IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Average True Range (ATR)

Ehlers Instantaneous Trendline ATR LevelsOverview

This sophisticated technical analysis tool merges John Ehlers' cutting-edge Instantaneous Trendline methodology with a dynamic ATR-based bands system. The indicator is designed to provide traders with a comprehensive view of market trends while accounting for volatility, making it suitable for both trending and ranging markets. Works on all timeframes and chart types.

Key Features in Detail

1. Ehlers Instantaneous Trendline Implementation

- Advanced algorithm that reduces lag typically associated with moving averages

- Built-in volatility filtering system to minimize false signals

- Adaptive to market conditions through dynamic calculations

- Real-time trend direction identification

2. Multi-layered ATR Band System

- Hierarchical band structure with 18 total bands (9 upper, 9 lower)

- Color-coded visualization system:

Upper bands: Red gradient (darker = further from trendline)

Lower bands: Green gradient (darker = further from trendline)

Central trendline: Yellow for optimal visibility

- Customizable multipliers for each band level

- Independent visibility controls for each band

Configuration Options

Trendline Settings:

- Lower values: More responsive to price changes and faster reacting to break in ATR filter

- Higher values: Smoother trendline with less noise and slower reacting to break in ATR filter

ATR Configuration:

Period: Customizable from 1 to any positive integer

- Longer periods: More stable volatility measurement

- Shorter periods: More reactive to recent volatility changes

Filter Multiplier: Fine-tune volatility filtering

- Higher values: More filtered signals leading to less shift in bands

- Lower values: More sensitive to price movements leading to more band shifts

Practical Applications

1. Trend Analysis

Use the central trendline for primary trend direction

Monitor band crossovers for trend strength confirmation

Track price position relative to bands for trend context

2. Volatility Assessment

Band spacing indicates current market volatility

Width between bands helps identify consolidation vs. expansion phases

Price Extremes

3. Support and Resistance

Each band acts as a dynamic support/resistance level

Multiple timeframe analysis possible adjusting for different timeframe ATR

ReadyFor401ks Just Tell Me When!ReadyFor401ks Just Tell Me When!

LET ME START BY SAYING. NO INDICATOR WILL HELP YOU NAIL THE PERFECT ENTRY/EXIT ON A TRADE. YOU SHOULD ALWAYS EDUCATE YOURSELF AND HAVE A BASIC UNDERSTANDING OF INVESTING, TRADING, CHART ANALYSIS, AND THE RISKS INVOLVED WITH. THAT BEING SAID, WITH THE RIGHT ADJUSTMENTS, IT'S PRETTY D*$N CLOSE TO PERFECTION!

This indicator is designed to help traders identify t rend direction, continuation signals, and potential exits based on a dynamic blend of moving averages, ATR bands, and price action filters. Whether you’re an intraday trader scalping the 5-minute chart or a swing trader analyzing the weekly timeframe for LEAPS , this tool provides a clear, rule-based system to help guide your trading decisions.

⸻

Key Features & Benefits

🔹 Customizable Trend Power (Baseline) Calculation

• Choose from JMA, EMA, HMA, TEMA, DEMA, SMA, VAMA, and WMA for defining your baseline trend direction.

• The baseline helps confirm whether the market is in a bullish or bearish phase.

🔹 ATR-Based Trend Continuation & Volatility Measurement

• ATR bands dynamically adjust to market conditions, helping you spot breakouts and fakeouts.

• The indicator detects when price violates ATR range , which often signals impulse moves.

🔹 Clear Entry & Exit Signals

• Uses a Continuation MA (SSL2) to confirm trends.

• Includes a separate Exit MA (SSL3) that provides crossover signals to indicate when to exit trades or reverse positions .

• Plots trend continuation circles when ATR conditions align with trend signals.

🔹 Keltner Channel Baseline for Market Structure

• A modified Keltner Channel is integrated into the baseline to help filter out choppy conditions .

• If price remains inside the baseline, the market is in consolidation , while breakouts beyond the bands indicate strong trends .

🔹 Adaptive Color Coding for Market Conditions

• Bars change color based on momentum, making trend direction easy to read.

• Green = Bullish Trend, Red = Bearish Trend, Gray = Neutral/Chop.

🔹 Flexible Alerts for Trade Management

• Get real-time alerts when the Exit MA crosses price , helping you l ock in profits or switch directions .

⸻

How to Use This Indicator for Different Trading Styles

🟢 For Intraday Trading (5-Minute Chart Setup)

• Faster MA settings help react quickly to momentum shifts.

• Ideal for scalping breakouts, trend continuation setups, and intraday reversals.

• Watch for ATR violations and price interacting with the baseline/Keltner Channel for entries.

--------------------------------

My Settings for Intraday Trading on 5min Chart

ATR Period: 15

ATR Multi: 1

ATR Smoothing: WMA

Trend Power based off of: JMA

Trend Power Period: 30

Continuation Type: JMA

Continuation Length: 20

Calculate Exit of what MA?: HMA

Calculate Exit off what Period? 30

Source of Exit Calculation: close

JMA Phase *APPLIES TO JMA ONLY: 3

JMA Power *APPLIES TO JMA ONLY: 3

Volatility Lookback Period *APPLIES TO VAMA ONLY 30

Use True Range for Channel? Checked

Base Channel Multiplier: 0.4

ATR Continuation Criteria: 1.1

----------------------------------

🔵 For Swing Trading & LEAPS (Weekly Chart Setup - Default Settings)

• Slower MAs provide a broader view of trend structure.

• Helps capture multi-week trend shifts and confirm entry points for longer-term trades.

• Weekly ATR bands highlight when stocks are entering overextended conditions.

