On-Chain Signals [LuxAlgo]The On-Chain Signals indicator uses fundamental blockchain metrics to provide traders with an objective technical view of their favorite cryptocurrencies.

It uses IntoTheBlock datasets integrated within TradingView to generate four key signals: Net Network Growth, In the Money, Concentration, and Large Transactions.

Together, these four signals provide traders with an overall directional bias of the market. All of the data can be visualized as a gauge, table, historical plot, or average.

🔶 USAGE

The main goal of this tool is to provide an overall directional bias based on four blockchain signals, each with three possible biases: bearish, neutral, or bullish. The thresholds for each signal bias can be adjusted on the settings panel.

These signals are based on IntoTheBlock's On-Chain Signals.

Net network growth: Change in the total number of addresses over the last seven periods; i.e., how many new addresses are being created.

In the Money: Change in the seven-period moving average of the total supply in the money. This shows how many addresses are profitable.

Concentration: Change in the aggregate addresses of whales and investors from the previous period. These are addresses holding at least 0.1% of the supply. This shows how many addresses are in the hands of a few.

Large Transactions: Changes in the number of transactions over $100,000. This metric tracks convergence or divergence from the 21- and 30-day EMAs and indicates the momentum of large transactions.

All of these signals together form the blockchain's overall directional bias.

Bearish: The number of bearish individual signals is greater than the number of bullish individual signals.

Neutral: The number of bearish individual signals is equal to the number of bullish individual signals.

Bullish: The number of bullish individual signals is greater than the number of bearish individual signals.

If the overall directional bias is bullish, we can expect the price of the observed cryptocurrency to increase. If the bias is bearish, we can expect the price to decrease. If the signal is neutral, the price may be more likely to stay the same.

Traders should be aware of two things. First, the signals provide optimal results when the chart is set to the daily timeframe. Second, the tool uses IntoTheBlock data, which is available on TradingView. Therefore, some cryptocurrencies may not be available.

🔹 Display Mode

Traders have three different display modes at their disposal. These modes can be easily selected from the settings panel. The gauge is set by default.

🔹 Gauge

The gauge will appear in the center of the visible space. Traders can adjust its size using the Scale parameter in the Settings panel. They can also give it a curved effect.

The number of bars displayed directly affects the gauge's resolution: More bars result in better resolution.

The chart above shows the effect that different scale configurations have on the gauge.

🔹 Historical Data

The chart above shows the historical data for each of the four signals.

Traders can use this mode to adjust the thresholds for each signal on the settings panel to fit the behavior of each cryptocurrency. They can also analyze how each metric impacts price behavior over time.

🔹 Average

This display mode provides an easy way to see the overall bias of past prices in order to analyze price behavior in relation to the underlying blockchain's directional bias.

The average is calculated by taking the values of the overall bias as -1 for bearish, 0 for neutral, and +1 for bullish, and then applying a triangular moving average over 20 periods by default. Simple and exponential moving averages are available, and traders can select the period length from the settings panel.

🔶 DETAILS

The four signals are based on IntoTheBlock's On-Chain Signals. We gather the data, manipulate it, and build the signals depending on each threshold.

Net network growth

float netNetworkGrowthData = customData('_TOTALADDRESSES')

float netNetworkGrowth = 100*(netNetworkGrowthData /netNetworkGrowthData - 1)

In the Money

float inTheMoneyData = customData('_INOUTMONEYIN')

float averageBalance = customData('_AVGBALANCE')

float inTheMoneyBalance = inTheMoneyData*averageBalance

float sma = ta.sma(inTheMoneyBalance,7)

float inTheMoney = ta.roc(sma,1)

Concentration

float whalesData = customData('_WHALESPERCENTAGE')

float inverstorsData = customData('_INVESTORSPERCENTAGE')

float bigHands = whalesData+inverstorsData

float concentration = ta.change(bigHands )*100

Large Transactions

float largeTransacionsData = customData('_LARGETXCOUNT')

float largeTX21 = ta.ema(largeTransacionsData,21)

float largeTX30 = ta.ema(largeTransacionsData,30)

float largeTransacions = ((largeTX21 - largeTX30)/largeTX30)*100

🔶 SETTINGS

Display mode: Select between gauge, historical data and average.

Average: Select a smoothing method and length period.

🔹 Thresholds

Net Network Growth : Bullish and bearish thresholds for this signal.

In The Money : Bullish and bearish thresholds for this signal.

Concentration : Bullish and bearish thresholds for this signal.

Transactions : Bullish and bearish thresholds for this signal.

🔹 Dashboard

Dashboard : Enable/disable dashboard display

Position : Select dashboard location

Size : Select dashboard size

🔹 Gauge

Scale : Select the size of the gauge

Curved : Enable/disable curved mode

Select Gauge colors for bearish, neutral and bullish bias

🔹 Style

Net Network Growth : Enable/disable historical plot and choose color

In The Money : Enable/disable historical plot and choose color

Concentration : Enable/disable historical plot and choose color

Large Transacions : Enable/disable historical plot and choose color

Crypto

Crypto Options Greeks & Volatility Analyzer [BackQuant]Crypto Options Greeks & Volatility Analyzer

Overview

The Crypto Options Greeks & Volatility Analyzer is a comprehensive analytical tool that calculates Black-Scholes option Greeks up to the third order for Bitcoin and Ethereum options. It integrates implied volatility data from VOLMEX indices and provides multiple visualization layers for options risk analysis.

Quick Introduction to Options Trading

Options are financial derivatives that give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price (strike price) within a specific time period (expiration date). Understanding options requires grasping two fundamental concepts:

Call Options : Give the right to buy the underlying asset at the strike price. Calls increase in value when the underlying price rises above the strike price.

Put Options : Give the right to sell the underlying asset at the strike price. Puts increase in value when the underlying price falls below the strike price.

The Language of Options: Greeks

Options traders use "Greeks" - mathematical measures that describe how an option's price changes in response to various factors:

Delta : How much the option price moves for each $1 change in the underlying

Gamma : How fast delta changes as the underlying moves

Theta : Daily time decay - how much value erodes each day

Vega : Sensitivity to implied volatility changes

Rho : Sensitivity to interest rate changes

These Greeks are essential for understanding risk. Just as a pilot needs instruments to fly safely, options traders need Greeks to navigate market conditions and manage positions effectively.

Why Volatility Matters

Implied volatility (IV) represents the market's expectation of future price movement. High IV means:

Options are more expensive (higher premiums)

Market expects larger price swings

Better for option sellers

Low IV means:

Options are cheaper

Market expects smaller moves

Better for option buyers

This indicator helps you visualize and quantify these critical concepts in real-time.

Back to the Indicator

Key Features & Components

1. Complete Greeks Calculations

The indicator computes all standard Greeks using the Black-Scholes-Merton model adapted for cryptocurrency markets:

First Order Greeks:

Delta (Δ) : Measures the rate of change of option price with respect to underlying price movement. Ranges from 0 to 1 for calls and -1 to 0 for puts.

Vega (ν) : Sensitivity to implied volatility changes, expressed as price change per 1% change in IV.

Theta (Θ) : Time decay measured in dollars per day, showing how much value erodes with each passing day.

Rho (ρ) : Interest rate sensitivity, measuring price change per 1% change in risk-free rate.

Second Order Greeks:

Gamma (Γ) : Rate of change of delta with respect to underlying price, indicating how quickly delta will change.

Vanna : Cross-derivative measuring delta's sensitivity to volatility changes and vega's sensitivity to price changes.

Charm : Delta decay over time, showing how delta changes as expiration approaches.

Vomma (Volga) : Vega's sensitivity to volatility changes, important for volatility trading strategies.

Third Order Greeks:

Speed : Rate of change of gamma with respect to underlying price (∂Γ/∂S).

Zomma : Gamma's sensitivity to volatility changes (∂Γ/∂σ).

Color : Gamma decay over time (∂Γ/∂T).

