OPEN-SOURCE SCRIPT

KDE-Gaussian

Updated

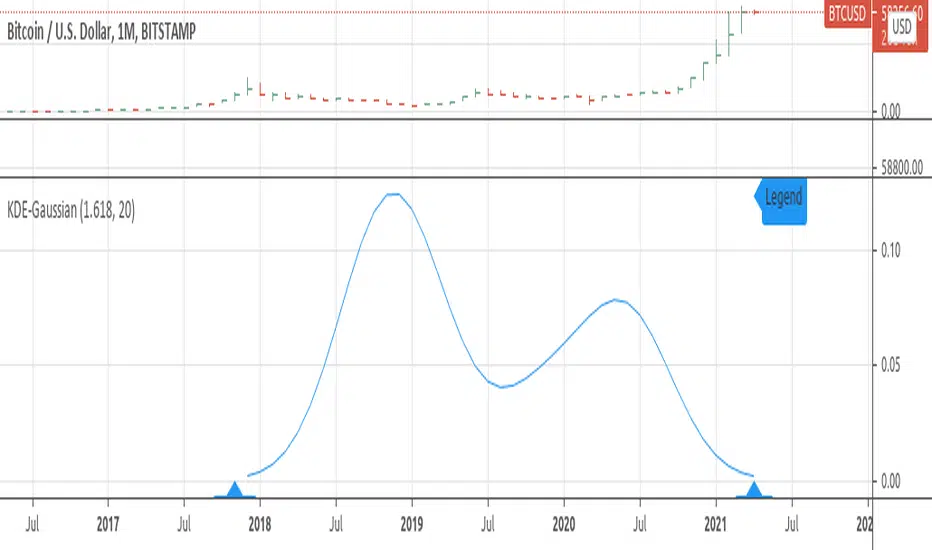

"In statistics, kernel density estimation (KDE) is a non-parametric way to estimate the probability density function of a random variable."

from wikipedia.com

from wikipedia.com

Release Notes

fixed a issue when using float type observations.added a draw function to draw the KDE graph(you need to see all the bar history to see it, doesnt work for float observations)

Release Notes

removed some redundant parameters, added bandwidth, nstep parameters, the graph looks stepd due to x axis havin interdigit floating numbers so it rounds to nearest causing that effect.Release Notes

improved the kde draw functionOpen-source script

In true TradingView spirit, the author of this script has published it open-source, so traders can understand and verify it. Cheers to the author! You may use it for free, but reuse of this code in publication is governed by House rules. You can favorite it to use it on a chart.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.