ATR Squeeze BackgroundThis simple but powerful indicator shades the background of your chart whenever volatility contracts, based on a custom comparison of fast and slow ATR (Average True Range) periods.

By visualizing low-volatility zones, you can:

* Identify moments of compression that may precede explosive price moves

* Stay out of choppy, low-momentum periods

* Adapt this as a component in a broader volatility or breakout strategy

🔧 How It Works

* A Fast ATR (default: 7 periods) and a Slow ATR (default: 40 periods) are calculated

* When the Fast ATR is lower than the Slow ATR, the background is shaded in blue

* This shading signals a contraction in volatility — a condition often seen before breakouts or strong directional moves

⚡️ Why This Matters

Many experienced traders pay close attention to volatility cycles. This background indicator helps visualize those cycles at a glance. It's minimal, non-intrusive, and easy to combine with your existing tools.

🙏 Credits

This script borrows core logic from the excellent “Relative Volume at Time” script by TradingView. Credit is given with appreciation.

⚠️ Disclaimer

This script is for educational purposes only.

It does not constitute financial advice, and past performance is not indicative of future results. Always do your own research and test strategies before making trading decisions.

Average True Range (ATR)

Advanced Supertrend StrategyA comprehensive Pine Script v5 strategy featuring an enhanced Supertrend indicator with multiple technical filters, risk management, and advanced signal confirmation for automated trading on TradingView.

## Features

- **Enhanced Supertrend**: Configurable ATR-based trend following with improved accuracy

- **RSI Filter**: Optional RSI-based signal filtering to avoid overbought/oversold conditions

- **Moving Average Filter**: Trend confirmation using SMA/EMA/WMA with customizable periods

- **Risk Management**: Built-in stop-loss and take-profit based on ATR multiples

- **Trend Strength Analysis**: Filters weak signals by requiring minimum trend duration

- **Breakout Confirmation**: Optional price breakout validation for stronger signals

- **Visual Interface**: Comprehensive chart plotting with multiple indicator overlays

- **Advanced Alerts**: Multiple alert conditions with detailed signal information

- **Backtesting**: Full strategy backtesting with commission and realistic execution

BERLIN-MAX 1V.5BERLIN-MAX 1V.5 is a comprehensive trading indicator designed for TradingView that combines multiple advanced strategies and tools. It integrates EMA crossover signals, UT Bot logic with ATR-based trailing stops, customizable stop-loss and target multipliers per timeframe, Hull Moving Averages with color-coded trends, linear regression channels for support and resistance, and a multi-timeframe RSI and volume signal table. This script aims to provide clear entry and exit signals for scalping and swing trading, enhancing decision-making across different market conditions.

RED E Support & ResistanceThe “RED-E Support & Resistance” indicator is designed to assist traders in visualizing key levels of support and resistance on a chart by employing ATR (Average True Range) to create dynamic horizontal zones. This indicator automatically plots robust support and resistance bands that can help identify potential areas where price may reverse, consolidate, or react. These levels are particularly beneficial for traders who employ concepts like Smart Money analysis, as they illustrate zones where institutional trading activity might occur.

How It Works:

• The indicator uses ATR-based calculations to determine the placement of the support and resistance zones. This approach accounts for market volatility, making the zones adaptive to changing conditions.

• The Zone Thickness parameter allows users to customize the width of the plotted zones, enhancing visibility and fitting them to their specific trading style.

• The support and resistance zones extend horizontally across the chart, providing clear reference points for potential price reactions.

Practical Application:

• Trend Analysis: Identify areas of significant price resistance and support to understand potential turning points or trends in the market.

• Risk Management: Use these zones to better inform stop-loss placements or set profit targets.

• Confirmation Tool: Combine the indicator with other technical analysis tools for confirmation of potential trade entries or exits.

Customization Options:

• Change the colors of the support and resistance zones for better integration with different chart themes.

• Adjust the ATR Length and Multiplier to fine-tune the sensitivity of the zones based on personal preferences and the characteristics of the asset being analyzed.

Disclaimer:

This indicator is for educational and informational purposes only. It is not intended to serve as investment advice or a recommendation to buy or sell any financial instrument. Always perform your own research and consider consulting with a financial professional before making trading decisions. Trading involves significant risk, and past performance does not guarantee future results.

3 hours ago

Release Notes

The “RED-E Support & Resistance” indicator is designed to assist traders in visualizing key levels of support and resistance on a chart by employing ATR (Average True Range) to create dynamic horizontal zones. This indicator automatically plots robust support and resistance bands that can help identify potential areas where price may reverse, consolidate, or react. These levels are particularly beneficial for traders who employ concepts like Smart Money analysis, as they illustrate zones where institutional trading activity might occur.

How It Works:

• The indicator uses ATR-based calculations to determine the placement of the support and resistance zones. This approach accounts for market volatility, making the zones adaptive to changing conditions.

• The Zone Thickness parameter allows users to customize the width of the plotted zones, enhancing visibility and fitting them to their specific trading style.

• The support and resistance zones extend horizontally across the chart, providing clear reference points for potential price reactions.

Practical Application:

• Trend Analysis: Identify areas of significant price resistance and support to understand potential turning points or trends in the market.

• Risk Management: Use these zones to better inform stop-loss placements or set profit targets.

• Confirmation Tool: Combine the indicator with other technical analysis tools for confirmation of potential trade entries or exits.

Customization Options:

• Change the colors of the support and resistance zones for better integration with different chart themes.

