Market Strength Buy Sell Indicator [TradeDots]A specialized tool designed to assist traders in evaluating market conditions through a multifaceted analysis of relative performance, beta-adjusted returns, momentum, and volume—allowing you to identify optimal points for long or short trades. By integrating multiple benchmarks (default S&P 500) and percentile-based thresholds, the script provides clear, actionable insights suitable for both day trading and higher-level timeframe assessments.

📝 HOW IT WORKS

1. Multi-Factor Composite Score

Relative Performance (RS Ratio): Compares your asset’s performance to a chosen benchmark (default: SPY). Values above 1.0 indicate outperformance, while below 1.0 suggest underperformance.

Beta-Adjusted Returns: Checks the ticker’s excess movement relative to expected market-related moves. This helps distinguish pure “alpha” from broad market effects.

Volume & Correlation: Volume spikes often confirm the momentum behind a move, while correlation measures how closely the asset tracks or diverges from its benchmark.

These components merge into a 0–100 composite score. Scores above 50 frequently imply bullish strength; drops below 50 often point to underperformance—potentially flagging short opportunities.

2. Intraday & Day Trading Focus

Monitoring Below 50: During the trading day, the script calculates live data against the benchmark, offering an intraday-sensitive composite score. A dip under 50 may indicate a short bias for that session, especially when accompanied by high volume or momentum shifts.

3. Higher Timeframe Monitoring

Daily Strategies: On daily or weekly charts, the script reveals overall relative strength or weakness compared to the S&P 500. This higher-level perspective helps form broader trading biases—crucial for swing or position trades spanning multiple days.

Long/Short Thresholds: Persistent readings above 50 on a daily chart typically reinforce a long bias, while consistent dips below 50 can sustain a short or cautious outlook.

4. Pair Trading Applications

Custom Benchmark Selection: By setting a specific ticker pair as your benchmark instead of the default S&P 500, you can identify spread trading opportunities between two correlated assets. This allows you to go long the outperforming asset while shorting the underperforming one when the spread reaches extreme levels.

4. Color-Coded Signals & Alerts

Visual Zones (25–75): Color-coded bands highlight strong outperformance (above 75) or pronounced underperformance (below 25).

Alerts on Strong Shifts: Automatic alerts can notify you of sudden entries or exits from bullish or bearish zones, so you can potentially act on new market information without delay.

⚙️ HOW TO USE

1. Select Your Timeframe: For scalping or day trading, lower intervals (e.g., 5-minute) offer immediate data resets at the session’s start. For multi-day insight, daily or weekly charts reveal broader performance trends.

2. Watch Key Levels Around 50: Intraday dips under 50 may be a cue to consider short trades, while bounces above 50 can confirm renewed strength.

3. Assess Benchmark Relationships: Compare your asset’s score and signals to the broader market. A stock falling below its pair’s relative strength line might lag overall market momentum.

4. Combine Tools & Validate: This script excels when integrated with other technical analysis methods (e.g., support/resistance, chart patterns) and fundamental factors for a holistic market view.

❗ LIMITATIONS

No Direction Guarantee: The indicator identifies relative strength but does not guarantee directional price moves.

Delayed Updates: Since calculations update after each bar close, sudden intrabar changes may not immediately reflect.

Market-Specific Behaviors: Some assets or unusual market conditions may deviate from typical benchmarks, weakening signal reliability.

Past ≠ Future: High or low relative strength in the past may not predict continued performance.

RISK DISCLAIMER

All forms of trading and investing involve risk, including the possible loss of principal. This indicator analyzes relative performance but cannot assure profits or eliminate losses. Past performance of any strategy does not guarantee future results. Always combine analysis with proper risk management and your broader trading plan. Consult a licensed financial advisor if you are unsure of your individual risk tolerance or investment objectives.

Benchmark

Custom Index CompositeCustom Index Composite calculates an unweighted composite index by averaging the daily returns of multiple stock tickers. Instead of using price-level weighting, it focuses solely on percentage change, allowing you to compare diverse market themes side by side on a common basis.

Why Use a Custom Index Composite?

Unlike traditional indices that often lean on market capitalization or price-level data, a custom composite based solely on returns strips out the bias inherent to high-priced stocks. This provides several benefits:

Objective Cross-Comparison:

When stocks or market themes trade at very different price levels, it can be difficult to assess performance objectively. Using percentage returns, the composite creates an even playing field, enabling a clear comparison between different assets or themes.

