SMC Liquidity Sweep + OB [Fixed]This is a Smart Money Concept (SMC) backtest-ready strategy built to identify high-probability reversal points using two key institutional principles: liquidity sweep and order block confirmation. Designed specifically for pairs like XAUUSD, this system detects where the market sweeps resting liquidity (e.g., stop hunts above recent highs or below recent lows) and looks for a clean reversal candle (order block) to confirm the trap and trigger precise entries.

Unlike BOS or FVG-based models, this version focuses purely on stop-hunt logic and clean price action to simulate institutional behavior—ideal for Smart Money and ICT-style traders who want clear, non-repainting, high-RR setups.

🔍 How the Strategy Works

Liquidity Sweep Detection

The strategy monitors the chart for price breaking above recent swing highs or below recent swing lows (based on a customizable lookback window). This acts as a trigger for a potential trap or liquidity raid.

Order Block Confirmation

After a sweep is detected, the system waits for a confirming candle — a reversal (engulfing-type) candle that acts as an order block:

For longs: a bullish candle that closes higher than the previous bearish candle’s high

For shorts: a bearish candle that closes lower than the previous bullish candle’s low

Entry & Risk Management

Once confirmation is valid, a market entry is placed:

Stop Loss (SL): A fixed pip distance below/above the entry candle

Take Profit (TP): Calculated based on a user-defined Risk-Reward Ratio (e.g., 1:2, 1:3)

Trades are managed automatically and logged into the Strategy Tester with full visibility

🔧 Strategy Parameters

Setting Description

Stop Loss (Pips) Fixed SL distance from entry to protect capital

Risk/Reward Ratio Dynamically calculates TP relative to SL (e.g., RR 2.0 = TP 2x SL)

Liquidity Lookback How many candles back to evaluate swing highs/lows for potential sweeps

Order Block Filter Validates entry only after candle confirmation post-sweep

Direction Filter Supports both long and short signals or one-sided entry filters

📈 Use Case & Optimization

This strategy works best when applied to:

XAUUSD, NAS100, BTCUSD, US30, and high-volatility pairs

Timeframes like 5m, 15m, 1H, where sweeps and reversals are more visible

Traders who follow ICT, SMC, or price action frameworks

Reversal or continuation traders looking for clean execution after liquidity grabs

Because it uses pure price action and logical candle structures, it avoids lag and repainting found in indicator-based systems.

💡 Smart Money Concept Logic Used

Liquidity Grab: Detects stop hunts above recent highs/below lows

Order Block Entry: Entry confirmed only after strong reversal candle at sweep zone

High RR Control: SL and TP customizable to reflect real trading plans

Non-Repainting Structure: All entries are based on confirmed candle closes

📊 Built-in Backtesting Features

Plots trades visually with entry arrows and signal labels

Uses strategy.entry() and strategy.exit() for full testing accuracy

Outputs full performance metrics: win rate, profit factor, drawdown, etc.

All parameters tunable from the settings panel

📎 Release Notes

v1.0

Core SMC strategy with liquidity sweep + OB entry logic

Fully backtestable with fixed SL & dynamic TP

Plots buy/sell signals visually

Optimized for metals, indices, and crypto

⚠️ Disclaimer

This TradingView script is intended for educational and research purposes only. It is not financial advice or a live signal system. Always backtest on your own charts, confirm entries with your personal analysis, and apply strict risk management.

Cryptomarket

NAIFCHART_Algo Pro# NAIFCHART Algo Pro: Advanced Candlestick Pattern Analysis Tool

## Overview

The NAIFCHART Algo Pro indicator represents an innovative approach to candlestick pattern analysis, combining traditional engulfing patterns with advanced technical filters. This indicator was developed and shared by the trading community at t.me focusing on high-probability reversal signals through multi-layered confirmation.

## Core Algorithm Components

**Candle Stability Index**: Measures the ratio between candle body and total range (including wicks). Higher values indicate more decisive price action with stronger conviction. Default setting of 0.5 ensures only stable, well-formed candles generate signals, filtering out indecisive market conditions.

**RSI Momentum Filter**: Utilizes 14-period RSI with customizable threshold (default 50) to confirm overbought/oversold conditions. Buy signals require RSI below the threshold, while sell signals need RSI above the inverse threshold, ensuring momentum alignment with pattern direction.

**Candle Delta Analysis**: Examines price movement over a specified period (default 5 candles) to confirm directional bias. This filter ensures patterns occur after meaningful price moves in the opposite direction, increasing reversal probability.

**Engulfing Pattern Recognition**: Identifies classic bullish and bearish engulfing formations where the current candle completely engulfs the previous candle's body, indicating potential momentum shift.

## Signal Generation Logic

**Buy Signal Criteria**:

- Bullish engulfing pattern formation

- Candle stability above threshold level

- RSI below specified threshold (oversold condition)

- Price decrease over the delta length period

- Confirmed bar state (prevents repainting)

**Sell Signal Criteria**:

- Bearish engulfing pattern formation

- Candle stability above threshold level

- RSI above inverse threshold (overbought condition)

- Price increase over the delta length period

- Confirmed bar state (prevents repainting)

## Advanced Features

**Signal Filtering**: Optional "Disable Repeating Signals" feature prevents signal clusters by blocking consecutive identical signals. This enhances chart clarity and reduces noise in trending markets where multiple patterns might form in sequence.

**Visual Customization**: Multiple label styles including text bubbles, triangles, and arrows with full color customization. Label sizes range from tiny to huge, allowing adaptation to different chart configurations and personal preferences.

**Alert Integration**: Built-in alert system notifies traders immediately when buy or sell conditions are met, enabling real-time trade execution without constant chart monitoring.

## Implementation Strategy

**Timeframe Optimization**: The indicator performs effectively across multiple timeframes, with higher timeframes (1-hour and above) providing more reliable signals due to reduced market noise. Shorter timeframes require more conservative position sizing due to increased false signal probability.

**Parameter Tuning**:

- Increase Candle Stability Index for more selective signals in volatile markets

- Adjust RSI threshold based on market conditions (lower for trending markets, higher for ranging conditions)

- Modify Candle Delta Length for different trend confirmation periods

**Risk Management**: Combine signals with proper stop loss placement below/above the engulfing pattern's extreme points. Consider position sizing based on pattern strength and overall market context.

## Market Application

**Reversal Trading**: Primary application focuses on identifying high-probability reversal points after extended moves. The multi-filter approach significantly reduces false signals compared to basic engulfing pattern strategies.

**Trend Confirmation**: In trending markets, signals align with pullback completion, providing optimal entry points for trend continuation strategies. The RSI and delta filters help identify temporary retracements rather than trend changes.

**Range Trading**: Within sideways markets, signals often occur near range boundaries, providing effective support and resistance bounce opportunities with clearly defined risk parameters.

## Performance Optimization

**Market Selection**: The indicator performs best on liquid instruments with clear candlestick formations. Avoid extremely volatile or thin markets where patterns may be less reliable.

**Session Timing**: Consider trading sessions when focusing on specific markets. Major session overlaps often provide clearer patterns due to increased participation and volume.

**Confirmation Techniques**: While the indicator provides internal filtering, additional confirmation through volume analysis, key support/resistance levels, or broader market context enhances signal reliability.

## Community Resources

Access ongoing strategy discussions and optimization techniques through the source community at t.me where traders share practical applications and parameter adjustments for different market conditions.