• Adjust the ATR Length and Multiplier to fine-tune the sensitivity of the zones based on personal preferences and the characteristics of the asset being analyzed.

Disclaimer:

This indicator is for educational and informational purposes only. It is not intended to serve as investment advice or a recommendation to buy or sell any financial instrument. Always perform your own research and consider consulting with a financial professional before making trading decisions. Trading involves significant risk, and past performance does not guarantee future results.

Combined Predictive Indicator### Combined Predictive Zones & Levels

This indicator is a powerful hybrid tool designed to provide a comprehensive map of potential future price action. It merges two distinct predictive models into a single, cohesive view, helping traders identify key levels of support, resistance, and areas of high confluence.

#### How It Works: Two Models in One

This script is built on two core components that you can use together or analyze separately:

**Part 1: Classic Range & Fibonacci Prediction**

This model uses classic technical analysis principles to project a potential range for the upcoming price action.

* **Highest High / Lowest Low:** It identifies the significant trading range over a user-defined lookback period.

* **Fibonacci Levels:** It automatically plots key Fibonacci retracement levels (e.g., 38.2% and 61.8%) within this range, which often act as critical support or resistance.

* **ATR & Average Range:** It calculates a "predicted" upper and lower boundary based on the average historical range and current volatility (ATR).

**Part 2: Advanced Predictive Ranges (Self-Adjusting Channels)**

This is a dynamic model that creates adaptive support and resistance zones based on a smoothed average price and volatility.

* **Dynamic Average:** It uses a unique moving average that only adjusts when the price moves significantly, creating a stable baseline.

* **ATR-Based Zones:** It projects multiple levels of support (S1, S2) and resistance (R1, R2) around this average, which widen and narrow based on market volatility. These zones often signal areas where price might stall or reverse.

#### Key Features:

* **Hybrid Model for Confluence:** The true power of this indicator lies in finding where the levels from both models overlap. A Fibonacci level aligning with a Predictive Range support zone is a much stronger signal.

* **Comprehensive Data Table:** A clean, on-chart table displays the precise values of all key predictive levels, allowing for quick reference and precise trade planning.

* **Multi-Timeframe (MTF) Capability:** The Advanced Predictive Ranges can be calculated on a higher timeframe, giving you a broader market context.

* **Fully Customizable:** All lengths, multipliers, and levels for both models are fully adjustable in the settings to fit any asset or trading style.

* **Clear Visuals:** All zones and levels are color-coded for intuitive and easy-to-read analysis.

#### How to Use:

1. Look for areas of **confluence** where multiple levels from both models cluster together. These are high-probability zones for price reactions.

2. Use the Predictive Range zones (S1/S2 and R1/R2) as potential targets for trades or as areas to watch for entries and exits.

3. Pay attention to the on-chart table for exact price levels to set limit orders or stop-losses.

**Disclaimer:** This script is an analytical tool for educational purposes and should not be considered financial advice. All trading involves risk. Past performance is not indicative of future results. Always use this indicator as part of a comprehensive trading strategy with proper risk management.

Feedback is welcome! If you find this tool useful, please leave a like.

Market DashboardMarket Dashboard — All-in-One Technical Indicator Panel

The Market Dashboard is a powerful visual tool that consolidates key technical indicators into a single on-chart table, helping traders make faster and more informed decisions. This script includes:

RSI — Detects overbought and oversold market conditions

MACD — Shows trend momentum and crossover signals

CVD (Cumulative Volume Delta) — Highlights buyer vs. seller pressure

Volume Analysis — Flags unusually high volume

ATR (Average True Range) — Displays current market volatility

Session Detector — Automatically identifies ASIAN, LONDON, or NEW YORK sessions based on UTC time

Fully Customizable — Adjust table position and text size to fit your chart layout

Designed for traders who want a clean, real-time snapshot of market dynamics, directly on the chart.

Supertrend AT v1.0### Overview

"Supertrend AT v1.0" is an automated trading strategy based on the Supertrend indicator, designed to detect trend reversals and execute entries accordingly. This script supports both **long and short** positions and includes customizable risk management features such as **RPT (Risk Per Trade)** and **RR (Risk/Reward ratio)**.

### Key Features

- 📈 **Supertrend-based Entry Logic**:

- Enters a **long position** when the Supertrend flips from red to green (downtrend → uptrend).

- Enters a **short position** when the Supertrend flips from green to red (uptrend → downtrend).

- 💰 **Auto-Calculated Position Sizing**:

- Quantity is automatically calculated to ensure that loss per trade (including commission) matches the specified risk percentage (RPT).

- 🎯 **Take-Profit and Stop-Loss**:

- Both targets are dynamically computed using the RR ratio and account for commission fees.

- 📊 **Visual Elements**:

- Entry, stop, and target prices are plotted on the chart.

- Real-time PnL and account equity are shown in a dashboard.

- Optional on-screen README guide explains the strategy and key terms.

### Inputs

- **RPT (%)**: Risk per transaction (based on account equity).

- **RR**: Reward-to-risk ratio.

- **Commission (%)**: Used in all calculations (must match the Properties tab).

- **Supertrend Settings**: Adjustable factor and length.

- **Market Decimal Places**: For accurate quantity rounding according to exchange rules.

- **Time Filter**: Set start and end time for trading logic activation.

### Risk Management Logic

This strategy calculates trade size and targets using a formula that considers both the price distance between entry and stop-loss and the effect of commission fees. This ensures:

- Consistent risk across trades

- Realistic take-profit levels

- Exchange-compliant order quantities

### Notes

- ⚠️ Be sure to set the **correct commission rate** and **decimal precision** for your exchange.

