Dynamic Trend Fusion (DTF)The "Dynamic Trend Fusion" (DTF) indicator is a powerful technical analysis tool for traders. It stands out from other indicators due to its adaptability and ability to provide insights into different trading styles. Users can choose from various trading options such as "Short-term Trading," "Long-term Trading," "Aggressive Short-term," "Conservative Long-term," "Balanced Approach," "High Sensitivity," "Low Sensitivity," "Day Trading," and "Swing Trading." These options allow traders to customize the indicator to suit their specific trading strategies.

DTF combines the Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) indicators, normalizing them to a similar scale for a comprehensive view of market conditions. It then calculates a combined value and smoothes it using a moving average.

One of its standout features is the ability to identify bullish and bearish states, which is represented visually on the chart. When the indicator detects a transition from a bullish to a bearish state or vice versa, the color of the line changes.

Additionally, DTF offers alert conditions, notifying users when the market shifts into a bullish or bearish state, allowing for timely decision-making.

In summary, the DTF indicator sets itself apart by providing traders with a versatile tool that can be tailored to various trading styles and offers clear visual signals for trend changes, enhancing trading precision and efficiency.

Centered Oscillators

Multi-data oscillatorThe multi-data oscillator is a tool created to help traders visualize clearly how an oscillator works and moves considering different input parameters.

In this tool, you can choose to visualize the script as the RSI, the CCI, the LOC indicator, a custom-created formula that simply shows the location of the data considering X past values, or the average of all of these three indicators.

In the settings, you can choose both the length of the indicator and the smoothing factor.

Additionally, the indicator has a gradient color that changes considering the deviation and the variance of the different lines used to calculate the average line, displayed with more thickness.

[KVA]nRSIThe nRSI stands as a groundbreaking enhancement of the traditional Relative Strength Index (RSI), specifically engineered for traders seeking a more refined and accurate tool in fast-moving markets.

Customizable Price Change Period (n): Unlike the traditional RSI which solely relies on a fixed period for average gains and losses, the nRSI introduces an additional parameter, n, to calculate price changes.

This adaptation focuses on minimizing market noise, sharpening the indicator's sensitivity to genuine trends and patterns.

Enhanced Signal Precision : By reducing the influence of short-term price spikes and fluctuations, the nRSI delivers a more precise signal. This precision is particularly crucial in volatile market conditions, where traditional indicators may be swayed by transient movements.

Ideal Usage

Strategic Trading Decisions : Ideal for traders who need to filter out insignificant price movements to make more strategic, informed trading decisions.

Reliable Divergence Spotting : Enhanced noise reduction aids in identifying more reliable divergences, key for predicting potential market reversals.

Trend Confirmation : The smoothed RSI, assisted by the moving average, becomes an invaluable tool for confirming the validity of market trends, minimizing false signals.

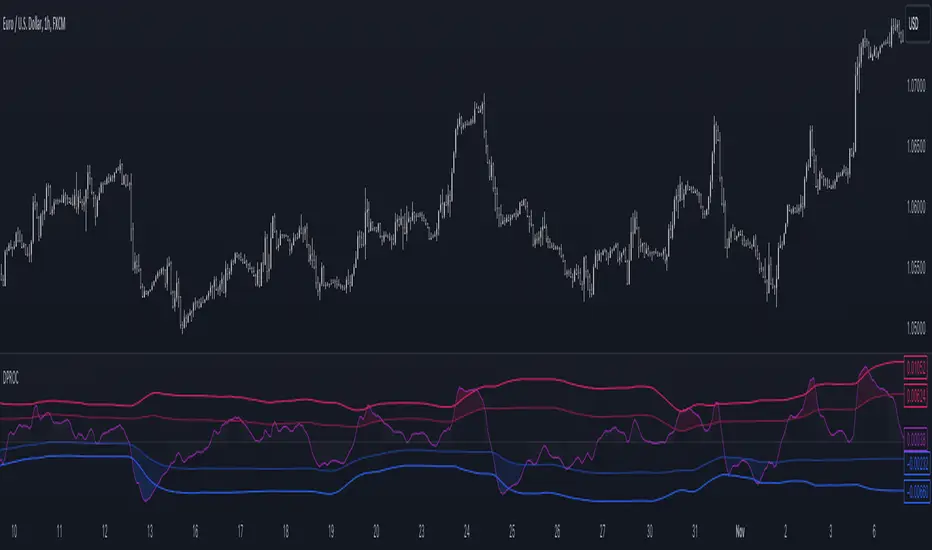

Detrended Price Rate of ChangeThe Detrended Price Rate of Change is an oscillator developed to help traders identify potential conditions of overbought and oversold markets.

The formula of the oscillator includes both the Detrended price formula, useful to spot divergences, and the Rate of change simplified formula, which helps in identifying overextended markets and gives useful information on price momentum.

Enhanced McClellan Summation Index

The Enhanced McClellan Summation Index (MSI) is a comprehensive tool that transforms the MSI indicator with Heikin-Ashi visualization, offering improved trend analysis and momentum insights. This indicator includes MACD and it's histogram calculations to refine trend signals, minimize false positives and offer additional momentum analysis.

Methodology:

McClellan Summation Index (MSI) -

The MSI begins by calculating the ratio between advancing and declining issues in the specified index.

float decl = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘥𝘦𝘤𝘭𝘪𝘯𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float adv = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘢𝘥𝘷𝘢𝘯𝘤𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float ratio = (adv - decl) / (adv + decl)

It then computes a cumulative sum of the MACD (the difference between a 19-period EMA and a 39-period EMA) of this ratio. The result is a smoothed indicator reflecting market breadth and momentum.

macd(float r) =>

ta.ema(r, 19) - ta.ema(r, 39)

float msi = ta.cum(macd(ratio))

Heikin-Ashi Transformation -

Heikin-Ashi is a technique that uses a modified candlestick formula to create a smoother representation of price action. It averages the open, close, high, and low prices of the current and previous periods. This transformation reduces noise and provides a clearer view of trends.

type bar

float o = open

float h = high

float l = low

float c = close

bar b = bar.new()

float ha_close = math.avg(b.o, b.h, b.l, b.c)

MACD and Histogram -

The Enhanced MSI incorporates MACD and histogram calculations to provide additional momentum analysis and refine trend signals. The MACD represents the difference between the 12-period EMA and the 26-period EMA of the MSI. The histogram is the visual representation of the difference between the MACD and its signal line.

Options:

Index Selection - Choose from TVC:NYA , NASDAQ:NDX , or TVC:XAX to tailor the MSI-HA to the desired market index.