Ultima : Third-order volatility sensitivity (∂²ν/∂σ²).

2. Implied Volatility Analysis

The indicator includes a sophisticated IV ranking system that analyzes current implied volatility relative to its recent history:

IV Rank : Percentile ranking of current IV within its 30-day range (0-100%)

IV Percentile : Percentage of days in the lookback period where IV was lower than current

IV Regime Classification : Very Low, Low, High, or Very High

Color-Coded Headers : Visual indication of volatility regime in the Greeks table

Trading regime suggestions based on IV rank:

IV Rank > 75%: "Favor selling options" (high premium environment)

IV Rank 50-75%: "Neutral / Sell spreads"

IV Rank 25-50%: "Neutral / Buy spreads"

IV Rank < 25%: "Favor buying options" (low premium environment)

3. Gamma Zones Visualization

Gamma zones display horizontal price levels where gamma exposure is highest:

Purple horizontal lines indicate gamma concentration areas

Opacity scaling : Darker shading represents higher gamma values

Percentage labels : Shows gamma intensity relative to ATM gamma

Customizable zones : 3-10 price levels can be analyzed

These zones are critical for understanding:

Pin risk around expiration

Potential for explosive price movements

Optimal strike selection for gamma trading

Market maker hedging flows

4. Probability Cones (Expected Move)

The probability cones project expected price ranges based on current implied volatility:

1 Standard Deviation (68% probability) : Shown with dashed green/red lines

2 Standard Deviations (95% probability) : Shown with dotted green/red lines

Time-scaled projection : Cones widen as expiration approaches

Lognormal distribution : Accounts for positive skew in asset prices

Applications:

Strike selection for credit spreads

Identifying high-probability profit zones

Setting realistic price targets

Risk management for undefined risk strategies

5. Breakeven Analysis

The indicator plots key price levels for options positions:

White line : Strike price

Green line : Call breakeven (Strike + Premium)

Red line : Put breakeven (Strike - Premium)

These levels update dynamically as option premiums change with market conditions.

6. Payoff Structure Visualization

Optional P&L labels display profit/loss at expiration for various price levels:

Shows P&L at -2 sigma, -1 sigma, ATM, +1 sigma, and +2 sigma price levels

Separate calculations for calls and puts

Helps visualize option payoff diagrams directly on the chart

Updates based on current option premiums

Configuration Options

Calculation Parameters

Asset Selection : BTC or ETH (limited by VOLMEX IV data availability)

Expiry Options : 1D, 7D, 14D, 30D, 60D, 90D, 180D

Strike Mode : ATM (uses current spot) or Custom (manual strike input)

Risk-Free Rate : Adjustable annual rate for discounting calculations

Display Settings

Greeks Display : Toggle first, second, and third-order Greeks independently

Visual Elements : Enable/disable probability cones, gamma zones, P&L labels

Table Customization : Position (6 options) and text size (4 sizes)

Price Levels : Show/hide strike and breakeven lines

Technical Implementation

Data Sources

Spot Prices : INDEX:BTCUSD and INDEX:ETHUSD for underlying prices

Implied Volatility : VOLMEX:BVIV (Bitcoin) and VOLMEX:EVIV (Ethereum) indices

Real-Time Updates : All calculations update with each price tick

Mathematical Framework

The indicator implements the full Black-Scholes-Merton model:

Standard normal distribution approximations using Abramowitz and Stegun method

Proper annualization factors (365-day year)

Continuous compounding for interest rate calculations

Lognormal price distribution assumptions

Alert Conditions

Four categories of automated alerts:

Price-Based : Underlying crossing strike price

Gamma-Based : 50% surge detection for explosive moves

Moneyness : Deep ITM alerts when |delta| > 0.9

Time/Volatility : Near expiration and vega spike warnings

Practical Applications

For Options Traders

Monitor all Greeks in real-time for active positions

Identify optimal entry/exit points using IV rank

Visualize risk through probability cones and gamma zones

Track time decay and plan rolls

For Volatility Traders

Compare IV across different expiries

Identify mean reversion opportunities

Monitor vega exposure across strikes

Track higher-order volatility sensitivities

Conclusion

The Crypto Options Greeks & Volatility Analyzer transforms complex mathematical models into actionable visual insights. By combining institutional-grade Greeks calculations with intuitive overlays like probability cones and gamma zones, it bridges the gap between theoretical options knowledge and practical trading application.

Whether you're:

A directional trader using options for leverage

A volatility trader capturing IV mean reversion

A hedger managing portfolio risk

Or simply learning about options mechanics

This tool provides the quantitative foundation needed for informed decision-making in cryptocurrency options markets.

Remember that options trading involves substantial risk and complexity. The Greeks and visualizations provided by this indicator are tools for analysis - they should be combined with proper risk management, position sizing, and a thorough understanding of options strategies.

As crypto options markets continue to mature and grow, having professional-grade analytics becomes increasingly important. This indicator ensures you're equipped with the same analytical capabilities used by institutional traders, adapted specifically for the unique characteristics of 24/7 cryptocurrency markets.

Time-Decaying Percentile Oscillator [BackQuant]Time-Decaying Percentile Oscillator

1. Big-picture idea

Traditional percentile or stochastic oscillators treat every bar in the look-back window as equally important. That is fine when markets are slow, but if volatility regime changes quickly yesterday’s print should matter more than last month’s. The Time-Decaying Percentile Oscillator attempts to fix that blind spot by assigning an adjustable weight to every past price before it is ranked. The result is a percentile score that “breathes” with market tempo much faster to flag new extremes yet still smooth enough to ignore random noise.

2. What the script actually does

Build a weight curve

• You pick a look-back length (default 28 bars).

• You decide whether weights fall Linearly , Exponentially , by Power-law or Logarithmically .

• A decay factor (lower = faster fade) shapes how quickly the oldest price loses influence.

• The array is normalised so all weights still sum to 1.

Rank prices by weighted mass

• Every close in the window is paired with its weight.

• The pairs are sorted from low to high.

• The cumulative weight is walked until it equals your chosen percentile level (default 50 = median).

• That price becomes the Time-Decayed Percentile .

Find dispersion with robust statistics

• Instead of a fragile standard deviation the script measures weighted Median-Absolute-Deviation about the new percentile.

• You multiply that deviation by the Deviation Multiplier slider (default 1.0) to get a non-parametric volatility band.

Build an adaptive channel

• Upper band = percentile + (multiplier × deviation)

• Lower band = percentile – (multiplier × deviation)

Normalise into a 0-100 oscillator

• The current close is mapped inside that band:

0 = lower band, 50 = centre, 100 = upper band.

• If the channel squeezes, tiny moves still travel the full scale; if volatility explodes, it automatically widens.

Optional smoothing

• A second-stage moving average (EMA, SMA, DEMA, TEMA, etc.) tames the jitter.

• Length 22 EMA by default—change it to tune reaction speed.

Threshold logic

• Upper Threshold 70 and Lower Threshold 30 separate standard overbought/oversold states.

• Extreme bands 85 and 15 paint background heat when aggressive fade or breakout trades might trigger.

Divergence engine

• Looks back twenty bars.

• Flags Bullish divergence when price makes a lower low but oscillator refuses to confirm (value < 40).

• Flags Bearish divergence when price prints a higher high but oscillator stalls (value > 60).

3. Component walk-through

• Source – Any price series. Close by default, switch to typical price or custom OHLC4 for futures spreads.

• Look-back Period – How many bars to rank. Short = faster, long = slower.

• Base Percentile Level – 50 shows relative position around the median; set to 25 / 75 for quartile tracking or 90 / 10 for extreme tails.

• Deviation Multiplier – Higher values widen the dynamic channel, lowering whipsaw but delaying signals.

• Decay Settings

– Type decides the curve shape. Exponential (default 1.16) mimics EMA logic.

– Factor < 1 shrinks influence faster; > 1 spreads influence flatter.