Tailored Benchmarking:

By selecting and combining specific tickers, you can create benchmarks that better represent the segments or strategies you’re interested in. This is particularly useful when standard indices do not capture the nuances of your investment approach.

Performance Normalization:

Converting raw price data into daily percentage returns minimizes distortions that arise from price differences. This normalization helps in understanding true performance trends across the chosen tickers, making the composite index a more reliable gauge of relative market movement.

Custom Analysis Framework:

The indicator offers flexibility to adjust the lookback period (defaulting to about 3 months) so you can fine-tune the sensitivity of the index to recent market behavior. This enables you to either smooth out volatility or capture a more immediate trend, depending on your analytical needs.

Key Features:

Configurable Appearance:

You can easily configure the line color, line width, index name, and index name color via the options panel.

Ticker Configuration:

By default, you can enter up to 15 different tickers into the composite index. Technically, the indicator supports up to 40 tickers (these additional inputs are commented out by default to maintain performance), and you may enable them individually if required.

Calculated Bars Length:

The indicator uses a “Calculated bars length” setting, which is set by default to 63 days (approximately 3 months). This value can be adjusted, and it is recommended to use the greatest common denominator for consistent analysis.

How To Configure Your Chart:

Add the Indicator:

Place the Custom Index Composite on your chart.

Disable Main Symbol Visibility:

Hide the primary symbol’s plot and set its scale to “None” to prevent interference with the composite display.

Pin to Right Scale:

Set the scale of the first composite indicator to “Pinned to right scale.” This helps maintain consistency across different composite indicators.

Add Multiple Composites:

You can add additional composite indicators and set their scales to “Pinned to right scale” (or alternatively to “A”) for convenient comparison.

Limitations:

If a ticker symbol is set once in the options, it cannot be cleared to an empty value later. As a result, the symbol will continue to appear in the indicator’s title on the chart. The only way to remove an unwanted symbol is to completely reset the settings and re-enter your desired tickers.

Relative Performance Indicator by ComLucro - 2025_V01The "Relative Performance Indicator by ComLucro - 2025_V01" is a powerful tool designed to analyze an asset's performance relative to a benchmark index over multiple timeframes. This indicator provides traders with a clear view of how their chosen asset compares to a market index in short, medium, and long-term periods.

Key Features:

Customizable Lookback Periods: Analyze performance across three adjustable periods (default: 20, 50, and 200 bars).

Relative Performance Analysis: Calculate and visualize the difference in percentage performance between the asset and the benchmark index.

Dynamic Summary Label: Displays a detailed breakdown of the asset's and index's performance for the latest bar.

User-Friendly Interface: Includes customizable colors and display options for clear visualization.

How It Works:

The script fetches closing prices of both the asset and a benchmark index.

It calculates percentage changes over the selected lookback periods.

The indicator then computes the relative performance difference between the asset and the index, plotting it on the chart for easy trend analysis.

Who Is This For?:

Traders and investors who want to compare an asset’s performance against a benchmark index.

Those looking to identify trends and deviations between an asset and the broader market.

Disclaimer:

This tool is for educational purposes only and does not constitute financial or trading advice. Always use it alongside proper risk management strategies and backtest thoroughly before applying it to live trading.

Chart Recommendation:

Use this script on clean charts for better clarity. Combine it with other technical indicators like moving averages or trendlines to enhance your analysis. Ensure you adjust the lookback periods to match your trading style and the timeframe of your analysis.

Additional Notes:

For optimal performance, ensure the benchmark index's data is available on your TradingView subscription. The script uses fallback mechanisms to avoid interruptions when index data is unavailable. Always validate the settings and test them to suit your trading strategy.

Relative Performance AnalysisRelative Performance Analysis Script

This Pine Script creates a detailed table on your TradingView chart to compare the performance of a specified asset against a benchmark over multiple time frames. The table is fully customizable, allowing you to select its location on the chart and display performance metrics for different periods.

Features:

Customizable Table Location: Choose where the table appears on your chart from a range of predefined positions (e.g., bottom left, top center).

Dynamic Column Headers: The table includes columns for the ticker, description, and performance metrics for various time periods (1 day, 1 week, 1 month, 3 months, 6 months, and 1 year).

