Gold DynamicThis is a custom-made TradingView indicator designed to visualize "sequential price levels" based on a user-defined step value, dynamically centered around the current gold price. It draws horizontal lines at multiples of a chosen step value (e.g., 7) both above and below the current price.

Key Features:

Dynamic Price Levels: Lines are calculated relative to the live price, providing relevant support/resistance or structural levels for the current market context.

Customizable Step Value: Easily adjust the Sequence Step Value (e.g., 7, 10, 14) from the indicator settings to align with your trading theory.

Adjustable Line Count: Control the Number of Lines ABOVE Current Price and Number of Lines BELOW Current Price to show as many or as few levels as desired.

Extended Lines: Horizontal lines extend indefinitely to both the left (historical data) and right (future projection) for comprehensive visualization.

Clear Price Labels: Each line displays its exact price value, positioned at the far right of the chart for quick reference.

Customizable Appearance: Modify line color, width, and style (solid, dotted, dashed) to suit your charting preferences.

Exact Values: All displayed price labels are rounded to whole numbers for clear, precise visualization without decimal values.

This indicator is ideal for traders looking to apply a fixed-step price theory to their gold analysis.

Dynamiclevels

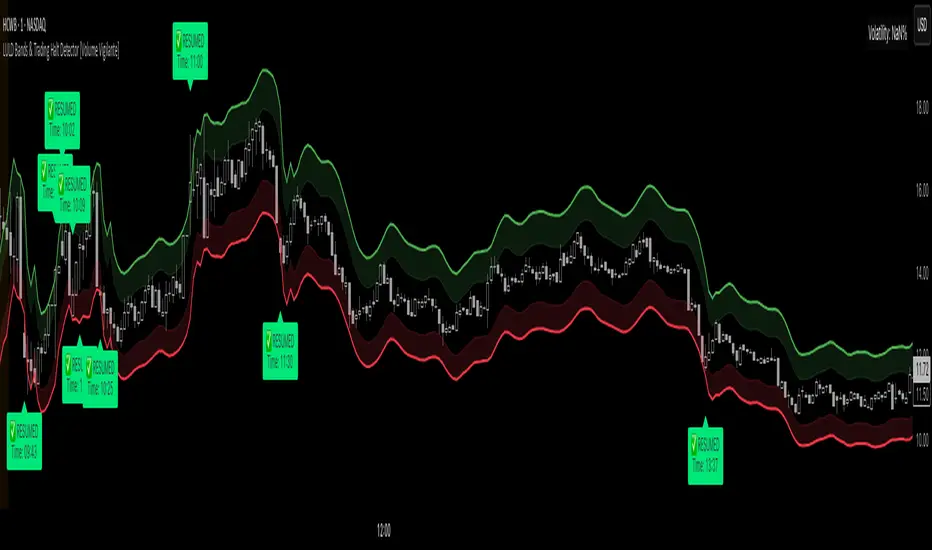

LULD Bands & Trading Halt Detector [Volume Vigilante]📖 LULD Bands & Trading Halt Detector

This advanced tool visualizes official Limit Up / Limit Down (LULD) price bands and detects regulatory trading halts and resumptions based on SEC and NASDAQ rules. It is engineered for high accuracy by anchoring all calculations to the 1-minute timeframe, ensuring reliable signals across any chart resolution.

📌 What Does This Script Do?

- Draws real-time LULD price band estimations and optional buffer (caution) zones directly on the chart.

- Detects trading halt resumptions by monitoring time gaps between candles and other regulatory criteria. (Note: Due to Pine Script limitations, halts cannot be detected in real-time, only resumptions after they occur.)

- Triggers real-time alerts for:

- Trading Resumptions (Limit Up & Limit Down)

- LULD Zone Entries (Caution Zone)

- Band Breaches (Limit Up and Limit Down)

- Plots historical halt resumption markers to analyse past events.

📐 How It Works:

- Implements official SEC/NASDAQ LULD rules for Tier 1 and Tier 2 securities.

- Applies special band adjustments for the final 25 minutes of trading (after 3:35 PM ET).

- Anchors all logic to the 1-minute timeframe for precise calculations, even on higher timeframe charts.

- Includes adjustable volume and volatility filters to eliminate false signals (ghost halts) on low-- liquidity assets, especially Tier 2 securities when TradingView fails to print candles.

⚙️ How to Use It:

1.) Apply the script to any asset or timeframe.

2.) Adjust Volume and Volatility Filters to reduce noise. (Recommended: 500,000+ volume, 10%+ volatility.)

3.) Enable or disable visual components like bands, buffer zones, and halt resumption labels.

4.) Configure alerts directly from the script settings panel.

5.) Apply alerts to individual assets via "Add Alert On..." or to entire watchlists using "Add Alert on the List."

🧩 What Makes This Script Unique?

- True 1-Minute Anchored Calculations: Ensures alerts and visuals match official trading halt criteria regardless of chart timeframe.

- Customisable Buffered Zones: Visualise proximity to regulatory price limits and avoid volatility traps.

- Combines halt resumption detection, limit up/down band visualisation, and real-time alerts into one clean, modular tool.

📚 Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Use at your own discretion and consult a licensed financial advisor before making trading decisions based on it.

Official Resources:

- NASDAQ LULD Regulations (FAQ):

www.nasdaqtrader.com

Current Nasdaq Trading Halts:

www.nasdaqtrader.com

Auto Support Resistance Channels [TradingFinder] Top/Down Signal🔵 Introduction

In technical analysis, a price channel is one of the most widely used tools for identifying and tracking price trends. A price channel consists of two parallel trendlines, typically drawn from swing highs (resistance) and swing lows (support). These lines define dynamic support and resistance zones and provide a clear framework for interpreting price fluctuations.

Drawing a channel on a price chart allows the analyst to more precisely identify entry points, exit levels, take-profit zones, and stop-loss areas based on how the price behaves within the boundaries of the channel.

Price channels in technical analysis are generally categorized into three types: upward channels with a positive slope, downward channels with a negative slope, and horizontal (range-bound) channels with near-zero slope. Each type offers unique insights into market behavior depending on the price structure and prevailing trend.

Structurally, channels can be formed using either minor or major pivot points. A major channel typically reflects a stronger, more reliable structure that appears on higher timeframes, whereas a minor channel often captures short-term fluctuations or corrective movements within a larger trend.

For instance, a major downward channel may indicate sustained selling pressure across the market, while a minor upward channel could represent a temporary pullback within a broader bearish trend.

The validity of a price channel depends on several factors, including the number of price touches on the channel lines, the symmetry and parallelism of the trendlines, the duration of price movement within the channel, and price behavior around the median line.

When a price channel is broken, it is generally expected that the price will move in the breakout direction by at least the width of the channel. This makes price channels especially useful in breakout analysis.

In the following sections, we will explore the different types of price channels, how to draw them accurately, the structural differences between minor and major channels, and key trade interpretations when price interacts with channel boundaries.

Up Channel :

Down Channel :

🔵 How to Use

A price channel is a practical tool in technical analysis for identifying areas of support, resistance, trend direction, and potential breakout zones. The structure consists of two parallel trendlines within which price fluctuates.

Traders use the relative position of price within the channel to make informed trading decisions. The two primary strategies include range-based trades (buying low, selling high) and breakout trades (entering when price exits the channel).

🟣 Up Channel

In an upward channel, price moves within a positively sloped range. The lower trendline acts as dynamic support, while the upper trendline serves as dynamic resistance. A common strategy involves buying near the lower support and taking profit or selling near the upper resistance.

If price breaks below the lower trendline with strong volume or a decisive candle, it can signal a potential trend reversal. Channels constructed from major pivots generally reflect dominant uptrends, while those based on minor pivots are often corrective structures within a broader bearish movement.

🟣 Down Channel

In a downward channel, price moves between two negatively sloped lines. The upper trendline functions as resistance, and the lower trendline as support. Ideal entry for short trades occurs near the upper boundary, especially when confirmed by bearish price action or a resistance level.

Exit targets are typically located near the lower support. If the upper boundary is broken to the upside, it may be an early sign of a bullish trend reversal. Like upward channels, a major down channel represents broader selling pressure, while a minor one may indicate a brief retracement in a bullish move.

🟣 Range Channel

A horizontal or range-bound channel is characterized by price oscillating between two nearly flat lines. This type of channel typically appears during sideways markets or periods of consolidation.

Traders often buy near the lower boundary and sell near the upper boundary to take advantage of contained volatility. However, fake breakouts are more frequent in range-bound structures, so it is important to wait for confirmation through candlestick signals and volume. A confirmed breakout beyond the channel boundaries can justify entering a trade in the direction of the breakout.

🔵 Settings

Pivot Period :This parameter defines how sensitive the channel detection is. A higher value causes the algorithm to identify major pivot points, resulting in broader and longer-term channels. Lower values focus on minor pivots and create tighter, short-term channels.

🔔 Alerts

Alert Configuration :

Enable or disable the full alert system

Set a custom alert name

Choose the alert frequency: every time, once per bar, or on bar close

Define the time zone for alert timestamps (e.g., UTC)

Channel Alert Types :

Each channel type (Major/Minor, Internal/External, Up/Down) supports two alert types :

Break Alert : Triggered when price breaks above or below the channel boundaries

React Alert : Triggered when price touches and reacts (bounces) off the channel boundary

🎨 Display Settings

For each of the eight channel types, you can customize:

Visibility : show or hide the channel

Auto-delete previous channels when new ones are drawn

Style : line color, thickness, type (solid, dashed, dotted), extension (right only, both sides)

🔵 Conclusion

The price channel is a foundational structure in technical analysis that enables traders to analyze price movement, identify dynamic support and resistance zones, and locate potential entry and exit points with greater precision.

When constructed properly using minor or major pivots, a price channel offers a consistent and intuitive framework for interpreting market behavior—often simpler and more visually clear than many other technical tools.

Understanding the differences between upward, downward, and range-bound channels—as well as recognizing the distinctions between minor and major structures—is critical for selecting the right trading strategy. Upward channels tend to generate buying opportunities, downward channels prioritize short setups, and horizontal channels provide setups for both mean-reversion and breakout trades.

Ultimately, the reliability of a price channel depends on various factors such as the number of touchpoints, the duration of the channel, the parallelism of the lines, and how the price reacts to the median line.

By taking these factors into account, an experienced analyst can effectively use price channels as a powerful tool for trend forecasting and precise trade execution. Although conceptually simple, successful application of price channels requires practice, pattern recognition, and the ability to filter out market noise.

Dynamic Heat Levels [BigBeluga]This indicator visualizes dynamic support and resistance levels with an adaptive heatmap effect. It helps traders identify key price interaction zones and potential mean reversion opportunities by displaying multiple levels that react to price movement.

🔵Key Features:

Multi-Level Heatmap Channel:

- The indicator plots multiple dynamic levels forming a structured channel.

- Each level represents a historical price interaction zone, helping traders identify critical areas.

- The channel expands or contracts based on market conditions, adapting dynamically to price movements.

Heatmap-Based Strength Indication:

- Levels change in transparency and color intensity based on price interactions for the length period .

- The more frequently price interacts with a level, the more visible and intense the color becomes.

- When a level reaches a threshold (count > 10), it starts to turn red, signaling a high-heat zone with significant price activity.

🔵Usage:

Support & Resistance Analysis: Identify price levels where the market frequently interacts, making them strong areas for trade decisions.

Heatmap Strength Assessment: More intense red levels indicate areas with heavy price activity, useful for detecting key liquidity zones.

Dynamic Heat Levels is a powerful tool for traders looking to analyze price interaction zones with a heatmap effect. It offers a structured visualization of market dynamics, allowing traders to gauge the significance of key levels and detect mean reversion setups effectively.

Trendilo ARTrendilo AR is a custom trading indicator designed to identify market trends using advanced techniques such as the Arnaud Legoux Moving Average (ALMA), volume confirmations, and dynamic volatility bands. This indicator provides a clear visualization of trends, including significant changes and custom alerts.

Review of Indicators Used

1. ALMA

Description:

ALMA is a moving average that applies an advanced filter to smooth price data, reducing noise and focusing on actual trends.

Usage in the Indicator:

Used to calculate the smoothed percentage price change and determine trend direction. Customizable parameters include:

- Length: Defines the number of bars to consider.

- Offset: Adjusts sensitivity toward recent prices.

- Sigma: Controls the degree of smoothing.

Advantages:

- Reduced lag in trend detection.

- Resistance to market noise.

2. ATR

Description:

ATR measures the market’s average volatility by considering the range between high and low prices over a given period.

Usage in the Indicator:

ATR is used to calculate "dynamic smoothing", adjusting the indicator’s sensitivity based on current market volatility.

Advantages:

- Adapts to high or low volatility conditions.

- Helps define dynamic support and resistance levels.

3. SMA

Description:

SMA calculates the average of prices or volume over a specific time period.

Usage in the Indicator:

Used to calculate the volume moving average (Volume SMA) to confirm whether the current volume supports the detected trend.

Advantages:

- Easy to understand and calculate.

- Provides volume-based trend confirmation.

4. RMS Bands

Description:

RMS Bands calculate the standard deviation of percentage price changes, creating upper and lower levels that act as overbought and oversold indicators.

Usage in the Indicator:

- Define the range within which the market is considered neutral.

- Crosses above or below the bands indicate trend changes.

Advantages:

- Visual identification of strong trends.

- Helps filter false signals.

Colors and Visuals Used in the Indicator

1. ALMA Line

Colors:

- Green: Indicates a confirmed uptrend (with sufficient volume).

- Red: Indicates a confirmed downtrend (with sufficient volume).

- Gray: Indicates a neutral phase or insufficient volume to confirm a trend.

2. RMS Bands

- Upper and Lower Lines:

- Purple (with transparency): These lines represent the RMS bands (upper and lower) and

adjust opacity based on trend strength.

- Stronger trends result in less transparency (more solid colors).

3. Highlighted Background (Strong Trends)

- Color:

- Light Green (transparent): Highlights a strong trend when the smoothed percentage change (ALMA) exceeds 1.5 times the RMS.

4. Horizontal Lines

- Baseline (0):

- Dark Gray: Serves as a central reference to identify the directionality of percentage changes.

- Additional Line (0.1):

- Blue: A customizable line to mark user-defined key levels.

5. Bar Colors

- Bar Colors:

- Green: When the price is in a confirmed uptrend.

- Red: When the price is in a confirmed downtrend.

- No color: When there is insufficient volume or no clear trend.

How to Use the Indicator

1. Initial Setup

1. Add the Indicator to Your Chart: Copy the code into the Pine Editor on TradingView and apply it to your chart.

2. Customize Parameters: Adjust values based on your trading strategy:

- Smoothing: Controls the level of smoothing for percentage changes.

- Lookback Length: Defines the observation period for calculations.

- Band Multiplier: Adjusts the width of RMS bands.

2. Signal Interpretation

1. Indicator Colors:

- Green: Confirmed uptrend.

- Red: Confirmed downtrend.

- Gray: No clear trend or insufficient volume.

2. RMS Bands:

- If the ALMA line (smoothed percentage change) crosses above the upper RMS band, it signals a potential uptrend.

- If it crosses below the lower RMS band, it signals a potential downtrend.

3. Volume Confirmation:

- The indicator's color activates only if the current volume exceeds the Volume SMA.

3. Alerts and Decisions

1. Trend Change Alerts:

- The indicator automatically triggers alerts when an uptrend or downtrend is detected.

- Configure these alerts to receive real-time notifications.

2. Strong Trend Signals:

- When the magnitude of the percentage change exceeds 1.5 times the RMS, the chart background highlights the strong trend.

4. Trading Strategies

1. Buy:

- Enter long positions when:

- The indicator turns green.

- Volume confirms the trend.

- Consider placing a stop-loss just below the lower RMS band.

2. Sell:

- Enter short positions when:

- The indicator turns red.

- Volume confirms the trend.

- Consider placing a stop-loss just above the upper RMS band.

3. Neutral:

- Avoid trading when the indicator is gray, as no clear trend or insufficient volume is present.

Disclaimer: As this is my first published indicator, please use it with caution. Feedback is highly appreciated to improve its performance.

Happy Trading!

Truly Iterative Gaussian ChannelOVERVIEW

The Truly Iterative Gaussian Channel is a robust channeling system that integrates a Gaussian smoothing kernel with a rolling standard deviation to create dynamically adaptive upper and lower boundaries around price. This indicator provides a smooth, yet responsive representation of price movements while minimizing lag and dynamically adjusting channel width to reflect real-time market volatility. Its versatility makes it effective across various timeframes and trading styles, offering significant potential for experimentation and integration into advanced trading systems.

TRADING USES

The Gaussian indicator can be used for multiple trading strategies. Trend following relies on the middle Gaussian line to gauge trend direction: prices above this line indicate bullish momentum, while prices below signal bearish momentum. The upper and lower boundaries act as dynamic support and resistance levels, offering breakout or pullback entry opportunities. Mean reversion focuses on identifying reversal setups when price approaches or breaches the outer boundaries, aiming for a return to the Gaussian centerline. Volatility filtering helps assess market conditions, with narrow channels indicating low volatility or consolidation and suggesting fewer trading opportunities or an impending breakout. Adaptive risk management uses channel width to adjust for market volatility, with wider channels signaling higher risk and tighter channels indicating lower volatility and potentially safer entry points.

THEORY

Gaussian kernel smoothing, derived from the Gaussian normal distribution, is a cornerstone of probability and statistics, valued for its ability to reduce noise while preserving critical signal features. In this indicator, it ensures price movements are smoothed with precision, minimizing distortion while maintaining responsiveness to market dynamics.

The rolling standard deviation complements this by dynamically measuring price dispersion from the mean, enabling the channel to adapt in real time to changing market conditions. This combination leverages the mathematical correctness of both tools to balance smoothness and adaptability.

An iterative framework processes data efficiently, bar by bar, without recalculating historical value to ensure reliability and preventing repainting to create a mathematically grounded channel system suitable for a wide range of market environments.

The Gaussian channel excels at filtering noise while remaining responsive to price action, providing traders with a dependable tool for identifying trends, reversals, and volatility shifts with consistency and precision.

CALIBRATION

Calibration of the Gaussian channel involves adjusting its length to modify sensitivity and adaptability based on trading style. Shorter lengths (e.g., 50-100) are ideal for intraday traders seeking quick responses to price fluctuations. Medium lengths (e.g., 150-200) cater to swing traders aiming to capture broader market trends. Longer lengths (e.g., 250-400+) are better suited for positional traders focusing on long-term price movements and stability.

MARKET USAGE

Stock, Forex, Crypto, Commodities, and Indices.

Pulse Oscillator [UAlgo]The "Pulse Oscillator " is a trading tool designed to capture market momentum and trend changes by combining the strengths of multiple well-known technical indicators. By integrating the RSI (Relative Strength Index), CCI (Commodity Channel Index), and Stochastic Oscillator, this indicator provides traders with a comprehensive view of market conditions, offering both trend filtering and precise buy/sell signals. The oscillator is customizable, allowing users to fine-tune its parameters to match different trading strategies and timeframes. With its built-in smoothing techniques and level adjustments, the Pulse Oscillator aims to be a reliable tool for both trend-following and counter-trend trading strategies.

🔶 Key Features

Multi-Indicator Integration: Combines RSI, CCI, and Stochastic Oscillator to create a weighted momentum oscillator.

Why Use Multi-Indicator Integration?

Script uses Multi-Indicator Integration to combine the strengths of different technical indicators—such as RSI, CCI, and Stochastic Oscillator—into a single tool. This approach helps to reduce the weaknesses of individual indicators, providing a more comprehensive and reliable analysis of market conditions. By integrating multiple indicators, we can generate more accurate signals, filter out noise, and enhance our trading decisions.

Customizable Parameters: Allows users to adjust weights, periods, and smoothing techniques, providing flexibility to adapt the indicator to various market conditions.

Trend Filtering Option: An optional trend filter is available to enhance the accuracy of buy and sell signals, reducing the risk of false signals in choppy markets.

Dynamic Levels: The indicator dynamically calculates multiple levels of support and resistance, adjusting to market conditions with customizable decay factors and offsets.

Visual Clarity: The indicator visually represents different levels and trends with color-coded plots and fills, making it easier for traders to interpret market conditions at a glance.

Alerts: Configurable alerts for buy and sell signals, as well as trend changes, enabling traders to stay informed of key market movements without constant monitoring.

🔶 Interpreting the Indicator

Buy Signal: A buy signal is generated when the Slow Line crosses under the Fast Line during an uptrend or when the trend filter is disabled. This indicates a potential bullish reversal or continuation of an upward trend.

Sell Signal: A sell signal occurs when the Slow Line crosses above the Fast Line during a downtrend or when the trend filter is disabled, signaling a potential bearish reversal or continuation of a downward trend.

Trend Change: The indicator detects trend changes when the Fast Line shifts from increasing to decreasing or vice versa, providing early warning of possible market reversals.

Dynamic Levels: The indicator calculates upper and lower levels based on the Fast Line's values. These levels can be used to identify overbought or oversold conditions and potential areas of support or resistance.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

CCI based support and resistance strategy

WARNING:

Commissions and slippage has not been considered! Don’t take it easy adding commissions and slippage could turns a fake-profitable strategy to a real disaster.

We consider account size as 10k and we enter 1000 for each trade.

Less than 100 trades is too small sample community and it’s not reliable, Also the performance of the past do not guarantee future performance. This result was handpicked by author and will differ by other timeframes, instruments and settings.

*PLEASE SHARE YOUR SETTINGS THAT WORK WITH THE COMMUNITY.

Introduction:

The CCI-based dynamic support and resistance is a "Bands and Channels" kind of indicator consisting an upper and lower band. This is a strategy which uses CCI-based (Made by me) indicator to execute trades.

SL and TP are calculated based on max ATR during last selected time period. You can edit strategy settings using "Ksl", "Ktp" and the other button for time period. “KSL” and “KTP” are 2.5 and 5 by default.

Bands are calculated regarding CCI previous high and low pivot. CCI length, right pivot length and left pivot length are 50.

A dynamic support and resistance has been calculated using last upper-cci minus a buffer and last lower-cci plus the buffer. The buffer is 10.

If "Trend matter?" button is on you can detect trend by color of the upper and lower line. Green is bullish and red is bearish! "Trend matter?" is on.

The "show mid?" button makes mid line visible, which is average of upper and lower lines, visible. The button is not active by default.

Reaction to the support could be a buy signal while a reaction to the resistance could interpreted as a sell signal.

How this strategy work?

Donald Lambert, a technical analyst, created the CCI, or Commodity Channel Index, which he first published in 1980. CCI is calculated regarding CCI can be used both as trend-detector or an oscillator. As an oscillator most traders believe in static predefined levels. Overbought and oversold candles which are clear in the chart could be used as sell and buy signals.

During my trading career I’ve noticed that there might be some reversal points for the CCI. I believe CCI could have to potential to reverse more from lately reversal point. Of course, just like other trading strategies we are talking about probabilities. We do not expect a win trade each time.

On price chart

Now this the question! What price should the instrument reach that CCI turns to be equal to our reversing aim for CCI? Imagine we have found last important bearish reversal of CCI in 200. Now, if we need the CCI to be 200 what price should we wait for?

How to calculate?

This is the CCI formula:

CCI = (Typical Price - SMA of TP) / (0.015 x Mean Deviation)

Where, Typical Price (TP) = (High + Low + Close)/3

For probable reversing points, high and low pivots of 50 bars have been used.

So we do have an Upper CCI and a Lower CCI. They are valid until the next pivot is available.

By relocating factors in CCI formula you can reach the “Typical Price”.

“

Typical Price = CCI (0.015 * Mean Deviation) + SMA of TP

So we could have a Support or Resistance by replacing CCI with Upper and Lower CCI.

A buy signal is valid if the trend is bullish (or “trend matter” is off) and lowest low of last 2 candles is lower than support and close is greater than both support and open.

A Sell signal is produced in opposite situation.

There are 2+1 options for trend!

Trend matter box is on by default, which means we’ll just open trades in direction of the trend. It’s available to turn it off.

Other 2 options are cross and slope. Cross calculated by comparing fast SMA and slow SMA. The slope one differentiate slow SMA to last “n” one.

Considering last day and today highest ATR as the ATR to calculating SL and TP is our unique technique.

AI Moving Average (Expo)█ Overview

The AI Moving Average indicator is a trading tool that uses an AI-based K-nearest neighbors (KNN) algorithm to analyze and interpret patterns in price data. It combines the logic of a traditional moving average with artificial intelligence, creating an adaptive and robust indicator that can identify strong trends and key market levels.

█ How It Works

The algorithm collects data points and applies a KNN-weighted approach to classify price movement as either bullish or bearish. For each data point, the algorithm checks if the price is above or below the calculated moving average. If the price is above the moving average, it's labeled as bullish (1), and if it's below, it's labeled as bearish (0). The K-Nearest Neighbors (KNN) is an instance-based learning algorithm used in classification and regression tasks. It works on a principle of voting, where a new data point is classified based on the majority label of its 'k' nearest neighbors.

The algorithm's use of a KNN-weighted approach adds a layer of intelligence to the traditional moving average analysis. By considering not just the price relative to a moving average but also taking into account the relationships and similarities between different data points, it offers a nuanced and robust classification of price movements.

This combination of data collection, labeling, and KNN-weighted classification turns the AI Moving Average (Expo) Indicator into a dynamic tool that can adapt to changing market conditions, making it suitable for various trading strategies and market environments.

█ How to Use

Dynamic Trend Recognition

The color-coded moving average line helps traders quickly identify market trends. Green represents bullish, red for bearish, and blue for neutrality.

Trend Strength

By adjusting certain settings within the AI Moving Average (Expo) Indicator, such as using a higher 'k' value and increasing the number of data points, traders can gain real-time insights into strong trends. A higher 'k' value makes the prediction model more resilient to noise, emphasizing pronounced trends, while more data points provide a comprehensive view of the market direction. Together, these adjustments enable the indicator to display only robust trends on the chart, allowing traders to focus exclusively on significant market movements and strong trends.

Key SR Levels

Traders can utilize the indicator to identify key support and resistance levels that are derived from the prevailing trend movement. The derived support and resistance levels are not just based on historical data but are dynamically adjusted with the current trend, making them highly responsive to market changes.

█ Settings

k (Neighbors): Number of neighbors in the KNN algorithm. Increasing 'k' makes predictions more resilient to noise but may decrease sensitivity to local variations.

n (DataPoints): Number of data points considered in AI analysis. This affects how the AI interprets patterns in the price data.

maType (Select MA): Type of moving average applied. Options allow for different smoothing techniques to emphasize or dampen aspects of price movement.

length: Length of the moving average. A greater length creates a smoother curve but might lag recent price changes.

dataToClassify: Source data for classifying price as bullish or bearish. It can be adjusted to consider different aspects of price information

dataForMovingAverage: Source data for calculating the moving average. Different selections may emphasize different aspects of price movement.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

UtilsLibrary "Utils"

Utility functions. Mathematics, colors, and auxiliary algorithms.

setTheme(vc, theme)

Set theme for levels (predefined colors).

Parameters:

vc : (valueColorSpectrum) Object to associate a color with a value, taking into account the previous value and its levels.

theme : (int) Theme (predefined colors).

0 = 'User defined'

1 = 'Spectrum Blue-Green-Red'

2 = 'Monokai'

3 = 'Green'

4 = 'Purple'

5 = 'Blue'

6 = 'Red'

Returns: (void)

setTheme(vc, colorLevel_Lv1, colorLevel_Lv1_Lv2, colorLevel_Lv2_Lv3, colorLevel_Lv3_Lv4, colorLevel_Lv4_Lv5, colorLevel_Lv5)

Set theme for levels (customized colors).

Parameters:

vc : (valueColorSpectrum) Object to associate a color with a value, taking into account the previous value and its levels

colorLevel_Lv1 : (color) Color associeted with value when below Level 1.

colorLevel_Lv1_Lv2 : (color) Color associeted with value when between Level 1 and 2.

colorLevel_Lv2_Lv3 : (color) Color associeted with value when between Level 2 and 3.

colorLevel_Lv3_Lv4 : (color) Color associeted with value when between Level 3 and 4.

colorLevel_Lv4_Lv5 : (color) Color associeted with value when between Level 4 and 5.

colorLevel_Lv5 : (color) Color associeted with value when above Level 5.

Returns: (void)

setCurrentColorValue(vc)

Set color to a current value, taking into account the previous value and its levels

Parameters:

vc : (valueColorSpectrum) Object to associate a color with a value, taking into account the previous value and its levels

Returns: (void)

setCurrentColorValue(vc, gradient)

Set color to a current value, taking into account the previous value.

Parameters:

vc : (valueColor) Object to associate a color with a value, taking into account the previous value

gradient

Returns: (void)

setCustomLevels(vc, level1, level2, level3, level4, level5)

Set boundaries for custom levels.

Parameters:

vc : (valueColorSpectrum) Object to associate a color with a value, taking into account the previous value and its levels

level1 : (float) Boundary for level 1

level2 : (float) Boundary for level 2

level3 : (float) Boundary for level 3

level4 : (float) Boundary for level 4

level5 : (float) Boundary for level 5

Returns: (void)

getPeriodicColor(originalColor, density)

Returns a periodic color. Useful for creating dotted lines for example.

Parameters:

originalColor : (color) Original color.

density : (float) Density of color. Expression used in modulo to obtain the integer remainder.

If the remainder equals zero, the color appears, otherwise it remains hidden.

Returns: (color) Periodic color.

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source : (float) Source

sampleLength : (int) Sample Length

pcntAbove : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

valueColorSpectrum

# Object to associate a color with a value, taking into account the previous value and its levels.

Fields:

currentValue

previousValue

level1

level2

level3

level4

level5

currentColorValue

colorLevel_Lv1

colorLevel_Lv1_Lv2

colorLevel_Lv2_Lv3

colorLevel_Lv3_Lv4

colorLevel_Lv4_Lv5

colorLevel_Lv5

theme

valueColor

# Object to associate a color with a value, taking into account the previous value

Fields:

currentValue

previousValue

currentColorValue

colorUp

colorDown

Fair value bands / quantifytools— Overview

Fair value bands, like other band tools, depict dynamic points in price where price behaviour is normal or abnormal, i.e. trading at/around mean (price at fair value) or deviating from mean (price outside fair value). Unlike constantly readjusting standard deviation based bands, fair value bands are designed to be smooth and constant, based on typical historical deviations. The script calculates pivots that take place above/below fair value basis and forms median deviation bands based on this information. These points are then multiplied up to 3, representing more extreme deviations.

By default, the script uses OHLC4 and SMA 20 as basis for the bands. Users can form their preferred fair value basis using following options:

Price source

- Standard OHLC values

- HL2 (High + low / 2)

- OHLC4 (Open + high + low + close / 4)

- HLC3 (High + low + close / 3)

- HLCC4 (High + low + close + close / 4)

Smoothing

- SMA

- EMA

- HMA

- RMA

- WMA

- VWMA

- Median

Once fair value basis is established, some additional customization options can be employed:

Trend mode

Direction based

Cross based

Trend modes affect fair value basis color that indicates trend direction. Direction based trend considers only the direction of the defined fair value basis, i.e. pointing up is considered an uptrend, vice versa for downtrend. Cross based trends activate when selected source (same options as price source) crosses fair value basis. These sources can be set individually for uptrend/downtrend cross conditions. By default, the script uses cross based trend mode with low and high as sources.

Cross based (downtrend not triggered) vs. direction based (downtrend triggered):

Threshold band

Threshold band is calculated using typical deviations when price is trading at fair value basis. In other words, a little bit of "wiggle room" is added around the mean based on expected deviation. This feature is useful for cross based trends, as it allows filtering insignificant crosses that are more likely just noise. By default, threshold band is calculated based on 1x median deviation from mean. Users can increase/decrease threshold band width via input menu for more/less noise filtering, e.g. 2x threshold band width would require price to cross wiggle room that is 2x wider than typical, 0x erases threshold band altogether.

Deviation bands

Width of deviation bands by default is based on 1x median deviations and can be increased/decreased in a similar manner to threshold bands.

Each combination of customization options produces varying behaviour in the bands. To measure the behaviour and finding fairest representation of fair and unfair value, some data is gathered.

— Fair value metrics

Space between each band is considered a lot, named +3, +2, +1, -1, -2, -3. For each lot, time spent and volume relative to volume moving average (SMA 20) is recorded each time price is trading in a given lot:

Depending on the asset, timeframe and chosen fair value basis, shape of the distributions vary. However, practically always time is distributed in a normal bell curve shape, being highest at lots +1 to -1, gradually decreasing the further price is from the mean. This is hardly surprising, but it allows accurately determining dynamic areas of normal and abnormal price behaviour (i.e. low risk area between +1 and -1, high risk area between +-2 to +-3). Volume on the other hand is typically distributed the other way around, being lowest at lots +1 to -1 and highest at +-2 to +-3. When time and volume are distributed like so, we can conclude that 1) price being outside fair value is a rare event and 2) the more price is outside fair value, the more anomaly behaviour in volume we tend to find.

Viewing metric calculations

Metric calculation highlights can be enabled from the input menu, resulting in a lot based coloring and visibility of each lot counter (time, cumulative relative volume and average relative volume) in data window:

— Alerts

Available alerts are the following:

Individual

- High crossing deviation band (bands +1 to +3 )

- Low crossing deviation band (bands -1 to -3 )

- Low at threshold band in an uptrend

- High at threshold band in a downtrend

- New uptrend

- New downtrend

Grouped

- New uptrend or downtrend

- Deviation band cross (+1 or -1)

- Deviation band cross (+2 or -2)

- Deviation band cross (+3 or -3)

— Practical guide

Example #1 : Risk on/risk off trend following

Ideal trend stays inside fair value and provides sufficient cool offs between the moves. When this is the case, fair value bands can be used for sensible entry/exit levels within the trend.

Example #2 : Mean reversions

When price shows exuberance into an extreme deviation, followed by a stall and signs of exhaustion (wicks), an opportunity for mean reversion emerges. The higher the deviation, the more volatility in the move, the more signalling of exhaustion, the better.

Example #3 : Tweaking bands for desired behaviour

The faster the length of fair value basis, the more momentum price needs to hit extreme deviation levels, as bands too are moving faster alongside price. Decreasing fair value basis length typically leads to more quick and aggressive deviations and less steady trends outside fair value.

SUPER MACD📈 MACD Indicator Update - Version 2

🔹 New Features and Improvements:

1️⃣ New MACD Calculation Options:

Users can now choose from various Moving Averages to calculate the MACD. The default options are SMA (Simple Moving Average) and EMA (Exponential Moving Average), but there are 14 other versions available to experiment with:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

2️⃣ Improved Input Visibility and Organization:

We’ve reorganized the inputs so that the most commonly used ones are now placed at the beginning for quicker and more convenient configuration.

3️⃣ Bug Fixes and Code Improvements:

Minor bugs have been fixed, and the code has been optimized for better stability and performance. The code is now cleaner and fully functional in version 6.

4️⃣ Cometreon Public Library Integration:

To lighten the code and improve its modularity, we’ve integrated the Cometreon public library. This makes the code more efficient and reduces the need to duplicate common functions.

☄️ With this update, the MACD indicator becomes even more versatile and user-friendly, offering a wide range of calculation methods and an improved interface!

Dynamic Zones of On Chart Stochastic [Loxx]Dynamic Zones of On Chart Stochastic is a Stochastic indicator that sits on top of the chart instead of below as an oscillator. Dynamic zone levels are included to find breakouts/breakdowns and reversals.

What is the Stochastic Oscillator?

A stochastic oscillator is a momentum indicator comparing a particular closing price of a security to a range of its prices over a certain period of time. The sensitivity of the oscillator to market movements is reducible by adjusting that time period or by taking a moving average of the result. It is used to generate overbought and oversold trading signals, utilizing a 0–100 bounded range of values.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included

Bar coloring

Signals

Alerts

4 types of signal smoothing

Fisher Transform w/ Dynamic Zones [Loxx]What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included

3 signal types

Bar coloring

Alerts

Channels fill

Loxx's Expanded Source Types

Dynamic Zone Range on OMA [Loxx]Dynamic Zone Range on OMA is an One More Moving Average oscillator with Dynamic Zones.

What is the One More Moving Average (OMA)?

The usual story goes something like this : which is the best moving average? Everyone that ever started to do any kind of technical analysis was pulled into this "game". Comparing, testing, looking for new ones, testing ...

The idea of this one is simple: it should not be itself, but it should be a kind of a chameleon - it should "imitate" as much other moving averages as it can. So the need for zillion different moving averages would diminish. And it should have some extra, of course:

The extras:

it has to be smooth

it has to be able to "change speed" without length change

it has to be able to adapt or not (since it has to "imitate" the non-adaptive as well as the adaptive ones)

The steps:

Smoothing - compared are the simple moving average (that is the basis and the first step of this indicator - a smoothed simple moving average with as little lag added as it is possible and as close to the original as it is possible) Speed 1 and non-adaptive are the reference for this basic setup.

Speed changing - same chart only added one more average with "speeds" 2 and 3 (for comparison purposes only here)

Finally - adapting : same chart with SMA compared to one more average with speed 1 but adaptive (so this parameters would make it a "smoothed adaptive simple average") Adapting part is a modified Kaufman adapting way and this part (the adapting part) may be a subject for changes in the future (it is giving satisfactory results, but if or when I find a better way, it will be implemented here)

Some comparisons for different speed settings (all the comparisons are without adaptive turned on, and are approximate. Approximation comes from a fact that it is impossible to get exactly the same values from only one way of calculation, and frankly, I even did not try to get those same values).

speed 0.5 - T3 (0.618 Tilson)

speed 2.5 - T3 (0.618 Fulks/Matulich)

speed 1 - SMA , harmonic mean

speed 2 - LWMA

speed 7 - very similar to Hull and TEMA

speed 8 - very similar to LSMA and Linear regression value

Parameters:

Length - length (period) for averaging

Source - price to use for averaging

Speed - desired speed (i limited to -1.5 on the lower side but it even does not need that limit - some interesting results with speeds that are less than 0 can be achieved)

Adaptive - does it adapt or not

Variety Moving Averages w/ Dynamic Zones contains 33 source types and 35+ moving averages with double dynamic zones levels.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included

4 signal types

Bar coloring

Alerts

Channels fill

Variety Moving Averages w/ Dynamic Zones [Loxx]Variety Moving Averages w/ Dynamic Zones contains 33 source types and 35+ moving averages with double dynamic zones levels.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included

Bar coloring

Alerts

Channels fill

Loxx's Expanded Source Types

35+ moving average types

Rainbow Oscillator The Rainbow Oscillator is a technical indicator that shows prices in overbought or oversold areas. That allows you to catch the price reversal point.

---------------

FEATURES

---------------

.:: Dynamic levels ::.

The indicator levels are divided into several zones, which have a fibonacci ratio. Zones determine the overbought/oversold level. Blue and green level zones are better for buying, red and orange for selling. Dynamic levels are used as replacements for classic levels such as -100 and 100 for the CCI indicator or 30 and 70 for the RSI indicator. Dynamic levels work much better than static levels, as they are more adaptive to the current market situation.

.:: Composite oscillator (3 in 1) ::.

The main signal line of the indicator includes all three oscillators RSI, CCI, Stoch in different ratios. In the settings, you can change the proportions or completely remove one of the oscillators by setting its weight to 0

.:: CCI + RSI + Stoch ratio setting ::.

Each of the oscillators has its own weight in the calculation formula: w2 * cci ( + w1 * ( rsi - 50) + (1 - w2 - w1) * ( stoch - 50), this allows you to create the resulting oscillator from all indicators, depending on the weight of each of them. Each weight value must be between 0 and 1 so that the sum of all weights does not exceed 1.

.:: Smoothing levels and lines of the oscillator ::.

Smoothing the oscillator readings allows you to filter out the noise and get more accurate data. Level offset allows you to customize the support for inputs.

.:: Market Flat ::.

Dynamic creation of levels allows you to find in the price reversal zone, even when the price is in a flat

.:: Sources ::.

You can change the data source for the indicator to the number of longs and shorts for the selected asset. For example, BTCUSDLONGS / BTCUSDSHORTS is perfect for Bitcoin, then the oscillator will work on this data and will not use the quote price.

.:: Trend Detection ::.

The main line of the oscillator has 2 colors - green and red. Red means downtrend, green means uptrend. Trend reversal points are most often found in overbought and oversold zones.

.:: Alerts ::.

Alerts inside for next events: Buy (blue point) Sell (red point) and TrendReversal (change line color)

----------------

TRADING

—-------------

There are several possible entry points for the indicator, let's consider them all.

1) Trend reversal.

Long entry: The indicator line is in the green zone below 0 (oversold), while the line changes color from red (downward) to green (upward)

Short entry: The indicator line is in the red zone above the 0 (overbought) mark, while the line changes color from green to red.

2) Red and blue dots.

Long entry: Blue dot

Short Entry: Red Dot

I prefer to use the first trading method.

----------------

SETTINGS

----------------

.:: Trend Filter (checkbox) ::.

Use trend confirmation for red/blue dots. When enabled, the blue dot requires an uptrend, red dot requires downtrend confirmation before appearing.

.:: Use long/shorts (checkbox) ::.

Change formula to use longs and shorts positions as data source (instead of quote price)

.:: RSI weight / CCI weight / Stoch weight ::.

Weight control coefficients for RSI and CCI indicators, respectively. When you set RSI Weight = 0, equalize the combo of CCI and Stoch , when RSI Weight is zero and CCI Weight is equal to the oscillator value will be plotted

only from Stoch . Intermediate values have a high degree of measurement of each of the three oscillators in percentage terms from 0 to 100. The calculation uses the formula: w2 * cci ( + w1 * ( rsi - 50) + (1 - w2 - w1) * ( stoch - 50),

where w1 is RSI Weight and w2 is CCI Weight, Stoch weight is calculated on the fly as (1 - w2 - w1), so the sum of w1 + w2 should not exceed 1, in this case Stoch will work as opposed to CCI and RSI .

.:: Oscillograph fast and slow periods ::.

The fast period is the period for the moving average used to smooth CCI, RSI and Stoch. The slow period is the same. The fast period must always be less than the slow period.

.:: Oscillograph samples period::.

The period of smoothing the total values of indicators - creates a fast and slow main lines of the oscillator.

.:: Oscillograph samples count::.

How many times smoothing applied to source data.

.:: Oscillator samples type ::.

Smoothing line type e.g. EMA, SMA, RMA …

.:: Level period ::.

Periodically moving averages used to form the levels (zone) of the Rainbow Oscillator indicator

.:: Level offset ::.

Additional setting for shifting levels from zero points. Can be useful for absorbing levels and filtering input signals. The default is 0.

.:: Level redundant ::.

It characterizes the severity of the state at each iteration of the level of the disease. If set to 1 - the levels will not decrease when the oscillator values fall. If it has a value of 0.99 - the levels are reduced by 0.01

each has an oscillator in 1% of cases and is pressed to 0 by more aggressive ones.

.:: Level smooth samples ::.

setting allows you to set the number of strokes per level. Measuring the number of averages with the definition of the type of moving averages

.:: Level MA Type ::.

Type of moving average, average for the formation of a smoothing overbought and oversold zone

RSI - Dynamic Overbought/Oversold RangeDefault overbought/oversold levels of RSI does not hold good for instruments which are trending well. It happens often that instruments keep trading in single half of the range for prolonged time without even touching the other half. This also came up often in tradingview pine chat discussions where I participate regularly.

Hence, thought of creating this script to help other scriptors in finding different methods to derive dynamic high/low range of RSI. This can also be adopted for other range bound oscillators - though not inlcuded in this script.

⬜ Method

▶ Derive multitimeframe RSI. Parameters - Resolution, Source and Length are pretty straight forward. Repaint when unchecked uses previous bar value.

▶ Dynamic range detection follows below steps.

Get highest and lowest of the oscillator source for Range Length period.

Use Detection method further to refine the highest and lowest range. If detection method is "highlow", then it looks for lowest value for high range and highest value for low range. If not, uses moving average.

◽Note: Detection range length is used only for finding highest and lowest of Oscillator value ranges. Further detection range method of highlow and other moving average types use Oscillator length.

Screener - Mean Reversion Channel█ OVERVIEW

This is Screener script for Mean Reversion Channel Indicator

█ Description & How To Use

The screener works by scanning through up to 40 symbols and list down symbols that are currently within Overbought/Oversold Zone as defined by Mean Reversion Channel indicator.

The Overbought/Oversold Zone are further categorized and sorted by:

Strong : Indicated by "(Strong)" next to the symbol name

Normal : Indicated by the absence of "(Strong)" or "(Weak)" next to the symbol name

Weak : Indicated by "(Weak)" next to the symbol name

Notes: Refer to chart above to see how the Zone are categorized.

Notes: If the screener displays "Nothing Interesting". It simply means none of the screened assets are within the Overbought/Oversold Zone.

█ Features

- Scan up to 40 symbols at a time (By default, no asset is define. Once configured all the symbols you required, remember to save as default to save you from pain of configuring it again in the future)

- Options to scan by zones

- Custom Timeframe

█ Limitation

Due to multiple use of security() function required to call other symbols, expect the screener to be slow at certain times

█ Disclaimer

Past performance is not an indicator of future results.

My opinions and research are my own and do not constitute financial advice in any way whatsoever.

Nothing published by me constitutes an investment recommendation, nor should any data or Content published by me be relied upon for any investment/trading activities.

I strongly recommends that you perform your own independent research and/or speak with a qualified investment professional before making any financial decisions.

Any ideas to further improve this indicator are welcome :)

Credit: QuantNomad for his script idea on custom screener

Mean Reversion Channel - (fareid's MRI Variant)Description :

Mean Reversion Channel objective, based on Mean Reversion theory ( everything has a tendency to revert back to its mean), is to help visualizing:

Inner Channel -> Dynamic Support and Resistance

Outer Channel -> Overbought/Oversold Zone which may signal consolidation phase or potential reversal due to unsustainable move

Details on some of the filtering type used for mean calculation can be read in Ehlers Technical Papers: "Swiss Army Knife Indicator" and/or his book "Cybernetics Analysis for Stock and Futures"

Disclaimer:

These study scripts was built only to test/visualize an idea to see its viability and if it can be used to optimize existing strategy.

Any ideas to further improve this indicator are welcome :)

Automatic Fibonacci Pivot Point S/R LevelsThis is a great tool to find confluences between Fibonacci Pivot point on various time frames.

Fib Pivots used

23.6%

38.2%

50%

61.8%

76.4%

100%

127.2%

141.4%

161.8%

200%

If price is between two levels on the update the lines shift

Yearly Pivots shown on 1m - Daily timeframes

PIvots recalculate on every day

Monthly pivots show on 1m - 60m timeframes

Pivots recalculate every hour

Weekly pivots show on 1m - 15m timeframes

Pivots recalculate every 30m

There is a lot of code but it got the job done.

It would easy to interchange if you prefer different types of pivots

It would be easy to add an on/off if you dont want so many levels on your smaller time frames

If anyone can streamline it please do