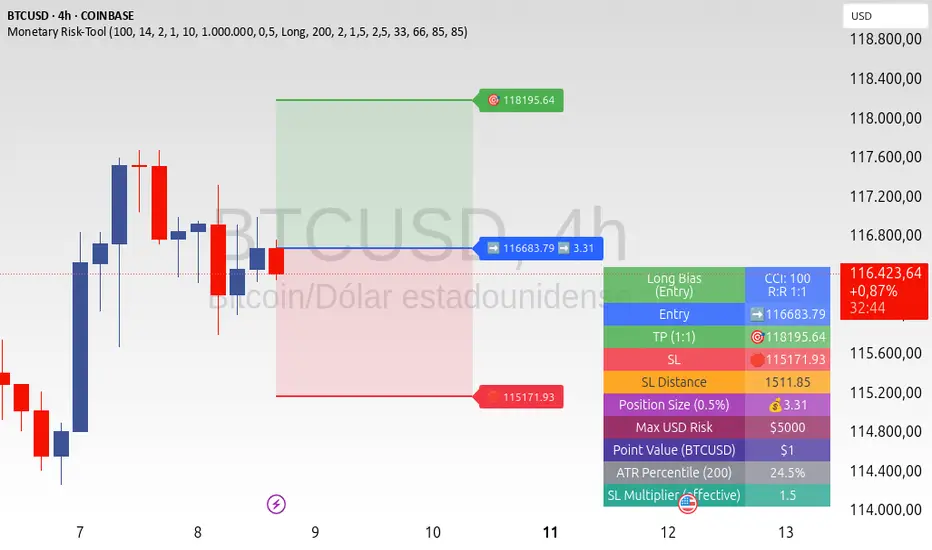

ATR+CCI Monetary Risk Tool - TP/SL⚙️ ATR+CCI Monetary Risk Tool — Volatility-aware TP/SL & Position Sizing

Exact prices (no rounding), ATR-percentile dynamic stops, and risk-budget sizing for consistent execution.

🧠 What this indicator is

A risk-first planning tool. It doesn’t generate orders; it gives you clean, objective levels (Entry, SL, TP) and position size derived from your risk budget. It shows only the latest setup to keep charts readable, and a compact on-chart table summarizing the numbers you actually act on.

✨ What makes it different

Dynamic SL by regime (ATR percentile): Instead of a fixed multiple, the SL multiplier adapts to the current volatility percentile (low / medium / high). That helps avoid tight stops in noisy markets and over-wide stops in quiet markets.

Risk budgeting, not guesswork: Size is computed from Account Balance × Max Risk % divided by SL distance × point value. You risk the same dollars across assets/timeframes.

Precision that matches your instrument: Entry, TP, SL, and SL Distance are displayed as exact prices (no rounding), truncated to syminfo.mintick so they align with broker/exchange precision.

Symbol-aware point value: Uses syminfo.pointvalue so you don’t maintain tick tables.

Non-repaint option: Work from closed bars to keep the plan stable.

🔧 How to use (quick start)

Add to chart and pick your timeframe and symbol.

In settings:

Set Account Balance (USD) and Max Risk per Trade (%).

Choose R:R (1:1 … 1:5).

Pick ATR Period and CCI Period (defaults are sensible).

Keep Dynamic ATR ON to adapt SL by regime.

Keep Use closed-bar values ON to avoid repaint when planning.

Read the labels (Entry/TP/SL) and the table (SL Distance, Position Size, Max USD Risk, ATR Percentile, effective SL Mult).

Combine with your entry trigger (price action, levels, momentum, etc.). This indicator handles risk & targets.

📐 How levels are computed

Bias: CCI ≥ 0 ⇒ long, otherwise short.

ATR Percentile: Percent rank of ATR(atrPeriod) over a lookback window.

Effective SL Mult:

If percentile < Low threshold ⇒ use Low SL Mult (tighter).

If between thresholds ⇒ use Base SL Mult.

If percentile > High threshold ⇒ use High SL Mult (wider).

Stop-Loss: SL = Entry ± ATR × SL_Mult (minus for long, plus for short).

Take-Profit: TP = Entry ± (Entry − SL) × R (R from the R:R dropdown).

Position Size:

USD Risk = Balance × Risk%

Contracts = USD Risk ÷ (|Entry − SL| × PointValue)

For futures, quantity is floored to whole contracts.

Exact prices: Entry/TP/SL and SL Distance are not rounded; they’re truncated to mintick so what you see matches valid price increments.

📊 What you’ll see on chart

Latest Entry (blue), TP (green), SL (red) with labels (optional emojis: ➡️ 🎯 🛑).

Info Table with:

Bias, Entry, TP, SL (exact, truncated to mintick)

SL Distance (exact, truncated)

Position Size (contracts/units)

Max USD Risk

Point Value

ATR Percentile and effective SL Mult

🧪 Practical examples

High-volatility session (e.g., XAUUSD, 1H): ATR percentile is high ⇒ wider SL, smaller size. Reduces churn from normal noise during macro events.

Range-bound market (e.g., EURUSD, 4H): ATR percentile low ⇒ tighter SL, better R:R. Helps you avoid carrying unnecessary risk.

Index swing planning (e.g., ES1!, Daily): Non-repaint levels + risk budgeting = consistent sizing across days/weeks, easier to review and journal.

🧭 Why traders should use it

Consistency: Same dollar risk regardless of instrument or volatility regime.

Clarity: One-trade view forces focus; you see the numbers that matter.

Adaptivity: Stops calibrated to the market’s current behavior, not last month’s.

Discipline: A visible checklist (SL distance, size, USD risk) before you hit buy/sell.

🔧 Input guide (practical defaults)

CCI Period: 100 by default; use as a bias filter, not an entry signal.

ATR Period: 14 by default; raise for smoother, lower for more reactive.

ATR Percentile Lookback: 200 by default (stable regime detection).

Percentile thresholds: 33/66 by default; widen the gap to change how often regimes switch.

SL Mults: Start ~1.5 / 2.0 / 2.5 (low/base/high). Tune by asset.

Risk % per trade: Common pro ranges are 0.25–1.0%; adjust to your risk tolerance.

R:R: Start with 1:2 or 1:3 for balanced skew; adapt to strategy edge.

Closed-bar values: Keep ON for planning/live; turn OFF only for exploration.

💡 Best practices

Combine with your entry logic (structure, momentum, liquidity levels).

Review ATR percentile and effective SL Mult across sessions so you understand regime shifts.

For futures, remember size is floored to whole contracts—safer by design.

Journal trades with the table snapshot to improve risk discipline over time.

⚠️ Notes & limitations

This is not a strategy; it does not place orders or alerts.

No slippage/commissions modeled here; build a strategy() version for backtests that mirror your broker/exchange.

Displayed non-price metrics use two decimals; prices and SL Distance are exact (truncated to mintick).

📎 Disclaimer

For educational purposes only. Not financial advice. Markets involve risk. Test thoroughly before trading live.

ATR

Mutanabby_AI | Ultimate Algo | Remastered+Overview

The Mutanabby_AI Ultimate Algo Remastered+ represents a sophisticated trend-following system that combines Supertrend analysis with multiple moving average confirmations. This comprehensive indicator is designed specifically for identifying high-probability trend continuation and reversal opportunities across various market conditions.

Core Algorithm Components

**Supertrend Foundation**: The primary signal generation relies on a customizable Supertrend indicator with adjustable sensitivity (1-20 range). This adaptive trend-following tool uses Average True Range calculations to establish dynamic support and resistance levels that respond to market volatility.

**SMA Confirmation Matrix**: Multiple Simple Moving Averages (SMA 4, 5, 9, 13) provide layered confirmation for signal strength. The algorithm distinguishes between regular signals and "Strong" signals based on SMA 4 vs SMA 5 relationship, offering traders different conviction levels for position sizing.

**Trend Ribbon Visualization**: SMA 21 and SMA 34 create a visual trend ribbon that changes color based on their relationship. Green ribbon indicates bullish momentum while red signals bearish conditions, providing immediate visual trend context.