Performance Calculation: Calculates the percentage change in performance between the current close price and the previous close price for each time frame.

Color-Coded Performance: Uses a color scheme to highlight performance levels, with specific colors for positive and negative changes to easily visualize performance trends.

Benchmark and Asset Comparison: Displays performance metrics for both a benchmark (e.g., SPY) and the asset currently viewed on the chart, providing a clear comparison.

Inputs:

Benchmark Symbol: Specify the symbol of the benchmark asset (e.g., SPY).

Benchmark Description: Provide a description for the benchmark asset.

Chart Symbol: Automatically uses the symbol of the chart for comparison.

Usage:

Add the script to your TradingView chart.

Configure the benchmark symbol and description as needed.

The table will automatically populate with performance data and be positioned according to your selection.

Disclaimer:

This script is for informational and educational purposes only and is not intended as financial advice. The performance data displayed in the table is based on historical prices and is not indicative of future performance. Trading involves risk, and you should always do your own research and consult with a qualified financial advisor before making any investment decisions. The creator of this script assumes no responsibility for any losses or damages incurred as a result of using this tool.

Relative Strength according to Oster (RSO)Overview:

Relative Strength according to Oster (RSO) is an innovative tool that redefines how traders assess an asset's market strength. Moving beyond traditional indicators, RSO offers a sophisticated and highly responsive measure of an asset's potential to continue performing well. By integrating groundbreaking methodologies, RSO equips traders with unparalleled insights into market dynamics, making it an essential tool for anyone looking to stay ahead in today's fast-paced trading environment.

Understanding RSL (Relative Strength according to Levy):

At its core, Relative Strength according to Levy (RSL) is a powerful concept rooted in the idea that an asset currently exhibiting strength is more likely to maintain or even enhance that strength in the future. RSL calculates this by comparing an asset's current price to its moving average, providing a clear picture of its relative performance over time. The further its value is above 1, the higher the market momentum and vice versa. This relationship to the moving average is crucial, as it indicates not just where the asset stands today but also its trajectory in the context of historical performance. The ability to identify assets that consistently outperform is a game-changer for traders, and RSL has long been a cornerstone in this pursuit.

RSO vs. Traditional RSL: A Leap Forward

The RSO takes the traditional RSL concept and propels it into new territory with its innovative correlation-based approach. This is where RSO truly shines, offering a unique and sophisticated analysis that goes far beyond the basics.

Why RSO is Revolutionary:

Correlation Adjustment: The RSO doesn’t just measure an asset’s strength in isolation. Instead, it adjusts its readings based on how closely the asset's price movements correlate with a chosen benchmark. This groundbreaking feature ensures that the RSO is not just reactive to past performance but also predictive of how the asset might behave relative to the broader market, adding a layer of precision that is unparalleled in traditional strength indicators.

Superior Strength Option: With the RSO, traders have the option to include superior strength factors, adding another dimension of insight. This feature allows for more stable and reliable long-term signals. On the flip side, those who prefer a more dynamic trading style can opt to exclude this factor for more frequent, shorter-term signals. This level of customization is rare and sets the RSO apart as a truly adaptable tool.

Enhanced Market Insights: RSO’s correlation-based approach doesn’t just show how strong an asset is—it reveals how that strength is likely to develop in relation to the benchmark's underlying trends. This isn’t merely about comparing performance; it’s about understanding the asset’s potential trajectory in a much broader market context. Such insight is invaluable for making informed, strategic trading decisions.

Practical Application:

The RSO isn’t just innovative in theory; it’s designed for practical, real-world trading. Traders can set customized alerts based on RSO’s readings, ensuring they’re always aware of key buy or sell signals as they occur. The flexibility to include or exclude superior strength factors means that RSO can be tailored to fit any trading style, whether focused on long-term investments or short-term opportunities.

Conclusion:

In conclusion, the Relative Strength according to Oster (RSO) is more than just an indicator; it’s a breakthrough in market analysis. By integrating correlation adjustments and offering unparalleled customization options, RSO provides traders with insights that are both deeper and more actionable than ever before. This innovative tool is designed to empower traders, giving them the edge they need to succeed in an increasingly complex market landscape. Whether you’re a seasoned trader or just starting out, the RSO is a must-have tool for navigating market trends with confidence and precision.

