Smart AlertsThis indicator provides back-tested signals and alerts from multiple technical indicators.

No more guessing whether or not you should trust an indicator. See your indicators' past performance at a glance.

No more false alarms. Disable re-painting of signals.

When multiple indicators overlap, a Confluence indicator will print (large triangle). With your settings properly tuned, this will show a HIGH probability of a move.

Current Signal/Alert Options (more to come):

RSI Oversold

RSI Overbought

EMA Crossing Up

EMA Crossing Down

Buy Signal Confluence

Sell Signal Confluence

Instructions:

-Enable/disable individual indicators so you can fine tune one at a time

-Adjust the indicator's settings

-Adjust your trade parameters (Max Wait, Take Profit %). Signals that would have given the desired profit in the time allowed will be painted orange.

-Repeat this process with each indicator until you're satisfied

-Set-up alerts

Backtest

Smart EMA SignalsThis indicator starts by plotting each time the price action crosses above or below the EMA, of which you can tune the timeframe and duration.

It then takes it a step further and plots whether or not that indicator would have given you a profitable trade, of which you can also tune the parameters (Max wait time, and % Profit).

Once you have your EMA tuned to your liking, set up alerts to notify you of a golden opportunity.

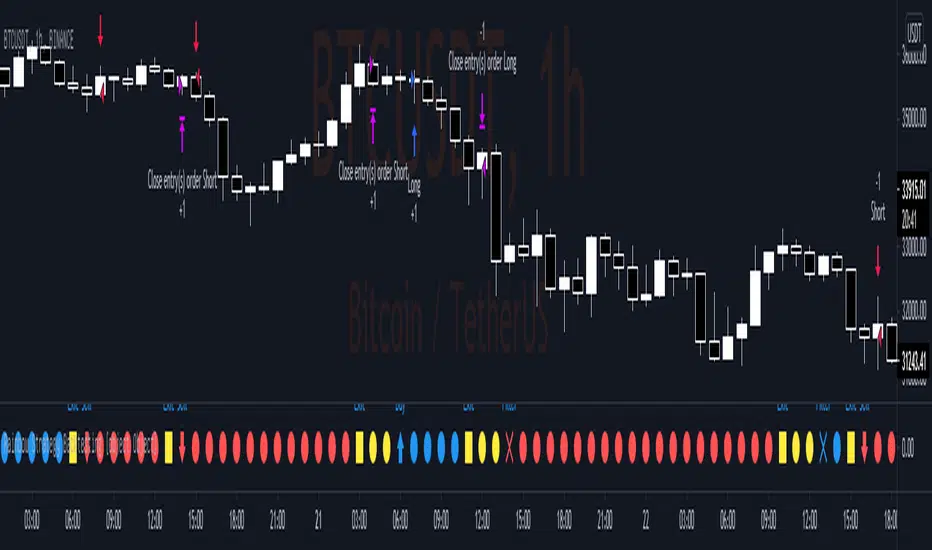

QFL single TF with alertsBacktesting compatible QFL pine script w/alerts

This version of QFL was made based on this one:

From author:

www.tradingview.com

I made the following additions according to my requirements:

- I need to use pine script 4

- I needed to avoid repainting issues so I'm not calling directly security, I'm using the wrapper function.

- There might be still repainting issues when you use "max base age" which uses the function "barssince" so be careful, you can disable it by setting its value to zero.

- Alerts so I can use it for automated trading and bots

- In order to make this signal compatible with the backtest script there's an option provided in the settings. If you enable this option this indicator will plot 1 whenever there's a BUY signal. This will allow the backtest to pick the "QFL Buy" from external indicator so it can perform the backtest.

I recommend some of these settings to start playing with the chart in 15 min / QFL in 1, 2 or 4 hours.

The higher the TF the more conservative.

QFL with 3.5% is pretty popular but you can try higher QFL percentage settings for a more conservative approach.

Rainbow Strategy BacktestingRainbow Strategy Backtesting base on "Rainbow Moving Average" Strategy as below:

1.Rainbow Moving Average setup

- Source: source of 1st MA

- Type: SMA/EMA

- Period: period of 1st MA

- Displacement: period of 2nd MA to 7th MA with source is previous MA

2.Trend Define

- Up Trend: Main MA moving at the top of Rainbow

- Down Trend: Main MA moving at the bottom of Rainbow

- Sideway: Main MA moving between the top and the bottom of Rainbow

3.Signal

- Buy Signal: When Rainbow change to Up Trend.

- Sell Signal: When Rainbow change to Down Trend.

- Exit: When Rainbow change to Sideway.