**RSI-Based Candle Coloring**: Advanced 61-tier RSI system colors candles with gradient precision from deep red (RSI ≤20) through purple transitions to bright green (RSI ≥79). This visual enhancement helps traders instantly assess momentum strength and overbought/oversold conditions.

Signal Generation Logic

**Buy Signal Criteria**:

- Price crosses above Supertrend line

- Close price must be above SMA 9 (trend confirmation)

- Signal strength determined by SMA 4 vs SMA 5 relationship

- "Strong Buy" when SMA 4 ≥ SMA 5

- Regular "Buy" when SMA 4 < SMA 5

**Sell Signal Criteria**:

- Price crosses below Supertrend line

- Close price must be below SMA 9 (trend confirmation)

- Signal strength based on SMA relationship

- "Strong Sell" when SMA 4 ≤ SMA 5

- Regular "Sell" when SMA 4 > SMA 5

Advanced Risk Management System

**Automated TP/SL Calculation**: The indicator automatically calculates stop loss and take profit levels using ATR-based measurements. Risk percentage and ATR length are fully customizable, allowing traders to adapt to different market conditions and personal risk tolerance.

**Multiple Take Profit Targets**:

- 1:1 Risk-Reward ratio for conservative profit taking

- 2:1 Risk-Reward for balanced trade management

- 3:1 Risk-Reward for maximum profit potential

**Visual Risk Display**: All risk management levels appear as both labels and optional trend lines on the chart. Customizable line styles (solid, dashed, dotted) and positioning ensure clear visualization without chart clutter.

**Dynamic Level Updates**: Risk levels automatically recalculate with each new signal, maintaining current market relevance throughout position lifecycles.

Visual Enhancement Features

**Customizable Display Options**: Toggle trend ribbon, TP/SL levels, and risk lines independently. Decimal precision adjustments (1-8 decimal places) accommodate different instrument price formats and personal preferences.

**Professional Label System**: Clean, informative labels show entry points, stop losses, and take profit targets with precise price levels. Labels automatically position themselves for optimal chart readability.

**Color-Coded Momentum**: The gradient RSI candle coloring system provides instant visual feedback on momentum strength, helping traders assess market energy and potential reversal zones.

Implementation Strategy

**Timeframe Optimization**: The algorithm performs effectively across multiple timeframes, with higher timeframes (4H, Daily) providing more reliable signals for swing trading. Lower timeframes work well for day trading with appropriate risk adjustments.

**Sensitivity Adjustment**: Lower sensitivity values (1-5) generate fewer but higher-quality signals, ideal for conservative approaches. Higher sensitivity (15-20) increases signal frequency for active trading styles.

**Risk Management Integration**: Use the automated risk calculations as baseline parameters, adjusting risk percentage based on account size and market conditions. The 1:1, 2:1, 3:1 targets enable systematic profit-taking strategies.

Market Application

**Trend Following Excellence**: Primary strength lies in capturing significant trend movements through the Supertrend foundation with SMA confirmation. The dual-layer approach reduces false signals common in single-indicator systems.

**Momentum Assessment**: RSI-based candle coloring provides immediate momentum context, helping traders assess signal strength and potential continuation probability.

**Range Detection**: The trend ribbon helps identify ranging conditions when SMA 21 and SMA 34 converge, alerting traders to potential breakout opportunities.

Performance Optimization

**Signal Quality**: The requirement for both Supertrend crossover AND SMA 9 confirmation significantly improves signal reliability compared to basic trend-following approaches.

**Visual Clarity**: The comprehensive visual system enables rapid market assessment without complex calculations, ideal for traders managing multiple instruments.

**Adaptability**: Extensive customization options allow fine-tuning for specific markets, trading styles, and risk preferences while maintaining the core algorithm integrity.

## Non-Repainting Design

**Educational Note**: This indicator uses standard TradingView functions (Supertrend, SMA, RSI) with normal behavior patterns. Real-time updates on current candles are expected and standard across all technical indicators. Historical signals on closed candles remain fixed and unchanged, ensuring reliable backtesting and analysis.

**Signal Confirmation**: Final signals are confirmed only when candles close, following standard technical analysis principles. The algorithm provides clear distinction between developing signals and confirmed entries.

Technical Specifications

**Supertrend Parameters**: Default sensitivity of 4 with ATR length of 11 provides balanced signal generation. Sensitivity range from 1-20 allows adaptation to different market volatilities and trading preferences.

**Moving Average Configuration**: SMA periods of 8, 9, and 13 create multi-layered trend confirmation, while SMA 21 and 34 form the visual trend ribbon for broader market context.

**Risk Management**: ATR-based calculations with customizable risk percentage ensure dynamic adaptation to market volatility while maintaining consistent risk exposure principles.

Recommended Settings

**Conservative Approach**: Sensitivity 4-5, RSI length 14, higher timeframes (4H, Daily) for swing trading with maximum signal reliability.

**Active Trading**: Sensitivity 6-8, RSI length 8-10, intermediate timeframes (1H) for balanced signal frequency and quality.

**Scalping Setup**: Sensitivity 10-15, RSI length 5-8, lower timeframes (15-30min) with enhanced risk management protocols.

## Conclusion

The Mutanabby_AI Ultimate Algo Remastered+ combines proven trend-following principles with modern visual enhancements and comprehensive risk management. The algorithm's strength lies in its multi-layered confirmation approach and automated risk calculations, providing both novice and experienced traders with clear signals and systematic trade management.

Success with this system requires understanding the relationship between signal strength indicators and adapting sensitivity settings to match current market conditions. The comprehensive visual feedback system enables rapid decision-making while the automated risk management ensures consistent trade parameters.

Practice with different sensitivity settings and timeframes to optimize performance for your specific trading style and risk tolerance. The algorithm's systematic approach provides an excellent framework for disciplined trend-following strategies across various market environments.

TSD Quantum [Moeinudin Montazerfaraj] 🔸 "TSD" stands for **Trend 1-2-3 and Supply & Demand**, which is the foundation of the trading style this indicator is built upon.

🔹 TSD Quantum is a specialized indicator designed exclusively for day traders who trade EURUSD, XAUUSD (Gold), and DAX40 on the 1H, 15M, and 5M timeframes using a Supply & Demand-based strategy.

This indicator is **not suitable for other symbols** and has been tailored specifically for these three assets to ensure high precision and effectiveness.

---

### 🔍 Key Features:

✅ **Trading Checklist Panel**

A built-in checklist helps you track every rule in your trading plan. If even one condition is left unchecked, the system highlights it in red and marks the trade as "Not Allowed." This feature enhances trading discipline.

✅ **Spread & ATR Control Panel**

Supports both auto-calculated and fixed values for spread and ATR. This is especially helpful when placing stop-losses quickly and accurately.

✅ **Inside & Outside Candle Detection**

A dedicated panel highlights whether the last candle is inside or outside. Hovering your mouse over the chart elements automatically colorizes the candles:

🔵 Blue = Outside candle

🔴 Red = Inside candle

Also displays the high/low of the latest outside bar.

✅ **Weekly Trade Stats Panel**

Custom-built for the mentioned three assets. You can enter your trades using either fixed risk or floating risk models.

✅ **Performance Metrics**

Helps you build and adjust a floating risk model—so you don’t have to enter every trade with the same lot size. Improves risk management across multiple trades.

✅ **Base Candles Display**

Grey and white base candles are marked based on supply and demand zones.

✅ **EOT Candles**

Candles with a green dot underneath indicate valid EOT opportunities for potential move-outs.

✅ **RC (Rejection Candle) Detection**

RC candles are automatically detected to alert you of potential traps or weaknesses during Supply/Demand formations.

---

### ⚠️ Disclaimer

This indicator does **not** issue buy/sell signals and **cannot guarantee profit or prevent loss**. It is a **tool for discretionary trading**, not an automated expert advisor.

All decisions must be made by the trader based on their own strategy and risk tolerance.

This is the **latest tested version** of TSD Quantum. All features have been validated and function as intended. Future updates will be provided if needed.

