ER-Adaptive ATR [Loxx]Average True Range (ATR) is widely used indicator in many occasions for technical analysis. It is calculated as the RMA of true range. This version adds a "twist": it uses Perry Kaufman's Efficiency Ratio to calculate adaptive true range

You can use this indicator the same way you'd use the standard ATR.

Average True Range (ATR)

Strategy Myth-Busting #1 - UT Bot+STC+Hull [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our first one is an automated version of the " The ULTIMATE Scalping Trading Strategy for 2022 " strategy from " My Trading Journey " who claims to have achieved not only profits but a 98.3% win rate. As you can see from the backtest results below, I was unable to substantiate anything close to that that claim on the same symbol (NVDA), timeframe (5m) with identical instrument settings that " My Trading Journey " was demonstrating with. Strategy Busted.

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

This strategy uses a combination of 3 open-source public indicators:

UT Bot Alerts by QuantNomad

STC Indicator - A Better MACD By shayankm

Basic Hull Ma Pack tinkered by InSilico

Trading Rules:

5 min candles

Long

New Buy Signal from UT Bot Alerts Strategy

STC is green and below 25 and rising

Hull Suite is green

Short

New Sell Signal from UT Bot Alerts Strategy

STC is red and above 75 and falling

Hull Suite is red

[MT Trader] Backtest template w/ Supertrend Strategy---EN: In this strategy template you will find some functions already pre-programmed to be used in your strategies to speed up the programming process, among them we can highlight the default stop loss and take profit functions, which will help to set easily and quickly, defining the price range in which we want to prevent large losses or protect our profits from unexpected market movements.

🔴 Stop Loss: Among the functions of the stop loss are the 4 most known, first we have the fixed percentage range (%) and price ($), when the price reaches this fixed price will limit the losses of the operation avoiding larger losses, then we have the average true range (ATR), a moving average of true range and X period that can give us good reference points to place our stop loss, finally the last point higher or lower is the most used by traders to place their stop loss.

In addition, the price range between the entry and stop loss can be converted into a trailing stop loss.

🟢 Take Profit: We have 3 options for take profit, just like stop loss, the fixed range of percentage(%) and price($), are available, in addition to this we have the 1:# ratio option, which multiplies by X number the range between the entry and stop loss to use it as take profit, perfect for strategies that use ATR or last high/low point for their strategy.

📈 Heikin Ashi Entrys: The heikin ashi entries are trades that are calculated based on heikin ashi candles but their price is executed in Japanese candles, thus avoiding the false results that occur in heikin candlestick charts, making that in certain cases better results are obtained in the strategies that are executed with this option compared to Japanese candlesticks.

📊 Dashboard: A more visual and organized way to see the results and data needed for our strategy.

Feel free to use this template to program your own strategies, if you find bugs or want to request a new feature let me know in the comments or through my telegram @hvert_mt

__________________________________________________________________________________________________________________________________________________

---ES: En esta plantilla de estrategia podrás encontrar algunas funciones ya pre-programadas para ser usadas en tus estrategias para acelerar procesos de programación, entre ellas podemos destacar las funciones por defecto de stop loss y take profit, que ayudaran a establecer de manera fácil y rápida, definiendo los rango de precio en los que queremos prevenirnos de perdidas grandes o proteger nuestras ganancias de movimientos inesperados del mercado.

🔴 Stop Loss: Entre las funciones del stop loss están las 4 más conocidas, en primer lugar tenemos el rango de porcentaje fijo(%) y el precio($), cuando el precio alcance este precio fijo se limitaran las perdidas de la operación evitando perdidas mas grandes, después tenemos el promedio de rango verdadero(ATR), una media móvil del rango verdadero y X periodo que nos puede dar buenos puntos de referencia para colocar nuestro stop loss, por ultimo el ultimo punto mas alto o mas bajo es de los mas usados por los traders para colocar su stop loss.

Adicional a esto, el rango de precio entre la entrada y el stop loss se puede convertir en un trailing stop loss.

🟢 Take Profit: Tenemos 3 opciones para take profit, al igual que en el stop loss, el rango fijo de porcentaje(%) y precio($) se encuentran disponibles, adicional a esto tenemos la opción de ratio 1:#, que multiplica por X numero el rango entre la entrada y el stop loss para usarlo como take profit, perfecto para estrategias que usen ATR o ultimo punto alto/bajo.

