OPEN-SOURCE SCRIPT

VWAP with Standard Deviation Bands

Updated

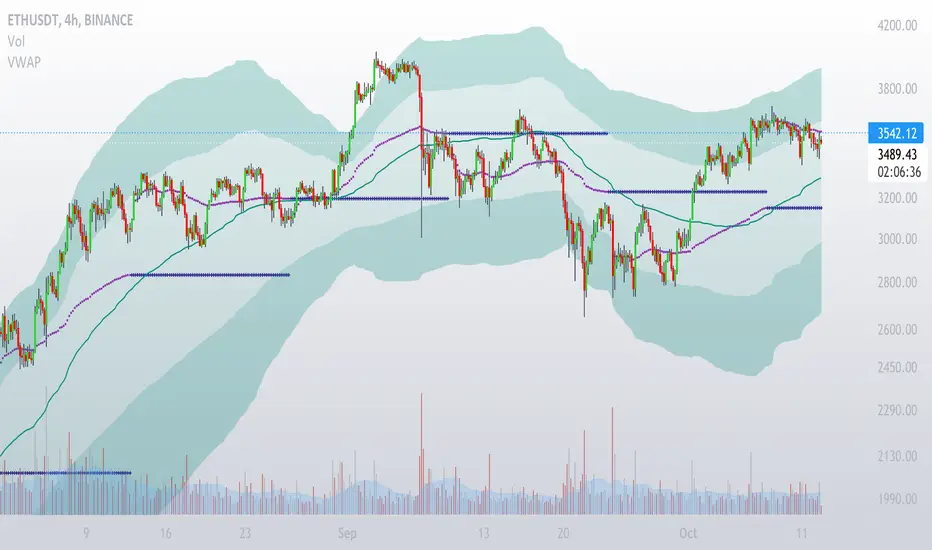

Volume Weighted Average Price (VWAP), with Standard Deviation Bands

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

Release Notes

version=5added rolling VWAP with stdev bands

more divisions in stdev bands (4)

plots style changed

Open-source script

In true TradingView spirit, the author of this script has published it open-source, so traders can understand and verify it. Cheers to the author! You may use it for free, but reuse of this code in publication is governed by House rules. You can favorite it to use it on a chart.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.