Distribution Position Size Panel

This panel is an example position size panel that I prepared and I consider the rates reasonable.

I have prepared this panel so that the money allocated to the investment ends 14 consecutive signals.

The sum of the ratios is 100 units.

You can adjust your positions according to this panel.

The first steps are low rates.

If the phrases are strong, you can specify a position size from the lower digits.

Likewise, when you make a big profit, you can empty your profits in the lower steps.

In the event of a color change, you can return to the beginning or lower limit.

NOTE: This script is an auxiliary command to the distribution blocks script,

if you want to use another script, you can add distribution days to yours.

14 th stake does not appear in the preview, you need to reduce the size of the distribution blocks indicator slightly.

Rafael Zioni's examples of the panels helped a lot, thanks to him.

Stay tuned ! Regards , Noldo.

Accumulation / Distribution Line (ADL)

Distribution BlocksThis idea has been created by the combination of the two existing systems as a result of my efforts to create a distributional buying and selling guide that has plagued my head for a long time.

1st idea is Accumulation / Distribution Line :

2nd idea is Distribution Day :

These two ideas, the intellectual assistance of professional brokers, and my observations of cot data played a role in the formation of this idea.

Let's start.

No matter how often we divide our risk, both our minds are not comfortable and our capital may end at any moment, and if we do not use professional systems, our chances of success are 50 percent.

If we take this system as an aid to our classic systems, we can determine the amount of risk with those predictions and gradually trade.

If we don't use leverage and we have a little predictive ability, our chances of success go above 50 percent.

But for the first time, we can keep our first lot very low and increase the number of positions in the same order of orders (example: buy and buy and buy).

If we keep the first amount low, the folds won't hurt us.

When we catch up with the trend, purchases with larger position sizes than lower prices lower our average price, so that we can make a good profit when the rising trend starts.

By accepting the zone changes as the reset point just like in the martingale system, we enter the folds in the new zone with our first lot weight.

Although we cannot catch the trend, we determine the stoploss level by adding the first point we entered or the first point we entered and the commission cost.

In fact, this method is the method of buying and selling very large traders and producers, banks, pro-brokers, hedge funds and in other words the new popular phrase "whales".

Because if he trades otherwise, he cannot find buyers because his goods are too big.

I like the comfort of mind in this way.

Finally, your methods separating the negative and positive regions (macd, rsi, interpretation observation etc.)

the stronger you are, the higher your success rate.

I think the Accumulation Distribution method is very successful, but it can be adjusted for the period.

I can't wait to integrate my relativity system on this.

And when my deep learning series is over, I will integrate them on ANN series and share them publicly.

To start with, I can say briefly.

If your capital is 100:

(first lot + (increase multiplier * first lot) + (increase multiplier * increase multiplier * first lot) + .....) = 100

I tell you that you can have the same position in this series 10 - 15 times,

this will help you decide how small a position size is to be used as the starting rate and choose a low increment multiplier!

I think that this idea cannot be converted into strategy, because when our expectations come true, we may want to free all positions and start again.And I think that's better.

And in sudden movements and developments we take action with different expectations.

I'm going to talk about this script's calculations and profits on educational ideas.

Regards , Noldo.

Volume Ticks - Increasing Volume Bar Count [LucF]Volume Ticks is a zero-lag market sentiment indicator. It works by providing a cumulative count of increasing volume columns.

A one count is added for each increasing volume column where close>open, and one is subtracted on an increasing volume column if close<open. That’s it. The count does not change when volume hasn’t increased compared to the previous bar’s volume, nor when price does not change. Price movement during the bar, whether 0.001% or 100%, is irrelevant to Volume Ticks; it only moves by 1 at a time.

Given that price is not used in Ticks, it is intriguing how well it tracks—or often leads—price movement. The fact that it doesn’t use price also makes it an ideal companion to most indicators that do use price, whether in momentum or mean-reversion based strategies.

As with my TLD indicator , the postulate behind Ticks is that price movement occurring on increasing volume is more significant than otherwise. In my opinion, the usefulness of Ticks tends to validate this.

Features

The averages can be turned on and off.

A long-term sentiment marker can be turned on.