Normalized Performance ComparisonThis script visualizes the relative performance of a primary asset against a benchmark composed of three reference assets. Here's how it works:

User Inputs:

- Users specify ticker symbols for three reference assets (default: Platinum, Palladium, Rhodium).

Data Retrieval:

- Fetches closing prices for the primary asset (the one the script is applied to) and the three reference assets.

Normalization:

- Each asset's price is normalized by dividing its current price by its initial price at the start of the chart. This allows for performance comparison on a common scale.

Benchmark Creation:

- The normalized prices of the three reference assets are combined to create a composite benchmark.

Ratio Calculation:

- Computes the ratio of the normalized primary asset price to the combined normalized benchmark price, highlighting relative performance.

Plotting:

- Plots this ratio as a blue line on the chart, showing the primary asset's performance relative to the benchmark over time.

This script helps users quickly assess how well the primary asset is performing compared to a set of reference assets.

Pivots Benchmark For Indicators (MA / OSC) This measures the pivot of your source. the peaks and valleys. and, shows ou some neat statistics if you were to use those as your entry/exit points. I consider it a purist MA designers Acid Test. if you can get good numbers on this, (remember to deduct fees), you probably should feel confident in your indicator's quality. it isn't very forgiving.

170 themes Dark/Light

your choice of highlight colour for Best/Worst achievement values.

compare to open/close average, or a 3 length EMA on close.

display solo bench of your source.

help popup for indicator values, (hideable)

show/hide individual pivot distances, which source to measure as pivot

time to measure historical setting

number of pivots to keep in buffer

it does back test and runs live!

Closed Source for now, as it is a demo version i've made with partial capabilities.

it's part of a set of performance benchmarks i hope to have finished soon.

when i release the major components i've been building up to for 2 years,

this and everything else will be open sourced.

SFC Smart Money BenchmarkA benchmark is a standard or point of reference, which traders can use to measure something else.

This indicator is showing how correlated pairs are performing and what is the current correlation between them.

Features:

- Market performance - daily, weekly, monthly

- Sigma - volatility . It will be coloured in red, if the volatility is bigger than one standard deviation.

-Correlation - Positive correlation will be coloured in green if it is confirmed by the P-value, negative correlation in red.

-Confidence intervals

-Determination

Markets:

- Metal sector

- US Stock Indices

- Major USD Pairs

Market performance

The indicator is plotting a table with the current performance of the particular group, for example the metal sector and all correlated Gold pairs. The table is showing the performance of the pairs based on monthly, weekly and daily bases in the same time. In this case the trader can track all pairs simultaneously and see if there are anomalies between the pairs - SMT Divergence.

For example:

We know that Gold and Silver are very strong correlated pairs. In this case if Gold is going up, but Silver not, probably this move is only current manipulation and the true move is not clear. In that moment the trader can decide not to open an order or take some profit.

With the Sigma value traders also can track the current volatility of the price. The strength of the volatility is measured by the standard deviation.

-1>Sigma<1 - The asset is moving normally

-2>Sigma<-1 or 21 - The asset is volatile

-3>Sigma<-2 or 32 - The asset is very volatile

Correlation

The indicator is showing the current correlation between all pair from the table. The correlation is set to the first pair of the table. In order to make the correlation more accurate the indicator calculates the P-value and the Determination coefficient. The confidence intervals are also displayed in order to show how strong correlation should be expected.

Pearson correlation is a measure of linear correlation between two sets of data. It is the ratio between the covariance of two variables and the product of their standard deviations; thus, it is essentially a normalized measurement of the covariance, such that the result always has a value between −1 and 1. As with covariance itself, the measure can only reflect a linear correlation of variables, and ignores many other types of relationships or correlations.

P-value evaluates how well your data rejects the null hypothesis, which states that there is no relationship between two compared groups. Successfully rejecting this hypothesis tells you that your results may be statistically significant. In academic research, p-value is defined as the probability of obtaining results ‘as extreme’ or ‘more extreme’, given that the null hypothesis is true — essentially, how likely it is that you would receive the results (or more dramatic results) you did assuming that there is no correlation or relationship (e.g. the thing that you’re testing) among the subjects

Coefficient of Determination is just the square of pearson’s correlation coefficient R. This is done as it is easier to explain linear regression in terms of R² than R. As R ranges from -1 to 1, R² would range from 0 to 1 — clearly explaining relationship with 0 being not related and 1 being perfectly related.