---

🙏 Thank you for reviewing this script. We hope it becomes a valuable addition to your day trading toolkit!

Fibonacci-Based Volume Flow (VFI)Fibonacci-based Volume Flow is an advanced next-generation evolution of LazyBear’s original VFI script that calculates and averages up to 21 Fibonacci-based VFI pairings to create a smoothed composite volume flow signal. This unique and powerful approach reduces noise, adapts to volatility, and provides a clearer view of trend strength and market structure across all timeframes. It also includes dynamic fibonacci guide levels, adaptive lookbacks, EMA crossovers, and structure-aware pivot labeling to help traders identify high-quality reversals, confirm directional bias, and detect divergences with greater precision. It's ideal for traders looking to enhance momentum analysis through volume-based confirmation.

🧠 Key Features🧠

🔹 Multi-VFI Fibonacci Fusion🔹

Blends up to 21 VFI signals (5, 13, 21, 34… up to 610) into smartly paired averages (e.g., 13/34, 55/144) — forming a smoothed composite VFI that’s more adaptive, less noisy, and highly responsive across market conditions.

🔸🔸 Dynamic Lookbacks🔸 🔸

Automatically adjusts histogram high/low tracking based on your chart’s timeframe — no more static tuning. Perfect for scalping fast charts or confirming long-term trends.

🟥🟩 Color-Coded Histogram🟥🟩

Visualizes VFI momentum with gradient coloring.

🧩🧩 Signal Crossovers 🧩🧩

Color-coded crossover lines persistently show bullish or bearish dominance.

Includes three powerful crossover systems:

➖5/13 VFI: Fast, early reversal detection

➖8/21 VFI: Swing-trading sweet spot

➖55/144 VFI: Trend confirmation across long cycles

🏷️ 🏷️Pivot Structure Labels🏷️🏷️

Labels oscillator swings with full structural logic:

➖HH, HL, LH, LL, EQ

➖Displays percent change, price at pivot, oscillator reading

➖Smart coloring detects divergence & trend continuation

📈 📈Dynamic Histogram Guides📈📈

Optional zero and ±50% bands anchor histogram levels based on real histogram extremes, not static thresholds — visually frame momentum shifts with context.

📍 📍Persistent High/Low Pivot Lines📍📍

Track the most significant histogram pivots (not price) across time, with smart labels:

➖Volume flow structure zones

➖Label shows price at pivot, oscillator level, and bars since event

➖Ideal for spotting divergence zones, momentum failures, and trend exhaustion.

🔍 🔍Volatility Table (ATR%)🔍🔍

💡Shows real-time volatility compression or expansion

💡Uses multiple ATR periods (e.g., 14 & 55) for short- and medium-term comparison

💡Helps traders understand whether momentum is likely to continue or stall

🔩🔩Volume-weighted VFI baselines🔩🔩

🟢A daily session-based VWAP of the VFI, which resets each day and highlights intraday volume flow context.

🟠A rolling VWA of VFI, which acts like a VWMA over a fixed window (e.g., 55 bars), smoothing short-term fluctuations and supporting trend/momentum confirmation.

These VWAP-style overlays help traders identify strength vs. weakness relative to volume-weighted baselines — useful for divergence spotting, mean reversion setups, or breakout confirmation.

🧰 🧰Under the Hood: How It Works🧰🧰

🔧 Core VFI Logic

Based on LazyBear’s foundational VFI:

➖Uses log returns of price (HLC3)

➖Filters insignificant moves using volatility-weighted thresholds

➖Normalizes volume via adaptive capping (e.g., 2.5× average)

🌀 Composite Blend System

Each VFI instance is smoothed and then fused via user-selectable pairs. This creates a customizable average VFI representing short, mid, and long-term pressure — one value, many time horizons.

📊 EMA Signal Layer

Crosses trigger persistent color shifts in signal lines, making trend strength clear at a glance.

VFI blend feeds into EMA crossovers. You can toggle visibility for:

➖Fast (5/13)

➖Medium (8/21)

➖Slow (55/144)

🧭 Pivot Framework

Structure logic only compares pivots on same-side polarity:

➖Highs compare to highs above zero

➖Lows compare to lows below zero

This avoids nonsensical comparisons and preserves logical sequences (HH → LH → HL).

🧱 Dynamic Labels

All pivots and persistent levels display:

➖Oscillator value

➖Price value

➖Structure tag (e.g., LH, HL)

➖% change from prior pivot

➖Lookback info

➖Bar age

Unlike traditional VFI:

✅ It blends timeframes with Fibonacci precision

✅ Uses dynamic, volatility-aware logic

✅ Embeds visual structure & divergence intelligence

✅ Enhances entry confidence and exit timing

🔧 This isn’t just an indicator — it’s a volume-informed decision engine.

Ideal For:

🔶Trend-followers wanting cleaner volume-based confirmation

🔶Reversal traders spotting structure + divergence

🔶Scalpers or investors needing adaptable signals

🔶Those who loved LazyBear's VFI

📌 Final Note:

As powerful as Fibonacci Blended Volume Flow is, no single indicator should be used in isolation. For best results, combine it with price action analysis, higher-timeframe context, and complementary tools like trendlines, moving averages, or support/resistance levels. Use it as part of a well-rounded trading approach to confirm setups — not to define them alone.

Trend Strength Index [Alpha Extract]The Trend Strength Index leverages Volume Weighted Moving Average (VWMA) and Average True Range (ATR) to quantify trend intensity in cryptocurrency markets, particularly Bitcoin. The combination of VWMA and ATR is particularly powerful because VWMA provides a more accurate representation of the market's true average price by weighting periods of higher trading volume more heavily—capturing genuine momentum driven by increased participation rather than treating all price action equally, which is crucial in volatile assets like Bitcoin where volume spikes often signal institutional interest or market shifts.

Meanwhile, ATR normalizes this measurement for volatility, ensuring that trend strength readings remain comparable across different market conditions; without ATR's adjustment, raw price deviations from the mean could appear artificially inflated during high-volatility periods (like during news events or liquidations) or understated in low-volatility sideways markets, leading to misleading signals. Together, they create a volatility-adjusted, volume-sensitive metric that reliably distinguishes between meaningful trend developments and noise.

This indicator measures the normalized distance between price and its volume-weighted mean, providing a clear visualization of trend strength while accounting for market volatility. It helps traders identify periods of strong directional movement versus consolidation, with color-coded gradients for intuitive interpretation.

🔶 CALCULATION

The indicator processes price data through these analytical stages:

Volume Weighted Moving Average: Computes a smoothed average weighted by trading volume

Volatility Normalization: Uses ATR to account for market volatility

Distance Measurement: Calculates absolute deviation between current price and VWMA

Strength Normalization: Divides price deviation by ATR for a volatility-adjusted metric

Formula:

VWMA = Volume-Weighted Moving Average of Close over specified length

ATR = Average True Range over specified length

Price Distance = |Close - VWMA|

Trend Strength = Price Distance / ATR

🔶 DETAILS Visual Features:

VWMA Line: Blue line overlay on the price chart representing the volume-weighted mean

Trend Strength Area: Histogram-style area plot with dynamic color gradient (red for weak trends, transitioning through orange and yellow to green for strong trends)

Threshold Line: Horizontal red line at the customizable Trend Enter level

Background Highlight: Subtle green background when trend strength exceeds the enter threshold for strong trend visualization

Alert System: Triggers notifications for strong trend detection

Interpretation:

0-Weak (Red): Minimal trend strength, potential consolidation or ranging market

Mid-Range (Orange/Yellow): Building momentum, watch for breakout potential

At/Above Enter Threshold (Green): Strong trend conditions, potential for continued directional moves

Threshold Crossing: Trend strength crossing above the enter level signals increasing conviction in the current direction

Color Transitions: Gradual shifts from warm (red/orange) to cool (green) tones indicate strengthening trends

🔶 EXAMPLES

Strong Trend Entry: When trend strength crosses above the enter threshold (e.g., 1.2), it identifies the onset of a powerful move where price deviates significantly from the mean.