📈 Entradas Heikin Ashi: Las entradas Heikin Ashi son trades que son calculados en base a las velas Aeikin Ashi pero su precio esta ejecutado a velas japonesas, evitando así los falsos resultados que se producen en graficas de velas Heikin, esto haciendo que en ciertos casos se obtengan mejores resultados en las estrategias que son ejecutadas con esta opción en comparación con las velas japonesas.

📊 Panel de Control: Una manera mas visual y organizada de ver los resultados y datos necesarios de nuestra estrategia.

Siéntete libre de usar esta plantilla para programar tus propias estrategias, si encuentras errores o quieres solicitar una nueva función házmelo saber en los comentarios o a través de mi Telegram: @hvert_mt

ATR-Adaptive JMA [Loxx]Not many know that the JMA (Jurik Moving Average) is already an adaptive indicator (it is adapting using the usual market volatility monitoring mode). Hence, making it adaptive "once more" makes it double adaptive. Fro the adaptivity in this case, we are use ATR (Average True Range) to make the JMA double adaptive. The ATR period is the same as the JMA period (there is no separate setting for that) so the usage of the indicator is as simple as it gets.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Included:

Bar coloring

ATR Multiplier OverlayFunctions like ATR Multiplier by bjr117, but is overlaid on chart to make your setting of stop-loss and take profit levels easier.

Simply set the multiplier, script will take the ATR for that time with whatever setting, multiply it with your input and plot that number plus and minus each candle close.

SST-V2this scrips is combination of Moving average that you can alter with buy and Sell signal.

it is easy to use. u can go with the trend as of the bar color turn to blue it is indcate tha ur in bullish trend

and with turn to red it indicate that your in down trend.

Use Ema 200 for trend confluences

hope you like it.

thank's

Sadflute

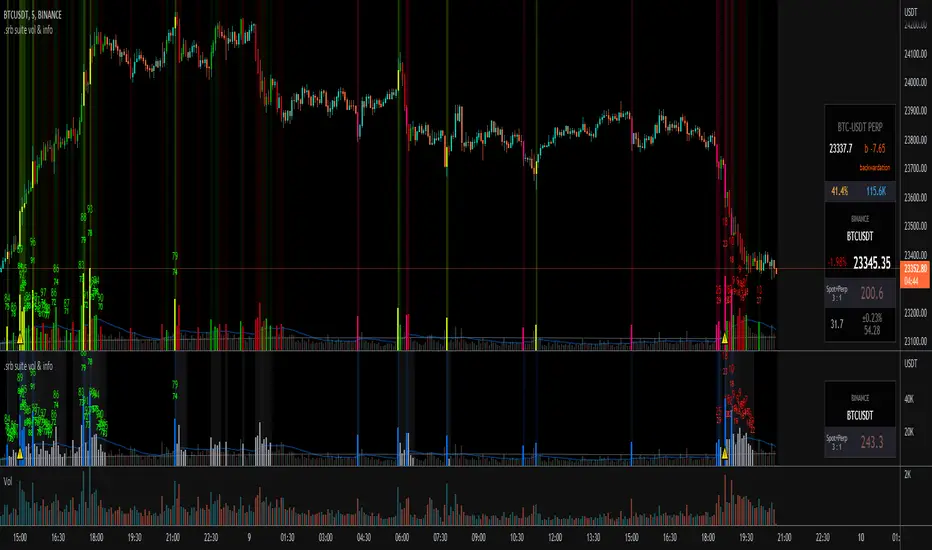

.srb suite vol & infoThe volume indicator

what can replace the built-in volume indicator and It also has some useful features.

and designed to work as overlay in the same pane with open-source indicator by default.

Regular volume Indicator

Volume SMA plot

Large Volume ! emphasize by color & mark.

Ultra Volume ! overlay marking ; x2 x4 x6 lager than regular average volume. it will help you can take the reversal

BTC-agg. Volume

4 BTC-spot & 4 BTC-PERP volume aggregated.

It might helps you don't miss out on important volume flows.

Weighted to spot trading volume when using PERP+spot volume.

If enabled, BTC-agg.Vol automatically applied when selecting BTC-pair.