The collaborative environment provides valuable insights into optimal settings for various trading styles and market environments, along with real-time feedback on signal quality and performance.

## Conclusion

NAIFCHART Algo Pro offers a sophisticated approach to candlestick pattern trading through intelligent filtering and confirmation mechanisms. The indicator's strength lies in combining traditional pattern recognition with modern technical analysis filters, creating a robust framework for identifying high-probability reversal opportunities.

Success with this tool requires understanding each component's role in signal generation and adapting parameters to match current market conditions and personal trading style. The community-driven development ensures practical relevance and ongoing refinement based on real trading experiences.

Practice with demo accounts to develop familiarity with signal timing and optimal parameter settings before live implementation. The indicator's systematic approach provides clear entry signals while maintaining flexibility for different risk management and position sizing strategies.

Top Crypto Above 28-Day AverageDescription

The “Top Crypto Above 28-Day Average” (CRYPTOTW) script scans a selectable universe of up to 120 top-capitalization cryptocurrencies (divided into customizable 40-symbol batches), then plots the count of those trading above their own 28-period simple moving average. It helps you gauge broad market strength and identify which tokens are showing momentum relative to their recent trend.

Key Features

• Batch Selection: Choose among “Top40,” “Mid40,” or “Low40” market-cap groups, or set a custom batch size (up to 40 symbols) to keep within the API limit.

• Dynamic Plot: Displays a live line chart of how many cryptos are above their 28-day MA on each bar.

• Reference Lines: Automatic horizontal lines at 25%, 50%, and 75% of your batch to provide quick visual thresholds.

• Background Coloration: The chart background shifts green/yellow/red based on whether more than 70%, 50–70%, or under 50% of the batch is above the MA.

• Optional Table: On the final bar, show a sortable table of up to 28 tickers currently above their 28-day MA, including current price, percent above MA, and “Above” status color-coding.

• Alerts:

• Strong Batch Performance: Fires when >70% of the batch is above the MA.

• Weak Batch Performance: Fires when <10 cryptos (i.e. <25%) are above the MA.

Inputs

• Show Results Table (show_table): Toggle the detailed table on/off.

• Table Position (table_position): Select one of the four corners for your table overlay.

• Max Cryptos to Display (max_display): Limit the number of rows in the results table.

• Current Batch (current_batch): Pick “Top40,” “Mid40,” or “Low40.”

• Batch Size (batch_size): Define the number of symbols (1–40) you want to include from the chosen batch.

How to Use

1. Add the CRYPTOTW indicator to any chart.

2. Select your batch and size to focus on the segment of the crypto market you follow.

3. Watch the plotted line to see the proportion of tokens with bullish momentum.

4. (Optional) Enable the results table to see exactly which tokens are outperforming their 28-day average.

5. Set alerts to be notified when the batch either overheats (strong performance) or cools off significantly.

Why It Matters

By tracking the share of assets riding their 28-day trend, you gain a macro-level view of market breadth—crucial for spotting emerging rallies or early signs of broad weakness. Whether you’re swing-trading individual altcoins or assessing overall market mood, this tool distills complex data into an intuitive, actionable signal.

Williams VIX For Bottoms [DCD]Williams VIX Original - Authentic Volatility Fear Gauge

What This Indicator Does

The Williams VIX Fix measures market fear by calculating how far current lows deviate from recent highs, identifying potential market bottoms during high volatility periods. This implementation provides Larry Williams' original formula in its purest form.

How It Works

Core Formula:

VIX Fix = ((Highest High over 22 periods - Current Low) / Highest High over 22 periods) × 100

The calculation process:

Measures Relative Distance: Compares current low to highest high over lookback period

Converts to Percentage: Normalizes values for cross-market comparison

Applies Statistical Analysis: Uses Bollinger Bands (2 std dev) around VIX Fix values

Filters with Percentiles: 85th percentile threshold removes noise

Signal Generation

Green Flash Signals trigger when either condition is met:

VIX Fix exceeds upper Bollinger Band (2 standard deviations above 20-period MA)

VIX Fix exceeds Range High (85th percentile of recent values)

This dual-condition approach reduces false signals while capturing genuine volatility spikes.

What Makes This Original

Pure Formula Implementation: Uses Williams' exact original calculation without modifications

Dual Confirmation System: Combines Bollinger Bands with percentile analysis

Professional Visualization: Histogram display, background highlighting, and live value table

Comprehensive Alerts: Signal start/end notifications plus Green Flash alerts

How to Use

Primary Purpose: Spot high-probability reversal zones during market fear climaxes

Signal Interpretation:

Green triangle + background highlight = High volatility reversal zone

Higher VIX Fix values = Stronger fear/better reversal potential

Use with price action confirmation for best results

Optimal Settings:

Timeframes: 4H, Daily, Weekly

Markets: All (stocks, crypto, forex, commodities)

Combine with support levels and candlestick patterns

Key Parameters:

VIX Fix Length (22): Lookback period for highest high

Std Dev Multiplier (2.0): Bollinger Band sensitivity

Percentile High (0.85): Only top 15% of readings trigger signals

The VIX Fix excels at identifying market fear climaxes that coincide with significant price bottoms, making it valuable for swing traders seeking high-probability entries during market stress.

RSI SwingRadar🧠 Strategy Overview

This long-only strategy combines RSI/MA crossovers with ATR-based risk management, designed for cleaner entries during potential bounce phases — especially tuned for assets like XMR/USDT.

🔍 Core Logic:

- RSI Crossover: Entry occurs when the 14-period RSI crosses above its 14-period SMA, signaling a potential shift in momentum.

- Oversold Filter: The RSI must have been below a user-defined oversold threshold (default: 35) on the previous candle, filtering for bounce setups after a pullback.

- ATR-Based Stop/Target: Stop-loss is placed below the low by a user-adjustable ATR multiplier (default: 0.5×). Take-profit is calculated with a Risk:Reward multiplier (default: 4×).

These elements work in tandem — RSI crossovers give momentum confirmation, oversold filtering adds context, and ATR-based exits adapt to volatility, creating a compact yet responsive strategy.

📉 Visuals:

- Dynamic Bands: The chart displays the active stop-loss, entry price, and take-profit as colored bands for easy visual tracking.

- Clean Overlay: Designed with simplicity — only confirmed setups are shown, keeping noise low.

✅ Suggested Use:

- Works best on XMR/USDT or similarly trending assets.

- Best suited for pullback entries during broader uptrends.

- Adjustable for different volatility conditions and asset behaviors.

⚠️ Disclaimer

- This strategy is for educational and research purposes only.

- It does not guarantee profitability in any market.

- Always backtest, forward-test, and understand your own risk tolerance before using any

strategy in a live environment.

- Past performance is not indicative of future results.

- This script is not financial advice.

Momentum Long + Short Strategy (BTC 3H)Momentum Long + Short Strategy (BTC 3H)

🔍 How It Works, Step by Step

Detect the Trend (📈/📉)

Calculate two moving averages (100-period and 500-period), either EMA or SMA.

For longs, we require MA100 > MA500 (uptrend).

For shorts, we block entries if MA100 exceeds MA500 by more than a set percentage (to avoid fading a powerful uptrend).

Apply Momentum Filters (⚡️)

RSI Filter: Measures recent strength—only allow longs when RSI crosses above its smoothed average, and shorts when RSI dips below the oversold threshold.

