Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

Backquant

Rolling Log Returns [BackQuant]Rolling Log Returns

The Rolling Log Returns indicator is a versatile tool designed to help traders, quants, and data-driven analysts evaluate the dynamics of price changes using logarithmic return analysis. Widely adopted in quantitative finance, log returns offer several mathematical and statistical advantages over simple returns, making them ideal for backtesting, portfolio optimization, volatility modeling, and risk management.

What Are Log Returns?

In quantitative finance, logarithmic returns are defined as:

ln(Pₜ / Pₜ₋₁)

or for rolling periods:

ln(Pₜ / Pₜ₋ₙ)

where P represents price and n is the rolling lookback window.

Log returns are preferred because:

They are time additive : returns over multiple periods can be summed.

They allow for easier statistical modeling , especially when assuming normally distributed returns.

They behave symmetrically for gains and losses, unlike arithmetic returns.

They normalize percentage changes, making cross-asset or cross-timeframe comparisons more consistent.

Indicator Overview

The Rolling Log Returns indicator computes log returns either on a standard (1-period) basis or using a rolling lookback period , allowing users to adapt it to short-term trading or long-term trend analysis.

It also supports a comparison series , enabling traders to compare the return structure of the main charted asset to another instrument (e.g., SPY, BTC, etc.).

Core Features

✅ Return Modes :

Normal Log Returns : Measures ln(price / price ), ideal for day-to-day return analysis.

Rolling Log Returns : Measures ln(price / price ), highlighting price drift over longer horizons.

✅ Comparison Support :

Compare log returns of the primary instrument to another symbol (like an index or ETF).

Useful for relative performance and market regime analysis .

✅ Moving Averages of Returns :

Smooth noisy return series with customizable MA types: SMA, EMA, WMA, RMA, and Linear Regression.

Applicable to both primary and comparison series.

✅ Conditional Coloring :

Returns > 0 are colored green ; returns < 0 are red .

Comparison series gets its own unique color scheme.

✅ Extreme Return Detection :

Highlight unusually large price moves using upper/lower thresholds.

Visually flags abnormal volatility events such as earnings surprises or macroeconomic shocks.

Quantitative Use Cases

🔍 Return Distribution Analysis :

Gain insight into the statistical properties of asset returns (e.g., skewness, kurtosis, tail behavior).

📉 Risk Management :

Use historical return outliers to define drawdown expectations, stress tests, or VaR simulations.

🔁 Strategy Backtesting :

Apply rolling log returns to momentum or mean-reversion models where compounding and consistent scaling matter.

📊 Market Regime Detection :

Identify periods of consistent overperformance/underperformance relative to a benchmark asset.

📈 Signal Engineering :

Incorporate return deltas, moving average crossover of returns, or threshold-based triggers into machine learning pipelines or rule-based systems.

Recommended Settings

Use Normal mode for high-frequency trading signals.

Use Rolling mode for swing or trend-following strategies.

Compare vs. a broad market index (e.g., SPY or QQQ ) to extract relative strength insights.

Set upper and lower thresholds around ±5% for spotting major volatility days.

Conclusion

The Rolling Log Returns indicator transforms raw price action into a statistically sound return series—equipping traders with a professional-grade lens into market behavior. Whether you're conducting exploratory data analysis, building factor models, or visually scanning for outliers, this indicator integrates seamlessly into a modern quant's toolbox.

Wavelet Filter with Adaptive Upsampling [BackQuant]Wavelet Filter with Adaptive Upsampling

The Wavelet Filter with Adaptive Upsampling is an advanced filtering and signal reconstruction tool designed to enhance the analysis of financial time series data. It combines wavelet transforms with adaptive upsampling techniques to filter and reconstruct price data, making it ideal for capturing subtle market movements and enhancing trend detection. This system uses high-pass and low-pass filters to decompose the price series into different frequency components, applying adaptive thresholding to eliminate noise and preserve relevant signal information.

Shout out to Loxx for the Least Squares fitting of trigonometric series and Quinn and Fernandes algorithm for finding frequency

www.tradingview.com

Key Features

1. Frequency Decomposition with High-Pass and Low-Pass Filters:

The indicator decomposes the input time series using high-pass and low-pass filters to separate the high-frequency (detail) and low-frequency (trend) components of the data. This decomposition allows for a more accurate analysis of underlying trends, while mitigating the impact of noise.

2. Soft Thresholding for Noise Reduction:

A soft thresholding function is applied to the high-frequency component, allowing for the reduction of noise while retaining significant market signals. This function adjusts the coefficients of the high-frequency data, removing small fluctuations and leaving only the essential price movements.

3. Adaptive Upsampling Process:

The upsampling process in this script can be customized using different methods: sinusoidal upsampling, advanced upsampling, and simple upsampling. Each method serves a unique purpose:

Sinusoidal Upsample uses a sine wave to interpolate between data points, providing a smooth transition.

Advanced Upsample utilizes a Quinn-Fernandes algorithm to estimate frequency and apply more sophisticated interpolation techniques, adapting to the market’s cyclical behavior.

Simple Upsample linearly interpolates between data points, providing a basic upsampling technique for less complex analysis.

4. Reconstruction of Filtered Signal:

The indicator reconstructs the filtered signal by summing the high and low-frequency components after upsampling. This allows for a detailed yet smooth representation of the original time series, which can be used for analyzing underlying trends in the market.

5. Visualization of Reconstructed Data:

The reconstructed series is plotted, showing how the upsampling and filtering process enhances the clarity of the price movements. Additionally, the script provides the option to visualize the log returns of the reconstructed series as a histogram, with positive returns shown in green and negative returns in red.

6. Cumulative Series and Trend Detection:

A cumulative series is plotted to visualize the compounded effect of the filtered and reconstructed data. This feature helps traders track the overall performance of the asset over time, identifying whether the asset is following a sustained upward or downward trend.

7. Adaptive Thresholding and Noise Estimation:

The system estimates the noise level in the high-frequency component and applies an adaptive thresholding process based on the standard deviation of the downsampled data. This ensures that only significant price movements are retained, further refining the trend analysis.

8. Customizable Parameters for Flexibility:

Users can customize the following parameters to adjust the behavior of the indicator:

Frequency and Phase Shift: Control the periodicity of the wavelet transformation and the phase of the upsampling function.

Upsample Factor: Adjust the level of interpolation applied during the upsampling process.

Smoothing Period: Determine the length of time used to smooth the signal, helping to filter out short-term fluctuations.

References

Enhancing Cross-Sectional Currency Strategies with Context-Aware Learning to Rank

arxiv.org

Daubechies Wavelet - Wikipedia

en.wikipedia.org

Quinn Fernandes Fourier Transform of Filtered Price by Loxx

Note on Usage for Mean-Reversion Strategy

This indicator is primarily designed for trend-following strategies. However, by taking the inverse of the signals, it can be adapted for mean-reversion strategies. This involves buying underperforming assets and selling outperforming ones. Caution: This method may not work effectively with highly correlated assets, as the price movements between correlated assets tend to mirror each other, limiting the effectiveness of mean-reversion strategies.

Final Thoughts

The Wavelet Filter with Adaptive Upsampling is a powerful tool for traders seeking to improve their understanding of market trends and noise. By using advanced wavelet decomposition and adaptive upsampling, this system offers a clearer, more refined picture of price movements, enhancing trend-following strategies. It’s particularly useful for detecting subtle shifts in market momentum and reconstructing price data in a way that removes noise, providing more accurate insights into market conditions.

Volume Momentum [BackQuant]Volume Momentum

The Volume Momentum indicator is designed to help traders identify shifts in market momentum based on volume data. By analyzing the relative volume momentum, this indicator provides insights into whether the market is gaining strength (uptrend) or losing momentum (downtrend). The strategy uses a combination of percentile-based volume normalization, weighted moving averages (WMA), and exponential moving averages (EMA) to assess volume trends.