💡 Example:

Let’s say you’re looking at TSLA on a Weekly Chart using the default settings. You notice that price crosses above the continuation MA (SSL2) while remaining above the baseline (trend power MA). The bar turns green, and price breaks above ATR resistance, signaling a strong bullish continuation. This could be a great opportunity to enter a long-term swing trade or LEAPS options position.

On the flip side, if price reverses below the Exit MA (SSL3) and turns red while breaking the lower ATR band, it might signal a good time to exit longs or enter a short trade.

⸻

Final Thoughts

The ReadyFor401ks Just Tell Me When! indicator is an all-in-one trading system that simplifies trend-following, volatility measurement, and trade management. By integrating multiple moving average types, ATR filters, and clear visual cues, it allows traders to stay disciplined and remove emotions from their trading decisions.

✅ Perfect for scalpers, day traders, and swing traders alike!

🔔 Set up alerts for automated trade signals and never miss a key move!

💬 If you find this indicator useful, leave a comment and share how you use it in your trading! 🚀

Range%This indicator displays the range of each candle i.e. High minus Low as a percentage of the previous closing price. It does not account for gaps, making it particularly useful for intraday trading. By tracking the volatility cycle of candles, this indicator helps identify periods of increased or decreased market volatility, allowing traders to pinpoint the best days to execute trades.

If the Range% is below low line candles will turn White and If Range% is above the High Line Candles will turn Red.

ATR Multiples from LOD/HODAn indicator that plots ATR (Average True Range) multiples from the current Low of Day (LOD) and High of Day (HOD). The indicator should:

Calculate the Low of Day (LOD) and High of Day (HOD) dynamically for the current trading session.

Use the ATR (Average True Range), with a customizable length, as the base measurement.

Plot multiple levels above the LOD and below the HOD, based on user-defined ATR multiples (e.g., 1x ATR, 2x ATR, 3x ATR, etc.).

Customizable Inputs:

ATR Length

ATR Multiples (Up to 5 levels)

Line color and style for each level

Display the ATR multiples on the chart as horizontal lines extending throughout the trading session.

FVG | iSolani

Unveiling Market Inefficiencies with Precision

In fast-moving markets, spotting hidden opportunities often hinges on identifying imbalances between price and value. The FVG | iSolani indicator revolutionises this process by detecting Fair Value Gaps (FVGs) —zones where price action skips over "fair" valuation levels, creating potential retracement targets. Combining advanced filtering, dynamic visualisation, and automated management, this tool empowers traders to pinpoint high-probability setups with unprecedented clarity.

Core Methodology

The indicator employs a multi-layered approach to identify FVGs:

Three-Bar Gap Analysis: Bullish FVGs form when the current low exceeds the high of two bars prior, while bearish FVGs occur when the current high stays below the low of two bars back.

Volatility-Adjusted Filtering: Gaps are measured against a 100-bar standard deviation to exclude insignificant price jumps.

Volume Confirmation: Only gaps accompanied by above-average volume (relative to a 1-bar SMA) are validated, filtering out low-conviction moves.

Auto-Invalidation System: Continuously monitors price action to remove FVG zones once price closes within their range, maintaining chart cleanliness.

Breaking New Ground

This tool introduces three paradigm-shifting innovations:

Volume-Weighted Significance: Unlike traditional FVG detectors, it ties gap validity to volume spikes, emphasising institutional activity.

Adaptive Zone Management: Boxes automatically extend rightward (when enabled) and self-destruct when invalidated, eliminating manual cleanup.

Smart Color Encoding: Offers both monochrome (for multi-timeframe analysis) and standard bull/bear color schemes, with customisable transparency.

Engine Under the Hood

The script operates through four key processes:

Gap Detection: Scans every new bar for three-candle patterns meeting FVG criteria.

Statistical Filtering: Applies user-defined threshold (default: 1σ) to separate meaningful gaps from market noise.

Box Rendering: Draws semi-transparent zones between gap boundaries using TradingView's box objects, styled according to user preferences.

Array-Based Memory: Stores all active FVGs in arrays, enabling real-time validation checks against current price action.

Standard Configuration

Optimised default settings balance visibility and functionality:

Filter: 1.0 (1 standard deviation threshold)

Colors: "Mono" mode (gray boxes) with 90% transparency

Text Labels: Enabled in medium gray

Extension: Gaps extend indefinitely rightward

Borders: Dotted lines with visible outlines

Through its fusion of quantitative rigor and visual adaptability, the FVG | iSolani transforms raw price data into actionable intelligence. By focusing on volume-confirmed gaps and automating zone management, it cuts through market chaos to reveal structurally significant levels—a must-have for traders navigating breakouts, reversals, or order-flow analysis.

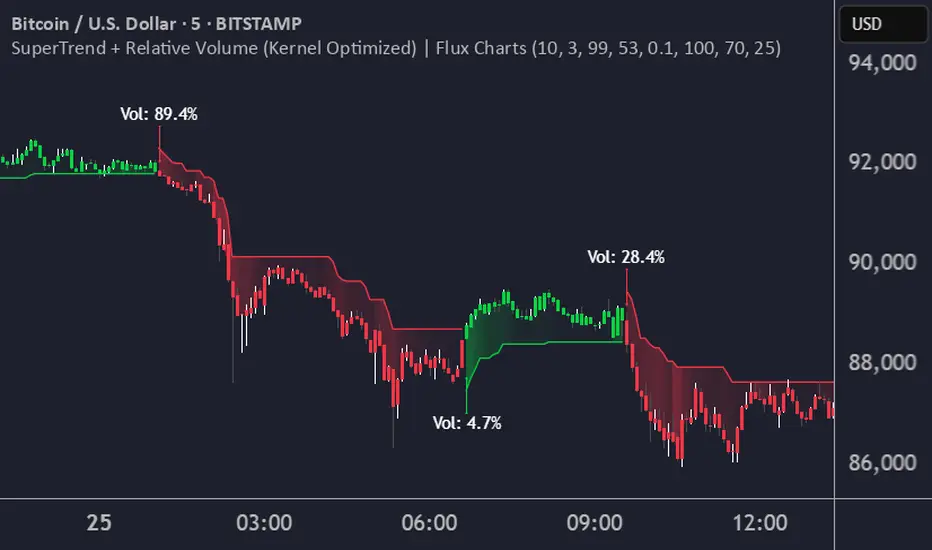

SuperTrend + Relative Volume (Kernel Optimized)Introducing our new KDE Optimized Supertrend + Relative Volume Indicator!