– Toggle Enable Time Decay off to compare with classic equal-weight stochastic.

• Smoothing Block – Choose one of seven MA flavours plus length.

• Thresholds – Overbought / Oversold / Extreme levels. Push them out when working on very mean-reverting assets like FX; pull them in for trend monsters like crypto.

• Display toggles – Show or hide threshold lines, extreme filler zones, bar colouring, divergence labels.

• Colours – Bullish green, bearish red, neutral grey. Every gradient step is automatically blended to generate a heat map across the 0-100 range.

4. How to read the chart

• Oscillator creeping above 70 = market auctioning near the top of its adaptive range.

• Fast poke above 85 with no follow-through = exhaustion fade candidate.

• Slow grind that lives above 70 for many bars = valid bullish trend, not a fade.

• Cross back through 50 shows balance has shifted; treat it like a micro trend change.

• Divergence arrows add extra confidence when you already see two-bar reversal candles at range extremes.

• Background shading (semi-transparent red / green) warns of extreme states and throttles your position size.

5. Practical trading playbook

Mean-reversion scalps

1. Wait for oscillator to reach your desired OB/ OS levels

2. Check the slope of the smoothing MA—if it is flattening the squeeze is mature.

3. Look for a one- or two-bar reversal pattern.

4. Enter against the move; first target = midline 50, second target = opposite threshold.

5. Stop loss just beyond the extreme band.

Trend continuation pullbacks

1. Identify a clean directional trend on the price chart.

2. During the trend, TDP will oscillate between midline and extreme of that side.

3. Buy dips when oscillator hits OS levels, and the same for OB levels & shorting

4. Exit when oscillator re-tags the same-side extreme or prints divergence.

Volatility regime filter

• Use the Enable Time Decay switch as a regime test.

• If equal-weight oscillator and decayed oscillator diverge widely, market is entering a new volatility regime—tighten stops and trade smaller.

Divergence confirmation for other indicators

• Pair TDP divergence arrows with MACD histogram or RSI to filter false positives.

• The weighted nature means TDP often spots divergence a bar or two earlier than standard RSI.

Swing breakout strategy

1. During consolidation, band width compresses and oscillator oscillates around 50.

2. Watch for sudden expansion where oscillator blasts through extreme bands and stays pinned.

3. Enter with momentum in breakout direction; trail stop behind upper or lower band as it re-expands.

6. Customising decay mathematics

Linear – Each older bar loses the same fixed amount of influence. Intuitive and stable; good for slow swing charts.

Exponential – Influence halves every “decay factor” steps. Mirrors EMA thinking and is fastest to react.

Power-law – Mid-history bars keep more authority than exponential but oldest data still fades. Handy for commodities where seasonality matters.

Logarithmic – The gentlest curve; weight drops sharply at first then levels off. Mimics how traders remember dramatic moves for weeks but forget ordinary noise quickly.

Turn decay off to verify the tool’s added value; most users never switch back.

7. Alert catalogue

• TD Overbought / TD Oversold – Cross of regular thresholds.

• TD Extreme OB / OS – Breach of danger zones.

• TD Bullish / Bearish Divergence – High-probability reversal watch.

• TD Midline Cross – Momentum shift that often precedes a window where trend-following systems perform.

8. Visual hygiene tips

• If you already plot price on a dark background pick Bullish Color and Bearish Color default; change to pastel tones for light themes.

• Hide threshold lines after you memorise the zones to declutter scalping layouts.

• Overlay mode set to false so the oscillator lives in its own panel; keep height about 30 % of screen for best resolution.

9. Final notes

Time-Decaying Percentile Oscillator marries robust statistical ranking, adaptive dispersion and decay-aware weighting into a simple oscillator. It respects both recent order-flow shocks and historical context, offers granular control over responsiveness and ships with divergence and alert plumbing out of the box. Bolt it onto your price action framework, trend-following system or volatility mean-reversion playbook and see how much sooner it recognises genuine extremes compared to legacy oscillators.

Backtest thoroughly, experiment with decay curves on each asset class and remember: in trading, timing beats timidity but patience beats impulse. May this tool help you find that edge.

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

Price Exhaustion Envelope [BackQuant]Price Exhaustion Envelope

Visual preview of the bands:

What it is

The Price Exhaustion Envelope (PEE) is a multi‑factor overextension detector wrapped inside a dynamic envelope framework. It measures how “tired” a move is by blending price stretch, volume surges, momentum and acceleration, plus optional RSI divergence. The result is a composite exhaustion score that drives both on‑chart signals and the adaptive width of three optional envelope bands around a smoothed baseline. When the score spikes above or below your chosen threshold, the script can flag exhaustion, paint candles, tint the background and fire alerts.

How it works under the hood

Exhaustion score

Price component: distance of close from its mean in standard deviation units.

Volume component: normalized volume pressure that highlights unusual participation.

Momentum component: rate of change and acceleration of price, scaled by their own volatility.

RSI divergence (optional): bullish and bearish divergences gently push the score lower or higher.

Mode control: choose Price, Volume, Momentum or Composite. Composite averages the main pieces for a balanced view.

Energy scale (0 to 100)

The composite score is pushed through a logistic transform to create an “energy” value. High energy (above 70 to 80) signals a move that may be running hot, while very low energy (below 20 to 30) points to exhaustion on the downside.

Envelope engine

Baseline: EMA of price over the main lookback length.

Width: base width is standard deviation times a multiplier.

Type selector:

• Static keeps the width fixed.

• Dynamic expands width in proportion to the absolute exhaustion score.

• Adaptive links width to the energy reading so bands breathe with market “heat.”

Smoothing: a short EMA on the width reduces jitter and keeps bands pleasant to trade around.

Band architecture

You can toggle up to three symmetric bands on each side of the baseline. They default to 1.0, 1.6 and 2.2 multiples of the smoothed width. Soft transparent fills create a layered thermograph of extension. The outermost band often maps to true blow‑off extremes.

On‑chart elements

Baseline line that flips color in real time depending on where price sits.

Up to three upper and lower bands with progressive opacity.

Triangle markers at fresh exhaustion triggers.

Tiny warning glyphs at extreme upper or lower breaches.

Optional bar coloring to visually tag exhausted candles.

Background halo when energy > 80 or < 20 for instant context.

A compact info table showing State, Score, Energy, Momentum score and where price sits inside the envelope (percent).

How to use it in trading

Mean reversion plays

When price pierces the outer band and an exhaustion marker prints, look for reversal candles or lower‑timeframe confirmation to fade the move back toward the baseline.

For conservative entries, wait for the composite score to roll back under the threshold or for energy to drop from extreme to neutral.

Set stops just beyond the extreme levels (use extreme_upper and extreme_lower as natural invalidation points). Targets can be the baseline or the opposite inner band.

Trend continuation with smart pullbacks

In strong trends, the first tag of Band 1 or Band 2 against the dominant direction often offers low‑risk continuation entries. Use energy readings: if energy is low on a pullback during an uptrend, a bounce is more likely.

Combine with RSI divergence: hidden bullish divergence near a lower band in an uptrend can be a powerful confirmation.

Breakout filtering

A breakout that occurs while the composite score is still moderate (not exhausted) has a higher chance of follow‑through. Skip signals when energy is already above 80 and price is punching the outer band, as the move may be late.

Watch env_position (Envelope %) in the table. Breakouts near 40 to 60 percent of the envelope are “healthy,” while those at 95 percent are stretched.

Scaling out and risk control

Use exhaustion alerts to trim positions into strength or weakness.

Trail stops just outside Band 2 or Band 3 to stay in trends while letting the envelope expand in volatile phases.

Multi‑timeframe confluence

Run the script on a higher timeframe to locate exhaustion context, then drill down to a lower timeframe for entries.

Opposite signals across timeframes (daily exhaustion vs. 5‑minute breakout) warn you to reduce size or tighten management.