The correlation confidence interval is the range in which the population correlation is most likely to be found.

The degree of certainty for which it is likely to be within that range is called the confidence level.

When you collect sample data, you can not know the exact value of the correlation.

Note:

For the Stock indices there is an extra calculation, showing the current market expectations - Fear and Greed Index. The calculated index could differs a bit from the original CNN Fear and Greed indicator, because they calculate the index based on Future markets. This indicator calculate the index based on the market that we trade - indices.

Supported pairs:

-Option Gold - XAUUSD , GDX , Silver , Aluminum, Platinum , Palladium, 30Y US Yields, 10Y US Yields, 2Y US Yields, XAUEUR, XAUGBP, XAUAUD , XAUCAD , XAUCNY , XAUJPY

-Option Others - Table1: SP500 , US30, NAS100 ; Table2: DXY , EURUSD , GBPUSD , AUDUSD

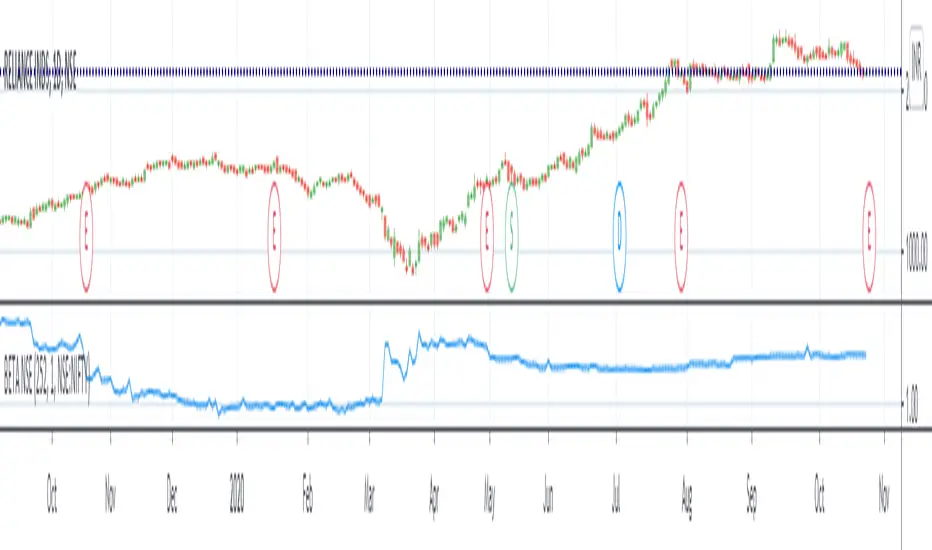

BETA (against any benchmark index - defaulted to NSE:NIFTY)Beta value of a stock relative to benchmark index. Thanks to Ricardo Santos for the original script. This script is adapted from it.

To understand beta, refer Investopedia link: www.investopedia.com

A beta value of 1 means the stock is directly correlated to benchmark index - volatility would be same as overall market.

Beta value less than 1 and greater than 0 means the stock is less volatile than the market.

Beta value more than 1 would mean the stock is more volatile than the market.

A beta value of 1.2 would roughly translate to the stock being 20% more volatile than the overall market.

A negative beta value indicates the stock is inversely correlated to market.

In the example chart, you can see the Beta value change in NSE:RELIANCE with respect to NSE:NIFTY.

Godmode 4.0.2 [Supply/Demand]First off, a huge thank you to the following people:

LEGION:

LazyBear: www.tradingview.com

xSilas: www.tradingview.com

Ni6HTH4awK: www.tradingview.com

sco77m4r7and:

SNOW_CITY: www.tradingview.com

oh92: www.tradingview.com

alexgrover: www.tradingview.com

cI8DH: www.tradingview.com

DonovanWall: www.tradingview.com

shtcoinr: www.tradingview.com

This is the third iteration of Godmode. This time I borrowed the method used by shtcoinr to render supply/demand, resistance and support zones. The idea here is to input the appropriate benchmark tickerid to the asset class you're trading and to paint zones according to the price activity of the selected tickerid. This works very well trying to paint meaningful zones against noisy stocks, currencies, commodities etc. Use a correlation coefficient to determine the best benchmark for your asset class.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Godmode 4.0.1 [Correlator]First off, a huge thank you to the following people:

@LEGION:

@LazyBear: www.tradingview.com

@xSilas: www.tradingview.com

@Ni6HTH4awK: www.tradingview.com

@sco77m4r7and:

@SNOW_CITY: www.tradingview.com

@oh92: www.tradingview.com

@alexgrover: www.tradingview.com

@cI8DH: www.tradingview.com

@DonovanWall: www.tradingview.com

This is my second iteration of Godmode. This time I allowed the possibility to correlate two benchmarks against one another, thereby giving you twice the signals (once there's a strong correlation between the two, inverse or otherwise). That aside, there are no changes to this indicator that the first iteration doesn't have:

There are still more iterations planned, but if you guys have any ideas or wishes regarding what direction I go, then please let me know.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources as well as any other scripts I publish.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Godmode 4.0.0 [Oscillator]First off, a huge thank you to the following people:

LEGION:

LazyBear: www.tradingview.com

xSilas: www.tradingview.com

Ni6HTH4awK: www.tradingview.com

sco77m4r7and:

SNOW_CITY: www.tradingview.com

oh92: www.tradingview.com

alexgrover: www.tradingview.com

cI8DH: www.tradingview.com

DonovanWall: www.tradingview.com

Since I've been on TradingView I've become somewhat enthralled by Godmode and the collective work that goes in to it, so I decided to publish my own iteration, building off the ideas already present. (This is a great way to get familiar with Pine by the way, just in case there are any beginners reading this)

Changes

The first change I made was to allow the user to select whatever tickerid they wanted as a benchmark. If trading XBTUSD on BitMEX for example, the indicator will react to exchange-specific activity, which means it will respond to all the little whipsaws, whipsaws that can be especially present on a futures exchange. By typing CRYPTOCAP:BTC or CRYPTOCAP:TOTAL we endeavor to remove noise. It can also signal earlier. Less noise and less lag. Another idea would be to choose a benchmark that has a strong inverse relationship with the asset you're trading: try CRYPTOCAP:USDT as the benchmark against BTC to see what I mean.

I also added the ability to smooth the plot, yet again removing noise but adding considerable lag.

The linear regression of the wave-trend is calculated in place of the EMA. This is plotted as columns with the midline (50) as the base. This is just calculating the slope of the wave-trend and can signal a weakening trend before a reversal takes place.

Using cI8DH's True RSI script () as inspiration, I added a function for calculating the True TSI in an attempt to remove any bullish bias. Funnily enough, when I tried to do the same with the RSI I had some problems. I'll try to resolve this in the coming weeks.

Made slight changes to the aesthetics. Tried to bring the two main plots alive by making their bold, opaque colors stand off the subtle tones in the background.

To Do List

1. I would like to sort out the issue with the True RSI.

2. When the plots are smoothed, there's an issue with the green 'Caution!' dots appearing in the lower half of the indicator.

3. I'd like to adjust the code so that if the 'Benchmark' box is empty, that it will automatically register the current tickerid as the 'Benchmark'.

If anyone has any suggestions on other fixes or how to apply the fixes mentioned by me, please don't hesitate to reach out to me here or through other media platforms.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