ADX Filter: Gauges trend strength—ensures we only enter when a meaningful trend exists (optional).

ATR Filter: Confirms volatility—avoids choppy, low-volatility conditions by requiring ATR to exceed its smoothed value (optional).

Confirm Entry Conditions (✅)

Long Entry:

Price is above both MAs

Trend alignment & optional filters pass ✅

Short Entry:

Price is below both MAs and below the lower Bollinger Band

RSI is sufficiently oversold

Trend-blocker & ATR filter pass ✅

Position Sizing & Risk (💰)

Each trade uses 100 % of account equity by default.

One pyramid addition allowed, so you can scale in if the move continues.

Commission and slippage assumptions built in for realistic backtests.

Stops & Exits (🛑)

Long Stop-Loss: e.g. 3 % below entry.

Long Auto-Exit: If price falls back under the 500-period MA.

Short Stop-Loss: e.g. 3 % above entry.

Short Take-Profit: e.g. 4 % below entry.

🎨 Why It’s Powerful & Customizable

Modular Filters: Turn on/off RSI, ADX, ATR filters to suit different market regimes.

Adjustable Thresholds: Fine-tune stop-loss %, take-profit %, RSI lengths, MA gaps and more.

Multi-Timeframe Potential: Although coded for 3 h BTC, you can adapt it to stocks, forex or other cryptos—just recalibrate!

Backtest Fine-Tuned: Default settings were optimized via backtesting on historical BTC data—but they’re not guarantees of future performance.

⚠️ Warning & Disclaimer

This strategy is for educational purposes only and designed for a toy fund. Crypto markets are highly volatile—you can lose 100 % of your capital. It is not a predictive “holy grail” but a rules-based framework using past data. The parameters have been fine-tuned on historical data and are not valid for future trades without fresh calibration. Always practice with paper-trading first, use proper risk management, and do your own research before risking real money. 🚨🔒

Good luck exploring and experimenting! 🚀📊

MestreDoFOMO Future Projection BoxMestreDoFOMO Future Projection Box - Description & How to Use

Description

The "MestreDoFOMO Future Projection Box" is a TradingView indicator tailored for crypto traders (e.g., BTC/USDT on 1H, 4H, or 1D timeframes). It visualizes current price ranges, projects future levels, and confirms trends using semi-transparent boxes. With labeled price levels and built-in alerts, it’s a simple yet powerful tool for identifying support, resistance, and potential price targets.

How It Works

Blue Box (Current Channel): Shows the recent price range over the last 10 bars (adjustable). The top is the highest high plus an ATR buffer, and the bottom is the lowest low minus the buffer. Labels display exact levels (e.g., "Top: 114000", "Bottom: 102600").

Green Box (Future Projection): Projects the price range 10 bars ahead (adjustable) based on the trend slope of the moving average. Labels show "Proj Top" and "Proj Bottom" for future targets.

Orange Box (Moving Average): Traces a 50-period EMA (adjustable) to confirm the trend. An upward slope signals a bullish trend; a downward slope signals a bearish trend. A label shows the current MA value (e.g., "MA: 105000").

Alerts: Triggers when the price nears the projected top or bottom, helping you catch breakouts or retracements.

How to Use

Add the Indicator: Apply "MestreDoFOMO Future Projection Box" to your chart in TradingView.

Interpret the Trend: Check the orange box’s slope—upward for bullish, downward for bearish.

Identify Key Levels: Use the blue box’s top as resistance and bottom as support. On a 4H chart, if the top is 114,000, expect resistance; if the bottom is 102,600, expect support.

Plan Targets: Use the green box for future targets—top for profit-taking (e.g., 114,000), bottom for stop-loss or buying (e.g., 102,600).

Set Alerts: Enable alerts for "Near Upper Projection" or "Near Lower Projection" to get notified when the price hits key levels.

Trade Examples:

Bullish: If the price breaks above the blue box top (e.g., 114,000), buy with a target at the green box top. Set a stop-loss below the green box bottom.

Bearish: If the price rejects at the blue box top and drops below the orange MA, short with a target at the blue box bottom.

Customize: Adjust the lookback period, projection bars, ATR multiplier, and MA length in the settings to fit your trading style.

Tips

Use on 1H for short-term trades, 4H for swing trades, or 1D for long-term trends.

Combine with volume or RSI to confirm signals.

Validate levels with market structure (e.g., candlestick patterns).

PORTFOLIO TABLE Simple [Titans_Invest]PORTFOLIO TABLE Simple

This is a simple table for you to monitor your assets or cryptocurrencies in your SPOT wallet without needing to access your broker’s website or wallet app.

⯁ HOW TO USE THIS TABLE❓

You only need to select the asset and enter the amount of each one.

The table will show how much you have of each asset and the total value of your portfolio.

You’ll be able to monitor up to 39 assets in real time.

⯁ CONVERT VALUES

You can also activate and select a currency for conversion.

For example, cryptocurrency assets are calculated in US dollars, but you can select euros as the conversion currency.

The values originally in dollars will then be displayed in euros.

⯁ Track your Portfolio in real time:

⯁ Add your local Currency to Convert Values:

⯁ Follow your Portfolio Live:

___________________________________________________________

📜 SCRIPT : PORTFOLIO TABLE Simple

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

___________________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

BTC vs ALT Lag Detector [MEXC Overlay]This indicator monitors the price movement of Bitcoin (BTC) and compares it in real time to a customizable list of major altcoins on the MEXC exchange.

It helps you identify lagging altcoins — tokens that are underperforming or overperforming BTC’s price action over a selected timeframe. These temporary deviations can offer profitable entry or rotation opportunities, especially for scalpers, day traders, and arbitrage-style strategies.

Key Features:

- Real-time deviation detection between BTC and altcoins

- Customizable comparison timeframe: 1m, 6m, 12m, 30m, 1h, 4h, or 1d

- Deviation threshold alert: Highlights coins that lag BTC by more than 0.5%, 1%, 2%, or 3%

- Compact stats table embedded in the price chart

- Fully adjustable layout: Table position (Top/Bottom/Center + Left/Right), Font size (Tiny, Small, Medium)

- Built-in alert system when deviation exceeds your chosen threshold

How to Use It:

Set your desired timeframe for comparison (e.g., 1 hour).

Select a deviation threshold (e.g., 1.0%).

The table will show:

Each altcoin’s % change

BTC’s % change

The delta (deviation) vs BTC

Red highlights indicate alts whose deviation exceeded the threshold.

When at least one alt lags beyond your threshold, the indicator can trigger an alert — helping you capitalize on potential catch-up trades.

Please provide any feedback on it.

Multiple MAsHere's a well-written description in English for your "Multiple MAs" indicator that you can use when publishing on TradingView. It’s concise, professional, and highlights the key features of the indicator while explaining its purpose for traders.

---

### Multiple MAs Indicator

#### Overview

The **Multiple MAs** indicator is a versatile and straightforward tool designed to help traders visualize price trends using multiple Simple Moving Averages (SMAs) on a single chart. By plotting six SMAs with customizable lengths (MA5, MA10, MA20, MA50, MA100, and MA200), this indicator provides a clear view of short-term, medium-term, and long-term trends, making it ideal for trend-following strategies, crossover analysis, and identifying potential support/resistance levels.

