[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

ATR

MTF Signal XpertMTF Signal Xpert – Detailed Description

Overview:

MTF Signal Xpert is a proprietary, open‑source trading signal indicator that fuses multiple technical analysis methods into one cohesive strategy. Developed after rigorous backtesting and extensive research, this advanced tool is designed to deliver clear BUY and SELL signals by analyzing trend, momentum, and volatility across various timeframes. Its integrated approach not only enhances signal reliability but also incorporates dynamic risk management, helping traders protect their capital while navigating complex market conditions.

Detailed Explanation of How It Works:

Trend Detection via Moving Averages

Dual Moving Averages:

MTF Signal Xpert computes two moving averages—a fast MA and a slow MA—with the flexibility to choose from Simple (SMA), Exponential (EMA), or Hull (HMA) methods. This dual-MA system helps identify the prevailing market trend by contrasting short-term momentum with longer-term trends.

Crossover Logic:

A BUY signal is initiated when the fast MA crosses above the slow MA, coupled with the condition that the current price is above the lower Bollinger Band. This suggests that the market may be emerging from a lower price region. Conversely, a SELL signal is generated when the fast MA crosses below the slow MA and the price is below the upper Bollinger Band, indicating potential bearish pressure.

Recent Crossover Confirmation:

To ensure that signals reflect current market dynamics, the script tracks the number of bars since the moving average crossover event. Only crossovers that occur within a user-defined “candle confirmation” period are considered, which helps filter out outdated signals and improves overall signal accuracy.

Volatility and Price Extremes with Bollinger Bands

Calculation of Bands:

Bollinger Bands are calculated using a 20‑period simple moving average as the central basis, with the upper and lower bands derived from a standard deviation multiplier. This creates dynamic boundaries that adjust according to recent market volatility.

Signal Reinforcement:

For BUY signals, the condition that the price is above the lower Bollinger Band suggests an undervalued market condition, while for SELL signals, the price falling below the upper Bollinger Band reinforces the bearish bias. This volatility context adds depth to the moving average crossover signals.

Momentum Confirmation Using Multiple Oscillators

RSI (Relative Strength Index):

The RSI is computed over 14 periods to determine if the market is in an overbought or oversold state. Only readings within an optimal range (defined by user inputs) validate the signal, ensuring that entries are made during balanced conditions.

MACD (Moving Average Convergence Divergence):

The MACD line is compared with its signal line to assess momentum. A bullish scenario is confirmed when the MACD line is above the signal line, while a bearish scenario is indicated when it is below, thus adding another layer of confirmation.

Awesome Oscillator (AO):

The AO measures the difference between short-term and long-term simple moving averages of the median price. Positive AO values support BUY signals, while negative values back SELL signals, offering additional momentum insight.

ADX (Average Directional Index):

The ADX quantifies trend strength. MTF Signal Xpert only considers signals when the ADX value exceeds a specified threshold, ensuring that trades are taken in strongly trending markets.

Optional Stochastic Oscillator:

An optional stochastic oscillator filter can be enabled to further refine signals. It checks for overbought conditions (supporting SELL signals) or oversold conditions (supporting BUY signals), thus reducing ambiguity.

Multi-Timeframe Verification

Higher Timeframe Filter:

To align short-term signals with broader market trends, the script calculates an EMA on a higher timeframe as specified by the user. This multi-timeframe approach helps ensure that signals on the primary chart are consistent with the overall trend, thereby reducing false signals.

Dynamic Risk Management with ATR

ATR-Based Calculations:

The Average True Range (ATR) is used to measure current market volatility. This value is multiplied by a user-defined factor to dynamically determine stop loss (SL) and take profit (TP) levels, adapting to changing market conditions.

Visual SL/TP Markers:

The calculated SL and TP levels are plotted on the chart as distinct colored dots, enabling traders to quickly identify recommended exit points.

Optional Trailing Stop:

An optional trailing stop feature is available, which adjusts the stop loss as the trade moves favorably, helping to lock in profits while protecting against sudden reversals.

Risk/Reward Ratio Calculation:

MTF Signal Xpert computes a risk/reward ratio based on the dynamic SL and TP levels. This quantitative measure allows traders to assess whether the potential reward justifies the risk associated with a trade.

Condition Weighting and Signal Scoring

Binary Condition Checks:

Each technical condition—ranging from moving average crossovers, Bollinger Band positioning, and RSI range to MACD, AO, ADX, and volume filters—is assigned a binary score (1 if met, 0 if not).

Cumulative Scoring:

These individual scores are summed to generate cumulative bullish and bearish scores, quantifying the overall strength of the signal and providing traders with an objective measure of its viability.

Detailed Signal Explanation:

A comprehensive explanation string is generated, outlining which conditions contributed to the current BUY or SELL signal. This explanation is displayed on an on‑chart dashboard, offering transparency and clarity into the signal generation process.

On-Chart Visualizations and Debug Information

Chart Elements:

The indicator plots all key components—moving averages, Bollinger Bands, SL and TP markers—directly on the chart, providing a clear visual framework for understanding market conditions.

Combined Dashboard:

A dedicated dashboard displays key metrics such as RSI, ADX, and the bullish/bearish scores, alongside a detailed explanation of the current signal. This consolidated view allows traders to quickly grasp the underlying logic.

Debug Table (Optional):

For advanced users, an optional debug table is available. This table breaks down each individual condition, indicating which criteria were met or not met, thus aiding in further analysis and strategy refinement.

Mashup Justification and Originality

MTF Signal Xpert is more than just an aggregation of existing indicators—it is an original synthesis designed to address real-world trading complexities. Here’s how its components work together:

Integrated Trend, Volatility, and Momentum Analysis:

By combining moving averages, Bollinger Bands, and multiple oscillators (RSI, MACD, AO, ADX, and an optional stochastic), the indicator captures diverse market dynamics. Each component reinforces the others, reducing noise and filtering out false signals.

Multi-Timeframe Analysis:

The inclusion of a higher timeframe filter aligns short-term signals with longer-term trends, enhancing overall reliability and reducing the potential for contradictory signals.

Adaptive Risk Management:

Dynamic stop loss and take profit levels, determined using ATR, ensure that the risk management strategy adapts to current market conditions. The optional trailing stop further refines this approach, protecting profits as the market evolves.

Quantitative Signal Scoring:

The condition weighting system provides an objective measure of signal strength, giving traders clear insight into how each technical component contributes to the final decision.

How to Use MTF Signal Xpert:

Input Customization:

Adjust the moving average type and period settings, ATR multipliers, and oscillator thresholds to align with your trading style and the specific market conditions.

Enable or disable the optional stochastic oscillator and trailing stop based on your preference.

Interpreting the Signals:

When a BUY or SELL signal appears, refer to the on‑chart dashboard, which displays key metrics (e.g., RSI, ADX, bullish/bearish scores) along with a detailed breakdown of the conditions that triggered the signal.

Review the SL and TP markers on the chart to understand the associated risk/reward setup.

Risk Management:

Use the dynamically calculated stop loss and take profit levels as guidelines for setting your exit points.

Evaluate the provided risk/reward ratio to ensure that the potential reward justifies the risk before entering a trade.

Debugging and Verification:

Advanced users can enable the debug table to see a condition-by-condition breakdown of the signal generation process, helping refine the strategy and deepen understanding of market dynamics.

Disclaimer:

MTF Signal Xpert is intended for educational and analytical purposes only. Although it is based on robust technical analysis methods and has undergone extensive backtesting, past performance is not indicative of future results. Traders should employ proper risk management and adjust the settings to suit their financial circumstances and risk tolerance.

MTF Signal Xpert represents a comprehensive, original approach to trading signal generation. By blending trend detection, volatility assessment, momentum analysis, multi-timeframe alignment, and adaptive risk management into one integrated system, it provides traders with actionable signals and the transparency needed to understand the logic behind them.