The system focuses on the relationship between price and volume, utilizing normalized volume data to highlight key market changes. This approach allows traders to focus on volume-driven price movements, helping them to capture momentum shifts early.

Key Features

1. Volume Normalization and Percentile Calculation:

The signed volume (positive when the close is higher than the open, negative when the close is lower) is normalized against the rolling average volume. This normalized volume is then subjected to a percentile interpolation, allowing for a robust statistical measure of how the current volume compares to historical data. The percentile level is customizable, with 50 representing the median.

2. Weighted and Smoothed Moving Averages for Trend Detection:

The normalized volume is smoothed using weighted moving averages (WMA) and exponential moving averages (EMA). These smoothing techniques help eliminate noise, providing a clearer view of the underlying momentum. The WMA filters out short-term fluctuations, while the EMA ensures that the most recent data points have a higher weight, making the system more responsive to current market conditions.

3. Trend Reversal Detection:

The indicator detects momentum shifts by evaluating whether the volume momentum crosses above or below zero. A positive volume momentum indicates a potential uptrend, while a negative momentum suggests a possible downtrend. These trend reversals are identified through crossover and crossunder conditions, triggering alerts when significant changes occur.

4. Dynamic Trend Background and Bar Coloring:

The script offers customizable background coloring based on the trend direction. When volume momentum is positive, the background is colored green, indicating a bullish trend. When volume momentum is negative, the background is colored red, signaling a bearish trend. Additionally, the bars themselves can be colored based on the trend, further helping traders quickly visualize market momentum.

5. Alerts for Momentum Shifts:

The system provides real-time alerts for traders to monitor when volume momentum crosses a critical threshold (zero), signaling a trend reversal. The alerts notify traders when the market momentum turns bullish or bearish, assisting them in making timely decisions.

6. Customizable Parameters for Flexible Usage:

Users can fine-tune the behavior of the indicator by adjusting various parameters:

Volume Rolling Mean: The period used to calculate the average volume for normalization.

Percentile Interpolation Length: Defines the range over which the percentile is calculated.

Percentile Level: Determines the percentile threshold (e.g., 50 for the median).

WMA and Smoothing Periods: Control the smoothing and response time of the indicator.

7. Trend Background Visualization and Trend-Based Bar Coloring:

The background fill is shaded according to whether the volume momentum is positive or negative, providing a visual cue to indicate market strength. Additionally, bars can be color-coded to highlight the trend, making it easier to see the trend’s direction without needing to analyze numerical data manually.

8. Note on Mean-Reversion Strategy:

If you take the inverse of the signals, this indicator can be adapted for a mean-reversion strategy. Instead of following the trend, the strategy would involve buying assets that are underperforming and selling assets that are overperforming, based on volume momentum. However, it’s important to note that this approach may not work effectively on highly correlated assets, as their price movements may be too similar, reducing the effectiveness of the mean-reversion strategy.

Final Thoughts

The Volume Momentum indicator offers a comprehensive approach to analyzing volume-based momentum shifts in the market. By using volume normalization, percentile interpolation, and smoothed moving averages, this system helps identify the strength and direction of market trends. Whether used for trend-following or adapted for mean-reversion, this tool provides traders with actionable insights into the market’s volume-driven movements, improving decision-making and portfolio management.

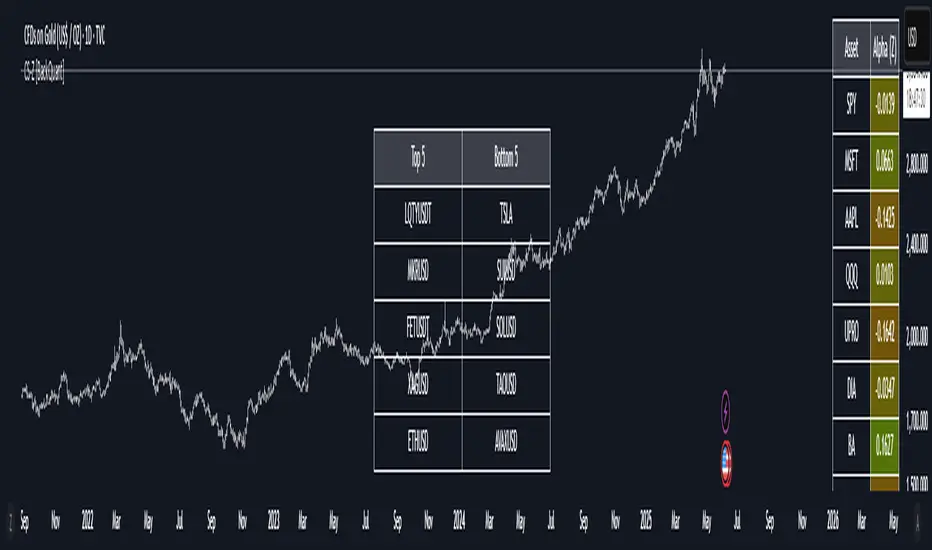

40 Ticker Cross-Sectional Z-Scores [BackQuant]40 Ticker Cross-Sectional Z-Scores

BackQuant’s 40 Ticker Cross-Sectional Z-Scores is a powerful portfolio management strategy that analyzes the relative performance of up to 40 different assets, comparing them on a cross-sectional basis to identify the top and bottom performers. This indicator computes Z-scores for each asset based on their log returns and evaluates them relative to the mean and standard deviation over a rolling window. The Z-scores represent how far an asset's return deviates from the average, and these values are used to rank the assets, allowing for dynamic asset allocation based on performance.

By focusing on the strongest-performing assets and avoiding the weakest, this strategy aims to enhance returns while managing risk. Additionally, by adjusting for standard deviations, the system offers a risk-adjusted method of ranking assets, making it suitable for traders who want to dynamically allocate capital based on performance metrics rather than just price movements.

Key Features

1. Cross-Sectional Z-Score Calculation:

The system calculates Z-scores for 40 different assets, evaluating their log returns against the mean and standard deviation over a rolling window. This enables users to assess the relative performance of each asset dynamically, highlighting which assets are performing better or worse compared to their historical norms. The Z-score is a useful statistical tool for identifying outliers in asset performance.

2. Asset Ranking and Allocation:

The system ranks assets based on their Z-scores and allocates capital to the top performers. It identifies the top and bottom assets, and traders can allocate capital to the top-performing assets, ensuring that their portfolio is aligned with the best performers. Conversely, the bottom assets are removed from the portfolio, reducing exposure to underperforming assets.

3. Rolling Window for Mean and Standard Deviation Calculations:

The Z-scores are calculated based on rolling means and standard deviations, making the system adaptive to changing market conditions. This rolling calculation window allows the strategy to adjust to recent performance trends and minimize the impact of outdated data.

4. Mean and Standard Deviation Visualization:

The script provides real-time visualizations of the mean (x̄) and standard deviation (σ) of asset returns, helping traders quickly identify trends and volatility in their portfolio. These visual indicators are useful for understanding the current market environment and making more informed allocation decisions.

5. Top & Bottom Performer Tables:

The system generates tables that display the top and bottom performers, ranked by their Z-scores. Traders can quickly see which assets are outperforming and underperforming. These tables provide clear and actionable insights, helping traders make informed decisions about which assets to include in their portfolio.

6. Customizable Parameters:

The strategy allows traders to customize several key parameters, including:

Rolling Calculation Window: Set the window size for the rolling mean and standard deviation calculations.

Top & Bottom Tickers: Choose how many of the top and bottom assets to display and allocate capital to.

