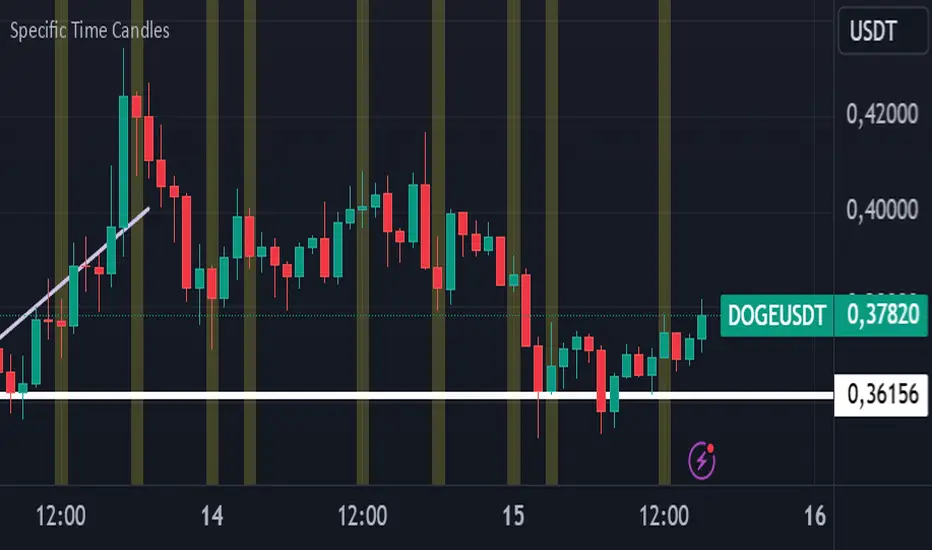

Specific Time CandlesSpecific Time Candles Indicator

The Specific Time Candles indicator is a powerful tool designed for traders who want to focus on specific time intervals within their charts. This custom indicator allows you to highlight and analyze price action during user-defined time periods, providing clarity and precision in your trading strategy.

Key Features:

Custom Time Intervals: Select any start and end time to create candles that focus on your preferred trading hours. This is particularly useful for traders who want to concentrate on market sessions, such as the London or New York session, or any other specific time frame relevant to their trading plan.

Enhanced Visualization: By isolating specific time periods, this indicator helps reduce noise and provides a clearer view of market movements during key trading hours. This can be beneficial for identifying trends, reversals, and potential breakout opportunities.

Flexible Configuration: Easily adjust the indicator settings to match your trading schedule. Whether you are a day trader, swing trader, or scalper, you can customize the time frames to suit your needs.

Compatibility: The indicator is compatible with multiple asset classes, including forex, stocks, commodities, and cryptocurrencies, making it a versatile tool for any trader.

User-Friendly Interface: Designed with simplicity in mind, the Specific Time Candles indicator is easy to set up and use, even for those who are new to TradingView.

How to Use:

Add the indicator to your chart from the TradingView library.

Set your desired start and end times in the indicator settings.

Observe the newly formed candles that represent the specified time intervals.

Use these candles to make informed trading decisions based on the focused analysis of market activity during your chosen periods.

Benefits:

Precision Trading: Focus on the most relevant market data, eliminating distractions from other time periods.

Improved Decision-Making: Gain insights into market behavior during critical times, enhancing your ability to make strategic trades.

Time Management: Efficiently manage your trading by concentrating on specific times, allowing for better planning and execution.

The Specific Time Candles indicator is a must-have for traders looking to refine their strategies by concentrating on precise market windows. Whether you are targeting high-volatility periods or specific trading sessions, this indicator provides the tools you need to succeed.

Bands and Channels

Renko Periodic Spiral of Archimedes-Secret Geometry - AYNETHow It Works

Dynamic Center:

The spiral is centered on the close price of the chart, with an optional vertical offset (center_y_offset).

Spiral Construction:

The spiral is drawn using segments_per_turn to divide each turn into small line segments.

spacing determines the radial distance between successive turns.

num_turns controls how many full rotations the spiral will have.

Line Drawing:

Each segment is computed using trigonometric functions (cos and sin) to calculate its endpoints.

These segments are drawn sequentially to form the spiral.

Inputs

Center Y Offset: Adjusts the vertical position of the spiral relative to the close price.

Number of Spiral Turns: Total number of full rotations in the spiral.

Spacing Between Turns: Distance between consecutive turns.

Segments Per Turn: Number of segments used to create each turn (higher values make the spiral smoother).

Line Color: Customize the color of the spiral lines.

Line Width: Adjust the thickness of the spiral lines.

Example

If num_turns = 5, spacing = 2, and segments_per_turn = 100:

The spiral will have 5 turns, with a radial distance of 2 between each turn, divided into 100 segments per turn.

Let me know if you have further requests or adjustments to the visualization!

Mandala Visualization-Secret Geometry-AYNETCode Explanation

Dynamic Center:

The center Y coordinate is dynamic and defaults to the close price.

You can change it to a fixed level if desired.

Concentric Rings:

The script draws multiple circular rings spaced evenly using ring_spacing.

Symmetry Lines:

The Mandala includes num_lines radial symmetry lines emanating from the center.

Customization Options:

num_rings: Number of concentric circles.

ring_spacing: Distance between each ring.

num_lines: Number of radial lines.

line_color: Color of the rings and lines.

line_width: Thickness of the rings and lines.

How to Use

Add the script to your TradingView chart.

Adjust the input parameters to fit the Mandala within your chart view.

Experiment with different numbers of rings, lines, and spacing for unique Mandala patterns.

Let me know if you'd like additional features or visual tweaks!

Torus Visualization-Secret Geometry-AYNETExplanation:

Outer and Inner Circles:

The script draws two main circles: the outer boundary and the inner boundary of the Torus.

Bands Between Circles:

Additional concentric circles are drawn to create the illusion of a Torus structure.

Customizable Inputs:

You can control the outer radius, inner radius, number of segments for smoother circles, and the number of bands to improve visualization.

Parameters:

center_x and center_y define the center of the Torus on the chart.

outer_radius and inner_radius control the size of the Torus.

segments define the resolution of the circles (more segments = smoother appearance).

Visualization:

The Torus appears as a series of concentric circles, giving a 2D approximation of the 3D structure.

This script can be visualized on any chart, and the Torus will adjust its position based on the specified center and radius values.

Platonic Solids Visualization-Scret Geometry-AYNETExplanation:

Input Options:

solid: Choose the type of Platonic Solid (Tetrahedron, Cube, Octahedron, etc.).

size: Adjust the size of the geometry.

color_lines: Choose the color for the edges.

line_width: Set the width of the edges.

Geometry Calculations:

Each solid is drawn based on predefined coordinates and connected using the line.new function.

Geometric Types Supported:

Tetrahedron: A triangular pyramid.