ATR stop lossPlots the stop loss level based on average true range (ATR) and a multiplier of choice (1 to 2.5, default is 1.5), subtracted from closing price.

Additions in this version:

You can now show percentage labels to help evaluate the level of risk.

The color of the plotted line and the text labels can be picked by the user.

High-Low Breakout Strategy with ATR traling Stop LossThis script is a TradingView Pine Script strategy that implements a High-Low Breakout Strategy with ATR Trailing Stop.created by SK WEALTH GURU, Here’s a breakdown of its key components:

Features and Functionality

Custom Timeframe and High-Low Detection

Allows users to select a custom timeframe (default: 30 minutes) to detect high and low levels.

Tracks the high and low within a user-specified period (e.g., first 30 minutes of the session).

Draws horizontal lines for high and low, persisting for a specified number of days.

Trade Entry Conditions

Long Entry: If the closing price crosses above the recorded high.

Short Entry: If the closing price crosses below the recorded low.

The user can choose to trade Long, Short, or Both.

ATR-Based Trailing Stop & Risk Management

Uses Average True Range (ATR) with a multiplier (default: 3.5) to determine a dynamic trailing stop-loss.

Trades reset daily, ensuring a fresh start each day.

Trade Execution and Partial Profit Taking

Stop-loss: Default at 1% of entry price.

Partial profit: Books 50% of the position at 3% profit.

Max 2 trades per day: If the first trade hits stop-loss, the strategy allows one re-entry.

Intraday Exit Condition

All positions close at 3:15 PM to ensure no overnight risk.

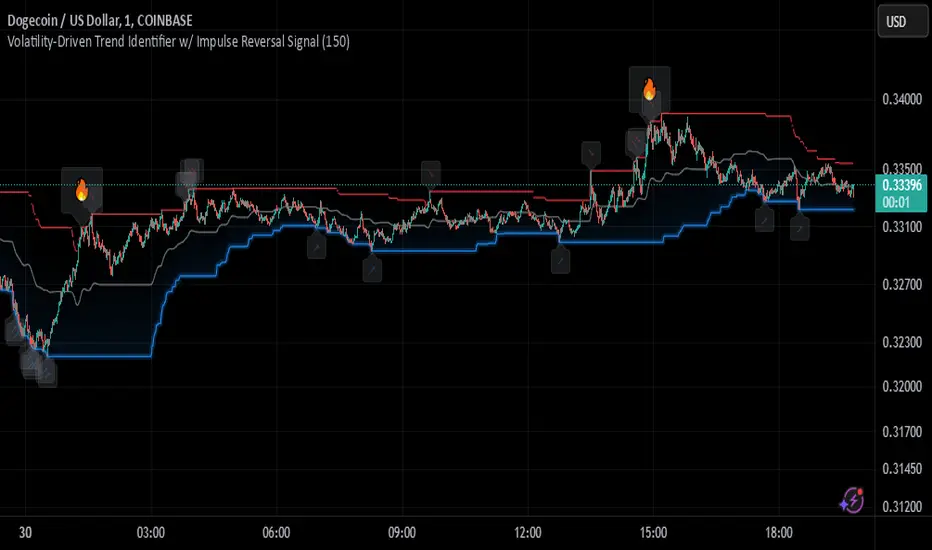

Johnny's Volatility-Driven Trend Identifier w/ Reversal SignalsJohnny's Volatility-Driven Trend Identifier w/ Reversal Signals is designed to identify high-probability trend shifts and reversals by incorporating volatility, momentum, and impulse-based filtering. It is specifically built for traders who want to capture strong trend movements while minimizing false signals caused by low volatility noise.

By leveraging Rate of Change (ROC), Relative Strength Index (RSI), and Average True Range (ATR)-based volatility detection, the indicator dynamically adapts to market conditions. It highlights breakout trends, reversals, and early signs of momentum shifts using strategically placed labels and color-coded trend visualization.

Inspiration taken from Top G indicator .

What This Indicator Does

The Volatility-Driven Trend Identifier works by:

Measuring Market Extremes & Momentum:

Uses ROC normalization with standard deviation to identify impulse moves in price action.

Implements RSI filtering to determine overbought/oversold conditions that validate trend strength.

Utilizes ATR-based volatility tracking to ensure signals only appear when meaningful market movements are occurring.

Identifying Key Trend Events:

Power Peak (🔥): Marks a confirmed strong downtrend, ideal for shorting opportunities.

Surge (🚀): Indicates a confirmed strong uptrend, signaling a potential long entry.

Soft Surge (↗): Highlights a mild bullish reentry or early uptrend formation.

Soft Peak (↘): Shows a mild bearish reentry or early downtrend formation.

Providing Adaptive Filtering for Reliable Signals:

Filters out weak trends with a volatility check, ensuring signals appear only in strong market conditions.

Implements multi-level confirmation by combining trend strength metrics, preventing false breakouts.

Uses gradient-based visualization to color-code market sentiment for quick interpretation.

What This Indicator Signals

Breakouts & Impulse Moves: 🚀🔥

The Surge (🚀) and Power Peak (🔥) labels indicate confirmed momentum breakouts, where the trend has been validated by a combination of ROC impulse, RSI confirmation, and ATR volatility filtering.

These signals suggest that the market is entering a strong trend, and traders can align their entries accordingly.

Early Trend Formation & Reentries: ↗ ↘

The Soft Surge (↗) and Soft Peak (↘) labels indicate areas where a trend might be forming, but is not yet fully confirmed.

These signals help traders anticipate potential entries before the trend gains full strength.

Volatility-Adaptive Trend Filtering: 📊

Since the indicator only activates in volatile conditions, it avoids the pitfalls of low-range choppy markets where false signals frequently occur.

ATR-driven adaptive windowing allows the indicator to dynamically adjust its sensitivity based on real-time volatility conditions.

How to Use This Indicator

1. Identifying High-Probability Entries

Bullish Entries (Long Trades)

Look for 🚀 Surge signals in an uptrend.

Confirm with RSI (should be above 50 for momentum).

Ensure volatility is increasing to validate the breakout.

Use ↗ Soft Surge signals for early entries before the trend fully confirms.

Bearish Entries (Short Trades)

Look for 🔥 Power Peak signals in a downtrend.

RSI should be below 50, indicating downward momentum.

Volatility should be rising, ensuring market momentum is strong.

Use ↘ Soft Peak signals for early entries before a full bearish confirmation.

2. Avoiding False Signals

Ignore signals when the market is ranging (low ATR).

Check RSI and ROC alignment to ensure trend confirmation.

Use additional confluences (e.g., price action, support/resistance levels, moving averages) for enhanced accuracy.

3. Trend Confirmation & Filtering

The stronger the trend, the higher the likelihood that Surge (🚀) and Power Peak (🔥) signals will continue in their direction.

Soft Surge (↗) and Soft Peak (↘) act as early warning signals before major breakouts occur.

What Makes This a Machine Learning-Inspired Moving Average?

While this indicator is not a direct implementation of machine learning (as Pine Script lacks AI/ML capabilities), it mimics machine learning principles by adapting dynamically to market conditions using the following techniques:

Adaptive Trend Selection:

It does not rely on fixed moving averages but instead adapts dynamically based on volatility expansion and momentum detection.

ATR-based filtering adjusts the indicator’s sensitivity to real-time conditions.

Multi-Factor Confirmation (Feature Engineering Equivalent in ML):

Combines ROC, RSI, and ATR in a structured way, similar to how ML models use multiple inputs to filter and classify data.

Implements conditional trend recognition, ensuring that only valid signals pass through the filter.

Noise Reduction with Data Smoothing:

The algorithm avoids false signals by incorporating trend intensity thresholds, much like how ML models remove outliers to refine predictions.

Adaptive filtering ensures that low-volatility environments do not produce misleading signals.

Why Use This Indicator?