4.RSI Filter

- "Enable": Only signals have 1st RSI moving between Overbought and Oversold and 2nd RSI moving outside Middle Channel are accepted.

- The filter may help trader avoid bull trap, bear trap and choppy market.

5.Backtesting Infomation

- Ticker: BTCUSDT

- Timeframe: H1

- Rainbow parameter:

+ Source: hlc3

+ Type: SMA

+ Period: 12

+ Displacement: 3

- RSI Filter parameter:

+ Enable

+ 1st RSI filter: period 12, overbought 65, oversold 35

+ 2nd RSI filter: period 9, upper middle 56, lower middle 44

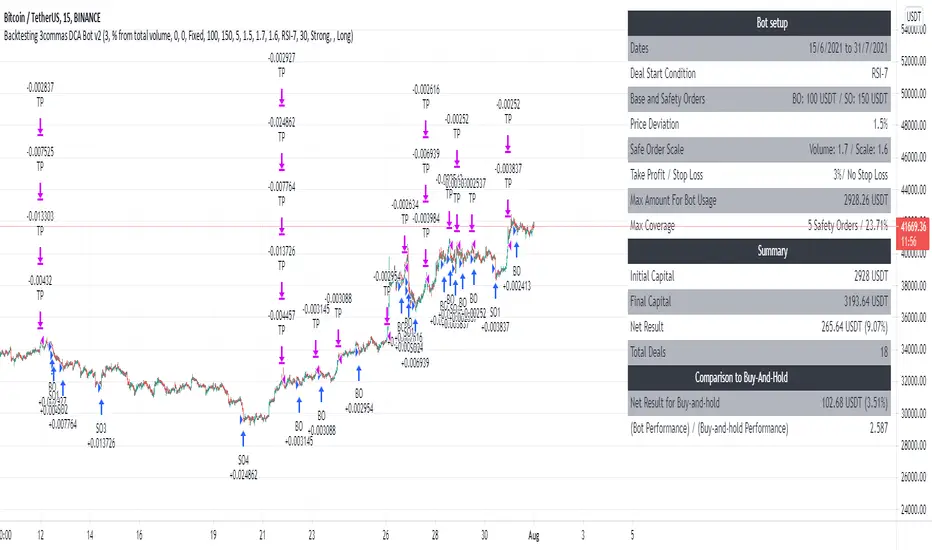

Backtesting 3commas DCA Bot v2Updating previously published simulated 3commas DCA logic with a sexier insert and more meaningful default parameters.

3Commas Bollinger StrategyThis strategy is intended for use as a way of backtesting various parameters available on 3commas.io composite bot using a bollinger band type trading strategy. While it's primary intention is to provide users a way of backtesting bot parameters, it can also be used to trigger a deal start by either using the {{strategy.open.alert_message}} field in your alert and providing the bot details in the configuration screen for the strategy or by including the usual deal start message provided by 3commas. You can find more information about how to do this from help.3commas.io

The primary inputs for the strategy are:

// USER INPUTS

Short MA Window - The length of the Short moving average

Long MA Window - The length of the Long moving average

Upper Band Offset - The offset to use for the upper bollinger offset

Lower Band Offset - The offset to use for the lower bollinger offset

Long Stop Loss % - The stop loss percentage to test

Long Take Profit % - The Take profit percentage to test

Initial SO Deviation % - The price deviation percentage required to place to first safety order

Safety Order Vol Step % - The volume scale to test

3Commas Bot ID - (self explanatory)

Bot Email Token - Found in the deal start message for your bot (see link in previous section for details)

3Commas Bot Trading Pair - The pair to include for composite bot start deals (should match format of 3commas, not TradingView IE. USDT_BTC not BTCUSDT)

Start Date, Month, Year and End Date, Month and Year all apply to the backtesting window. By default it will use as much data as it can given the current period select (there is less historical data available for periods below 1H) back as far as 2016 (there appears to be no historical data on Trading view much before this). If you would like to test a different period of time, just change these values accordingly.

Known Issues

Currently there are a couple of issues with this strategy that you should be aware of. I may fix them at some point in the future but they don't really bug me so this is more for informational purposes than a promise that they may one day be fixed.

Does not test trailing take profit

Number of safety orders and Safety Order Step Scale are currently not user configurable (must edit source code)

Using the user configuration to generate deal start message assumes you are triggering a composite bot, not a simple bot.

Combo Backtest 123 Reversal & MASS Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Mass Index was designed to identify trend reversals by measuring

the narrowing and widening of the range between the high and low prices.

As this range widens, the Mass Index increases; as the range narrows

the Mass Index decreases.

The Mass Index was developed by Donald Dorsey.