This innovative indicator combines the power of the Supertrend indicator along with Relative Volume. It utilizes the Kernel Density Estimation (KDE) to estimate the probability of a candlestick marking a significant trend break or reversal.

❓How to Interpret the KDE %:

The KDE % is a crucial metric that reflects the likelihood that the current candlestick represents a true break in the SuperTrend line, supported by an increase in relative volume. It estimates the probability of a trend shift or continuation based on historical SuperTrend breaks and volume patterns:

Low KDE %: A lower probability that the current break is significant. Price action is less likely to reverse, and the trend may continue.

Moderate KDE - High KDE %: An increased possibility that a trend reversal or consolidation could occur. Traders should start watching for confirmation signals.

📌How Does It Work?

The SuperTrend indicator uses the Average True Range (ATR) to determine the direction of the trend and identifies when the price crosses the SuperTrend line, signaling a potential trend reversal. Here's how the KDE Optimized SuperTrend Indicator works:

SuperTrend Calculation: The SuperTrend indicator is calculated, and when the price breaks above (bullish) or below (bearish) the SuperTrend line, it is logged as a significant event.

Relative Volume: For each break in the SuperTrend line, we calculate the relative volume (current volume vs. the average volume over a defined period). High relative volume can suggest stronger confirmation of the trend break.

KDE Array Calculation: KDE is applied to the break points and relative volume data:

Define the KDE options: Bandwidth, Number of Steps, and Array Range (Array Max - Array Min).

Create a density range array using the defined number of steps, corresponding to potential break points.

Apply a Gaussian kernel function to the break points and volume data to estimate the likelihood of the trend break being significant.

KDE Value and Signal Generation: The KDE array is updated as each break occurs. The KDE % is calculated for the breakout candlestick, representing the likelihood of the trend break being significant. If the KDE value exceeds the defined activation threshold, a darker bullish or bearish arrow is plotted after bar confirmation. If the KDE value falls below the threshold, a more transparent arrow is drawn, indicating a possible but lower probability break.

⚙️Settings:

SuperTrend Settings:

ATR Length: The period over which the Average True Range (ATR) is calculated.

Multiplier: The multiplier applied to the ATR to determine the SuperTrend threshold.

KDE Settings:

Bandwidth: Determines the smoothness of the KDE function and the width of the influence of each break point.

Number of Bins (Steps): Defines the precision of the KDE algorithm, with higher values offering more detailed calculations.

KDE Threshold %: The level at which relative volume is considered significant for confirming a break.

Relative Volume Length: The number of historic candles used in calculating KDE %

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

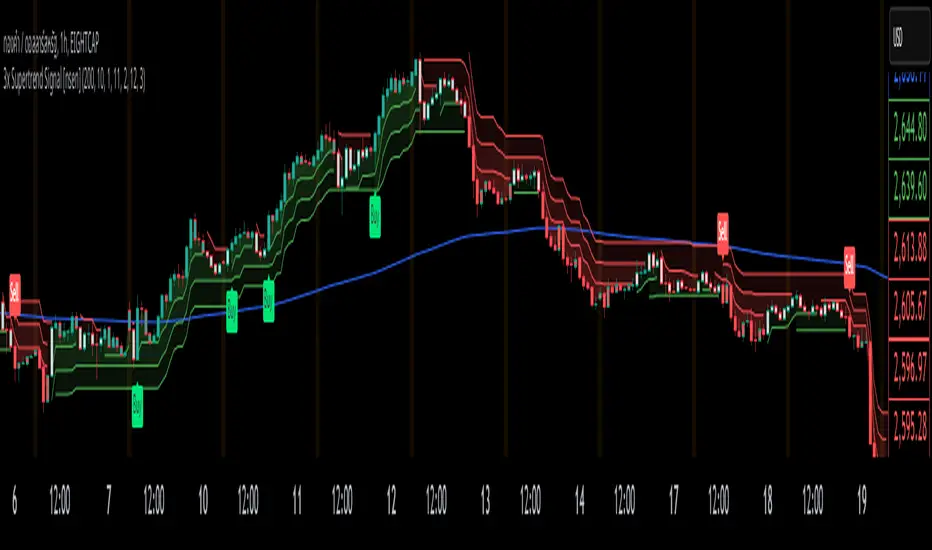

3x Supertrend + EMA200 Signal Buy/Sell [nsen]The indicator uses signals from three Supertrend lines to determine whether to trade Buy or Sell, with the assistance of a moving average for bias.

Buy/Sell signals are generated when the conditions are met:

A Buy signal is triggered when all three Supertrend lines indicate a bullish trend and are above the EMA.

A Sell signal is triggered when all three Supertrend lines indicate a bearish trend and are below the EMA.