✔ Reduces False Signals: Multi-factor validation ensures only high-confidence signals are triggered.

✔ Works in All Market Conditions: Volatility-adaptive nature allows the indicator to perform well in both trending and ranging markets.

✔ Great for Swing & Intraday Trading: It helps spot momentum shifts early and allows traders to catch major market moves before they fully develop.

✔ Visually Intuitive: Color-coded trends and clear signal markers make it easy to interpret.

Choppiness IndexThis Pine Script v6 indicator calculates the Choppiness Index over a user-defined length and segments it based on user-defined thresholds for choppy and trending market conditions. The indicator allows users to toggle the visibility of choppy, trending, and neutral segments using checkboxes.

Here's how it works:

Inputs: Users can set the length for the Choppiness Index calculation and thresholds for choppy and trending conditions. They can also choose which segments to display.

Choppiness Index Calculation: The script calculates the Choppiness Index using the ATR and the highest-high and lowest-low over the specified length.

Segment Determination: The script determines which segment the current Choppiness Index value falls into based on the thresholds. The color changes exactly at the threshold values.

Dynamic Plotting: The Choppiness Index is plotted with a color that changes based on the segment. The plot is only visible if the segment is "turned on" by the user.

Threshold Lines: Dashed horizontal lines are plotted at the choppy and trending thresholds for reference.

This indicator helps traders visualize market conditions and identify potential transitions between choppy and trending phases, with precise color changes at the threshold values.

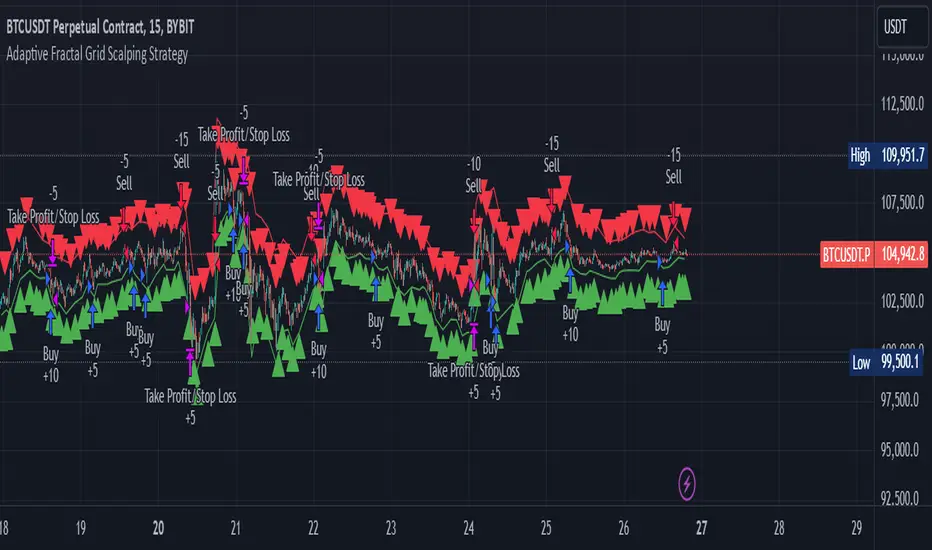

Adaptive Fractal Grid Scalping StrategyThis Pine Script v6 component implements an "Adaptive Fractal Grid Scalping Strategy" with an added volatility threshold feature.

Here's how it works:

Fractal Break Detection: Uses ta.pivothigh and ta.pivotlow to identify local highs and lows.

Volatility Clustering: Measures volatility using the Average True Range (ATR).

Adaptive Grid Levels: Dynamically adjusts grid levels based on ATR and user-defined multipliers.

Directional Bias Filter: Uses a Simple Moving Average (SMA) to determine trend direction.

Volatility Threshold: Introduces a new input to specify a minimum ATR value required to activate the strategy.

Trade Execution Logic: Places limit orders at grid levels based on trend direction and fractal levels, but only when ATR exceeds the volatility threshold.

Profit-Taking and Stop-Loss: Implements profit-taking at grid levels and a trailing stop-loss based on ATR.

How to Use

Inputs: Customize the ATR length, SMA length, grid multipliers, trailing stop multiplier, and volatility threshold through the input settings.

Visuals: The script plots fractal points and grid levels on the chart for easy visualization.

Trade Signals: The strategy automatically places buy/sell orders based on the detected fractals, trend direction, and volatility threshold.

Profit and Risk Management: The script includes logic for taking profits and setting stop-loss levels to manage trades effectively.

This strategy is designed to capitalize on micro-movements during high volatility and avoid overtrading during low-volatility trends. Adjust the input parameters to suit your trading style and market conditions.

Radial Basis Kernal ATR [BackQuant]Radial Basis Kernel ATR

The Radial Basis Kernel ATR is a trading indicator that combines the classic Average True Range (ATR) with advanced Radial Basis Function (RBF) kernel smoothing . This innovative approach creates a highly adaptive and precise tool for detecting volatility, identifying trends, and providing dynamic support and resistance levels.

With its configurable parameters and ability to adjust to market conditions, this indicator offers traders a robust framework for making informed decisions across various assets and timeframes.

Key Feature: Radial Basis Function Kernel Smoothing

The Radial Basis Function (RBF) kernel is at the heart of this indicator, applying sophisticated mathematical techniques to smooth price data and calculate an enhanced version of ATR. By weighting data points dynamically, the RBF kernel ensures that recent price movements are given appropriate emphasis without overreacting to short-term noise.

The RBF kernel uses a gamma factor to control the degree of smoothing, making it highly adaptable to different asset classes and market conditions:

Gamma Factor Adjustment :

For low-volatility data (e.g., indices), a smaller gamma (0.05–0.1) ensures smoother trends and avoids overly sharp responses.

For high-volatility data (e.g., cryptocurrencies), a larger gamma (0.1–0.2) captures the increased price fluctuations while maintaining stability.

Experimentation is Key : Traders are encouraged to backtest and visually compare different gamma values to find the optimal setting for their specific asset and strategy.

The gamma factor dynamically adjusts based on the variance of the source data, ensuring the indicator remains effective across a wide range of market conditions.

Average True Range (ATR) with Dynamic Bands

The ATR is a widely used volatility measure that captures the degree of price movement over a specific period. This indicator enhances the traditional ATR by integrating the RBF kernel, resulting in a smoothed and adaptive ATR calculation.

Dynamic bands are created around the RBF kernel output using a user-defined ATR factor , offering valuable insights into potential support and resistance zones. These bands expand and contract based on market volatility, providing a visual representation of potential price movement.

Moving Average Confluence

For additional confirmation, the indicator includes the option to overlay a moving average on the smoothed ATR. Traders can choose from several moving average types, such as EMA , SMA , or Hull , and adjust the lookback period to suit their strategy. This feature helps identify broader trends and potential confluence areas, making the indicator even more versatile.

Long and Short Trend Detection

The indicator provides long and short signals based on the directional movement of the smoothed ATR:

Long Signal : Triggered when the ATR crosses above its previous value, indicating bullish momentum.

Short Signal : Triggered when the ATR crosses below its previous value, signaling bearish momentum.

These trend signals are visually highlighted on the chart with green and red bar coloring (optional), providing clear and actionable insights.

Customization Options

The Radial Basis Kernel ATR offers extensive customization options, allowing traders to tailor the indicator to their preferences:

RBF Kernel Settings

Source : Select the price data (e.g., close, high, low) used for the kernel calculation.

Kernel Length : Define the lookback period for the RBF kernel, controlling the smoothing effect.

Gamma Factor : Adjust the smoothing sensitivity, with smaller values for smoother trends and larger values for responsiveness.

ATR Settings

ATR Period : Set the period for ATR calculation, with shorter periods capturing more short-term volatility and longer periods providing a broader view.

ATR Factor : Adjust the scaling of ATR bands for dynamic support and resistance levels.