#### Features

- **Customizable MA Lengths**: Adjust the periods of all six moving averages (MA5, MA10, MA20, MA50, MA100, MA200) to suit your trading style and timeframe.

- **Distinct Visuals**: Each MA is plotted with a unique color and line width for easy identification:

- MA5 (Dodger Blue, 1px)

- MA10 (Green, 1px)

- MA20 (Red, 2px)

- MA50 (Purple, 3px)

- MA100 (Gray, 3px)

- MA200 (White, 3px)

- **Overlay on Price Chart**: The indicator overlays directly on the price chart, allowing for seamless integration with other technical analysis tools.

- **High Precision**: Displays values with 8-decimal precision, ensuring accuracy for assets with small price movements (e.g., forex pairs or cryptocurrencies).

#### How to Use

1. **Trend Identification**: Use the longer MAs (e.g., MA100, MA200) to determine the overall trend direction. If the price is above these MAs, the trend is likely bullish; if below, it’s likely bearish.

2. **Crossover Signals**: Look for crossovers between shorter MAs (e.g., MA5 crossing MA20) for potential entry or exit signals. For example:

- A bullish signal occurs when a shorter MA crosses above a longer MA.

- A bearish signal occurs when a shorter MA crosses below a longer MA.

3. **Support and Resistance**: MAs often act as dynamic support or resistance levels. Watch for price reactions around these lines, especially the MA50, MA100, and MA200.

4. **Divergence Analysis**: Compare the slope of different MAs to identify potential trend reversals or weakening momentum.

#### Settings

- **MA5 Length**: Default is 5 bars.

- **MA10 Length**: Default is 10 bars.

- **MA20 Length**: Default is 20 bars.

- **MA50 Length**: Default is 50 bars.

- **MA100 Length**: Default is 100 bars.

- **MA200 Length**: Default is 200 bars.

#### Best Practices

- **Timeframe**: This indicator works on any timeframe but is particularly effective on daily, 4-hour, and 1-hour charts for swing trading or trend-following strategies.

- **Combine with Other Tools**: Pair the Multiple MAs with other indicators like RSI, MACD, or volume analysis to confirm signals and avoid false breakouts.

- **Adjust for Volatility**: For highly volatile assets, consider increasing the MA lengths to reduce noise and focus on broader trends.

#### Notes

- The indicator is lightweight and optimized for performance, ensuring it runs smoothly even on lower timeframes.

- Colors and line widths are pre-set for clarity but can be customized in the indicator settings if needed.

#### Credits

Created by kosar_v. Feedback and suggestions are welcome to improve this tool for the TradingView community!

Regime Filter IndicatorRegime Filter – Crypto Market Trend Indicator

📊 Overview

The Regime Filter is a powerful market analysis indicator designed specifically for crypto trading. It helps traders identify whether the market is in a bullish or bearish phase by analyzing key assets in the cryptocurrency market, including Bitcoin (BTC), Bitcoin Dominance (BTC.D), and the Altcoin Market (TOTAL3). The indicator compares these assets against their respective Simple Moving Averages (SMA) to determine the overall market regime, allowing traders to make more informed decisions.

🔍 How It Works

The Regime Filter evaluates three main components to determine the market's sentiment:

1. BTC Dominance (BTC.D) vs. 40 SMA (Medium Timeframe)

The Bitcoin Dominance (BTC.D) is compared to its 40-period SMA on a mid-timeframe (e.g.,

1-hour). If BTC.D is below the 40 SMA, it indicates that altcoins are performing well relative

to Bitcoin, suggesting a bullish altcoin market. If BTC.D is above the 40 SMA, Bitcoin is

gaining dominance, indicating a potential bearish phase for altcoins.

2. TOTAL3 Market Cap vs. 100 SMA (Medium Timeframe)

The TOTAL3 index, which tracks the total market capitalization of all cryptocurrencies except

Bitcoin and Ethereum, is compared to its 100-period SMA. A bullish signal occurs when TOTAL3

is above the 100 SMA, indicating strength in altcoins, while a bearish signal occurs when

TOTAL3 is below the 100 SMA, signaling a potential weakness in the altcoin market.

3. BTC Price vs. 200 SMA (Higher Timeframe)

The current Bitcoin price is compared to its 200-period Simple Moving Average (SMA) on a

higher timeframe (e.g., 4-hour). A bullish signal is given when the BTC price is above the 200

SMA, and a bearish signal when it's below.

🟢 Bullish Market Conditions

The market is considered bullish when:

- BTC Dominance (BTC.D) is below the 40 SMA, suggesting altcoins are gaining momentum.

- TOTAL3 Market Cap is above the 100 SMA, signaling strength in the altcoin market.

- BTC price is above the 200 SMA, indicating an uptrend in Bitcoin.

In these conditions, the background turns green 🟢, and a "Bullish" label is displayed on the chart.

🔴 Bearish Market Conditions

The market is considered bearish when:

- BTC Dominance (BTC.D) is above the 40 SMA, indicating Bitcoin is outperforming altcoins.

- TOTAL3 Market Cap is below the 100 SMA, signaling weakness in altcoins.

- BTC price is below the 200 SMA, indicating a downtrend in Bitcoin.

In these conditions, the background turns red 🔴, and a "Bearish" label appears on the chart.

⚙ Customization Options

- The Regime Filter offers flexibility for traders:

- Enable or Disable Specific SMAs: Customize the indicator by enabling or disabling the 200 SMA for Bitcoin, the 40 SMA for BTC Dominance, and the 100 SMA for TOTAL3.

- Adjust Timeframes: Choose the timeframes for each of the moving averages to suit your preferred trading strategy.

- Real-Time Data Adjustments: The indicator updates in real-time to reflect current market conditions, ensuring timely analysis.

📈 Best Use Cases

- Trend Confirmation: The Regime Filter is ideal for confirming the market's overall trend,

helping traders to align their positions with the dominant market sentiment.

- Trade Entry/Exit Signals: Use the indicator to identify favorable entry or exit points based on

whether the market is in a bullish or bearish phase.

- Market Overview: Gain a quick understanding of the broader crypto market, with a focus on

Bitcoin and altcoins, to make more strategic decisions.

⚠️ Important Notes

Trend-Following Indicator: The Regime Filter is a trend-following tool, meaning it works best in strong trending markets. It may not perform well in choppy, sideways markets.

Risk Management: This indicator is designed to assist in identifying market trends, but it does not guarantee profits. Always apply sound risk management strategies and use additional indicators when making trading decisions.

Not a Profit Guarantee: While this indicator can help identify potential market trends, no trading tool or strategy guarantees profits. Please trade responsibly and ensure that your decisions are based on comprehensive analysis and risk tolerance.

Spot - Fut spread v2"Spot - Fut Spread v2"

indicator is designed to track the difference between spot and futures prices on various exchanges. It automatically identifies the corresponding instrument (spot or futures) based on the current symbol and calculates the spread between the prices. This tool is useful for analyzing the delta between spot and futures markets, helping traders assess arbitrage opportunities and market sentiment.

Key Features:

- Automatic detection of spot and futures assets based on the current chart symbol.

- Flexible asset selection: the ability to manually choose the second asset if automatic selection is disabled.

- Spread calculation between futures and spot prices.

- Moving average of the spread for smoothing data and trend analysis.

Flexible visualization:

- Color indication of positive and negative spread.

- Adjustable background transparency.