Key inputs to experiment with

Lookback Period: larger values smooth the score and envelope, ideal for swing trading. Shorter values make it reactive for scalps.

Exhaustion Threshold: raise above 2.0 in choppy assets to cut noise, drop to 1.5 for smooth FX pairs.

Envelope Type: Dynamic is great for crypto spikes, Adaptive shines in stocks where volume and volatility wave together.

RSI Divergence: turn off if you prefer a pure price/volume model or if divergence floods the score in your asset.

Alert set included

Fresh upper exhaustion

Fresh lower exhaustion

Extreme upper breach

Extreme lower breach

RSI bearish divergence

RSI bullish divergence

Hook these to TradingView notifications so you get pinged the moment a move hits exhaustion.

Best practices

Always pair exhaustion signals with structure. Support and resistance, liquidity pools and session opens matter.

Avoid blindly shorting every upper signal in a roaring bull market. Let the envelope type help you filter.

Use the table to sanity‑check: a very high score but mid‑range env_position means the band may still be wide enough to absorb more movement.

Backtest threshold combinations on your instrument. Different tickers carry different volatility fingerprints.

Final note

Price Exhaustion Envelope is a flexible framework, not a turnkey system. It excels as a context layer that tells you when the crowd is pressing too hard or when a move still has fuel. Combine it with sound execution tactics, risk limits and market awareness. Trade safe and let the envelope breathe with the market.

Weighted Multi-Mode Oscillator [BackQuant]Weighted Multi‑Mode Oscillator

1. What Is It?

The Weighted Multi‑Mode Oscillator (WMMO) is a next‑generation momentum tool that turns a dynamically‑weighted moving average into a 0‑100 bounded oscillator.

It lets you decide how each bar is weighted (by volume, volatility, momentum or a hybrid blend) and how the result is normalised (Percentile, Z‑Score or Min‑Max).

The outcome is a self‑adapting gauge that delivers crystal‑clear overbought / oversold zones, divergence clues and regime shifts on any market or timeframe.

2. How It Works

• Dynamic Weight Engine

▪ Volume – emphasises bars with exceptional participation.

▪ Volatility – inverse ATR weighting filters noisy spikes.

▪ Momentum – amplifies strong directional ROC bursts.

▪ Hybrid – equal‑weight blend of the three dimensions.

• Multi‑Mode Smoothing

Choose from 8 MA types (EMA, DEMA, HMA, LINREG, TEMA, RMA, SMA, WMA) plus a secondary smoothing factor to fine‑tune lag vs. responsiveness.

• Normalization Suite

▪ Percentile – rank vs. recent history (context aware).

▪ Z‑Score – standard deviations from mean (statistical extremes).

▪ Min‑Max – scale between rolling high/low (trend friendly).

3. Reading the Oscillator

Zone Default Level Interpretation

Bull > 80 Acceleration; momentum buyers in control

Neutral 20 – 80 Consolidation / no edge

Bear < 20 Exhaustion; sellers dominate

Gradient line/area automatically shades from bright green (strong bull) to deep red (strong bear).

Optional bar‑painting colours price bars the same way for rapid chart scanning.

4. Typical Use‑Cases

Trend Confirmation – Set Weight = Hybrid, Smoothing = EMA. Enter pullbacks only when WMMO > 50 and rising.

Mean Reversion – Weight = Volatility, reduce upper / lower bands to 70 / 30 and fade extremes.

Volume Pulse – Intraday futures: Weight = Volume to catch participation surges before breakout candles.

Divergence Spotting – Compare price highs/lows to WMMO peaks for early reversal clues.

5. Inputs & Styling

Calculation: Source, MA Length, MA Type, Smoothing

Weighting: Volume period & factor, Volatility length, Momentum period

Normalisation: Method, Look‑back, Upper / Lower thresholds

Display: Gradient fills, Threshold lines, Bar‑colouring toggle, Line width & colours

All thresholds, colours and fills are fully customisable inside the settings panel.

6. Built‑In Alerts

WMMO Long – oscillator crosses up through upper threshold.

WMMO Short – oscillator crosses down through lower threshold.

Attach them once and receive push / e‑mail notifications the moment momentum flips.

7. Best Practices

Percentile mode is self‑adaptive and works well across assets; Z‑Score excels in ranges; Min‑Max shines in persistent trends.

Very short MA lengths (< 10) may produce jitter; compensate with higher “Smoothing” or longer look‑backs.

Pair WMMO with structure‑based tools (S/R, trend lines) for higher‑probability trade confluence.

Disclaimer

This script is provided for educational purposes only. It is not financial advice. Always back‑test thoroughly and manage risk before trading live capital.

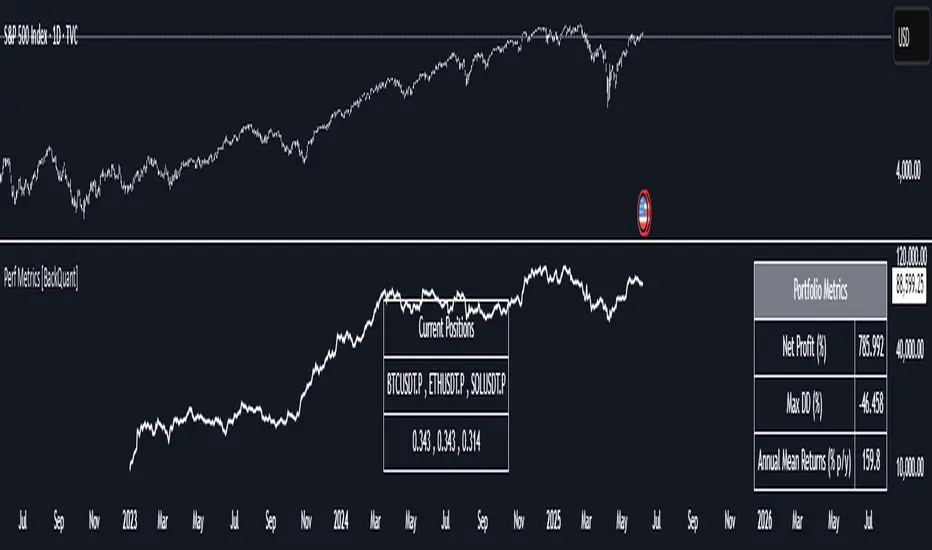

Performance Metrics With Bracketed Rebalacing [BackQuant]Performance Metrics With Bracketed Rebalancing

The Performance Metrics With Bracketed Rebalancing script offers a robust method for assessing portfolio performance, integrating advanced portfolio metrics with different rebalancing strategies. With a focus on adaptability, the script allows traders to monitor and adjust portfolio weights, equity, and other key financial metrics dynamically. This script provides a versatile approach for evaluating different trading strategies, considering factors like risk-adjusted returns, volatility, and the impact of portfolio rebalancing.

Please take the time to read the following:

Key Features and Benefits of Portfolio Methods

Bracketed Rebalancing:

Bracketed Rebalancing is an advanced strategy designed to trigger portfolio adjustments when an asset's weight surpasses a predefined threshold. This approach minimizes overexposure to any single asset while maintaining flexibility in response to market changes. The strategy is particularly beneficial for mitigating risks that arise from significant asset weight fluctuations. The following image illustrates how this method reacts when asset weights cross the threshold:

Daily Rebalancing:

Unlike the bracketed method, Daily Rebalancing adjusts portfolio weights every trading day, ensuring consistent asset allocation. This method aims for a more even distribution of portfolio weights, making it a suitable option for traders who prefer less sensitivity to individual asset volatility. Here's an example of Daily Rebalancing in action:

No Rebalancing:

For traders who prefer a passive approach, the "No Rebalancing" option allows the portfolio to remain static, without any adjustments to asset weights. This method may appeal to long-term investors or those who believe in the inherent stability of their selected assets. Here’s how the portfolio looks when no rebalancing is applied:

Portfolio Weights Visualization:

One of the standout features of this script is the visual representation of portfolio weights. With adjustable settings, users can track the current allocation of assets in real-time, making it easier to analyze shifts and trends. The following image shows the real-time weight distribution across three assets:

Rolling Drawdown Plot:

Managing drawdown risk is a critical aspect of portfolio management. The Rolling Drawdown Plot visually tracks the drawdown over time, helping traders monitor the risk exposure and performance relative to the peak equity levels. This feature is essential for assessing the portfolio's resilience during market downturns:

Daily Portfolio Returns:

Tracking daily returns is crucial for evaluating the short-term performance of the portfolio. The script allows users to plot daily portfolio returns to gain insights into daily profit or loss, helping traders stay updated on their portfolio’s progress:

Performance Metrics

Net Profit (%):

This metric represents the total return on investment as a percentage of the initial capital. A positive net profit indicates that the portfolio has gained value over the evaluation period, while a negative value suggests a loss. It's a fundamental indicator of overall portfolio performance.