Confluence Settings

Moving Average Type : Choose from various moving average types for additional trend confirmation.

Moving Average Period : Define the lookback period for the moving average overlay.

Visualization

Trend Coloring : Enable or disable bar coloring based on trend direction (green for long, red for short).

Background Highlighting : Add optional background shading to emphasize long and short trends visually.

Line Width : Customize the thickness of the plotted ATR line for better visibility.

Alerts and Automation

To help traders stay on top of market movements, the indicator includes built-in alerts for trend changes:

Kernel ATR Trend Up : Triggered when the ATR indicates a bullish trend.

Kernel ATR Trend Down : Triggered when the ATR signals a bearish trend.

These alerts ensure traders never miss important opportunities, providing timely notifications directly to their preferred device.

Suggested Gamma Values

The effectiveness of the gamma factor depends on the asset type and the selected kernel length:

Low Volatility Assets (e.g., indices): Use a smaller gamma factor (approximately 0.05–0.1) for smoother trends.

High Volatility Assets (e.g., crypto): Use a larger gamma factor (approximately 0.1–0.2) to capture sharper price movements.

Experimentation : Fine-tune the gamma factor using backtests or visual comparisons to optimize for specific assets and strategies.

Trading Applications

The Radial Basis Kernel ATR is a versatile tool suitable for various trading styles and strategies:

Trend Following : Use the smoothed ATR and dynamic bands to identify and follow trends with confidence.

Reversal Trading : Spot potential reversals by observing interactions with dynamic ATR bands and moving average confluence.

Volatility Analysis : Analyze market volatility to adjust risk management strategies or position sizing.

Final Thoughts

The Radial Basis Kernel ATR combines advanced mathematical techniques with the practical utility of ATR, offering traders a powerful and adaptive tool for volatility analysis and trend detection. Its ability to dynamically adjust to market conditions through the RBF kernel and gamma factor makes it a unique and indispensable part of any trader's toolkit.

By combining sophisticated smoothing , dynamic bands , and customizable visualization , this indicator enhances the ability to read market conditions and make more informed trading decisions. As always, backtesting and incorporating it into a broader strategy are recommended for optimal results.

Comprehensive Volume and Metrics with Pre-Market Volume Data

This script is designed for traders who want a detailed view of market activity, including regular market and pre-market volume, dollar volume, relative volume (RVOL), average daily range (ADR), average true range (ATR), relative strength index (RSI), and the QQQ’s percentage change.

The script includes customizable metrics displayed in tables on the chart for easy analysis, with the option to toggle the visibility of each metric.

Key Features:

Volume and Dollar Volume:

Displays the volume of shares traded during the current day (or pre-market, if enabled).

Includes a calculation of dollar volume, representing the total dollar amount of trades (Volume × Close Price).

Relative Volume (RVOL):

Displays RVOL Day, which is the relative volume of the current day compared to the 2-day moving average.

Shows RVOL 90D, indicating relative volume over the past 90 days.

Both RVOL metrics are calculated as percentages and display the percentage change compared to the standard (100%).

Pre-Market Data:

Includes pre-market volume (PVOL) and pre-market dollar volume (P$ VOL) which are displayed only if pre-market data is enabled.

Tracks volume and dollar volume during pre-market hours (4:00 AM to 9:30 AM Eastern Time) for more in-depth analysis.

Optionally, shows pre-market RSI based on volume-weighted close prices.

Average Daily Range (ADR):

Displays the percentage change between the highest and lowest prices over the defined ADR period (default is 20 days).

Average True Range (ATR):

Shows the ATR, a popular volatility indicator, for a given period (default is 14 bars).

RSI (Relative Strength Index):

Displays RSI for the given period (default is 14).

RSI is calculated using pre-market data when available.

QQQ:

Shows the percentage change of the QQQ ETF from the previous day’s close.

The QQQ percentage change is color-coded: green for positive, red for negative, and gray for no change.

Customizable Inputs:

Visibility Options: Toggle the visibility of each metric, such as volume, dollar volume, RVOL, ADR, ATR, RSI, and QQQ.

Pre-Market Data: Enable or disable the display of pre-market data for volume and dollar volume.

Table Positioning: Adjust the position of tables displaying the metrics either at the bottom-left or bottom-right of the chart.

Text Color and Table Background: Choose between white or black text for the tables and customize the background color.

Tables:

The script utilizes tables to display multiple metrics in an organized and easy-to-read format.

The values are updated dynamically, reflecting real-time data as the market moves.

Pre-Market Data:

The script calculates pre-market volume and dollar volume, along with other key metrics like RSI and RVOL, to help assess market sentiment before the market officially opens.

The pre-market data is accumulated from 4:00 AM to 9:30 AM ET, allowing for pre-market analysis and comparison to regular market hours.

User-Friendly and Flexible:

This script is designed to be highly customizable, giving you the ability to toggle which metrics to display and where they appear on the chart. You can easily focus on the data that matters most to your trading strategy.

Trendilo ARTrendilo AR is a custom trading indicator designed to identify market trends using advanced techniques such as the Arnaud Legoux Moving Average (ALMA), volume confirmations, and dynamic volatility bands. This indicator provides a clear visualization of trends, including significant changes and custom alerts.

Review of Indicators Used

1. ALMA

Description:

ALMA is a moving average that applies an advanced filter to smooth price data, reducing noise and focusing on actual trends.

Usage in the Indicator:

Used to calculate the smoothed percentage price change and determine trend direction. Customizable parameters include:

- Length: Defines the number of bars to consider.

- Offset: Adjusts sensitivity toward recent prices.

- Sigma: Controls the degree of smoothing.

Advantages:

- Reduced lag in trend detection.

- Resistance to market noise.

2. ATR

Description:

ATR measures the market’s average volatility by considering the range between high and low prices over a given period.

Usage in the Indicator:

ATR is used to calculate "dynamic smoothing", adjusting the indicator’s sensitivity based on current market volatility.

Advantages:

- Adapts to high or low volatility conditions.

- Helps define dynamic support and resistance levels.

3. SMA

Description:

SMA calculates the average of prices or volume over a specific time period.

Usage in the Indicator:

Used to calculate the volume moving average (Volume SMA) to confirm whether the current volume supports the detected trend.

Advantages:

- Easy to understand and calculate.

- Provides volume-based trend confirmation.

4. RMS Bands

Description:

RMS Bands calculate the standard deviation of percentage price changes, creating upper and lower levels that act as overbought and oversold indicators.

Usage in the Indicator:

- Define the range within which the market is considered neutral.

- Crosses above or below the bands indicate trend changes.

Advantages:

- Visual identification of strong trends.

- Helps filter false signals.

Colors and Visuals Used in the Indicator

1. ALMA Line

Colors:

- Green: Indicates a confirmed uptrend (with sufficient volume).

- Red: Indicates a confirmed downtrend (with sufficient volume).

- Gray: Indicates a neutral phase or insufficient volume to confirm a trend.

2. RMS Bands

- Upper and Lower Lines:

- Purple (with transparency): These lines represent the RMS bands (upper and lower) and

adjust opacity based on trend strength.

- Stronger trends result in less transparency (more solid colors).

3. Highlighted Background (Strong Trends)

- Color:

- Light Green (transparent): Highlights a strong trend when the smoothed percentage change (ALMA) exceeds 1.5 times the RMS.

4. Horizontal Lines

- Baseline (0):

- Dark Gray: Serves as a central reference to identify the directionality of percentage changes.

- Additional Line (0.1):

- Blue: A customizable line to mark user-defined key levels.

5. Bar Colors

- Bar Colors:

- Green: When the price is in a confirmed uptrend.

- Red: When the price is in a confirmed downtrend.

- No color: When there is insufficient volume or no clear trend.