Markers for BB exits and pause-reversals can be turned on, with the option of showing only long or short markers.

9 alerts can be defined on markers, with the option of choosing only long or short markers.

Use cases

Provides perspective when reading momentum indicators.

Helps identify false momentum tops or bottoms.

Comes in handy in detecting subtle sentiment in consolidations. Instances where slight price movement is accompanied by more important Ticks movements often predate more important price movements.

Helps detect exhaustion in trends.

Things to keep in mind

Volume Ticks show sentiment—not price nor trend. Because it so often mimics price, this is easy to forget.

Volume Ticks is not bound. Its position with regards to the zero line is not particularly useful either; position relative to and interplay between the MAs is much more useful.

Readings are more reliable with many data points. When used on monthly, weekly or daily charts, readings should be validated at shorter intervals. Over the same length of time, a compressed view of a shorter interval will usually provide more reliable readings than the longer interval view.

Being zero-lag, Ticks is inherently noisy. You will see this when using the Pause-Reversal markers.

The signal line will not move if no increasing volume is accompanying price movement, however important that movement may be.

Linear regressions are used in lieu of MAs, except the slow long MA (T5) which uses a simple moving average. The fast MA (T2) is double-smoothed.

Markers 2 are brighter when T3 and T4 are in the direction of the marker. The markers are not this indicator’s most useful feature.

Here is Ticks in action on a chart also using TLD:

Distribution Days-BuschiThis script is a simple extension of the script "Distribution Day" from user "kalle2017". Thanks to him!

As the name suggests, the idea is to recognize "distribution days", when the "firm hands sell to the shaky hands" (Kostolany). So, too many distribution days in a certain timeframe can be a sign for a coming correction / bear market.

A distribution day gets triggered when a loss compared on the day before exceeds 0.2 % and the trading volume is higher.

This indicator works on any daily chart symbol but should be primarily used on major indexes.

Possible inputs are "days back" to count how many trading should be examined(default: 25). Additionally, I implemented the possibility to draw a moving average (default: exponential, 50), to eliminate distribution days below, because it is more of an indicator for the upside. Perhaps a little bit too much / too complicated, therefore it is off by default.

IO_EMA_Delta_OscillatorThis is a EMA Delta Oscillator: An attempt to show ranging markets based on the slope of the EMA.

Green = Bullish Market

Blue = Ranging Market

Red = Bearish Market

The EMA Slope is normalized to make it work like an oscillator with values between 0 and 1.

Bar colors show the oscillator colors, bar borders show the actual candle colors.

- Invsto

(sarangab)

XBT Volatility Weighted Bottom Finder. [For Daily Charts]An update to:

Made it into and indicator.

v. 0.0.1

DESIGNED FOR DAILY CHARTS

Accumulation/Distribution Volume (ADV) [cI8DH]This is the simplified and optimized version of my original ADV indicator. It shows both regular volume bars and the accumulated/distributed (A/D) portion of them. The equation is elegant and intuitive. It calculates candle body to candle height ratio and multiplies it by volume: volume*(close-open)/(high-low). This is the building block of my three other indicators, ADL, ADP and ADMF.

- The volume bars has two shades of green and red. The dark shade shows amount of A/D and the light shade shows total volume (what you see on a regular volume indicator).

When money volume is enabled, volume is multiplied by price. As you can see in the chart below, trade volume in terms of USD was growing over the past years.

- Blue line is the moving average of A/D and the orange line is for total volume. When "Baseline Chart" option is enabled, this moving average is identical to ADMF indicator which can be a powerful indicator for assessing buy/sell pressure as well as money flow and volume divergences. You can turn off volume bars (from style menu) for better visibility or you can use the below indicators.

Please note that ADMF is now available as a part of ADP indicator as well and I recommend using the latter since ADP can also replace CMF and MFI indicators.

- If you change the aggregation to cumulative (while having money volume disabled), the gray line becomes identical to On Balance Volume (OBV) and the blue line identical to my ADL indicator. The latter I would argue is more accurate than Chaikin's ADL, William's A/D and OBV.