- ⚠️ If trade quantity is smaller than your exchange’s minimum unit, orders may be rejected.

- 🔧 For strategy to behave as intended in automation, double-check both **input tab** and **Properties tab** settings.

### Disclaimer

This strategy is for educational and research purposes only. It does not constitute financial advice. Always test on paper before using in a live environment.

ATR as % of CloseATR 14day period in % terms

the Normal ATR indicator by TV helps but this gives a clear idea as to the range in percentage terms as and when market rises to newer and newer highs

better than an absolute value

NAIFCHART_Osc+ ST+sqzmom# NAIFCHART Multi-Component Indicator: Trading Analysis Guide

## Overview

The NAIFCHART Osc+ ST+sqzmom indicator combines three proven technical analysis tools into a unified trading system. This indicator was developed and shared by the trading community at t.me providing traders with comprehensive market analysis through integrated momentum, trend, and volatility assessment.

## Core Components

**Wave Trend Oscillator**: Identifies overbought and oversold conditions using exponential moving averages. Key levels include overbought zones at 60 and 53, with oversold areas at -60 and -53. Crossover signals between the two oscillator lines generate entry opportunities, displayed as colored circles on the chart.

**Supertrend Indicator**: Determines market direction using Average True Range calculations with a 2.5 factor and 10-period ATR. Green lines indicate uptrends while red lines signal downtrends. The indicator adapts to market volatility, providing reliable trend identification across different market conditions.

**Squeeze Momentum**: Compares Bollinger Bands with Keltner Channels to identify consolidation periods and breakouts. Black squares indicate squeeze conditions (low volatility), green triangles signal upward breakouts, and red triangles mark downward breakouts.

## Trading Signals

**Long Entry Signals**: Green triangles from Squeeze Momentum, Supertrend line turning green, and bullish crossovers in Wave Trend Oscillator from oversold levels.

**Short Entry Signals**: Red triangles from Squeeze Momentum, Supertrend line turning red, and bearish crossovers in Wave Trend Oscillator from overbought levels.

## Risk Management Features

The indicator automatically calculates risk management levels using ATR-based calculations. Stop losses are positioned at 3x ATR distance, while three progressive take profit targets are set at 1x, 2x, and 3x ATR multiples. All levels are clearly displayed on the chart with colored lines and labels.

When trend direction changes, previous levels are automatically cleared and new calculations are generated, ensuring current market conditions are reflected in all risk parameters.

## Alert System

Comprehensive alerts include trend changes with complete trade setup details, squeeze release notifications for breakout opportunities, and trend weakness warnings for position management. Alert messages contain trading pair information, timeframe data, and all relevant entry and exit levels.

## Implementation Guidelines

**Timeframe Selection**: Higher timeframes (4-hour, daily) provide reliable signals for position trading. One-hour charts work well for day trading, while 15-30 minute timeframes enable scalping with enhanced risk management requirements.

**Risk Management**: Limit risk to 1-2% of capital per trade using the calculated stop loss levels for position sizing. Implement partial profit-taking at each target level while adjusting stops to protect gains.

**Market Adaptation**: The indicator's ATR-based calculations automatically adjust to market volatility. During high volatility periods, levels widen appropriately, while low volatility conditions result in tighter risk management parameters.

## Best Practices

Combine indicator signals with key support and resistance analysis for enhanced validation. Monitor volume to confirm breakout strength, particularly when Squeeze Momentum signals develop. Maintain awareness of economic events that may influence market behavior independent of technical signals.

The multi-component design provides internal confirmation through multiple signal alignment requirements, reducing false signals while maintaining reasonable trade frequency for active strategies.

## Community Resources

Access ongoing education and strategy discussions through the source community at t.me where traders share market analysis and optimization techniques for this indicator system.

## Conclusion

The NAIFCHART indicator offers a systematic approach to market analysis through proven technical components. Success requires understanding each element's functionality and implementing proper risk management principles. The community-driven development ensures practical relevance and ongoing support for traders seeking comprehensive market analysis tools.

Practice with demo accounts before live implementation to develop familiarity with signal interpretation and trade management procedures. The indicator's systematic approach reduces emotional decision-making while providing clear guidelines for entry, management, and exit strategies across various market conditions.

Fibonacci Range Detector ║ BullVision🔬 Overview

The Fibonacci Range Mapper is a dynamic technical tool designed to identify, track, and visualize price ranges using Fibonacci levels. Whether you're trading manually or prefer automated structure recognition, this indicator helps you contextualize market moves and locate key price zones with precision.

⚙️ Core Logic

🔍 Range Detection (Auto & Manual Modes)

In Auto mode, the indicator uses an advanced ZigZag system based on ATR or percentage thresholds to confirm market swings and construct Fibonacci-based ranges.

In Manual mode, traders can define their own swing low and high to generate precise custom ranges.

📐 Fibonacci Mapping

Each detected range is automatically plotted with key Fibonacci retracement levels — 0%, 25%, 50%, 75%, 100% — along with optional extensions (127.2% and 161.8%) to anticipate price continuations or reversals.

📋 Live Data Table

An integrated info panel dynamically displays crucial metrics:

• Range size

• Current price zone (Discount / Mid / Premium)

• Position within range (%)

• Distance to range extremes

• Range status (Pending or Confirmed)

🕰️ Historical Memory

Up to 20 past ranges can be stored and visualized simultaneously, helping traders recognize repeated price behaviors and contextual support/resistance levels.