WARNING:

- For purpose educate only

- This script to change bars colors.

RSI-VWAP Indicator %█ OVERALL

Simple and effective script that, as you already know, uses vwap as source of the rsi, and with good results as long as the market has no long-term downtrend.

RsiVwap = rsi (vwap (close), Length)

The default settings are for BTC in a 30 minute time frame. For other pairs and time frames you just have to play with the settings.

█ FEATURES

• The option to start trading from a certain date has been added.

• To make the profit more progressive, a percentage of your equity is used for entries and a percentage of your position is used for closings.

• The option to trade in Spot mode has been added, since, for the TradingView backtest, the money is infinite and if you do not limit it somehow,

it would offer you much better profits than the live trading.

QuantityOnLong = Spot ? (EquityPercent / 100) * ((strategy.equity / close) - strategy.position_size) : (EquityPercent / 100) * (strategy.equity / close)

• The option to stop the system when the drawdown exceeds the fixed limit has been added.

Drawdown, as you already know, is a very important measure of risk in trading systems.

The maximum drawdown will tell us what the maximum loss of a trading system has been during a period. This maximum loss is determined by:

strategy.risk.max_drawdown(Risk, strategy.percent_of_equity)

• Leverage plotted on labels added.

█ ALERTS

To enjoy the benefits of automatic trading, TradingView alerts can be used as direct buy-sell orders on spot, or long-close orders with leverage.

Currently there are Chrome extensions that act as a bridge between TradingView and your Exchange or Broker.

This is an example of syntax for this type of extensions. Copy and paste a message like this into the alert window:

{{strategy.order.action}} @ {{strategy.order.price}} | e = {{exchange}} a = account s = {{ticker}} b = {{strategy.order.action}} {{strategy.order.alert_message}}

█ NOTE

Certain Risks of Live Algorithmic Trading You Should Know:

• Backtesting cannot assure actual results.

• The relevant market might fail or behave unexpectedly.

• Your broker may experience failures in its infrastructure, fail to execute your orders in a correct or timely fashion or reject your orders.

• The system you use for generating trading orders, communicating those orders to your broker, and receiving queries and trading results from your broker may fail.

• Time lag at various point in live trading might cause unexpected behavior.

• The systems of third parties in addition to those of the provider from which we obtain various services, your broker, and the applicable securities market may fail or malfunction.

█ THANKS

Thanks to TradingView, its Pine code, its community and especially those Pine wizards who post their ideas that helps us to learn.

If the world is heading toward a equitable new world economic order, let's get rich first ...

Happy trading!

Ultimate Strategy TemplateHello Traders

As most of you know, I'm a member of the PineCoders community and I sometimes take freelance pine coding jobs for TradingView users.

Off the top of my head, users often want to:

- convert an indicator into a strategy, so as to get the backtesting statistics from TradingView

- add alerts to their indicator/strategy

- develop a generic strategy template which can be plugged into (almost) any indicator

My gift for the community today is my Ultimate Strategy Template

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

For doing so:

1) Find in your indicator where are the conditions printing the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator wether it's a MACD, ZigZag, Pivots, higher-highs, lower-lows or whatever indicator with clear buy and sell conditions

//@version=4

study(title='Moving Average Cross', shorttitle='Moving Average Cross', overlay=true, precision=6, max_labels_count=500, max_lines_count=500)

type_ma1 = input(title="MA1 type", defval="SMA", options= )

length_ma1 = input(10, title = " MA1 length", type=input.integer)

type_ma2 = input(title="MA2 type", defval="SMA", options= )

length_ma2 = input(100, title = " MA2 length", type=input.integer)

// MA

f_ma(smoothing, src, length) =>

iff(smoothing == "RMA", rma(src, length),

iff(smoothing == "SMA", sma(src, length),

iff(smoothing == "EMA", ema(src, length), src)))

MA1 = f_ma(type_ma1, close, length_ma1)

MA2 = f_ma(type_ma2, close, length_ma2)

// buy and sell conditions

buy = crossover(MA1, MA2)

sell = crossunder(MA1, MA2)

plot(MA1, color=color_ma1, title="Plot MA1", linewidth=3)

plot(MA2, color=color_ma2, title="Plot MA2", linewidth=3)

plotshape(buy, title='LONG SIGNAL', style=shape.circle, location=location.belowbar, color=color_ma1, size=size.normal)

plotshape(sell, title='SHORT SIGNAL', style=shape.circle, location=location.abovebar, color=color_ma2, size=size.normal)

/////////////////////////// SIGNAL FOR STRATEGY /////////////////////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title="🔌Connector🔌", transp=100)