Information panel (optimized for crypto-currency)

BTC-PERP price & delta (when Binance:BTCUSDT selected)

BTC dominance, Binance:BTCUSDTPERP OI

Symbol, Price, Daily up/down

ATR14 (for checking current volatility)

Recommended setup for .srb suite

tradingview | chart setting > Appearance > Top margin 0%, Bottom margin 0% for optimized screen usage

tradingview | chart setting > Appearance > Right margin 57

.srb suite vol & info --> Visual Order > Bring to Front

.srb suite vol & info --> Pin to scale > No scale (Full-screen)

Volatility Pivot Support and Resistance [Loxx]Volatility Pivot Support and Resistance calculates "pivots" (support/resistance lines) based on current symbol/timeframe Average True Range calculated volatility.

What is Average True Range?

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

The true range indicator is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges.

Included:

-Bar coloring

ATR-Stepped PDF MA [Loxx]ATR-Stepped PDF MA is and ATR-stepped moving average that uses a probability density function moving average.

What is Probability Density Function?

Probability density function based MA is a sort of weighted moving average that uses probability density function to calculate the weights.

Included:

-Toggle on/off bar coloring

-Toggle on/off signals

-Alerts long/short

Chandelier Exit - Heikin AshiThis is a redesign of the Chandelier Exit indicator. It removes stupid transitions between Chandelier Exit' states and highlights initial points for both lines.

This indicator was originally developed by Charles Le Beau and popularized by Dr . Alexander Elder in his book "Come Into My Trading Room: A Complete Guide to Trading" (2002).

In short, this is a trailing stop-loss based on the Average True Range (ATR).

If "Heikin Ashi for calculation" is checked, then ATR and buy/sell signals are calculated based on heikin ashi candles.

You don't need to change bar style to heikin ashi.

Thanks to everget for the initial version.

ADR% / ATR / Market CapDisplays the following values in a table in the upper right corner of the chart:

ADR%: Average daily range (in percent).

ATR: Average true range (hidden by default).

Market Cap: Total value of all a company's shares of stock.

All values are calculated based on daily bars, no matter what time frame you are currently viewing. Doesn't work for time frames >1D, which is why the table is not shown on weekly/monthly charts.

Credit to MikeC / TheScrutiniser and GlinckEastwoot for ADR% formula, and ArmerSchlucker for the original script which includes LoD Dist . instead of Market Cap.

Rets High/Low (2.0 Special Uncensored Edition)This script can be used as a visual aid in seeing the last highs and lows of price in a specific time period. It automatically updates the plots if new highs or lows are made within the given lookback period.

This is a fairly basic version currently, with new added features coming in future updates such as range between high/low and half and whole number detection.

Spinn ATR targetNot quite the usual approach to plotting targets on the chart, where the price will come with a given probability.

The indicator draws targets by studying the ATR of the target timeframe. More precisely, this is not exactly an ATR - the price move is taken from the closing price of the previous bar and is calculated both up and down separately.

The settings specify the percentage used to calculate the price move, at which the specified percentage of bars reached this price move in the past.

Simply put, if we set 50% in the settings, this means that a line will be drawn at the level at which the price reached this level in 50% of cases over a given period.

--

Не совсем обычный подход к построению целей на графике, куда цена придет с заданной вероятностью.

Индикатор рисует цели, изучая ATR целевого таймфрейма. Точнее, это не совсем ATR - ход цены берется от цены закрытия предыдущего бара и считается отдельно как вверх, так и вниз.

В настройках задается процент, исходя из которого вычисляется ход цены, при котором заданный процент баров достигал этого хода цены ранее.

Проще говоря, если мы задаем в настройках 50%, то это означает, что будет построена линия на том уровне, на котором цена в 50% случаев за заданный период достигала этого уровня.

Fake breakHi Traders,

I've developed an indicator which can detect fake-breaks on the chart.

In the following you'll find the definition of the fake break candles and also you will find how to recognize it on the chart with practical examples.

What is the fake break pattern?

Sometimes support and resistance lines broke with a full body and strong candles that gives us the idea of sharp movements on the chart but suddenly the next candle returns all the path of the previous candle. in this case we can say fake break is happening on the chart.