🎨 Visual Highlights

Zones of interest (0–25% = Discount, 75–100% = Premium) are color-coded with custom transparency, and labels can be toggled for clarity. The current active range updates in real time as structure evolves.

🔧 User Customization

• Detection Method: Choose between ATR or % ZigZag for automated swing identification

• Confirmation Delay: Set how many bars to wait before confirming a new high

• Manual Overrides: Select exact price levels when you want full control

• Extensions & Labels: Toggle additional lines and info to suit your charting style

• Visual Table Position: Customize where the data table appears on screen

• Color Scheme: Define your own zone gradients for better visual interpretation

📈 Use Cases

This indicator is ideal for traders who want to:

• Identify value zones within local or macro price structures

• Plan trades around Fibonacci retracement and extension levels

• Detect shifts in market structure using an adaptive ZigZag logic

• Track recurring price ranges and historical reaction points

• Enhance technical confluence with clean, visual price mapping

⚠️ Important Notes

This tool is not a buy/sell signal generator — it is a visual framework for structure-based analysis.

Use it in conjunction with your existing strategy and risk management process.

Always confirm with broader context and multi-timeframe alignment.

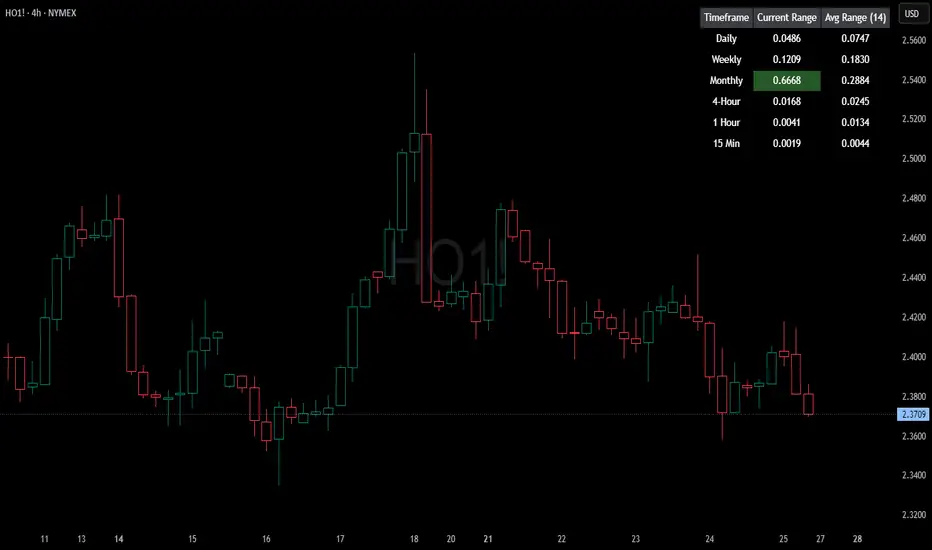

HTF Current/Average RangeThe "HTF(Higher Timeframe) Current/Average Range" indicator calculates and displays the current and average price ranges across multiple timeframes, including daily, weekly, monthly, 4 hour, and user-defined custom timeframes.

Users can customize the lookback period, table size, timeframe, and font color; with the indicator efficiently updating on the final bar to optimize performance.

When the current range surpasses the average range for a given timeframe, the corresponding table cell is highlighted in green, indicating potential maximum price expansion and signaling the possibility of an impending retracement or consolidation.

For day trading strategies, the daily average range can serve as a guide, allowing traders to hold positions until the current daily range approaches or meets the average range, at which point exiting the trade may be considered.

For scalping strategies, the 15min and 5min average range can be utilized to determine optimal holding periods for fast trades.

Other strategies:

Intraday Trading - 1h and 4h Average Range

Swing Trading - Monthly Average Range

Short-term Trading - Weekly Average Range

Also using these statistics in accordance with Power 3 ICT concepts, will assist in holding trades to their statistical average range of the chosen HTF candle.

CODE

The core functionality lies in the data retrieval and table population sections.

The request.security function (e.g., = request.security(syminfo.tickerid, "D", , lookahead = barmerge.lookahead_off)) retrieves high and low prices from specified timeframes without lookahead bias, ensuring accurate historical data.

These values are used to compute current ranges and average ranges (ta.sma(high - low, avgLength)), which are then displayed in a dynamically generated table starting at (if barstate.islast) using table.new, with conditional green highlighting when the current range is greater than average range, providing a clear visual cue for volatility analysis.

Minimalist Trend & Risk For 5-Min Timeframe

Of course. Here is a professionally written TradingView description for your indicator, following the specified formatting and incorporating the strategy you outlined.

Minimalist Trend & Risk For 5-Min Timeframe

Overview

This is a clean, on-chart visual tool designed to identify high-probability entries and manage risk, specifically tailored for a 5-minute scalping or day trading strategy. It combines a higher-timeframe trend anchor with a current-timeframe trigger line and a volatility-based stop loss level, keeping your chart uncluttered and your decisions clear.

Visual Components

Trend EMA (50-period, 15-min): This is your main trend guide. The thick, colored line represents the 50 EMA from the 15-minute chart.

Green: Confirmed uptrend.

Red: Confirmed downtrend.

Gray: Neutral or consolidating market.

Price EMA (21-period, 5-min): The thin white line is the 21 EMA based on your current chart (5-minute). This acts as a dynamic trigger line that price must reclaim after a pullback.