Example: During a rally, trend strength rising from yellow (around 1.0) to green (1.2+) often precedes sustained upward momentum, providing entry opportunities for trend followers.

Consolidation Detection: Low trend strength values in red shades (below 0.5) highlight periods of low volatility and mean reversion potential.

Example: After a sharp sell-off, persistent red values signal a likely sideways phase, allowing traders to avoid whipsaws and wait for orange/yellow transitions as a precursor to recovery.

Volatility-Adjusted Pullbacks: In volatile markets, the ATR component ensures trend strength remains accurate; a dip back to yellow from green during minor corrections can indicate healthy pullbacks within a strong trend.

Example: Trend strength briefly falling to yellow levels (e.g., 0.8-1.1) after hitting green provides profit-taking signals without invalidating the overall bullish bias if the VWMA holds as support.

Threshold Alert Integration: The alert condition combines strength value with the enter threshold for timely notifications.

Example: Receiving a "Strong Trend Detected" alert when the area plot turns green helps confirm Bitcoin's breakout from consolidation, aligning with increased volume for higher-probability trades.

🔶 SETTINGS

Customization Options:

Lengths: VWMA length (default 14), ATR length (default 14)

Thresholds: Trend enter (default 1.2, step 0.1), trend exit (default 1.15, for potential future signal enhancements)

Visuals: Automatic color scaling with red at 0, transitioning to green at/above enter threshold

Alert Conditions: Strong trend detection (when strength > enter)

The Trend Strength Index equips traders with a robust, easy-to-interpret tool for gauging trend intensity in volatile markets like Bitcoin. By normalizing price deviations against volatility, it delivers reliable signals for identifying high-momentum opportunities while the gradient coloring and alerts facilitate quick assessments in both trending and choppy conditions.

Time-Price Velocity [QuantAlgo]🟢 Overview

The Time-Price Velocity indicator uses advanced velocity-based analysis to measure the rate of price change normalized against typical market movement, creating a dynamic momentum oscillator that identifies market acceleration patterns and momentum shifts. Unlike traditional momentum indicators that focus solely on price change magnitude, this indicator incorporates time-weighted displacement calculations and ATR normalization to create a sophisticated velocity measurement system that adapts to varying market volatility conditions.

This indicator displays a velocity signal line that oscillates around zero, with positive values indicating upward price velocity and negative values indicating downward price velocity. The signal incorporates acceleration background columns and statistical normalization to help traders identify momentum shifts and potential reversal or continuation opportunities across different timeframes and asset classes.

🟢 How It Works

The indicator's key insight lies in its time-price velocity calculation system, where velocity is measured using the fundamental physics formula:

velocity = priceChange / timeWeight

The system normalizes this raw velocity against typical price movement using Average True Range (ATR) to create market-adjusted readings:

normalizedVelocity = typicalMove > 0 ? velocity / typicalMove : 0

where "typicalMove = ta.atr(lookback)" provides the baseline for normal price movement over the specified lookback period.

The Time-Price Velocity indicator calculation combines multiple sophisticated components. First, it calculates acceleration as the change in velocity over time:

acceleration = normalizedVelocity - normalizedVelocity

Then, the signal generation applies EMA smoothing to reduce noise while preserving responsiveness:

signal = ta.ema(normalizedVelocity, smooth)

This creates a velocity-based momentum indicator that combines price displacement analysis with statistical normalization, providing traders with both directional signals and acceleration insights for enhanced market timing.

🟢 How to Use

1. Signal Interpretation and Threshold Zones

Positive Values (Above Zero): Time-price velocity indicating bullish momentum with upward price displacement relative to normalized baseline

Negative Values (Below Zero): Time-price velocity indicating bearish momentum with downward price displacement relative to normalized baseline

Zero Line Crosses: Velocity transitions between bullish and bearish regimes, indicating potential trend changes or momentum shifts

Upper Threshold Zone: Area above positive threshold (default 1.0) indicating strong bullish velocity and potential reversal point

Lower Threshold Zone: Area below negative threshold (default -1.0) indicating strong bearish velocity and potential reversal point

2. Acceleration Analysis and Visual Features

Acceleration Columns: Background histogram showing velocity acceleration (the rate of change of velocity), with green columns indicating accelerating velocity and red columns indicating decelerating velocity. The interpretation depends on trend context: red columns in downtrends indicate strengthening bearish momentum, while red columns in uptrends indicate weakening bullish momentum

Acceleration Column Height: The height of each column represents the magnitude of acceleration, with taller columns indicating stronger acceleration or deceleration forces

Bar Coloring: Optional price bar coloring matches velocity direction for immediate visual trend confirmation

Info Table: Real-time display of current velocity and acceleration values with trend arrows and change indicators

3. Additional Features:

Confirmed vs Live Data: Toggle between confirmed (closed) bar analysis for stable signals or current bar inclusion for real-time updates

Multi-timeframe Adaptability: Velocity normalization ensures consistent readings across different chart timeframes and asset volatilities

Alert System: Built-in alerts for threshold crossovers and direction changes

🟢 Examples with Preconfigured Settings

Default : Balanced configuration suitable for most timeframes and general trading applications, providing optimal balance between sensitivity and noise filtering for medium-term analysis.

Scalping : High sensitivity setup with shorter lookback period and reduced smoothing for ultra-short-term trades on 1-15 minute charts, optimized for capturing rapid momentum shifts and frequent trading opportunities.

Swing Trading : Extended lookback period with enhanced smoothing and higher threshold for multi-day positions, designed to filter market noise while capturing significant momentum moves on 1-4 hour and daily timeframes.

Dual Supertrend tohungmc tikDual Supertrend is an advanced trend-following indicator that combines two Supertrend strategies — a Large Supertrend and a Small Supertrend — to provide you with more precise entry and exit signals.

This indicator plots two Supertrend lines:

Large Supertrend (Blue and Orange): A broader trend that reacts slower to price movements.

Small Supertrend (Green and Red): A faster trend that responds quicker to market changes.

Key Features:

Customizable ATR Periods and Multipliers for both Large and Small Supertrends.

Buy/Sell Signals: When the Small Supertrend trend changes, and it's aligned with the Large Supertrend, you get reliable buy and sell signals.

Highlighting: The background can be highlighted in green or red, depending on whether the Large Supertrend is in an uptrend or downtrend.

Alerts: Alerts can be set for buy/sell signals or when the trend direction changes.

Use Case:

This indicator is designed for traders looking to follow both long-term and short-term trends. By combining the slower Large Supertrend with the faster Small Supertrend, it gives a more comprehensive view of market trends and better entry/exit points.

Indicator Inputs:

ATR Periods and Multipliers: Control how sensitive the Supertrend reacts to market changes.

Highlighting: Enable/Disable background highlighting.

Buy/Sell Signals: Option to show buy/sell signals based on trend direction changes.

ATR Squeeze BackgroundThis simple but powerful indicator shades the background of your chart whenever volatility contracts, based on a custom comparison of fast and slow ATR (Average True Range) periods.

By visualizing low-volatility zones, you can:

* Identify moments of compression that may precede explosive price moves

* Stay out of choppy, low-momentum periods

* Adapt this as a component in a broader volatility or breakout strategy

🔧 How It Works

* A Fast ATR (default: 7 periods) and a Slow ATR (default: 40 periods) are calculated

* When the Fast ATR is lower than the Slow ATR, the background is shaded in blue

* This shading signals a contraction in volatility — a condition often seen before breakouts or strong directional moves

⚡️ Why This Matters

Many experienced traders pay close attention to volatility cycles. This background indicator helps visualize those cycles at a glance. It's minimal, non-intrusive, and easy to combine with your existing tools.

🙏 Credits

This script borrows core logic from the excellent “Relative Volume at Time” script by TradingView. Credit is given with appreciation.

⚠️ Disclaimer

This script is for educational purposes only.

It does not constitute financial advice, and past performance is not indicative of future results. Always do your own research and test strategies before making trading decisions.

