Average True Range BandsAverage True Range Bands

The 30-day Average True Range is useful in Futures and Forex trading for placing stop orders for entry.

In the example above, a trader may want to initiate a Short position on a break below the support trendline.

A good place to enter this trade would be a price break below the support trendline minus 50 to 100% of the current ATR value.

ATR Bands provides a useful visual overlay of the current ATR value above and below the current price to speed up order entry decisions.

Average True Range (ATR)

AverageTrueRangeConvergenceDivergenceV1sloth288Simple indicator with the thought of merging MACD and ATR. The idea has come from trying to find a way to define sideways markets. Whipped this up quickly to explore the idea.

Feel free to throw in suggestions or even mention other open source indicators that define sideways markets well.

Simple instructions

If histogram green, breakouts/trade zone.

If histogram red, sideways/keep out.

Show ATR and 1st hour high+low1. Shows TR at daily bars

2. Shows ATR lines intraday: 100% and 75% (customizable)

3. Shows hint with ATR for current day and percent passed

4. Show high and low of the 1st hour

Twin Range FilterAn experiment to combine two range filters and plot the average of both to smooth out the signals.

This works significantly better than the typical ATR set-up, but there's still too much noise here to set and forget with bots. Use it as the basis of your own system with additional filtering on top.

Random Walk Index 1337A modification of the original Random Walk Index (RWI) script by everget, this one updates to version 4 and adds a threshold value and colouring.

If both high and low are below the default threshold of 1.0 the line chart will be coloured in grey.

Adjusting the length and threshold should allow you to see flat and choppy periods.

Bollinger Band SqueezeThe Bollinger Band Squeeze is calculated according to the ATR. With the default settings. If the BB width is smaller than the ATR * 2 the background is painted green. If the BB width is larger than the ATR * 5 the background is painted red

ATR Percentage of PriceThis indicator takes the standard ATR and expresses it as a percentage of the OHLC4 price. This has the advantage of normalising the ATR value across the history of an asset. For example, an ATR of value 20 when the price is 2000 actually has a very different meaning when the price rises to 4000. The ATR may be the same value but actually the volatility it represents has halved.

I also add an SMA to the value and a histogram which shows the difference between the two. Positive values mean that volatility is expanding while negative values mean volatility is contracting.

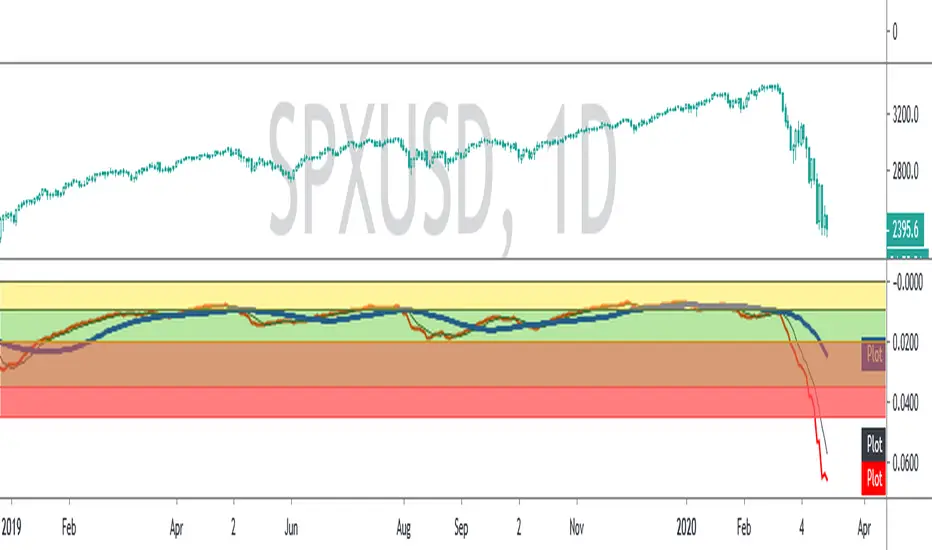

SPX ATR14 indicator This indicator works well on SPX 500

Needs to be inverted so Red is at the bottom

Levels of pullbacks are used to determine trend .

Pullback to the Green zone normal Bull Market

Pullback to the Brown Zone are warning of potential Bear Market , but if it holds , just a deeper correction within a Bull Market

Pullbacks into the Red , Bear Market .

In Bear , wait until indicator is forming a reversal trend up and price should make a divergence by either making a new low or retesting previous low.