Table Orientation: Select between vertical or horizontal table formats to suit the user’s preference.

7. Forward Test & Out-of-Sample Testing:

The system includes out-of-sample forward tests, ensuring that the strategy is evaluated based on real-time performance, not just historical data. This forward testing approach helps validate the robustness of the strategy in dynamic market conditions.

8. Visual Feedback and Alerts:

The system provides visual feedback on the current asset rankings and allocations, with dynamic labels and plots on the chart. Additionally, users receive alerts when allocations change, keeping them informed of important adjustments.

9. Risk Management via Z-Scores and Std Dev:

The system’s approach to asset selection is based on Z-scores, which normalize performance relative to the historical mean. By incorporating standard deviation, it accounts for the volatility and risk associated with each asset. This allows for more precise risk management and portfolio construction.

10. Note on Mean Reversion Strategy:

If you take the inverse of the signals provided by this indicator, the strategy can be used for mean-reversion rather than trend-following. This would involve buying the underperforming assets and selling the outperforming ones. However, it's important to note that this approach does not work well with highly correlated assets, as the relationship between the assets could result in the same directional movement, undermining the effectiveness of the mean-reversion strategy.

References

www.uts.edu.au

onlinelibrary.wiley.com

www.cmegroup.com

Final Thoughts

The 40 Ticker Cross-Sectional Z-Scores strategy offers a data-driven approach to portfolio management, dynamically allocating capital based on the relative performance of assets. By using Z-scores and standard deviations, this strategy ensures that capital is directed to the strongest performers while avoiding weaker assets, ultimately improving the risk-adjusted returns of the portfolio. Whether you’re focused on trend-following or looking to explore mean-reversion strategies, this flexible system can be tailored to suit your investment goals.

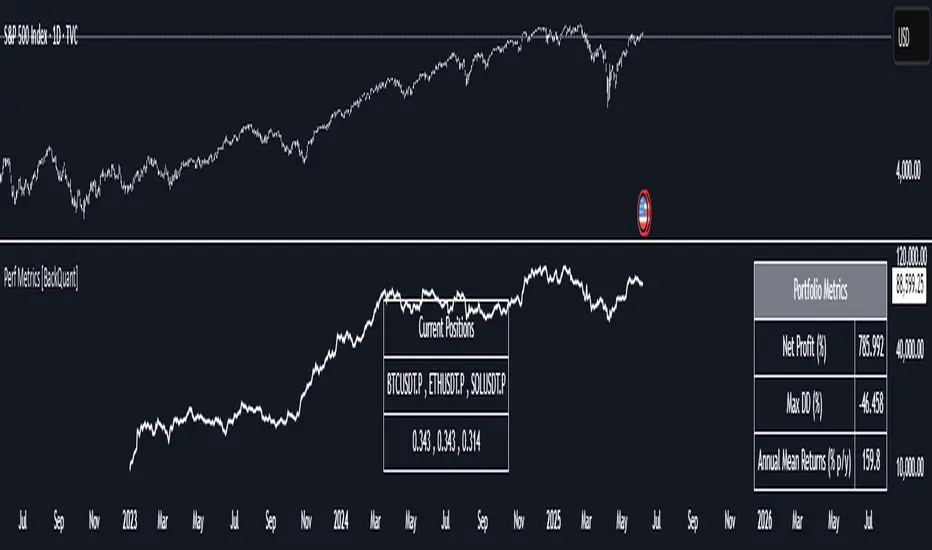

Performance Metrics With Bracketed Rebalacing [BackQuant]Performance Metrics With Bracketed Rebalancing

The Performance Metrics With Bracketed Rebalancing script offers a robust method for assessing portfolio performance, integrating advanced portfolio metrics with different rebalancing strategies. With a focus on adaptability, the script allows traders to monitor and adjust portfolio weights, equity, and other key financial metrics dynamically. This script provides a versatile approach for evaluating different trading strategies, considering factors like risk-adjusted returns, volatility, and the impact of portfolio rebalancing.

Please take the time to read the following:

Key Features and Benefits of Portfolio Methods

Bracketed Rebalancing:

Bracketed Rebalancing is an advanced strategy designed to trigger portfolio adjustments when an asset's weight surpasses a predefined threshold. This approach minimizes overexposure to any single asset while maintaining flexibility in response to market changes. The strategy is particularly beneficial for mitigating risks that arise from significant asset weight fluctuations. The following image illustrates how this method reacts when asset weights cross the threshold:

Daily Rebalancing:

Unlike the bracketed method, Daily Rebalancing adjusts portfolio weights every trading day, ensuring consistent asset allocation. This method aims for a more even distribution of portfolio weights, making it a suitable option for traders who prefer less sensitivity to individual asset volatility. Here's an example of Daily Rebalancing in action:

No Rebalancing:

For traders who prefer a passive approach, the "No Rebalancing" option allows the portfolio to remain static, without any adjustments to asset weights. This method may appeal to long-term investors or those who believe in the inherent stability of their selected assets. Here’s how the portfolio looks when no rebalancing is applied:

Portfolio Weights Visualization:

One of the standout features of this script is the visual representation of portfolio weights. With adjustable settings, users can track the current allocation of assets in real-time, making it easier to analyze shifts and trends. The following image shows the real-time weight distribution across three assets:

Rolling Drawdown Plot:

Managing drawdown risk is a critical aspect of portfolio management. The Rolling Drawdown Plot visually tracks the drawdown over time, helping traders monitor the risk exposure and performance relative to the peak equity levels. This feature is essential for assessing the portfolio's resilience during market downturns:

Daily Portfolio Returns:

Tracking daily returns is crucial for evaluating the short-term performance of the portfolio. The script allows users to plot daily portfolio returns to gain insights into daily profit or loss, helping traders stay updated on their portfolio’s progress:

Performance Metrics

Net Profit (%):

This metric represents the total return on investment as a percentage of the initial capital. A positive net profit indicates that the portfolio has gained value over the evaluation period, while a negative value suggests a loss. It's a fundamental indicator of overall portfolio performance.

Maximum Drawdown (Max DD):

Maximum Drawdown measures the largest peak-to-trough decline in portfolio value during a specified period. It quantifies the most significant loss an investor would have experienced if they had invested at the highest point and sold at the lowest point within the timeframe. A smaller Max DD indicates better risk management and less exposure to significant losses.

Annual Mean Returns (% p/y):

This metric calculates the average annual return of the portfolio over the evaluation period. It provides insight into the portfolio's ability to generate returns on an annual basis, aiding in performance comparison with other investment opportunities.

Annual Standard Deviation of Returns (% p/y):

This measure indicates the volatility of the portfolio's returns on an annual basis. A higher standard deviation signifies greater variability in returns, implying higher risk, while a lower value suggests more stable returns.

Variance:

Variance is the square of the standard deviation and provides a measure of the dispersion of returns. It helps in understanding the degree of risk associated with the portfolio's returns.

Sortino Ratio:

The Sortino Ratio is a variation of the Sharpe Ratio that only considers downside risk, focusing on negative volatility. It is calculated as the difference between the portfolio's return and the minimum acceptable return (MAR), divided by the downside deviation. A higher Sortino Ratio indicates better risk-adjusted performance, emphasizing the importance of avoiding negative returns.

Sharpe Ratio:

The Sharpe Ratio measures the portfolio's excess return per unit of total risk, as represented by standard deviation. It is calculated by subtracting the risk-free rate from the portfolio's return and dividing by the standard deviation of the portfolio's excess return. A higher Sharpe Ratio indicates more favorable risk-adjusted returns.

Omega Ratio:

The Omega Ratio evaluates the probability of achieving returns above a certain threshold relative to the probability of experiencing returns below that threshold. It is calculated by dividing the cumulative probability of positive returns by the cumulative probability of negative returns. An Omega Ratio greater than 1 indicates a higher likelihood of achieving favorable returns.