- Text label displaying the current spread and moving average values.

- Error alerts in case of invalid data.

How the Indicator Works:

- Determines whether the current symbol is a futures contract.

- Based on this, selects the corresponding spot or futures symbol.

- Retrieves price data and calculates the spread between them.

- Displays the spread value and its moving average.

- The chart background color changes based on the spread value (positive or negative).

- In case of an error, the indicator provides an alert with an explanation.

Customization Parameters:

-Exchange selection: the ability to specify a particular exchange from the list.

- Automatic pair selection: enable or disable automatic selection of the second asset.

- Moving average period: user-defined.

- Colors for positive and negative spread values.

- Moving average color.

- Background transparency.

- Background coloring source (based on spread or its moving average).

Application:

The indicator is suitable for traders who analyze the difference between spot and futures prices, look for arbitrage opportunities, and assess the premium or discount of futures relative to the spot market.

Crypto Strategy SUSDT 10 minThis strategy is designed to trade the **SUSDT** pair on a **10-minute time frame**, using a combination of an Exponential Moving Average (EMA) and percentage-based Stop Loss (SL) and Take Profit (TP) levels.

### How the strategy works:

1. **EMA Calculation**:

- The strategy calculates a 24-period Exponential Moving Average (EMA) based on the closing price.

- This EMA serves as the primary trend indicator.

2. **Entry Conditions**:

- **Long Position**: A long position is entered when the closing price is above the EMA and the opening price is below the EMA. This indicates a potential upward trend.

- **Short Position**: A short position is entered when the closing price is below the EMA and the opening price is above the EMA. This indicates a potential downward trend.

3. **Stop Loss and Take Profit**:

- Both Stop Loss (SL) and Take Profit (TP) are calculated based on the entry price of the position.

- **For Long Positions**:

- Stop Loss is set as a percentage below the entry price.

- Take Profit is set as a percentage above the entry price.

- **For Short Positions**:

- Stop Loss is set as a percentage above the entry price.

- Take Profit is set as a percentage below the entry price.

- The percentage values for SL and TP can be adjusted in the strategy's settings (default: SL = 2%, TP = 4%).

4. **Exit Conditions**:

- The position is closed automatically when either the Stop Loss or Take Profit level is reached.

5. **Visualization**:

- The 24-period EMA is plotted on the chart as a blue line, helping visualize the trend direction.

### Key Features:

- **Pair and Time Frame**: The strategy is optimized for the SUSDT pair on a 10-minute time frame.

- **Customizable Parameters**: Users can adjust the Stop Loss and Take Profit percentages to suit their risk tolerance and trading style.

- **Trend-Following Approach**: The strategy uses the EMA to identify and follow the current market trend.

This strategy is simple yet effective for capturing trends while managing risk through predefined Stop Loss and Take Profit levels.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

GRID EXTENSIONGRID EXTENSION

Overview

The GRID EXTENSION is a simple grid-based indicator for TradingView, built with Pine Script v6. It plots horizontal price levels starting from a user-defined anchor price, with spacing set by a tick increment. Use it to identify key support, resistance, or price zones on charts for Crypto, Forex, or Futures.

Key Features

Custom Grid Levels: Plot up to 22 levels (e.g., 0, 0.25, 1.25, -2.50) with options to show/hide, set values, and choose colors.

Market-Specific Tick Increments: Select your asset type (Crypto, Forex, Futures) and choose from a range of tick increments tailored for each market:

Crypto: 1 to 5000 ticks (e.g., 100 ticks = $0.001 on ADA/USD, 5000 ticks = $50 on BTC/USD).

Forex: 5 to 5000 ticks (e.g., 100 ticks = 1 pip on EUR/USD, 5000 ticks = 50 pips).

Futures: 1 to 2500 ticks (e.g., 25 ticks = 6.25 points on E-mini S&P 500, $312.50 per contract).

Visual Options:

Extend lines to the right.

Show price and level labels (as values or percentages).

Place labels on the left or right.

Adjust background transparency for filled areas between levels.

How to Use

Set Asset Type: Choose "Crypto," "Forex," or "Futures" to match your chart.

Set Anchor Price: Enter a starting price for the grid.

Pick Tick Increment: Select a tick increment from the dropdown, following the guidance for your asset type (see Key Features).

Customize Levels: Turn levels on/off, set values, and pick colors.

Add to Chart: Apply the indicator to see the grid on your chart.

Tips

Use levels to mark support/resistance zones for entries or exits.

Extend lines to project future price zones.

Choose smaller increments (e.g., 5 ticks) for scalping, or larger ones (e.g., 1000 ticks) for swing trading.

Combine with indicators like moving averages for better signals.

Settings

Asset Type: Select "Crypto," "Forex," or "Futures" (default: "Crypto").

Anchor Price: Starting price for the grid (default: 0.0).

Tick Increment: Space between levels (options: 1, 5, 10, 25, 50, 100, 250, 500, 1000, 2500, 5000). Choose based on asset type.

Extend Right: Extend lines to the right (default: true).

Show Prices: Show price labels (default: true).

Show Levels: Show level values or percentages (default: true).

Format: Display levels as "Values" or "Percent" (default: "Values").

Labels Position: Place labels on "Left" or "Right" (default: "Left").

Background Transparency: Set transparency for filled areas (default: 100, range 0-100).

Level Options: Enable/disable levels, set values, and choose colors.

Notes

Set the anchor price to a key level (like a recent high or low) for best results.

Check the tick increment tooltip to ensure the spacing suits your market type.

Works on any chart, best for clear price trends or ranges.

Acknowledgments

Made with Pine Script v6 for TradingView. This is v1.0—feedback welcome for future updates!

Ivan Gomes StrategyIG Signals+ - Ivan Gomes Strategy

This script is designed for scalping and binary options trading, generating buy and sell signals at the beginning of each candle. Although it is mainly optimized for short-term operations, it can also be used for medium and long-term strategies with appropriate adjustments.

How It Works

• The indicator provides buy or sell signals at the start of the candle, based on a statistical probability of candle patterns, depending on the timeframe.

• It is essential to enter the trade immediately after the signal appears and exit at the end of the same candle.

• If the first operation results in a loss (Loss), the script will send another trade signal at the start of the next candle. However, if the first trade results in a win (Gain), no new signal will be generated.

• The signals follow cycles of 3 candles, regardless of the timeframe. However, if a Doji candle appears, the cycle is interrupted, and no signals will be generated until the next valid cycle starts.

• The strategy consists of up to two trades per cycle: if the first trade is not successful, the second trade serves as an additional attempt to recover.

Key Points to Consider

1. Avoid trading in sideways markets – If price levels do not fluctuate significantly, the accuracy of the signals may decrease.

2. Trade in the direction of the trend – Using Ichimoku clouds or other trend indicators can help confirm trend direction and improve signal reliability. If the market is in an uptrend (bullish trend) and the indicator generates a sell signal, the most prudent decision would be to wait for a buy signal that aligns with the main trend. The same applies to downtrends, where buy signals may be riskier.

These decisions should be based on chart reading and supported by other technical analysis tools, such as support and resistance levels, which indicate zones where price might face obstacles or reverse direction. Additionally, Fibonacci retracement levels can help identify possible pullback points within a trend. Moving averages are also useful for visualizing the general market direction and confirming whether an indicator signal aligns with the overall price structure. Combining these tools can increase trade accuracy and prevent unnecessary trades against the main trend, reducing risks.