ATR % Line from LoD/HoDATR % Line Trading Indicator - Entry Filter Tool

This Pine Script creates a sophisticated ATR (Average True Range) percentage-based entry filter indicator for TradingView that helps traders avoid buying overextended stocks and identify optimal entry zones based on volatility.

Core Functionality - Entry Discipline

The script calculates a maximum entry threshold by taking a percentage of the Average True Range (ATR) and projecting it from the current day's low. This creates a dynamic "no-buy zone" that adapts to market volatility, helping traders avoid purchasing stocks that have already moved too far from their daily base.

Key Calculation:

Measures the ATR over a specified period (default: 14 bars)

Takes a user-defined percentage of that ATR (default: 25%)

Projects this distance from the day's low to establish a maximum entry threshold

Entry Rule: Avoid buying when price exceeds this ATR% level from the daily low or high.

Visual Features

Entry Threshold Line:

Draws a horizontal line at the calculated maximum entry level

Line extends forward for clear visualization of the "no-buy zone"

Red zones above this line indicate overextended conditions

Fully customizable appearance with color, width, and style options

Smart Entry Alerts:

Optional labels show the ATR percentage threshold and exact price level

Visual confirmation when stocks are trading in acceptable entry zones vs. extended areas

Real-Time Monitoring Table:

Displays current distance from daily low as ATR percentage

Shows whether current price is in "safe entry zone" or "extended territory"

Customizable display options for clean chart analysis

Practical Applications for Entry Management

Avoiding Extended Entries:

Primary Use: Don't initiate long positions when price is more than X% ATR from the daily low

Prevents buying stocks that have already made their daily move

Reduces risk of buying at temporary tops within the trading session

Entry Zone Identification:

Price trading below the ATR% line = potential entry opportunity

Price trading above the ATR% line = wait for pullback or skip the trade

Combines volatility analysis with momentum discipline

Risk Management Benefits:

Improved Entry Timing: Enter closer to daily support levels

Better Risk/Reward: Shorter distance to stop loss (daily low)

Reduced Chasing: Systematic approach prevents FOMO-driven entries

Volatility Awareness: Higher volatility stocks get wider acceptable entry ranges

Configuration for Entry Filtering

Key Settings for Entry Management:

ATR Percentage: Set your maximum acceptable extension (15-30% common for day trading)

Reference Point: Use "Low" to measure extension from daily base

Line Style: Make highly visible to clearly see entry threshold

Alert Integration: Visual confirmation of entry-friendly zones

Typical Usage Scenarios:

Conservative Entries: 15-20% ATR from daily low

Moderate Extensions: 25-35% ATR for stronger momentum plays

Aggressive Setups: 40%+ ATR for breakout situations (use with caution)

Entry Strategy Integration

Pre-Market Planning:

Set ATR% threshold based on stock's typical volatility

Identify key levels where entries become unfavorable

Plan alternative entry strategies for extended stocks

Intraday Execution:

Monitor real-time ATR% extension from daily low

Avoid new long positions when threshold is exceeded

Wait for pullbacks to re-enter acceptable entry zones

This tool transforms volatility analysis into practical entry discipline, helping traders maintain consistent entry standards and avoid the costly mistake of chasing overextended stocks. By respecting ATR-based extension limits, traders can improve their entry timing and overall trade profitability.

ATR Plots + OverlayATR Plots + Overlay

This tool calculates and displays Average True Range (ATR)-based levels on your chart for any selected timeframe, giving traders a quick visual reference for expected price movement relative to the most recent bar’s open price. It plots guide levels above and below that open and shows how much of the typical ATR-based range has already been covered—all in one interactive table and on-chart overlay.

What It Does

ATR Calculation:

Uses true range data over a user-defined period (default 14), smoothed via RMA, SMA, EMA, or WMA, on the selected timeframe (e.g., 1h, 4h, daily) to calculate the ATR value.

Projected Levels:

Plots four reference levels relative to the open price of the most recent bar on the chosen timeframe:

+100% ATR: Open + ATR

+50% ATR: Open + 50% of ATR

−50% ATR: Open − 50% of ATR

−100% ATR: Open − ATR

Coverage %:

Tracks high and low prices for the current session on the selected timeframe and calculates what percentage of the ATR has already been covered:

Coverage % = (High − Low) ÷ ATR × 100

Interactive Table:

Shows the ATR value and current coverage percentage in a customizable table overlay. Position, color scheme, borders, transparency, and an optional empty top row are all adjustable via settings.

Customization Options

Table Settings:

Position the table (top/bottom × left/right).

Customize background color, text color, border color, and thickness.

Optionally add an empty top row for spacing.

Line Settings:

Choose color, line style (solid/dotted/dashed), and width.

Lines automatically update with each new bar on the selected timeframe, anchored to that bar’s open price.

General Inputs:

ATR length (number of bars).

Smoothing method (RMA, SMA, EMA, WMA).

Timeframe selection for ATR calculations (e.g., 15m, 1h, Daily).

How to Use It for Trading

Measure Volatility: Quickly gauge the expected price movement based on ATR for any timeframe.

Identify Overextension: Use the coverage % to see how much of the expected ATR range is already consumed.

Plan Entries & Exits: Align trade targets and stops with ATR levels for more objective planning.

Visual Reference: Horizontal guide lines and table update automatically as new bars form, keeping information clear and actionable.

Ideal For

Intraday traders using ATR levels to frame trades.

Swing traders wanting ATR-based reference points for larger timeframes.

Anyone seeking a volatility-based framework for planning stops, targets, or identifying overextended conditions.

Combined Predictive Indicator### Combined Predictive Zones & Levels

This indicator is a powerful hybrid tool designed to provide a comprehensive map of potential future price action. It merges two distinct predictive models into a single, cohesive view, helping traders identify key levels of support, resistance, and areas of high confluence.

#### How It Works: Two Models in One

This script is built on two core components that you can use together or analyze separately:

**Part 1: Classic Range & Fibonacci Prediction**

This model uses classic technical analysis principles to project a potential range for the upcoming price action.

* **Highest High / Lowest Low:** It identifies the significant trading range over a user-defined lookback period.

* **Fibonacci Levels:** It automatically plots key Fibonacci retracement levels (e.g., 38.2% and 61.8%) within this range, which often act as critical support or resistance.

* **ATR & Average Range:** It calculates a "predicted" upper and lower boundary based on the average historical range and current volatility (ATR).

**Part 2: Advanced Predictive Ranges (Self-Adjusting Channels)**

This is a dynamic model that creates adaptive support and resistance zones based on a smoothed average price and volatility.

* **Dynamic Average:** It uses a unique moving average that only adjusts when the price moves significantly, creating a stable baseline.

* **ATR-Based Zones:** It projects multiple levels of support (S1, S2) and resistance (R1, R2) around this average, which widen and narrow based on market volatility. These zones often signal areas where price might stall or reverse.

#### Key Features:

* **Hybrid Model for Confluence:** The true power of this indicator lies in finding where the levels from both models overlap. A Fibonacci level aligning with a Predictive Range support zone is a much stronger signal.

* **Comprehensive Data Table:** A clean, on-chart table displays the precise values of all key predictive levels, allowing for quick reference and precise trade planning.

* **Multi-Timeframe (MTF) Capability:** The Advanced Predictive Ranges can be calculated on a higher timeframe, giving you a broader market context.

* **Fully Customizable:** All lengths, multipliers, and levels for both models are fully adjustable in the settings to fit any asset or trading style.

* **Clear Visuals:** All zones and levels are color-coded for intuitive and easy-to-read analysis.

#### How to Use:

1. Look for areas of **confluence** where multiple levels from both models cluster together. These are high-probability zones for price reactions.

2. Use the Predictive Range zones (S1/S2 and R1/R2) as potential targets for trades or as areas to watch for entries and exits.

3. Pay attention to the on-chart table for exact price levels to set limit orders or stop-losses.

**Disclaimer:** This script is an analytical tool for educational purposes and should not be considered financial advice. All trading involves risk. Past performance is not indicative of future results. Always use this indicator as part of a comprehensive trading strategy with proper risk management.