Stop Loss Zone (ATR-based): The thin red line provides a suggested stop loss level based on current market volatility (ATR). It automatically appears below price in an uptrend and above price in a downtrend, helping you define your risk on every trade.

How To Use for a Long Entry Strategy

The strategy is to trade pullbacks in the direction of the higher-timeframe trend. This indicator helps you visualize each step of the setup.

1. Identify the Trend: Wait for the main Trend EMA (the thick line) to be green. This confirms you are in an established uptrend on the 15-minute timeframe and should only be looking for long entries.

2. Wait for a Pullback: The core of the strategy is patience. Wait for a 5-minute candlestick to pull back and close below the 15-minute Trend EMA. This confirms a temporary dip within the larger uptrend, offering a better entry price.

3. Spot the Entry Trigger: After the pullback, the entry signal occurs when a 5-minute candlestick closes back above the faster, white Price EMA (21-period). This signals that momentum is returning in the direction of the main trend.

4. Manage Your Risk: Use the red Stop Loss Zone line that appears below your entry as a guide to set your initial stop loss. This helps ensure your risk is managed dynamically based on current volatility.

This indicator simplifies a powerful pullback strategy by plotting all the necessary components directly on your chart, allowing for quick and disciplined trade execution.

ATR Circle PlotTitle: ATR Circle Plot

Short Title: ATR Circle Plot

Description:

ATR Circle Plot is a dynamic overlay indicator that visualizes volatility-based levels around the open price of each bar, using the Average True Range (ATR). It plots two customizable levels—Upper and Lower ATR—calculated by multiplying the ATR by a user-defined factor (default: 1.0) and adding/subtracting it from the open price. These levels are displayed as colored circles on the chart, ideal for identifying potential breakout or stop-loss zones. A movable table summarizes the ATR value, Upper Level, and Lower Level with tick precision, and a new toggleable label feature displays these values directly on the chart for quick reference.

Perfect for traders in volatile markets like forex, futures, or stocks, this indicator helps set risk parameters or spot key price levels. Users can adjust the ATR timeframe, length, multiplier, table position, and circle colors to suit their strategy. The optional chart labels enhance usability by overlaying ATR metrics at the latest price levels, reducing the need to check the table during fast-moving markets.

Key Features:

Plots Upper and Lower ATR levels as colored circles around the open price.

Toggleable table (top/bottom, left/right) showing ATR and level values in ticks.

Optional chart labels for ATR, Upper, and Lower levels, toggleable via input.

Customizable ATR length, multiplier, timeframe, and colors for flexibility.

Lightweight and compatible with any chart timeframe.

How to Use:

Add the indicator to your chart and adjust the ATR length, multiplier, and timeframe as needed. Enable/disable the table or labels based on your preference. Use the Upper and Lower ATR levels as dynamic support/resistance or stop-loss guides. For example, place stops beyond the Upper/Lower levels or target breakouts when price crosses them. Combine with trend or momentum indicators for a robust setup.

Note: Leave the ATR Timeframe input empty to use the chart’s timeframe, or specify a higher timeframe (e.g., “D” for daily) for broader volatility context. Ensure your chart’s tick size aligns with the asset for accurate table values.

Tags: ATR, volatility, support resistance, stop loss, table, labels, breakout

Category: Volatility

Ultimate ATR ProUltimate ATR Pro - Professional Volatility Analysis Tool

Unlock Market Turning Points with Precision Volatility Analysis

Key Features

1. Advanced ATR Calculation Engine

4 MA Types: RMA (Wilder's), SMA, EMA, WMA

Customizable Period: Adjust ATR length (default: 14)

Multi-Timeframe Compatible: Works on all chart intervals

2. Smart Volatility Extremum Detection

Low Volatility Signals: Identifies ATR contraction periods

High Volatility Signals: Detects ATR expansion phases

Custom Lookback Period: Set detection window (10-500 bars)

3. Professional Divergence System

Bullish Divergence: Price ↑ while ATR ↓ (trend continuation signal)

Bearish Divergence: Price ↓ while ATR ↑ (trend acceleration signal)

Visual Connection Lines: Dotted lines highlight price-ATR relationships

4. Visual Extreme Value Lines (NEW!)

Lowest ATR Line: Customizable dotted line showing minimum volatility level

Highest ATR Line: Customizable dotted line marking maximum volatility level

Dynamic Positioning: Auto-updates with each new bar

5. Complete Customization System

Full Color Control:

Signal markers (low/high volatility)

Divergence labels

ATR line

Extreme value lines

Background highlights

Toggle Features: Enable/disable any visual element

6. Intelligent Alert System

Dual Alert Types:

Volatility Extremes (Low/High ATR)

Divergence Signals (Bullish/Bearish)

Smart Cooldown: Prevent alert fatigue with adjustable cooldown period

Visual Alert Tags: Color-coded notifications at chart top

7. Professional Dashboard

Real-time status monitoring:

Current volatility state

Cooldown timers

Extreme ATR values

Divergence detection status

Color-coded for instant recognition

How Traders Benefit

Strategic Applications

markdown

复制

| SIGNAL | MARKET CONDITION | TRADING IMPLICATION |

|-----------------------|---------------------------|------------------------------------|

| Low Volatility | Contraction/Consolidation | Prepare for breakout strategies |

| High Volatility | Expansion/Climax | Watch for reversals or pauses |

| Bullish Divergence | Price↑ ATR↓ | Trend continuation opportunity |

| Bearish Divergence | Price↓ ATR↑ | Trend acceleration warning |

| Lowest ATR Line Break | Volatility breakout | Confirm directional movement |

Risk Management Tools

ATR-Based Position Sizing: Use extreme values to calculate optimal trade size

Dynamic Stop Loss: Adjust stops based on current volatility regime

Volatility Filtering: Avoid trading during uncertain high-volatility periods

Setup Recommendations

Parameter Guide

pine

复制

length: 14 // Standard ATR period

lookback: 50 // Optimal for swing trading

cooldownPeriod: 14// Balanced alert frequency

minLineColor: #00C853 // Bright green for low volatility

maxLineColor: #FF3D00 // Bright red for high volatility

Professional Configurations

Day Trading: Lookback=20-30, Cooldown=5-10

Swing Trading: Lookback=50-100, Cooldown=10-20

Position Trading: Lookback=100-200, Cooldown=20-50

Why Choose Ultimate ATR Pro?

"Transforms complex volatility analysis into clear, actionable visual cues - the essential tool for breakout traders and risk managers alike."

Install Now To:

Spot consolidation before big moves

Identify exhaustion at trend extremes

Automate volatility-based position sizing

Receive instant alerts at critical volatility turns

Gain professional-grade insights into market dynamics

Master market rhythms with the most advanced ATR analysis tool on TradingView!

Compatibility: Works flawlessly across stocks, forex, crypto, and commodities on all timeframes.

Version: 2.0 (Enhanced with Extreme Value Lines)

Category: Volatility Analysis | Risk Management | Professional Trading

ATR % of yesterday close with SMA (Bull/Bear colored)This script visualizes the Average True Range (ATR) as a percentage of a user-selected price point for a quick view of volatility.

ATR % values are plotted as a color-coded histogram. Bullish days (close > prior close) paint the bar green; bearish days (close < prior close) paint it red; unchanged days are gray.

Two simple moving average (SMA) overlays to reveal volatility trends.

Variables:

Histogram bars represent ATR as a % of one of:

- Previous Close (default option)

- Previous Open

- Today Close

- Today Open

Two SMA lines (default: blue for 20-period, orange for 5-period) shown on ATR % for trend/range regime tracking.

Optionally display the ATR % in continuous line (yellow)—hidden by default.

If you find it helpful, feel free to share any feedback and how you incorporate it into your trading strategy with the community!

Ultimate ATR Extreme DetectorUltimate ATR Extreme Detector

Professional Volatility Analysis Tool for Strategic Trading

Discover Market Turning Points with Precision

Key Features

Smart Extremum Detection: Identifies when ATR reaches its highest or lowest point in your specified lookback period

Quad Visual Alert System:

▲ Green bottom triangles for low volatility signals

▼ Red top triangles for high volatility signals

Background color highlighting for instant state recognition

Status panel showing current volatility extremes

Dual Alert Modes:

TradingView native alerts ("ATR Low/High Signal")

Visual chart alerts with period details (e.g., "Alert: ATR Low (50 bars)")

4 Calculation Methods: RMA (Wilder's), SMA, EMA, and WMA

Fully Customizable:

Adjustable ATR period (default: 14)

Variable lookback window (default: 50)

Toggle features on/off via intuitive input settings

How It Works

The indicator scans volatility extremes using proprietary logic:

Calculates True Range using selected method (RMA/SMA/EMA/WMA)

Compares current ATR value against historical data

Flags critical moments when:

Volatility contracts to N-period lows (prepare for breakouts)

Volatility expands to N-period highs (watch for trend exhaustion)

Strategic Applications

markdown

复制

| SIGNAL | MARKET CONDITION | TRADING IMPLICATION |

|------------------|-----------------------|--------------------------------|

| Low Volatility | Contraction/Consolidation | Anticipate breakout moves |

| High Volatility | Expansion/Climax | Prepare for reversals or pauses |

Position Sizing: Use ATR values to determine optimal stop distances

Entry Timing: Combine with price action at key support/resistance

Risk Management: Adjust stops dynamically based on volatility regime

Optimization Guide

Day Trading: Short lookback (20-30 periods)

Swing Trading: Medium lookback (50-100 periods)

Position Trading: Long lookback (100-200 periods)

Volatility Analysis: Compare multiple timeframes simultaneously

Professional Setup Recommendations

Combine with:

Breakout Confirmation: Volume spikes, chart patterns

Reversal Signals: RSI divergence, candlestick reversals

Volatility Filters: Bollinger Band contraction, Keltner Channel breakout

Compatibility: Works flawlessly across FX, stocks, crypto, and commodities on all timeframes.

Why Traders Choose This Indicator

"Transforms complex volatility analysis into clear, actionable visual cues – the essential tool for breakout traders and risk managers alike."

Install Now to:

Spot consolidation before big moves

Identify exhaustion at trend extremes

Automate volatility-based position sizing

Receive instant alerts at critical volatility turns

Master market rhythms with professional-grade volatility intelligence!

Qossai Stock Info### Qossai Stock Info Indicator

This indicator provides a concise overlay of essential stock information directly on your chart, presented in a clean, organized table. Designed for quick glances, it helps traders and investors stay informed about key fundamental and volatility metrics of the currently viewed symbol.

**Key Features:**

* **Symbol/Ticker Display:** Clearly shows the ticker of the asset you are currently viewing.

* **Dynamic Market Capitalization (Market Cap):** Automatically calculates and displays the market capitalization in a readable format (Millions, Billions, or Trillions), providing instant insight into the company's size.