Cube: A square-based 2D projection.

Octahedron: Two pyramids joined at the base.

Unsupported Solids:

Dodecahedron and Icosahedron are geometrically more complex and not rendered in this basic implementation.

Visualization:

The chosen Platonic Solid will be drawn relative to the center position (center_y) on the chart.

Adjust the size and center_y inputs to position the shape correctly.

Let me know if you need improvements or have a specific geometry to implement!

Sri Yantra-Scret Geometry - AYNETExplanation of the Script

Inputs:

periods: Number of bars used for calculating the moving average and standard deviation.

yloc: Chooses the display location (above or below the bars).

Moving Average and Standard Deviation:

ma: Moving average of the close price for the specified period.

std: Standard deviation, used to set the range for the Sri Yantra triangle points.

Triangle Points:

p1, p2, and p3 are the points for constructing the triangle, with p1 and p2 set at two standard deviations above and below the moving average, and p3 at the moving average itself.

Sri Yantra Triangle Drawing:

Three lines form a triangle, with the moving average line serving as the midpoint anchor.

The triangle pattern shifts across bars as new moving average values are calculated.

Moving Average Plot:

The moving average is plotted in red for visual reference against the triangle pattern.

This basic script emulates the Sri Yantra pattern using price data, creating a spiritual and aesthetic overlay on price charts, ideal for users looking to incorporate sacred geometry into their technical analysis.

Fibonacci Levels Strategy with High/Low Criteria-AYNETThis code represents a TradingView strategy that uses Fibonacci levels in conjunction with high/low price criteria over specified lookback periods to determine buy (long) and sell (short) conditions. Below is an explanation of each main part of the code:

Explanation of Key Sections

User Inputs for Higher Time Frame and Candle Settings

Users can select a higher time frame (timeframe) for analysis and specify whether to use the "Current" or "Last" higher time frame (HTF) candle for calculating Fibonacci levels.

The currentlast setting allows flexibility between using real-time or the most recent closed higher time frame candle.

Lookback Periods for High/Low Criteria

Two lookback periods, lowestLookback and highestLookback, allow users to set the number of bars to consider when finding the lowest and highest prices, respectively.

This determines the criteria for entering trades based on how recent highs or lows compare to current prices.

Fibonacci Levels Configuration

Fibonacci levels (0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, and 100%) are configurable. These are used to calculate price levels between the high and low of the higher time frame candle.

Each level represents a retracement or extension relative to the high/low range of the HTF candle, providing important price levels for decision-making.

HTF Candle Calculation

HTF candle data is calculated based on the higher time frame selected by the user, using the newbar check to reset htfhigh, htflow, and htfopen values.

The values are updated with each new HTF bar or as prices move within the same HTF bar to track the highest high and lowest low accurately.

Set Fibonacci Levels Array

Using the calculated HTF candle's high, low, and open, the Fibonacci levels are computed by interpolating these values according to the user-defined Fibonacci levels.

A fibLevels array stores these computed values.

Plotting Fibonacci Levels

Each Fibonacci level is plotted on the chart with a different color, providing visual indicators for potential support/resistance levels.

High/Low Price Criteria Calculation

The lowest and highest prices over the specified lookback periods (lowestLookback and highestLookback) are calculated and plotted on the chart. These serve as dynamic levels to trigger long or short entries.

Trade Signal Conditions

longCondition: A long (buy) signal is generated when the price crosses above both the lowest price criteria and the 50% Fibonacci level.

shortCondition: A short (sell) signal is generated when the price crosses below both the highest price criteria and the 50% Fibonacci level.

Executing Trades

Based on the longCondition and shortCondition, trades are entered with the strategy.entry() function, using the labels "Long" and "Short" for tracking on the chart.

Strategy Use

This strategy allows traders to utilize Fibonacci retracement levels and recent highs/lows to identify trend continuation or reversal points, potentially providing entry points aligned with larger market structure. Adjusting the lowestLookback and highestLookback along with Fibonacci levels enables a customizable approach to suit different trading styles and market conditions.

Star of David Drawing-AYNETExplanation of Code

Settings:

centerTime defines the center time for the star pattern, defaulting to January 1, 2023.

centerPrice is the center Y-axis level for positioning the star.

size controls the overall size of the star.

starColor and lineWidth allow customization of the color and thickness of the lines.

Utility Function:

toRadians converts degrees to radians, though it’s not directly used here, it might be useful for future adjustments to angles.

Star of David Drawing Function:

The drawStarOfDavid function calculates the position of each point on the star relative to the center coordinates (centerTime, centerY) and size.

The pattern has six key points that form two overlapping triangles, creating the Star of David pattern.

The time offsets (offset1 and offset2) determine the horizontal spread of the star, scaling according to size.

The line.new function is used to draw the star lines with the calculated coordinates, casting timestamps to int to comply with line.new requirements.

Star Rendering:

Finally, drawStarOfDavid is called to render the Star of David pattern on the chart based on the input parameters.

This code draws the Star of David on a chart at a specified time and price level, with customizable size, color, and line width. Adjust centerTime, centerPrice, and size as needed for different star placements on the chart.

Holt-Winters Forecast BandsDescription:

The Holt-Winters Adaptive Bands indicator combines seasonal trend forecasting with adaptive volatility bands. It uses the Holt-Winters triple exponential smoothing model to project future price trends, while Nadaraya-Watson smoothed bands highlight dynamic support and resistance zones.

This indicator is ideal for traders seeking to predict future price movements and visualize potential market turning points. By focusing on broader seasonal and trend data, it provides insight into both short- and long-term market directions. It’s particularly effective for swing trading and medium-to-long-term trend analysis on timeframes like daily and 4-hour charts, although it can be adjusted for other timeframes.

Key Features:

Holt-Winters Forecast Line: The core of this indicator is the Holt-Winters model, which uses three components — level, trend, and seasonality — to project future prices. This model is widely used for time-series forecasting, and in this script, it provides a dynamic forecast line that predicts where price might move based on historical patterns.

Adaptive Volatility Bands: The shaded areas around the forecast line are based on Nadaraya-Watson smoothing of historical price data. These bands provide a visual representation of potential support and resistance levels, adapting to recent volatility in the market. The bands' fill colors (red for upper and green for lower) allow traders to identify potential reversal zones without cluttering the chart.

Dynamic Confidence Levels: The indicator adapts its forecast based on market volatility, using inputs such as average true range (ATR) and price deviations. This means that in high-volatility conditions, the bands may widen to account for increased price movements, helping traders gauge the current market environment.

How to Use:

Forecasting: Use the forecast line to gain insight into potential future price direction. This line provides a directional bias, helping traders anticipate whether the price may continue along a trend or reverse.