Indicator ใช้สัญญาณจาก Supertrend ทั้งหมด 3 เส้น โดยใช้ในการกำหนดว่าจะเลือกเทรด Buy หรือ Sell โดยการใช้ moveing average เข้ามาช่วยในการ bias

แสดงสัญญาณ Buy/Sell เมื่อเข้าเงื่อนไข

- Supertrend ทั้ง 3 เส้นเป็นสัญญาณ Bullish และอยู่เหนือเส้น EMA จะเปิดสัญญาณ Buy

- Supertrend ทั้ง 3 เส้นเป็นสัญญาณ Bearish และอยู่ใต้เส้น EMA จะเปิดสัญญาณ Sell

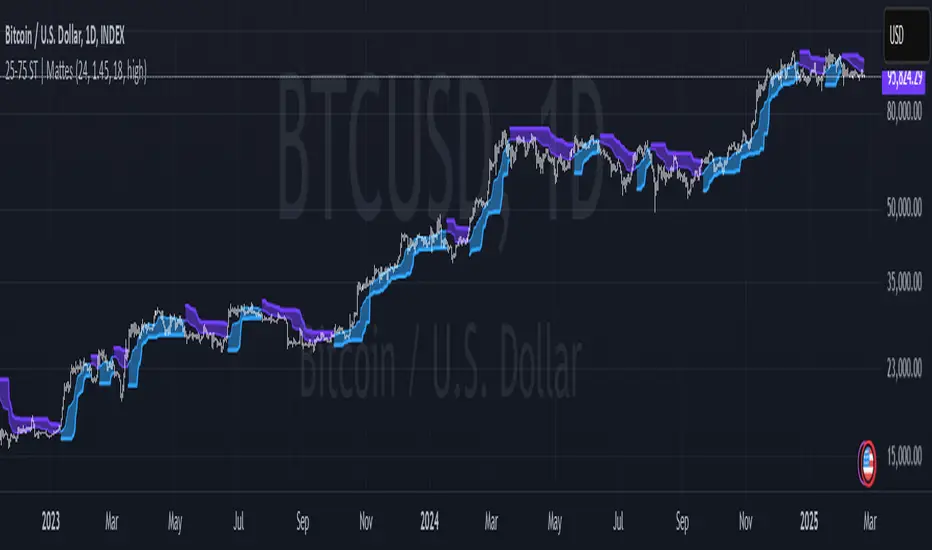

25-75 Percentile SuperTrend | Mattes25-75 Percentile SuperTrend | Mattes

Overview

The 25-75 Percentile SuperTrend is an advanced trend-following indicator that enhances the traditional SuperTrend concept by incorporating percentile-based smoothing. Instead of using a simple moving average or median price, this indicator calculates the 25th and 75th percentiles over a user-defined period. These percentiles act as dynamic trend levels, adjusting more responsively to price volatility while reducing noise.

How It’s Calculated

Percentile Smoothing:

The 25th percentile of the selected source (low-end smoothing).

The 75th percentile of the selected source (high-end smoothing).

SuperTrend Logic:

The upper band is set at the 75th percentile + ATR multiplier.

The lower band is set at the 25th percentile - ATR multiplier.

The trend flips when the price crosses above/below these dynamic bands.

Signal Generation :

A bullish trend occurs when price remains above the lower band.

A bearish trend occurs when price remains below the upper band.

Trend shifts are highlighted with colored bars and lines for easy visualization.

How It Differs From Traditional SuperTrend

Uses Percentiles Instead of a Moving Average:

Traditional SuperTrend relies on ATR-based offsets from a moving average.

This version replaces the moving average with percentile smoothing, which adapts better to price behavior.

Better Noise Filtering:

Since percentiles are less sensitive to outliers, this indicator reduces false signals in choppy markets.

More Adaptive to Market Conditions:

The percentile smoothing dynamically adjusts trend detection based on price distribution rather than fixed calculations.

Why It’s Useful

✅ Reduces Whipsaws: Helps minimize false breakouts by using percentile-based bands instead of traditional ATR-only bands.

✅ Works in Different Market Conditions: Effective in both trending and ranging environments due to its adaptive nature.

✅ Enhances Trend Confidence: Provides clearer signals by filtering noise more effectively than standard SuperTrend indicators.

Application Examples

Trend Following: Use it to identify strong upward or downward trends.

Stop-Loss Placement: The upper and lower bands can serve as dynamic stop-loss levels.

Breakout Confirmation: Trend flips can confirm breakout signals from other indicators.

Mean Reversion Strategy Filtering: The 25-75 range helps identify strong versus weak reversals.

Risks & Disclaimers

Not a Standalone Strategy: This indicator should be used with other confirmation tools like volume analysis, momentum oscillators, or support/resistance levels.

False Signals in Sideways Markets: Although it reduces noise, choppy markets can still generate occasional false trend flips.

Market Adaptation Required: The best parameters may vary depending on the asset and timeframe.

This indicator was heavily inspired and influenced by the IRS/viResearch Median SuperTrend, improving upon its concept by transforming its median based calculation into a more responsive & effective counterpart of its former self.

Shoutout to all my Masterclass Brothers and L4 Gs !

Volatility-Volume Index (VVI)Volatility-Volume Index (VVI) – Indicator Description

The Volatility-Volume Index (VVI) is a custom trading indicator designed to identify market consolidation and anticipate breakouts by combining volatility (ATR) and trading volume into a single metric.

How It Works

Measures Volatility : Uses a 14-period Average True Range (ATR) to gauge price movement intensity.

Tracks Volume : Monitors trading activity to identify accumulation or distribution phases.

Normalization : ATR and volume are normalized using their respective 20-period Simple Moving Averages (SMA) for a balanced comparison.

Interpretation

VVI < 1: Low volatility and volume → Consolidation phase (range-bound market).

VVI > 1: Increased volatility and/or volume → Potential breakout or trend continuation.

How to Use VVI

Detect Consolidation:

Look for extended periods where VVI remains below 1.

Confirm with sideways price movement in a narrow range.