MACD Settings - Adjust the parameters for the MACD calculation to fine-tune the indicator's responsiveness.

Ratio Multiplier - Apply scaling to the MSI to suit different market conditions and indices.

Benefits of Heikin-Ashi -

Smoothed Trends - Heikin-Ashi reduces market noise, providing a more apparent and smoothed representation of trends.

Clearer Patterns - Candlestick patterns are more distinct, aiding in the identification of trend reversals and continuations.

Utility and Use Cases:

Trend & Momentum Analysis - Utilize the tool's Heikin-Ashi visualization for clearer trend identification in confluence with it's MACD and histogram to gain additional insights into the strength and direction of trends, while filtering out potential false positives.

Breadth Analysis - Explore market breadth through the MSI's cumulative breadth indicator, gauging the overall health and strength of the underlying market.

- Alerts Setup Guide -

The Enhanced MSI is a robust indicator that combines the breadth analysis of the McClellan Summation Index with the clarity of Heikin-Ashi visualization and additional momentum insights from MACD and histogram calculations. Its customization options make it adaptable to various indices and market conditions, offering traders a comprehensive tool for trend and momentum analysis.

MACD Pulse CheckThis custom script, titled " MACD Pulse Check ," is a modified and enhanced version of the traditional Moving Average Convergence Divergence (MACD) indicator, commonly used in trading for trend-following and momentum strategies. Here's a breakdown of its features and benefits over the traditional MACD:

Multiple MACD Lines with Different Parameters:

The script calculates six different MACD lines using various combinations of fast, slow, and signal lengths. This diverse range allows for a more comprehensive analysis of the market momentum and trend across different time scales and sensitivities.

Average of MACD Lines:

By averaging these six MACD lines, the script creates a more smoothed and potentially less noisy signal. This can help in reducing false signals and improving the reliability of trend indications.

Sideways Market Detection:

A unique feature of this script is its ability to identify sideways or range-bound markets using a user-defined threshold. This is calculated by comparing the current price to the price five candles ago and seeing if the change is within a certain percentage threshold. Identifying sideways markets is crucial as trend-following strategies like MACD typically perform poorly in these conditions.

Visual and Color-Coded Signals:

The script plots shapes (circles) on the chart, where the color (green for bullish, red for bearish, sideways price action will display as either a dull green or a dull red) quickly indicates the market condition. This visual representation makes it easier to interpret the signals at a glance, and spot sideways price action while still having a general idea of trend.

Benefits for Traders:

Versatility: By averaging multiple MACD lines, traders get a more nuanced view of the market momentum, potentially leading to more informed trading decisions.

Reduced False Signals:

The averaging process and sideways market detection can help in filtering out false or weak signals, which is a common issue with the traditional MACD.

Ease of Use:

The color-coded visual signals simplify the process of identifying market trends and conditions, making the tool accessible even for less experienced traders.

In summary, "MACD Pulse Check" enhances the traditional MACD by providing a more comprehensive, and visually intuitive tool, potentially leading to better trading decisions in varying market conditions. However, it's important to note that no indicator is foolproof and should always be used in conjunction with other analysis methods and sound risk management practices.

MACD_RSI_trend_followingINFO:

This indicator can be used to build-up a strategy for trading of assets which are currently in trending phase.

My preference is to use it on slowly moving assets like GOLD and on higher timeframes, but practice may show that we find more usefull cases.

This script uses two indicators - MACD and RSI, as the timeframe that those are extracted for is configurable (defaults with the Chart TF, but can be any other selected by the user).

The strategy has the following simple idea - buy if any if the conditions below is true:

The selected TF MACD line crosses above the signal line and the TF RSI is above the user selected trigger value

The selected TF MACD line is above the signal line and the TF RSI crosses above the user selected trigger value

Once we're in position we wait for the selected TF MACD line to cross below the signal line, and then we set a SL at the low of that bar

DETAILS and USAGE:

In the current implementation I find two possible use cases for the indicator:

as a stand-alone indicator on the chart which can also fire alerts that can help to determine if we want to manually enter/exit trades based on them

can be used to connect to the Signal input of the TTS (TempalteTradingStrategy) by jason5480 in order to backtest it, thus effectively turning it into a strategy (instructions below in TTS CONNECTIVITY section)

In the example below we see a position opened at the bar after the buy indicator from the script has been triggered, and then later after the SL indicator from the script has been triggered a SL has been set on the lower wick of the closing candle, and the position eventually got closed once the price hit that level. Note that most of the drawing on the example snapshot below are from the TTS indicator following the buy/sell/SL conditions themseves:

Trading period can be selected from the indicator itself to limit to more interesting periods.

Arrow indications are drawn on the chart to indicate the trading conditions met in the script - green arrow for a buy signal indication and orange for LTF crossunder to indicate setting of SL.

SETTINGS:

Leaving all of the settings as in vanilla use case, as both the MACD and RSI indicator's settings follow the default ones for the stand-alone indicators themselves.

The start-end date is a time filter that can be extermely usefull when backtesting different time periods.

Pesonal preference is using the script on a D/W timeframe, while the indicator is configured to use Monthly chart.

The default value of the RSI filter is left to 50, which can be changed. I.e. if the RSI is above 50 we have a regime filter based on the MACD criteria.

EXTERNAL LIBRARIES:

The script uses a couple of external libraries:

HeWhoMustNotBeNamed/enhanced_ta/14 - collection of TA indicators

jason5480/tts_convention/3 - more details about the Template Trading Strategy below

I would like to highly appreciate and credit the work of both HeWhoMustNotBeNamed and jason5480 for providing them to the community.

TTS SETTINGS (NEEDED IF USED TO BACKTEST WITH TTS):

The TempalteTradingStrategy is a strategy script developed in Pine by jason5480, which I recommend for quick turn-around of testing different ideas on a proven and tested framework

I cannot give enough credit to the developer for the efforts put in building of the infrastructure, so I advice everyone that wants to use it first to get familiar with the concept and by checking

by checking jason5480's profile www.tradingview.com

The TTS itself is extremely functional and have a lot of properties, so its functionality is beyond the scope of the current script -

Again, I strongly recommend to be thoroughly epxlored by everyone that plans on using it.

In the nutshell it is a script that can be feed with buy/sell signals from an external indicator script and based on many configuration options it can determine how to execute the trades.