How to Use the Indicator

1. Initial Setup

1. Add the Indicator to Your Chart: Copy the code into the Pine Editor on TradingView and apply it to your chart.

2. Customize Parameters: Adjust values based on your trading strategy:

- Smoothing: Controls the level of smoothing for percentage changes.

- Lookback Length: Defines the observation period for calculations.

- Band Multiplier: Adjusts the width of RMS bands.

2. Signal Interpretation

1. Indicator Colors:

- Green: Confirmed uptrend.

- Red: Confirmed downtrend.

- Gray: No clear trend or insufficient volume.

2. RMS Bands:

- If the ALMA line (smoothed percentage change) crosses above the upper RMS band, it signals a potential uptrend.

- If it crosses below the lower RMS band, it signals a potential downtrend.

3. Volume Confirmation:

- The indicator's color activates only if the current volume exceeds the Volume SMA.

3. Alerts and Decisions

1. Trend Change Alerts:

- The indicator automatically triggers alerts when an uptrend or downtrend is detected.

- Configure these alerts to receive real-time notifications.

2. Strong Trend Signals:

- When the magnitude of the percentage change exceeds 1.5 times the RMS, the chart background highlights the strong trend.

4. Trading Strategies

1. Buy:

- Enter long positions when:

- The indicator turns green.

- Volume confirms the trend.

- Consider placing a stop-loss just below the lower RMS band.

2. Sell:

- Enter short positions when:

- The indicator turns red.

- Volume confirms the trend.

- Consider placing a stop-loss just above the upper RMS band.

3. Neutral:

- Avoid trading when the indicator is gray, as no clear trend or insufficient volume is present.

Disclaimer: As this is my first published indicator, please use it with caution. Feedback is highly appreciated to improve its performance.

Happy Trading!

00 Averaging Down Backtest Strategy by RPAlawyer v21FOR EDUCATIONAL PURPOSES ONLY! THE CODE IS NOT YET FULLY DEVELOPED, BUT IT CAN PROVIDE INTERESTING DATA AND INSIGHTS IN ITS CURRENT STATE.

This strategy is an 'averaging down' backtester strategy. The goal of averaging/doubling down is to buy more of an asset at a lower price to reduce your average entry price.

This backtester code proves why you shouldn't do averaging down, but the code can be developed (and will be developed) further, and there might be settings even in its current form that prove that averaging down can be done effectively.

Different averaging down strategies exist:

- Linear/Fixed Amount: buy $1000 every time price drops 5%

- Grid Trading: Placing orders at price levels, often with increasing size, like $1000 at -5%, $2000 at -10%

- Martingale: doubling the position size with each new entry

- Reverse Martingale: decreasing position size as price falls: $4000, then $2000, then $1000

- Percentage-Based: position size based on % of remaining capital, like 10% of available funds at each level

- Dynamic/Adaptive: larger entries during high volatility, smaller during low

- Logarithmic: position sizes increase logarithmically as price drops

Unlike the above average costing strategies, it applies averaging down (I use DCA as a synonym) at a very strong trend reversal. So not at a certain predetermined percentage negative PNL % but at a trend reversal signaled by an indicator - hence it most closely resembles a dynamically moving grid DCA strategy.

Both entering the trade and averaging down assume a strong trend. The signals for trend detection are provided by an indicator that I published under the name '00 Parabolic SAR Trend Following Signals by RPAlawyer', but any indicator that generates numeric signals of 1 and -1 for buy and sell signals can be used.

The indicator must be connected to the strategy: in the strategy settings under 'External Source' you need to select '00 Parabolic SAR Trend Following Signals by RPAlawyer: Connector'. From this point, the strategy detects when the indicator generates buy and sell signals.

The strategy considers a strong trend when a buy signal appears above a very conservative ATR band, or a sell signal below the ATR band. The conservative ATR is chosen to filter ranging markets. This very conservative ATR setting has a default multiplier of 8 and length of 40. The multiplier can be increased up to 10, but there will be very few buy and sell signals at that level and DCA requirements will be very high. Trade entry and DCA occur at these strong trends. In the settings, the 'ATR Filter' setting determines the entry condition (e.g., ATR Filter multiplier of 9), and the 'DCA ATR' determines when DCA will happen (e.g., DCA ATR multiplier of 6).

The DCA levels and DCA amounts are determined as follows:

The first DCA occurs below the DCA Base Deviation% level (see settings, default 3%) which acts as a threshold. The thick green line indicates the long position avg price, and the thin red line below the green line indicates the 3% DCA threshold for long positions. The thick red line indicates the short position avg price, and the thin red line above the thick red line indicates the short position 3% DCA threshold. DCA size multiplier defines the DCA amount invested.

If the loss exceeds 3% AND a buy signal arrives below the lower ATR band for longs, or a sell signal arrives above the upper ATR band for shorts, then the first DCA will be executed. So the first DCA won't happen at 3%, rather 3% is a threshold where the additional condition is that the price must close above or below the ATR band (let's say the first DCA occured at 8%) – this is why the code resembles a dynamic grid strategy, where the grid moves such that alongside the first 3% threshold, a strong trend must also appear for DCA. At this point, the thick green/red line moves because the avg price is modified as a result of the DCA, and the thin red line indicating the next DCA level also moves. The next DCA level is determined by the first DCA level, meaning modified avg price plus an additional +8% + (3% * the Step Scale Multiplier in the settings). This next DCA level will be indicated by the modified thin red line, and the price must break through this level and again break through the ATR band for the second DCA to occur.

Since all this wasn't complicated enough, and I was always obsessed by the idea that when we're sitting in an underwater position for days, doing DCA and waiting for the price to correct, we can actually enter a short position on the other side, on which we can realize profit (if the broker allows taking hedge positions, Binance allows this in Europe).

This opposite position in this strategy can open from the point AFTER THE FIRST DCA OF THE BASE POSITION OCCURS. This base position first DCA actually indicates that the price has already moved against us significantly so time to earn some money on the other side. Breaking through the ATR band is also a condition for entry here, so the hedge position entry is not automatic, and the condition for further DCA is breaking through the DCA Base Deviation (default 3%) and breaking through the ATR band. So for the 'hedge' or rather opposite position, the entry and further DCA conditions are the same as for the base position. The hedge position avg price is indicated by a thick black line and the Next Hedge DCA Level is indicated by a thin black line.

The TPs are indicated by green labels for base positions and red labels for hedge positions.

No SL built into the strategy at this point but you are free to do your coding.

Summary data can be found in the upper right corner.

The fantastic trend reversal indicator Machine learning: Lorentzian Classification by jdehorty can be used as an external indicator, choose 'backtest stream' for the external source. The ATR Band multiplicators need to be reduced to 5-6 when using Lorentz.

The code can be further developed in several aspects, and as I write this, I already have a few ideas 😊

ADR Table BY @ICT_YEROADR Table BY @ICT_YERO

Created by: @ICT_YERO

This custom indicator is designed to provide the Average Daily Range (ADR) for multiple timeframes, including Daily, 4-Hour, and 1-Hour. The indicator is tailored to assist traders in understanding price volatility and making informed trading decisions.

Key Features

Multi-Timeframe ADR Calculation:

Automatically calculates and displays the ADR for Daily, 4-Hour, and 1-Hour timeframes.

Helps traders identify potential price movement ranges for different trading sessions.

Dynamic Range Visualization:

Clear visual representation of the ADR on the chart, making it easy to spot price extremes.

Real-time updates to reflect changes in price movement.

Custom Alerts:

Option to set alerts when the price approaches the ADR high or low.

Useful for identifying potential reversal zones or breakout opportunities.

User-Friendly Interface:

Simple and intuitive settings to customize colors, levels, and display preferences.

Seamlessly integrates with your existing TradingView setup.

ICT-Inspired Methodology:

Designed for traders who follow ICT concepts, focusing on precision and high-probability setups.

Applications

Range Trading: Helps determine the high and low boundaries for scalping or intraday setups.