Gain-to-Pain Ratio:

The Gain-to-Pain Ratio measures the return per unit of risk, focusing on the magnitude of gains relative to the severity of losses. It is calculated by dividing the total gains by the total losses experienced during the evaluation period. A higher ratio suggests a more favorable balance between reward and risk.

www.linkedin.com

Compound Annual Growth Rate (CAGR) (% p/y):

CAGR represents the mean annual growth rate of the portfolio over a specified period, assuming the investment has been compounding over that time. It provides a smoothed annual rate of growth, eliminating the effects of volatility and offering a clearer picture of long-term performance.

Portfolio Alpha (% p/y):

Portfolio Alpha measures the portfolio's performance relative to a benchmark index, adjusting for risk. It is calculated using the Capital Asset Pricing Model (CAPM) and represents the excess return of the portfolio over the expected return based on its beta and the benchmark's performance. A positive alpha indicates outperformance, while a negative alpha suggests underperformance.

Portfolio Beta:

Portfolio Beta assesses the portfolio's sensitivity to market movements, indicating its exposure to systematic risk. A beta greater than 1 suggests the portfolio is more volatile than the market, while a beta less than 1 indicates lower volatility. Beta is used to understand the portfolio's potential for gains or losses in relation to market fluctuations.

Skewness of Returns:

Skewness measures the asymmetry of the return distribution. A positive skew indicates a distribution with a long right tail, suggesting more frequent small losses and fewer large gains. A negative skew indicates a long left tail, implying more frequent small gains and fewer large losses. Understanding skewness helps in assessing the likelihood of extreme outcomes.

Value at Risk (VaR) 95th Percentile:

VaR at the 95th percentile estimates the maximum potential loss over a specified period, given a 95% confidence level. It provides a threshold value such that there is a 95% probability that the portfolio will not experience a loss greater than this amount.

Conditional Value at Risk (CVaR):

CVaR, also known as Expected Shortfall, measures the average loss exceeding the VaR threshold. It provides insight into the tail risk of the portfolio, indicating the expected loss in the worst-case scenarios beyond the VaR level.

These metrics collectively offer a comprehensive view of the portfolio's performance, risk exposure, and efficiency. By analyzing these indicators, investors can make informed decisions, balancing potential returns with acceptable levels of risk.

Conclusion

The Performance Metrics With Bracketed Rebalancing script provides a comprehensive framework for evaluating and optimizing portfolio performance. By integrating advanced metrics, adaptive rebalancing strategies, and visual analytics, it empowers traders to make informed decisions in managing their investment portfolios. However, it's crucial to consider the implications of rebalancing strategies, as academic research indicates that predictable rebalancing can lead to market impact costs. Therefore, adopting flexible and less predictable rebalancing approaches may enhance portfolio performance and reduce associated costs.

PDF-MA Supertrend [BackQuant]PDF-MA Supertrend

The PDF-MA Supertrend combines the innovative Probability Density Function (PDF) smoothing with the widely popular Supertrend methodology, creating a robust tool for identifying trends and generating actionable trading signals. This indicator is designed to provide precise entries and exits by dynamically adapting to market volatility while visualizing long and short opportunities directly on the chart.

Core Feature: PDF Smoothing

At the foundation of this indicator is the PDF smoothing technique, which applies a Probability Density Function to calculate a smoothed moving average. This method allows the indicator to assign adaptive weights to data points, making it responsive to market changes without overreacting to short-term volatility.

Key parameters include:

Variance: Controls the spread of the PDF weighting. A smaller variance results in sharper responses, while a larger variance smooths out the curve.

Mean: Shifts the PDF’s center, allowing traders to tweak how weights are distributed around the data points.

Smoothing Method: Offers the choice between EMA (Exponential Moving Average) and SMA (Simple Moving Average) for blending the PDF-smoothed data with traditional moving average methods.

By combining these parameters, the PDF smoothing creates a moving average that effectively captures underlying trends.

Supertrend: Adaptive Trend and Volatility Tracking

The Supertrend is a well-known volatility-based indicator that dynamically adjusts to market conditions using the ATR (Average True Range). In this script, the PDF-smoothed moving average acts as the price input, making the Supertrend calculation more adaptive and precise.

Key Supertrend Features:

ATR Period: Determines the lookback period for calculating market volatility.

Factor: Multiplies the ATR to set the distance between the Supertrend and the price. A higher factor creates wider bands, filtering out smaller price movements, while a lower factor captures tighter trends.

Dynamic Direction: The Supertrend flips its direction based on price interactions with the calculated upper and lower bands:

Uptrend : When the price is above the Supertrend, the direction turns bullish.

Downtrend : When the price is below the Supertrend, the direction turns bearish.

This combination of PDF smoothing and Supertrend calculation ensures that trends are detected with greater accuracy, while volatility filters out market noise.

Long and Short Signal Generation

The PDF-MA Supertrend generates actionable trading signals by detecting transitions in the trend direction:

Long Signal (𝕃): Triggered when the trend transitions from bearish to bullish. This is visually represented with a green triangle below the price bars.

Short Signal (𝕊): Triggered when the trend transitions from bullish to bearish. This is marked with a red triangle above the price bars.

These signals provide traders with clear entry and exit points, ensuring they can capitalize on emerging trends while avoiding false signals.

Customizable Visualization Options

The indicator offers a range of visualization settings to help traders interpret the data with ease:

Show Supertrend: Option to toggle the visibility of the Supertrend line.

Candle Coloring: Automatically colors candlesticks based on the trend direction:

Green for long trends.

Red for short trends.

Long and Short Signals (𝕃 + 𝕊): Displays long (𝕃) and short (𝕊) signals directly on the chart for quick identification of trade opportunities.

Line Color Customization: Allows users to customize the colors for long and short trends.

Alert Conditions

To ensure traders never miss an opportunity, the PDF-MA Supertrend includes built-in alerts for trend changes:

Long Signal Alert: Notifies when a bullish trend is identified.

Short Signal Alert: Notifies when a bearish trend is identified.

These alerts can be configured for real-time notifications via SMS, email, or push notifications, making it easier to stay updated on market movements.

Suggested Parameter Adjustments

The indicator’s effectiveness can be fine-tuned using the following guidelines:

Variance:

For low-volatility assets (e.g., indices): Use a smaller variance (1.0–1.5) for smoother trends.

For high-volatility assets (e.g., cryptocurrencies): Use a larger variance (1.5–2.0) to better capture rapid price changes.

ATR Factor:

A higher factor (e.g., 2.0) is better suited for long-term trend-following strategies.

A lower factor (e.g., 1.5) captures shorter-term trends.

Smoothing Period:

Shorter periods provide more reactive signals but may increase noise.

Longer periods offer stability and better alignment with significant trends.

Experimentation is encouraged to find the optimal settings for specific assets and trading strategies.

Trading Applications

The PDF-MA Supertrend is a versatile indicator suited to a variety of trading approaches:

Trend Following : Use the Supertrend line and signals to follow market trends and ride sustained price movements.

Reversal Trading : Spot potential trend reversals as the Supertrend flips direction.

Volatility Analysis : Adjust the ATR factor to filter out minor price fluctuations or capture sharp movements.

Final Thoughts

The PDF-MA Supertrend combines the precision of Probability Density Function smoothing with the adaptability of the Supertrend methodology, offering traders a powerful tool for identifying trends and volatility. With its customizable parameters, actionable signals, and built-in alerts, this indicator is an excellent choice for traders seeking a robust and reliable system for trend detection and entry/exit timing.

As always, backtesting and incorporating this indicator into a broader strategy are recommended for optimal results.