Maximum Drawdown (Max DD):

Maximum Drawdown measures the largest peak-to-trough decline in portfolio value during a specified period. It quantifies the most significant loss an investor would have experienced if they had invested at the highest point and sold at the lowest point within the timeframe. A smaller Max DD indicates better risk management and less exposure to significant losses.

Annual Mean Returns (% p/y):

This metric calculates the average annual return of the portfolio over the evaluation period. It provides insight into the portfolio's ability to generate returns on an annual basis, aiding in performance comparison with other investment opportunities.

Annual Standard Deviation of Returns (% p/y):

This measure indicates the volatility of the portfolio's returns on an annual basis. A higher standard deviation signifies greater variability in returns, implying higher risk, while a lower value suggests more stable returns.

Variance:

Variance is the square of the standard deviation and provides a measure of the dispersion of returns. It helps in understanding the degree of risk associated with the portfolio's returns.

Sortino Ratio:

The Sortino Ratio is a variation of the Sharpe Ratio that only considers downside risk, focusing on negative volatility. It is calculated as the difference between the portfolio's return and the minimum acceptable return (MAR), divided by the downside deviation. A higher Sortino Ratio indicates better risk-adjusted performance, emphasizing the importance of avoiding negative returns.

Sharpe Ratio:

The Sharpe Ratio measures the portfolio's excess return per unit of total risk, as represented by standard deviation. It is calculated by subtracting the risk-free rate from the portfolio's return and dividing by the standard deviation of the portfolio's excess return. A higher Sharpe Ratio indicates more favorable risk-adjusted returns.

Omega Ratio:

The Omega Ratio evaluates the probability of achieving returns above a certain threshold relative to the probability of experiencing returns below that threshold. It is calculated by dividing the cumulative probability of positive returns by the cumulative probability of negative returns. An Omega Ratio greater than 1 indicates a higher likelihood of achieving favorable returns.

Gain-to-Pain Ratio:

The Gain-to-Pain Ratio measures the return per unit of risk, focusing on the magnitude of gains relative to the severity of losses. It is calculated by dividing the total gains by the total losses experienced during the evaluation period. A higher ratio suggests a more favorable balance between reward and risk.

www.linkedin.com

Compound Annual Growth Rate (CAGR) (% p/y):

CAGR represents the mean annual growth rate of the portfolio over a specified period, assuming the investment has been compounding over that time. It provides a smoothed annual rate of growth, eliminating the effects of volatility and offering a clearer picture of long-term performance.

Portfolio Alpha (% p/y):

Portfolio Alpha measures the portfolio's performance relative to a benchmark index, adjusting for risk. It is calculated using the Capital Asset Pricing Model (CAPM) and represents the excess return of the portfolio over the expected return based on its beta and the benchmark's performance. A positive alpha indicates outperformance, while a negative alpha suggests underperformance.

Portfolio Beta:

Portfolio Beta assesses the portfolio's sensitivity to market movements, indicating its exposure to systematic risk. A beta greater than 1 suggests the portfolio is more volatile than the market, while a beta less than 1 indicates lower volatility. Beta is used to understand the portfolio's potential for gains or losses in relation to market fluctuations.

Skewness of Returns:

Skewness measures the asymmetry of the return distribution. A positive skew indicates a distribution with a long right tail, suggesting more frequent small losses and fewer large gains. A negative skew indicates a long left tail, implying more frequent small gains and fewer large losses. Understanding skewness helps in assessing the likelihood of extreme outcomes.

Value at Risk (VaR) 95th Percentile:

VaR at the 95th percentile estimates the maximum potential loss over a specified period, given a 95% confidence level. It provides a threshold value such that there is a 95% probability that the portfolio will not experience a loss greater than this amount.

Conditional Value at Risk (CVaR):

CVaR, also known as Expected Shortfall, measures the average loss exceeding the VaR threshold. It provides insight into the tail risk of the portfolio, indicating the expected loss in the worst-case scenarios beyond the VaR level.

These metrics collectively offer a comprehensive view of the portfolio's performance, risk exposure, and efficiency. By analyzing these indicators, investors can make informed decisions, balancing potential returns with acceptable levels of risk.

Conclusion

The Performance Metrics With Bracketed Rebalancing script provides a comprehensive framework for evaluating and optimizing portfolio performance. By integrating advanced metrics, adaptive rebalancing strategies, and visual analytics, it empowers traders to make informed decisions in managing their investment portfolios. However, it's crucial to consider the implications of rebalancing strategies, as academic research indicates that predictable rebalancing can lead to market impact costs. Therefore, adopting flexible and less predictable rebalancing approaches may enhance portfolio performance and reduce associated costs.

Session Status Table📌 Session Status Table

Session Status Table is an indicator that displays the real-time status of the four major trading sessions:

* 🇯🇵 Asia (Tokyo)

* 🇬🇧 London

* 🇺🇸 New York AM

* 🇺🇸 New York PM

It shows which sessions are currently open, how much time remains until they open or close, and optionally sends alerts in advance.

🧩 Features:

* Real-time session table — shows the status of each session on the chart.

* Color-coded statuses:

* 🟢 Green – Session is open

* 🔴 Red – Session is closed

* ⚪ Gray – Weekend

* Countdown timers until session open or close.

* User alerts — receive a notification a custom number of minutes before a session starts.

⚙️ Customization:

* Table position — fully configurable.

* Session colors — customizable for open, closed, and weekend states.

* Session labels — customizable with icons.

* Notifications:

* Enabled through TradingView's Alerts panel.

* User-defined lead time before session opens.

🕒 Time Zones:

All times are calculated in UTC to ensure consistency across different markets and regions, avoiding discrepancies from time zones and daylight saving time.

🚨 How to enable alerts:

1. Open the "Alerts" panel in TradingView.

2. Click "Create Alert".

3. In the condition dropdown, choose "Session Status Table".

4. Set to any alert() trigger.

5. Save — you'll be notified a set number of minutes before each session begins.

ℹ️ Technical Notes:

* Built with Pine Script version 6.

* Logically divided into clear sections: inputs, session calculations, table rendering, and alerts.

* Optimized for performance and reliability on all timeframes.

Ideal for traders who use session activity in their strategies — especially in Forex, crypto, and futures markets.

Arnaud Legoux Trend Aggregator | Lyro RSArnaud Legoux Trend Aggregator

Introduction

Arnaud Legoux Trend Aggregator is a custom-built trend analysis tool that blends classic market oscillators with advanced normalization, advanced math functions and Arnaud Legoux smoothing. Unlike conventional indicators, 𝓐𝓛𝓣𝓐 aggregates market momentum, volatility and trend strength.

Signal Insight

The 𝓐𝓛𝓣𝓐 line visually reflects the aggregated directional bias. A rise above the middle line threshold signals bullish strength, while a drop below the middle line indicates bearish momentum.

