DR Oscillator 8 * Measures price deviation: Calculates the percentage difference between the closing price and a simple moving average.

* Defines upper and lower limits: User-defined upper and lower limits determine overbought and oversold conditions.

* Signal line: A simple moving average of the deviation is plotted as a signal line.

* Deviation smoothing (optional): The deviation can be smoothed using a moving average to create a smoother line.

* Additional signal line (optional): An additional signal line can be added for further analysis.

* Visual representation: The oscillator is plotted with different colors to indicate overbought, oversold, or neutral conditions.

* Background coloring: The background color changes based on the oscillator's value to provide visual cues for buy or sell signals.

In summary:

The DR Oscillator helps traders identify potential buying and selling opportunities by measuring the extent to which a security's price has deviated from its moving average. When the oscillator moves above the upper limit, it suggests that the asset may be overbought and due for a price correction. Conversely, when it moves below the lower limit, it may indicate an oversold condition and a potential buying opportunity.

However, it's important to note that the DR Oscillator is just one tool and should be used in conjunction with other technical indicators and fundamental analysis for more accurate trading decisions.

Cycles

rsi wf breakoutRSI Breakout Asif

RSI Breakout Asif Indicator

Overview:

The RSI Breakout Asif indicator is a custom script designed to analyze and highlight potential

breakout points using the Relative Strength Index (RSI) combined with Williams Fractals. This

indicator is specifically developed for traders who want to identify key momentum shifts in the

market.

Features:

1. RSI Analysis:

- The RSI is calculated using a user-defined length and price source.

- Horizontal lines are plotted at levels 70 (overbought), 50 (neutral), and 30 (oversold) to visually

aid decision-making.

2. Williams Fractals on RSI:

- Detects fractal highs and lows based on RSI values.

- Highlights these fractal points with dynamic, symmetrical lines for better visibility.

3. Customization:

- Users can adjust the RSI length and price source for personalized analysis.

- Fractal settings (left and right bar length) are also adjustable, making the indicator versatile for

different trading styles.

4. Visual Enhancements:

- Fractal highs are marked in red, while fractal lows are marked in green.

Asif - Page 1

RSI Breakout Asif

- Precise line placement ensures clarity and reduces chart clutter.

5. Practical Utility:

- Use the fractal breakout signals in conjunction with other technical indicators for enhanced

decision-making.

Usage:

- Add the RSI Breakout Asif indicator to your TradingView chart.

- Adjust the settings according to your trading strategy.

- Observe the RSI values and fractal points to identify potential breakout zones.

Disclaimer:

This indicator is a technical analysis tool and should be used in combination with other analysis

methods. It does not guarantee profitable trades.

Watermarked by Asif.

Asif - Page 2

Swing & Day Trading Strategy dddddThis TradingView Pine Script is designed for swing and day trading, incorporating multiple technical indicators and tools to enhance decision-making. It calculates and plots exponential moving averages (EMAs) for 5, 9, 21, 50, and 200 periods to identify trends and crossovers. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) provide momentum and overbought/oversold signals. The script dynamically identifies and marks support and resistance levels based on recent highs and lows, while also detecting and labeling key candlestick patterns such as bullish and bearish engulfing, doji, and hammer candles. Bullish and bearish signals are highlighted on the chart with green and red backgrounds, respectively, and alerts are generated to notify traders of these conditions. All visualizations, including EMAs, support/resistance lines, and candlestick labels, are overlaid directly on the stock chart for easy interpretation. This comprehensive approach assists traders in spotting potential trading opportunities effectively.

Edufx AMD~Accumulation, Manipulation, DistributionEdufx AMD Indicator

This indicator visualizes the market cycles using distinct phases: Accumulation, Manipulation, Distribution, and Reversal. It is designed to assist traders in identifying potential entry points and understanding price behavior during these phases.

Key Features:

1. Phases and Logic:

-Accumulation Phase: Highlights the price range where market accumulation occurs.

-Manipulation Phase:

- If the price sweeps below the accumulation low, it signals a potential "Buy Zone."

- If the price sweeps above the accumulation high, it signals a potential "Sell Zone."

-Distribution Phase: Highlights where price is expected to expand and establish trends.

-Reversal Phase: Marks areas where the price may either continue or reverse.

2. Weekly and Daily Cycles:

- Toggle the visibility of Weekly Cycles and Daily Cycles independently through the settings.

- These cycles are predefined with precise timings for each phase, based on your selected on UTC-5 timezone.

3. Customizable Appearance:

- Adjust the colors for each phase directly in the settings to suit your preferences.

- The indicator uses semi-transparent boxes to represent the phases, allowing easy visualization without obstructing the chart.

4. Static Boxes:

- Boxes representing the phases are drawn only once for the visible chart range and do not dynamically delete, ensuring important consistent reference points.

RRS Separator 3This Pine Script indicator, titled "RRS Separator 3", is designed to draw vertical lines on a chart to separate different time frames. Here's a breakdown of its main features:

1.Time Frame Separators: The script draws vertical lines to mark the beginning of 5-minute, 15-minute, 1-hour, and 4-hour intervals on intraday charts.

2.Customizable Appearance: Users can customize the appearance of each time frame's separator lines, including:

Visibility (show/hide)

Color

Line style (solid, dashed, or dotted)

Line width

3.Dynamic Line Drawing: The script calculates the positions for future time frame separators and draws them in advance, extending beyond the current bar.

4.Compatibility: It's designed to work on various intraday time frames, adjusting its behavior based on the chart's current time frame.

5.Efficient Line Management: The script uses arrays to manage the drawn lines, clearing old lines and redrawing them on each update to ensure accuracy and prevent clutter.

6.Time Calculations: It performs various time-related calculations to determine the correct positioning of lines for each time frame.

7.Conditional Drawing: Lines are only drawn if they meet certain conditions (e.g., the chart's time frame is smaller than the separator's time frame).

8.Performance Considerations: The script includes max_bars_back and max_lines_count parameters to manage memory usage and performance.

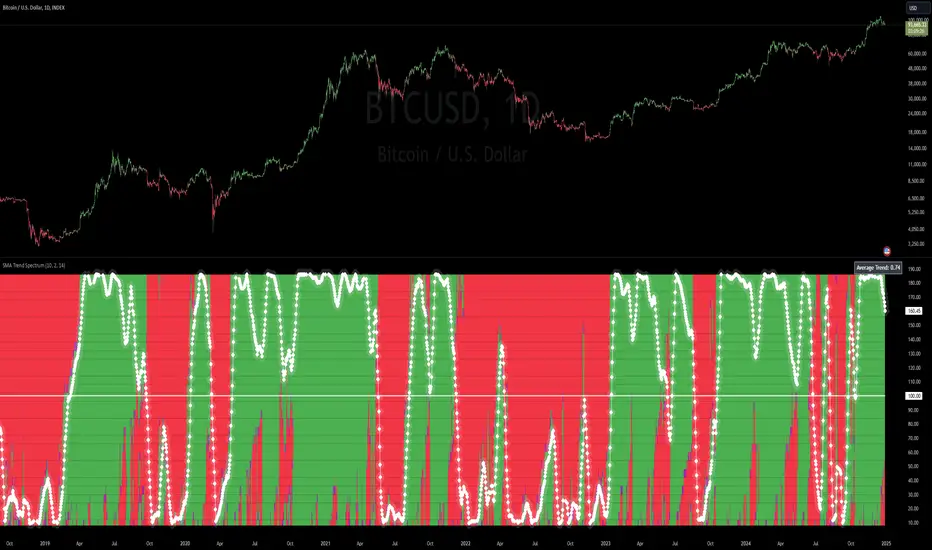

SMA Trend Spectrum [InvestorUnknown]The SMA Trend Spectrum indicator is designed to visually represent market trends and momentum by using a series of Simple Moving Averages (SMAs) to create a color-coded spectrum or heatmap. This tool helps traders identify the strength and direction of market trends across various time frames within one chart.

Functionality:

SMA Calculation: The indicator calculates multiple SMAs starting from a user-defined base period (Starting Period) and increasing by a specified increment (Period Increment). This creates a sequence of moving averages that span from short-term to long-term perspectives.

Trend Analysis: Each segment of the spectrum compares three SMAs to determine the market's trend strength: Bullish (color-coded green) when the current price is above all three SMAs. Neutral (color-coded purple) when the price is above some but not all SMAs. Bearish (color-coded red) when the price is below all three SMAs.

f_col(x1, x2, x3) =>

min = ta.sma(src, x1)

mid = ta.sma(src, x2)

max = ta.sma(src, x3)

c = src > min and src > mid and src > max ? bull : src > min or src > mid or src > max ? ncol : bear

Heatmap Visualization: The indicator plots these trends as a vertical spectrum where each row represents a different set of SMAs, forming a heatmap-like display. The color of each segment in the heatmap directly correlates with market conditions, providing an intuitive view of market sentiment.

Signal Smoothing: Users can choose to smooth the trend signal using either a Simple Moving Average (SMA), Exponential Moving Average (EMA), or leave it as raw data (Signal Smoothing). The length of smoothing can be adjusted (Smoothing Length). The signal is displayed in a scaled way to automatically adjust for the best visual experience, ensuring that the trend is clear and easily interpretable across different chart scales and time frames

Additional Features:

Plot Signal: Optionally plots a line representing the average trend across all calculated SMAs. This line helps in identifying the overall market direction based on the spectrum data.

Bar Coloring: Bars on the chart can be colored according to the average trend strength, providing a quick visual cue of market conditions.

Usage:

Trend Identification: Use the heatmap to quickly assess if the market is trending strongly in one direction or if it's in a consolidation phase.

Entry/Exit Points: Look for shifts in color patterns to anticipate potential trend changes or confirmations for entry or exit points.

Momentum Analysis: The gradient from bearish to bullish across the spectrum can be used to gauge momentum and potentially forecast future price movements.

Notes:

The effectiveness of this indicator can vary based on market conditions, asset volatility, and the chosen SMA periods and increments.

It's advisable to combine this tool with other technical indicators or fundamental analysis for more robust trading decisions.

Disclaimer: Past performance does not guarantee future results. Always use this indicator as part of a broader trading strategy.

[w3ss1] Timeframe SyncThe "Timeframe Sync" indicator provides a comprehensive view of price action across multiple timeframes for a single symbol, allowing traders to analyze market conditions from a multi-timeframe perspective with ease.

Key Features:

Flexible Symbol Selection: Choose between analyzing the symbol of the current chart or select another symbol to monitor.

Customizable Timeframes: Control which timeframes you want to analyze through toggle switches. Choose from 11 different timeframes ranging from 1-minute to Monthly charts, with the ability to customize each one:

1m, 5m, 15m, 30m, 1H, 4H, 8H, 12H, 1D, 1W, 1M

Visual Feedback:

-Candle Close Color: Each timeframe's last closed candle is color-coded. Bullish closes are highlighted in green, bearish in dark shades, and inside candles in orange.

-Bias Indicator: The indicator shows whether the close is "above", "below", or "inside" the previous candle's high/low range, providing insight into the market's momentum.

Table Display: Information is presented in a clear table format:

-The first row shows the symbol being analyzed.

-The second row displays "Candle close" to indicate the relevance of the information below.

-Each subsequent row represents a different timeframe, showing its abbreviation and the bias of the last close.

Conditional Display: Timeframes are only shown if they are relevant to the current chart's timeframe. This ensures that you're not looking at outdated data when on lower timeframes.

Customization:

-Adjust text size, table position, background color, text color, and colors for different candle close scenarios.

Usage:

Ideal for traders who need a quick multi-timeframe analysis without switching charts.

Helps in confirming short-term moves with longer-term trends or spotting divergences across timeframes.

Instructions:

Add the indicator to your chart.

Customize the timeframes you wish to monitor via the toggle switches.

Optionally, select a different symbol if not analyzing the current chart's symbol.

Adjust colors and table settings to your preference.

Observe how price action behaves across different timeframes to make informed trading decisions.

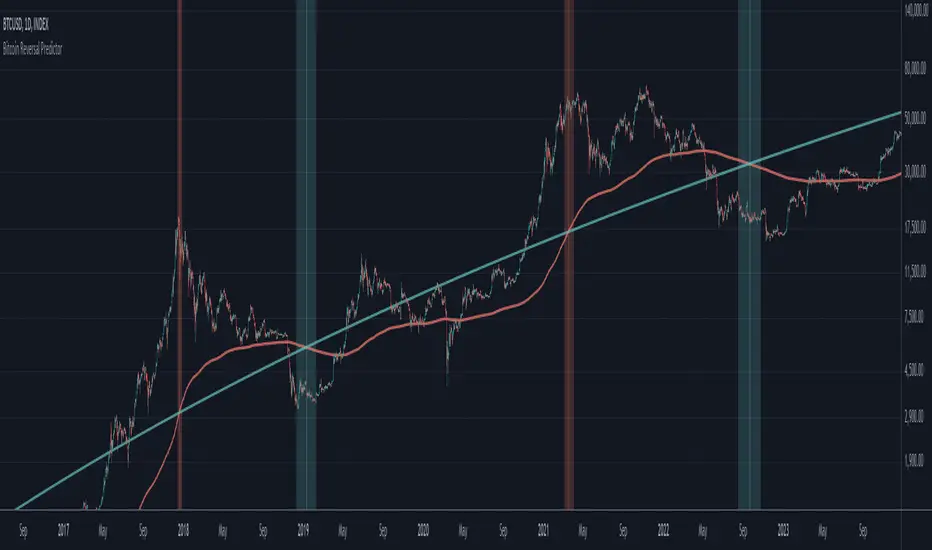

Bitcoin Reversal PredictorOverview

This indicator displays two lines that, when they cross, signal a potential reversal in Bitcoin's price trend. Historically, the high or low of a bull market cycle often occurs near the moment these lines intersect. The lines consist of an Exponential Moving Average (EMA) and a logarithmic regression line fitted to all of Bitcoin's historical data.

Inspiration

The inspiration for this indicator came from the PI Cycle Top indicator, which has accurately predicted past bull market peaks. However, I believe the PI Cycle Top indicator may not be as effective in the future. In that indicator, two lines cross to mark the top, but the extent of the cross has been diminishing over time. This was especially noticeable in the 2021 cycle, where the lines barely crossed. Because of this, I created a new indicator that I think will continue to provide reliable reversal signals in the future.

How It Works

The logarithmic regression line is fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). This results in a steadily decreasing line. The EMA oscillates above and below this regression line. Each time the two lines cross, a vertical colored bar appears, indicating that Bitcoin's price momentum is likely to reverse.

Use Cases

- Price Bottoming:

Bitcoin often bottoms out when the EMA crosses below the logarithmic regression line.

- Price Topping:

In contrast, Bitcoin often peaks when the EMA crosses above the logarithmic regression line.

- Profitable Strategy:

Trading at the crossovers of these lines can be a profitable strategy, as these moments often signal significant price reversals.

Bitcoin Logarithmic Regression BandsOverview

This indicator displays logarithmic regression bands for Bitcoin. Logarithmic regression is a statistical method used to model data where growth slows down over time. I initially created these bands in 2019 using a spreadsheet, and later coded them in TradingView in 2021. Over time, the bands proved effective at capturing Bitcoin's bull market peaks and bear market lows. In 2024, I decided to share this indicator because I believe these logarithmic regression bands offer the best fit for the Bitcoin chart.

How It Works

The logarithmic regression lines are fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). The two lines in the upper and lower bands share the same 'a' factor, but I adjust the 'b' factor by 0.2 to more accurately capture the bull market peaks and bear market lows. The formula for logaritmic regression is 10^((a * ln) - b).

How to Use the Logarithmic Regression Bands

1. Lower Band (Support Band):

The two lines in the lower band create a potential support area for Bitcoin’s price. Historically, Bitcoin’s price has always found its lows within this band during past market cycles. When the price is within the lower band, it suggests that Bitcoin is undervalued and could be set for a rebound.

2. Upper Band (Resistance Band):

The two lines in the upper band create a potential resistance area for Bitcoin’s price. Bitcoin has consistently reached its highs in this band during previous market cycles. If the price is within the upper band, it indicates that Bitcoin is overvalued, and a potential price correction may be imminent.

Use Cases

- Price Bottoming:

Bitcoin tends to bottom out at the lower band before entering a prolonged bull market or a period of sideways movement.

- Price Topping:

In reverse, Bitcoin tends to top out at the upper band before entering a bear market phase.

- Profitable Strategy:

Buying at the lower band and selling at the upper band can be a profitable trading strategy, as these bands often indicate key price levels for Bitcoin’s market cycles.

US and Asia Trading Hoursadds vertical lines to your chart that show US trading hours 9-4 and NY trading hours based off of EST

Adaptive Trend Finder - Pulse Frequency(Basic)The Adaptive Pulse Frequency & Amplitude Trend Indicator is a Pine Script-based tool designed for lower timeframe volume analysis and trend detection. By analyzing volume dynamics and identifying significant "pulses" in market activity, this indicator provides insights into bullish and bearish trends. Here's an overview of its key features and components:

1. Lower Timeframe Volume Analysis

Custom Timeframe Input: The indicator scans lower timeframe data to approximate Up/Down volume, with an optional override to set a custom timeframe.

Volume Delta Calculation: Tracks changes in volume (deltaVolume), representing the difference between up and down volume for each bar.

2. Adaptive Pulse Detection

Rolling Percentile Threshold: Dynamically calculates a threshold based on the pulsePercentile of the absolute delta volume within a specified lookback period (pulseLookback).

Pulse Identification: Bars where the absolute delta volume exceeds the adaptive threshold are classified as "pulses," indicating significant market activity.

Bullish Pulse: Positive delta volume exceeding the threshold.

Bearish Pulse: Negative delta volume exceeding the threshold.

3. Frequency & Amplitude Analysis

Pulse Frequency: Measures the number of bullish or bearish pulses within a rolling window (freqLookback), providing insights into the activity level.

Pulse Amplitude: Computes the cumulative volume delta for bullish and bearish pulses over a defined period (ampLookback), offering a finer view of market strength:

Bullish Amplitude: Sum of positive delta volume for bullish pulses.

Bearish Amplitude: Sum of absolute delta volume for bearish pulses.

4. Trend Logic

Trend Classification:

Bullish Trend: Higher bullish pulse frequency and amplitude.

Bearish Trend: Higher bearish pulse frequency and amplitude.

Neutral Trend: Mixed or inconclusive signals.

Advanced Metrics: Combines frequency and amplitude for robust trend assessment.

5. Visualization

Dynamic Threshold: Plots the adaptive threshold for real-time pulse detection.

Trend Visualization: Colors the chart background based on the identified trend (Bullish, Bearish, Neutral).

Amplitude and Frequency Lines: Displays separate plots for:

Net Frequency (Bullish - Bearish pulses).

Net Amplitude (Bullish amplitude - Bearish amplitude).

Individual bullish and bearish amplitudes for reference.

Use Case

This indicator is ideal for traders seeking to:

Analyze market activity on lower timeframes.

Identify shifts in bullish/bearish momentum through volume dynamics.

Enhance trend-following strategies with adaptive frequency and amplitude metrics.

With its focus on precision and adaptability, the Adaptive Pulse Frequency & Amplitude Trend Indicator is a powerful tool for volume-based market analysis.

WD Gann: Close Price X Bars Ago with Line or Candle PlotThis indicator is inspired by the principles of WD Gann, a legendary trader known for his groundbreaking methods in time and price analysis. It helps traders track the close price of a security from X bars ago, a technique that is often used to identify key price levels in relation to past price movements. This concept is essential for Gann’s market theories, which emphasize the relationship between time and price.

WD Gann’s analysis often revolved around specific numbers that he considered significant, many of which correspond to squared numbers (e.g., 1, 4, 9, 16, 25, 36, 49, 64, 81, 100, 121, 144, 169, 196, 225, 256, 289, 324, 361, 400, 441, 484, 529, 576, 625, 676, 729, 784, 841, 900, 961, 1024, 1089, 1156, 1225, 1296, 1369, 1444, 1521, 1600, 1681, 1764, 1849, 1936). These numbers are believed to represent natural rhythms and cycles in the market. This indicator can help you explore how past price levels align with these significant numbers, potentially revealing key price zones that could act as support, resistance, or reversal points.

Key Features:

- Historical Close Price Calculation: The indicator calculates and displays the close price of a security from X bars ago (where X is customizable). This method aligns with Gann's focus on price relationships over specific time intervals, providing traders with valuable reference points to assess market conditions.

- Customizable Plot Type: You can choose between two plot types for visualizing the historical close price:

- Line Plot: A simple line that represents the close price from X bars ago, ideal for those who prefer a clean and continuous representation.

- Candle Plot: Displays the close price as a candlestick chart, providing a more detailed view with open, high, low, and close prices from X bars ago.

- Candle Color Coding: For the candle plot type, the script color-codes the candles. Green candles appear when the close price from X bars ago is higher than the open price, indicating bullish sentiment; red candles appear when the close is lower, indicating bearish sentiment. This color coding gives a quick visual cue to market sentiment.

- Customizable Number of Bars: You can adjust the number of bars (X) to look back, providing flexibility for analyzing different timeframes. Whether you're conducting short-term or long-term analysis, this input can be fine-tuned to suit your trading strategy.

- Gann Method Application: WD Gann's methods involved analyzing price action over specific time periods to predict future movements. This indicator offers traders a way to assess how the price of a security has behaved in the past in relation to a chosen time interval, a critical concept in Gann's theories.

How to Use:

1. Input Settings:

- Number of Bars (X): Choose the number of bars to look back (e.g., 100, 200, or any custom period).

- Plot Type: Select whether to display the data as a Line or Candles.

2. Interpretation:

- Using the Line plot, observe how the close price from X bars ago compares to the current market price.

- Using the Candles plot, analyze the full price action of the chosen bar from X bars ago, noting how the close price relates to the open, high, and low of that bar.

3. Gann Analysis: Integrate this indicator into your broader Gann-based analysis. By looking at past price levels and their relationship to significant squared numbers, traders can uncover potential key levels of support and resistance or even potential reversal points. The historical close price can act as a benchmark for predicting future market movements.

Suggestions on WD Gann's Emphasis in Trading:

WD Gann’s trading methods were rooted in several key principles that emphasized the relationship between time and price. These principles are vital to understanding how the "Close Price X Bars Ago" indicator fits into his overall analysis:

1. Time Cycles: Gann believed that markets move in cyclical patterns. By studying price levels from specific time intervals, traders can spot these cycles and predict future market behavior. This indicator allows you to see how the close price from X bars ago relates to current market conditions, helping to spot cyclical highs and lows.

2. Price and Time Squaring: A core concept in Gann’s theory is that certain price levels and time periods align, often marking significant reversal points. The squared numbers (e.g., 1, 4, 9, 16, 25, etc.) serve as potential key levels where price and time might "square" to create support or resistance. This indicator helps traders spot these historical price levels and their potential relevance to future price action.

3. Geometric Angles: Gann used angles (like the 45-degree angle) to predict market movements, with the belief that prices move at specific geometric angles over time. This indicator gives traders a reference for past price levels, which could align with key angles, helping traders predict future price movement based on Gann's geometry.

4. Numerology and Key Intervals: Gann paid particular attention to numbers that held significance, including squared numbers and numbers related to the Fibonacci sequence. This indicator allows traders to analyze price levels based on these key numbers, which can help in identifying potential turning points in the market.

5. Support and Resistance Levels: Gann’s methods often involved identifying levels of support and resistance based on past price action. By tracking the close price from X bars ago, traders can identify past support and resistance levels that may become significant again in future market conditions.

Perfect for:

Traders using WD Gann’s methods, such as Gann angles, time cycles, and price theory.

Analysts who focus on historical price levels to predict future price action.

Those who rely on numerology and geometric principles in their trading strategies.

By integrating this indicator into your trading strategy, you gain a powerful tool for analyzing market cycles and price movements in relation to key time intervals. The ability to track and compare the historical close price to significant numbers—like Gann’s squared numbers—can provide valuable insights into potential support, resistance, and reversal points.

Disclaimer:

This indicator is based on the methods and principles of WD Gann and is for educational purposes only. It is not intended as financial advice. Trading involves significant risk, and you should not trade with money that you cannot afford to lose. Past performance is not indicative of future results. The use of this indicator is at your own discretion and risk. Always do your own research and consider consulting a licensed financial advisor before making any investment decisions.

Open_close AND HIGH_LOW_diffAverage of Absolute (Open - Close) Indicator

This indicator calculates the average of the absolute difference between the open and close prices of the last n candles and plots the result in a separate panel.

Key Features:

Customizable Period: Users can set the number of candles (n) to include in the average calculation.

Absolute Value Calculation: The script computes the absolute difference (|Open - Close|) for each candle, ensuring only positive values are averaged.

Separate Panel Visualization: The indicator is displayed in a separate panel below the main chart for clear and uncluttered analysis.

Red Plot: The average value is plotted with a bold red line for easy identification.

Use Cases:

Analyze the average volatility of price movements over a specified period.

Identify periods of consistent price differences between open and close levels.

Complement other volatility or trend-based indicators.

This tool is ideal for traders who want to monitor the consistency of price fluctuations and integrate it into their decision-making process.

How to Use:

Add the script to your TradingView chart.

Adjust the "Number of Candles" input to match your preferred look-back period.

Observe the red line in the separate panel to analyze the average absolute difference over time.

Feel free to reach out with suggestions or feedback to enhance the functionality of this script!

Mean Reversion V-FThis strategy workings on high volatile stock or crypto assets

It using 5 dynamic band's to get in the long position.

In same time depends on the band increases the units of the asset to get in the next position.

The unit's of the asset can be adjusted. Make sure to adjust the unit for different asset.

The bands are determined of main SMA.

There is no stop loss.

Take profit is trialing - HMA or % or average price + take profit - note if you use % trailing back test is not realistic but is working on real time.

Deviations can be adjust depends on the asset volatility.

Improved G-Trend DetectionIt is the Improved version of G trend channel detection.

The Umair Trend Detection Indicator is a powerful tool designed to help traders identify potential buy and sell opportunities by combining dynamic price channels with RSI-based confirmation. This indicator is suitable for all types of financial markets, including stocks, forex, and cryptocurrencies.

Key Features:

Dynamic G-Channels

Calculates upper, lower, and average price channels based on the "G-Channel" methodology.

Helps identify market extremes and potential reversal points.

RSI Confirmation

Integrates RSI (Relative Strength Index) to filter buy and sell signals.

Avoids false signals by ensuring market momentum aligns with trend direction.

Buy/Sell Signals

Generates "Buy" signals when bullish conditions align with oversold RSI levels.

Generates "Sell" signals when bearish conditions align with overbought RSI levels.

Exit Signals

Provides optional exit points for both long and short positions using a buffer for confirmation.

Visual Clarity

Displays clearly plotted channels and average lines to help visualize price trends.

Buy and sell signals are marked with arrows for easy identification on the chart.

Custom Alerts

Offers customizable alerts for buy, sell, and exit conditions, ensuring traders never miss an opportunity.

Input Parameters:

Channel Length: Controls the sensitivity of the G-Channels.

Multiplier: Adjusts the width of the channels to suit different market conditions.

RSI Settings: Customize RSI length and thresholds for overbought/oversold conditions.

Exit Signal Buffer: Adds flexibility to the exit strategy by delaying signals for confirmation.

How It Helps:

The Umair Trend Detection Indicator is perfect for traders looking for an easy-to-use trend-following system with strong confirmation. By combining dynamic channels with RSI, it provides accurate and reliable signals to enter and exit trades, minimizing risks associated with false breakouts or trend reversals.

Use Cases:

Trend Trading: Identify and follow long-term trends with confidence.

Swing Trading: Spot reversals and capitalize on medium-term price movements.

Risk Management: Use exit signals to lock in profits or limit losses effectively.

This indicator is a versatile tool for both novice and experienced traders. Fine-tune its settings to align with your trading style and improve your decision-making in any market.

Bitcoin Pi Cycle TrackerThe Bitcoin Pi Cycle Tracker is based on the widely recognized Pi Cycle Top Indicator, a concept used to identify potential market cycle tops in Bitcoin's price. This implementation combines the 111-day Simple Moving Average (SMA) and the 350-day SMA (multiplied by 2) to detect key crossover points. When the 111-day SMA crosses above the 350-day SMA x2, it signals a potential market peak.

Key Features:

Plots the 111-day SMA (blue) and the 350-day SMA x2 (red) for clear visualization.

Displays visual markers and vertical lines at crossover points to highlight key moments.

Sends alerts for crossovers, helping traders stay ahead of market movements.

This tool is an implementation of the Pi Cycle concept originally popularized by Bitcoin market analysts. Use it to analyze historical price cycles and prepare for significant market events. Please note that while the Pi Cycle Indicator has been historically effective, it should be used alongside other tools for a comprehensive trading strategy.

EMA RSI Trend Reversal Ver.1Overview:

The EMA RSI Trend Reversal indicator combines the power of two well-known technical indicators—Exponential Moving Averages (EMAs) and the Relative Strength Index (RSI)—to identify potential trend reversal points in the market. The strategy looks for key crossovers between the fast and slow EMAs, and uses the RSI to confirm the strength of the trend. This combination helps to avoid false signals during sideways market conditions.

How It Works:

Buy Signal:

The Fast EMA (9) crosses above the Slow EMA (21), indicating a potential shift from a downtrend to an uptrend.

The RSI is above 50, confirming strong bullish momentum.

Visual Signal: A green arrow below the price bar and a Buy label are plotted on the chart.

Sell Signal:

The Fast EMA (9) crosses below the Slow EMA (21), indicating a potential shift from an uptrend to a downtrend.

The RSI is below 50, confirming weak or bearish momentum.

Visual Signal: A red arrow above the price bar and a Sell label are plotted on the chart.

Key Features:

EMA Crossovers: The Fast EMA crossing above the Slow EMA signals potential buying opportunities, while the Fast EMA crossing below the Slow EMA signals potential selling opportunities.

RSI Confirmation: The RSI helps confirm trend strength—values above 50 indicate bullish momentum, while values below 50 indicate bearish momentum.

Visual Cues: The strategy uses green arrows and red arrows along with Buy and Sell labels for clear visual signals of when to enter or exit trades.

Signal Interpretation:

Green Arrow / Buy Label: The Fast EMA (9) has crossed above the Slow EMA (21), and the RSI is above 50. This is a signal to buy or enter a long position.

Red Arrow / Sell Label: The Fast EMA (9) has crossed below the Slow EMA (21), and the RSI is below 50. This is a signal to sell or exit the long position.

Strategy Settings:

Fast EMA Length: Set to 9 (this determines how sensitive the fast EMA is to recent price movements).

Slow EMA Length: Set to 21 (this smooths out price movements to identify the broader trend).

RSI Length: Set to 14 (default setting to track momentum strength).

RSI Level: Set to 50 (used to confirm the strength of the trend—above 50 for buy signals, below 50 for sell signals).

Risk Management (Optional):

Use take profit and stop loss based on your preferred risk-to-reward ratio. For example, you can set a 2:1 risk-to-reward ratio (2x take profit for every 1x stop loss).

Backtesting and Optimization:

Backtest the strategy on TradingView by opening the Strategy Tester tab. This will allow you to see how the strategy would have performed on historical data.

Optimization: Adjust the EMA lengths, RSI period, and risk-to-reward settings based on your asset and time frame.

Limitations:

False Signals in Sideways Markets: Like any trend-following strategy, this indicator may generate false signals during periods of low volatility or sideways movement.

Not Suitable for All Market Conditions: This indicator performs best in trending markets. It may underperform in choppy or range-bound markets.

Strategy Example:

XRP/USD Example:

If you're trading XRP/USD and the Fast EMA (9) crosses above the Slow EMA (21), while the RSI is above 50, the indicator will signal a Buy.

Conversely, if the Fast EMA (9) crosses below the Slow EMA (21), and the RSI is below 50, the indicator will signal a Sell.

Bitcoin (BTC/USD):

On the BTC/USD chart, when the indicator shows a green arrow and a Buy label, it’s signaling a potential long entry. Similarly, a red arrow and Sell label indicate a short entry or exit from a previous long position.

Summary:

The EMA RSI Trend Reversal Indicator helps traders identify potential trend reversals with clear buy and sell signals based on the EMA crossovers and RSI confirmations. By using green arrows and red arrows, along with Buy and Sell labels, this strategy offers easy-to-understand visual signals for entering and exiting trades. Combine this with effective risk management and backtesting to optimize your trading performance.

Push Up Pullback BuyThe Push Up Pullback Buy (PUPB) indicator is designed to identify trend continuation opportunities by detecting key market movements:

Push-Ups: Rapid upward price movements exceeding a customizable minimum change.

Pullbacks: Temporary price corrections following a push-up.

Trend Confirmation: Validates higher highs and higher lows during pullbacks to ensure trend continuation.

Multi-Timeframe Analysis: Incorporates lower timeframe breakout confirmation for enhanced precision.

This indicator provides visual cues (arrows and signals) directly on your chart, making it intuitive for traders to spot potential buy opportunities. Ideal for trend-following strategies and traders looking to capitalize on pullback entries in bullish markets.

Customizable parameters allow you to adapt the indicator to your preferred trading style and instruments.

Opening Candle High/Low with Time Zone and Minute Offset

Title: Opening Candle High/Low with Time Zone and Minute Offset

Description:

The Opening Candle High/Low with Time Zone and Minute Offset indicator is a versatile tool that highlights the high and low of the first candle of the trading session, adjusted for your preferred time zone and minute offset. It is particularly useful for traders who focus on opening ranges as key reference points for their trading strategies.

---

Features:

1. Time Zone and Minute Adjustment:

- Allows customization of the start time by applying a time zone offset (in hours) and a minute offset.

- Ideal for traders operating in different time zones or trading sessions that don't align with midnight UTC.

2. Dynamic First Candle Detection:

- Automatically captures the high and low of the first candle after the adjusted time.

- Resets daily, ensuring accurate levels for each new trading session.

3. Visual Representation:

- Plots the high and low levels of the first candle directly on the chart for easy reference.

- Uses distinct colors (green for the high and red for the low) and adjustable line widths for clarity.

4. Simplicity and Versatility:

- Works across all markets and timeframes, providing essential information for opening range breakout strategies, support/resistance analysis, or session-based trading.

---

How It Works:

1. Time Adjustment:

- The indicator adjusts the current chart time by applying the user-defined hour and minute offsets.

- This ensures the "opening candle" aligns with your specific trading session requirements.

2. First Candle Detection:

- When the adjusted time matches the start of a new day (midnight with offsets), the indicator captures the high and low of the first candle.

- These values are stored and remain static throughout the trading day.

3. Plotting:

- The high and low levels of the opening candle are plotted on the chart, providing visual reference points for traders.

---

Use Case:

- This indicator is ideal for traders who rely on the opening range of a session for planning trades, such as breakout or reversal strategies.

- It can also serve as a key tool for identifying significant price levels in session-based trading.

Simplify your trading analysis and align your strategy with this customizable and intuitive indicator.

Previous Week High & Low with middle lineDescription:

The Previous Week High & Low Indicator is a powerful tool designed to provide traders with key reference levels from the previous trading week. It dynamically calculates and plots the previous week's high, low, and midpoint levels directly on your chart, helping you identify critical support and resistance zones.

Features:

1. **Previous Week High and Low Lines**:

- The indicator displays the high and low prices of the previous trading week, allowing you to analyze price action relative to these levels.

- These lines are plotted as step lines, visible only during the active trading days (Monday to Friday), ensuring clean and uncluttered charts.

2. Midpoint Line:

- The midpoint between the previous week's high and low is calculated and displayed as a reference level.

- This white line can act as a psychological pivot point for market participants.

3. Customizable Display:

- You can toggle the visibility of the high and low lines using input options, tailoring the indicator to your preferences.

4. Precision and Aesthetics:

- The lines are plotted with precision and styled for clarity, using subtle transparency for an unobtrusive yet informative appearance.

Use Case:

- This indicator is ideal for traders who rely on historical price levels for planning entries, exits, or stop-loss placements.

- It works seamlessly with any timeframe and asset, making it versatile for various trading strategies.

How It Works:

- The indicator fetches the previous week's high and low prices using the weekly timeframe and "lookahead" mode to ensure these levels remain static after the week's close.

- The lines are plotted only on weekdays (Monday to Friday) to exclude weekend data, ensuring accuracy for markets that operate 24/5.

This tool simplifies your chart analysis and empowers you to make informed trading decisions based on historical price dynamics.

Range PolarityDescription:

This indicator is a "Rate of Change" style oscillator designed to measure market dynamics through the lens of price ranges. By utilizing the true range in conjunction with high and low separation, this script produces two distinct oscillators: one for positive price shifts and one for negative price shifts.

Key Features:

High/Low Isolation:

The script calculates the relative movement of upwards and downwards price movements over a user-defined period. This separation provides a nuanced view of market behavior, offering two separate signals for comparison.

Dynamic Transform Smoothing:

A smoothing transform is applied to the signals, ensuring better outlier handling while maintaining sensitivity to price extremes. This makes the oscillator especially suited for identifying overbought and oversold conditions.

Zero-Centered:

The zero line acts as a "gravity point," where shifts away or toward zero indicate market momentum. Signal crosses or reversals from extreme zones can signal potential entry or exit points.

Outlier Identification:

Unlike traditional ATR based strategies (e.g., Keltner Channels ), this indicator isolates high and low ranges, creating a more granular view of market extremes. These measurements can help identify shifts from the outlying positions and reversal opportunities.

Visual Enhancements:

Multiple layers enhance the visual distinction of the positive and negative transformations. Horizontal lines at key thresholds provide visual reference for overbought, oversold, and equilibrium zones.

How to Use:

Primary signals are shifts from outlying positions or a positive/negative cross. An extreme reading itself can reveal an incoming reversal when calibrated with other indicators or compared with higher timeframes. Pairing "Range Polarity" with volume and momentum can create a comprehensive strategy.

In conclusion, be aware the base length controls the window for high/low contributions while the transform smoothing enhances the raw data through normalization within a tempered range to filter out insignificant fluctuations.

Merry Christmas to all and have a Happy New Year!

ROC with AveragesMain Idea

This script provides traders with a comprehensive view of market momentum by calculating the Rate of Change (ROC) and categorizing its impact into averages of positive, negative, and total values.

Key Features

Rate of Change (ROC) Calculation: Measures the percentage change in closing prices over a user-defined period.

Categorical Averages:

Positive Average: Average ROC for upward movements.

Negative Average: Average ROC for downward movements.

Total Average: Aggregate average across all movements.

Dynamic Visualization: Plots ROC alongside its categorized averages for better trend analysis.

Benefits

Simplifies the evaluation of market trends by breaking down data into actionable insights.

Helps traders identify the strength of upward or downward movements.

Offers a clear visual representation for quick decision-making.

This structure highlights the purpose and value of the script while aligning with the Minto Pyramid Principle. Let me know if you'd like further refinements!

الفكرة الرئيسية

يوفر هذا السكربت للمتداولين رؤية شاملة لزخم السوق من خلال حساب معدل التغير (ROC) وتصنيفه إلى متوسطات القيم الإيجابية والسلبية والإجمالية.

المميزات الرئيسية

حساب معدل التغير (ROC): يقيس النسبة المئوية للتغير في أسعار الإغلاق خلال فترة محددة يختارها المستخدم.

المتوسطات التصنيفية:

المتوسط الإيجابي: متوسط معدل التغير للحركات الصعودية.

المتوسط السلبي: متوسط معدل التغير للحركات الهبوطية.

المتوسط الإجمالي: متوسط إجمالي يشمل جميع الحركات.

تصور ديناميكي: يعرض معدل التغير إلى جانب المتوسطات المصنفة لتسهيل تحليل الاتجاهات.

الفوائد

يبسط تقييم اتجاهات السوق من خلال تقسيم البيانات إلى رؤى قابلة للتنفيذ.

يساعد المتداولين على تحديد قوة الحركات الصعودية أو الهبوطية.

يقدم تمثيلاً بصرياً واضحاً لاتخاذ قرارات سريعة ودقيقة.

MTF Countdown with Direction - AynetIndicator Definition and Inputs:

pineCopyindicator('MTF Countdown with Direction - Aynet', overlay = true)

This code creates a Multiple Time Frame (MTF) countdown indicator with direction

The overlay = true parameter places the indicator on top of the price chart

Timeframe Options:

Users can choose to show/hide the following timeframes:

1 minute

5 minutes

15 minutes

30 minutes

1 hour

4 hours

Daily

Time Calculations:

pineCopyget_current_time()

Calculates the current time

Converts Unix timestamp to seconds

Calculates time since midnight

Returns time broken down into hours, minutes, and seconds

Countdown Calculation:

pineCopyget_period_countdown(period_seconds)

Calculates remaining time for each timeframe

Computes elapsed time in current period

Returns remaining time in hours, minutes, and seconds

Direction and Closing Price Calculation:

Separate functions for each timeframe (get_direction_and_close_1m(), get_direction_and_close_5m(), etc.)

Each function:

Gets current closing price

Compares with previous closing price

Determines direction (up: 1, down: -1, sideways: 0)

Returns direction and closing price

Table Creation and Updates:

Creates a table in the top right corner

Table consists of 4 columns:

Period (Timeframe)

Time Left (Remaining time)

Direction (Shown with arrows)

Close (Closing price)

Each row has a different background color

Direction arrows:

Green up arrow (▲): Price rising

Red down arrow (▼): Price falling

Gray line (―): Price sideways

Dynamic Data Structures:

pineCopyvar timeframes = array.new_int()

var timeframe_names = array.new_string()

var show_array = array.new_bool()

Uses dynamic arrays for timeframes

Adds selected timeframes to arrays on first run

Key Features:

Shows remaining time until period close

Displays price direction for each timeframe

Shows current closing prices

All information in a single, easy-to-read table

This indicator helps traders by providing a comprehensive view of:

When each timeframe will close

The direction of price movement

Current closing prices

across multiple timeframes in a single table, making it easier to track market movements across different time periods.

The color-coding and arrow system makes it visually intuitive to understand market direction at a glance, while the countdown timer helps with timing decisions.