The TTS has many settings that can be applied, so below I will cover only the ones that differ from the default ones, at least according to my testing - do your own research, you may find something even better :)

The current/latest version that I've been using as of writing and testing this script is TTSv48

Settings which differ from the default ones:

from - False (time filter is from the indicator script itself)

Deal Conditions Mode - External (take enter/exit conditions from an external script)

🔌Signal 🛈➡ - MACD_RSI_trend_following: 🔌Signal to TTSv48 (this is the output from the indicator script, according to the TTS convention)

Sat/Sun - true (for crypto, in order to trade 24/7)

Order Type - STOP (perform stop order)

Distance Method - HHLL (HigherHighLowerLow - in order to set the SL according to the strategy definition from above)

The next are just personal preferenes, you can feel free to experiment according to your trading style

Take Profit Targets - 0 (either 100% in or out, no incremental stepping in or out of positions)

Dist Mul|Len Long/Short- 10 (make sure that we don't close on profitable trades by any reason)

Quantity Method - EQUITY (personal backtesting preference is to consider each backtest as a separate portfolio, so determine the position size by 100% of the allocated equity size)

Equity % - 100 (note above)

Dual_MACD_trendingINFO:

This indicator is useful for trending assets, as my preference is for low-frequency trading, thus using BTCUSD on 1D/1W chart

In the current implementation I find two possible use cases for the indicator:

- as a stand-alone indicator on the chart which can also fire alerts that can help to determine if we want to manually enter/exit trades based on the signals from it (1D/1W is good for non-automated trading)

- can be used to connect to the Signal input of the TTS (TempalteTradingStrategy) by jason5480 in order to backtest it, thus effectively turning it into a strategy (instructions below in TTS CONNECTIVITY section)

Trading period can be selected from the indicator itself to limit to more interesting periods.

Arrow indications are drawn on the chart to indicate the trading conditions met in the script - light green for HTF crossover, dark green for LTF crossover and orange for LTF crossunder.

Note that the indicator performs best in trending assets and markets, and it is advisable to use additional indicators to filter the trading conditions when market/asset is expected to move sideways.

DETAILS:

It uses a couple of MACD indicators - one from the current timeframe and one from a higher timeframe, as the crossover/crossunder cases of the MACD line and the signal line indicate the potential entry/exit points.

The strategy has the following flow:

- If the weekly MACD is positive (MACD line is over the signal line) we have a trading window.

- If we have a trading window, we buy when the daily macd line crosses AND closes above the signal line.

- If we are in a position, we await the daily MACD to cross AND close under the signal line, and only then place a stop loss under the wick of that closing candle.

The user can select both the higher (HTF) and lower (LTF) timeframes. Preferably the lower timeframe should be the one that the Chart is on for better visualization.

If one to decide to use the indicator as a strategy, it implements the following buy and sell criterias, which are feed to the TTS, but can be also manually managed via adding alerts from this indicator.

Since usually the LTF is preceeding the crossover compared to the HTF, then my interpretation of the strategy and flow that it follows is allowing two different ways to enter a trade:

- crossover (and bar close) of the macd over the signal line in the HIGH TIMEFRAME (no need to look at the LOWER TIMEFRMAE)

- crossover (and bar close) of the macd over the signal line in the LOW TIMEFRAME, as in this case we need to check also that the macd line is over the signal line for the HIGH TIMEFRAME as well (like a regime filter)

The exit of the trade is based on the lower timeframe MACD only, as we create a stop loss equal to the lower wick of the bar, once the macd line crosses below the signal line on that timeframe

SETTINGS:

All of the indicator's settings are for the vanilla/general case.

User can set all of the MACD parameters for both the higher and lower (current) timeframes, currently left to default of the MACD stand-alone indicator itself.

The start-end date is a time filter that can be extermely usefull when backtesting different time periods.

TTS SETTINGS (NEEDED IF USED TO BACKTEST WITH TTS)

The TempalteTradingStrategy is a strategy script developed in Pine by jason5480, which I recommend for quick turn-around of testing different ideas on a proven and tested framework

I cannot give enough credit to the developer for the efforts put in building of the infrastructure, so I advice everyone that wants to use it first to get familiar with the concept and by checking

by checking jason5480's profile www.tradingview.com

The TTS itself is extremely functional and have a lot of properties, so its functionality is beyond the scope of the current script -

Again, I strongly recommend to be thoroughly epxlored by everyone that plans on using it.

In the nutshell it is a script that can be feed with buy/sell signals from an external indicator script and based on many configuration options it can determine how to execute the trades.

The TTS has many settings that can be applied, so below I will cover only the ones that differ from the default ones, at least according to my testing - do your own research, you may find something even better :)

The current/latest version that I've been using as of writing and testing this script is TTSv48

Settings which differ from the default ones:

- from - False (time filter is from the indicator script itself)

- Deal Conditions Mode - External (take enter/exit conditions from an external script)

- 🔌Signal 🛈➡ - Dual_MACD: 🔌Signal to TTSv48 (this is the output from the indicator script, according to the TTS convention)

- Sat/Sun - true (for crypto, in order to trade 24/7)

- Order Type - STOP (perform stop order)

- Distance Method - HHLL (HigherHighLowerLow - in order to set the SL according to the strategy definition from above)

The next are just personal preferenes, you can feel free to experiment according to your trading style

- Take Profit Targets - 0 (either 100% in or out, no incremental stepping in or out of positions)

- Dist Mul|Len Long/Short- 10 (make sure that we don't close on profitable trades by any reason)

- Quantity Method - EQUITY (personal backtesting preference is to consider each backtest as a separate portfolio, so determine the position size by 100% of the allocated equity size)

- Equity % - 100 (note above)

EXAMPLES:

If used as a stand-alone indicator, the green arrows on the bottom will represent:

- light green - MACD line crossover signal line in the HTF

- darker green - MACD line crossover signal line in the LTF

- orange - MACD line crossunder signal line in the LTF

I recommend enabling the alerts from the script to cover those cases.

If used as an input to the TTS, we'll get more decorations on the chart from the TTS itself.

In the example below we open a trade on the next day of LTF crossover, then a few days later a crossunder in the LTF occurs, so we set a SL at the low of the wick of this day. Few days later the price doesn't recover and hits that SL, so the position is closed.

EUR/USD 45 MIN Strategy - FinexBOTThis strategy uses three indicators:

RSI (Relative Strength Index) - It indicates if a stock is potentially overbought or oversold.

CCI (Commodity Channel Index) - It measures the current price level relative to an average price level over a certain period of time.

Williams %R - It is a momentum indicator that shows whether a stock is at the high or low end of its trading range.

Long (Buy) Trades Open:

When all three indicators suggest that the stock is oversold (RSI is below 25, CCI is below -130, and Williams %R is below -85), the strategy will open a buy position, assuming there is no current open trade.