Accumulation/Distribution Level (ADL) [Cyrus c|:D]This indicator shows Accumulation/Distribution level which can be used for confirming trends or reversals (via divergence). It is an alternative to Chaikin's Accumulation/Distribution Line (ADL) and On Balance Volume (OBV) indicators. It can also replicate PVT and OBV via options in the input menu.

Here is a comparison of four related indicators:

OBV is too simple and has serious flaws as explained in PVT's wiki.

Chaikin's ADL is a broken indicator as can be seen in the chart below:

A/D Level addresses the flaws in these two indicators. It simply sums up portions of the volume that contributes to price change. These portions are visualized in dark green and red on "Accumulation/Distribution Volume (ADV)" indicator. This can also be achieved by ADV indicator if you are nerd enough.

PS: There is Williams A/D as well which is also a broken indicator.

Accumulation/Distribution VolumeThis is a simple yet powerful indicator that can replace volume, Money Flow, Chaikin Money Flow, Price Volume Trend (PVT), Accumulation/Distribution Line (ADL), On Balance Volume (OBV).

When "Baseline Chart" option is disabled, it looks similar to regular volume. The volume bars has two shades of green and red. The dark shade shows amount of accumulation and the light shade shows total volume (what you see on a regular volume indicator). Blue line is the moving average (or cumulative total) of A/D and the gray line is for total volume.

When money volume is enabled, volume it multiplied by price. As you can see in the chart below, trade volume in terms of USD was declining after ATH. This is not the case in regular volume chart which shows instrument volume (chart above).

In Baseline view, the aggregation method you choose can turn it into different indicators. With EMA/SMA aggregation, blue and gray line shows buy/sell pressure. At 0, there is not buy or sell pressure.

If you turn off volume bars (from style menu), it gives you a reliable indicator to measure divergence. This should be more reliable than most other range-bound indicators (i.e. RSI, MFI, CMF). I will publish a TA about correctly measuring divergence (it's a must read even if you are a pro trader). Make sure that the length is set to a large number on smaller TFs such as 4h.

For following results, set aggregation to cumulative and turn off money volume:

When wick weight=0, the GRAY line is identical to OBV indicator.

When normalized by spread and wick weight=10, the BLUE line is identical to ADL (improved by true range).

When normalized by previous bar price, wick weight=0, the BLUE line is identical to PVT.

How I use this indicator:

- Baseline chart, replaced my regular volume indicator

- Mostly 4h TF for divergence

- EMA aggregation (and occasional cumulative aggregation) with length above 50. I change the length to 100 and 200 for confirmation.

- Wick weight=0 or max 2.

With this indicator, you can learn how different indicators are built and how they are different from each other. I will publish a TA to explain more about different indicators and their pros and cons.

I will publish this indicator without volume bars and additional options to make it range bound.

Weis Wave ChartThis indicator is based on the Weis Wave described by David H. Weis in his book Trades About to Happen: A Modern Adaptation of the Wyckoff Method, more info how to use this indicator can be found in this video . The Weis Wave is an adaptation of Richard D. Wyckoff’s method Wave Charts. It works in all time periods and can be applied to all asset types.

Unlike other implementations I found here on TradingView, this implementation make use of a Renko-like zig zag pattern, very similar to how it is described in David H. Weis' book. The settings for the zig zag pattern are very similar to the standard Renko settings here on TradingView, in the "Renko Assignment Method" you either chose "ATR" or "Traditional" (read more about it here ). The ATR length or the brick size is then entered in the textbox "Value". You can also chose another setting in the "Renko Assignment Method" drop down named "Part of Price" which calculate the brick size from the current close and divide it by the value in the text box "Value". It is also possible to chose if the zig zag pattern shall use the high/low, the open/close or just the close as the most extreme values in its calculation, you select this in the drop down "Price Source".

TradingView's pine script does currently not support to print non-static text on the chart, so it is not possible at this point to write out the volume on the zig zag chart. It is also not possible to have both an overlay and separate chart pane in the same indicator, therefor this indicator is split up in two.