Volatility Analysis: Understand market behavior during different times of the day or week.

Reversal Zones: Identify areas where price is likely to reverse, based on ADR extremes.

Whether you're a scalper, day trader, or swing trader, this indicator provides a comprehensive overview of price volatility across multiple timeframes, making it an essential tool for your trading arsenal.

AI InfinityAI Infinity – Multidimensional Market Analysis

Overview

The AI Infinity indicator combines multiple analysis tools into a single solution. Alongside dynamic candle coloring based on MACD and Stochastic signals, it features Alligator lines, several RSI lines (including glow effects), and optionally enabled EMAs (20/50, 100, and 200). Every module is individually configurable, allowing traders to tailor the indicator to their personal style and strategy.

Important Note (Disclaimer)

This indicator is provided for educational and informational purposes only.

It does not constitute financial or investment advice and offers no guarantee of profit.

Each trader is responsible for their own trading decisions.

Past performance does not guarantee future results.

Please review the settings thoroughly and adjust them to your personal risk profile; consider supplementary analyses or professional guidance where appropriate.

Functionality & Components

1. Candle Coloring (MACD & Stochastic)

Objective: Provide an immediate visual snapshot of the market’s condition.

Details:

MACD Signal: Used to identify bullish and bearish momentum.

Stochastic: Detects overbought and oversold zones.

Color Modes: Offers both a simple (two-color) mode and a gradient mode.

2. Alligator Lines

Objective: Assist with trend analysis and determining the market’s current phase.

Details:

Dynamic SMMA Lines (Jaw, Teeth, Lips) that adjust based on volatility and market conditions.

Multiple Lengths: Each element uses a separate smoothing period (13, 8, 5).

Transparency: You can show or hide each line independently.

3. RSI Lines & Glow Effects

Objective: Display the RSI values directly on the price chart so critical levels (e.g., 20, 50, 80) remain visible at a glance.

Details:

RSI Scaling: The RSI is plotted in the chart window, eliminating the need to switch panels.

Dynamic Transparency: A pulse effect indicates when the RSI is near critical thresholds.

Glow Mode: Choose between “Direct Glow” or “Dynamic Transparency” (based on ATR distance).

Custom RSI Length: Freely adjustable (default is 14).

4. Optional EMAs (20/50, 100, 200)

Objective: Utilize moving averages for trend assessment and identifying potential support/resistance areas.

Details:

20/50 EMA: Select which one to display via a dropdown menu.

100 EMA & 200 EMA: Independently enabled.

Color Logic: Automatically green (price > EMA) or red (price < EMA). Each EMA’s up/down color is customizable.

Configuration Options

Candle Coloring:

Choose between Gradient or Simple mode.

Adjust the color scheme for bullish/bearish candles.

Transparency is dynamically based on candle body size and Stochastic state.

Alligator Lines:

Toggle each line (Jaw/Teeth/Lips) on or off.

Select individual colors for each line.

RSI Section:

RSI Length can be set as desired.

RSI lines (0, 20, 50, 80, 100) with user-defined colors and transparency (pulse effect).

Additional lines (e.g., RSI 40/60) are also available.

Glow Effects:

Switch between “Dynamic Transparency” (ATR-based) and “Direct Glow”.

Independently applied to the RSI 100 and RSI 0 lines.

EMAs (20/50, 100, 200):

Activate each one as needed.

Each EMA’s up/down color can be customized.

Example Use Cases

Trend Identification:

Enable Alligator lines to gauge general trend direction through SMMA signals.

Timing:

Watch the Candle Colors to spot potential overbought or oversold conditions.

Fine-Tuning:

Utilize the RSI lines to closely monitor important thresholds (50 as a trend barometer, 80/20 as possible reversal zones).

Filtering:

Enable a 50 EMA to quickly see if the market is trading above (bullish) or below (bearish) it.

Catalyst TrendCatalyst Trend – A Comprehensive Trend and Regime Analyzer

The Catalyst Trend indicator was designed to dynamically and intuitively merge various classic analytical techniques. The goal is to filter out short-term market noise and reveal reliable trend phases or potential turning points. Below is a detailed explanation of its core elements and practical usage.

1. Concept and Idea

Multidimensional Trend Detection

This indicator goes beyond a simple momentum or volatility focus. It factors in multiple measurements to provide a more well-rounded market perspective.

Versatile Indicator Fusion

Linear Regression (LinReg): Multiple LinReg calculations are combined to smooth out price fluctuations and produce a robust trendline—known here as the “Cycle Reduced Line.”

ADX (Average Directional Index): Measures trend strength.

RSI (Relative Strength Index): Flags potential overbought or oversold conditions, in both the current timeframe and a higher timeframe.

ATR (Average True Range): Assesses volatility; used to dynamically adjust calculation lengths.

By weaving these elements together, the indicator adds value beyond simply stacking multiple indicators. It adapts to real-time market conditions, aiming to highlight genuine trends and reduce false signals.

2. Key Functions and Calculations

Dynamic Length & Smoothing

A blend of volatility (ATR), ADX values, and RSI inputs determines how many candles are used in the LinReg calculations and how heavily the data is smoothed.

This allows the indicator to respond promptly during periods of high volatility, while automatically adjusting to filter out unnecessary noise in quieter phases.c

Cycle Reduced Line

The script averages several offset LinReg calculations to produce a cleaner overall signal. Random outliers are thus minimized, making the trend path more visually consistent.

An additional EMA smoothing (“Final Smoothing”) further stabilizes this trendline, reducing the impact of minor price fluctuations.

Channel Bands (Optional)

These bands are derived from the standard deviation of the price residual (the difference between the smoothed price and the trendline).

They highlight potential over-extension zones: the upper band can mark short-term overbought areas, while the lower band might indicate oversold conditions.

Trend and Sideways Determination

Slope Calculation: The slope of the trendline (comparing the current bar to the previous one) helps identify short-term directional shifts.

DX Threshold: Once the ADX surpasses a user-defined threshold and the slope is positive, it may indicate a developing uptrend. Similarly, if the slope is negative and ADX > threshold, it could signal a potential downtrend.

Multi-Level Color Coding

Original Mode: Interpolated colors reflect uptrends, downtrends, and sideways phases, factoring in metrics like ADX and RSI.

Single Color: For a neutral look, the indicator can be displayed in one uniform color.

HTF RSI: This mode uses the higher-timeframe RSI to color the trendline (Long/Short/Neutral), offering a quick gauge of overarching market pressure.

3. Use Cases and Interpretation

Timeframes & Markets

The indicator is versatile and adapts well to different intervals, from 5-minute charts to weekly views.

It can be applied to various markets—crypto, forex, stocks—since volatility and trend strength are universal concepts.

Signal Recognition

Color Swings into a more pronounced upward hue (e.g., green) may signal mounting strength.

Neutral or mixed tones often point to sideways phases, which breakout traders might watch for potential price surges.

A shift to downward colors (e.g., red) may indicate a growing bearish trend.

Channel Bands & Volatility

When the bands spread widely, it’s wise to proceed with caution: abrupt spikes above the upper band or below the lower band can flag rapid short-term extremes.

These bands are more of a reference for potential overextension than a strict buy or sell trigger.

Additional Confirmations

Not a standalone panacea: The Catalyst Trend indicator is an analytical tool, best used alongside other methods such as volume analysis or price action (candlestick patterns, support/resistance levels) to bolster confidence in trading decisions.

4. Practical Tips

Parameter Adjustments

Depending on the market—crypto vs. traditional currency pairs—different ADX, RSI, or smoothing periods may be more effective. Experiment with the settings to tailor the indicator to your preferred timeframe.

Strategic Integration

Trailing Stops: For those riding a trend, the trendline or the channel bands may serve as a reference to trail stop-loss orders.

Trend Confirmation: Using RSI and ADX filters can help traders avoid sideways markets or stay the course when the trend is strong.