Feedback is welcome! If you find this tool useful, please leave a like.

ATR as % of CloseATR 14day period in % terms

the Normal ATR indicator by TV helps but this gives a clear idea as to the range in percentage terms as and when market rises to newer and newer highs

better than an absolute value

Fibonacci Range Detector ║ BullVision🔬 Overview

The Fibonacci Range Mapper is a dynamic technical tool designed to identify, track, and visualize price ranges using Fibonacci levels. Whether you're trading manually or prefer automated structure recognition, this indicator helps you contextualize market moves and locate key price zones with precision.

⚙️ Core Logic

🔍 Range Detection (Auto & Manual Modes)

In Auto mode, the indicator uses an advanced ZigZag system based on ATR or percentage thresholds to confirm market swings and construct Fibonacci-based ranges.

In Manual mode, traders can define their own swing low and high to generate precise custom ranges.

📐 Fibonacci Mapping

Each detected range is automatically plotted with key Fibonacci retracement levels — 0%, 25%, 50%, 75%, 100% — along with optional extensions (127.2% and 161.8%) to anticipate price continuations or reversals.

📋 Live Data Table

An integrated info panel dynamically displays crucial metrics:

• Range size

• Current price zone (Discount / Mid / Premium)

• Position within range (%)

• Distance to range extremes

• Range status (Pending or Confirmed)

🕰️ Historical Memory

Up to 20 past ranges can be stored and visualized simultaneously, helping traders recognize repeated price behaviors and contextual support/resistance levels.

🎨 Visual Highlights

Zones of interest (0–25% = Discount, 75–100% = Premium) are color-coded with custom transparency, and labels can be toggled for clarity. The current active range updates in real time as structure evolves.

🔧 User Customization

• Detection Method: Choose between ATR or % ZigZag for automated swing identification

• Confirmation Delay: Set how many bars to wait before confirming a new high

• Manual Overrides: Select exact price levels when you want full control

• Extensions & Labels: Toggle additional lines and info to suit your charting style

• Visual Table Position: Customize where the data table appears on screen

• Color Scheme: Define your own zone gradients for better visual interpretation

📈 Use Cases

This indicator is ideal for traders who want to:

• Identify value zones within local or macro price structures

• Plan trades around Fibonacci retracement and extension levels

• Detect shifts in market structure using an adaptive ZigZag logic

• Track recurring price ranges and historical reaction points

• Enhance technical confluence with clean, visual price mapping

⚠️ Important Notes

This tool is not a buy/sell signal generator — it is a visual framework for structure-based analysis.

Use it in conjunction with your existing strategy and risk management process.

Always confirm with broader context and multi-timeframe alignment.

Markov Chain Trend ProbabilityA Markov Chain is a mathematical model that predicts future states based on the current state, assuming that the future depends only on the present (not the past). Originally developed by Russian mathematician Andrey Markov, this concept is widely used in:

Finance: Risk modeling, portfolio optimization, credit scoring, algorithmic trading

Weather Forecasting: Predicting sunny/rainy days, temperature patterns, storm tracking

Here's an example of a Markov chain: If the weather is sunny, the probability that will be sunny 30 min later is say 90%. However, if the state changes, i.e. it starts raining, how the probability that will be raining 30 min later is say 70% and only 30% sunny.

Similar concept can be applied to markets price action and trends.

Mathematical Foundation

The core principle follows the Markov Property: P(X_{t+1}|X_t, X_{t-1}, ..., X_0) = P(X_{t+1}|X_t)

Transition Matrix :

-------------Next State

Current----

--------P11 P12

-----P21 P22

Probability Calculations:

P(Up→Up) = Count(Up→Up) / Count(Up states)

P(Down→Down) = Count(Down→Down) / Count(Down states)

Steady-state probability: π = πP (where π is the stationary distribution)

State Definition:

State = UPTREND if (Price_t - Price_{t-n})/ATR > threshold

State = DOWNTREND if (Price_t - Price_{t-n})/ATR < -threshold

How It Works in Trading

This indicator applies Markov Chain theory to market trends by:

Defining States: Classifies market conditions as UPTREND or DOWNTREND based on price movement relative to ATR (Average True Range)

Learning Transitions: Analyzes historical data to calculate probabilities of moving from one state to another

Predicting Probabilities: Estimates the likelihood of future trend continuation or reversal

How to Use

Parameters:

Lookback Period: Number of bars to analyze for trend detection (default: 14)

ATR Threshold: Sensitivity multiplier for state changes (default: 0.5)

Historical Periods: Sample size for probability calculations (default: 33)

Trading Applications:

Trend confirmation for entry/exit decisions

Risk assessment through probability analysis

Market regime identification

Early warning system for potential trend reversals

The indicator works on any timeframe and asset class. Enjoy!

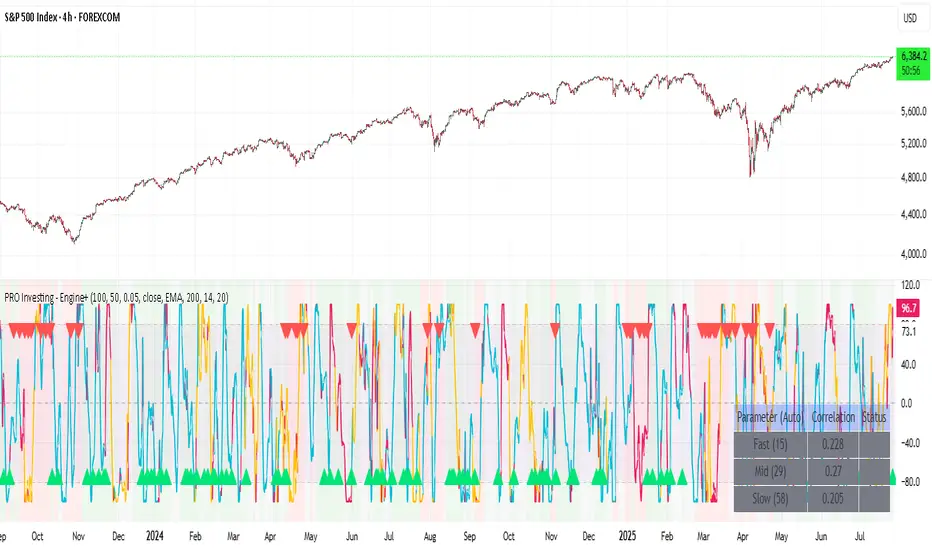

PRO Investing - Apex EnginePRO Investing - Apex Engine

1. Core Concept: Why Does This Indicator Exist?

Traditional momentum oscillators like RSI or Stochastic use a fixed "lookback period" (e.g., 14). This creates a fundamental problem: a 14-period setting that works well in a fast, trending market will generate constant false signals in a slow, choppy market, and vice-versa. The market's character is dynamic, but most tools are static.

The Apex Engine was built to solve this problem. Its primary innovation is a self-optimizing core that continuously adapts to changing market conditions. Instead of relying on one fixed setting, it actively tests three different momentum profiles (Fast, Mid, and Slow) in real-time and selects the one that is most synchronized with the current price action.

This is not just a random combination of indicators; it's a deliberate synthesis designed to create a more robust momentum tool. It combines:

Volatility analysis (ATR) to generate adaptive lookback periods.

Momentum measurement (ROC) to gauge the speed of price changes.

Statistical analysis (Correlation) to validate which momentum measurement is most effective right now.

Classic trend filters (Moving Average, ADX) to ensure signals are only taken in favorable market conditions.

The result is an oscillator that aims to be more responsive in volatile trends and more stable in quiet periods, providing a more intelligent and adaptive signal.

2. How It Works: The Engine's Three-Stage Process

To be transparent, it's important to understand the step-by-step logic the indicator follows on every bar. It's a process of Adapt -> Validate -> Signal.

Stage 1: Adapt (Dynamic Length Calculation)

The engine first measures market volatility using the Average True Range (ATR) relative to its own long-term average. This creates a volatility_factor. In high-volatility environments, this factor causes the base calculation lengths to shorten. In low-volatility, they lengthen. This produces three potential Rate of Change (ROC) lengths: dynamic_fast_len, dynamic_mid_len, and dynamic_slow_len.