BITMEX:XBTUSD

CRYPTOCAP:BTC

CRYPTOCAP:TOTAL

CRYPTOCAP:USDT.D

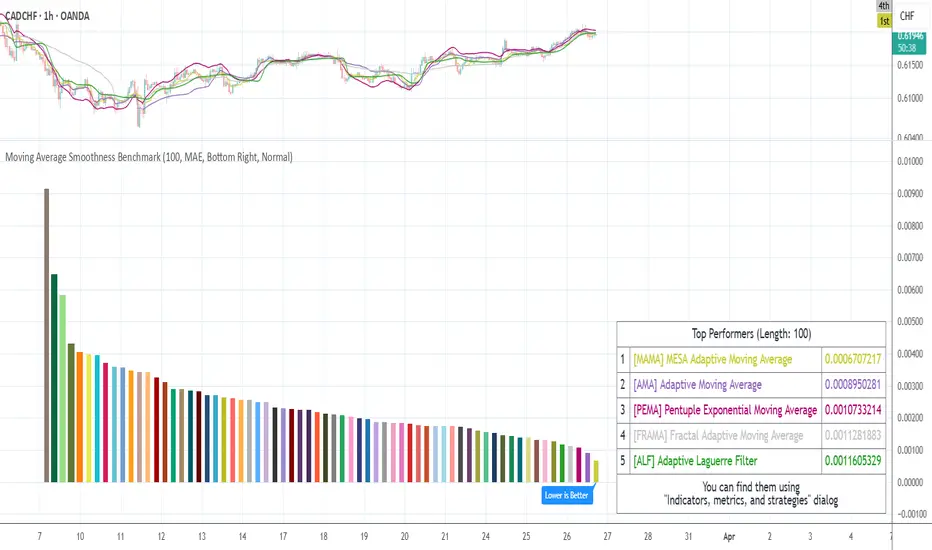

Moving Average Smoothness BenchmarkHey there!

This tool will help you to choose a moving average/filter that has the lowest lag throughout the whole history for the specified period.

What does it do?

It calculates the mean absolute errors for each moving average or filter and shows histogram with results. The lower error the lower lag of the moving average.

So, the best average will be at the end of the list of labels on the chart.

Settings

The main setting is a period for all moving averages.

Additionally, it allows to customize some multi-parametric moving average such as JMA, ALMA, McGinley Dynamic, Tillson's T3, REMA, Adaptive Laguerre Filter, Hampel Filter, Recursive Median Filter and Middle-High-Low MA.

NOTE : The results may vary on the different tickers and timeframes. This tool measures the performances on the current ticker and on the current timeframe.

Supported averages/filters (use short titles to match movings on the chart)

SMA, Simple MA

EMA, Exponential MA

WMA, Weighted (Linear) MA

RMA, Running MA (by J. Welles Wilder)

VWMA, Volume Weighted MA (by Buff P. Dormeier)

AHMA, Ahrens MA (by Richard D. Ahrens)

ALMA, Arnaud Legoux MA (by Arnaud Legoux and Dimitris Kouzis-Loukas)

ALF, Adaptive Laguerre Filter (by John F. Ehlers)

ARSI, Adaptive RSI

DEMA, Double Exponential MA (by Patrick G. Mulloy)

EDCF, Ehlers Distance Coefficient Filter (by John F. Ehlers)

EVWMA, Elastic Volume Weighted MA (by Christian P. Fries)

FRAMA, Fractal Adaptive MA (by John F. Ehlers)

HFSMA, Hampel Filter on Simple Moving Average

HFEMA, Hampel Filter on Exponential Moving Average

HMA, Hull MA (by Alan Hull)

HWMA, Henderson Weighted MA (by Robert Henderson)

IIRF, Infinite Impulse Response Filter (by John F. Ehlers)

JMA1, Jurik MA with power of 1 (by Mark Jurik)

JMA2, Jurik MA with power of 2 (by Mark Jurik)

JMA3, Jurik MA with power of 3 (by Mark Jurik)

JMA4, Jurik MA with power of 4 (by Mark Jurik)

LF, Laguerre Filter (by John F. Ehlers)

LMA, Leo MA (by ProRealCode' user Leo)

LSMA, Least Squares MA (Moving Linear Regression)

MD, McGinley Dynamic (by John R. McGinley)

MHLMA, Middle-High-Low MA (by Vitali Apirine)

REMA, Regularized Exponential MA (by Chris Satchwell)

RMF, Recursive Median Filter (by John F. Ehlers)

RMTA, Recursive Moving Trend Average (by Dennis Meyers)

SHMMA, Sharp Modified MA (by Joe Sharp)

SWMA, Sine Weighted MA

TEMA, Triple Exponential MA (by Patrick G. Mulloy)

TMA, Triangular MA

T3, (by Tim Tillson)

VIDYA, Variable Index Dynamic Average (by Tushar S. Chande)

ZLEMA, Zero Lag Exponential MA (by John F. Ehlers and Ric Way)

BF2, Butterworth Filter with 2 poles

BF3, Butterworth Filter with 3 poles

SSF2, Super Smoother Filter with 2 poles (by John F. Ehlers)

SSF3, Super Smoother Filter with 3 poles (by John F. Ehlers)

GF1, Gaussian Filter with 1 pole

GF2, Gaussian Filter with 2 poles

GF3, Gaussian Filter with 3 poles

GF4, Gaussian Filter with 4 poles

Good luck and Merry Christmas!