5. Important Final Notes

No Guarantee of Profits

No indicator can predict the future. Markets are inherently volatile and often unpredictable.

Responsible Risk Management

Test the indicator in a demo environment or with smaller positions before committing to large trades.

DAILY Supertrend + EMA Crossover with RSI FilterThis strategy is a technical trading approach that combines multiple indicators—Supertrend, Exponential Moving Averages (EMAs), and the Relative Strength Index (RSI)—to identify and manage trades.

Core Components:

1. Exponential Moving Averages (EMAs):

Two EMAs, one with a shorter period (fast) and one with a longer period (slow), are calculated. The idea is to spot when the faster EMA crosses above or below the slower EMA. A fast EMA crossing above the slow EMA often suggests upward momentum, while crossing below suggests downward momentum.

2. Supertrend Indicator:

The Supertrend uses Average True Range (ATR) to establish dynamic support and resistance lines. These lines shift above or below price depending on the prevailing trend. When price is above the Supertrend line, the trend is considered bullish; when below, it’s considered bearish. This helps ensure that the strategy trades only in the direction of the overall trend rather than against it.

3. RSI Filter:

The RSI measures momentum. It helps avoid buying into markets that are already overbought or selling into markets that are oversold. For example, when going long (buying), the strategy only proceeds if the RSI is not too high, and when going short (selling), it only proceeds if the RSI is not too low. This filter is meant to improve the quality of the trades by reducing the chance of entering right before a reversal.

4. Time Filters:

The strategy only triggers entries during user-specified date and time ranges. This is useful if one wants to limit trading activity to certain trading sessions or periods with higher market liquidity.

5. Risk Management via ATR-based Stops and Targets:

Both stop loss and take profit levels are set as multiples of the ATR. ATR measures volatility, so when volatility is higher, both stops and profit targets adjust to give the trade more breathing room. Conversely, when volatility is low, stops and targets tighten. This dynamic approach helps maintain consistent risk management regardless of market conditions.

Overall Logic Flow:

- First, the market conditions are analyzed through EMAs, Supertrend, and RSI.

- When a buy (long) condition is met—meaning the fast EMA crosses above the slow EMA, the trend is bullish according to Supertrend, and RSI is below the specified “overbought” threshold—the strategy initiates or adds to a long position.

- Similarly, when a sell (short) condition is met—meaning the fast EMA crosses below the slow EMA, the trend is bearish, and RSI is above the specified “oversold” threshold—it initiates or adds to a short position.

- Each position is protected by an automatically calculated stop loss and a take profit level based on ATR multiples.

Intended Result:

By blending trend detection, momentum filtering, and volatility-adjusted risk management, the strategy aims to capture moves in the primary trend direction while avoiding entries at excessively stretched prices. Allowing multiple entries can potentially amplify gains in strong trends but also increases exposure, which traders should consider in their risk management approach.

In essence, this strategy tries to ride established trends as indicated by the Supertrend and EMAs, filter out poor-quality entries using RSI, and dynamically manage trade risk through ATR-based stops and targets.

ATR/DTR with Custom Percentage DisplayThis Pine Script indicator provides a detailed view of the Average True Range (ATR) and Daily True Range (DTR), along with additional calculated metrics to assist in analyzing price volatility. The key features of the indicator include:

ATR Calculation:

The ATR is calculated over a user-defined timeframe, allowing traders to assess average market volatility over a specific period.

DTR Calculation:

The DTR represents the absolute range (high - low) of the current or chosen timeframe, providing insights into the day's price movement.

ATR/DTR Percentage:

This metric calculates the DTR as a percentage of the ATR, showing how the daily range compares to the average range, with dynamic coloring to highlight when it exceeds a user-defined threshold.

Custom Percentage of ATR:

Users can input a custom percentage to calculate and display a corresponding value of the ATR. For example, entering 15% will compute and display 15% of the ATR in the indicator’s table.

Dynamic Table Display:

The indicator outputs all these metrics in a well-organized table that is overlaid on the chart. The table includes:

ATR

DTR

ATR/DTR percentage

The user-defined percentage of ATR

Customizable Features:

Color Coding: The table dynamically changes its background color when the ATR/DTR percentage exceeds a user-defined threshold.

Placement Options: The table's position on the chart can be adjusted (e.g., bottom-right, top-center) for optimal visibility.

Use Case:

This indicator is ideal for traders who want a deeper understanding of market volatility and prefer visual representation of how current price movements compare to historical averages. It is especially useful for:

Setting volatility-based stop-loss levels.

Identifying high-volatility trading opportunities.

Tailoring strategies around price movement patterns.

Visual ATR StopThis indicator uses the Average True Range (ATR) to display a visual range for stop placement. Two multiplier values (example, 1 and 3) can be set to create a filled area below the price. This area represents the range between the two ATR levels, adjusted by subtracting the current price, providing a simple way to visualize stop-loss placement based on volatility.

The indicator is customizable; for example, negative values can place the area above the price for short positions. The filled color can also be removed, which allows precise levels to be marked above and below.

Precision Trading Strategy: Golden EdgeThe PTS: Golden Edge strategy is designed for scalping Gold (XAU/USD) on lower timeframes, such as the 1-minute chart. It captures high-probability trade setups by aligning with strong trends and momentum, while filtering out low-quality trades during consolidation or low-volatility periods.

The strategy uses a combination of technical indicators to identify optimal entry points:

1. Exponential Moving Averages (EMAs): A fast EMA (3-period) and a slow EMA (33-period) are used to detect short-term trend reversals via crossover signals.

2. Hull Moving Average (HMA): A 66-period HMA acts as a higher-timeframe trend filter to ensure trades align with the overall market direction.

3. Relative Strength Index (RSI): A 12-period RSI identifies momentum. The strategy requires RSI > 55 for long trades and RSI < 45 for short trades, ensuring entries are backed by strong buying or selling pressure.

4. Average True Range (ATR): A 14-period ATR ensures trades occur only during volatile conditions, avoiding choppy or low-movement markets.

By combining these tools, the PTS: Golden Edge strategy creates a precise framework for scalping and offers a systematic approach to capitalize on Gold’s price movements efficiently.

Adaptive Supertrend with Dynamic Optimization [EdgeTerminal]The Enhanced Adaptive Supertrend represents a significant evolution of the traditional Supertrend indicator, incorporating advanced mathematical optimization, dynamic volatility adjustment, intelligent signal filtering, reduced noise and false positives.

Key Features

Dynamic volatility-adjusted bands

Self-optimizing multiplier

Intelligent signal filtering system

Cooldown period to prevent signal clustering

Clear buy/sell signals with optimal positioning

Smooth trend visualization

RSI and MACD integration for confirmation

Performance-based optimization

Dynamic Band Calculation

Dynamic Band Calculation automatically adapts to market volatility, generates wider bands in volatile periods, reducing false signals. It also generates tighter bands in stable periods, capturing smaller moves and smooth transitions between different volatility regimes.

RSI Integration

The RSI and MACD play multiple crucial roles in the Adaptive Supertrend.

It first helps with momentum factor calculation. This dynamically adjusts band width based on momentum conditions. When the RSI is oversold, bands widen by 20% to prevent false signals during strong downtrends and provide more room for price movements in extreme conditions.

When the RSI is overbought, brands tighten by 20% and they become more sensitive to potential reversals to help catch trend changes earlier.

This reduces false signals in strong trends, helps detect potential reversals earlier than the usual, create adaptive band width based on market conditions and finally, better protection against whipsaws.

MACD Integration

The MACD in this supertrend indicator serves as a trend confirmation tool. The idea is to use MACD crossovers to confirm trend changes to reduce false trend change signals and enhance the signal quality.

For this to become a signal, MACD crossovers must align with price movement to help filter out weak or false signals, which acts as an additional layer of trend confirmation.