You can find the volume indicator here:

Weis Wave VolumeThis indicator is based on the Weis Wave described by David H. Weis in his book Trades About to Happen: A Modern Adaptation of the Wyckoff Method, more info how to use this indicator can also be found in this video . The Weis Wave is an adaptation of Richard D. Wyckoff’s method Wave Charts. It works in all time periods and can be applied to all asset types. For assets that do not support volume Weis propose in his book to use the true range instead, so if you want to use this indicator for assets that do not support volume, make sure to enable the checkbox "Use True Range instead of Volume".

Unlike other implementations I found here on Trading, this implementation make use of a Renko-like zig zag pattern, very similar to how it is described in David H. Weis' book. The settings for the zig zag pattern are very similar to the standard Renko settings here on TradingView, in the "Renko Assignment Method" you either chose "ATR" or "Traditional" (read more about it here ). The ATR length or the brick size is then entered in the textbox "Value". You can also chose another setting in the "Renko Assignment Method" drop down named "Part of Price" which calculate the brick size from the current close and divide it by the value in the text box "Value". It is also possible to chose if the zig zag pattern shall use the high/low, the open/close or just the close as the most extreme values in its calculation, you select this in the drop down "Price Source". If you want the price to oscillate around a zero value, enable the "Oscillating" checkbox.

TradingView's pine script does currently not support to print non-static text on the chart, so it is not possible at this point to write out the volume on the zig zag chart. It is also not possible to have both an overlay and separate chart pane in the same indicator, therefor this indicator is split up in two.

You can find the zig zag indicator here:

Twiggs-ss

The modified indicator money flow Chaikin -LasyBear. Drastically accumulation and a sharp distribution of the painted color

OBV Accumulation / Distribution combination v2OBV takes difference between old close and new close and multiplies by volume without considering high and low.

This assigns the entire volume into a single direction even tho movement could've been in both.

Accum/dist takes difference between close and high and low without considering previous close or open. This causes huge deviation from OBV when you have close or open far from high or low and price moving in the other direction like in a series of descending hammers.

This is attempt to combine both so relative motion between candles is detected and volume direction is assigned based relative to movement within a candle to account for volume in both directions.

+ and - depends if close is above previous close (+ if above, - if below)

Maximum upward volume counts if close = high and previous close = low, this makes multiplier 1 and thus entire volume is counted upwards

Maximum downward volume counts if close = low and previous close = high, this makes multiplier -1 and thus entire volume is counted downwards.

Zero volume movement occurs when close = previous close.

Half upward volume movement occurs if close-previous_close is half the range from high-low.

Update:

Open used instead of previous close due to issues with grabbing previous close on some charts. This seems more accurate for gaps without volume.

OBV Accumulation/Distribution combinationOBV takes difference between old close and new close and multiplies by volume without considering high and low.

This assigns the entire volume into a single direction even tho movement could've been in both.

Accum/dist takes difference between close and high and low without considering previous close or open. This causes huge deviation from OBV when you have close or open far from high or low and price moving in the other direction like in a series of descending hammers.

This is attempt to combine both so relative motion between candles is detected and volume direction is assigned based relative to movement within a candle to account for volume in both directions.

+ and - depends if close is above previous close (+ if above, - if below)

Maximum upward volume counts if close = high and previous close = low, this makes multiplier 1 and thus entire volume is counted upwards

Maximum downward volume counts if close = low and previous close = high, this makes multiplier -1 and thus entire volume is counted downwards.

Zero volume movement occurs when close = previous close.

Half upward volume movement occurs if close-previous_close is half the range from high-low.

Accumulation/Distribution MACDMACD of acc/dist instead of the normal stuff.

Dunno if it's actually useful.

Just wanted to see what happened.