The Blue MA is the 33 MA and can be used as a form of stop trend indicator on the cross below the MA

KeltnerModified + DonchianColoredKeltner Channel + color coded candles when making new Donchian highs/lows

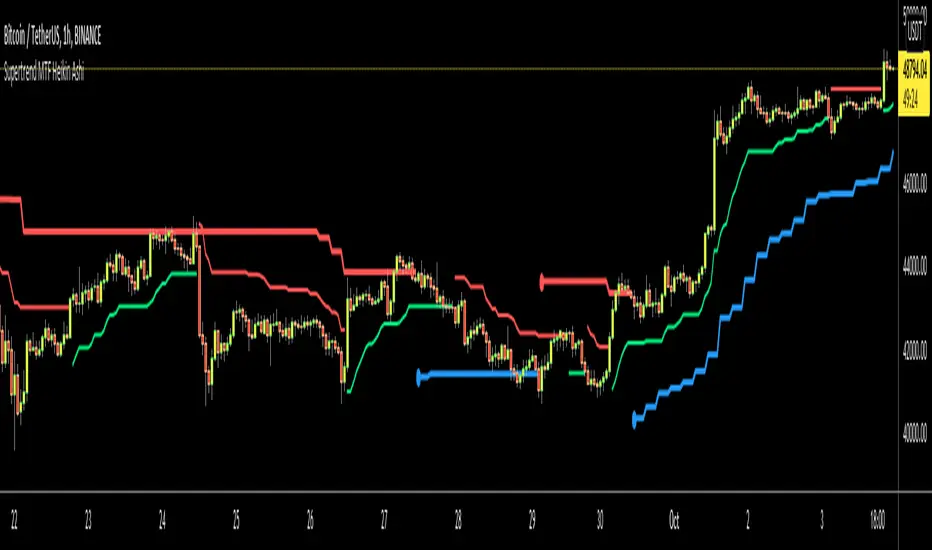

Supertrend MTF Heikin AshiThis is non-repaiting Supertrend Multi Time Frame script, uses Heikin Ashi Candles as source on normal chart

There is an option for Higher Time Frame. if you choose "Auto" then Higher Time Frame calculation is made by the script. If you choose "User Defined" option and then you can select Time Frame.

You better use this script with other indicators such as RSI, Momentum etc.

Enjoy!

Zero Lag Keltner ChannelsThis is Keltner Channelz (KC) with Zero Lag Moving Average (ZLMA as base). It is smoother and has less lag than the original (EMA/SMA) variant.

It also can be used as a trend indicator and trend confirmation indicator. The upper and lower bands are green if it is an up trend, and red if a down trend. If both have the same color it is a stronger trend.

Trailing SL Strategy [QuantNomad]I'm a big fan of simple strategies.

This one is a very simple one. So it consists only from one Trailing SL. When SL is hit, the position is reversed and SL is tracked for a new position.

You can choose one of 3 types of SL:

% of your price

ATR - it is calculated as current ATR * multiplier

Absolute

As you can see even this simple strategy can show pretty good results.

ATR based Stop and Take-Profit levels in realtime Little tool to quickly identify stops and take-profit levels based on Average True Range. User can change ATR multipiers, as well as the ATR length used. Green and red lines show these levels; plot is visible over last 8 bars only to reduce clutter. Label showing the current ATR, up above the last bar

Adam H Grimes - Keltner Channels with Day's High & LowThe indicator shows the day's high and low along with the Keltner Channels.

Keltner Channel Period - 20

Keltner Channel Multiple - 2.25

Renko Weis Wave VolumeThis is live and non-repainting Renko Weis Wave Volume tool. The tool has it’s own engine and not using integrated function of Trading View.

Renko charts ignore time and focus solely on price changes that meet a minimum requirement. Time is not a factor on Renko chart but as you can see with this script Renko RSI created on time chart.

Renko chart provide several advantages, some of them are filtering insignificant price movements and noise, focusing on important price movements and making support/resistance levels much easier to identify.

As source Closing price or High/Low can be used.

Traditional or ATR can be used for scaling. If ATR is chosen then there is rounding algorithm according to mintick value of the security. For example if mintick value is 0.001 and brick size (ATR/Percentage) is 0.00124 then box size becomes 0.001. And also while using dynamic brick size (ATR), box size changes only when Renko closing price changed.

This tool is based on the Weis Wave described by David H. Weis (a Wyckoff specialist). The Weis Waves Indicator sums up volumes in each wave. This is how we receive a bar chart of cumulative volumes of alternating waves and The cumulative volume makes the Weis wave charts unique.

If there is no volume information for the security then this tool has an option to use “True Range” instead of volume .

Better to use this script with the following one:

Enjoy!

[LunaOwl] 超級趨勢2 (SuperTrend2)It is very similar to the previous version. I changed the function from study to a strategy, and added the Average true range to RMA again.

I don't know the academic suitability, but using this strategy to trade the Altcoins market may have a good effect.

refer to Binance for 0.1% of fees, starting from Q4 2017.

跟以前的版本變化不大,我將腳本函數從"study"更改為"strategy",然後將平均真實範圍再次用遞迴平均線均化數值。

不知道學術上的適不適合這麼做...但是,直到目前交易小幣現貨市場,效果還算不錯,用用看。

交易手續費參考幣安小幣,0.1%,從2017年第四季開始測。

Updated:

--1. use RMA to reduce ATR noise.

--2. for the highly volatile Altcions market, strategy should focus on reducing noise.

--3. the Street commonly used alpha filtering for Random Walk.