Anticipate Breakouts:

A spike above 1 signals a possible trend shift or breakout.

Why Use VVI?

Unlike traditional volatility indicators (ATR, Bollinger Bands) or volume-based tools (VWAP), VVI combines both elements to provide a clearer picture of consolidation zones and breakout potential.

Custom SL/TP ZonesThe "Please Don't Stop Me Now" Indicator 📊

Ever found yourself staring at a chart, thinking "This is DEFINITELY the bottom!" only to watch your stop loss get hit faster than your ex replacing you? Well, this indicator won't stop that from happening, but at least you'll know exactly where you're going to be wrong! 🎯

How it works:

See a setup you like? Pick your candle of choice (make sure it's closed - we're not fortune tellers here)

Hit either Bull or Bear (choose wisely, or don't - we all know it's 50/50 anyway)

3. Marvel at the beautiful boxes showing your:

Take Profit Zone (where you'll exit too early)

Stop Loss Zone (where you'll probably exit, let's be honest)

Features:

Uses ATR for dynamic zones because "one size fits all" only works in disappointing Halloween costumes

Extends 10 bars into the future, giving you plenty of time to watch your prediction go wrong

Price labels included so you know exactly where to set your alerts (and subsequently ignore them)

Customizable multipliers for when you're feeling extra brave (or foolish)

Clean interface that won't distract you from your bad decisions

Remember: The market can stay irrational longer than you can stay solvent, but at least with this indicator, you'll know exactly where your rationality ends and your "This time it's different" begins!

Happy Trading! (Results may vary, tears not included)

Settings:

TP Multiplier: How far to your dreams (Default: 4.0)

SL Multiplier: How far to your nightmares (Default: 2.0)

Bar Offset: Pick your poison (1 = last closed bar)

Colors: Because trading isn't painful enough in grayscale

Smart MA Crossover BacktesterSmart MA Crossover Backtester - Strategy Overview

Strategy Name: Smart MA Crossover Backtester

Published on: TradingView

Applicable Markets: Works well on crypto (tested profitably on ETH)

Strategy Concept

The Smart MA Crossover Backtester is an improved Moving Average (MA) crossover strategy that incorporates a trend filter and an ATR-based stop loss & take profit mechanism for better risk management. It aims to capture trends efficiently while reducing false signals by only trading in the direction of the long-term trend.

Core Components & Logic

Moving Averages (MA) for Entry Signals

Fast Moving Average (9-period SMA)

Slow Moving Average (21-period SMA)

A trade signal is generated when the fast MA crosses the slow MA.

Trend Filter (200-period SMA)

Only enters long positions if price is above the 200-period SMA (bullish trend).

Only enters short positions if price is below the 200-period SMA (bearish trend).

This helps in avoiding counter-trend trades, reducing whipsaws.

ATR-Based Stop Loss & Take Profit

Uses the Average True Range (ATR) with a multiplier of 2 to calculate stop loss.

Risk-Reward Ratio = 1:2 (Take profit is set at 2x ATR).

This ensures dynamic stop loss and take profit levels based on market volatility.

Trading Rules

✅ Long Entry (Buy Signal):

Fast MA (9) crosses above Slow MA (21)

Price is above the 200 MA (bullish trend filter active)

Stop Loss: Below entry price by 2× ATR

Take Profit: Above entry price by 4× ATR

✅ Short Entry (Sell Signal):

Fast MA (9) crosses below Slow MA (21)

Price is below the 200 MA (bearish trend filter active)

Stop Loss: Above entry price by 2× ATR

Take Profit: Below entry price by 4× ATR

Why This Strategy Works Well for Crypto (ETH)?

🔹 Crypto markets are highly volatile – ATR-based stop loss adapts dynamically to market conditions.

🔹 Long-term trend filter (200 MA) ensures trading in the dominant direction, reducing false signals.

🔹 Risk-reward ratio of 1:2 allows for profitable trades even with a lower win rate.

This strategy has been tested on Ethereum (ETH) and has shown profitable performance, making it a strong choice for crypto traders looking for trend-following setups with solid risk management. 🚀

True Range & ATRDescription : This indicator plots both the True Range (TR) and the Average True Range (ATR) in a separate pane below the main chart.

- TR represents the absolute price movement range within each candle.

- ATR is a smoothed version of TR over a user-defined period (default: 14), providing insight into market volatility.

- TR is displayed as a histogram for a clearer view of individual candle ranges.

- ATR is plotted as a line to show the smoothed trend of volatility.

This indicator helps traders assess market volatility and potential price movements.

ATR Trailing Stop by GideonMATR Trailing Stop Indicator

This ATR Trailing Stop Indicator is designed for traders who wish to enhance their exit strategies by leveraging volatility-based stops. It offers a systematic approach to trend management and risk control, enabling traders to capture extended trends while protecting their capital during market reversals. Works on Indian Indices as well.

Overview:

The ATR Trailing Stop indicator is a dynamic trend-following tool that adjusts stop levels based on market volatility. By incorporating the Average True Range (ATR), the indicator provides a flexible exit strategy that adapts to changing market conditions, helping traders lock in profits during trends and limit losses during reversals.

How It Works:

True Range and ATR Calculation:

The indicator first calculates the True Range (TR) for each bar, defined as the maximum of:

The difference between the high and low,

The absolute difference between the high and the previous close, and

The absolute difference between the low and the previous close.

Using the TR values, the ATR is computed over a user-defined period (default is 14 bars) with an option to use either a Simple Moving Average (SMA) or an Exponential Moving Average (EMA) as the smoothing method.