Stage 2: Validate (Self-Optimizing Mode Selection)

This is the core of the engine. It calculates the ROC for all three dynamic lengths. To determine which is best, it uses the ta.correlation() function to measure how well each ROC's movement has correlated with the actual bar-to-bar price changes over the "Optimization Lookback" period. The ROC length with the highest correlation score is chosen as the most effective profile for the current moment. This "active" mode is reflected in the oscillator's color and the dashboard.

Stage 3: Signal (Normalized Velocity Oscillator)

The winning ROC series is then normalized into a consistent oscillator (the Velocity line) that ranges from -100 (extreme oversold) to +100 (extreme overbought). This ensures signals are comparable across any asset or timeframe. Signals are only generated when this Velocity line crosses its signal line and the trend filters (explained below) give a green light.

3. How to Use the Indicator: A Practical Guide

Reading the Visuals:

Velocity Line (Blue/Yellow/Pink): The main oscillator line. Its color indicates which mode is active (Fast, Mid, or Slow).

Signal Line (White): A moving average of the Velocity line. Crossovers generate potential signals.

Buy/Sell Triangles (▲ / ▼): These are your primary entry signals. They are intentionally strict and only appear when momentum, trend, and price action align.

Background Color (Green/Red/Gray): This is your trend context.

Green: Bullish trend confirmed (e.g., price above a rising 200 EMA and ADX > 20). Only Buy signals (▲) can appear.

Red: Bearish trend confirmed. Only Sell signals (▼) can appear.

Gray: No clear trend. The market is likely choppy or consolidating. No signals will appear; it is best to stay out.

Trading Strategy Example:

Wait for a colored background. A green or red background indicates the market is in a tradable trend.

Look for a signal. For a green background, wait for a lime Buy triangle (▲) to appear.

Confirm the trade. Before entering, confirm the signal aligns with your own analysis (e.g., support/resistance levels, chart patterns).

Manage the trade. Set a stop-loss according to your risk management rules. An exit can be considered on a fixed target, a trailing stop, or when an opposing signal appears.

4. Settings and Customization

This script is open-source, and its settings are transparent. You are encouraged to understand them.

Synaptic Engine Group:

Volatility Period: The master control for the adaptive engine. Higher values are slower and more stable.

Optimization Lookback: How many bars to use for the correlation check.

Switch Sensitivity: A buffer to prevent frantic switching between modes.

Advanced Configuration & Filters Group:

Price Source: The data source for momentum calculation (default close).

Trend Filter MA Type & Length: Define your long-term trend.

Filter by MA Slope: A key feature. If ON, allows for "buy the dip" entries below a rising MA. If OFF, it's stricter, requiring price to be above the MA.

ADX Length & Threshold: Filters out non-trending, choppy markets. Signals will not fire if the ADX is below this threshold.

5. Important Disclaimer

This indicator is a decision-support tool for discretionary traders, not an automated trading system or financial advice. Past performance is not indicative of future results. All trading involves substantial risk. You should always use proper risk management, including setting stop-losses, and never risk more than you are prepared to lose. The signals generated by this script should be used as one component of a broader trading plan.

% / ATR Buy, Target, Stop + Overlay & P/L% / ATR Buy, Target, Stop + Overlay & P/L

This tool combines volatility‑based and fixed‑percentage trade planning into a single, on‑chart overlay—with built‑in profit‑and‑loss estimates. Toggle between ATR or percentage modes, plot your Buy, Target and Stop levels, and see the dollar gain or loss for a specified position size—all in one interactive table and chart display.

NOTE: To activate plotted lines, price labels, P/L rows and table values, enter a Buy Price greater than zero.

What It Does

Mode Toggle: Choose between “ATR” (volatility‑based) or “%” (fixed‑percentage) calculations.

Buy Price Input: Manually enter your entry price.

ATR Mode:

Target = Buy + (ATR × Target Multiplier)

Stop = Buy − (ATR × Stop Multiplier)

Percentage Mode:

Target = Buy × (1 + Target % / 100)

Stop = Buy × (1 – Stop % / 100)

P/L Estimates: Specify a dollar amount to “invest” at your Buy price, and the script calculates:

Gain ($): Profit if Target is hit

Loss ($): Cost if Stop is hit

Visual Overlay: Draws horizontal lines for Buy, Target and Stop, with optional price labels on the chart scale.

Interactive Table: Displays Buy, Target, Stop, ATR/timeframe info (in ATR mode), percentages (in % mode), and P/L rows.

Customization Options

Line Settings:

Choose color, style (solid/dashed/dotted), and width for Buy, Target, Stop lines.

Extend lines rightward only or in both directions.

Table Settings:

Position the table (top/bottom × left/right).

Toggle individual rows: Buy Price; Target (multiplier or %); Stop (multiplier or %); Target ATR %; Stop ATR %; ATR Time Frame; ATR Value; Gain ($); Loss ($).

Customize text colors for each row and background transparency.

General Inputs:

ATR length and optional ATR timeframe override (e.g. use daily ATR on an intraday chart).

Target/Stop multipliers or percentages.

Dollar Amount for P/L calculations.

How to Use It for Trading

Plan Your Entry: Enter your intended Buy Price and position size (dollar amount).

Select Mode: Toggle between ATR or % mode depending on whether you prefer volatility‑based or fixed offsets.

Assess R:R and P/L: Instantly see your Target, Stop levels, and potential profit or loss in dollars.

Visual Reference: Lines and price labels update in real time as you tweak inputs—ideal for live trading, backtesting or trade journaling.

Ideal For

Traders who want both volatility‑based and percentage‑based exit options in one tool

Those who need on‑chart P/L estimates based on position size

Swing and intraday traders focused on objective, rule‑based trade management

Anyone who uses ATR for adaptive stops/targets or fixed percentages for simpler exits

ATR Dynamic Stop (Table + Plot + ATR %)📊 This script displays dynamic stop levels based on ATR, designed for active traders.

Features:

- Shows long and short stop levels (price ± ATR × multiplier).

- Displays values as a floating table on the top-right corner.

- Optional plot lines directly on the chart.

- Option to calculate based on realtime price or last close.

- Displays the ATR value both in price units and as a percentage of the selected price.

- Fully customizable table: text size, text color, background color.

Inputs:

- ATR Multiplier and Length.

- Show/hide stop lines on the chart.

- Select price source (realtime or last close).

- Table appearance options.

Ideal for:

- Traders who want a clear visual stop guide.

- Combining volatility with risk management.

ATR Trailing Stop with ATR Targets [v6]What the Indicator Does

This custom TradingView indicator is designed for active traders who want to automate and visualize their trailing stop management and target setting, using true market volatility. It combines the Average True Range (ATR) with dynamic market structure logic to:

Trail a stop-loss behind major swings in real time, using 2×ATR (adjustable) from the highest high in uptrends or the lowest low in downtrends.

Flip trading bias between bullish and bearish when the stop is breached.

Identify and plot three profit targets (at 1, 2, and 3 ATR from the breakout/flip point) after every stop-flip, helping traders scale out or set take-profits objectively.

Maintain a visible presence on your chart every bar to avoid indicator errors, with color and labeling for clear distinction between long/short phases.

How the Indicator Works

1. ATR Calculation

ATR Period and Multiplier: You select your preferred ATR length (default is 14 bars) and a multiplier (default is 2.0).

Volatility Adjustment: ATR measures the average "true" bar range, so the trailing stop and targets adapt to current volatility.

2. Trailing Stop Logic

Uptrend (bullish bias): The indicator tracks the highest high made since the last bearish-to-bullish flip and sets the stop at - .

The stop only raises (never lowers) during an uptrend, protecting gains in strong moves.

Downtrend (bearish bias): Tracks the lowest low made since the last bullish-to-bearish flip, with stop at + .

The stop only lowers (never raises) in a downtrend.