Support and Resistance Zones: The shaded bands act as dynamic support and resistance zones. When price enters the upper (red) band, it may be in an overbought area, while the lower (green) band may indicate oversold conditions. These bands adjust with volatility, so they reflect the current market conditions rather than fixed levels.

Timeframe Recommendations:

This indicator performs best on daily and 4-hour charts due to its reliance on trend and seasonality. It can be used on lower timeframes, but accuracy may vary due to increased price noise.

For traders looking to capture swing trades, the daily and 4-hour timeframes provide a balance of trend stability and signal reliability.

Adjustable Settings:

Alpha, Beta, and Gamma: These settings control the level, trend, and seasonality components of the forecast. Alpha is generally the most sensitive setting for adjusting responsiveness to recent price movements, while Beta and Gamma help fine-tune the trend and seasonal adjustments.

Band Smoothing and Deviation: These settings control the lookback period and width of the volatility bands, allowing users to customize how closely the bands follow price action.

Parameters:

Prediction Length: Sets the length of the forecast, determining how far into the future the prediction line extends.

Season Length: Defines the seasonality cycle. A setting of 14 is typical for bi-weekly cycles, but this can be adjusted based on observed market cycles.

Alpha, Beta, Gamma: These parameters adjust the Holt-Winters model's sensitivity to recent prices, trends, and seasonal patterns.

Band Smoothing: Determines the smoothing applied to the bands, making them either more reactive or smoother.

Ideal Use Cases:

Swing Trading and Trend Following: The Holt-Winters model is particularly suited for capturing larger market trends. Use the forecast line to determine trend direction and the bands to gauge support/resistance levels for potential entries or exits.

Identifying Reversal Zones: The adaptive bands act as dynamic overbought and oversold zones, giving traders potential reversal areas when price reaches these levels.

Important Notes:

No Buy/Sell Signals: This indicator does not produce direct buy or sell signals. It’s intended for visual trend analysis and support/resistance identification, leaving trade decisions to the user.

Not for High-Frequency Trading: Due to the nature of the Holt-Winters model, this indicator is optimized for higher timeframes like the daily and 4-hour charts. It may not be suitable for high-frequency or scalping strategies on very short timeframes.

Adjust for Volatility: If using the indicator on lower timeframes or more volatile assets, consider adjusting the band smoothing and prediction length settings for better responsiveness.

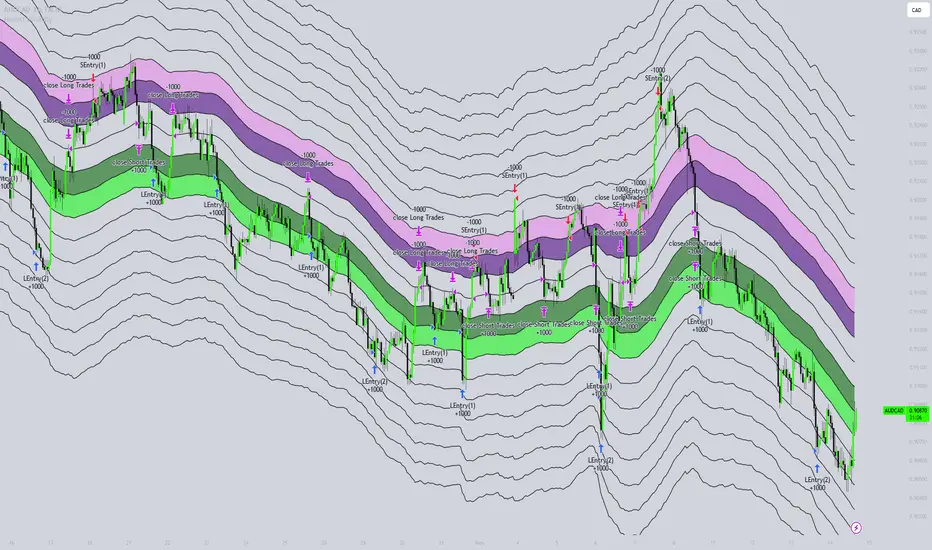

Honest Volatility Grid [Honestcowboy]The Honest Volatility Grid is an attempt at creating a robust grid trading strategy but without standard levels.

Normal grid systems use price levels like 1.01;1.02;1.03;1.04... and place an order at each of these levels. In this program instead we create a grid using keltner channels using a long term moving average.

🟦 IS THIS EVEN USEFUL?

The idea is to have a more fluid style of trading where levels expand and follow price and do not stick to precreated levels. This however also makes each closed trade different instead of using fixed take profit levels. In this strategy a take profit level can even be a loss. It is useful as a strategy because it works in a different way than most strategies, making it a good tool to diversify a portfolio of trading strategies.

🟦 STRATEGY

There are 10 levels below the moving average and 10 above the moving average. For each side of the moving average the strategy uses 1 to 3 orders maximum (3 shorts at top, 3 longs at bottom). For instance you buy at level 2 below moving average and you increase position size when level 6 is reached (a cheaper price) in order to spread risks.

By default the strategy exits all trades when the moving average is reached, this makes it a mean reversion strategy. It is specifically designed for the forex market as these in my experience exhibit a lot of ranging behaviour on all the timeframes below daily.

There is also a stop loss at the outer band by default, in case price moves too far from the mean.

What are the risks?

In case price decides to stay below the moving average and never reaches the outer band one trade can create a very substantial loss, as the bands will keep following price and are not at a fixed level.

Explanation of default parameters

By default the strategy uses a starting capital of 25000$, this is realistic for retail traders.

Lot sizes at each level are set to minimum lot size 0.01, there is no reason for the default to be risky, if you want to risk more or increase equity curve increase the number at your own risk.

Slippage set to 20 points: that's a normal 2 pip slippage you will find on brokers.

Fill limit assumtion 20 points: so it takes 2 pips to confirm a fill, normal forex spread.

Commission is set to 0.00005 per contract: this means that for each contract traded there is a 5$ or whatever base currency pair has as commission. The number is set to 0.00005 because pinescript does not know that 1 contract is 100000 units. So we divide the number by 100000 to get a realistic commission.

The script will also multiply lot size by 100000 because pinescript does not know that lots are 100000 units in forex.

Extra safety limit

Normally the script uses strategy.exit() to exit trades at TP or SL. But because these are created 1 bar after a limit or stop order is filled in pinescript. There are strategy.orders set at the outer boundaries of the script to hedge against that risk. These get deleted bar after the first order is filled. Purely to counteract news bars or huge spikes in price messing up backtest.

🟦 VISUAL GOODIES

I've added a market profile feature to the edge of the grid. This so you can see in which grid zone market has been the most over X bars in the past. Some traders may wish to only turn on the strategy whenever the market profile displays specific characteristics (ranging market for instance).

These simply count how many times a high, low, or close price has been in each zone for X bars in the past. it's these purple boxes at the right side of the chart.