3. Works based on probability statistics – The algorithm analyzes candle formations and their statistical probabilities depending on the timeframe to optimize trade entries.

4. Best suited for scalping and binary options – This strategy performs best in 1-minute and 5-minute timeframes, allowing for multiple trades throughout the day.

Technical Details

• The script detects the candle cycle and assigns an index to each candle to identify patterns and possible reversals.

• It recognizes reference candles, stores their colors, and compares them with subsequent candles to determine if a signal should be triggered.

• Doji candle rules are implemented to avoid false signals in indecisive market conditions. When a Doji appears, the script does not generate signals for that cycle.

• The indicator displays visual alerts and notifications, ensuring fast execution of trades.

Disclaimer

The IG Signals+ indicator was created to assist traders who struggle to analyze the market by providing objective trade signals. However, no strategy is foolproof, and this script does not guarantee profits.

Trading involves significant financial risk, and users should test it in a demo account before trading with real money. Proper risk management is crucial for long-term success.

Autocorrelation Price Forecasting [The Quant Science]Discover how to predict future price movements using autocorrelation and linear regression models to identify potential trading opportunities.

An advanced model to predict future price movements using autocorrelation and linear regression. This script helps identify recurring market cycles and calculates potential gains, with clear visual signals for quick and informed decisions.

Main function

This script leverages an autocorrelation model to estimate the future price of an asset based on historical price relationships. It also integrates linear regression on percentage returns to provide more accurate predictions of price movements.

Insights types

1) Red label on a green candle: Bearish forecast and swing trading opportunity.

2) Red label on a red candle: Bearish forecast and trend-following opportunity.

3) Green label on a red candle: Bullish forecast and swing trading opportunity.

4) Green label on a green candle: Bullish forecast and trend-following opportunity.

IMPORTANT!

The indicator displays a future price forecast. When negative, it estimates a future price drop.

When positive, it estimates a future price increase.

Key Features

Customizable inputs

Analysis Length: number of historical bars used for autocorrelation calculation. Adjustable between 1 and 200.

Forecast Colors: customize colors for bullish and bearish signals.

Visual insights

Labels: hypothetical gains or losses are displayed as labels above or below the bars.

Dynamic coloring: bullish (green) and bearish (red) signals are highlighted directly on the chart.

Forecast line: A continuous line is plotted to represent the estimated future price values.

Practical applications

Short-term Trading: identify repetitive market cycles to anticipate future movements.

Visual Decision-making: colored signals and labels make it easier to visualize potential profit or loss for each trade.

Advanced Customization: adjust the data length and colors to tailor the indicator to your strategies.

Limitations

Prediction price models have some limitations. Trading decisions should be made with caution, considering additional market factors and risk management strategies.

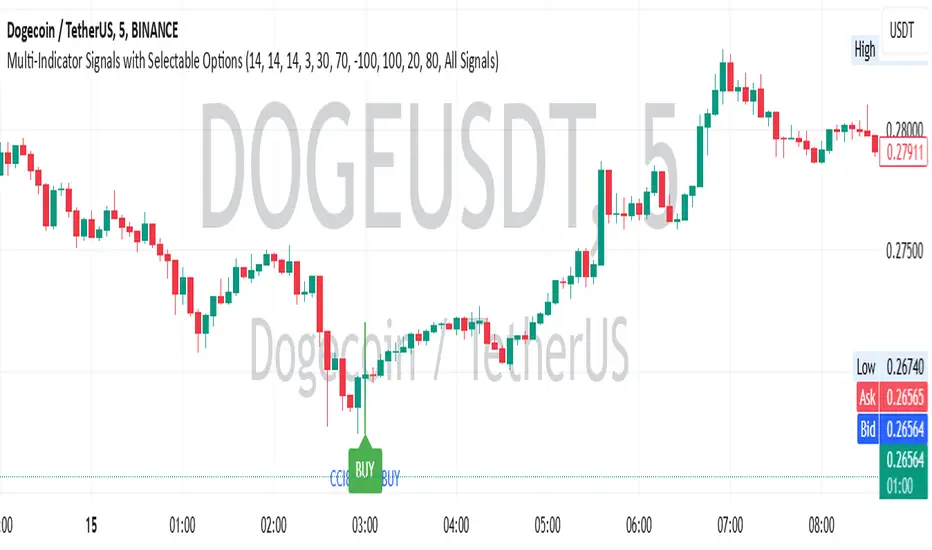

Multi-Indicator Signals with Selectable Options by DiGetMulti-Indicator Signals with Selectable Options

Script Overview

This Pine Script is a multi-indicator trading strategy designed to generate buy/sell signals based on combinations of popular technical indicators: RSI (Relative Strength Index) , CCI (Commodity Channel Index) , and Stochastic Oscillator . The script allows you to select which combination of signals to display, making it highly customizable and adaptable to different trading styles.

The primary goal of this script is to provide clear and actionable entry/exit points by visualizing buy/sell signals with arrows , labels , and vertical lines directly on the chart. It also includes input validation, dynamic signal plotting, and clutter-free line management to ensure a clean and professional user experience.

Key Features

1. Customizable Signal Types

You can choose from five signal types:

RSI & CCI : Combines RSI and CCI signals for confirmation.

RSI & Stochastic : Combines RSI and Stochastic signals.

CCI & Stochastic : Combines CCI and Stochastic signals.

RSI & CCI & Stochastic : Requires all three indicators to align for a signal.

All Signals : Displays individual signals from each indicator separately.

This flexibility allows you to test and use the combination that works best for your trading strategy.

2. Clear Buy/Sell Indicators

Arrows : Buy signals are marked with upward arrows (green/lime/yellow) below the candles, while sell signals are marked with downward arrows (red/fuchsia/gray) above the candles.

Labels : Each signal is accompanied by a label ("BUY" or "SELL") near the arrow for clarity.

Vertical Lines : A vertical line is drawn at the exact bar where the signal occurs, extending from the low to the high of the candle. This ensures you can pinpoint the exact entry point without ambiguity.

3. Dynamic Overbought/Oversold Levels

You can customize the overbought and oversold levels for each indicator:

RSI: Default values are 70 (overbought) and 30 (oversold).

CCI: Default values are +100 (overbought) and -100 (oversold).

Stochastic: Default values are 80 (overbought) and 20 (oversold).

These levels can be adjusted to suit your trading preferences or market conditions.

4. Input Validation

The script includes built-in validation to ensure that oversold levels are always lower than overbought levels for each indicator. If the inputs are invalid, an error message will appear, preventing incorrect configurations.

5. Clean Chart Design

To avoid clutter, the script dynamically manages vertical lines:

Only the most recent 50 buy/sell lines are displayed. Older lines are automatically deleted to keep the chart clean.

Labels and arrows are placed strategically to avoid overlapping with candles.

6. ATR-Based Offset

The vertical lines and labels are offset using the Average True Range (ATR) to ensure they don’t overlap with the price action. This makes the signals easier to see, especially during volatile market conditions.

7. Scalable and Professional

The script uses arrays to manage multiple vertical lines, ensuring scalability and performance even when many signals are generated.

It adheres to Pine Script v6 standards, ensuring compatibility and reliability.

How It Works

Indicator Calculations :

The script calculates the values of RSI, CCI, and Stochastic Oscillator based on user-defined lengths and smoothing parameters.

It then checks for crossover/crossunder conditions relative to the overbought/oversold levels to generate individual signals.

Combined Signals :

Depending on the selected signal type, the script combines the individual signals logically:

For example, a "RSI & CCI" buy signal requires both RSI and CCI to cross into their respective oversold zones simultaneously.

Signal Plotting :

When a signal is generated, the script:

Plots an arrow (upward for buy, downward for sell) at the corresponding bar.

Adds a label ("BUY" or "SELL") near the arrow for clarity.

Draws a vertical line extending from the low to the high of the candle to mark the exact entry point.

Line Management :

To prevent clutter, the script stores up to 50 vertical lines in arrays (buy_lines and sell_lines). Older lines are automatically deleted when the limit is exceeded.

Why Use This Script?

Versatility : Whether you're a scalper, swing trader, or long-term investor, this script can be tailored to your needs by selecting the appropriate signal type and adjusting the indicator parameters.

Clarity : The combination of arrows, labels, and vertical lines ensures that signals are easy to spot and interpret, even in fast-moving markets.

Customization : With adjustable overbought/oversold levels and multiple signal options, you can fine-tune the script to match your trading strategy.

Professional Design : The script avoids clutter by limiting the number of lines displayed and using ATR-based offsets for better visibility.

How to Use This Script

Add the Script to Your Chart :

Copy and paste the script into the Pine Editor in TradingView.

Save and add it to your chart.

Select Signal Type :

Use the "Signal Type" dropdown menu to choose the combination of indicators you want to use.

Adjust Parameters :

Customize the lengths of RSI, CCI, and Stochastic, as well as their overbought/oversold levels, to match your trading preferences.

Interpret Signals :

Look for green arrows and "BUY" labels for buy signals, and red arrows and "SELL" labels for sell signals.

Vertical lines will help you identify the exact bar where the signal occurred.

Tips for Traders

Backtest Thoroughly : Before using this script in live trading, backtest it on historical data to ensure it aligns with your strategy.

Combine with Other Tools : While this script provides reliable signals, consider combining it with other tools like support/resistance levels or volume analysis for additional confirmation.

Avoid Overloading the Chart : If you notice too many signals, try tightening the overbought/oversold levels or switching to a combined signal type (e.g., "RSI & CCI & Stochastic") for fewer but higher-confidence signals.

Crypto Market Cap Momentum Analyzer (AiBitcoinTrend)The Crypto Market Cap Momentum Analyzer (AiBitcoinTrend) is a robust tool designed to uncover trading opportunities by blending market cap analysis and momentum dynamics. Inspired by research-backed quantitative strategies, this indicator helps traders identify trend-following and mean-reversion setups in the cryptocurrency market by evaluating recent performance and market cap size.

This indicator classifies cryptocurrencies into market cap quintiles and ranks them based on their 2-week momentum. It then suggests potential trades—whether to go long, anticipate reversals, or simply hold—based on the crypto's market cap group and momentum trends.

👽 How the Indicator Works

👾 Market Cap Classification

The indicator categorizes cryptocurrencies into one of five market cap groups based on user-defined inputs:

Large Cap: Highest market cap tier

Upper Mid Cap: Second highest group

Mid Cap: Middle-tier market caps

Lower Mid Cap: Slightly below the mid-tier

Small Cap: Lowest market cap tier

This classification dynamically adjusts based on the provided market cap data, ensuring that you’re always working with a representative market structure.

👾 Momentum Calculation

By default, the indicator uses a 2-week momentum measure (e.g., a 14-day lookback when set to daily). It compares a cryptocurrency’s current price to its price 14 bars ago, thereby quantifying its short-term performance. Users can adjust the momentum period and rebalance period to capture shorter or longer-term trends depending on their trading style.

👾 Dynamic Ranking and Trade Suggestions

After assigning cryptos to size quintiles, the indicator sorts them by their momentum within each quintile. This two-step process results in:

Long Trade: For smaller market cap groups (Small, Lower Mid, Mid Cap) that have low (bottom-quintile) momentum, anticipating a trend continuation or breakout.

Reversal Trade: For the largest market cap group (Large Cap) that shows low momentum, expecting a mean-reversion back to equilibrium.

Hold: In scenarios where the coin’s momentum doesn’t present a strong contrarian or trend-following signal.

👽 Applications

👾 Trend-Following in Smaller Caps: Identify small or mid-cap cryptos with low momentum that might be poised for a breakout or sustained trend.

👾 Mean-Reversion in Large Caps: Pinpoint large-cap cryptocurrencies experiencing a temporary lull in performance, potentially ripe for a rebound.

👽 Why It Works in Crypto

The cryptocurrency market is heavily driven by retail investor sentiment and volatility. Research shows that:

Small-Cap Cryptos: Tend to experience higher volatility and speculative trends, making them ideal for momentum trades.

Large-Cap Cryptos: Exhibit more predictable behavior, making them suitable for mean-reversion strategies when momentum is low.

This indicator captures these dynamics to give traders a strategic edge in identifying both momentum and reversal opportunities.

👽 Indicator Settings

👾 Rebalance Period: The frequency at which momentum and trade suggestions are recalculated (Daily, Weekly, Monthly).

Shorter Periods (Daily): Fast updates, suitable for short-term trades, but more noise.

Longer Periods (Weekly/Monthly): Smoother signals, ideal for swing trading and more stable trends.

👾 Momentum Period: The lookback period for momentum calculation (default is 14 bars).

Shorter Periods: More responsive but prone to noise.

Longer Periods : Reflects broader trends, reducing sensitivity to short-term fluctuations.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Cryptocurrency SentimentOverview

This script focuses on calculating and visualizing the sentiment difference between LONG positions and SHORT positions for a selected cryptocurrency pair on the Bitfinex exchange. It provides a clean and clear visual representation of the sentiment, helping traders analyze market behavior.

Key Features

Dynamic Symbol Selection:

The script automatically detects the cryptocurrency symbol from the chart (syminfo.basecurrency) and dynamically constructs the LONGS and SHORTS ticker symbols.

Works seamlessly for pairs like BTCUSD, ETHUSD, and others available on Bitfinex.

Sentiment Calculation:

The sentiment difference is calculated as:

Sentiment Difference=−1×(100− SHORTS/LONGS ×100)

LONGS : The total number of long positions.

SHORTS : The total number of short positions.

If SHORTS is 0, the value is safely skipped to avoid division errors.

Color Coding:

The script visually highlights the sentiment difference:

Green Line: Indicates that LONG positions are dominant (bullish sentiment).

Red Line: Indicates that SHORT positions are dominant (bearish sentiment).

Zero Reference Line:

A gray horizontal line at 0 helps users quickly identify the transition between bullish (above zero) and bearish (below zero) sentiment.

How It Works

Fetching Data:

The script uses request.security to fetch LONGS and SHORTS data at the current chart timeframe (timeframe.period) for the dynamically generated Bitfinex tickers.

Handling Data:

Missing or invalid data (NaN) is filtered out to prevent errors.

Extreme spikes or irregular values are safely avoided.

Visualization:

The sentiment difference is plotted with dynamic color coding:

Green when LONGS > SHORTS (bullish sentiment).

Red when SHORTS > LONGS (bearish sentiment).

Benefits

Market Sentiment Insight: Helps traders quickly identify if the market is leaning towards bullish or bearish sentiment based on actual LONG and SHORT position data.

Dynamic and Adaptive: Automatically adjusts to the selected cryptocurrency symbol on the chart.

Clean Visualization: Focuses solely on sentiment difference with color-coded signals, making it easy to interpret.

Best Use Cases

Trend Confirmation: Use the sentiment difference to confirm trends during bullish or bearish moves.

Market Reversals: Identify potential reversals when sentiment shifts from positive (green) to negative (red) or vice versa.

Sentiment Monitoring: Monitor the overall market bias for cryptocurrencies like BTC, ETH, XRP, etc., in real-time.

Sample Chart Output

Above Zero → Green Line: Bullish sentiment dominates.

Below Zero → Red Line: Bearish sentiment dominates.

Zero Line → Transition point for shifts in sentiment.

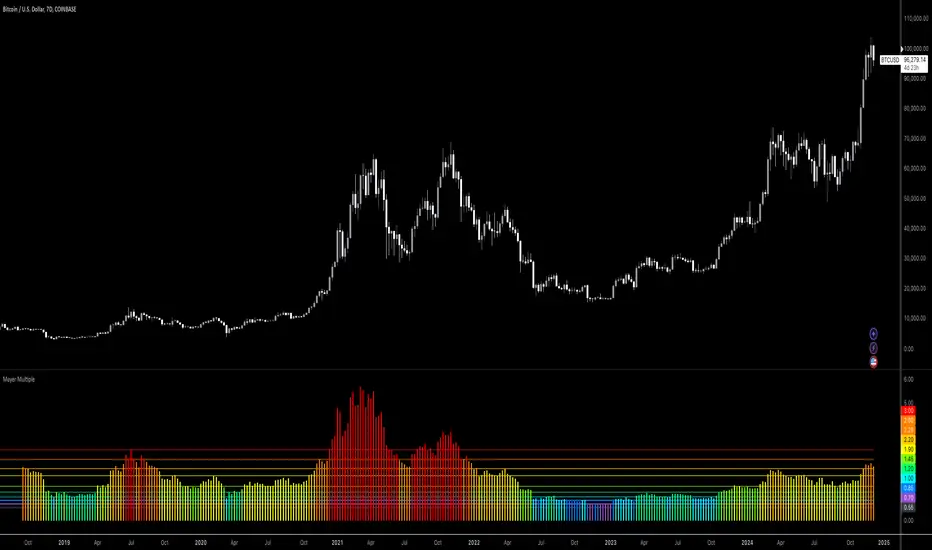

Bitcoin: Mayer MultipleMayer Multiple Indicator

The Mayer Multiple is a powerful tool designed to help traders assess market conditions and identify optimal buying or selling opportunities. It calculates the ratio between the current price and its 200-day simple moving average (SMA), visualizing key thresholds that indicate value zones, caution areas, and overheated markets.

Key Features:

Dynamic Market Zones: Clearly marked levels like "Smash Buy," "Boost DCA," and "Extreme Euphoria" to guide your trading decisions.

Customizable Input: Adjust the SMA length to fit your strategy.

Color-Coded Signals: Intuitive visualization of market sentiment for quick analysis.

Comprehensive Thresholds: Historical insights into price behavior with plotted reference levels based on probabilities.

This indicator is ideal for traders aiming to enhance their long-term strategies and improve decision-making in volatile markets. Use it to gain an edge in identifying potential turning points and managing risk effectively.

DCA Valuation & Unrealized GainsThis Pine Script for TradingView calculates and visualizes the relationship between a Dollar Cost Average (DCA) price and the All-Time High (ATH) price for over 50 different cryptocurrencies. Here's what it does:

1. Inputs for DCA Prices:

- Users can manually input DCA prices for specific cryptocurrencies (e.g., BTC, ETH, BNB).

2. Dynamic ATH Calculation:

- Dynamically calculates the ATH price for the current asset using the highest price in the chart's loaded data and persists this value across bars.

3. Percentage Change from DCA to ATH:

- Computes the percentage gain from the DCA price to the ATH price.

4. Visualizations:

- Draws a line at the DCA price and the ATH price, both extended to the right.

- Adds an arrow pointing from the DCA price to the ATH, offset by 10 bars into the future.

- Displays labels for:

- The percentage gain from DCA to ATH.

- "No DCA Configured" if no valid DCA price is set for the asset.

5. Color Coding:

- Labels and arrows are color-coded to indicate positive or negative percentage changes:

- Green for gains.

- Red for losses.

6. Adaptability:

- The script dynamically adjusts to the current asset based on its ticker and uses the corresponding DCA price.

This functionality provides traders with clear insights into their investment's performance relative to its ATH, aiding in decision-making.

-----

To add a new asset to the script:

1. Define the DCA Input: Add a new input for the asset's DCA price using the `input.float` function. For example:

dcaPriceNEW = input.float(title="NEW DCA Price", defval=0.1, tooltip="Set the DCA price for NEW")

2. Add the Asset Logic: Include a conditional check for the new asset in the ticker matching logic:

if str.contains(currentAsset, "NEW") and dcaPriceNEW != 0

dcaPrice := dcaPriceNEW

Where NEW is the ticker symbol of the asset you're adding.

NOTE: SOLO had to be put before SOL because otherwise the indicator was pulling the DCA price from SOL even on the SOLO chart. If you have a similar issue, try that fix.

Adding an asset requires only these two changes. Once done, the script dynamically incorporates the new asset into its calculations and visualizations.

Cryptocurrency StrengthMulti-Currency Analysis: Monitor up to 19 different currencies simultaneously, including major pairs like USD, EUR, JPY, and GBP, as well as emerging market currencies such as CNY, INR, and BRL.

Customizable Display: Easily toggle the visibility of each currency and personalize their colors to suit your preferences, allowing for a tailored analysis experience.

Real-Time Strength Measurement: The indicator calculates and displays the relative strength of each currency in real-time, helping you identify potential trends and trading opportunities.

Clear Visual Representation: With color-coded lines and a dynamic legend, the indicator presents complex currency relationships in an easy-to-understand format.

Advantages

Comprehensive Market View: Gain insights into the broader forex market dynamics by analyzing multiple currencies at once.

Trend Identification: Quickly spot strong and weak currencies, aiding in the identification of potential trending pairs.

Divergence Detection: Use the indicator to identify divergences between currency strength and price action, potentially signaling reversals or continuation patterns.

Flexible Time Frames: Apply the indicator across various time frames to align with your trading strategy, from intraday to long-term analysis.

Enhanced Decision Making: Make more informed trading decisions by understanding the relative strength of currencies involved in your trades.

Unique Qualities

TSI-Based Calculations: Utilizes the True Strength Index for a more nuanced and responsive measure of currency strength compared to simple price-based indicators.

Adaptive Legend: The indicator features a dynamic legend that updates automatically based on the selected currencies, ensuring a clutter-free and relevant display.

Emerging Market Inclusion: Unlike many standard currency strength indicators, this tool includes a wide range of emerging market currencies, providing a truly global perspective.

Whether you're a seasoned forex trader or just starting out, this Currency Strength Indicator offers valuable insights that can complement your existing strategy and potentially improve your trading outcomes. Its combination of comprehensive analysis, customization options, and clear visualization makes it an essential tool for navigating the complex world of currency trading.