Short (Sell) Trades Open:

When all three indicators suggest the stock is overbought (RSI is above 75, CCI is above 130, and Williams %R is above -15), the strategy will open a sell position, assuming there is no current open trade.

SL (Stop Loss) and TP (Take Profit):

SL (Stop Loss) is 0.45%.

TP (Take Profit) is 1.2%.

The strategy automatically sets these exit points as a percentage of the entry price for both long and short positions to manage risks and secure profits. You can easily adopt these inputs according to your strategy. However, default settings are recommended.

K`s Extreme DurationExtreme duration uses a special combination of the RSI and its relative position to deliver a reversal signal.

The following are the conditions to generate signals:

* Bullish signal: The current 8-period RSI is below 50 and above 35 while the previous 5 RSI's are below 35.

* Bearish signal: The current 8-period RSI is above 50 and below 65 while the previous 5 RSI's are above 65.

MACD_base_and_reference_TF//====================================================================================================================

The "MACD_with_reference" indicator aims to illustrate the MACD (Moving Average Convergence Divergence) on two distinct timeframes: the base timeframe (typically the chart's timeframe, e.g., 1D) and the reference timeframe (defaulted to 1W). This tool provides a means to determine momentum shifts within the stock, potentially guiding traders in adjusting or trimming positions.

// ================================================== INFO ==================================================

Key Features of the Indicator:

- Dual Timeframe MACD: Displays MACD on both the primary (base) and higher (reference) timeframes - transparent.

- Momentum Analysis: indication of MACD crossdown of the signal line on the refenence TF to indicate momentum loss on the higher timeframe, guiding decisions to manage positions.

- MACD Line Status: Beneath the chart, a red/green bar line signifies the MACD line's position relative to the signal line on the higher timeframe.

- Alert Creation: Allows for alerts on the MACD and signal line crossdown on the higher timeframe, aiding in planning stop-loss settings for owned stocks.

// ================================================== NOTES ==================================================

The "MACD_with_reference" indicator finds optimal usage in several scenarios:

- Chart Analysis: Replacing the MACD indicator during chart reviews.

- Alert Setup: Setting alerts for owned stocks to plan ahead for stop-loss placements or position closures.

// ================================================== TODO ==================================================

//#endregion ========================================================================================================

// Continue the script code...

Fisher+ [OSC]The Fisher Transform Indicator is classified as an oscillator, meaning that its value swings above and below a central point. This characteristic allows traders to identify overbought and oversold conditions, providing potential clues about market reversals. As mentioned previously, it is an oscillator so the strength of the move is displayed by how long the fisher line stays above/below zero. Indicator can be used to aid in confluence near supply/demand zones.

White Line = Fisher

Red/Blue Line = Moving Average

--Changes color whether fisher line is above/below the MA

Red/Blue Shaded Line = Moving Average

--Changes color based on a smoothing factor

Red/Blue Shaded Fill = Asset in Overbought/Oversold Conditions

Red/Blue Circles = Asset in Extreme Overbought/Oversold Conditions

Red/Blue Triangles = MACD Signals Below/Above "0"

Divergence Labels = Asset Signaling Divergence

The moving average line will turn red/blue as long as the fisher line is below/above the moving average. The shaded MA line will switch colors based on if it is moving in an up/down trend. The MA can also be used as a signal and treated similar to an oscillator. Market trending conditions will either keep the MA below/above the dashed zero line.

MACD code credited to LazyBear's MACD Leader indicator. It is used to filter out/confirm any signals such as divergences. As long as the MACD Leader line is above both the MACD line and signal lines then it'll signal with with a triangle. MACD divergences will be added at a later time.

Spot-Vol CorrelationSpot-Vol Correlation Script Guide

Purpose:

This TradingView script measures the correlation between percentage changes in the spot price (e.g., for SPY, an ETF that tracks the S&P 500 index) and the changes in volatility (e.g., as indicated by the VIX, the Volatility Index). Its primary objective is to discern whether the relationship between spot price and volatility behaves as expected ("normal" condition) or diverges from the expected pattern ("abnormal" condition).

Normal vs. Abnormal Correlation:

Normal Correlation: Historically, the VIX (or volatility) and the spot price of major indices like the S&P 500 have an inverse relationship. When the spot price of the index goes up, the VIX tends to go down, indicating lower volatility. Conversely, when the index drops, the VIX generally rises, signaling increased volatility.

Abnormal Correlation: There are instances when this inverse relationship doesn't hold, and both the spot price and the VIX move in the same direction. This is considered an "abnormal" condition and might indicate unusual market dynamics, potential uncertainty, or impending shifts in market sentiment.

Using the Script:

Inputs:

First Symbol: This is set by default to VIX, representing volatility. However, users can input any other volatility metric they prefer.

Second Symbol: This is set to SPY by default, representing the spot price of the S&P 500 index. Like the first symbol, users can substitute SPY with any other asset or index of their choice.

Length of Calculation Period: Users can define the lookback period for the correlation calculation. By default, it's set to 10 periods (e.g., days for a daily chart).

Upper & Lower Bounds of Normal Zone: These parameters define the range of correlation values that are considered "normal" or expected. By default, this is set between -0.60 and -1.00.

Visuals:

Correlation Line: The main line plot shows the correlation coefficient between the two input symbols. When this line is within the "normal zone", it indicates that the spot price and volatility are inversely correlated. If it's outside this zone, the correlation is considered "abnormal".

Green Color: Indicates a period when the spot price and VIX are behaving as traditionally expected (i.e., one rises while the other falls).

Red Color: Denotes a period when the spot price and VIX are both moving in the same direction, which is an abnormal condition.

Shaded Area (Normal Zone): The area between the user-defined upper and lower bounds is shaded in green, highlighting the range of "normal" correlation values.

Interpretation:

Monitor the color and position of the correlation line relative to the shaded area:

If the line is green and within the shaded area, the market dynamics are as traditionally expected.

If the line is red or outside the shaded area, users should exercise caution as this indicates a divergence from typical behavior, which can precede significant market moves or heightened uncertainty.

S/R and Reversal BarsToday I'm proposing an idea to form S/R with a slightly different basic idea. This is a combination of CCI and candlestick study, and we will use this to mark possible reversal candles and possible S/R lines.

This is nothing complicated, I've used a basic CCI indicator with certain rules/system to mark S/R levels on the chart. (Have loaded traditional CCI indicator on bottom for comparison)

S/R levels are market as followed

Cross -

Lime = Support

Red = Resistance

Zero/Balance line - Yellow circles

The idea is to use this indicator to trade sideways market more successfully, in trending market this can be futile if you are not waiting for the break-out or breakdowns with confirmation.