Basically, I identified my buy, sell conditions in the code and added this at the bottom of my indicator code

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title="🔌Connector🔌", transp=100)

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal , and -1 for the bearish signal

Now you can connect your indicator to the Strategy Template using the method below or that one

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings and in the Data Source field select your 🔌Connector🔌 (which comes from your indicator)

From then, you should start seeing the signals and plenty of other stuff on your chart

🔥 Note that whenever you'll update your indicator values, the strategy statistics and visual on your chart will update in real-time

Settings

- Color Candles : Color the candles based on the trade state (bullish, bearish, neutral)

- Close positions at market at the end of each session : useful for everything but cryptocurrencies

- Session time ranges : Take the signals from a starting time to an ending time

- Close Direction : Choose to close only the longs, shorts, or both

- Date Filter : Take the signals from a starting date to an ending date

- Set the maximum losing streak length with an input

- Set the maximum winning streak length with an input

- Set the maximum consecutive days with a loss

- Set the maximum drawdown (in % of strategy equity)

- Set the maximum intraday loss in percentage

- Limit the number of trades per day

- Limit the number of trades per week

- Stop-loss: None or Percentage or Trailing Stop Percentage or ATR

- Take-Profit: None or Percentage or ATR

- Risk-Reward based on ATR multiple for the Stop-Loss and Take-Profit

This script is open-source so feel free to use it, and optimize it as you want

Alerts

Maybe you didn't know it but alerts are available on strategy scripts.

I added them in this template - that's cool because:

- if you don't know how to code, now you can connect your indicator and get alerts

- you have now a cool template showing you how to create alerts for strategy scripts

Source: www.tradingview.com

I hope you'll like it, use it, optimize it and most importantly....make some optimizations to your indicators thanks to this Strategy template

Special Thanks

Special thanks to @JosKodify as I borrowed a few risk management snippets from his website: kodify.net

Additional features

I thought of plenty of extra filters that I'll add later on this week on this strategy template

Best

Dave

Combo Backtest 123 Reversal & Line Regression Intercept This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Laguerre-based RSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is RSI indicator which is more sesitive to price changes.

It is based upon a modern math tool - Laguerre transform filter.

With help of Laguerre filter one becomes able to create superior

indicators using very short data lengths as well. The use of shorter

data lengths means you can make the indicators more responsive to

changes in the price.

WARNING:

- For purpose educate only

- This script to change bars colors.

MACD With Trend Filter: Visual Backtest Module TemplateSample Strategy: MACD Crossover with trend filter options

MA Filter : Price Close Above MA, Search for Buy, Price Close Below MA, Search for Sell

ADX Filter : Take trade only when ADX is above certain treshold

MACD Signal : MACD Cross above signal line while under 0 line indicate Buy Signal

MACD Cross below signal line while above 0 line indicate Sell Signal

-----------------------------

Using Alert Module:

Enable Alert --> Enable TV's alert and plot signal to chart

Alert Type --> Set to take Buy only, Sell only or Both alert

----------------------------

Using Backtest Module:

Enable Backtest --> Enable Backtest simulation

Backtest Type --> Set to take Buy only, Sell only or Both

SL Type -->

ATR : Set SL in ATR times Multiplier below/above entry price

Fixed : Set SL in fixed point below entry point (in 'Dollar'). e.g. for Stocks -> 0.5 equals to 50cent while for EURUSD currency -> 0.005 equal to 50 pips

HiLo Bar : Set SL at highest/lowest wick of previous bar plus/minus Fixed point. e.g. EURUSD HiLo=3 and Fixed Point = 0.0005, buy trade will place SL 5 Pips below lowest of previous 3 bar

SL ATR Period --> Set Lookback Period used for SL's ATR calculation

SL ATR Multi --> Set ATR Multiplier for SL

SL Fixed --> Set Fixed Level for SL (Use when SL Type is either Fixed or HiLo Bar)

SL Bar --> Set Number of previous bar to check for SL placement

TP RR Ratio --> Set TP based on RR multiplier. e.g. 2 means TP level will be twice further from entry point compared to Entry-SL distance.

Notes: The point is for preliminary testing, so it only supports 1 trade at a time and no Trailing Stop

----------------------------

Disclaimer:

This script main objective is to create my personal indicator template so that i just have to modify the indicator module for preliminary testing in future.

Testing Alert Module so i can re-use it as template in future study/indicator

Testing Visual Backtest Module so i can re-use it as template in future study/indicator

i believe using Strategy function is a better approach for this but the entry/exit level seems to be hit n miss (at least for me, still trying to figure what i did wrong)

also, i rather code the strategy in other platform where i can use the more accurate tick data if i want to validate backtest statistics.