Thanks to ChrisMoody who's macd script I stole

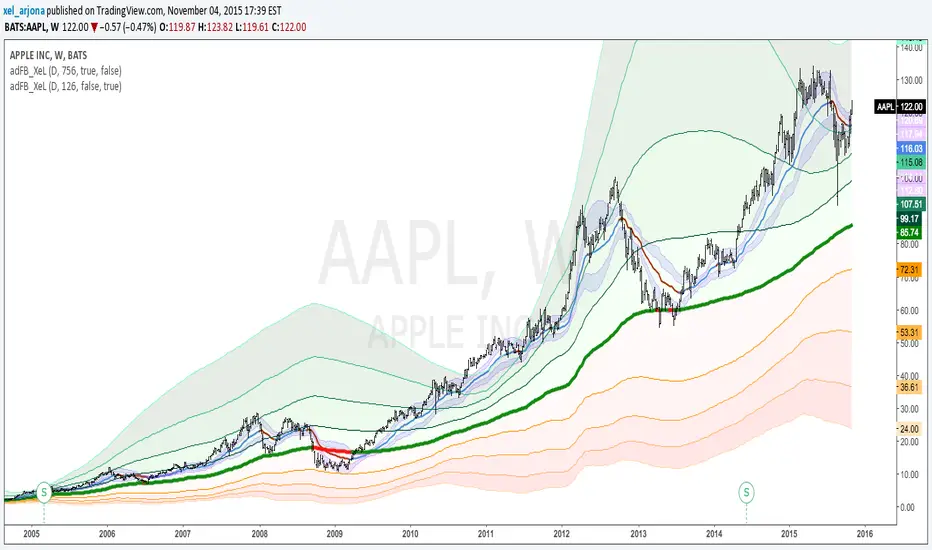

EVWMA Acc/Dist. Pressure & FRACTAL BANDS by @XeL_ArjonaEVWMA ACCUMULATION/DISTRIBUTION PRESSURE & FRACTAL BANDS

Version: 3.0 @ 4.11.2015

By Ricardo M Arjona @XeL_Arjona

DISCLAIMER:

The following indicator IS NOT INTENDED TO BE A FORMAL INVESTMENT ADVICE OR TRADING RECOMMENDATION BY THE AUTHOR, nor should be construed as such. Users will be fully responsible by their use regarding any kind of trading vehicles or assets.

The following script and ideas within this work are FREELY AND PUBLICLY availables on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

-== IMPORTANT: THIS IS AN EXPERIMENTAL INDICATOR ==-

What is this?

This work is a derivation of my previous Accumulation/Distribution scripts publicly available in TradingView in an effort to clean, speedup and make the indicator cleaner as possible.

The current indicator is based on already tested and Mathematically proof concepts as described below:

The MAIN Rolling back median line or "Vortex" is constructed by a simple and equal weighting of distributed volume along the candle range (This approach is just an "estimator" of Buyers Vs. Sellers given the lack of tick resolution in TradingView, a real "DELTA" can only be 100% reliable with Market Depth (Ask/Bid ticks)), Given this, with each "volume weights", the price is post-processed against a true statistical Average calculation formerly: ELASTIC VOLUME WEIGHTED MOVING AVERAGE.

The FRACTAL BANDS are just Standard Deviation's with GOLDEN RATIO as multiplier (1.618) derived one from each other within it's origin on the former "Vortex Median".

The Standard Error Bands comply as the original indicator described by Jon Andersen but given the true statistical nature of EVWMA, the original LinReg line has been substituted by the former.

ALL NEW IDEAS OR MODIFICATIONS to this indicator are welcome in favor to deploy a better technical tool. Any important addition to this work MUST REMAIN PUBLIC by means of CreativeCommons CC & TradingView user rules. (C) 2015 @XeL_Arjona

Mr.J -- Accumulation Distribution OscillatorEdit: More examples in comments, TV doesn't like to publish with split charts ;)

As a popular volume indicator, Accumulation Distribution Oscillator makes it easy and simple to interpret amplitude changes in the accumulation distribution. Either an observed peak in positive or negative amplitude can be used to snipe high/low points or a crossover from a positive number to a negative amplitude can indicate the change of Accumulation to Distribution.

Hidden divergences can also be found by looking for differences in the price/volume amplitude, similar to OBV divergence rules.

Accumulation/Distribution With Moving AveragesHelps To Identify the Underlying Trend of Buying & Selling Forces.

Accumulation/Distribution with Moving AveragesThis Acc/Dist Script Lends a Broader Perspective to the Trend of the Indicator . It can be used to compare with the Trend of the Market to Identify Reversals & Confirm Market Trends !