Additionally, MACD line position relative to signal line indicates trend strength, helps maintain positions in strong trends and assists in early detection of trend weakening.

Momentum Integration

Momentum Integration prevents false signals in extreme conditions, It adjusts dynamic bands based on market momentum, improves trend confirmation in strong moves and reduces whipsaws during consolidations.

Improved signals

There are a few systems to generate better signals, allowing for generally faster signals compared to original supertrend, such as:

Enforced cooldown period between signals

Prevents signal clustering

Clearer entry/exit points

Reduced false signals during choppy markets

Performance Optimization

This script implements a Sharpe ratio-inspired optimization algorithm to balance returns against risk, penalize large drawdowns, adapt parameters in real-time and improve risk-adjusted performance

Parameter Settings

ATR Period: 10 (default) - adjust based on timeframe

Initial Multiplier: 3.0 (default) - will self-optimize

Optimization Period: 50 (default) - longer periods for more stability

Smoothing Period: 3 (default) - adjust for signal smoothness

Best Practices

Use on multiple timeframes for confirmation

Allow the optimization process to run for at least 50 bars

Monitor the adaptive multiplier for trend strength indication

Consider RSI and MACD alignment for stronger signals

ATR% Multiple from Key Moving AverageThis script gives signal when the ATR% multiple from any chosen moving average is beyond the configurable threshold value. This indicator quantifies how extended the stock is from a given key moving average.

A lot of traders use ATR% multiple from 10DMA, 21EMA, 50SMA or 200SMA to determine how extended a stock is and accordingly sell partials or exit. By default the indicator takes 50SMA and when the ATR% multiple is greater than 7 then it gives the signal to take partials. You can back test this indicator with previous trades and determine the ideal threshold for the signal. For small and midcaps a threshold of 7 to 10 ATR% multiples from 50SMA is where partials can be taken while large caps can revert to mean even earlier at 3 to 5 ATR% multiples from 50SMA.

You can modify this script and use it anyway you please as long as you make it opensource on TradingView.

Position Sizing Calculator (Real-Time)█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the 5-minute timeframe, this script provides traders with continuously updated, dynamic position sizes. It enables traders to instantly determine the exact number of shares and dollar amount to use for entering a trade within their acceptable risk tolerance whenever a trade opportunity arises.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

Support/Resistance Strength [UAlgo]The Support/Resistance Strength indicator is a tool designed for traders seeking a precise understanding of key support and resistance levels in the market. This tool dynamically identifies and visualizes support and resistance zones based on pivot points and strength criteria, providing traders with actionable insights for better decision-making.

By incorporating features such as ATR-based or percentage-based channel calculations, customizable strength thresholds, and intuitive visualization of key levels, the indicator caters to traders of various skill levels and strategies. It also adapts dynamically to market conditions, allowing users to identify frequently tested zones with minimal manual input.

🔶 Key Features

Dynamic Support and Resistance Zones

Automatically detects significant support and resistance levels using pivot high and low calculations.

Offers ATR-based or percentage-based channel customization to cater to diverse trading styles.

Customizable Parameters

Lookback period for pivot calculations, strength threshold, and maximum stored pivots are fully adjustable.

Display options for showing specific numbers of recent support/resistance lines.

Intuitive Visualization

Highlights key support and resistance levels with color-coded lines and labels.

Includes percentage deviation from the current price for quick assessment.

Interactive Updates

Continuously updates support and resistance levels to reflect changing market dynamics.

Displays pivot points visually for enhanced clarity.

Can be used effectively on various timeframes, from intraday to daily and weekly charts.

🔶 Interpreting the Indicator

Identifying Key Levels

Support levels are indicated by green (lime) lines and resistance levels by red lines. The transparency of colors is adjustable for visual preference.

Labels display the exact price level and the percentage difference from the current price.

Strength Threshold

The "Minimum S/R Strength" parameter defines how frequently a level must be tested to be considered significant.

Higher strength values indicate zones that have been tested more frequently, suggesting stronger support or resistance.

Pivot Points

The indicator marks pivot high and low points on the chart to provide a visual representation of the calculated levels.

Dynamic Updates

The indicator adapts to the most recent price action. If the price moves above a resistance level or below a support level, the color of the lines and labels will dynamically change to reflect the current price positioning.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

HMA Gaussian Volatility AdjustedOverview

The "HMA Gaussian Volatility Adjusted" indicator introduces a unique combination of HMA smoothing with a Gaussian filter and two components to measure volatility (Average True Range (ATR) and Standard Deviation (SD)). This tool provides traders with a stable and accurate measure of price trends by integrating a Gaussian Filter smoothed using HMA with a customized calculation of volatility. This innovative approach allows for enhanced sensitivity to market fluctuations while filtering out short-term price noise.

Technical Composition and Calculation

The "HMA Gaussian Volatility Adjusted" indicator incorporates HMA smoothing and dynamic standard deviation calculations to build upon traditional volatility measures.

HMA & Gaussian Smoothing:

HMA Calculation (HMA_Length): The script applies a Hull Moving Average (HMA) to smooth the price data over a user-defined period, reducing noise and helping focus on broader market trends.

Gaussian Filter Calculation (Length_Gaussian): The smoothed HMA data is further refined by putting it into a Gaussian filter to incorporate a normal distribution.

Volatility Measurement:

ATR Calculation (ATR_Length, ATR_Factor): The indicator incorporates the Average True Range (ATR) to measure market volatility. The user-defined ATR multiplier is applied to this value to calculate upper and lower trend bands around the Gaussian, providing a dynamic measure of potential price movement based on recent volatility.

Standard Deviation Calculation (SD_Length): The script calculates the standard deviation of the price over a user-defined length, providing another layer of volatility measurement. The upper and lower standard deviation bands (SDD, SDU) act as additional indicators of price extremes.

Momentum Calculation & Scoring

When the indicator signals SHORT:

Diff = Price - Upper Boundary of the Standard Deviation (calculated on a Gaussian filter).

When the indicator signals LONG:

Diff = Price - Upper Boundary of the ATR (calculated on a Gaussian filter).

The calculated Diff signals how close the indicator is to changing trends. An EMA is applied to the Diff to smooth the data. Positive momentum occurs when the Diff is above the EMA, and negative momentum occurs when the Diff is below the EMA.

Trend Detection

Trend Logic: The indicator uses the calculated bands to identify whether the price is moving within or outside the standard deviation and ATR bands. Crosses above or below these bands, combined with positive/negative momentum, signals potential uptrends or downtrends, offering traders a clear view of market direction.

Features and User Inputs

The "HMA Gaussian Volatility Adjusted" script offers a variety of user inputs to customize the indicator to suit traders' styles and market conditions:

HMA Length: Allows traders to adjust the sensitivity of the HMA smoothing to control the amount of noise filtered from the price data.

Gaussian Length: Users can define the length at which the Gaussian filter is applied.

ATR Length and Multiplier: These inputs let traders fine-tune the ATR calculation, affecting the size of the dynamic upper and lower bands to adjust for price volatility.

Standard Deviation Length: Controls how the standard deviation is calculated, allowing further customization in detecting price volatility.

EMA Confluence: This input lets traders determine the length of the EMA used to calculate price momentum.

Type of Plot Setting: Allows users to determine how the indicator signal is plotted on the chart (Background color, Trend Lines, BOTH (backgroung color and Trend Lines)).

Transparency: Provides users with customization of the background color's transparency.

Color Long/Short: Offers users the option to choose their preferred colors for both long and short signals.

Summary and Usage Tips

The "HMA Gaussian Volatility Adjusted" indicator is a powerful tool for traders looking to refine their analysis of market trends and volatility. Its combination of HMA smoothing, Gaussian filtering, and standard deviation analysis provides a nuanced view of market movements by incorporating various metrics to determine direction, momentum, and volatility. This helps traders make better-informed decisions. It's recommended to experiment with the various input parameters to optimize the indicator for specific needs.