Radial Basis Kernal ATR [BackQuant]Radial Basis Kernel ATR

The Radial Basis Kernel ATR is a trading indicator that combines the classic Average True Range (ATR) with advanced Radial Basis Function (RBF) kernel smoothing . This innovative approach creates a highly adaptive and precise tool for detecting volatility, identifying trends, and providing dynamic support and resistance levels.

With its configurable parameters and ability to adjust to market conditions, this indicator offers traders a robust framework for making informed decisions across various assets and timeframes.

Key Feature: Radial Basis Function Kernel Smoothing

The Radial Basis Function (RBF) kernel is at the heart of this indicator, applying sophisticated mathematical techniques to smooth price data and calculate an enhanced version of ATR. By weighting data points dynamically, the RBF kernel ensures that recent price movements are given appropriate emphasis without overreacting to short-term noise.

The RBF kernel uses a gamma factor to control the degree of smoothing, making it highly adaptable to different asset classes and market conditions:

Gamma Factor Adjustment :

For low-volatility data (e.g., indices), a smaller gamma (0.05–0.1) ensures smoother trends and avoids overly sharp responses.

For high-volatility data (e.g., cryptocurrencies), a larger gamma (0.1–0.2) captures the increased price fluctuations while maintaining stability.

Experimentation is Key : Traders are encouraged to backtest and visually compare different gamma values to find the optimal setting for their specific asset and strategy.

The gamma factor dynamically adjusts based on the variance of the source data, ensuring the indicator remains effective across a wide range of market conditions.

Average True Range (ATR) with Dynamic Bands

The ATR is a widely used volatility measure that captures the degree of price movement over a specific period. This indicator enhances the traditional ATR by integrating the RBF kernel, resulting in a smoothed and adaptive ATR calculation.

Dynamic bands are created around the RBF kernel output using a user-defined ATR factor , offering valuable insights into potential support and resistance zones. These bands expand and contract based on market volatility, providing a visual representation of potential price movement.

Moving Average Confluence

For additional confirmation, the indicator includes the option to overlay a moving average on the smoothed ATR. Traders can choose from several moving average types, such as EMA , SMA , or Hull , and adjust the lookback period to suit their strategy. This feature helps identify broader trends and potential confluence areas, making the indicator even more versatile.

Long and Short Trend Detection

The indicator provides long and short signals based on the directional movement of the smoothed ATR:

Long Signal : Triggered when the ATR crosses above its previous value, indicating bullish momentum.

Short Signal : Triggered when the ATR crosses below its previous value, signaling bearish momentum.

These trend signals are visually highlighted on the chart with green and red bar coloring (optional), providing clear and actionable insights.

Customization Options

The Radial Basis Kernel ATR offers extensive customization options, allowing traders to tailor the indicator to their preferences:

RBF Kernel Settings

Source : Select the price data (e.g., close, high, low) used for the kernel calculation.

Kernel Length : Define the lookback period for the RBF kernel, controlling the smoothing effect.

Gamma Factor : Adjust the smoothing sensitivity, with smaller values for smoother trends and larger values for responsiveness.

ATR Settings

ATR Period : Set the period for ATR calculation, with shorter periods capturing more short-term volatility and longer periods providing a broader view.

ATR Factor : Adjust the scaling of ATR bands for dynamic support and resistance levels.

Confluence Settings

Moving Average Type : Choose from various moving average types for additional trend confirmation.

Moving Average Period : Define the lookback period for the moving average overlay.

Visualization

Trend Coloring : Enable or disable bar coloring based on trend direction (green for long, red for short).

Background Highlighting : Add optional background shading to emphasize long and short trends visually.

Line Width : Customize the thickness of the plotted ATR line for better visibility.

Alerts and Automation

To help traders stay on top of market movements, the indicator includes built-in alerts for trend changes:

Kernel ATR Trend Up : Triggered when the ATR indicates a bullish trend.

Kernel ATR Trend Down : Triggered when the ATR signals a bearish trend.

These alerts ensure traders never miss important opportunities, providing timely notifications directly to their preferred device.

Suggested Gamma Values

The effectiveness of the gamma factor depends on the asset type and the selected kernel length:

Low Volatility Assets (e.g., indices): Use a smaller gamma factor (approximately 0.05–0.1) for smoother trends.

High Volatility Assets (e.g., crypto): Use a larger gamma factor (approximately 0.1–0.2) to capture sharper price movements.

Experimentation : Fine-tune the gamma factor using backtests or visual comparisons to optimize for specific assets and strategies.

Trading Applications

The Radial Basis Kernel ATR is a versatile tool suitable for various trading styles and strategies:

Trend Following : Use the smoothed ATR and dynamic bands to identify and follow trends with confidence.

Reversal Trading : Spot potential reversals by observing interactions with dynamic ATR bands and moving average confluence.

Volatility Analysis : Analyze market volatility to adjust risk management strategies or position sizing.

Final Thoughts

The Radial Basis Kernel ATR combines advanced mathematical techniques with the practical utility of ATR, offering traders a powerful and adaptive tool for volatility analysis and trend detection. Its ability to dynamically adjust to market conditions through the RBF kernel and gamma factor makes it a unique and indispensable part of any trader's toolkit.

By combining sophisticated smoothing , dynamic bands , and customizable visualization , this indicator enhances the ability to read market conditions and make more informed trading decisions. As always, backtesting and incorporating it into a broader strategy are recommended for optimal results.

PDF MA For Loop [BackQuant]PDF MA For Loop

Introducing the PDF MA For Loop, an innovative trading indicator that combines Probability Density Function (PDF) smoothing with a dynamic for-loop scoring mechanism. This advanced tool provides traders with precise trend-following signals, helping to identify long and short opportunities with improved clarity and adaptability to market conditions.

If you would like to check out the stand alone PDF Moving Average:

Core Concept: Probability Density Function (PDF) Smoothing

The PDF smoothing method is a unique approach that applies adaptive weights to price data based on a Probability Density Function. This ensures that recent data points receive appropriate emphasis while maintaining a smooth transition across the data set. The result is a moving average that is not only smoother but also more responsive to market changes.

Key parameters in PDF smoothing:

Variance : Controls the spread of the PDF, where a higher value results in broader smoothing and a lower value makes the moving average more sensitive.

Mean : Centers the PDF around a specific value, influencing the weighting and responsiveness of the smoothing process.

By combining PDF smoothing with traditional moving averages (EMA or SMA), the indicator creates a hybrid signal that balances responsiveness and reliability.

For-Loop Scoring Mechanism

At the heart of this indicator is the for-loop scoring mechanism, which evaluates the smoothed PDF moving average over a defined range of historical data points. This process assigns a score to the current market condition based on whether the PDF moving average is greater than or less than previous values.

Long Signal: A long signal is generated when the score exceeds the Long Threshold (default set at 40), indicating upward momentum.

Short Signal: A short signal is triggered when the score crosses below the Short Threshold (default set at -10), suggesting potential downward momentum.

This dynamic scoring system ensures that the indicator remains adaptive, capturing trends and shifts in market sentiment effectively.

Customization Options

The PDF MA For Loop includes a variety of customizable settings to fit different trading styles and strategies:

Calculation Settings

Price Source : Select the input price for the calculation (default is the close price).

Smoothing Method : Choose between EMA or SMA for the additional smoothing layer, providing flexibility to adapt to market conditions.

Smoothing Period : Adjust the lookback period for the smoothing function, with shorter periods providing more sensitivity and longer periods offering greater stability.

Variance & Mean : Fine-tune the PDF function parameters to control the weighting of the smoothing process.

Signal Settings

Thresholds : Customize the upper and lower thresholds to define the sensitivity of the long and short signals.