* **Average True Range (ATR) as Percentage:** Shows the 14-day Average True Range (a measure of volatility) as a percentage of the closing price, helping you gauge the typical price movement. The ATR period is customizable.

* **Earnings Countdown:** Keep track of upcoming events with a precise countdown displaying the number of days remaining until the next earnings announcement. This feature can be toggled on or off via the indicator's settings.

* **Clean Table Format:** All information is presented neatly in a table with a subtle black background, ensuring readability without cluttering your main chart view.

**How to Use:**

Simply add the "Qossai Stock Info" indicator to your chart. You can adjust the ATR length and toggle the earnings countdown visibility from the indicator's settings.

**Purpose:**

This tool aims to simplify access to critical stock data, empowering users to make quicker, more informed decisions by having vital information readily available on their screen.

---

Risk Context + Position SizingWhat This Indicator Does (And Doesn't Do)

This is NOT a buy/sell signal indicator. Instead, it's a risk management tool that helps you understand two critical things:

How volatile the market is right now (compared to recent history)

How much you should risk on your next trade based on that volatility

The Core Problem It Solves

Imagine you always risk the same amount on every trade - say $100. But sometimes the market is calm and predictable, other times it's wild and unpredictable. This indicator says: "Hey, the market is going crazy right now - maybe only risk $70 instead of your usual $100."

How It Works

Measures Market "Nervousness"

Uses ATR (Average True Range) to measure how much prices typically move each day

Compares today's volatility to the past 100 days

Shows you a percentile (0-100%) - higher = more volatile

Categorizes Risk Environment

LOW (green): Market is calm, you can size up slightly

NORMAL: Standard conditions, use your normal position size

HIGH (red): Market is jumpy, reduce your position size

EXTREME (dark red): Market is in chaos, significantly reduce size

Important Disclaimers

This doesn't predict price direction - it only measures current market stress

You still need a trading strategy - this just helps you size it properly

Past volatility doesn't guarantee future volatility

Always combine with proper stop losses and risk management

ATR Dynamic Stop (Table + Plot + ATR %)📊 This script displays dynamic stop levels based on ATR, designed for active traders.

Features:

- Shows long and short stop levels (price ± ATR × multiplier).

- Displays values as a floating table on the top-right corner.

- Optional plot lines directly on the chart.

- Option to calculate based on realtime price or last close.

- Displays the ATR value both in price units and as a percentage of the selected price.

- Fully customizable table: text size, text color, background color.

Inputs:

- ATR Multiplier and Length.

- Show/hide stop lines on the chart.

- Select price source (realtime or last close).

- Table appearance options.

Ideal for:

- Traders who want a clear visual stop guide.

- Combining volatility with risk management.

Trimmed ATR🧠 **Brief Description**:

Trimmed ATR is a modified volatility indicator that removes extreme values from the ATR calculation. This makes it more reliable for analyzing market conditions and filters out "noise" spikes. It is particularly useful for setting stop-losses and in strategies sensitive to false volatility.

🧾 **How Does Trimmed ATR Work?**

📌 For each bar:

- True Range (TR) is calculated.

- A sliding window of the last N TR values (where N = length) is stored.

- The TR list is sorted, and trimPercent % is cut off from each side:

- The smallest and largest values are removed.

- The remaining values are averaged → Trimmed ATR.

🔍 **Why Is This Important?**

Regular ATR can be distorted by outliers:

- A single spike can sharply inflate the ATR.

- This creates a false impression of market volatility.

🎯 Trimmed ATR solves this by eliminating the impact of anomalies, providing a more stable and accurate volatility measure.

📈 **What Does It Mean If Trimmed ATR Is Higher or Lower Than Regular ATR?**

🔵 **Trimmed ATR is lower than ATR** — this is normal:

- There are isolated TR spikes (high volatility on 1–2 bars).

- ATR increases, including these outliers.

- Trimmed ATR discards them → reflects the true average market background.

🧠 This is the most common case, indicating: a spike occurred, but the market is generally calm.

🟠 **Trimmed ATR is higher than ATR** — a rare but important signal:

- There were artificially low TR values (very small movements).

- ATR becomes too low.

- Trimmed ATR discards these "quiet" periods → provides a more realistic volatility estimate.

⚠️ This may indicate:

- Hidden pressure.

- Preparation for a breakout from a tight range.

- Underestimated volatility.

💡 **Applications**:

- **Trailing Stop**: Trimmed ATR helps avoid stop triggers due to noise.

- **Trend Filter**: Better reflects the "true" market dynamics.

- **Strategy Backtesting**: Eliminates distortions in volatility calculations.

Assaf ATRATR (Average True Range) is a volatility indicator developed by J. Welles Wilder. It measures how much an asset moves (in price), on average, during a specific time period. It does not indicate direction, only the degree of price volatility.

ATR Trailing Stop with ATR Targets [v6]What the Indicator Does

This custom TradingView indicator is designed for active traders who want to automate and visualize their trailing stop management and target setting, using true market volatility. It combines the Average True Range (ATR) with dynamic market structure logic to:

Trail a stop-loss behind major swings in real time, using 2×ATR (adjustable) from the highest high in uptrends or the lowest low in downtrends.

Flip trading bias between bullish and bearish when the stop is breached.

Identify and plot three profit targets (at 1, 2, and 3 ATR from the breakout/flip point) after every stop-flip, helping traders scale out or set take-profits objectively.

Maintain a visible presence on your chart every bar to avoid indicator errors, with color and labeling for clear distinction between long/short phases.