Since this is based on CCI, it will give static result only when bar is closed, till then it will be susceptible for repaint. This is inherited nature from CCI readings on current bar. I could change this to only making reading on closed bar (historical bar), but that takes away from the uniqueness of this indicator in giving early indications.

This is a great tool for intraday scalping, but it does work on all timeframes, it's not bound by granularity.

This is for education purpose only.

Past success or seemingly positive results on published posts are not indication of future success.

TASC 2023.11 VAcc█ OVERVIEW

The November 2023 edition of TASC's Traders' Tips features an article titled "VAcc: A Momentum Indicator Based On Velocity And Acceleration" by Scott Cong. This script implements the author's momentum indicator based on simple physics concepts.

█ CONCEPTS

The indicator is named VAcc as it is derived from the average velocity (V) and acceleration (Acc) over a specified lookback period. Consequently, its readings reflect two valuable characteristics of price data: rate (indicating the speed at which the price is moving) and rate of change (indicating whether the price is speeding up or slowing down).

In the article, the author reports that for longer periods, VAcc behaves similarly to the MACD , albeit with a more responsive nature. For shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator , but it trends more prominently and is less prone to overbought/oversold saturation.

To incorporate VAcc into trading strategies, the author suggests considering the following two permutations for the velocity and acceleration data series:

Strong upward condition: Velocity is rising, and acceleration is rising above zero.

Strong downward condition: Velocity is falling, and acceleration is falling.

In the current implementation, the chart displays the average velocity as a line, while the average acceleration is presented as a histogram.

█ CALCULATIONS

The calculation of VAcc involves the following steps:

For the current closing price, C , and for each bar C (i) within a specified lookback period from the current bar, the script calculates velocities, V (i) = ( C - C (i))/i. These velocities are then subjected to an exponential moving average to obtain the smoothed average velocity.

Similarly, for each bar within the lookback period, accelerations are calculated as Acc (i) = ( V - V (i))/i and then averaged without smoothing.

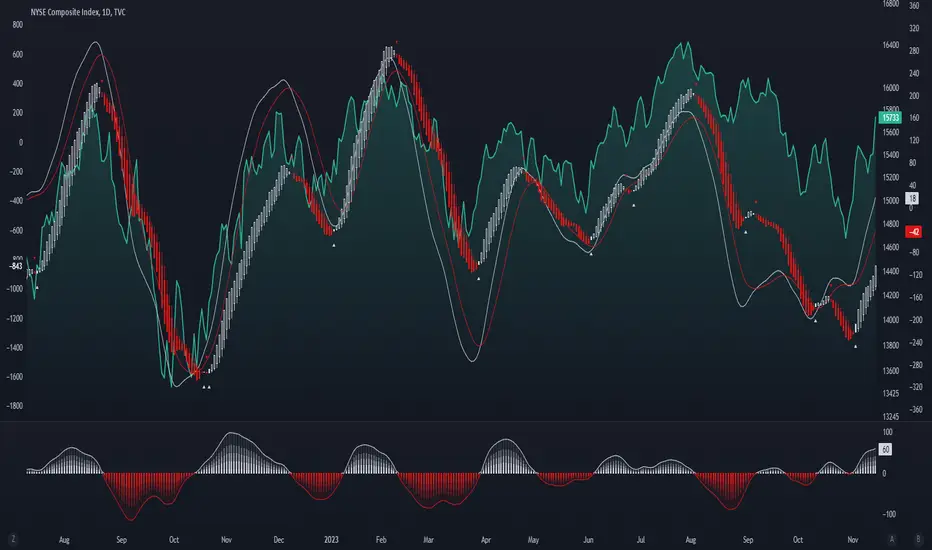

VAcc (Velocity & Acceleration)VAcc (Velocity & Acceleration) is a momentum indicator published by Scott Cong in Stocks & Commodities V. 41:09 (8–15). It applies concepts from physics, namely velocity and acceleration, to financial markets. VAcc functions similarly to the popular MACD (Moving Average Convergence Divergence) indicator when using a longer lookback period, but produces more responsive results. With shorter periods, VAcc exhibits characteristics reminiscent of the stochastic oscillator.

🟠 Algorithm

The average velocity over the past n periods is defined as

((C - C_n) / n + (C - C_{n-1}) / (n - 1) + … + (C - C_i) / i + (C - C_1) / 1) / n

At its core, the velocity is a weighted average of the rate of change over the past n periods.

The calculation of the acceleration follows a similar process, where it’s defined as

((V - V_n) / n + (V - V_{n - 1}) / (n - 1) + … + (V - V_i) / i + (V - V_1) / 1) / n

🟠 Comparison with MACD

A comparison of VAcc and MACD on the daily Nasdaq 100 (NDX) chart from August 2022 helps demonstrate VAcc's improved sensitivity. Both indicators utilized a lookback period of 26 days and smoothing of 9 periods.

The VAcc histogram clearly shows a divergence forming, with momentum weakening as prices reached new highs. In contrast, the corresponding MACD histogram significantly lagged in confirming the divergence, highlighting VAcc's ability to identify subtle shifts in trend momentum more immediately than the traditional MACD.

Ichimoku Oscillator With Divergences [ChartPrime]The Ichimoku Oscillator is a trading indicator designed to streamline the interpretation of Ichimoku clouds. It aims to refine and condense the complexities of the Chikou (the lag line), presenting its implications in real-time through an oscillator format, beneficial for those familiar with Ichimoku components but to have a new interpretation of their indicators.

The basics of an Ichimoku:

Conversion Line (Tenkan-Sen): It represents a midpoint of the highest and lowest prices over a specific period, usually 9 periods, reflecting short-term price movements.

Base Line (Kijun-Sen): It acts similarly to the Conversion Line but over a longer period, typically 26 periods, representing medium-term price movements.

Leading Span A & B (Kumo): Span A is the average of the Conversion Line and Base Line, and Span B is the midpoint of the highest and lowest prices over a usually longer period, typically 52 periods. Their interaction denotes trend direction, and the cloud color changes depending on whether Span A is above or below Span B, indicating bullish or bearish market conditions, respectively.

Lagging Span (Chikou Span): It is the current closing price plotted 26 periods behind, assisting in confirming the trend direction and potential momentum.