🟦 Script can be fully automated to MT5

There are risk settings in lot sizes or % for alerts and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

Adaptive Kalman Trend Filter (Zeiierman)█ Overview

The Adaptive Kalman Trend Filter indicator is an advanced trend-following tool designed to help traders accurately identify market trends. Utilizing the Kalman Filter—a statistical algorithm rooted in control theory and signal processing—this indicator adapts to changing market conditions, smoothing price data to filter out noise. By focusing on state vector-based calculations, it dynamically adjusts trend and range measurements, making it an excellent tool for both trend-following and range-based trading strategies. The indicator's adaptive nature is enhanced by options for volatility adjustment and three unique Kalman filter models, each tailored for different market conditions.

█ How It Works

The Kalman Filter works by maintaining a model of the market state through matrices that represent state variables, error covariances, and measurement uncertainties. Here’s how each component plays a role in calculating the indicator’s trend:

⚪ State Vector (X): The state vector is a two-dimensional array where each element represents a market property. The first element is an estimate of the true price, while the second element represents the rate of change or trend in that price. This vector is updated iteratively with each new price, maintaining an ongoing estimate of both price and trend direction.

⚪ Covariance Matrix (P): The covariance matrix represents the uncertainty in the state vector’s estimates. It continuously adapts to changing conditions, representing how much error we expect in our trend and price estimates. Lower covariance values suggest higher confidence in the estimates, while higher values indicate less certainty, often due to market volatility.

⚪ Process Noise (Q): The process noise matrix (Q) is used to account for uncertainties in price movements that aren’t explained by historical trends. By allowing some degree of randomness, it enables the Kalman Filter to remain responsive to new data without overreacting to minor fluctuations. This noise is particularly useful in smoothing out price movements in highly volatile markets.

⚪ Measurement Noise (R): Measurement noise is an external input representing the reliability of each new price observation. In this indicator, it is represented by the setting Measurement Noise and determines how much weight is given to each new price point. Higher measurement noise makes the indicator less reactive to recent prices, smoothing the trend further.

⚪ Update Equations:

Prediction: The state vector and covariance matrix are first projected forward using a state transition matrix (F), which includes market estimates based on past data. This gives a “predicted” state before the next actual price is known.

Kalman Gain Calculation: The Kalman gain is calculated by comparing the predicted state with the actual price, balancing between the covariance matrix and measurement noise. This gain determines how much of the observed price should influence the state vector.

Correction: The observed price is then compared to the predicted price, and the state vector is updated using this Kalman gain. The updated covariance matrix reflects any adjustment in uncertainty based on the latest data.

█ Three Kalman Filter Models

Standard Model: Assumes that market fluctuations follow a linear progression without external adjustments. It is best suited for stable markets.

Volume Adjusted Model: Adjusts the filter sensitivity based on trading volume. High-volume periods result in stronger trends, making this model suitable for volume-driven assets.

Parkinson Adjusted Model: Uses the Parkinson estimator, accounting for volatility through high-low price ranges, making it effective in markets with high intraday fluctuations.

These models enable traders to choose a filter that aligns with current market conditions, enhancing trend accuracy and responsiveness.

█ Trend Strength

The Trend Strength provides a visual representation of the current trend's strength as a percentage based on oscillator calculations from the Kalman filter. This table divides trend strength into color-coded segments, helping traders quickly assess whether the market is strongly trending or nearing a reversal point. A high trend strength percentage indicates a robust trend, while a low percentage suggests weakening momentum or consolidation.

█ Trend Range

The Trend Range section evaluates the market's directional movement over a specified lookback period, highlighting areas where price oscillations indicate a trend. This calculation assesses how prices vary within the range, offering an indication of trend stability or the likelihood of reversals. By adjusting the trend range setting, traders can fine-tune the indicator’s sensitivity to longer or shorter trends.

█ Sigma Bands

The Sigma Bands in the indicator are based on statistical standard deviations (sigma levels), which act as dynamic support and resistance zones. These bands are calculated using the Kalman Filter's trend estimates and adjusted for volatility (if enabled). The bands expand and contract according to market volatility, providing a unique visualization of price boundaries. In high-volatility periods, the bands widen, offering better protection against false breakouts. During low volatility, the bands narrow, closely tracking price movements. Traders can use these sigma bands to spot potential entry and exit points, aiming for reversion trades or trend continuation setups.

Trend Based

Volatility Based

█ How to Use

Trend Following:

When the Kalman Filter is green, it signals a bullish trend, and when it’s red, it indicates a bearish trend. The Sigma Cloud provides additional insights into trend strength. In a strong bullish trend, the cloud remains below the Kalman Filter line, while in a strong bearish trend, the cloud stays above it. Expansion and contraction of the Sigma Cloud indicate market momentum changes. Rapid expansion suggests an impulsive move, which could either signal the continuation of the trend or be an early sign of a possible trend reversal.

Mean Reversion: Watch for prices touching the upper or lower sigma bands, which often act as dynamic support and resistance.

Volatility Breakouts: Enable volatility-adjusted sigma bands. During high volatility, watch for price movements that extend beyond the bands as potential breakout signals.

Trend Continuation: When the Kalman Filter line aligns with a high trend strength, it signals a continuation in that direction.

█ Settings

Measurement Noise: Adjusts how sensitive the indicator is to price changes. Higher values smooth out fluctuations but delay reaction, while lower values increase sensitivity to short-term changes.

Kalman Filter Model: Choose between the standard, volume-adjusted, and Parkinson-adjusted models based on market conditions.

Band Sigma: Sets the standard deviation used for calculating the sigma bands, directly affecting the width of the dynamic support and resistance.

Volatility Adjusted Bands: Enables bands to dynamically adapt to volatility, increasing their effectiveness in fluctuating markets.

Trend Strength: Defines the lookback period for trend strength calculation. Shorter periods result in more responsive trend strength readings, while longer periods smooth out the calculation.

Trend Range: Specifies the lookback period for the trend range, affecting the assessment of trend stability over time.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Performance-INDIA & GLOBAL MARKETS-MADGrowth vs. Stability: India is expected to maintain relatively strong economic growth compared to many other global markets, which are facing slower growth or even recession risks. The Indian economy is benefiting from a large domestic market, young population, and rising digital and infrastructure investments.

Volatility: Indian markets are often more volatile due to domestic factors, such as political changes, policy announcements, and inflationary pressures. Global markets, on the other hand, tend to experience volatility based on external economic factors and geopolitical risks.

Inflation and Interest Rates: Both India and global markets are dealing with inflation, but India’s central bank (RBI) is seen as being proactive in controlling inflation through interest rate hikes. Globally, major central banks like the Fed and ECB are tightening their monetary policies, which is contributing to global economic slowdown concerns.