How the Indicator Works

1. ATR Calculation

ATR Period and Multiplier: You select your preferred ATR length (default is 14 bars) and a multiplier (default is 2.0).

Volatility Adjustment: ATR measures the average "true" bar range, so the trailing stop and targets adapt to current volatility.

2. Trailing Stop Logic

Uptrend (bullish bias): The indicator tracks the highest high made since the last bearish-to-bullish flip and sets the stop at - .

The stop only raises (never lowers) during an uptrend, protecting gains in strong moves.

Downtrend (bearish bias): Tracks the lowest low made since the last bullish-to-bearish flip, with stop at + .

The stop only lowers (never raises) in a downtrend.

Flip Point: If price closes through the trailing stop, the current bias “flips,” and the logic reverses (bullish to bearish or vice versa). At the new close, flip price and bar index are stored for target calculation.

3. ATR Targets after Flip

After each stop flip:

Three targets—based on the new close price—are calculated and plotted:

Long flip (new bull bias): Target1 = close + 1×ATR, Target2 = close + 2×ATR, Target3 = close + 3×ATR.

Short flip (new bear bias): Target1 = close - 1×ATR, Target2 = close - 2×ATR, Target3 = close - 3×ATR.

These targets help with scaling out, partial profit-taking, or setting automated orders.

4. Visual Feedback

Trailing stop line: Green for long bias, red for short bias.

Targets: Distinct color-coded circles at 1, 2, 3 ATR levels from the most recent flip.

Flip Labels: Mark the bar and price where bias flipped (“Long Flip” or “Short Flip”) for quick pattern recognition.

Subtle background shading: Ensures TradingView's requirement for “indicator output every bar.”

How to Use This Indicator

Parameter Setup

ATR Period and Multiplier: Adjust to match the timeframe and volatility of your instrument.

Lower periods/multipliers for short-term/volatile trading.

Higher values for smoother signals or higher timeframes.

Starting Trend: Set to match the expected initial bias if the instrument has strong trend characteristics.

Trading Application

1. Daily Bias Approach

Establish your bias in line with your trading plan (e.g., only trade long if price is above the previous day's high, short below the previous day's low).

Only look for trades in the indicator's current bias direction, as expressed by the stop and background color.

2. Entry

Use the indicator as a real-time confirmation or trailing stop for your entries.

Breakout: Enter when price establishes the current bias, using the trailing stop as your risk level.

Reversal: Wait for a bias flip after an extended move; enter in the direction of the new bias.

VWAP Rebound: Combine with a VWAP bounce—enter only if the indicator bias supports your direction.

3. Exits/Targets

Trailing stop management: Move your stop according to the plotted line; exit if your stop is hit.

Profit-taking: Scale out or take profits as price approaches each ATR-based target.

Use the dynamic labeling to identify reversal flips and reset your plan if stopped or the bias changes.

4. Market Context

Filter and frame setups by watching correlated indicators (DXY, VIX, AUDJPY, put/call ratio) and upcoming news; trade only in the daily bias direction for best consistency.

5. Practical Tips

Combine this indicator with your custom watchlist and alert settings to get notified on flips or targets.

Review the last label ("Long Flip"/"Short Flip") and targets to plan partial exits.

Remember: ATR adapts to volatility, so the stop and targets stay proportionate even when price action shifts.

ATR Trend Strategy + KAMA FilterATR Trend Strategy with XMA KAMA Filter

Strategy Description

This strategy combines a dynamic ATR trailing stop with an XMA KAMA filter to precisely detect trends and generate reliable entry signals.

It uses a two-step trend confirmation system:

1️⃣ ATR Trailing Stop

Based on the Average True Range (ATR), this trailing stop automatically adapts to market volatility.

It determines whether the market is in a bullish or bearish phase by comparing the current price to the ATR trailing stop level.

2️⃣ KAMA Filter (XMA Version)

KAMA (Kaufman Adaptive Moving Average) provides an additional trend filter.

This XMA version of KAMA avoids the traditional fast/slow parameters and instead dynamically calculates the ratio of signal to market "noise", helping to reduce false signals and over-sensitivity.

How It Works

Long Signal:

Price is above both the ATR trailing stop and the KAMA (XMA) line.

Short Signal:

Price is below both the ATR trailing stop and the KAMA (XMA) line.

What Makes This Strategy Different?

Unlike many classic strategies that rely on simple moving averages, this system uses an adaptive KAMA filter that responds better to changing market conditions and volatility.

The ATR trailing stop automatically adjusts to current market volatility, providing an extra layer of protection against false breakouts.

By combining these tools, this strategy offers:

Precise trend filtering

Avoidance of false breakouts and noise

Dynamic adjustment to market conditions

How to Use

Apply the strategy to any market chart (Forex, stocks, crypto, indices, etc.)

Adjust the ATR and KAMA parameters to match your trading plan

Use the TradingView Strategy Tester to evaluate performance before live trading

Who Is This For?

Swing traders and trend followers

Traders looking for clean, filtered signals with reduced noise

Medium-term traders seeking a system that adapts to market dynamics

Additional Info: Heikin Ashi Compatibility

This strategy is fully compatible with Heikin Ashi candles.

By applying it to a chart with Heikin Ashi candles, traders can further reduce market noise and enhance trend visualization.

The combination of ATR trailing stop + XMA KAMA filter + Heikin Ashi smoothing provides an even cleaner trend-following system, minimizing false signals and improving decision-making clarity.