Bitcoin Halving CountdownJust a simple Bitcoin halving countdown

Set up for the 2028 halving with the block height set at 1050000

Block height can be setup in the script settings for future halving

We don't have real time on-chain data on TradingView, so the script will update only once a day with a lag of one day (GLASSNODE data) until we get live data.

If you have any suggestions/questions leave a comment :)

Mescu

Chain

FunctionBaumWelchLibrary "FunctionBaumWelch"

Baum-Welch Algorithm, also known as Forward-Backward Algorithm, uses the well known EM algorithm

to find the maximum likelihood estimate of the parameters of a hidden Markov model given a set of observed

feature vectors.

---

### Function List:

> `forward (array pi, matrix a, matrix b, array obs)`

> `forward (array pi, matrix a, matrix b, array obs, bool scaling)`

> `backward (matrix a, matrix b, array obs)`

> `backward (matrix a, matrix b, array obs, array c)`

> `baumwelch (array observations, int nstates)`

> `baumwelch (array observations, array pi, matrix a, matrix b)`

---

### Reference:

> en.wikipedia.org

> github.com

> en.wikipedia.org

> www.rdocumentation.org

> www.rdocumentation.org

forward(pi, a, b, obs)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

Returns: - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

forward(pi, a, b, obs, scaling)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

scaling (bool) : Normalize `alpha` scale.

Returns: - #### Tuple with:

> - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

> - `array _c`: Array with normalization scale.

backward(a, b, obs)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

backward(a, b, obs, c)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

c (float ) : Array with Normalization scaling coefficients.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

baumwelch(observations, nstates)

**(Random Initialization)** Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

nstates (int)

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

baumwelch(observations, pi, a, b)

Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

pi (float ) : Initial probaility distribution.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

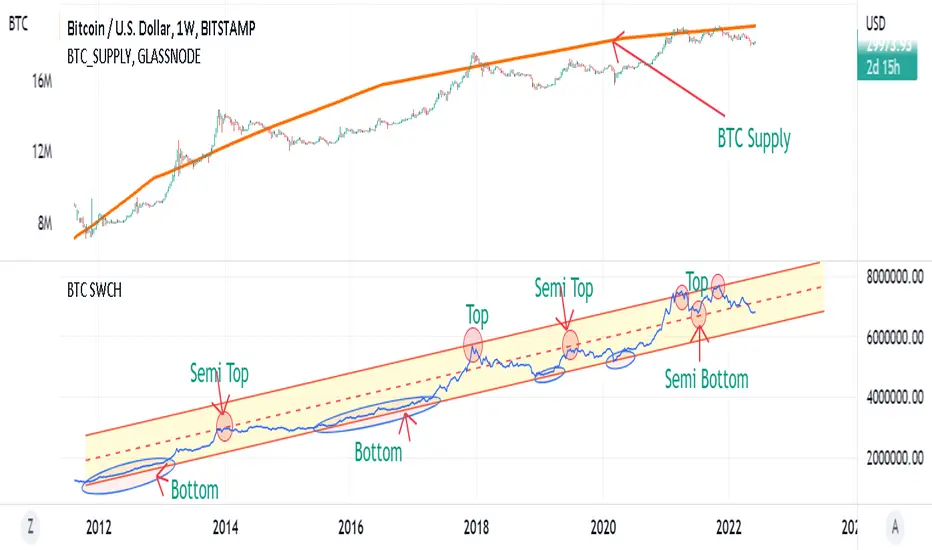

Supply Weighted Moving Average: OnchinUse this Onchain Channel in Weekly Timeframe - on BTCUSD BUTSTAMP Chart:

This Moving average channel is weighted based on BTC's new Supply:

I believe the slope of the Bitcoin trend line is correlated to the new supply and the issue of Halving.

The chart below shows this:

In fact, after each Halving, the supply is halved. Halving the supply increases the demand-for-supply ratio and increases the price. But the uptrend slope also halves after each halving.

Therefore, the slope of the bitcoin trend is correlated with the new supply rate. This is the logic of this new metric.

Accordingly, the moving average is weighted based on the new supply. This new channel can identify where bitcoin is too cheap or too expensive in the historical chart. It has also marked support/resistance Supply Weighted Moving Average.

BTC New Supply: OnchainThis Onchain Metric shows the sum of newly issued coins.

This metric is very useful for finding new bull run cycles in the market. The new bull run is accompanied by a significant drop in the new supply.

BTC Supply weighted channel: OnchainUse this oscillator in the weekly time frame and then draw the above linear channel

The premise of this idea is that the trend slope of the bitcoin price correlates with the bitcoin supply chart, which shows the total amount of bitcoin ever created/issued.

Therefore, Bitcoin price is weighted based on Bitcoin supply.

As a result, the above channel has been created, which is a linear channel, and it seems that it can be an oscillator to determine the bitcoin trend, as well as the tops and bottoms of the market.

Bitcoin seems to respect the bottom and top lines of this channel as well as its midline

Glassnode BTC SOPR ToolkitSOPR stand for Spent Output Profit Ratio. It’s a Bitcoin on-chain metric that shows whether Bitcoin spent outputs (UTXO’s) are being realized in profit or loss. It’s calculated by dividing realized value by the value at creation (price sold / price paid).

The SOPR metric traditionally uses a baseline of 1 instead of 0. For the purposes of the script, I've changed the baseline to 0.

SOPR signals > 0 show the overall market is transaction at a profit.

SOPR signals < 0 show the overall market is transacting at a loss.

SOPR servers as a great short/mid-term indicator.

SOPR Toolkit Features

- Smoothed SOPR

- SOPR Spikes

Smoothed SOPR

By default, ‘Smoothed SOPR’ is shown which applies a smoothing function to SOPR. This helps to visualize the broader SOPR trend.

Smoothed SOPR is calculated by taking the difference between positive and negative SOPR values.

SOPR is split into separate arrays based on if it's above or below the baseline A moving average is then applied to each array, then subtracted to get the difference.

You can also change whether or not a SMA, EMA, or Volume Weighted Simple/Exponential moving average is used. The VWMA is calculated using Glassnode’s BTC Total Transfer Volume metric.

SOPR Spikes

Shows relevant SOPR spikes.

SOPR spikes is calculated by applying a Bollinger Band to SOPR. Only values spike outside the bands are shown.

Adjust the StdDev to show more/less relevant spikes.

Enjoy :)

Test: Chain casting multiple functions performanceExperimental:

A simple test to check performance impact of chaining functions in pinescript.

Test calling frequency impact.

Test: Chain casting functions performanceExperimental:

A simple test to check performance impact of chaining functions in pinescript.

BTC exchange trade vol / on-chain transaction volThis Bitcoin indicator shows the percentage that the exchange traded volume is from the sum of the exchange traded volume + on-chain transaction volume.

The thin red line is the non-smoothed value calculated from daily volumes.

The thick black line is the 7-day EMA-smoothed value.

The exchange traded volume and the on-chain transaction volume are reported by Quandl and have a 1D resolution - so it is best to use this indicator on the daily time frame.

When the value is high, it shows the the interest of traders is high and they are intensely trading BTC. When the indicator is low, it means that BTC is "dormant": it is used for transfers, but not so much for trading - traders forgot about it for a while - which may be a good time to accumulate if the economy is in a general bull market.