RB Donchian Channel with Deviation RetracementBased on the Donchian Channel, this trading indicator leverages deviation retracements within the channel to identify strategic exit points and capture directional momentum. The Donchian Channel plots the highest high and lowest low over a specified period, creating a range that helps traders monitor price movements. By focusing on retracements within this range, the indicator allows traders to pinpoint exit levels, minimizing potential losses or securing gains as trends fluctuate. It uses a color-coded system to enhance readability and quick decision-making: blue indicates a long position, while red signals a short position. This approach to using retracements within the Donchian Channel provides a structured method for traders to follow momentum shifts and make data-driven trading choices.

Multifactor Buy/Sell Strategy V2 | RSI, MACD, ATR, EMA, Boll.BITGET:1INCHUSDT

This Pine Script code for TradingView is a multifactor Buy/Sell indicator that combines several technical factors to generate trading signals based on trend, volatility, and volume conditions. Here’s a breakdown of the main components and functionality:

Indicator Name

- Multifactor Buy/Sell Strategy V2 — an overlay indicator applied directly on the price chart.

### Input Parameters

The script includes multiple customizable parameters:

- RSI, EMA, MACD parameters — for setting periods and signals of MACD and RSI.

- ATR and Bollinger Bands — used for volatility analysis and level determination.

- Minimum Volatility Threshold — sets a minimum Bollinger Band width threshold for determining high volatility.

Core Indicators

1. RSI — calculated to identify oversold (below 30) and overbought (above 70) conditions.

2. EMA and MACD — calculates exponential moving averages and MACD histogram to determine trend direction.

3. ATR and Bollinger Bands — used to assess current volatility and establish dynamic upper and lower bands.

Volatility and Volume Analysis

- Determines the current ATR level and Bollinger Band width to evaluate high volatility.

- Calculates the volume moving average to track periods of increased volume during high volatility.

Trend Analysis

The script uses the difference between fast and slow EMAs to define strong trends:

- Uptrend — when the fast EMA is above the slow EMA, the price is above the fast EMA, and the trend is strong.

- Downtrend — when the fast EMA is below the slow EMA, the price is below the fast EMA, and the trend is strong.

Momentum Filter

- Based on the price change over the last three bars and compared against the minimum volatility threshold to identify strong momentum.

Buy and Sell Signal Generation

- Buy Signal: Uptrend with RSI oversold, positive MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

- Sell Signal: Downtrend with RSI overbought, negative MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

Visualization

- Buy and sell signals are displayed as green and red triangles on the chart.

- Plots for fast and slow EMAs, upper and lower bands, and Bollinger Bands.

Alerts

The script includes alert conditions for buy and sell signals, allowing notifications to be sent via email or mobile app.

Information Panel

A small table on the chart displays current volatility dataThis Pine Script code for TradingView is a multifactor Buy/Sell indicator that combines several technical factors to generate trading signals based on trend, volatility, and volume conditions. Here’s a breakdown of the main components and functionality:

Indicator Name

- Multifactor Buy/Sell Strategy V2 — an overlay indicator applied directly on the price chart.

Input Parameters

The script includes multiple customizable parameters:

- **RSI, EMA, MACD parameters** — for setting periods and signals of MACD and RSI.

- **ATR and Bollinger Bands** — used for volatility analysis and level determination.

- **Minimum Volatility Threshold** — sets a minimum Bollinger Band width threshold for determining high volatility.

Core Indicators

1. RSI — calculated to identify oversold (below 30) and overbought (above 70) conditions.

2. EMA and MACD — calculates exponential moving averages and MACD histogram to determine trend direction.

3. ATR and Bollinger Bands — used to assess current volatility and establish dynamic upper and lower bands.

Volatility and Volume Analysis

- Determines the current ATR level and Bollinger Band width to evaluate high volatility.

- Calculates the volume moving average to track periods of increased volume during high volatility.

Trend Analysis

The script uses the difference between fast and slow EMAs to define strong trends:

- Uptrend — when the fast EMA is above the slow EMA, the price is above the fast EMA, and the trend is strong.

- Downtrend — when the fast EMA is below the slow EMA, the price is below the fast EMA, and the trend is strong.

Momentum Filter

- Based on the price change over the last three bars and compared against the minimum volatility threshold to identify strong momentum.

Buy and Sell Signal Generation

- Buy Signal: Uptrend with RSI oversold, positive MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

- Sell Signal: Downtrend with RSI overbought, negative MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

Visualization

- Buy and sell signals are displayed as green and red triangles on the chart.

- Plots for fast and slow EMAs, upper and lower bands, and Bollinger Bands.

Alerts

The script includes alert conditions for buy and sell signals, allowing notifications to be sent via email or mobile app.

Information Panel

A small table on the chart displays current volatility

- Volatility Status — indicates high or low volatility.

- Bollinger Band Width — current width as a percentage.

- ATR Ratio — ratio of current ATR to long-term average ATR.

This script is suitable for trading in high-volatility conditions, combining multiple filters and factors to generate precise buy and sell signals.

Multi-Timeframe Moving Averages by Skyito"Hope everyone likes this and finds it useful! This multi-timeframe moving average indicator provides a comprehensive view of moving averages from various timeframes directly on one chart. It’s designed to help traders analyze market trends and levels more effectively without constantly switching between charts.

Script Explanation: This indicator supports a range of moving average types, including SMA, EMA, HMA, WMA, VWMA, RMA, SSMA, and DEMA, allowing for flexibility in analysis. Each moving average is fully customizable by length and type for each timeframe, giving you control over how trends are represented.

The indicator includes timeframes such as 15 minutes, 1 hour, 4 hours, 6 hours, 8 hours, 12 hours, 1 day, 3 days, 5 days, 1 week, 3 weeks, and 1 month. Each moving average is displayed as a line with a small dashed extension, showing a label that contains the moving average’s timeframe, type, and current price level. The dark blue labels are slightly enlarged to enhance readability on the chart, making it easier to track important levels at a glance.

Use Case: This tool is ideal for traders looking to stay aware of trend levels across multiple timeframes on one chart. Adjusting the moving averages’ lengths and types enables customization for any strategy, while the label information provides an immediate understanding of the timeframe and trend context.

Enjoy the streamlined view and the added insights from multi-timeframe analysis!"

Dollar Cost Averaging (YavuzAkbay)The Dollar Cost Averaging (DCA) indicator is designed to support long-term investors following a Dollar Cost Averaging strategy. The core aim of this tool is to provide insights into overbought and oversold levels, assisting investors in managing buy and sell decisions with a clear visual cue system. Specifically developed for use in trending or fluctuating markets, this indicator leverages support and resistance levels to give structure to investors' buying strategies. Here’s a detailed breakdown of the indicator’s key features and intended usage:

Key Features and Color Coding

Overbought/Oversold Detection:

The indicator shades candles from light green to dark green when an asset becomes increasingly overbought. Dark green signals indicate a peak, where the asset is overbought, suggesting a potential opportunity to take partial profits.