Advantage of an Oscillator:

Utilizing the oscillator format allows traders to interpret market dynamics more efficiently by visualizing the momentum and trend strength in a bounded range, enabling quick assessments of overbought or oversold conditions. Creating this oscillator provides multiple advantageous; particularly in sideway markets, helping to identify potential reversal points and offering insights on market entries and exits. When building this oscillator we've put a focus on unique interpretations such as overbought and sold areas and divergences; otherwise not found in traditional Ichimoku techniques. It is important to note these divergences are naturally not 100% real time.

When the oscillator turns green; the market is in an uptrend, red for downtrend and yellow for a transitioning market. The center line and the inner most cloud represent a balanced market state.

Key Features & Input Parameters:

Signal Source: Allows the selection of the price data source for signal generation, such as closing prices, and it’s the foundational parameter upon which the oscillator functions.

Normalization Settings: Users can select the normalization mode (“All”, “Window”, or “Disabled”), influencing how the oscillator scales its values. When enabled, it will scale from 100 to -100, allowing the user to understand better the relative positioning of price data.

Smoothing: This indicator offers advanced smoothing features, with options for additional smoothing, allowing traders to adjust the signal's sensitivity to price movements.

Kumo & Chikou Visibility: Traders can customize the visibility settings of Kumo and Chikou, tailoring the display of each component to their preference, enabling a cleaner and more intuitive view of market conditions.

Color Coding: Each component and condition, like bullish or bearish states, can be color-coded, providing visual cues to enhance the interpretability of market trends and states.

Color on Conversion: The oscillator provides an option to color the signal based on the crossover of the conversion and base lines.

Divergence: The oscillator can detect and highlight regular and hidden bullish and bearish divergences between the signal and price, aiding traders in identifying potential trend reversals or continuations.

Alerts:

The list of inbuilt alerts are provided below:

Inside Cloud: The signal line is inside the cloud.

Up Out of Cloud: The signal line crossed above the cloud.

Down Out of Cloud: The signal line crossed below the cloud.

Future Kumo Cross Bullish: The future Kumo lines have crossed in a bullish manner.

Future Kumo Cross Bearish: The future Kumo lines have crossed in a bearish manner.

Current Kumo Cross Bullish: The current Kumo lines have crossed in a bullish manner.

Current Kumo Cross Bearish: The current Kumo lines have crossed in a bearish manner.

Conversion Base Bullish: The conversion line crossed above the base line.

Conversion Base Bearish: The conversion line crossed below the base line.

Signal Bullish on Conversion Base: The signal line crossed above the maximum of conversion and base lines.

Signal Bearish on Conversion Base: The signal line crossed below the minimum of conversion and base lines.

Chikou Bullish: The Chikou line crossed above zero.

Chikou Bearish: The Chikou line crossed below zero.

Signal Over Max: The signal line crossed above the max level.

Signal Over High: The signal line crossed above the high level.

Signal Under Min: The signal line crossed below the min level.

Signal Under Low: The signal line crossed below the low level.

Chikou Over Max: The Chikou line crossed above the max level.

Chikou Over High: The Chikou line crossed above the high level.

Chikou Under Min: The Chikou line crossed below the min level.

Chikou Under Low: The Chikou line crossed below the low level.

Signal Crossover MA: The signal line crossed over the moving average.

Signal Crossunder MA: The signal line crossed under the moving average.

Regular Bullish Divergence: Regular bullish divergence detected.

Hidden Bullish Divergence: Hidden bullish divergence detected.

Regular Bearish Divergence: Regular bearish divergence detected.

Hidden Bearish Divergence: Hidden bearish divergence detected.

Bounce off of Kumo Up: Bullish Bounce off of Kumo.

Bounce off of Kumo Down: Bearish Bounce off of Kumo.

By providing a cohesive visualization of the Ichimoku elements and market momentum within a bounded range, this oscillator is a unique tool and insight into markets.

RVI_HTFThe "RVI_HTF" indicator is a tool designed to assist traders in analyzing market trends using the Relative Vigor Index (RVI) across different timeframes. It enables users to customize various aspects of the indicator's appearance and behavior. By monitoring the RVI on different timeframes, tracking its relationship with the moving average, and paying attention to extreme arrows above the 80 or below the 20 line, traders can anticipate potential reversals, trends, or changes in market momentum.

Above 80 Line: When the RVI moves above the 80 line, it suggests that the market may be overbought. Extreme upward arrows (indicating potential sell signals) can be a sign that a bullish trend might be reaching an exhaustion point. Traders may anticipate a possible trend reversal or pullback.

Below 20 Line: When the RVI dips below the 20 line, it implies that the market might be oversold. Extreme downward arrows (indicating potential buy signals) can be an early signal of a potential bullish reversal. Traders may anticipate an upcoming uptrend or bounce.

Crossing Above Moving Average: When the RVI crosses above its moving average on the selected timeframe, it can serve as an early indication of potential bullish strength in the market. This suggests that buying pressure may be increasing.

Crossing Below Moving Average: Conversely, when the RVI crosses below its moving average, it can signal potential bearish momentum. This indicates that selling pressure may be gaining strength.

Variables:

Timeframe (TF) Selection:

The indicator allows you to select the timeframe for the RVI calculation. You can choose from various options such as 1 minute (1), 5 minutes (5), 15 minutes (15), 30 minutes (30), 60 minutes (60), 240 minutes (240), Daily (D), Weekly (W), Monthly (M), or use "Auto" to automatically select a higher timeframe based on your current chart's timeframe.

Moving Average Type (MA_Type):

Function: Allows users to select the type of moving average used in RVI calculations.

Options: You can select from various moving average types, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

SMMA (Smoothed Moving Average, also known as RMA)

WMA (Weighted Moving Average)

VWMA (Volume Weighted Moving Average)

DEMA (Double Exponential Moving Average)

Moving Average Length (MA_Length):

Function: Permits users to set the number of periods for the selected moving average type.

Purpose: Controls the sensitivity of the RVI indicator. Longer lengths provide smoother results, while shorter lengths react more quickly to price changes.

Up Arrow Color (upArrowColor):

Function: Enables users to customize the color of arrows that indicate potential Overbought areas. (Only shown when the TF is same as or lower than the chart TF)

Down Arrow Color (downArrowColor):

Function: Allows users to specify the color of downward-pointing arrows signaling potential Oversold areas. (Only shown when the TF is same as or lower than the chart TF)

RVI Up Color (firstColor):

Function: Defines the color of the RVI line when it indicates a bullish condition on the higher timeframe.

RVI Down Color (secondColor):

Function: Specifies the color of the RVI line when it suggests a bearish condition on the higher timeframe.