For Loop Range : Set the range of historical data points analyzed by the for-loop, influencing the depth of the scoring mechanism.

UI Settings

Signal Line Width: Adjust the thickness of the plotted signal line for better visibility.

Candle Coloring: Enable or disable the coloring of candlesticks based on trend direction (green for long, red for short, gray for neutral).

Background Coloring: Add background shading to highlight long and short signals for an enhanced visual experience.

Alerts and Automation

The indicator includes built-in alert conditions to notify traders of important market events:

Long Signal Alert: Notifies when the score exceeds the upper threshold, indicating a bullish trend.

Short Signal Alert: Notifies when the score crosses below the lower threshold, signaling a bearish trend.

These alerts can be configured for real-time notifications, allowing traders to respond quickly to market changes without constant chart monitoring.

Trading Applications

The PDF MA For Loop is versatile and can be applied across various trading strategies and market conditions:

Trend Following: The PDF smoothing method combined with for-loop scoring makes this indicator particularly effective for identifying and following trends.

Reversal Trading: By observing the thresholds and score, traders can anticipate potential reversals when the trend shifts from long to short (or vice versa).

Risk Management: The dynamic thresholds and scoring provide clear signals, allowing traders to enter and exit trades with greater confidence and precision.

Final Thoughts

The PDF MA For Loopis merges advanced mathematical concepts with practical trading tools. By leveraging Probability Density Function smoothing and a dynamic for-loop scoring system, it provides traders with clear, actionable signals while adapting to market conditions.

Whether you’re looking for an edge in trend-following strategies or seeking precision in identifying reversals, this indicator offers the flexibility and power to enhance your trading decisions

As always, backtesting and integrating the PDF MA For Loop into a comprehensive trading strategy is recommended for optimal performance, as no single indicator should be used in isolation.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Machine Learning RSI [BackQuant]Machine Learning RSI

The Machine Learning RSI is a cutting-edge trading indicator that combines the power of Relative Strength Index (RSI) with Machine Learning (ML) clustering techniques to dynamically determine overbought and oversold thresholds. This advanced indicator adapts to market conditions in real-time, offering traders a robust tool for identifying optimal entry and exit points with increased precision.

Core Concept: Relative Strength Index (RSI)

The RSI is a well-known momentum oscillator that measures the speed and change of price movements, oscillating between 0 and 100. Typically, RSI values above 70 are considered overbought, and values below 30 are considered oversold. However, static thresholds may not be effective in all market conditions.

This script enhances the RSI by integrating a dynamic thresholding system powered by Machine Learning clustering, allowing it to adapt thresholds based on historical RSI behavior and market context.

Machine Learning Clustering for Dynamic Thresholds

The Machine Learning (ML) component uses clustering to calculate dynamic thresholds for overbought and oversold levels. Instead of relying on fixed RSI levels, this indicator clusters historical RSI values into three groups using a percentile-based initialization and iterative optimization:

Cluster 1: Represents lower RSI values (typically associated with oversold conditions).

Cluster 2: Represents mid-range RSI values.

Cluster 3: Represents higher RSI values (typically associated with overbought conditions).

Dynamic thresholds are determined as follows:

Long Threshold: The upper centroid value of Cluster 3.

Short Threshold: The lower centroid value of Cluster 1.

This approach ensures that the indicator adapts to the current market regime, providing more accurate signals in volatile or trending conditions.

Smoothing Options for RSI

To further enhance the effectiveness of the RSI, this script allows traders to apply various smoothing methods to the RSI calculation, including:

Simple Moving Average (SMA)

Exponential Moving Average (EMA)

Weighted Moving Average (WMA)

Hull Moving Average (HMA)

Linear Regression (LINREG)

Double Exponential Moving Average (DEMA)

Triple Exponential Moving Average (TEMA)

Adaptive Linear Moving Average (ALMA)

T3 Moving Average

Traders can select their preferred smoothing method and adjust the smoothing period to suit their trading style and market conditions. The option to smooth the RSI reduces noise and makes the indicator more reliable for detecting trends and reversals.

Long and Short Signals

The indicator generates long and short signals based on the relationship between the RSI value and the dynamic thresholds:

Long Signals: Triggered when the RSI crosses above the long threshold, signaling bullish momentum.

Short Signals: Triggered when the RSI falls below the short threshold, signaling bearish momentum.

These signals are dynamically adjusted to reflect real-time market conditions, making them more robust than static RSI signals.

Visualization and Clustering Insights

The Machine Learning RSI provides an intuitive and visually rich interface, including:

RSI Line: Plotted in real-time, color-coded based on its position relative to the dynamic thresholds (green for long, red for short, gray for neutral).

Dynamic Threshold Lines: The script plots the long and short thresholds calculated by the ML clustering process, providing a clear visual reference for overbought and oversold levels.

Cluster Plots: Each RSI cluster is displayed with distinct colors (green, orange, and red) to give traders insights into how RSI values are grouped and how the dynamic thresholds are derived.

Customization Options

The Machine Learning RSI is highly customizable, allowing traders to tailor the indicator to their preferences:

RSI Settings : Adjust the RSI length, source price, and smoothing method to match your trading strategy.

Threshold Settings : Define the range and step size for clustering thresholds, allowing you to fine-tune the clustering process.

Optimization Settings : Control the performance memory, maximum clustering steps, and maximum data points for ML calculations to ensure optimal performance.

UI Settings : Customize the appearance of the RSI plot, dynamic thresholds, and cluster plots. Traders can also enable or disable candle coloring based on trend direction.

Alerts and Automation

To assist traders in staying on top of market movements, the script includes alert conditions for key events:

Long Signal: When the RSI crosses above the long threshold.

Short Signal: When the RSI crosses below the short threshold.

These alerts can be configured to notify traders in real-time, enabling timely decisions without constant chart monitoring.

Trading Applications

The Machine Learning RSI is versatile and can be applied to various trading strategies, including:

Trend Following: By dynamically adjusting thresholds, this indicator is effective in identifying and following trends in real-time.

Reversal Trading: The ML clustering process helps identify extreme RSI levels, offering reliable signals for reversals.

Range-Bound Trading: The dynamic thresholds adapt to market conditions, making the indicator suitable for trading in sideways markets where static thresholds often fail.

Final Thoughts

The Machine Learning RSI represents a significant advancement in RSI-based trading indicators. By integrating Machine Learning clustering techniques, this script overcomes the limitations of static thresholds, providing dynamic, adaptive signals that respond to market conditions in real-time. With its robust visualization, customizable settings, and alert capabilities, this indicator is a powerful tool for traders seeking to enhance their momentum analysis and improve decision-making.

As always, thorough backtesting and integration into a broader trading strategy are recommended to maximize the effectiveness!

PDF Smoothed Moving Average [BackQuant]PDF Smoothed Moving Average

Introducing BackQuant’s PDF Smoothed Moving Average (PDF-MA) — an innovative trading indicator that applies Probability Density Function (PDF) weighting to moving averages, creating a unique, trend-following tool that offers adaptive smoothing to price movements. This advanced indicator gives traders an edge by blending PDF-weighted values with conventional moving averages, helping to capture trend shifts with enhanced clarity.

Core Concept: Probability Density Function (PDF) Smoothing

The Probability Density Function (PDF) provides a mathematical approach to applying adaptive weighting to data points based on a specified variance and mean. In the PDF-MA indicator, the PDF function is used to weight price data, adding a layer of probabilistic smoothing that enhances the detection of trend strength while reducing noise.

The PDF weights are controlled by two key parameters:

Variance: Determines the spread of the weights, where higher values spread out the weighting effect, providing broader smoothing.

Mean : Centers the weights around a particular price value, influencing the trend’s directionality and sensitivity.

