidden Bullish Divergence

- Earnings next week

- Enter Long when the prices are favorable in the lower timeframe

- SL: Close below 20 DEMA

ITTFAQ – BUY SIGNAL (SECOND STRIKE) | 14 JULY 2025ITTFAQ – BUY SIGNAL (SECOND STRIKE) | 14 JULY 2025

Given the recent formation of a bullish structure, we're revising both buy and stop loss levels to reflect the current opportunity.

NCL – BUY SIGNAL (SECOND STRIKE) | 14 JULY 2025NCL – BUY SIGNAL (SECOND STRIKE) | 14 JULY 2025

After a successful first strike that achieved all targets, NCL has now broken out of consolidation zones on both higher (yellow) and shorter (light blue) time frames. This setup presents a strong second strike opportunity.

EMCO – BUY SIGNAL | 14 JULY 2025EMCO – BUY SIGNAL | 14 JULY 2025

After breaking out of a trading range (light blue channel) and achieving a high of Rs. 59, EMCO completed its pullback and retest phase, positioning itself for upward movement.

C (Citi) eyes on $76.14: Golden Covid ready to launch BreakOutC with all banks has recovered to pre-tariff levels.

It has pierced a proven Golden Covid fib at $76.14

Look for a Retest (preferably with a Ping) for entry.

PLTR: Trend Analysis 📈 PLTR | SMC Trend Continuation or Reversal? Watch This Key Zone

🔍 Chart Type: 15m

🧠 Strategy: Smart Money Concepts (LuxAlgo), EMA Stack (20/50/100/200)

📊 Volume Surge: 177.99K

🧭 Narrative: Institutional Accumulation + Premium Rejection

🚨 Current Price: $145.88

📍 Market Structure:

Price is currently reacting from a Premium Zone just above a recent Break of Structure (BoS).

We've seen a Chg of Character (ChgofCHoCH) and several bullish BoS confirming smart money intent.

Volume expansion at the highs suggests potential liquidity grab.

📐 Key Levels:

Premium Zone near $146

Equilibrium at ~$143

Discount Zone begins near $140

Strong Edge (deep discount) below $138

Long-term Target remains at $165.11 if bullish channel is respected.

📉 Bearish Scenario:

Break below Equilibrium and retest of Discount Zone = liquidity sweep

Watch if price retraces toward $140.10 (blue line) or lower for a higher-probability long.

📈 Bullish Scenario:

Break above current swing high confirms expansion toward $152+ and eventually $165.11

EMA stack remains bullishly aligned → trending continuation likely unless broken with momentum.

🔎 Institutional Insight:

Smart Money is likely building positions below equilibrium before major continuation. Liquidity pockets between $138–$140 are prime zones for potential long entries.

📆 Watchlist Catalyst:

Earnings cycle or Palantir federal contract news could align with breakout.

🧠 VolanX DSS Rating: BULLISH BIAS

✅ Structure: Bullish

✅ Volume: High

✅ Liquidity: Grabbed above recent highs

⛔ Confirmation: Await premium rejection or retrace to discount

—

🔁 Executed via VolanX Scanner + WaverVanir DSS

📊 Trade the future. Protect the edge. Lead with intelligence.

#WaverVanir #PLTR #SmartMoneyConcepts #VolumeProfile #MarketStructure #TechnicalAnalysis #VolanX #InstitutionalTrading #QuantFinance #TradingEdge #PropTrading

HUYA | HUYA | Long at $2.61HUYA NYSE:HUYA operates game live streaming platforms in China. This stock got my attention based on the reported fundamentals and price position, but moderate "Chinese delisting" risks exist given the US's new political administration.

Book Value = $3.23 (Undervalued)

Forward P/E = 4.1x (Growth)

Debt-to-equity = 0x (Healthy)

Quick Ratio = 1.56x (Healthy)

Altman's Z Score = <1.8 (Bankruptcy risk is relatively high)

From a technical analysis perspective, the stock price momentum has shifted upward based on the historical simple moving average. The price often consolidates within and slightly outside of this simple moving average band before progressing higher (after a long period of selling). While near term-declines are a risk, a longer-term hold (if the fundamentals do not change and delisting doesn't occur) may pay off given the value, growth, and overall health of the company.