RVI-Based Moving Average Up Color (firstColorMA):

Function: Customizes the color of the RVI-based moving average line when it indicates a bullish condition.

RVI-Based Moving Average Down Color (secondColorMA):

Function: Defines the color of the RVI-based moving average line when it suggests a bearish condition.

[blackcat] L3 CCI-RSI ComboCCI-RSI Combo indicator is a combination indicator that includes CCI and RSI. It uses some parameters to calculate the values of CCI and RSI, and generates corresponding charts based on these values. On the chart, when CCI exceeds 100 or falls below -100, yellow or magenta filling areas are displayed. Additionally, gradient colors are used on the RSI chart to represent different value ranges. Based on the values of CCI and RSI, buying or selling signals can be identified and "B" or "S" labels are displayed at the corresponding positions. It utilizes some technical indicators and logic to generate buying and selling signals, and displays the corresponding labels on the chart.

Here are the main parts of the code:

1. Definition of some variables:

- `N`, `M`, `N1`: Parameters used to calculate CCI and RSI.

- `xcn(cond, len)` and `xex(cond, len)`: Two functions used to calculate the number of times a condition is met.

2. Calculation of CCI (Commodity Channel Index):

- Calculate the CCI value based on the formula `(TYP - ta.sma(TYP, M)) / (0.015 * ta.stdev(TYP, M))`.

- Use the `plot()` function to plot CCI on the chart and set the color based on its value.

3. Calculation of RSI (Relative Strength Index):

- First calculate RSI1 by taking the average of positive differences between closing prices and the average of all absolute differences, and then multiplying by 100.

- Then use the ALMA function to transform RSI1 into a smoother curve.

- Use the `plot()` function to plot RSI on the chart and select gradient colors for shading based on its value.

4. Setting up the gradient color array:

- Create a color array using `array.new_color()` and add a series of color values to it.

5. Generating buying and selling signals based on conditions:

- Use logical operators and technical indicator functions to determine the conditions for buying and selling.

- Use the `label.new()` function to draw the corresponding labels on the chart to represent buying or selling signals.

MADALGO`s Enhanced OBV DivergencesDescription:

MADALGO's Enhanced OBV Divergences indicator is a unique tool designed for traders to visualize the divergences between price action and On Balance Volume (OBV), a fundamental aspect often indicative of underlying strength or weakness in the market. By keenly identifying these divergences, traders are better positioned to anticipate potential trend reversals or trend continuations, making this script an invaluable addition to their technical analysis toolkit.

This script meticulously scans for both regular and hidden bullish/bearish divergences, providing a comprehensive view of market sentiment. The core of this indicator is built around the OBV, which cumulatively adds or subtracts volume based on the price movement per period, thus providing a running total of volume and portraying the force behind the price movements.

The regular divergences are classic indicators of a potential reversal in the current trend, while hidden divergences are often indicative of trend continuation. These divergences are pinpointed based on the relative positions of the OBV and price highs/lows, over customizable lookback periods and within specified lookback ranges.

Features:

Regular and Hidden Divergences: Clearly marked bullish and bearish divergences provide insights into potential market turning points.

On Balance Volume (OBV) Line: Visualize the continuous flow of buying and selling pressure, enabling the identification of accumulation or distribution phases essential for understanding the market's strength or weakness.

Moving Average of OBV: An optional feature to smooth the OBV line, aiding in the identification of the overarching trend.

Dynamic Statistics Label: A floating label provides real-time updates on essential statistics like the Rate of Percentage Change (RPC) of OBV, the last divergences, and bars since the last divergences.

Inputs:

Pivot Lookback Right and Pivot Lookback Left: Define the lookback periods for identifying pivot points in the OBV line.

Max of Lookback Range and Min of Lookback Range: Define the range for considering divergences.

RPC Period: Defines the period for calculating the Rate of Percentage Change of the OBV.

MA Period: Defines the period for the optional moving average of the OBV.

Plot Bullish, Plot Hidden Bullish, Plot Bearish, Plot Hidden Bearish: Toggle visibility of respective divergences.

Plot Moving Average: Toggle visibility of the OBV moving average.

Usage:

Add the script to your TradingView chart.

Tailor the input parameters in the settings panel to align with your analysis requirements.

The divergences, OBV line, and optional moving average will be plotted on your chart, with a dynamic label displaying real-time statistics.

Set up alerts to be notified of identified divergences, enabling timely decision-making.

Alerts:

Regular bullish/bearish divergence in OBV found: Triggered when a regular bullish or bearish divergence is identified.

Hidden bullish/bearish divergence in OBV found: Triggered when a hidden bullish or bearish divergence is identified.

Underlying Concepts:

The OBV Divergences indicator is rooted in the principle that volume precedes price movement. When prices are rising with increased volume, it suggests that buying pressure is prevailing and may lead to continued upward momentum. Conversely, rising prices with decreasing volume might indicate a lack of buying conviction and could signal a potential price reversal. The identification of divergences between price and OBV can therefore serve as a powerful signal for traders. These examples can be seen below in the image

The Moving Average of the OBV further aids in understanding the prevailing trend by smoothing out the OBV line, providing a clearer picture of the market's longer-term momentum. The Rate of Percentage Change (RPC) provides insight into the momentum of volume, offering an additional layer of analysis. Together, these additional features enhance the core OBV analysis, enabling a more nuanced understanding of volume dynamics fundamental for making more informed trading decisions.

License:

This Source Code Form is subject to the terms of the Mozilla Public License, v. 2.0. If a copy of the MPL was not distributed with this file, you can obtain one at Mozilla Public License 2.0.

PCA-Risk IndicatorOBJECTIVE:

The objective of this indicator is to synthesize, via PCA (Principal Component Analysis), several of the most used indicators with in order to simplify the reading of any asset on any timeframe.

It is based on my Bitcoin Risk Long Term indicator, and is the evolution of another indicator that I have not published 'Average Risk Indicator'.

The idea of this indicator is to use statistics, in this case the PCA, to reduce the number of dimensions (indicator) to aggregate them in some synthetic indicators (PCX)

I invite you to dig deeper into the PCA, but that is to try to keep as much information as possible from the raw data. The signal minus the noise.

I realized this indicator a year ago, but I publish it now because I do not see the interest to keep it private.

USAGE:

Unlike the Bitcoin Risk Long Term indicator, it does not make sense to change or disable the input indicators unless you use the 'Average Indicator' function. Because each input is weighted to generate the outputs, the PCX.