These PDF weights are applied to each price point over the chosen period, creating an adaptive and smooth moving average that more closely reflects the underlying price trend.

Blending PDF with Standard Moving Averages

To further improve the PDF-MA, this indicator combines the PDF-weighted average with a traditional moving average, selected by the user as either an Exponential Moving Average (EMA) or Simple Moving Average (SMA). This blended approach leverages the strengths of each method: the responsiveness of PDF smoothing and the robustness of conventional moving averages.

Smoothing Method: Traders can choose between EMA and SMA for the additional moving average layer. The EMA is more responsive to recent prices, while the SMA provides a consistent average across the selected period.

Smoothing Period: Controls the length of the lookback period, affecting how sensitive the average is to price changes.

The result is a PDF-MA that provides a reliable trend line, reflecting both the PDF weighting and traditional moving average values, ideal for use in trend-following and momentum-based strategies.

Trend Detection and Candle Coloring

The PDF-MA includes a built-in trend detection feature that dynamically colors candles based on the direction of the smoothed moving average:

Uptrend: When the PDF-MA value is increasing, the trend is considered bullish, and candles are colored green, indicating potential buying conditions.

Downtrend: When the PDF-MA value is decreasing, the trend is considered bearish, and candles are colored red, signaling potential selling or shorting conditions.

These color-coded candles provide a quick visual reference for the trend direction, helping traders make real-time decisions based on the current market trend.

Customization and Visualization Options

This indicator offers a range of customization options, allowing traders to tailor it to their specific preferences and trading environment:

Price Source : Choose the price data for calculation, with options like close, open, high, low, or HLC3.

Variance and Mean : Fine-tune the PDF weighting parameters to control the indicator’s sensitivity and responsiveness to price data.

Smoothing Method : Select either EMA or SMA to customize the conventional moving average layer used in conjunction with the PDF.

Smoothing Period : Set the lookback period for the moving average, with a longer period providing more stability and a shorter period offering greater sensitivity.

Candle Coloring : Enable or disable candle coloring based on trend direction, providing additional clarity in identifying bullish and bearish phases.

Trading Applications

The PDF Smoothed Moving Average can be applied across various trading strategies and timeframes:

Trend Following : By smoothing price data with PDF weighting, this indicator helps traders identify long-term trends while filtering out short-term noise.

Reversal Trading : The PDF-MA’s trend coloring feature can help pinpoint potential reversal points by showing shifts in the trend direction, allowing traders to enter or exit positions at optimal moments.

Swing Trading : The PDF-MA provides a clear trend line that swing traders can use to capture intermediate price moves, following the trend direction until it shifts.

Final Thoughts

The PDF Smoothed Moving Average is a highly adaptable indicator that combines probabilistic smoothing with traditional moving averages, providing a nuanced view of market trends. By integrating PDF-based weighting with the flexibility of EMA or SMA smoothing, this indicator offers traders an advanced tool for trend analysis that adapts to changing market conditions with reduced lag and increased accuracy.

Whether you’re trading trends, reversals, or swings, the PDF-MA offers valuable insights into the direction and strength of price movements, making it a versatile addition to any trading strategy.

Savitzky-Golay Z-Score [BackQuant]Savitzky-Golay Z-Score

The Savitzky-Golay Z-Score is a powerful trading indicator that combines the precision of the Savitzky-Golay filter with the statistical strength of the Z-Score. This advanced indicator is designed to detect trend shifts, identify overbought or oversold conditions, and highlight potential divergences in the market, providing traders with a unique edge in detecting momentum changes and trend reversals.

Core Concept: Savitzky-Golay Filter

The Savitzky-Golay filter is a widely-used smoothing technique that preserves important signal features such as peak detection while filtering out noise. In this indicator, the filter is applied to price data (default set to HLC3) to smooth out volatility and produce a cleaner trend line. By specifying the window size and polynomial degree, traders can fine-tune the degree of smoothing to match their preferred trading style or market conditions.

Z-Score: Measuring Deviation

The Z-Score is a statistical measure that indicates how far the current price is from its mean in terms of standard deviations. In trading, the Z-Score can be used to identify extreme price moves that are likely to revert or continue trending. A positive Z-Score means the price is above the mean, while a negative Z-Score indicates the price is below the mean.

This script calculates the Z-Score based on the Savitzky-Golay filtered price, enabling traders to detect moments when the price is diverging from its typical range and may present an opportunity for a trade.

Long and Short Conditions

The Savitzky-Golay Z-Score generates clear long and short signals based on the Z-Score value:

Long Signals : When the Z-Score is positive, indicating the price is above its smoothed mean, a long signal is generated. The color of the bars turns green, signaling upward momentum.

Short Signals : When the Z-Score is negative, indicating the price is below its smoothed mean, a short signal is generated. The bars turn red, signaling downward momentum.

These signals allow traders to follow the prevailing trend with confidence, using statistical backing to avoid false signals from short-term volatility.

Standard Deviation Levels and Extreme Levels

This indicator includes several features to help visualize overbought and oversold conditions:

Standard Deviation Levels: The script plots horizontal lines at +1, +2, -1, and -2 standard deviations. These levels provide a reference for how far the current price is from the mean, allowing traders to quickly identify when the price is moving into extreme territory.

Extreme Levels: Additional extreme levels at +3 and +4 (and their negative counterparts) are plotted to highlight areas where the price is highly likely to revert. These extreme levels provide important insight into market conditions that are far outside the norm, signaling caution or potential reversal zones.

The indicator also adapts the color shading of these extreme zones based on the Z-Score’s strength. For example, the area between +3 and +4 is shaded with a stronger color when the Z-Score approaches these values, giving a visual representation of market pressure.

Divergences: Detecting Hidden and Regular Signals

A key feature of the Savitzky-Golay Z-Score is its ability to detect bullish and bearish divergences, both regular and hidden:

Regular Bullish Divergence: This occurs when the price makes a lower low while the Z-Score forms a higher low. It signals that bearish momentum is weakening, and a bullish reversal could be near.

Hidden Bullish Divergence: This divergence occurs when the price makes a higher low while the Z-Score forms a lower low. It signals that bullish momentum may continue after a temporary pullback.

Regular Bearish Divergence: This occurs when the price makes a higher high while the Z-Score forms a lower high, signaling that bullish momentum is weakening and a bearish reversal may be near.

Hidden Bearish Divergence: This divergence occurs when the price makes a lower high while the Z-Score forms a higher high, indicating that bearish momentum may continue after a temporary rally.

These divergences are plotted directly on the chart, making it easier for traders to spot when the price and momentum are out of sync and when a potential reversal may occur.

Customization and Visualization

The Savitzky-Golay Z-Score offers a range of customization options to fit different trading styles:

Window Size and Polynomial Degree: Adjust the window size and polynomial degree of the Savitzky-Golay filter to control how much smoothing is applied to the price data.

Z-Score Lookback Period: Set the lookback period for calculating the Z-Score, allowing traders to fine-tune the sensitivity to short-term or long-term price movements.

Display Options: Choose whether to display standard deviation levels, extreme levels, and divergence labels on the chart.

Bar Color: Color the price bars based on trend direction, with green for bullish trends and red for bearish trends, allowing traders to easily visualize the current momentum.

Divergences: Enable or disable divergence detection, and adjust the lookback periods for pivots used to detect regular and hidden divergences.

Alerts and Automation

To ensure you never miss an important signal, the indicator includes built-in alert conditions for the following events:

Positive Z-Score (Long Signal): Triggers an alert when the Z-Score crosses above zero, indicating a potential buying opportunity.

Negative Z-Score (Short Signal): Triggers an alert when the Z-Score crosses below zero, signaling a potential short opportunity.

Shifting Momentum: Alerts when the Z-Score is shifting up or down, providing early warning of changing market conditions.