Conversely, candles turn from light red to dark red when the market is oversold. Dark red signifies a heavily oversold condition, marking an ideal buying window for initiating or adding to a position. This color scheme provides a quick visual reference for investors to manage entries and exits effectively.

Support and Resistance Levels:

To address the risk of assets falling further after an overbought signal, the DCA indicator dynamically calculates support and resistance levels. These levels guide investors on key price areas to watch for potential price reversals, allowing them to make more informed buying or selling decisions.

Support levels help investors assess whether they should divide their capital across multiple buy orders, starting at the current oversold zone and extending to anticipated support zones for maximum flexibility.

Usage Methodology

This indicator is intended for Dollar Cost Averaging, a method where investors gradually add to their position rather than entering all at once. Here’s how it complements the DCA approach:

Buy at Oversold Levels: When the indicator shows a dark red candle, it signals that the asset is oversold, marking an optimal entry point. The presence of support levels can help investors determine if they should fully invest their intended amount or stagger buys at potential lower levels.

Sell at Overbought Levels: When the indicator transitions to dark green, it suggests that the asset is overbought. This is an ideal time to consider selling a portion of holdings to realize gains. The resistance levels, marked by the indicator, offer guidance on where the price may encounter selling pressure, aiding investors in planning partial exits.

Customizable Settings

The DCA indicator offers several user-adjustable parameters:

Pivot Frequency and Source: Define the pivot point frequency and the source (candle wick or body) for more tailored support/resistance detection.

Maximum Pivot Points: Set the maximum number of pivot points to be used in support/resistance calculations, providing flexibility in adapting to different market structures.

Channel Width and Line Width: Adjust the width of the channel for support/resistance levels and the thickness of the lines for easier visual tracking.

Color Intensities for Overbought/Oversold Levels: Customize the shading intensity for each overbought and oversold level to align with your trading preferences.

Bollinger Bands + RSI StrategyThe Bollinger Bands + RSI strategy combines volatility and momentum indicators to spot trading opportunities in intraday settings. Here’s a concise summary:

Components:

Bollinger Bands: Measures market volatility. The lower band signals potential buying opportunities when the price is considered oversold.

Relative Strength Index (RSI): Evaluates momentum to identify overbought or oversold conditions. An RSI below 30 indicates oversold, suggesting a buy, and above 70 indicates overbought, suggesting a sell.

Strategy Execution:

Buy Signal : Triggered when the price falls below the lower Bollinger Band while the RSI is also below 30.

Sell Signal : Activated when the price exceeds the upper Bollinger Band with an RSI above 70.

Exit Strategy : Exiting a buy position is considered when the RSI crosses back above 50, capturing potential rebounds.

Advantages:

Combines price levels with momentum for more reliable signals.

Clearly defined entry and exit points help minimize emotional trading.

Considerations:

Can produce false signals in very volatile or strongly trending markets.

Best used in markets without a strong prevailing trend.

This strategy aids traders in making decisions based on technical indicators, enhancing their ability to profit from short-term price movements.

Liquidity Channels [TFO]This indicator was built to visually demonstrate the significance of major, untouched pivots. With traders commonly placing orders at or near significant pivots, these areas are commonly referred to as Resting Liquidity. If we attribute some factor of growth over time, we can quickly visualize that certain pivots originated much further away than others, if their channels appear larger.

A pivot in this case is validated by the Liquidity Strength parameter. If set to 50 for example, then a pivot high is validated if its high is greater than the high of the 50 bars to the left and right of itself. This also implies a delay in finding pivots, as the drawings won't actually appear until validation, which would occur 50 bars after the original high has formed in this case. This is typical of indicators using swing highs and lows, as one must wait some period of time to validate the pivots in question.

The Channel Growth parameter dictates how much the Liquidity Channels will expand over time. The following chart is an example, where the left-hand side is using a Channel Growth of 1, and the right-hand side is using a Channel Growth of 10.

When price reaches these levels, they become invalidated and will stop extending to the right. The other condition for invalidation is the Delete After (Bars) parameter which, when enabled, declares that untouched levels will be deleted if the distance from their origin exceeds this many bars.

This indicator also offers an option to Hide Expanding Channels for those who just want the actual levels on their chart, without the extra visuals, which would look something like the below chart.

Nasan Hull-smoothed envelope The Nasan Hull-Smoothed Envelope indicator is a sophisticated overlay designed to track price movement within an adaptive "envelope." It dynamically adjusts to market volatility and trend strength, using a series of smoothing and volatility-correction techniques. Here's a detailed breakdown of its components, from the input settings to the calculated visual elements:

Inputs

look_back_length (500):

Defines the lookback period for calculating intraday volatility (IDV), smoothing it over time. A higher value means the indicator considers a longer historical range for volatility calculations.

sl (50):

Sets the smoothing length for the Hull Moving Average (HMA). The HMA smooths various lines, creating a balance between sensitivity and stability in trend signals.

mp (1.5):

Multiplier for IDV, scaling the volatility impact on the envelope. A higher multiplier widens the envelope to accommodate higher volatility, while a lower one tightens it.

p (0.625):

Weight factor that determines the balance between extremes (highest high and lowest low) and averages (sma of high and sma of low) in the high/low calculations. A higher p gives more weight to extremes, making the envelope more responsive to abrupt market changes.

Volatility Calculation (IDV)

The Intraday Volatility (IDV) metric represents the average volatility per bar as an exponentially smoothed ratio of the high-low range to the close price. This is calculated over the look_back_length period, providing a base volatility value which is then scaled by mp. The IDV enables the envelope to dynamically widen or narrow with market volatility, making it sensitive to current market conditions.

Composite High and Low Bands

The high and low bands define the upper and lower bounds of the envelope.

High Calculation

a_high:

Uses a multi-period approach to capture the highest highs over several intervals (5, 8, 13, 21, and 34 bars). Averaging these highs provides a more stable reference for the high end of the envelope, capturing both immediate and recent peak values.

b_high:

Computes the average of shorter simple moving averages (5, 8, and 13 bars) of the high prices, smoothing out fluctuations in the recent highs. This generates a balanced view of high price trends.

high_c:

Combines a_high and b_high using the weight p. This blend creates a composite high that balances between recent peaks and smoothed averages, making the upper envelope boundary adaptive to short-term price shifts.

Low Calculation

a_low and b_low:

Similar to the high calculation, these capture extreme lows and smooth low values over the same intervals. This approach creates a stable and adaptive lower bound for the envelope.

low_c:

Combines a_low and b_low using the weight p, resulting in a composite low that adjusts to price fluctuations while maintaining a stable trend line.

Volatility-Adjusted Bands

The final composite high (c_high) and composite low (c_low) bands are adjusted using IDV, which accounts for intraday volatility. When volatility is high, the bands expand; when it’s low, they contract, providing a visual representation of volatility-adjusted price bounds.

