OPEN-SOURCE SCRIPT

MTF MA Ribbon and Bands + BB, Gaussian F. and R. VWAP with StDev

Updated

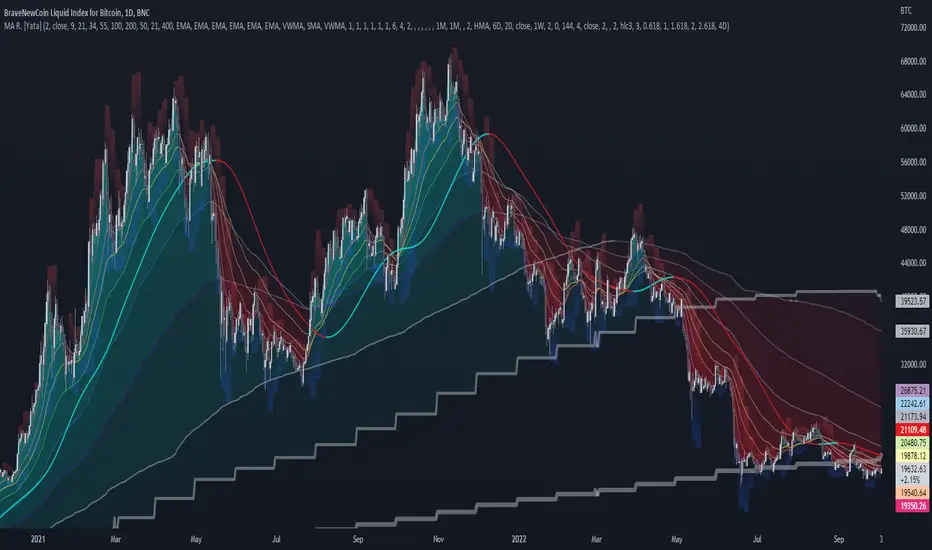

█ Multi Timeframe Moving Average Ribbon and Bands + Bollinger Bands, Gaussian Filter and Rolling Volume Weighted Average Price with Standard Deviation Bands

Up to 9 moving averages can be independently applied.

The length, type and timeframe of each moving average are configurable.

The lines, colors and background fill are customizable too.

This script can also display:

Types of Moving Averages:

█ Moving Average

Moving Averages are price based, lagging (or reactive) indicators that display the average price of a security over a set period of time.

A Moving Average is a good way to gauge momentum as well as to confirm trends, and define areas of support and resistance.

█ Bollinger Bands

Bollinger Bands consist of a band of three lines which are plotted in relation to security prices.

The line in the middle is usually a Simple Moving Average (SMA) set to a period of 20 days (the type of trend line and period can be changed by the trader, a 20 day moving average is by far the most popular).

The SMA then serves as a base for the Upper and Lower Bands which are used as a way to measure volatility by observing the relationship between the Bands and price.

█ Gaussian Filter

Gaussian filter can be used for smoothing.

It rejects high frequencies (fast movements) better than an EMA and has lower lag.

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve.

In the case of low-pass filters, only the upper half of the curve describes the filter.

The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

█ Rolling VWAP

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day.

Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe.

You can thus use the rolling VWAP on any chart that includes volume information in its data feed.

Because the rolling VWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset.

Made with the help from scripts of: adam24x, VishvaP, loxx and pmk07.

Up to 9 moving averages can be independently applied.

The length, type and timeframe of each moving average are configurable.

The lines, colors and background fill are customizable too.

This script can also display:

- Moving Average Bands

- Bollinger Bands

- Gaussian Filter

- Rolling VWAP and Standard Deviation Bands

Types of Moving Averages:

- Simple Moving Average (SMA)

- Exponential Moving Average (EMA)

- SmoothedMoving Average (SMMA)

- Weighted Moving Average (WMA)

- Volume Weighted Moving Average (VWMA)

- Least Squares Moving Average (LSMA)

- Hull Moving Average (HMA)

- Arnaud Legoux Moving Average (ALMA)

█ Moving Average

Moving Averages are price based, lagging (or reactive) indicators that display the average price of a security over a set period of time.

A Moving Average is a good way to gauge momentum as well as to confirm trends, and define areas of support and resistance.

█ Bollinger Bands

Bollinger Bands consist of a band of three lines which are plotted in relation to security prices.

The line in the middle is usually a Simple Moving Average (SMA) set to a period of 20 days (the type of trend line and period can be changed by the trader, a 20 day moving average is by far the most popular).

The SMA then serves as a base for the Upper and Lower Bands which are used as a way to measure volatility by observing the relationship between the Bands and price.

█ Gaussian Filter

Gaussian filter can be used for smoothing.

It rejects high frequencies (fast movements) better than an EMA and has lower lag.

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve.

In the case of low-pass filters, only the upper half of the curve describes the filter.

The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

█ Rolling VWAP

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day.

Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe.

You can thus use the rolling VWAP on any chart that includes volume information in its data feed.

Because the rolling VWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset.

Made with the help from scripts of: adam24x, VishvaP, loxx and pmk07.

Release Notes

FixRelease Notes

CleaningRelease Notes

Added transparency and gradient stepRelease Notes

Added circles line for VWAPOpen-source script

In true TradingView spirit, the author of this script has published it open-source, so traders can understand and verify it. Cheers to the author! You may use it for free, but reuse of this code in publication is governed by House rules. You can favorite it to use it on a chart.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.