Another way to interpret the 𝓐𝓛𝓣𝓐 is through overbought and oversold conditions. When the 𝓐𝓛𝓣𝓐 rises above the +0.7 threshold, it suggests an overbought market and signals a strong uptrend. Conversely, a drop below the -0.7 level indicates an oversold condition and a strong downtrend.

When the oscillator hovers near the zero line, especially within the neutral ±0.3 band, it suggests that no single directional force is dominating—common during consolidation phases or pre-breakout compression.

Real-World Example

Usually 𝓐𝓛𝓣𝓐 is used by following the bar color for simple signals; however, like most indicators there are unique ways to use an indicator. Let’s dive deep into such ways.

The market begins with a green bar color, raising awareness for a potential long setup—but not a direct entry. In this methodology, bar coloring serves as an alert mechanism rather than a strict entry trigger.

The first long position was initiated when the 𝓐𝓛𝓣𝓐 signal line crossed above the +0.3 threshold, suggesting a shift in directional acceleration. This entry coincided with a rising price movement, validating the trade.

As price advanced, the position was exited into cash—not reversed into a short—because the short criteria for this use case are distinct. The exit was prompted by 𝓐𝓛𝓣𝓐 crossing back below the +0.3 level, signaling the potential weakening of the long trend.

Later, as 𝓐𝓛𝓣𝓐 crossed below 0, attention shifted toward short opportunities. A short entry was confirmed when 𝓐𝓛𝓣𝓐 dipped below -0.3, indicating growing downside momentum. The position was eventually closed when 𝓐𝓛𝓣𝓐 crossed back above the -0.3 boundary—signaling a possible deceleration of the bearish move.

This logic was consistently applied in subsequent setups, emphasizing the role of 𝓐𝓛𝓣𝓐’s thresholds in guiding both entries and exits.

Framework

The Arnaud Legoux Trend Aggregator (ALTA) combines multiple technical indicators into a single smoothed signal. It uses RSI, MACD, Bollinger Bands, Stochastic Momentum Index, and ATR.

Each indicator's output is normalized to a common scale to eliminate bias and ensure consistency. These normalized values are then transformed using a hyperbolic tangent function (Tanh).

The final score is refined with a custom Arnaud Legoux Moving Average (ALMA) function, which offers responsive smoothing that adapts quickly to price changes. This results in a clear signal that reacts efficiently to shifting market conditions.

⚠️ WARNING ⚠️: THIS INDICATOR, OR ANY OTHER WE (LYRO RS) PUBLISH, IS NOT FINANCIAL OR INVESTMENT ADVICE. EVERY INDICATOR SHOULD BE COMBINED WITH PRICE ACTION, FUNDAMENTALS, OTHER TECHNICAL ANALYSIS TOOLS & PROPER RISK. MANAGEMENT.

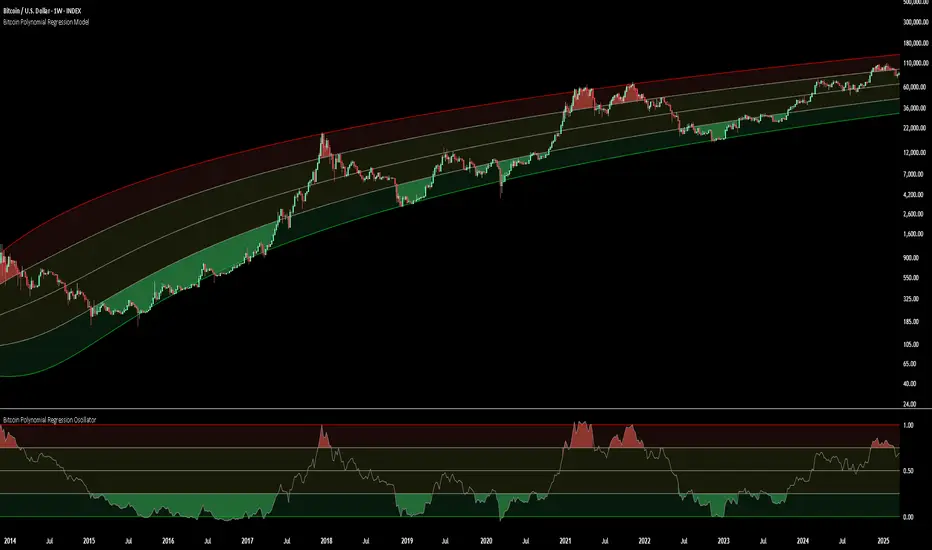

Bitcoin Power Law OscillatorThis is the oscillator version of the script. The main body of the script can be found here.

Understanding the Bitcoin Power Law Model

Also called the Long-Term Bitcoin Power Law Model. The Bitcoin Power Law model tries to capture and predict Bitcoin's price growth over time. It assumes that Bitcoin's price follows an exponential growth pattern, where the price increases over time according to a mathematical relationship.

By fitting a power law to historical data, the model creates a trend line that represents this growth. It then generates additional parallel lines (support and resistance lines) to show potential price boundaries, helping to visualize where Bitcoin’s price could move within certain ranges.

In simple terms, the model helps us understand Bitcoin's general growth trajectory and provides a framework to visualize how its price could behave over the long term.

The Bitcoin Power Law has the following function:

Power Law = 10^(a + b * log10(d))

Consisting of the following parameters:

a: Power Law Intercept (default: -17.668).

b: Power Law Slope (default: 5.926).

d: Number of days since a reference point(calculated by counting bars from the reference point with an offset).

Explanation of the a and b parameters:

Roughly explained, the optimal values for the a and b parameters are determined through a process of linear regression on a log-log scale (after applying a logarithmic transformation to both the x and y axes). On this log-log scale, the power law relationship becomes linear, making it possible to apply linear regression. The best fit for the regression is then evaluated using metrics like the R-squared value, residual error analysis, and visual inspection. This process can be quite complex and is beyond the scope of this post.

Applying vertical shifts to generate the other lines:

Once the initial power-law is created, additional lines are generated by applying a vertical shift. This shift is achieved by adding a specific number of days (or years in case of this script) to the d-parameter. This creates new lines perfectly parallel to the initial power law with an added vertical shift, maintaining the same slope and intercept.

In the case of this script, shifts are made by adding +365 days, +2 * 365 days, +3 * 365 days, +4 * 365 days, and +5 * 365 days, effectively introducing one to five years of shifts. This results in a total of six Power Law lines, as outlined below (From lowest to highest):

Base Power Law Line (no shift)

1-year shifted line

2-year shifted line

3-year shifted line

4-year shifted line

5-year shifted line

The six power law lines:

Bitcoin Power Law Oscillator

This publication also includes the oscillator version of the Bitcoin Power Law. This version applies a logarithmic transformation to the price, Base Power Law Line, and 5-year shifted line using the formula: log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed Base Power Law Line and 5-year shifted line with the formula:

normalized price = log(close) - log(Base Power Law Line) / log(5-year shifted line) - log(Base Power Law Line)

Finally, the normalized price was multiplied by 5 to map its value between 0 and 5, aligning with the shifted lines.

Interpretation of the Bitcoin Power Law Model:

The shifted Power Law lines provide a framework for predicting Bitcoin's future price movements based on historical trends. These lines are created by applying a vertical shift to the initial Power Law line, with each shifted line representing a future time frame (e.g., 1 year, 2 years, 3 years, etc.).

By analyzing these shifted lines, users can make predictions about minimum price levels at specific future dates. For example, the 5-year shifted line will act as the main support level for Bitcoin’s price in 5 years, meaning that Bitcoin’s price should not fall below this line, ensuring that Bitcoin will be valued at least at this level by that time. Similarly, the 2-year shifted line will serve as the support line for Bitcoin's price in 2 years, establishing that the price should not drop below this line within that time frame.

On the other hand, the 5-year shifted line also functions as an absolute resistance , meaning Bitcoin's price will not exceed this line prior to the 5-year mark. This provides a prediction that Bitcoin cannot reach certain price levels before a specific date. For example, the price of Bitcoin is unlikely to reach $100,000 before 2021, and it will not exceed this price before the 5-year shifted line becomes relevant. After 2028, however, the price is predicted to never fall below $100,000, thanks to the support established by the shifted lines.