Trailing Stop Determination:

Two potential stop levels are calculated:

For an uptrend, the stop is determined as:

Stop = Close – (Multiplier × ATR)

For a downtrend, the stop is:

Stop = Close + (Multiplier × ATR)

The indicator maintains a persistent trailing stop that dynamically adjusts:

In an uptrend, the trailing stop only moves upward (or remains flat) to secure gains.

In a downtrend, it only moves downward, thereby protecting the position from excessive losses.

A reversal in trend is identified when the price crosses the trailing stop level, at which point the indicator flips the trend and resets the stop level accordingly.

Rationale:

Utilizing the ATR for trailing stops ensures that the stop levels are directly influenced by market volatility. This dynamic adjustment helps accommodate the natural price fluctuations of the market, providing a more adaptive risk management tool compared to fixed stop-loss levels. The approach is particularly useful in volatile markets where traditional static stops might be triggered prematurely.

Customization:

Key parameters that can be adjusted include:

ATR Period: The number of bars used to calculate the ATR.

ATR Multiplier: The factor that determines how far the trailing stop is set from the current price.

Smoothing Method: Option to choose between SMA and EMA for ATR calculation, allowing traders to tailor the sensitivity of the indicator to their specific trading style.

Custom Length ATRThis Custom Length ATR Indicator allows traders to calculate the Average True Range (ATR) dynamically based on a selected timeframe and number of days. Unlike traditional ATR indicators that are tied to the chart’s timeframe, this script lets users choose a specific timeframe scale (e.g., Daily, Hourly, etc.), ensuring consistent volatility measurement across different trading views.

AI Volume Breakout for scalpingPurpose of the Indicator

This script is designed for trading, specifically for scalping, which involves making numerous trades within a very short time frame to take advantage of small price movements. The indicator looks for volume breakouts, which are moments when trading volume significantly increases, potentially signaling the start of a new price movement.

Key Components:

Parameters:

Volume Threshold (volumeThreshold): Determines how much volume must increase from one bar to the next for it to be considered significant. Set at 4.0, meaning volume must quadruplicate for a breakout signal.

Price Change Threshold (priceChangeThreshold): Defines the minimum price change required for a breakout signal. Here, it's 1.5% of the bar's opening price.

SMA Length (smaLength): The period for the Simple Moving Average, which helps confirm the trend direction. Here, it's set to 20.

Cooldown Period (cooldownPeriod): Prevents signals from being too close together, set to 10 bars.

ATR Period (atrPeriod): The period for calculating Average True Range (ATR), used to measure market volatility.

Volatility Threshold (volatilityThreshold): If ATR divided by the close price exceeds this, the market is considered too volatile for trading according to this strategy.

Calculations:

SMA (Simple Moving Average): Used for trend confirmation. A bullish signal is more likely if the price is above this average.

ATR (Average True Range): Measures market volatility. Lower volatility (below the threshold) is preferred for this strategy.

Signal Generation:

The indicator checks if:

Volume has increased significantly (volumeDelta > 0 and volume / volume >= volumeThreshold).

There's enough price change (math.abs(priceDelta / open) >= priceChangeThreshold).

The market isn't too volatile (lowVolatility).

The trend supports the direction of the price change (trendUp for bullish, trendDown for bearish).

If all these conditions are met, it predicts:

1 (Bullish) if conditions suggest buying.

0 (Bearish) if conditions suggest selling.

Cooldown Mechanism:

After a signal, the script waits for a number of bars (cooldownPeriod) before considering another signal to avoid over-trading.

Visual Feedback:

Labels are placed on the chart:

Green label for bullish breakouts below the low price.

Red label for bearish breakouts above the high price.

How to Use:

Entry Points: Look for the labels on your chart to decide when to enter trades.

Risk Management: Since this is for scalping, ensure each trade has tight stop-losses to manage risk due to the quick, small movements.

Market Conditions: This strategy might work best in markets with consistent volume and price changes but not extreme volatility.

Caveats:

This isn't real AI; it's a heuristic based on volume and price. Actual AI would involve machine learning algorithms trained on historical data.

Always backtest any strategy, and consider how it behaves in different market conditions, not just the ones it was designed for.

ATR stop lossPlots the stop loss level based on average true range (ATR) and a multiplier of choice (1 to 2.5, default is 1.5), subtracted from closing price.

Additions in this version:

You can now show percentage labels to help evaluate the level of risk.

The color of the plotted line and the text labels can be picked by the user.

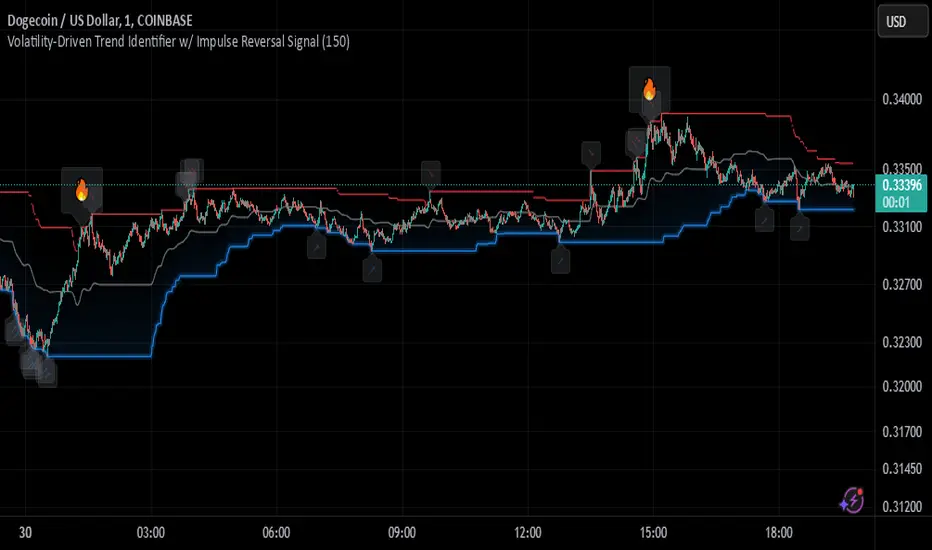

Johnny's Volatility-Driven Trend Identifier w/ Reversal SignalsJohnny's Volatility-Driven Trend Identifier w/ Reversal Signals is designed to identify high-probability trend shifts and reversals by incorporating volatility, momentum, and impulse-based filtering. It is specifically built for traders who want to capture strong trend movements while minimizing false signals caused by low volatility noise.