Thus, at $2.61, NYSE:HUYA is in a personal buy zone.

Targets into 2028:

$3.45 (+32.2%)

$5.80 (+122.2%)

Viking Holdings (VIK) – Sailing Ahead in Luxury TravelCompany Snapshot:

Viking NYSE:VIK is a premium cruise operator targeting affluent retirees and “active agers”, offering adult-only ships and experiential itineraries designed for high-value travelers seeking enrichment and comfort.

Key Catalysts:

Premium Brand with Pricing Power 💰

Unlike many peers, Viking has avoided deep discounting, maintaining premium pricing—a testament to brand equity and customer loyalty, protecting margins amid inflationary pressures.

Exceptional Demand & Occupancy 📈

Occupancy rates consistently above 90% reflect both high demand and strong operational execution, boosting revenue per cruise and signaling long-term customer retention.

Tailwinds from Demographic Trends 👴🏻👵🏻

Viking is uniquely positioned to benefit from the global growth in affluent aging populations, who prioritize experience-driven travel over material consumption.

Investment Outlook:

Bullish Entry Zone: Above $46.00–$47.00

Upside Target: $75.00–$76.00, powered by brand strength, margin durability, and demographic-driven demand.

🛳️ As a leader in luxury cruising, Viking is charting a long-term growth course anchored in loyalty, premium experiences, and generational travel trends.

#VikingCruises #VIK #LuxuryTravel #ExperientialTourism #CruiseStocks #ActiveAgers #RetirementBoom #TravelDemand #PremiumBrand #ConsumerDiscretionary

ADBE watch $362-364: Key Support zone must hold to end DownTrendADBE was struggling before last earnings and dumping since.

Currently trying to lift out of a significant support at $362-364

Looking for a Break-n-Retest of zone top Genesis fib at $324.26

.

VivoPower/RippleIf you concatenate VVRP/XRP, you can see that Ripple has been outperforming VVRP. But, we have a bunch of touches of the descending overhead, and I bet that VVPR breaks out from the overhead and starts outperforming XRP.

hdfc bank on side way formation hdfc bang today formed a negative pattern can go in consolidation for a while trendline support is good and needs to sustain above it for positive trend hold

Analyzing and trading stocks using Dr. Elder's Three Screen MethThe first thing I do is analyze the weekly chart. Here I want to see price divergence to the MACD indicator

Next, I go to the daily chart and want to see the divergence between the price and the indicator

I then move to the hourly chart and look for the divergence here.

The price has only risen a couple of points above the previous peak, but that's enough for me. I enter a trade when the bar is broken

NYSE:BK

Stocks SPOT ACCOUNT: WMT stocks Buy Trade with Take ProfitStocks SPOT ACCOUNT: NYSE:WMT stocks my buy trade with take profit.

This is my SPOT Accounts for Stocks Portfolio.

Trade shows my Buying and Take Profit Level.

Spot account doesn't need SL because its stocks buying account.

Looks good Trade.

Disclaimer: only idea, not advice

Stocks SPOT ACCOUNT: AMD stocks buy trade with take profitStocks SPOT ACCOUNT: NASDAQ:AMD stocks my buy trade with take profit.

This is my SPOT Accounts for Stocks Portfolio.

Trade shows my Buying and Take Profit Level.

Spot account doesn't need SL because its stocks buying account.

Stocks SPOT ACCOUNT: TESLA stocks buy trade with take profitStocks SPOT ACCOUNT: MARKETSCOM:TESLA stocks my buy trade with take profit.

Buy Stocks at 297 and Take Profit at 319.

This is my SPOT Accounts for Stocks Portfolio.

Trade shows my Buying and Take Profit Level.

Spot account doesn't need SL because its stocks buying account.

MRK eyes on $80.36/74: Double Golden zone break to end DownTrendMRK and all pharma has been dropping forever.

Just pierced the Double Golden zone yet again.

Break and Hold of this zone will say "bottom".

.