My study scripts was built only to test/visualize an idea to see its viability and if it can be used to optimize existing strategy.

credit: ADX code are originally from "ADX and DI" by @BeikabuOyaji although i re-wrote so i can have cleaner read and use RMA instead of SMA

Combo Backtest 123 Reversal & Volume SMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Volume and SMA

WARNING:

- For purpose educate only

- This script to change bars colors.

Logistic RSI, STOCH, ROC, AO, ... by DGTExperimental attemt of applying Logistic Map Equation for some of widly used indicators.

With this study "Awesome Oscillator (AO)", "Rate of Change (ROC)", "Relative Strength Index (RSI)", "Stochastic (STOCH)" and a custom interpretation of Logistic Map Equation is presented

Calculations with Logistic Map Equation makes sense when the calculated results are iterated many times within the same equation.

Here is the Logistic Map Equation : Xn+1 = r * Xn * (1 - Xn)

Where, the value of r is the key for this equation which changes amazingly the behaviour of the Logistic Map.

The value we have asigned for r is less then 1 and greater than 0 ( 0 < r < 1) and in this case the iterations performed with the maximum number of output series allowed by Pine is quite enough for our purpose and thanks to arrays we can easiliy store them for further processing

What we have as output:

Each iteration result is then plotted (excluding plotting the first iteration), as circles or line based on user preference

Values above and below zero level (0) are coloured differently to emphasis bull and bear power

Finally Standard Deviation of Array's Elements is ploted as line. Users may choose to display this line only

So where it comes the indicators "Awesome Oscillator (AO)", "Rate of Change (ROC)", "Relative Strength Index (RSI)", "Stochastic (STOCH)".

Those are the indicators whose values are assigned to our key varaiable in the Logistic Map equation forulma which is r

Further details regarding Logistic Map can found under the description of “Logistic EMA w/ Signals by DGT” study

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Combo Backtest 123 Reversal & Gann Swing Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Gann Swing Oscillator has been adapted from Robert Krausz's book,

"A W.D. Gann Treasure Discovered". The Gann Swing Oscillator helps

define market swings.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & FX Sniper: T3-CCI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This simple indicator gives you a lot of useful information - when to enter, when to exit

and how to reduce risks by entering a trade on a double confirmed signal.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Volatility Finite Volume ElementsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is another version of FVE indicator that we have posted earlier

in this forum.

This version has an important enhancement to the previous one that`s

especially useful with intraday minute charts.

Due to the volatility had not been taken into account to avoid the extra

complication in the formula, the previous formula has some drawbacks:

The main drawback is that the constant cutoff coefficient will overestimate

price changes in minute charts and underestimate corresponding changes in

weekly or monthly charts.

And now the indicator uses adaptive cutoff coefficient which will adjust to

all time frames automatically.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & FSK (Fast and Slow Kurtosis) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the Fast & Slow Kurtosis. The Kurtosis is a market

sentiment indicator. The Kurtosis is constructed from three different parts.

The Kurtosis, the Fast Kurtosis(FK), and the Fast/Slow Kurtosis(FSK).

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Fractal Chaos Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

Simple SMA Strategy Backtest Part 5Simple SMA strategy

In this stream, we will create an intraday trade cap.

WARNING:

- For purpose educate only

- This script to change bars colors

Stream:

www.tradingview.com

Combo Backtest 123 Reversal & Floor Pivot Points This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The name ‘Floor-Trader Pivot,’ came from the fact that Pivot points can

be calculated quickly, on the fly using price data from the previous day

as an input. Although time-frames of less than a day can be used, Pivots are

commonly plotted on the Daily Chart; using price data from the previous day’s

trading activity.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Future Lines of Demarcation This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

An FLD is a line that is plotted on the same scale as the price and is in fact the

price itself displaced to the right (into the future) by (approximately) half the

wavelength of the cycle for which the FLD is plotted. There are three FLD's that can be

plotted for each cycle:

An FLD based on the median price.

An FLD based on the high price.

An FLD based on the low price.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Fisher Transform Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Market prices do not have a Gaussian probability density function

as many traders think. Their probability curve is not bell-shaped.

But trader can create a nearly Gaussian PDF for prices by normalizing

them or creating a normalized indicator such as the relative strength

index and applying the Fisher transform. Such a transformed output

creates the peak swings as relatively rare events.

Fisher transform formula is: y = 0.5 * ln ((1+x)/(1-x))

The sharp turning points of these peak swings clearly and unambiguously

identify price reversals in a timely manner.

WARNING:

- For purpose educate only

- This script to change bars colors.