Flip Point: If price closes through the trailing stop, the current bias “flips,” and the logic reverses (bullish to bearish or vice versa). At the new close, flip price and bar index are stored for target calculation.

3. ATR Targets after Flip

After each stop flip:

Three targets—based on the new close price—are calculated and plotted:

Long flip (new bull bias): Target1 = close + 1×ATR, Target2 = close + 2×ATR, Target3 = close + 3×ATR.

Short flip (new bear bias): Target1 = close - 1×ATR, Target2 = close - 2×ATR, Target3 = close - 3×ATR.

These targets help with scaling out, partial profit-taking, or setting automated orders.

4. Visual Feedback

Trailing stop line: Green for long bias, red for short bias.

Targets: Distinct color-coded circles at 1, 2, 3 ATR levels from the most recent flip.

Flip Labels: Mark the bar and price where bias flipped (“Long Flip” or “Short Flip”) for quick pattern recognition.

Subtle background shading: Ensures TradingView's requirement for “indicator output every bar.”

How to Use This Indicator

Parameter Setup

ATR Period and Multiplier: Adjust to match the timeframe and volatility of your instrument.

Lower periods/multipliers for short-term/volatile trading.

Higher values for smoother signals or higher timeframes.

Starting Trend: Set to match the expected initial bias if the instrument has strong trend characteristics.

Trading Application

1. Daily Bias Approach

Establish your bias in line with your trading plan (e.g., only trade long if price is above the previous day's high, short below the previous day's low).

Only look for trades in the indicator's current bias direction, as expressed by the stop and background color.

2. Entry

Use the indicator as a real-time confirmation or trailing stop for your entries.

Breakout: Enter when price establishes the current bias, using the trailing stop as your risk level.

Reversal: Wait for a bias flip after an extended move; enter in the direction of the new bias.

VWAP Rebound: Combine with a VWAP bounce—enter only if the indicator bias supports your direction.

3. Exits/Targets

Trailing stop management: Move your stop according to the plotted line; exit if your stop is hit.

Profit-taking: Scale out or take profits as price approaches each ATR-based target.

Use the dynamic labeling to identify reversal flips and reset your plan if stopped or the bias changes.

4. Market Context

Filter and frame setups by watching correlated indicators (DXY, VIX, AUDJPY, put/call ratio) and upcoming news; trade only in the daily bias direction for best consistency.

5. Practical Tips

Combine this indicator with your custom watchlist and alert settings to get notified on flips or targets.

Review the last label ("Long Flip"/"Short Flip") and targets to plan partial exits.

Remember: ATR adapts to volatility, so the stop and targets stay proportionate even when price action shifts.

ADR TableTrack volatility and session momentum in real-time with customizable precision.

Key Features:

Average Daily Range (ADR): Configurable length (default 5 days), based on previous daily high–low ranges.

Session Anchor Options: Choose anchor at 4 am NY, 6 pm NY, 9:30 am NY, 8:30 am NY, Previous Day Close, or Current Bar.

Session Range & %ADR: Displays the real-time range from the chosen anchor, plus what percentage of ADR has been covered.

High / Low Target Levels: Calculates ADR targets based on anchor: anchor ± ADR.

Optional Target Lines: Draw horizontal lines for high and low targets across the session; customize color and width.

Dynamic Table Display: User-selectable table size and text size (Tiny to Huge) for optimal readability.

Robust Anchor Logic: Uses the first bar at-or-after anchor time each NY day, ensuring stability even on irregular intraday timeframes.

How to Use

Choose your anchor in settings.

View ADR, session range (with %ADR), and target price levels in the top-right pane.Toggle High/Low lines to overlay targets on the chart.

Adjust table and text size to match your workspace.

Why It Matters

Quickly assess where price stands relative to typical volatility.

Easily identify intraday price exhaustion or breakout zones.

Anchor flexibility enables use for both futures and equities, aligning with your trading session.

Clean, professional display—no clutter, no guesswork.

ATR Trailing + Alerts + Price LabelsATR Trend is a clean and intelligent trend-following overlay built for traders who want clarity during both trending and ranging markets.

This indicator dynamically detects bullish and bearish market trends using the Average True Range (ATR), applying a confirmation-based approach to filter out false signals and minor pullbacks.

The trend line is:

Blue 🔵 during uptrends.

Black ⚫ during downtrends.

Continuous, recalculating only when the market truly shifts — not just when price temporarily crosses the line.

When a confirmed trend reversal occurs:

A 🔼 or 🔽 label shows the exact price of the flip.

An alert can be triggered to notify the user immediately.

💡 Features:

✅ Single-line trend direction

✅ Filters out short-term noise

✅ Exact price labeling on trend change

✅ Built-in alerts for up/down trend shifts

⚙️ Inputs:

ATR Period – Length of ATR calculation (default: 14)

ATR Multiplier – Offset for trend line placement (default: 2.0)

Flip Sensitivity – Number of bars required to confirm a trend reversal (default: 3)

This tool is suitable for:

Swing traders avoid false breakouts

Scalpers looking for high-probability trend entries

Algorithmic setups requiring structured trend logic

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

UT Bot + LinReg Candles (Dual Sensitivity)

Script Description:

This indicator combines the popular UT Bot Alerts system with Linear Regression Candles (open source) for enhanced trend detection and trading signals in one singel script. The UT Bot features independent, then 2 x ATR sensitivity and periods controls for buy and sell signals, allowing you to fine-tune entries and exits to match your strategy. The script also overlays colored Linear Regression Candles with an optional signal line, helping you visually identify trend strength and direction. All calculations are performed on standard chart prices (no Heikin Ashi). Suitable for all asset classes and timeframes.

Eample setting for usdjpy 5 min chart for repeated buy and sell singnals based on trend:

BUY ATR period 300 multiplier 1

SELL ATR period 1 multiplier 2

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice. Use at your own risk; the author assumes no responsibility for any trading results or losses.

Credits goes to to Ugurvu for linreg candles and quantnomad for UT Bot alerts that make this script possible.

Author: Patrick

Random Coin Toss Strategy📌 Overview

This strategy is a probability-based trading simulation that randomly decides trade direction using a coin-toss mechanism and executes trades with a customizable risk-reward ratio. It's designed primarily for testing entry frequency and risk dynamics, not predictive accuracy.

🎯 Core Concept

Every N bars (configurable), the strategy performs a pseudo-random coin toss.

Based on the result:

If heads → Buy

If tails → Sell

Once a position is opened, it sets a Stop-Loss (SL) and Take-Profit (TP) based on a multiple of the current ATR (Average True Range) value.

⚙️ Configurable Inputs

ATR Length Period for ATR calculation, determines volatility basis.

SL Multiplier SL distance = ATR × multiplier (e.g., 1.0 means 1x ATR) .

TP Multiplier TP distance = ATR × multiplier (e.g., 2.0 = 2x ATR) .

Entry Frequency Bars to wait between each new coin toss decision.

Show TP/SL Zones Toggle on/off for drawing visual TP and SL zones.

Box Size Number of bars used to define the width of the TP/SL boxes.

🔁 Entry & Exit Logic

Entry:

Happens only when no current position exists and it's the correct bar interval.

Entry direction is randomly decided.

Exit:

Positions exit at either:

Take-Profit (TP) level

Stop-Loss (SL) level

Both are calculated using the configured ATR-based distances.

🖼️ Visual Features

TP and SL zones:

Rendered as shaded rectangles (boxes) only once per trade.

Green box for TP zone, red box for SL zone.

Automatically deleted and redrawn for each new trade to avoid chart clutter.

ATR Display Table:

A minimal info table at the top-right shows the current ATR value.

Updates every few bars for performance.

🧪 Use Cases

Ideal for risk-reward modeling, strategy prototyping, and understanding how volatility-based SL/TP behavior affects results.

Great for backtesting frequency, RR tweaks (e.g., 2:5 or 3:1), and execution structure in random conditions.

⚠️ Disclaimer

Since the trade direction is random, this script is not meant for predictive trading but serves as a powerful experiment framework for studying how SL, TP, and volatility interact with random chance in a controlled, repeatable system.