--4. compared to other MAs, the performance is not outstanding, but the advantage is stability.

--5. I choose the 4H time frame to test the Altcoins (ex: ETH).

稍做更新:

--1.平均真實區間利用了遞迴均線減少雜訊

--2.針對高波動率的小幣市場,中期順勢策略應該以減少雜訊為重點

--3.研究國外交易策略後,它們常用平滑因子過濾隨機走勢

--4.績效上和其它平均法比較並沒有突出,但優點是參數變動穩定性

--5.我選擇四小時線回測小幣市場,並且選擇經歷過牛熊市的以太坊

The purpose of publishing Chinese Scripts is to make Pine close to more Chinese user.

發布中文腳本的目的,是希望可以讓 Pine 親近更多中文圈的使用者。

ATR Stoploss Lines - Minimize Risk | Maximize ProfitThe ATR Stoploss is best used as a trailing stop. While actively managing your trades, move your stops up as price increases/decreases.

There is an offset of 1 candle, so the ATR will only be based on closed candles. This prevents you from moving your stop's when you really shouldn't.

The top lines are used for short positions and the bottom lines are used for long positions.

You can adjust the distance of the ATR lines from your candles by changing the multiplier in the settings.

You may want to increase the multiplier to 2-3 on less volatile assets, and keep it ~1.75 for volatile assets like BTC.

Feel free to reach out if you need any tips or more help with using these. Just remember, this indicator should only be used to manage your trades, not enter them.

London Breakout with MDX Trailing StopThis indicator aims to aid in using the regular London Breakout strategy, as well as improve on it by adding a trailing stop based on the Mean Deviation Index.

The London Breakout strategy (according to my personal understanding) basically sees the morning before London open as the accumulation or distribution range for large buyers or sellers, and assumes the market will break either above that mornings high or below that mornings low when they start to move price. It is mostly used to trade stock indices and forex.

This indicator plots the morning high and low for each day. The green line is the morning high, and the red line is the morning low. If price moves above the green line (the morning high) it fills that area with a green color. If price moves below the green line (the morning low) it fills that area with a red color. This makes the breakouts easy to spot.

The background color of the chart turns green when the MDX is above 0 (price is more than X times ATR above the mean) and a breakout above the morning high has occurred, and stays green until the opposite happens.

The background color of the chart turns red when the MDX is below 0 (price is more than X times ATR below the mean) and a breakout above the morning high has occurred, and stays green until the opposite happens.

The default for X above is 1.0, but this can be changed in the settings by changing "ATR Multiplier".

The background is always neutral during the morning session since the morning high and morning low are not established yet.

A trailing stop is shown when price is more than X times away from the mean and a breakout has occured. The distance is set using the MDX. The trailing stop uses a separate ATR multiplier though, to make the signal and trailing stop MDX values different, if one likes. The default ATR multiplier for the trailing stop is 1.25, but this can be changed is the settings by changing "ATR multiplier for trailing stop".

When the high or low of a candle breaks the trailing stop, it is moved further away, indicating you have been stopped out, but gives opportunity to use it if you enter again (so it doesn't just disappear).

As an added bonus, take profit levels have been added based on the mornnig range. The take profit distance is set by multiplying the range with a factor. The levels are then plotted that distance from the morning high and morning low.

MDX:

ATR BandsThe NNFX way

This indicator makes it easy to see the ATR values of the chart.

The red lines are at 1.5 ATR

The blue lines are at 1 ATR

Credits to www.tradingview.com for the code he published. I've extracted only the ATR to create this indicator. Many thanks ❤

UT Bot AlertsUT Bot indicator was initially developer by @Yo_adriiiiaan

The idea of original code belongs @HPotter

These are v4 alerts for my previously published strategy:

Original script:

Current vs. Average price performance (daily and weekly)This indicator is to be used only by the values it gives back, don't use the lines .

In "current week days" choose number of days that already BEGAN this week (ex. on Wednesday type 3)

Green1 - Current Daily Range

Orange1 - Average Daily Range

Green2 - Current Weekly Range

Red1 - Average Weekly Range

Orange2 - Today's price movement compared to the average daily price movement (in percentage)

Red2 - This week price movement compared to the average weekly price movement (in percentage)

By these values you can check how price performed today and this week in comparison to the average daily and weekly values - you can check with some probability if the movement is already exhausted or price can do some more action.

BERLIN Range Index | Panel versionThe original problem: The choppiness index is great at finding ranging markets, but it is sometimes very slow, which means most of the time it only catches the end of a trend.

This indicator tries to solve this. It uses the choppiness index and filters it using a factor that is based on the standard deviation of the ATR.

The ATR based filter is calculated by first calculating the running standard deviation of the ATR, and then looking at that in relation to its recent low to find a filtering factor to use on the choppiness index. This makes the choppiness index more reactive to trends, but also slightly more likely to missidentify ranges.

This is the panel version of the indicator. It plots the index and min/max values, as well as background colors to tell you when it thinks the market is ranging or trending.

Yellow = Trending

Transparent gray = Ranging