Basis Line

The basis line is a Hull Moving Average (HMA) of the average of c_high and c_low. The HMA is known for its smoothness and responsiveness, making the basis line a central trend indicator. The color of the basis line changes:

Green when the basis line is increasing.

Red when the basis line is decreasing.

This color-coded basis line serves as a quick visual reference for trend direction.

Short-Term Trend Strength Block

This component analyzes recent price action to assess short-term bullish and bearish momentum.

Conditions (green, red, green1, red1):

These are binary conditions that categorize price movements as bullish or bearish based on the close compared to the open and the close’s relationship with the exponential moving average (EMA). This separation helps capture different types of strength (above/below EMA) and different bullish or bearish patterns.

Composite Trend Strength Values:

Each of the bullish and bearish counts (above and below the EMA) is normalized, resulting in the following values:

green_EMAup_a and red_EMAup_a for bullish and bearish strength above the EMA.

green_EMAdown_a and red_EMAdown_a for bullish and bearish strength below the EMA.

Trend Strength (t_s):

This calculated metric combines the normalized trend strengths with extra weight to conditions above the EMA, giving more relevance to trends that have momentum behind them.

Enhanced Trend Strength

avg_movement:

Calculates the average absolute price movement over the short_term_length, providing a measurement of recent price activity that scales with volatility.

enhanced_t_s:

Multiplies t_s by avg_movement, creating an enhanced trend strength value that reflects both directional strength and the magnitude of recent price movement.

min and max:

Minimum and maximum percentile thresholds, respectively, based on enhanced_t_s for controlling the color gradient in the fill area.

Fill Area

The fill area between plot_c_high and plot_c_low is color-coded based on the enhanced trend strength (enhanced_t_s):

Gradient color transitions from blue to green based on the strength level, with blue representing weaker trends and green indicating stronger trends.

This visual fill provides an at-a-glance assessment of trend strength across the envelope, with color shifts highlighting momentum shifts.

Summary

The indicator’s purpose is to offer an adaptive price envelope that reflects real-time market volatility and trend strength. Here’s what each component contributes:

Basis Line: A trend-following line in the center that adjusts color based on trend direction.

Envelope (c_high, c_low): Adapts to volatility by expanding and contracting based on IDV, giving traders a responsive view of expected price bounds.

Fill Area: A color-gradient region representing trend strength within the envelope, helping traders easily identify momentum changes.

Overall, this tool helps to identify trend direction, market volatility, and strength of price movements, allowing for more informed decisions based on visual cues around price boundaries and trend momentum.

MACD+RSI+BBDESCRIPTION

The MACD + RSI + Bollinger Bands Indicator is a comprehensive technical analysis tool designed for traders and investors to identify potential market trends and reversals. This script combines three indicators: the Moving Average Convergence Divergence (MACD), the Relative Strength Index (RSI), and Bollinger Bands. Each of these indicators provides unique insights into market behavior.

FEATURES

MACD (Moving Average Convergence Divergence)

The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price.

The script calculates the MACD line, the signal line, and the histogram, which visually represents the difference between the MACD line and the signal line.

RSI (Relative Strength Index)

The RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is typically used to identify overbought or oversold conditions.

The script allows users to set custom upper and lower thresholds for the RSI, with default values of 70 and 30, respectively.

Bollinger Bands

Bollinger Bands consist of a middle band (EMA) and two outer bands (standard deviations away from the EMA). They help traders identify volatility and potential price reversals.

The script allows users to customize the length of the Bollinger Bands and the multiplier for the standard deviation.

Color-Coding Logic

The histogram color changes based on the following conditions:

Black: If the RSI is above the upper threshold and the closing price is above the upper Bollinger Band, or if the RSI is below the lower threshold and the closing price is below the lower Bollinger Band.

Green (#4caf50): If the RSI is above the upper threshold but the closing price is not above the upper Bollinger Band.

Light Green (#a5d6a7): If the histogram is positive and the RSI is not above the upper threshold.

Red (#f23645): If the RSI is below the lower threshold but the closing price is not below the lower Bollinger Band.

Light Red (#faa1a4): If the histogram is negative and the RSI is not below the lower threshold.

Inputs

Bollinger Bands Settings

Length: The number of periods for the moving average.

Basis MA Type: The type of moving average (SMA, EMA, SMMA, WMA, VWMA).

Source: The price source for the Bollinger Bands calculation.

StdDev: The multiplier for the standard deviation.

RSI Settings

RSI Length: The number of periods for the RSI calculation.

RSI Upper: The upper threshold for the RSI.

RSI Lower: The lower threshold for the RSI.

Source: The price source for the RSI calculation.

MACD Settings

Fast Length: The length for the fast moving average.

Slow Length: The length for the slow moving average.

Signal Smoothing: The length for the signal line smoothing.

Oscillator MA Type: The type of moving average for the MACD calculation.

Signal Line MA Type: The type of moving average for the signal line.

Usage

This indicator is suitable for various trading strategies, including day trading, swing trading, and long-term investing.

Traders can use the MACD histogram to identify potential buy and sell signals, while the RSI can help confirm overbought or oversold conditions.

The Bollinger Bands provide context for price volatility and potential breakout or reversal points.

Example:

From the example, it can clearly see that the Selling Climax and Buying Climax, marked as orange circle when a black histogram occurs.

Conclusion

The MACD + RSI + Bollinger Bands Indicator is a versatile tool that combines multiple technical analysis methods to provide traders with a comprehensive view of market conditions. By utilizing this script, traders can enhance their analysis and improve their decision-making process.

Period MarkerThis Period Marker Indicator for TradingView is a visual tool that allows you to highlight a specific date range on your chart. It uses a shaded background color to mark the defined period, making it easy to visually separate and focus on specific time intervals. This is especially useful for analyzing historical events, comparing specific timeframes, or marking earnings seasons or other critical periods in price action.

Key Features

Easy Date Range Selection:

The indicator has a calendar-style date input for both the start and end dates. This allows for quick and precise selection of date ranges without manually entering each date component (year, month, day).

Customizable Period Highlight:

When active, the indicator shades the background of the chart over the specified period. The default highlight color is a semi-transparent green, but this can be customized within the script to any color and opacity you prefer.

The shaded background helps you easily identify and focus on the defined date range.

Dynamic Adjustment:

You can adjust the start and end dates in real-time, and the background shading will automatically update to reflect the new period, allowing flexibility in testing and viewing multiple periods quickly.

Practical Uses

Event Marking: Track significant historical events (e.g., economic data releases, geopolitical events) to see their effects on price action.

Seasonal Analysis: Highlight and compare seasonal trends, such as quarterly earnings or year-end rallies, across multiple years.