By leveraging Rate of Change (ROC), Relative Strength Index (RSI), and Average True Range (ATR)-based volatility detection, the indicator dynamically adapts to market conditions. It highlights breakout trends, reversals, and early signs of momentum shifts using strategically placed labels and color-coded trend visualization.

Inspiration taken from Top G indicator .

What This Indicator Does

The Volatility-Driven Trend Identifier works by:

Measuring Market Extremes & Momentum:

Uses ROC normalization with standard deviation to identify impulse moves in price action.

Implements RSI filtering to determine overbought/oversold conditions that validate trend strength.

Utilizes ATR-based volatility tracking to ensure signals only appear when meaningful market movements are occurring.

Identifying Key Trend Events:

Power Peak (🔥): Marks a confirmed strong downtrend, ideal for shorting opportunities.

Surge (🚀): Indicates a confirmed strong uptrend, signaling a potential long entry.

Soft Surge (↗): Highlights a mild bullish reentry or early uptrend formation.

Soft Peak (↘): Shows a mild bearish reentry or early downtrend formation.

Providing Adaptive Filtering for Reliable Signals:

Filters out weak trends with a volatility check, ensuring signals appear only in strong market conditions.

Implements multi-level confirmation by combining trend strength metrics, preventing false breakouts.

Uses gradient-based visualization to color-code market sentiment for quick interpretation.

What This Indicator Signals

Breakouts & Impulse Moves: 🚀🔥

The Surge (🚀) and Power Peak (🔥) labels indicate confirmed momentum breakouts, where the trend has been validated by a combination of ROC impulse, RSI confirmation, and ATR volatility filtering.

These signals suggest that the market is entering a strong trend, and traders can align their entries accordingly.

Early Trend Formation & Reentries: ↗ ↘

The Soft Surge (↗) and Soft Peak (↘) labels indicate areas where a trend might be forming, but is not yet fully confirmed.

These signals help traders anticipate potential entries before the trend gains full strength.

Volatility-Adaptive Trend Filtering: 📊

Since the indicator only activates in volatile conditions, it avoids the pitfalls of low-range choppy markets where false signals frequently occur.

ATR-driven adaptive windowing allows the indicator to dynamically adjust its sensitivity based on real-time volatility conditions.

How to Use This Indicator

1. Identifying High-Probability Entries

Bullish Entries (Long Trades)

Look for 🚀 Surge signals in an uptrend.

Confirm with RSI (should be above 50 for momentum).

Ensure volatility is increasing to validate the breakout.

Use ↗ Soft Surge signals for early entries before the trend fully confirms.

Bearish Entries (Short Trades)

Look for 🔥 Power Peak signals in a downtrend.

RSI should be below 50, indicating downward momentum.

Volatility should be rising, ensuring market momentum is strong.

Use ↘ Soft Peak signals for early entries before a full bearish confirmation.

2. Avoiding False Signals

Ignore signals when the market is ranging (low ATR).

Check RSI and ROC alignment to ensure trend confirmation.

Use additional confluences (e.g., price action, support/resistance levels, moving averages) for enhanced accuracy.

3. Trend Confirmation & Filtering

The stronger the trend, the higher the likelihood that Surge (🚀) and Power Peak (🔥) signals will continue in their direction.

Soft Surge (↗) and Soft Peak (↘) act as early warning signals before major breakouts occur.

What Makes This a Machine Learning-Inspired Moving Average?

While this indicator is not a direct implementation of machine learning (as Pine Script lacks AI/ML capabilities), it mimics machine learning principles by adapting dynamically to market conditions using the following techniques:

Adaptive Trend Selection:

It does not rely on fixed moving averages but instead adapts dynamically based on volatility expansion and momentum detection.

ATR-based filtering adjusts the indicator’s sensitivity to real-time conditions.

Multi-Factor Confirmation (Feature Engineering Equivalent in ML):

Combines ROC, RSI, and ATR in a structured way, similar to how ML models use multiple inputs to filter and classify data.

Implements conditional trend recognition, ensuring that only valid signals pass through the filter.

Noise Reduction with Data Smoothing:

The algorithm avoids false signals by incorporating trend intensity thresholds, much like how ML models remove outliers to refine predictions.

Adaptive filtering ensures that low-volatility environments do not produce misleading signals.

Why Use This Indicator?

✔ Reduces False Signals: Multi-factor validation ensures only high-confidence signals are triggered.

✔ Works in All Market Conditions: Volatility-adaptive nature allows the indicator to perform well in both trending and ranging markets.

✔ Great for Swing & Intraday Trading: It helps spot momentum shifts early and allows traders to catch major market moves before they fully develop.

✔ Visually Intuitive: Color-coded trends and clear signal markers make it easy to interpret.

Average Candle Size (Points)ATR but with the ability to add threshold lines (UP TO 3) that help gauge how volatile the market is. Also, note that the default threshold values are set up for NQ Futures so you will need to change your values to your specific needs.