I extracted several courses (Bitcoin, Gold, S&P, CAC40) on several timeframes (W, D, 4h, 1h) of Trading view and use the Excel generated for the data on which I played the PCA analysis.

The results:

explained_variance_ratio: 0.55540809 / 0.13021972 / 0.07303142 / 0.03760925

explained_variance: 11.6639671 / 2.73470717 / 1.53371209 / 0.7898212

Interpretation:

Simply put, 55% of the information contained in each indicator can be represented with PC1, +13% with PC2, +7% with PC3, +3% with PC4.

What is important to understand is that PC1, which serves as a thermometer in a way, gives a simple indication of over-buying or over-selling area better than any other indicator.

PC2, difficult to interpret, is more reactive because precedes PC1, but can give false signals.

PC3 and PC4 do not seem relevant to me.

The way I use it is to take PC1 for Risk indicator, and display PC2 with 'Area'. When PC2 turns around and PC1 arrives on extremes, it can be good points to act.

NOTES :

- It is surprising that a simple average of all the indicators gives a fairly relevant result

- With Average indicator as Risk indicator, you can combine the indicators of your choice and see the predictive power with the staining of bars.

- You can add alerts on the levels of your choice on the Risk Indicator

- If you have any idea of adding an indicator, modification, criticism, bug found: share them, it’s appreciated!

---- FR ----

OBJECTIF :

L'objectif de cet indicateur est de synthétiser, via l'ACP (Analyse en Composantes Principales), plusieurs indicateurs parmi les plus utilisés avec afin de simplifier la lecture de n'importe quel actif sur n'importe quel timeframe.

Il est inspiré de mon indicateur 'Bitcoin Risk Long Term indicator', et est l'évolution d'un autre indicateur que je n'ai pas publié 'Average Risk Indicator'.

L'idée de cet indicateur est d'utiliser les statistiques, en l'occurence l'ACP, pour réduire le nombre de dimensions (indicateur) pour les agréger dans quelques indicateurs synthétiques (PCX)

Je vous invite à creuser l'ACP, mais c'est chercher à conserver un maximum d'informations à partir de la donnée brute. Le signal moins le bruit.

J'ai réalisé cet indicateur il y a un an, mais je le publie maintenant car je ne vois pas l'intérêt de le garder privé.

UTILISATION :

Contrairement à 'Bitcoin Risk Long Term indicator', il ne fait pas sens de modifier ou désactiver les indicateurs inputs, sauf si vous utiliser la fonction 'Average Indicator'. Car chaque input est pondéré pour générer les outputs, les PCX.

J'ai extrait plusieurs cours (Bitcoin, Gold, S&P, CAC40) sur plusieurs timeframes (W, D, 4h, 1h) de Trading view et utiliser les Excel généré pour la data sur laquelle j'ai joué l'analyse ACP.

Les résultats :

explained_variance_ratio : 0.55540809 / 0.13021972 / 0.07303142 / 0.03760925

explained_variance : 11.6639671 / 2.73470717 / 1.53371209 / 0.7898212

Interprétation :

Pour faire simple, 55% de l'information contenu dans chaque indicateur peut être représenté avec PC1, +13% avec PC2, +7% avec PC3, +3% avec PC4.

Ce qui faut y comprendre c'est que le PC1, qui sert de thermomètre en quelque sorte, donne une indication simple de zone de sur-achat ou sur-vente mieux que n'importe quel autre indicateur.

PC2, difficile à interpréter, est plus réactif car précède PC1, mais peut donner des faux signaux.

PC3 et PC4 ne me semble pas pertinent.

La manière dont je m'en sert c'est de prendre PC1 pour Risk indicator, et d'afficher PC2 avec 'Region'. Lorsque PC2 se retourne et que PC1 arrive sur des extrêmes, cela peut être des bons points pour agir.

NOTES :

- Il est étonnant de constater qu'une simple moyenne de tous les indicateurs donne un résultat assez pertinent

- Avec Average indicator comme Risk indicator, vous pouvez combiner les indicateurs de vos choix et voir la force prédictive avec la coloration des bars.

- Vous pouvez ajouter des alertes sur les niveaux de votre choix sur le Risk Indicator

- Si vous avez la moindre idée d'ajout d'indicateur, modification, critique, bug trouvé : partagez-les, c'est apprécié !

Heatmap MACD StrategyHello traders

A customer gave me the idea indirectly after I made an update to that script:

Supertrend MTF Heatmap

Important Notes

The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

I wanted to showcase that any Heatmap script can be converted into a strategy.

The strategy default settings are:

Initial Capital: 100000 USD

Position Size: 1 contract

Commission Percent: 0.075%

Slippage: 1 tick

No margin/leverage used

For example, those are realistic settings for trading CFD indices with low timeframes, but not the best possible settings for all assets/timeframes.

Concept

The Heatmap MACD Strategy allows selecting one MACD in five different timeframes.

You'll get an exit signal whenever one of the 5 MACDs changes direction.

Then, the strategy re-enters whenever all the MACDs are in the same direction again.

It takes:

long trades when all the 5 MACD histograms are bullish

short trades when all the 5 MACD histograms are bearish

You can select the same timeframe multiple times if you don't need five timeframes.

For example, if you only need the 30min, the 1H, and 2H, you can set your timeframes as follow:

30m

30m

30m

1H

2H

Risk Management Features

Nothing too fancy

All the features below are pips-based

Stop-Loss

Trailing Stop-Loss

Stop-Loss to Breakeven after a certain amount of pips has been reached

Take Profit 1st level and closing X% of the trade

Take Profit 2nd level and close the remaining of the trade

What's next?

I'll publish this script's open-source Pineconnector, ProfitView, and AutoView versions for educational purposes.

Thank you

Dave

Triple Ehlers Market StateClear trend identification is an important aspect of finding the right side to trade, another is getting the best buying/selling price on a pullback, retracement or reversal. Triple Ehlers Market State can do both.

Three is always better

Ehlers’ original formulation produces bullish, bearish and trendless signals. The indicator presented here gate stages three correlation cycles of adjustable lengths and degree thresholds, displaying a more refined view of bullish, bearish and trendless markets, in a compact and novel way.

Stick with the default settings, or experiment with the cycle period and threshold angle of each cycle, then choose whether ‘Recent trend weighting’ is included in candle colouring.

John Ehlers is a highly respected trading maths head who may need no introduction here. His idea for Market State was published in TASC June 2020 Traders Tips. The awesome interpretation of Ehlers’ work on which Triple Ehlers Market State’s correlation cycle calculations are based can be found at:

DISCLAIMER: None of this is financial advice.