These alerts can be configured to notify you via email, SMS, or app notification, allowing you to stay on top of the market without having to constantly monitor the chart.

Trading Applications

The Savitzky-Golay Z-Score is a versatile tool that can be applied across multiple trading strategies:

Trend Following: By smoothing the price and calculating the Z-Score, this indicator helps traders follow the prevailing trend while avoiding false signals from short-term volatility.

Mean Reversion: The Z-Score highlights moments when the price is far from its mean, helping traders identify overbought or oversold conditions and capitalize on potential reversals.

Divergence Trading: Regular and hidden divergences between the Z-Score and price provide early warning of trend reversals, allowing traders to enter trades at opportune moments.

Final Thoughts

The Savitzky-Golay Z-Score is an advanced statistical tool designed to provide a clearer view of market trends and momentum. By applying the Savitzky-Golay filter and Z-Score analysis, this indicator reduces noise and highlights key areas where the market may reverse or accelerate, giving traders a significant edge in understanding price behavior.

Whether you’re a trend follower or a reversal trader, this indicator offers the flexibility and insights you need to navigate complex markets with confidence.

Savitzky Golay Median Filtered RSI [BackQuant]Savitzky Golay Median Filtered RSI

Introducing BackQuant's Savitzky Golay Median Filtered RSI, a cutting-edge indicator that enhances the classic Relative Strength Index (RSI) by applying both a Savitzky-Golay filter and a median filter to provide smoother and more reliable signals. This advanced approach helps reduce noise and captures true momentum trends with greater precision. Let’s break down how the indicator works, the features it offers, and how it can improve your trading strategy.

Core Concept: Relative Strength Index (RSI)

The Relative Strength Index (RSI) is a widely used momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100, with levels above 70 typically indicating overbought conditions and levels below 30 indicating oversold conditions. However, the standard RSI can sometimes generate noisy signals, especially in volatile markets, making it challenging to identify reliable entry and exit points.

To improve upon the traditional RSI, this indicator introduces two powerful filters: the Savitzky-Golay filter and a median filter.

Savitzky-Golay Filter: Smoothing with Precision

The Savitzky-Golay filter is a digital filtering technique used to smooth data while preserving important features, such as peaks and trends. Unlike simple moving averages that can distort important price data, the Savitzky-Golay filter uses polynomial regression to fit the data, providing a more accurate and less lagging result.

In this script, the Savitzky-Golay filter is applied to the RSI values to smooth out short-term fluctuations and provide a more reliable signal. By using a window size of 5 and a polynomial degree of 2, the filter effectively reduces noise without compromising the integrity of the underlying price movements.

Median Filter: Reducing Outliers

After applying the Savitzky-Golay filter, the median filter is applied to the smoothed RSI values. The median filter is particularly effective at removing short-lived outliers, further enhancing the accuracy of the RSI by reducing the impact of sudden and temporary price spikes or drops. This combination of filters creates an ultra-smooth RSI that is better suited for detecting true market trends.

Long and Short Signals

The Savitzky Golay Median Filtered RSI generates long and short signals based on user-defined threshold levels:

Long Signals: A long signal is triggered when the filtered RSI exceeds the Long Threshold (default set at 176). This indicates that momentum is shifting upward, and it may present a good buying opportunity.

Short Signals: A short signal is generated when the filtered RSI falls below the Short Threshold (default set at 162). This suggests that momentum is weakening, potentially signaling a selling opportunity or exit from a long position.

These threshold levels can be adjusted to suit different market conditions and timeframes, allowing traders to fine-tune the sensitivity of the indicator.

Customization and Visualization Options

The Savitzky Golay Median Filtered RSI comes with several customization options, enabling traders to tailor the indicator to their specific needs:

Calculation Source: Select the price source for the RSI calculation (default is OHLC4, but it can be changed to close, open, high, or low prices).

RSI Period: Adjust the lookback period for the RSI calculation (default is 14).

Median Filter Length: Control the length of the median filter applied to the smoothed RSI, affecting how much noise is removed from the signal.

Threshold Levels: Customize the long and short thresholds to define the sensitivity for generating buy and sell signals.

UI Settings: Choose whether to display the RSI and thresholds on the chart, color the bars according to trend direction, and adjust the line width and colors used for long and short signals.

Visual Feedback: Color-Coded Signals and Thresholds

To make the signals easier to interpret, the indicator offers visual feedback by coloring the price bars and the RSI plot according to the current market trend:

Green Bars indicate long signals when momentum is bullish.

Red Bars indicate short signals when momentum is bearish.

Gray Bars indicate neutral or undecided conditions when no clear signal is present.

In addition, the Long and Short Thresholds can be plotted directly on the chart to provide a clear reference for when signals are triggered, allowing traders to visually gauge the strength of the RSI relative to its thresholds.

Alerts for Automation

For traders who prefer automated notifications, the Savitzky Golay Median Filtered RSI includes built-in alert conditions for long and short signals. You can configure these alerts to notify you when a buy or sell condition is met, ensuring you never miss a trading opportunity.

Trading Applications

This indicator is versatile and can be used in a variety of trading strategies:

Trend Following: The combination of Savitzky-Golay and median filtering makes this RSI particularly useful for identifying strong trends without being misled by short-term noise. Traders can use the long and short signals to enter trades in the direction of the prevailing trend.

Reversal Trading: By adjusting the threshold levels, traders can use this indicator to spot potential reversals. When the RSI moves from overbought to oversold levels (or vice versa), it may signal a shift in market direction.

Swing Trading: The smoothed RSI provides a clear signal for short to medium-term price movements, making it an excellent tool for swing traders looking to capitalize on momentum shifts.

Risk Management: The filtered RSI can be used as part of a broader risk management strategy, helping traders avoid false signals and stay in trades only when the momentum is strong.

Final Thoughts

The Savitzky Golay Median Filtered RSI takes the classic RSI to the next level by applying advanced smoothing techniques that reduce noise and improve signal reliability. Whether you’re a trend follower, swing trader, or reversal trader, this indicator provides a more refined approach to momentum analysis, helping you make better-informed trading decisions.

As with all indicators, it is important to backtest thoroughly and incorporate sound risk management strategies when using the Savitzky Golay Median Filtered RSI in your trading system.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Kalman For Loop [BackQuant]Kalman For Loop

Introducing BackQuant's Kalman For Loop (Kalman FL) — a highly adaptive trading indicator that uses a Kalman filter to smooth price data and generate actionable long and short signals. This advanced indicator is designed to help traders identify trends, filter out market noise, and optimize their entry and exit points with precision. Let’s explore how this indicator works, its key features, and how it can enhance your trading strategies.

Core Concept: Kalman Filter

The Kalman Filter is a mathematical algorithm used to estimate the state of a system by filtering noisy data. It is widely used in areas such as control systems, signal processing, and time-series analysis. In the context of trading, a Kalman filter can be applied to price data to smooth out short-term fluctuations, providing a clearer view of the underlying trend.

Unlike moving averages, which use fixed weights to smooth data, the Kalman Filter adjusts its estimate dynamically based on the relationship between the process noise and the measurement noise. This makes the filter more adaptive to changing market conditions, providing more accurate trend detection without the lag associated with traditional smoothing techniques.

Please see the original Kalman Price Filter

In this script, the Kalman For Loop applies the Kalman filter to the price source (default set to the closing price) to generate a smoothed price series, which is then used to calculate signals.

Adaptive Smoothing with Process and Measurement Noise

Two key parameters govern the behavior of the Kalman filter:

Process Noise: This controls the extent to which the model allows for uncertainty in price changes. A lower process noise value will make the filter smoother but slower to react to price changes, while a higher value makes it more sensitive to recent price fluctuations.