In essence, the shifted Power Law lines offer a way to predict both the minimum price levels that Bitcoin will hit by certain dates and the earliest dates by which certain price points will be reached. These lines help frame Bitcoin's potential future price range, offering insight into long-term price behavior and providing a guide for investors and analysts. Lets examine some examples:

Example 1:

In Example 1 it can be seen that point A on the 5-year shifted line acts as major resistance . Also it can be seen that 5 years later this price level now corresponds to the Base Power Law Line and acts as a major support at point B(Note: Vertical yearly grid lines have been added for this purpose👍).

Example 2:

In Example 2, the price level at point C on the 3-year shifted line becomes a major support three years later at point D, now aligning with the Base Power Law Line.

Finally, let's explore some future price predictions, as this script provides projections on the weekly timeframe :

Example 3:

In Example 3, the Bitcoin Power Law indicates that Bitcoin's price cannot surpass approximately $808K before 2030 as can be seen at point E, while also ensuring it will be at least $224K by then (point F).

Bitcoin Power LawThis is the main body version of the script. The Oscillator version can be found here.

Understanding the Bitcoin Power Law Model

Also called the Long-Term Bitcoin Power Law Model. The Bitcoin Power Law model tries to capture and predict Bitcoin's price growth over time. It assumes that Bitcoin's price follows an exponential growth pattern, where the price increases over time according to a mathematical relationship.

By fitting a power law to historical data, the model creates a trend line that represents this growth. It then generates additional parallel lines (support and resistance lines) to show potential price boundaries, helping to visualize where Bitcoin’s price could move within certain ranges.

In simple terms, the model helps us understand Bitcoin's general growth trajectory and provides a framework to visualize how its price could behave over the long term.

The Bitcoin Power Law has the following function:

Power Law = 10^(a + b * log10(d))

Consisting of the following parameters:

a: Power Law Intercept (default: -17.668).

b: Power Law Slope (default: 5.926).

d: Number of days since a reference point(calculated by counting bars from the reference point with an offset).

Explanation of the a and b parameters:

Roughly explained, the optimal values for the a and b parameters are determined through a process of linear regression on a log-log scale (after applying a logarithmic transformation to both the x and y axes). On this log-log scale, the power law relationship becomes linear, making it possible to apply linear regression. The best fit for the regression is then evaluated using metrics like the R-squared value, residual error analysis, and visual inspection. This process can be quite complex and is beyond the scope of this post.

Applying vertical shifts to generate the other lines:

Once the initial power-law is created, additional lines are generated by applying a vertical shift. This shift is achieved by adding a specific number of days (or years in case of this script) to the d-parameter. This creates new lines perfectly parallel to the initial power law with an added vertical shift, maintaining the same slope and intercept.

In the case of this script, shifts are made by adding +365 days, +2 * 365 days, +3 * 365 days, +4 * 365 days, and +5 * 365 days, effectively introducing one to five years of shifts. This results in a total of six Power Law lines, as outlined below (From lowest to highest):

Base Power Law Line (no shift)

1-year shifted line

2-year shifted line

3-year shifted line

4-year shifted line

5-year shifted line

The six power law lines:

Bitcoin Power Law Oscillator

This publication also includes the oscillator version of the Bitcoin Power Law. This version applies a logarithmic transformation to the price, Base Power Law Line, and 5-year shifted line using the formula: log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed Base Power Law Line and 5-year shifted line with the formula:

normalized price = log(close) - log(Base Power Law Line) / log(5-year shifted line) - log(Base Power Law Line)

Finally, the normalized price was multiplied by 5 to map its value between 0 and 5, aligning with the shifted lines.

Interpretation of the Bitcoin Power Law Model:

The shifted Power Law lines provide a framework for predicting Bitcoin's future price movements based on historical trends. These lines are created by applying a vertical shift to the initial Power Law line, with each shifted line representing a future time frame (e.g., 1 year, 2 years, 3 years, etc.).

By analyzing these shifted lines, users can make predictions about minimum price levels at specific future dates. For example, the 5-year shifted line will act as the main support level for Bitcoin’s price in 5 years, meaning that Bitcoin’s price should not fall below this line, ensuring that Bitcoin will be valued at least at this level by that time. Similarly, the 2-year shifted line will serve as the support line for Bitcoin's price in 2 years, establishing that the price should not drop below this line within that time frame.

On the other hand, the 5-year shifted line also functions as an absolute resistance , meaning Bitcoin's price will not exceed this line prior to the 5-year mark. This provides a prediction that Bitcoin cannot reach certain price levels before a specific date. For example, the price of Bitcoin is unlikely to reach $100,000 before 2021, and it will not exceed this price before the 5-year shifted line becomes relevant. After 2028, however, the price is predicted to never fall below $100,000, thanks to the support established by the shifted lines.

In essence, the shifted Power Law lines offer a way to predict both the minimum price levels that Bitcoin will hit by certain dates and the earliest dates by which certain price points will be reached. These lines help frame Bitcoin's potential future price range, offering insight into long-term price behavior and providing a guide for investors and analysts. Lets examine some examples:

Example 1:

In Example 1 it can be seen that point A on the 5-year shifted line acts as major resistance . Also it can be seen that 5 years later this price level now corresponds to the Base Power Law Line and acts as a major support at point B (Note: Vertical yearly grid lines have been added for this purpose👍).

Example 2:

In Example 2, the price level at point C on the 3-year shifted line becomes a major support three years later at point D, now aligning with the Base Power Law Line.

Finally, let's explore some future price predictions, as this script provides projections on the weekly timeframe :

Example 3:

In Example 3, the Bitcoin Power Law indicates that Bitcoin's price cannot surpass approximately $808K before 2030 as can be seen at point E, while also ensuring it will be at least $224K by then (point F).

Parabolic RSI Strategy [ChartPrime × PineIndicators]This strategy combines the strengths of the Relative Strength Index (RSI) with a Parabolic SAR logic applied directly to RSI values.

Full credit to ChartPrime for the original concept and indicator, licensed under the MPL 2.0.

It provides clear momentum-based trade signals using an innovative method that tracks RSI trend reversals via a customized Parabolic SAR, enhancing traditional oscillator strategies with dynamic trend confirmation.

How It Works

The system overlays a Parabolic SAR on the RSI, detecting trend shifts in RSI itself rather than on price, offering early reversal insight with visual and algorithmic clarity.

Core Components

1. RSI-Based Trend Detection

Calculates RSI using a customizable length (default: 14).

Uses upper and lower thresholds (default: 70/30) for overbought/oversold zones.

2. Parabolic SAR Applied to RSI

A custom Parabolic SAR function tracks momentum within the RSI, not price.

This allows the system to capture RSI trend reversals more responsively.

Configurable SAR parameters: Start, Increment, and Maximum acceleration.

3. Signal Generation

Long Entry: Triggered when the SAR flips below the RSI line.

Short Entry: Triggered when the SAR flips above the RSI line.

Optional RSI filter ensures that:

Long entries only occur above a minimum RSI (e.g. 50).

Short entries only occur below a maximum RSI.

Built-in logic prevents new positions from being opened against trend without prior exit.

Trade Modes & Controls

Choose from:

Long Only

Short Only

Long & Short

Optional setting to reverse positions on opposite signal (instead of waiting for a flat close).

Visual Features

1. RSI Plotting with Thresholds

RSI is displayed in a dedicated pane with overbought/oversold fill zones.

Custom horizontal lines mark threshold boundaries.

2. Parabolic SAR Overlay on RSI

SAR dots color-coded for trend direction.

Visible only when enabled by user input.

3. Entry & Exit Markers

Diamonds: Mark entry points (above for shorts, below for longs).

Crosses: Mark exit points.