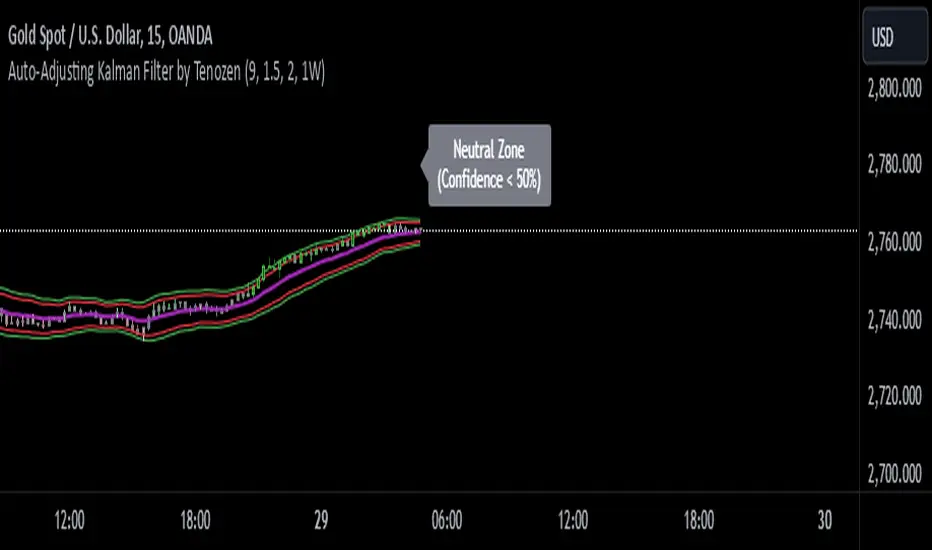

Auto-Adjusting Kalman Filter by TenozenNew year, new indicator! Auto-Adjusting Kalman Filter is an indicator designed to provide an adaptive approach to trend analysis. Using the Kalman Filter (a recursive algorithm used in signal processing), this algo dynamically adjusts to market conditions, offering traders a reliable way to identify trends and manage risk! In other words, it's a remaster of my previous indicator, Kalman Filter by Tenozen.

What's the difference with the previous indicator (Kalman Filter by Tenozen)?

The indicator adjusts its parameters (Q and R) in real-time using the Average True Range (ATR) as a measure of market volatility. This ensures the filter remains responsive during high-volatility periods and smooth during low-volatility conditions, optimizing its performance across different market environments.

The filter resets on a user-defined timeframe, aligning its calculations with dominant trends and reducing sensitivity to short-term noise. This helps maintain consistency with the broader market structure.

A confidence metric, derived from the deviation of price from the Kalman filter line (measured in ATR multiples), is visualized as a heatmap:

Green : Bullish confidence (higher values indicate stronger trends).

Red : Bearish confidence (higher values indicate stronger trends).

Gray : Neutral zone (low confidence, suggesting caution).

This provides a clear, objective measure of trend strength.

How it works?

The Kalman Filter estimates the "true" price by filtering out market noise. It operates in two steps, that is, prediction and update. Prediction is about projection the current state (price) forward. Update is about adjusting the prediction based on the latest price data. The filter's parameters (Q and R) are scaled using normalized ATR, ensuring adaptibility to changing market conditions. So it means that, Q (Process Noise) increases during high volatility, making the filter more responsive to price changes and R (Measurement Noise) increases during low volatility, smoothing out the filter to avoid overreacting to minor fluctuations. Also, the trend confidence is calculated based on the deviation of price from the Kalman filter line, measured in ATR multiples, this provides a quantifiable measure of trend strength, helping traders assess market conditions objectively.

How to use?

Use the Kalman Filter line to identify the prevailing trend direction. Trade in alignment with the filter's slope for higher-probability setups.

Look for pullbacks toward the Kalman Filter line during strong trends (high confidence zones)

Utilize the dynamic stop-loss and take-profit levels to manage risk and lock in profits

Confidence Heatmap provides an objective measure of market sentiment, helping traders avoid low-confidence (neutral) zones and focus on high-probability opportunities

Guess that's it! I hope this indicator helps! Let me know if you guys got some feedback! Ciao!

ATR BeamsATR Beams is a simple indicator that utilizes the ATR to determine levels above and below price action that can serve as stop loss or trailing visual aids across all instruments.

This indicator is preset to an ATR value of 14 and a multiplier of 1 for the ATR.

Both of these parameters can be modified to your specific trading preference, the color and indicator line style can both also be modified to your visual preference.

I hope this provides you with a good visual aid

IU Range Trading StrategyIU Range Trading Strategy

The IU Range Trading Strategy is designed to identify range-bound markets and take trades based on defined price ranges. This strategy uses a combination of price ranges and ATR (Average True Range) to filter entry conditions and incorporates a trailing stop-loss mechanism for better trade management.

User Inputs:

- Range Length: Defines the number of bars to calculate the highest and lowest price range (default: 10).

- ATR Length: Sets the length of the ATR calculation (default: 14).

- ATR Stop-Loss Factor: Determines the multiplier for the ATR-based stop-loss (default: 2.00).

Entry Conditions:

1. A range is identified when the difference between the highest and lowest prices over the selected range is less than or equal to 1.75 times the ATR.

2. Once a valid range is formed:

- A long trade is triggered at the range high.

- A short trade is triggered at the range low.

Exit Conditions:

1. Trailing Stop-Loss:

- The stop-loss adjusts dynamically using ATR targets.

- The strategy locks in profits as the trade moves in your favor.

2. The stop-loss and take-profit levels are visually plotted for transparency and easier decision-making.

Features:

- Automated box creation to visualize the trading range.

- Supports one position at a time, canceling opposite-side entries.

- ATR-based trailing stop-loss for effective risk management.

- Clear visual representation of stop-loss and take-profit levels with colored bands.

This strategy works best in markets with defined ranges and can help traders identify breakout opportunities when the price exits the range.