This indicator detect fake break patterns based on two criteria:

1. It uses AverageTrueRange indicator to measure the strength of the pattern.

2. The returning candle should engulf minimum 75% of the break candle.

This indicator plot 2 terms in the name of "FB-D" and "FB-U" that are abbreviations of the "Fake Break Down" and "Fake Break Up".

You can also set alerts to get notified when fake breakout happens on the chart.

Notice: This pattern is only acceptable in valid support and resistance zones and you can not rely on it everywhere on the chart (specially in the middle of the waves).

Notice: The source code of this indicator is open and you are allowed to use it on your scripts by mentioning the name of author.

Disclaimer: This is not a financial advice or any signal to buy or sell, the goal of developing such an indicator is to use for educational purposes.

Spinn ATR tableThe table contains summary data on the ATR from different timeframes and for different periods. You can view both absolute values and the percentage of the average price move to the current price.

This data can be used to compare the ATR on different timeframes. And, most importantly, you can compare the ATR of different coins.

In addition, the last column shows the average deviation of the ATR for each of the timeframes. You can compare these values on different coins to determine which ones are more volatile .

Note.

Using the indicator on different timeframes may give slightly different values due to the difference in the stored data for these timeframes.

--

В таблице собраны сводные данные по ATR с разных таймфреймов и за разные периоды. Можно просматривать как абсолютные значения, так и процентное соотношение среднего хода цены к текущей цене.

Эти данные можно использовать, чтобы сравнить ATR на разных таймфреймах. И, самое главное, можно сравнивать ATR разных монет.

Кроме того, в последней колонке указано среднее отклонение ATR по каждому из таймфреймов. Можно сравнивать эти значения на разных монетах, чтобы определить - какие из них более волатильны .

Примечание.

Использование индикатора на разных таймфреймах может давать слегка разные значения из-за разницы в хранимых данных для этих таймфреймов.

ATR LevelsATR Levels

The indicator plots levels based on the ATR indicator

Initial data required for the indicator:

- Open price

- ATR

Levels are calculated as follows:

1. Open price +100% ATR

2. Open price +50% ATR

3. Open price

4. Open price -50% ATR

5. Open price -100% ATR

For visual convenience:

The area between levels 1-2 and 4-5 is filled with red

Zone between levels 2-4 - filled with green

Уровни среднего истинного диапазона

Индикатор строит уровни, основанные на индикаторе ATR (Средний истинный диапазон)

Исходные данные, необходимы для индикатора:

- Цена открытия

- ATR (Средний истинный диапазон)

Уровни рассчитываются следующим образом:

1. Цена открытия +100% ATR

2. Цена открытия +50% ATR

3. Цена открытия

4. Цена открытия -50% ATR

5. Цена открытия -100% ATR

Для удобства визуального восприятия:

Зона между уровнями 1-2 и 4-5 заполнена красным цветом

Зона между уровнями 2-4 - заполнена зеленым цветом

Percentage Average True RangeCalculates the percentage movement of an instrument per day.

Default is 1 period ATR (ATR(1)) but this can be changed in the settings.

Maths - (ATR (1)/closing price)*100

Above is the ATR (1)

Below is the %ATR(1)

Average True Range MultipliedModified version of an Average True Range indicator. You could adjust the multiplication of the ATR value on the settings. I personally use this indicator for a turtle trading strategy so I don't have to use calcuator to manually multiply the ATR value by two.

Adaptive ATR Keltner Channels [Loxx]Adaptive ATR Channels are adaptive Keltner channels. ATR is calculated using a rolling signal-to-noise ratio making this indicator flex more to changes in price volatility than the fixed Keltner Channels.

What is Average True Range (ATR)?

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.1

The true range is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges.

What are Keltner Channel (ATR)?

Keltner Channels are volatility-based bands that are placed on either side of an asset's price and can aid in determining the direction of a trend.

The Keltner channel uses the average-true range (ATR) or volatility, with breaks above or below the top and bottom barriers signaling a continuation.

ATR Adaptive EMA [Loxx]ATR adaptive EMA is an exponential moving average with dynamic ATR-adjusted length inputs.

What is Average True Range (ATR)?

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.1

The true range is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges.

Price Abnormality IndicatorIt shows abnormalities in the price. It calculates using ATR value by using the current price. The default value is the last 7 bars, but you can change it. It takes values between 0-100. High value shows that the price is too much volatile.