Backtesting Specific Periods: When analyzing strategies, you can visually isolate specific date ranges to review performance or behavior in defined intervals.

The Period Marker Indicator is a simple yet effective way to enhance time-based analysis on TradingView, helping you gain insights by focusing on relevant periods with ease.

Nami Bands with Future Projection [FXSMARTLAB]The Nami Bands ( Inspired by "Nami", meaning "wave" in Japanese) are two dynamic bands around price data: an upper band and a lower band. These bands are calculated based on an Asymmetric Linear Weighted Moving Average of price and a similarly asymmetric weighted standard deviation. This weighting method emphasizes recent data without overreacting to short-term price changes, thus smoothing the bands in line with prevailing market conditions.

Advantages and Benefits of Using the Indicator

* Volatility Analysis: The bands expand and contract with market volatility, helping traders assess periods of high and low volatility. Narrow bands indicate low volatility and potential consolidation, while wide bands suggest increased volatility and potential price movement.

* Dynamic Support and Resistance Levels: By adapting to recent trends, the bands serve as dynamic support (lower band) and resistance (upper band) levels, which traders can use for entry and exit signals.

* Overbought and Oversold Conditions: When prices reach or cross the bands’ outer limits, it may signal overbought (upper band) or oversold (lower band) conditions, suggesting possible reversals or trend slowdowns.

* Trend Confirmation and Continuation: The slope of the central moving average confirms trend direction. An upward slope generally indicates a bullish trend, while a downward slope suggests a bearish trend.

* Anticipating Breakouts and Reversals: The projected bands help identify where price movements may head, allowing traders to anticipate potential breakouts or reversals based on projected support and resistance.

Indicator Parameters

Source (src): The price data used for calculations, by default set to the average of high, low, and close (hlc3).

Length: The period over which calculations are made, defaulted to 50 periods.

Projection Length: The length for future band projection, defaulted to 20 periods.

StdDev Multiplier (mult): A multiplier for the standard deviation, defaulted to 2.0.

Internal Calculations

1. Asymmetric Linear Weighted Moving Average of Price

The indicator uses an Asymmetric Linear Weighted Moving Average (ALWMA) to calculate a central value for the price.

Asymmetric Weighting: This weighting technique assigns the highest weight to the most recent value, with weights decreasing linearly as the data points become older. This structure provides a nuanced focus on recent price trends, while still reflecting historical price levels.

2. Asymmetric Weighted Standard Deviation

The standard deviation in this indicator is also calculated using asymmetric weighting:

Purpose of Asymmetric Weighted Standard Deviation: Rather than aiming for high sensitivity to recent data, this standard deviation measure smooths out volatility by integrating weighted values across the length period, stabilizing the overall measurement of price variability.

This approach yields a balanced view of volatility, capturing broader market trends without being overly reactive to short-lived changes.

3. Upper and Lower Bands

The upper and lower bands are created by adding and subtracting the asymmetric weighted standard deviation from the asymmetric weighted average of price. This creates a dynamic envelope that adjusts to both recent price trends and the smoothed volatility measure:

These bands represent adaptable support and resistance levels that shift with recent market volatility.

Future Band Projection

The indicator provides a projection of the bands based on their current slope.

1. Calculating the Slope of the Bands

The slope for each band is derived from the difference between the current and previous values of each band.

2. Projecting the Bands into the Future

For each period into the future, up to the defined Projection Length, the bands are projected using the current slope.

This feature offers an anticipated view of where support and resistance levels may move, providing insight for future market behavior based on current trends.

Market Structure Algo V2 [OmegaTools]The Market Structure Algo V2 (MS Algo V2) is an advanced TradingView indicator developed by OmegaTools to provide traders with a comprehensive analysis of market structure. This tool refines the insights provided by its predecessor, combining enhanced pivot point analysis, dynamic market structure scoring, and zone visualization to deliver an intuitive view of potential market movements. Through custom settings, the MS Algo V2 allows users to tailor the indicator to fit their trading strategies more closely, offering enhanced adaptability to both short-term and long-term trends.

Core Functionality

The MS Algo V2 differentiates between internal and external market structures by analyzing pivot highs and lows over user-defined periods. The internal market structure focuses on shorter timeframes, providing insights into recent price action, while the external structure considers broader trends. This dual-layered approach helps traders distinguish between immediate and overarching market trends.

The indicator introduces improved visualization for areas of interest or zones around pivot points, adjustable through zone distance settings. These zones serve as potential support and resistance areas, helping traders anticipate price reactions at key levels. In addition to the zones, the indicator now provides gradient-based color coding on bars, reflecting the market structure’s bullish or bearish intensity. This visual enhancement aids in quickly interpreting the current trend's strength.

Dynamic signal generation has been refined in MS Algo V2. The indicator now offers both classic signals and breakout signals based on the market structure, including entries, exits, and change-of-character (CHoCH) alerts. Signals are generated based on price interactions with pivot levels, indicating potential long and short opportunities.

Operational Mechanism

The MS Algo V2 calculates pivot highs and lows over specified periods to define internal and external market structures. A market structure score is derived from these pivot points, classifying the market into bullish or bearish extremes. Signals are generated as the closing price interacts with these levels, marking entry and exit points based on the calculated structure.

A new feature in this version is zone visualization, where zones are plotted around a dynamic moving average derived from the exponential and simple moving averages (EMA and SMA). The zones are adjusted based on ATR (Average True Range) and the specified zone distance percentile, providing a clear visual representation of potential support and resistance regions. The external and internal zones are represented with different levels of transparency for quick reference.

Usage Guidelines

To apply the MS Algo V2 to your TradingView charts, adjust the internal and external market structure settings to match your preferred analysis timeframes. The line style and width of each structure can also be customized for a tailored view. The Zone Distance setting allows users to define the percentile range of the zones around the moving average, providing further flexibility in identifying potential areas of support and resistance.

For a color-coded overview of market sentiment, the bar gradient feature can be enabled. This option uses a gradient that reflects the bullish or bearish intensity of the market structure, giving traders a visual cue on the market’s overall trend. Color-coded signals and zone fill areas further assist in interpreting the current market structure and identifying potential trade areas.

The indicator includes customizable alerts for long and short signals, as well as specific breakout alerts (BOS) and change-of-character (CHoCH) signals. These alerts can help traders stay informed about significant market structure changes, supporting timely trading decisions.

Understanding the Indicator’s Originality

The MS Algo V2 stands out due to its robust integration of pivot analysis, zone visualization, and market structure scoring, offering a unique perspective on market dynamics. With features like color-coded signals, bar gradients, and configurable alerts, MS Algo V2 provides an edge in understanding both the current market environment and potential turning points. This indicator’s ability to represent the market’s structure visually makes it a powerful addition to any trader’s toolkit, especially for those seeking a deeper, multi-layered approach to market analysis.