Strategy Strengths

Provides early momentum reversal entries without relying on price candles.

Combines oscillator and trend logic without repainting.

Works well in both trending and mean-reverting markets.

Easy to configure with fine-tuned filter options.

Recommended Use Cases

Intraday or swing traders who want to catch RSI-based reversals early.

Traders seeking smoother signals than price-based Parabolic SAR entries.

Users of RSI looking to reduce false positives via trend tracking.

Customization Options

RSI Length and Thresholds.

SAR Start, Increment, and Maximum values.

Trade Direction Mode (Long, Short, Both).

Optional RSI filter and reverse-on-signal settings.

SAR dot color customization.

Conclusion

The Parabolic RSI Strategy is an innovative, non-repainting momentum strategy that enhances RSI-based systems with trend-confirming logic using Parabolic SAR. By applying SAR logic to RSI values, this strategy offers early, visualized, and filtered entries and exits that adapt to market dynamics.

Credit to ChartPrime for the original methodology, published under MPL-2.0.

Multi-Indicator Swing [TIAMATCRYPTO]v6# Strategy Description:

## Multi-Indicator Swing

This strategy is designed for swing trading across various markets by combining multiple technical indicators to identify high-probability trading opportunities. The system focuses on trend strength confirmation and volume analysis to generate precise entry and exit signals.

### Core Components:

- **Supertrend Indicator**: Acts as the primary trend direction filter with optimized settings (Factor: 3.0, ATR Period: 10) to balance responsiveness and reliability.

- **ADX (Average Directional Index)**: Confirms the strength of the prevailing trend, filtering out sideways or choppy market conditions where the strategy avoids taking positions.

- **Liquidity Delta**: A volume-based indicator that analyzes buying and selling pressure imbalances to validate trend direction and potential reversals.

- **PSAR (Optional)**: Can be enabled to add additional confirmation for trend changes, turned off by default to reduce signal filtering.

### Key Features:

- **Flexible Direction Trading**: Choose between long-only, short-only, or bidirectional trading to adapt to market conditions or account restrictions.

- **Conservative Risk Management**: Implements fixed percentage-based stop losses (default 2%) and take profits (default 4%) for a positive risk-reward ratio.

- **Realistic Backtesting Parameters**: Includes commission (0.1%) and slippage (2 points) to reflect real-world trading conditions.

- **Visual Signals**: Clear buy/sell arrows with customizable sizes for easy identification on the chart.

- **Information Panel**: Dynamic display showing active indicators and current risk settings.

### Best Used On:

Daily timeframes for cryptocurrencies, forex, or stock indices. The strategy performs optimally on assets with clear trending behavior and sufficient volatility.

### Default Settings:

Optimized for conservative position sizing (5% of equity per trade) with an initial capital of $10,000. The backtesting period (2021-2023) provides a statistically significant sample of varied market conditions.

Bitcoin Weekend FadeThis indicator is a tool for setting a bias based on weekend price movements, with the assumption that the crypto market often experiences stronger moves over the weekend due to thinner order books. It helps identify potential fade opportunities, suggesting that price movements from Saturday and Sunday may reverse during the weekdays.

How to use:

Sets a bias based on weekend price action.

Sets a bias based on weekend price action.

Use weekday price action for confirmation before acting on the bias.

Best suited for range-bound markets, where the price tends to revert to the mean.

Avoid fading high-timeframe breakouts, as they often indicate strong trends.

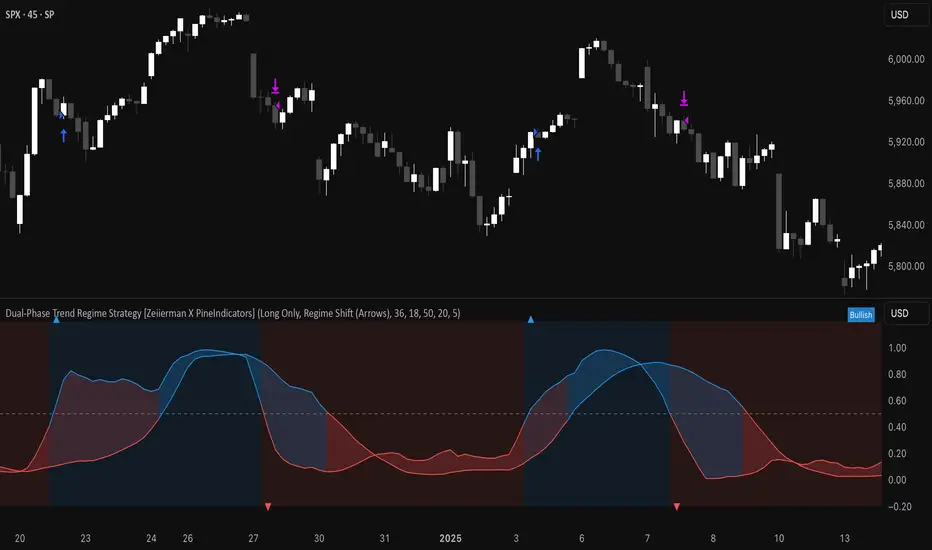

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

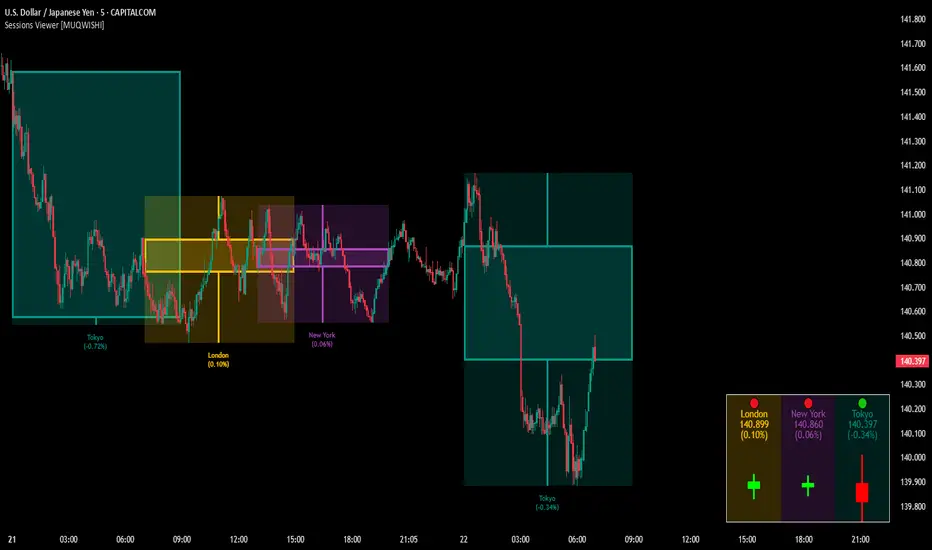

Market Sessions & Viewer Panel [By MUQWISHI]▋ INTRODUCTION :

The “Market Sessions & Viewer Panel” is a clean and intuitive visual indicator tool that highlights up to four trading sessions directly on the chart. Each session is fully customizable with its name, session time, and color. It also generates a panel that provides a quick-glance summary of each session’s candle/bar shape, helping traders gain insight into the volatility across all trading sessions.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

This indicator utilizes the “ Timezone — Library ”. A huge thanks to @n00btraders for effort and well-organized work.

_______________________

▋ SESSION PANEL:

The Session Panel allows traders to visually compare session volatility using a candlestick/bar pattern.

Each bar represents the price action during a session and includes the session status, session name, closing price, change(%) from open, and a tooltip that reveals detailed OHLC and volume when hovered over.

Chart Type:

It offers two styles Bar or Candle to display based on traders’ preference

Sorting:

Allowing to arrange session candles/bars based on…

—Left to Right: The most recently opened on the left, moving backward in time to the right.

—Right to Left: The most recently opened on the right, moving backward in time to the left.

—Default: Arrange sessions in the user-defined input order.

_______________________

▋ CHART VISUALIZATION: