30D Vs 90D Historical VolatilityVolatility equals risk for an underlying asset's price meaning bullish volatility is bearish for prices while bearish volatility is bullish. This compares 30-Day Historical Volatility to 90-Day Historical Volatility.

When the 30-Day crosses under the 90-day, this is typically when asset prices enter a bullish trend.

Conversely, When the 30-Day crosses above the 90-Day, this is when asset prices enter a bearish trend.

Peaks in volatility are bullish divergences while troughs are bearish divergences.

Educational

4AM-5AM BRT HighlighterThe 4AM-5AM BRT Highlighter is a simple yet effective tool designed to visually mark your preferred trading time on the chart. It highlights the period between 4:00 AM and 5:00 AM Brazilian Time (BRT/UTC-3) by default, helping you stay focused and aware of your prime trading window.

Key Features:

Clear Visual Highlight: Colors the background of your chart during the chosen timeframe, making it easy to see when your trading session starts and ends.

Customizable Colors: Easily adjust the highlight color and transparency to suit your visual preferences.

Accurate Time Conversion: Automatically accounts for Brazilian Time (BRT), ensuring the highlight appears correctly no matter your chart’s default timezone.

Whether you're trading currencies, metals, indexes, or cryptocurrencies, this indicator helps you maintain focus during your dedicated trading hour by clearly marking your active period on the chart.

Buy and Sell Signals Based on SMI {K28}Buy/Sell Signals Based on SMI

This indicator provides buy and sell signals based on the Stochastic Momentum Index (SMI) to assist traders in identifying potential entry and exit points in the market. Here’s how to effectively use this indicator:

Usage Instructions:

Signal Interpretation:

No signal is 100% guaranteed

Green Labels: Indicate strong buy signals when the SMI crosses above its EMA, especially if the candle is green (closing price higher than opening price).

Red Labels: Indicate strong sell signals when the SMI crosses below its EMA.

Cautious Signals:

Blue Buy Labels: These buy signals appear when the SMI is in a cautious zone (between -20 and 20). They may not be as reliable, so confirm these signals with other indicators before acting.

Yellow Sell Labels: These buy signals appear when the SMI is in a cautious zone (between -20 and 20). They may not be as reliable, so confirm these signals with other indicators before acting.

Gray Buy and Sell Labels: Indicate potential false signals (when the SMI is overbought or oversold). Use other confirmation indicators to verify these signals.

Trade Strategy:

This indicator is designed for traders looking to make small, consistent profits. Focus on executing more trades rather than waiting for larger price movements.

Be mindful that the indicator may yield frequent signals, so it's essential to maintain discipline and only take trades that meet your criteria for confirmation.

Important Notes:

Caution with Signals: Always exercise caution when acting on blue or gray labels. These may indicate less reliable signals, so it's crucial to confirm with additional indicators.

No Perfect Indicator: Please remember that no trading indicator is perfect. Use this indicator at your own risk, and consider incorporating risk management strategies into your trading plan.

Conclusion:

By employing this SMI indicator, you can enhance your trading strategy focused on generating small, consistent profits through frequent trades. However, always verify signals and stay aware of market conditions to optimize your trading performance.

Smart Money Setup 07 [TradingFinder] Liquidity Hunts & Minor OB🔵 Introduction

The Smart Money Concept relies on analyzing market structure, tracking liquidity flows, and identifying order blocks. Research indicates that traders who apply these methods can improve their accuracy in predicting market movements by up to 30%.

These elements allow traders to understand the behavior of market makers, including banks and large financial institutions, which have the ability to influence price movements and shape major market trends. By recognizing how these entities operate, traders can align their strategies with Smart Money actions and better anticipate shifts in the market.

Smart Money typically enters the market at points of high liquidity where trading opportunities are more attractive. By following these liquidity flows, professional traders can position themselves at market reversal points, leading to profitable trades.

The Smart Money Setup 07 indicator has been specifically designed to detect these complex patterns. Using advanced algorithms, this indicator automatically identifies both bullish and bearish trading setups, assisting traders in discovering hidden market opportunities.

As a powerful technical analysis tool, the Smart Money Setup indicator helps predict the actions of major market participants and highlights optimal entry and exit points. Essentially, this tool enables traders to act like institutional investors and market makers, making the most of price fluctuations in their favor.

Ultimately, the Smart Money Setup 07 indicator transforms complex technical analysis into a simple and practical tool. By detecting order blocks and liquidity zones, this tool helps traders execute their strategies with greater precision, leading to more informed and successful trading decisions.

🟣 Bullish Setup

🟣 Bearish Setup

🔵 How to Use

One of the key strengths of the Smart Money Setup 07 indicator is its ability to accurately identify order blocks and analyze liquidity flows. Order blocks represent areas where large buy or sell orders are placed by Smart Money investors, which often indicate key reversal points in the market. Traders can use these order blocks to pinpoint potential entry and exit opportunities.

The Smart Money Setup indicator detects and visually displays these order blocks on the chart, helping traders identify the best zones to enter or exit trades. Since these zones are frequently used by large institutional investors, following these blocks allows traders to capitalize on price fluctuations and trade with confidence.

🟣 Bullish Smart Money Setup

A Bullish Smart Money Setup forms when the market creates Higher Lows and Higher Highs. In this situation, the indicator analyzes pivot points, liquidity flows, and order blocks to identify buy opportunities. Liquidity points in these setups indicate areas where Smart Money is likely to enter long positions.

In the bullish setup image, multiple Higher Lows and Higher Highs are formed. The green zone represents a Bullish Order Block, signaling traders to enter a long trade. The Smart Money Setup indicator displays a green arrow, indicating a high-probability upward price movement from this liquidity zone.

🟣 Bearish Smart Money Setup

A Bearish Smart Money Setup occurs when the market structure shows Lower Highs and Lower Lows, indicating weakness in price. The indicator identifies these patterns and highlights potential sell opportunities. Liquidity points in this setup mark areas where Smart Money enters sell positions.

In the bearish setup image, a Lower High is followed by a Lower Low, with the red liquidity zone acting as a Bearish Order Block. The Smart Money Setup indicator shows a red arrow, signaling a likely downward move, offering traders an opportunity to enter short positions.

🔵 Settings

Pivot Period : This setting determines how many candles are needed to form a pivot point. A default value of 2 is optimal for quickly identifying key pivot points in price action.

Order Block Validity Period : This parameter defines the lifespan of an order block. Traders can adjust how long each order block remains valid. For instance, setting it to 500 means that an order block will be valid for 500 bars after its formation.

Mitigation Level OB : This setting allows traders to select whether order blocks should be based on the "Proximal," "50% OB," or "Distal" levels, helping traders manage risk more effectively.

Order Block Refinement : Traders can refine the order blocks with precision. The indicator offers two refinement modes: Defensive and Aggressive. The Defensive mode identifies safer order blocks, while the Aggressive mode targets higher-risk blocks with the potential for larger reversals.

🔵 Conclusion

The Smart Money Setup 07 indicator is a powerful tool for identifying key Smart Money movements in the market. It provides traders with essential insights for making informed trading decisions, particularly when combined with technical analysis and liquidity flow analysis. This indicator allows traders to accurately pinpoint entry and exit points, helping them maximize profits and minimize risk.

By offering a range of customizable settings, the Smart Money Setup indicator adapts to different trading styles and strategies. Furthermore, its ability to detect order blocks and identify supply and demand zones makes it an indispensable tool for any trader looking to enhance their strategy.

In conclusion, the Smart Money Setup 07 is a crucial tool for traders aiming to optimize their trading performance. By utilizing the concepts of Smart Money in technical analysis, traders can make more precise decisions and take advantage of market fluctuations.

Keltner Channel Strategy by Kevin DaveyKeltner Channel Strategy Description

The Keltner Channel Strategy is a volatility-based trading approach that uses the Keltner Channel, a technical indicator derived from the Exponential Moving Average (EMA) and Average True Range (ATR). The strategy helps identify potential breakout or mean-reversion opportunities in the market by plotting upper and lower bands around a central EMA, with the channel width determined by a multiplier of the ATR.

Components:

1. Exponential Moving Average (EMA):

The EMA smooths price data by placing greater weight on recent prices, allowing traders to track the market’s underlying trend more effectively than a simple moving average (SMA). In this strategy, a 20-period EMA is used as the midline of the Keltner Channel.

2. Average True Range (ATR):

The ATR measures market volatility over a 14-period lookback. By calculating the average of the true ranges (the greatest of the current high minus the current low, the absolute value of the current high minus the previous close, or the absolute value of the current low minus the previous close), the ATR captures how much an asset typically moves over a given period.

3. Keltner Channel:

The upper and lower boundaries are set by adding or subtracting 1.5 times the ATR from the EMA. These boundaries create a dynamic range that adjusts with market volatility.

Trading Logic:

• Long Entry Condition: The strategy enters a long position when the closing price falls below the lower Keltner Channel, indicating a potential buying opportunity at a support level.

• Short Entry Condition: The strategy enters a short position when the closing price exceeds the upper Keltner Channel, signaling a potential selling opportunity at a resistance level.

The strategy plots the upper and lower Keltner Channels and the EMA on the chart, providing a visual representation of support and resistance levels based on market volatility.

Scientific Support for Volatility-Based Strategies:

The use of volatility-based indicators like the Keltner Channel is supported by numerous studies on price momentum and volatility trading. Research has shown that breakout strategies, particularly those leveraging volatility bands such as the Keltner Channel or Bollinger Bands, can be effective in capturing trends and reversals in both trending and mean-reverting markets  .

Who is Kevin Davey?

Kevin Davey is a highly respected algorithmic trader, author, and educator, known for his systematic approach to building and optimizing trading strategies. With over 25 years of experience in the markets, Davey has earned a reputation as an expert in quantitative and rule-based trading. He is particularly well-known for winning several World Cup Trading Championships, where he consistently demonstrated high returns with low risk.

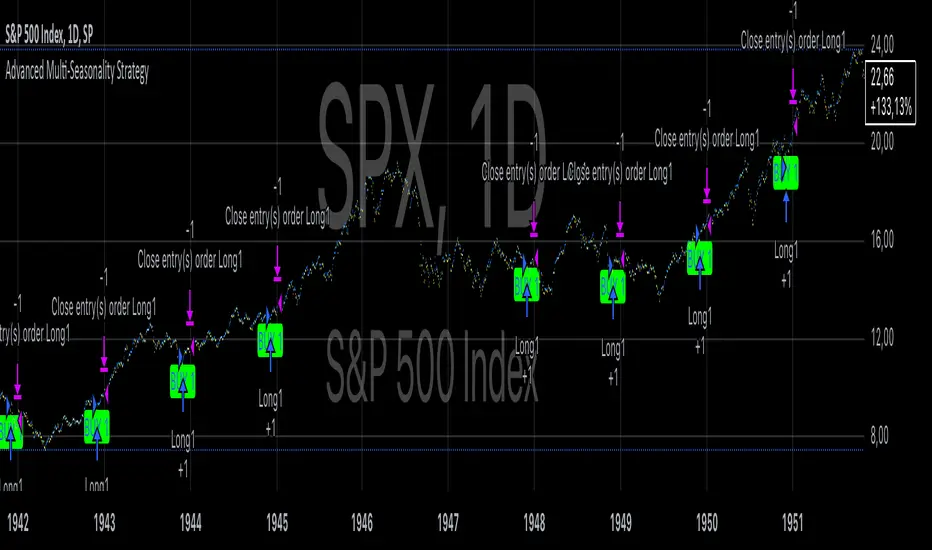

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

Statistical ArbitrageThe Statistical Arbitrage Strategy, also known as pairs trading, is a quantitative trading method that capitalizes on price discrepancies between two correlated assets. The strategy assumes that over time, the prices of these two assets will revert to their historical relationship. The core idea is to take advantage of mean reversion, a principle suggesting that asset prices will revert to their long-term average after deviating significantly.

Strategy Mechanics:

1. Selection of Correlated Assets:

• The strategy focuses on two historically correlated assets (e.g., equity index futures like Dow Jones Mini and S&P 500 Mini). These assets tend to move in the same direction due to similar underlying fundamentals, such as overall market conditions. By tracking their relative prices, the strategy seeks to exploit temporary mispricings.

2. Spread Calculation:

• The spread is the difference between the prices of the two assets. This spread represents the relationship between the assets and serves as the basis for determining when to enter or exit trades.

3. Mean and Standard Deviation:

• The historical average (mean) of the spread is calculated using a Simple Moving Average (SMA) over a chosen period. The strategy also computes the standard deviation (volatility) of the spread, which measures how far the spread has deviated from the mean over time. This allows the strategy to define statistically significant price deviations.

4. Entry Signal (Mean Reversion):

• A buy signal is triggered when the spread falls below the mean by a multiple (e.g., two) of the standard deviation. This indicates that one asset is temporarily undervalued relative to the other, and the strategy expects the spread to revert to its mean, generating profits as the prices converge.

5. Exit Signal:

• The strategy exits the trade when the spread reverts to the mean. At this point, the mispricing has been corrected, and the profit from the mean reversion is realized.

Academic Support:

Statistical arbitrage has been widely studied in finance and economics. Gatev, Goetzmann, and Rouwenhorst’s (2006) landmark study on pairs trading demonstrated that this strategy could generate excess returns in equity markets. Their research found that by focusing on historically correlated stocks, traders could identify pricing anomalies and profit from their eventual correction.

Additionally, Avellaneda and Lee (2010) explored statistical arbitrage in different asset classes and found that exploiting deviations in price relationships can offer a robust, market-neutral trading strategy. In these studies, the strategy’s success hinges on the stability of the relationship between the assets and the timely execution of trades when deviations occur.

Risks of Statistical Arbitrage:

1. Correlation Breakdown:

• One of the primary risks is the breakdown of correlation between the two assets. Statistical arbitrage assumes that the historical relationship between the assets will hold in the future. However, market conditions, company fundamentals, or external shocks (e.g., macroeconomic changes) can cause these assets to deviate permanently, leading to potential losses.

• For instance, if two equity indices historically move together but experience divergent economic conditions or policy changes, their prices may no longer revert to the expected mean.

2. Execution Risk:

• This strategy relies on efficient execution and tight spreads. In volatile or illiquid markets, the actual price at which trades are executed may differ significantly from expected prices, leading to slippage and reduced profits.

3. Market Risk:

• Although statistical arbitrage is designed to be market-neutral (i.e., not dependent on the overall market direction), it is not entirely risk-free. Systematic market shocks, such as financial crises or sudden shifts in market sentiment, can affect both assets simultaneously, causing the spread to widen rather than revert to the mean.

4. Model Risk:

• The assumptions underlying the strategy, particularly regarding mean reversion, may not always hold true. The model assumes that asset prices will return to their historical averages within a certain timeframe, but the timing and magnitude of mean reversion can be uncertain. Misestimating this timeframe can lead to extended drawdowns or unrealized losses.

5. Overfitting:

• Over-reliance on historical data to fine-tune the strategy parameters (e.g., the lookback period or standard deviation thresholds) may result in overfitting. This means that the strategy works well on past data but fails to perform in live markets due to changing conditions.

Conclusion:

The Statistical Arbitrage Strategy offers a systematic and quantitative approach to trading that capitalizes on temporary price inefficiencies between correlated assets. It has been proven to generate returns in academic studies and is widely used by hedge funds and institutional traders for its market-neutral characteristics. However, traders must be aware of the inherent risks, including correlation breakdown, execution risks, and the potential for prolonged deviations from the mean. Effective risk management, diversification, and constant monitoring are essential for successfully implementing this strategy in live markets.

BTC ETF Flow Trading SignalsTracks large money flows (500M+) across major Bitcoin ETFs (IBIT, BTCO, FBTC, ARKB, BITB)

Generates long/short signals based on institutional money movement

Shows flow trends and strength of movements

This script provides a foundation for comparing ETF inflows and Bitcoin price. The effectiveness of the analysis depends on the quality of the data and your interpretation of the results. Key levels of 500M and 350M Inflow/Outflow Enjoy

Collaboration with Vivid Vibrations

Enjoy & improve!

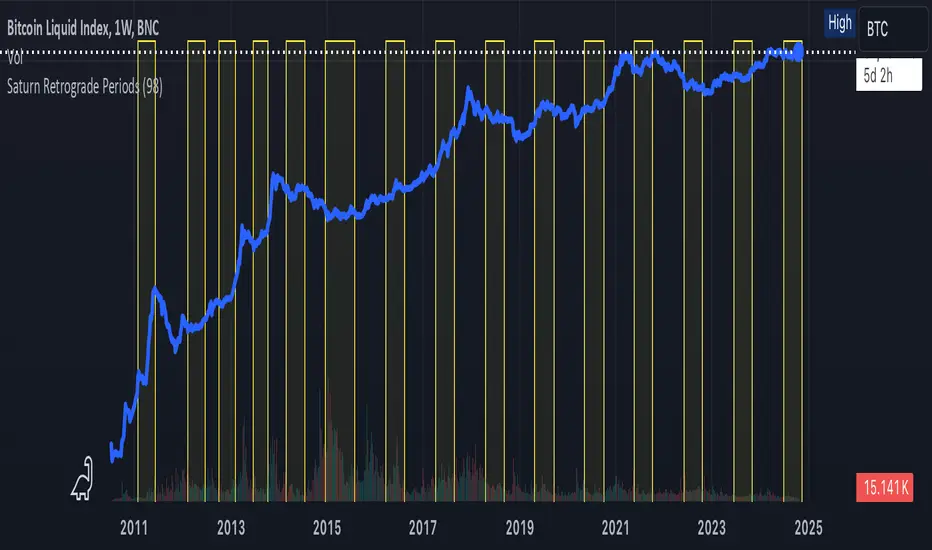

Saturn Retrograde PeriodsSaturn Retrograde Periods Visualizer for TradingView

This Pine Script visualizes all Saturn retrograde periods since 2009, including the current retrograde ending on November 15, 2024. The script overlays yellow boxes on your TradingView chart to highlight the exact periods of Saturn retrograde. It's a great tool for astrologically-inclined traders or those interested in market timing based on astrological events.

Key Features:

Full Historical Coverage: Displays Saturn retrograde periods from 2009 (the inception of Bitcoin) to the current retrograde ending in November 2024.

Customizable Appearance: You can easily adjust the color and opacity of the boxes directly from the script's settings window, making it flexible for various chart styles.

Visual Clarity: The boxes span the full vertical range of your chart, ensuring the retrograde periods are clearly visible over any asset, timeframe, or price action.

How to Use:

Add the script to your TradingView chart.

Adjust the color and opacity in the settings to suit your preferences.

View all relevant Saturn retrograde periods and analyze how these astrological events may align with price movements in your selected asset.

This script is perfect for traders and analysts who want to combine astrology with financial market analysis!

scripted by chat.gpt - version 1.0

Macros ICT KillZones [TradingFinder] Times & Price Trading Setup🔵 Introduction

ICT Macros, developed by Michael Huddleston, also known as ICT (Inner Circle Trader), is a powerful trading tool designed to help traders identify the best trading opportunities during key time intervals like the London and New York trading sessions.

For traders aiming to capitalize on market volatility, liquidity shifts, and Fair Value Gaps (FVG), understanding and using these critical time zones can significantly improve trading outcomes.

In today’s highly competitive financial markets, identifying the moments when the market is seeking buy-side or sell-side liquidity, or filling price imbalances, is essential for maximizing profitability.

The ICT Macros indicator is built on the renowned ICT time and price theory, which enables traders to track and leverage key market dynamics such as breaks of highs and lows, imbalances, and liquidity hunts.

This indicator automatically detects crucial market times and optimizes strategies for traders by highlighting the specific moments when price movements are most likely to occur. A standout feature of ICT Macros is its automatic adjustment for Daylight Saving Time (DST), ensuring that traders remain synced with the correct session times.

This means you can rely on accurate market timing without the need for manual updates, allowing you to focus on capturing profitable trades during critical timeframes.

🔵 How to Use

The ICT Macros indicator helps you capitalize on trading opportunities during key market moments, particularly when the market is breaking highs or lows, filling Fair Value Gaps (FVG), or addressing imbalances. This indicator is particularly beneficial for traders who seek to identify liquidity, market volatility, and price imbalances.

🟣 Sessions

London Sessions

London Macro 1 :

UTC Time : 06:33 to 07:00

New York Time : 02:33 to 03:00

London Macro 2 :

UTC Time : 08:03 to 08:30

New York Time : 04:03 to 04:30

New York Sessions

New York Macro AM 1 :

UTC Time : 12:50 to 13:10

New York Time : 08:50 to 09:10

New York Macro AM 2 :

UTC Time : 13:50 to 14:10

New York Time : 09:50 to 10:10

New York Macro AM 3 :

UTC Time : 14:50 to 15:10

New York Time : 10:50 to 11:10

New York Lunch Macro :

UTC Time : 15:50 to 16:10

New York Time : 11:50 to 12:10

New York PM Macro :

UTC Time : 17:10 to 17:40

New York Time : 13:10 to 13:40

New York Last Hour Macro :

UTC Time : 19:15 to 19:45

New York Time : 15:15 to 15:45

These time intervals adjust automatically based on Daylight Saving Time (DST), helping traders to enter or exit trades during key market moments when price volatility is high.

Below are the main applications of this tool and how to incorporate it into your trading strategies :

🟣 Combining ICT Macros with Trading Strategies

The ICT Macros indicator can easily be used in conjunction with various trading strategies. Two well-known strategies that can be combined with this indicator include:

ICT 2022 Trading Model : This model is designed based on identifying market liquidity, structural price changes, and Fair Value Gaps (FVG). By using ICT Macros, you can identify the key time intervals when the market is seeking liquidity, filling imbalances, or breaking through important highs and lows, allowing you to enter or exit trades at the right moment.

Silver Bullet Strategy : This strategy, which is built around liquidity hunting and rapid price movements, can work more accurately with the help of ICT Macros. The indicator pinpoints precise liquidity times, helping traders take advantage of market shifts caused by filling Fair Value Gaps or correcting imbalances.

🟣 Capitalizing on Price Volatility During Key Times

Large market algorithms often seek liquidity or fill Fair Value Gaps (FVG) during the intervals marked by ICT Macros. These periods are when price volatility increases, and traders can use these moments to enter or exit trades.

For example, if sell-side liquidity is drained and the market fills an imbalance, the price might move toward buy-side liquidity. By identifying these moments, which may also involve breaking a previous high or low, you can leverage rapid market fluctuations to your advantage.

🟣 Identifying Liquidity and Price Imbalances

One of the important uses of ICT Macros is identifying points where the market is seeking liquidity and correcting imbalances. You can determine high or low liquidity levels in the market before each ICT Macro, as well as Fair Value Gaps (FVG) and price imbalances that need to be filled, using them to adjust your trading strategy. This capability allows you to manage trades based on liquidity shifts or imbalance corrections without needing a bias toward a specific direction.

🔵 Settings

The ICT Macros indicator offers various customization options, allowing users to tailor it to their specific needs. Below are the main settings:

Time Zone Mode : You can select one of the following options to define how time is displayed:

UTC : For traders who need to work with Universal Time.

Session Local Time : The local time corresponding to the London or New York markets.

Your Time Zone : You can specify your own time zone (e.g., "UTC-4:00").

Your Time Zone : If you choose "Your Time Zone," you can set your specific time zone. By default, this is set to UTC-4:00.

Show Range Time : This option allows you to display the time range of each session on the chart. If enabled, the exact start and end times of each interval are shown.

Show or Hide Time Ranges : Toggle on/off for visual clarity depending on user preference.

Custom Colors : Set distinct colors for each session, allowing users to personalize their chart based on their trading style.These settings allow you to adjust the key time intervals of each trading session to your preference and customize the time format according to your own needs.

🔵 Conclusion

The ICT Macros indicator is a powerful tool for traders, helping them to identify key time intervals where the market seeks liquidity or fills Fair Value Gaps (FVG), corrects imbalances, and breaks highs or lows. This tool is especially valuable for traders using liquidity-based strategies such as ICT 2022 or Silver Bullet.

One of the key features of this indicator is its support for Daylight Saving Time (DST), ensuring you are always in sync with the correct trading session timings without manual adjustments. This is particularly beneficial for traders operating across different time zones.

With ICT Macros, you can capitalize on crucial market opportunities during sensitive times, take advantage of imbalances, and enhance your trading strategies based on market volatility, liquidity shifts, and Fair Value Gaps.

Enhanced Kelly Criterion with Risk ManagementThis script is a trading tool for risk management and position size calculations based on the Kelly criteria. The objective is to calculate the optimal position size for each trade based on win/loss ratio and win/loss ratio to manage your money.

Overview

Initial Funding: Starting with an initial capital of $10,000, the balance (amount of funds) of both “bullish” and “bearish” positions will increase or decrease depending on the outcome of the trade.

Risk Management: Users can set their risk tolerance from 1-100%. In addition, the maximum position size per trade is also limited at 50%, for example. This setting allows the user to limit risk.

Record of trade results: For each trade, a positive (bullish) or negative (bearish) line is determined, and wins and losses are recorded accordingly. Win/loss ratios and win/loss ratios are also calculated in real time from this data.

Win rate: Calculates the percentage of winning trades in a trade.

Win/Loss Ratio: Calculates the ratio of profit/loss between positive and negative trades.

Position sizing using the Kelly Criterion: Based on the win/loss ratio, the optimal position size to take on the next trade is calculated using the Kelly Criterion. However, this Kelly Criterion is treated with caution because of the potential for increased risk.

Controlling Risk and Position Size

Volatility adjustment using ATR (Average True Range): The script considers market volatility (range of price fluctuation) using a measure called ATR. This allows for smaller position sizes when price volatility is high, thereby reducing risk.

Position Size Limit: The maximum position size is limited so that the calculated position size does not exceed a certain range. This reduces the risk of large losses.

Display of Results

The script visually plots the final position size and amount of funds so that traders can see the changes in balance. To highlight points of change, position size expansions and contractions are shown, allowing traders to catch signs of sudden fluctuations or changes in volatility.

Suggested Improvements and Considerations

Kelly Criteria Overexposure Risk: Calculations based on the Kelly Criteria are theoretically correct, but they tend to take large positions. This can be very damaging in the event of losses. Therefore, while this script limits risk by setting a maximum position size, it is recommended that you adjust to an even more modest position size.

Data Reliability: The calculation of win/loss ratios and win/loss ratios relies on historical trade data, which can be unreliable until sufficient trade data is gathered. When trade data is scarce, calculations based on the Kelly Criteria may be overly optimistic.

Volatility considerations: Volatility adjustment using ATR is effective, but ATR alone may not be sufficient when markets fluctuate rapidly; if ATR adjustment is insufficient, additional risk mitigation techniques should be used in conjunction.

Overall, this script emphasizes risk management and optimizes position size using the Kelly criteria, but real market conditions require careful risk management with attention to overexposure.

NYSE, Euronext, and Shanghai Stock Exchange Hours IndicatorNYSE, Euronext, and Shanghai Stock Exchange Hours Indicator

This script is designed to enhance your trading experience by visually marking the opening and closing hours of major global stock exchanges: the New York Stock Exchange (NYSE), Euronext, and Shanghai Stock Exchange. By adding vertical lines and background fills during trading sessions, it helps traders quickly identify these critical periods, potentially informing better trading decisions.

Features of This Indicator:

NYSE, Euronext, and Shanghai Stock Exchange Hours: Displays vertical lines at market open and close times for these three exchanges. You can easily switch between showing or hiding the different exchanges to customize the indicator for your needs.

Background Fill: Highlights the trading hours of these exchanges using faint background colors, making it easy to spot when markets are in session. This feature is crucial for timing trades around overlapping trading hours and volume peaks.

Customizable Visuals: Adjust the color, line style (solid, dotted, dashed), and line width to match your preferences, making the indicator both functional and visually aligned with your chart's aesthetics.

How to Use the Indicator:

Add the Indicator to Your Chart: Add the script to your chart from the TradingView script library. Once added, the indicator will automatically plot vertical lines at the opening and closing times of the NYSE, Euronext, and Shanghai Stock Exchange.

Customize Display Settings: Choose which exchanges to display by enabling or disabling the NYSE, Euronext, or Shanghai sessions in the indicator settings. This allows you to focus only on the exchanges that are relevant to your trading strategy.

Adjust Visual Properties: Customize the appearance of the vertical lines and background fill through the settings. Modify the color of each exchange, adjust the line style (solid, dotted, dashed), and control the line thickness to suit your chart preferences. The background fill can also be customized to clearly highlight active trading sessions.

Identify Key Market Hours: Use the vertical lines and background fills to identify the market open and close times. This is particularly useful for understanding how price action changes during specific trading hours or for finding high liquidity periods when multiple markets are open simultaneously.

Adapt Trading Strategies: By knowing when major stock exchanges are open, you can adapt your trading strategy to take advantage of potential price movements, increased volatility, or volume. This can help you avoid low-liquidity times and capitalize on more active trading periods.

This indicator is especially valuable for traders focusing on cross-market dynamics or those interested in understanding how different sessions influence market liquidity and price action. With this tool, you can gain insight into market conditions and adapt your trading strategies accordingly. The clean visual separation of session times helps you maintain context, whether you're trading Forex, stocks, or cryptocurrencies.

Disclaimer: This script is intended for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument. Always conduct your own research and consult with a licensed financial advisor before making any trading decisions. Trading involves risk, and past performance is not indicative of future results.

DYNAMIC USD MOMENTUM INDICATOR

Hello traders,

Welcome to my script, an indicator helping you to quickly see the performance of USD in constant daily comparison to other currencies.

This script requests price data from other charts but displays overbought and oversold labels on any selected chart currency pair.

See attached images to spot high probability reversal days when USD is in extremes against multiple other currencies. The output labels represent the currency traded against USD and reaching overbought and oversold zoned on a dynamic RSI scale.

Suggested pairs with higher co relation to stronger or weaker dollar:

AUD/USD, CAD/USD, EUR/USD, GBP/USD, NZD/USD

CHF/USD and JPY/USD require more in depth analysis of individual performance of JPY AND CHF

Zone Color PatternZone Color Pattern indicator depicts the color pattern of zones on chart. This will help the user to identify the zones on Chart.

Green Zone is indicated by Green color.

Red Zone is indicated by Red Color.

Gray Zone is indicated by Gray Zone.

Zone Color Pattern indicator is based on 3 moving averages. Long term, Medium term and Short Term.By default they are 200, 50 and 20.

When you are on long term trend the position of MAs is 20 MA is on top,then comes 50 MA and 200 MA is positioned below 50 MA.The position of respective MAs change during down trend.

The color patterns display the distance between different MAs .The widening and contraction of space between different Moving Averages indicate the movement and direction of price.

Basically price tend to move in and move away from Average. This action tend to create a space between price and MAs.Color patterns between price and MAs reflect the gap between the price and M|As .All these effects can be visualized on chart in relevant colors to infer the status of price, movement, cross over by the User.

Buy trades are preferred when close is in Green Zone and price is above MA20.

Sell trades are preferred when close is in Red Zone and price is below MA20

Trades may be avoided when close is in Gray Zone.

Long Up Trend and Down Trend respective color triangle shapes and arrows on chart indicate the trends and direction.

The chart understanding has to be supplemented with other regular indicators along with appropriate risk reward techniques by user.

Table indicate difference between Last Price traded and Day open price.

Other columns in table display the position of close in different Zones.

DISCLAIMER: For educational and entertainment purpose only .Nothing in this content should be interpreted as financial advice or a recommendation to buy or sell any sort of security/ies or investment/s.

RSI Weighted Trend System I [InvestorUnknown]The RSI Weighted Trend System I is an experimental indicator designed to combine both slow-moving trend indicators for stable trend identification and fast-moving indicators to capture potential major turning points in the market. The novelty of this system lies in the dynamic weighting mechanism, where fast indicators receive weight based on the current Relative Strength Index (RSI) value, thus providing a flexible tool for traders seeking to adapt their strategies to varying market conditions.

Dynamic RSI-Based Weighting System

The core of the indicator is the dynamic weighting of fast indicators based on the value of the RSI. In essence, the higher the absolute value of the RSI (whether positive or negative), the higher the weight assigned to the fast indicators. This enables the system to capture rapid price movements around potential turning points.

Users can choose between a threshold-based or continuous weight system:

Threshold-Based Weighting: Fast indicators are activated only when the absolute RSI value exceeds a user-defined threshold. Below this threshold, fast indicators receive no weight.

Continuous Weighting: By setting the weight threshold to zero, the fast indicators always receive some weight, although this can result in more false signals in ranging markets.

// Calculate weight for Fast Indicators based on RSI (Slow Indicator weight is kept to 1 for simplicity)

f_RSI_Weight_System(series float rsi, simple float weight_thre) =>

float fast_weight = na

float slow_weight = na

if weight_thre > 0

if math.abs(rsi) <= weight_thre

fast_weight := 0

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

Slow and Fast Indicators

Slow Indicators are designed to identify stable trends, remaining constant in weight. These include:

DMI (Directional Movement Index) For Loop

CCI (Commodity Channel Index) For Loop

Aroon For Loop

Fast Indicators are more responsive and designed to spot rapid trend shifts:

ZLEMA (Zero-Lag Exponential Moving Average) For Loop

IIRF (Infinite Impulse Response Filter) For Loop

Each of these indicators is calculated using a for-loop method to generate a moving average, which captures the trend of a given length range.

RSI Normalization

To facilitate the weighting system, the RSI is normalized from its usual 0-100 range to a -1 to 1 range. This allows for easy scaling when calculating weights and helps the system adjust to rapidly changing market conditions.

// Normalize RSI (1 to -1)

f_RSI(series float rsi_src, simple int rsi_len, simple string rsi_wb, simple string ma_type, simple int ma_len) =>

output = switch rsi_wb

"RAW RSI" => ta.rsi(rsi_src, rsi_len)

"RSI MA" => ma_type == "EMA" ? (ta.ema(ta.rsi(rsi_src, rsi_len), ma_len)) : (ta.sma(ta.rsi(rsi_src, rsi_len), ma_len))

Signal Calculation

The final trading signal is a weighted average of both the slow and fast indicators, depending on the calculated weights from the RSI. This ensures a balanced approach, where slow indicators maintain overall trend guidance, while fast indicators provide timely entries and exits.

// Calculate Signal (as weighted average)

sig = math.round(((DMI*slow_w) + (CCI*slow_w) + (Aroon*slow_w) + (ZLEMA*fast_w) + (IIRF*fast_w)) / (3*slow_w + 2*fast_w), 2)

Backtest Mode and Performance Metrics

This version of the RSI Weighted Trend System includes a comprehensive backtesting mode, allowing users to evaluate the performance of their selected settings against a Buy & Hold strategy. The backtesting includes:

Equity calculation based on the signals generated by the indicator.

Performance metrics table comparing Buy & Hold strategy metrics with the system’s signals, including: Mean, positive, and negative return percentages, Standard deviations (of all, positive and negative returns), Sharpe Ratio, Sortino Ratio, and Omega Ratio

f_PerformanceMetrics(series float base, int Lookback, simple float startDate, bool Annualize = true) =>

// Initialize variables for positive and negative returns

pos_sum = 0.0

neg_sum = 0.0

pos_count = 0

neg_count = 0

returns_sum = 0.0

returns_squared_sum = 0.0

pos_returns_squared_sum = 0.0

neg_returns_squared_sum = 0.0

// Loop through the past 'Lookback' bars to calculate sums and counts

if (time >= startDate)

for i = 0 to Lookback - 1

r = (base - base ) / base

returns_sum += r

returns_squared_sum += r * r

if r > 0

pos_sum += r

pos_count += 1

pos_returns_squared_sum += r * r

if r < 0

neg_sum += r

neg_count += 1

neg_returns_squared_sum += r * r

float export_array = array.new_float(12)

// Calculate means

mean_all = math.round((returns_sum / Lookback) * 100, 2)

mean_pos = math.round((pos_count != 0 ? pos_sum / pos_count : na) * 100, 2)

mean_neg = math.round((neg_count != 0 ? neg_sum / neg_count : na) * 100, 2)

// Calculate standard deviations

stddev_all = math.round((math.sqrt((returns_squared_sum - (returns_sum * returns_sum) / Lookback) / Lookback)) * 100, 2)

stddev_pos = math.round((pos_count != 0 ? math.sqrt((pos_returns_squared_sum - (pos_sum * pos_sum) / pos_count) / pos_count) : na) * 100, 2)

stddev_neg = math.round((neg_count != 0 ? math.sqrt((neg_returns_squared_sum - (neg_sum * neg_sum) / neg_count) / neg_count) : na) * 100, 2)

// Calculate probabilities

prob_pos = math.round((pos_count / Lookback) * 100, 2)

prob_neg = math.round((neg_count / Lookback) * 100, 2)

prob_neu = math.round(((Lookback - pos_count - neg_count) / Lookback) * 100, 2)

// Calculate ratios

sharpe_ratio = math.round(mean_all / stddev_all * (Annualize ? math.sqrt(Lookback) : 1), 2)

sortino_ratio = math.round(mean_all / stddev_neg * (Annualize ? math.sqrt(Lookback) : 1), 2)

omega_ratio = math.round(pos_sum / math.abs(neg_sum), 2)

// Set values in the array

array.set(export_array, 0, mean_all), array.set(export_array, 1, mean_pos), array.set(export_array, 2, mean_neg),

array.set(export_array, 3, stddev_all), array.set(export_array, 4, stddev_pos), array.set(export_array, 5, stddev_neg),

array.set(export_array, 6, prob_pos), array.set(export_array, 7, prob_neu), array.set(export_array, 8, prob_neg),

array.set(export_array, 9, sharpe_ratio), array.set(export_array, 10, sortino_ratio), array.set(export_array, 11, omega_ratio)

// Export the array

export_array

The metrics help traders assess the effectiveness of their strategy over time and can be used to optimize their settings.

Calibration Mode

A calibration mode is included to assist users in tuning the indicator to their specific needs. In this mode, traders can focus on a specific indicator (e.g., DMI, CCI, Aroon, ZLEMA, IIRF, or RSI) and fine-tune it without interference from other signals.

The calibration plot visualizes the chosen indicator's performance against a zero line, making it easy to see how changes in the indicator’s settings affect its trend detection.

Customization and Default Settings

Important Note: The default settings provided are not optimized for any particular market or asset. They serve as a starting point for experimentation. Traders are encouraged to calibrate the system to suit their own trading strategies and preferences.

The indicator allows deep customization, from selecting which indicators to use, adjusting the lengths of each indicator, smoothing parameters, and the RSI weight system.

Alerts

Traders can set alerts for both long and short signals when the indicator flips, allowing for automated monitoring of potential trading opportunities.

Bullseye NYSE 1st5mThis script, "BullseyeNYSE1st5m," is a TradingView indicator designed to highlight the high and low price levels during the first 5 minutes of the NYSE trading session. It works as follows:

1. **Identify NYSE Trading Hours**: The script identifies bars that fall within NYSE trading hours, specifically focusing on the first five minutes after the market opens.

2. **Calculate First 5-Minute High and Low**: During the first five minutes of the trading day, the script captures and updates the high and low prices, storing these values for the remainder of the session.

3. **Plot High and Low Levels**: The high and low values from the first five minutes are plotted as lines on the chart in yellow. This helps traders quickly identify the initial range set by the market.

4. **Fill the Area Between High and Low**: The area between the high and low levels is filled with a translucent yellow color to visually emphasize the first five-minute range.

5. **Alerts for Breakouts**: Alerts are set to notify the user when the price closes above or below the first five-minute range. This helps traders stay informed of potential breakout opportunities beyond this key opening range.

This indicator is useful for day traders looking to leverage the first few minutes of NYSE trading to identify early support and resistance levels and to spot breakout opportunities.

Bullseye PDHL Bullseye PDHL Indicator

The Bullseye PDHL indicator is designed for traders who want to visually identify key price levels from the previous trading day, including the high, low, and significant Fibonacci retracement levels. This indicator helps traders understand potential support and resistance zones, which can be useful for planning entries and exits.

Key Features:

Previous Day’s High and Low:

Plots the previous day’s high and low as solid lines on the chart to easily identify important levels from the prior session.

These levels serve as critical support and resistance markers, which are often respected by the market.

Fibonacci Retracement Levels:

Plots three Fibonacci retracement levels (38.2%, 50%, and 61.8%) between the previous day’s high and low.

These levels are key reference points for assessing potential pullbacks or retracements during the current trading day.

Visual Representation:

The previous day’s high and low are plotted in cyan for easy differentiation.

The Fibonacci retracement levels (30%, 50%, 60%) are plotted in white, providing a clear visual reference for traders.

This indicator can help traders identify important reaction zones and areas where price might reverse or consolidate, making it a valuable addition for technical analysis.

EMA Distance & Sector InfoThis indicator provides insights into price trends relative to Exponential Moving Averages (EMAs) and displays sector/industry information about the asset. Below is a detailed explanation of its purpose and what it is designed to achieve:

Purpose of the Code

The indicator offers two key functionalities:

1. Analyzing Price Distance from Multiple EMAs:

• Helps traders understand how far the current price is from key EMAs, expressed as a percentage.

• Calculates average percentage distances over a specified period (default: 63 days) to spot consistent trends or mean reversion opportunities.

• Useful for trend-following strategies, allowing the trader to see when the price is above or below important EMAs (e.g., 9, 21, 50, 100, and 150-period EMAs).

2. Displaying Asset Sector and Industry Information:

• Displays the sector and industry of the asset being analyzed (e.g., Technology, Consumer Goods).

• Provides additional context when evaluating performance across a specific sector or comparing an asset to its peers.

Who Would Use This Indicator?

This indicator is particularly helpful for:

1. Swing Traders and Positional Traders:

• They can use it to track whether the price is trading significantly above or below critical EMAs, which often signals overbought/oversold conditions or trend strength.

• The average percentage distances help to identify momentum shifts or pullback opportunities.

2. Sector/Industry-Focused Investors:

• Understanding an asset’s sector and industry helps investors gauge how the asset fits into the broader market context.

• This is valuable for sector rotation strategies, where investors shift funds between sectors based on performance trends.

How It Helps in Trading Decisions

1. Entry and Exit Points:

• If the price is far above an EMA (e.g., 21 EMA), it might indicate an overbought condition or a strong trend, while a negative percentage could signal a pullback or reversal opportunity.

• The average percentage distances smooth the fluctuations and reveal longer-term trends.

2. Contextual Information:

• Knowing the sector and industry is useful when analyzing trends. For example, if Technology stocks are doing well, and this asset belongs to that sector, it could indicate sector-wide momentum.

Summary of the Indicator’s Purpose

This code provides:

• EMA trend monitoring: Visualizes the price position relative to multiple EMAs and averages those distances for smoother insights.

• Sector and industry information: Adds valuable context for asset performance analysis.

• Decision-making support: Helps traders identify overbought/oversold levels and assess the asset within the broader market landscape.

In essence, this indicator is a multi-purpose tool that combines technical analysis (through EMA distances) with fundamental context (via sector/industry info), making it valuable for traders and investors aiming to time entries/exits or understand market behavior better.

G-Channel with EMA StrategyThe G-Channel is a custom channel with an upper (a), lower (b), and average (avg) line. These lines are dynamically calculated based on the current and previous closing prices, using the length input (default 100) to smooth the values:

Upper Line (a): This is the maximum value of the current price or the previous upper value, adjusted by the difference between the upper and lower lines divided by the length.

Lower Line (b): This is the minimum value of the current price or the previous lower value, similarly adjusted by the difference between the upper and lower lines.

The average line (avg) is simply the midpoint between the upper and lower lines. The G-Channel signals trend direction:

Bullish Condition: The system looks for the condition when the price crosses over the lower line (b), indicating a potential upward trend.

Bearish Condition: When the price crosses under the upper line (a), it signals a potential downward trend.

Exponential Moving Average (EMA)

The strategy also incorporates an EMA with a default length of 200. The EMA serves as a trend filter to determine whether the market is trending upward or downward:

Price below EMA: Indicates a bearish trend.

Price above EMA: Indicates a bullish trend.

Buy/Sell Conditions

The strategy generates buy or sell signals based on the interaction between the G-Channel signals and the price relative to the EMA:

Buy Signal: The strategy triggers a buy when:

A bullish condition (recent crossover of price over the lower G-Channel line) is detected.

The price is below the EMA, indicating that despite the recent bullish signal, the market might still be undervalued or in a temporary downturn.

Sell Signal: The strategy triggers a sell when:

A bearish condition (recent crossunder of price below the upper G-Channel line) is detected.

The price is above the EMA, suggesting that the market might be overextended and poised for a downturn.

Visualization

The strategy plots:

The upper, lower, and average lines of the G-Channel, with the average line colored based on bullish (green) or bearish (red) conditions.

The EMA (orange) line to provide context on the general trend direction.

Markers for Buy and Sell signals to visually indicate the strategy's entry points.

Strategy Execution

When a buy or sell signal is detected:

Buy Entry: If the bullish condition and price < EMA condition are met, a long (buy) position is opened.

Sell Entry: If the bearish condition and price > EMA condition are met, a short (sell) position is opened.

Purpose

This strategy aims to catch price reversals at critical points (when the price moves through the G-Channel) while filtering trades using the EMA to avoid entering during unfavorable market trends.

Macro Timeframes with Opening PriceDescription: Macro Timeframe Horizontal Line Indicator

This indicator highlights macro periods on the chart by drawing a horizontal line at the opening price of each macro period. The macro timeframe is defined as the last 10 minutes of an hour (from :50 to :00) and the first 10 minutes of the following hour (from :00 to :10).

A horizontal black line is plotted at the opening price of the macro period, starting at :50 and extending through the duration of the macro window. However, you can customize it however you see fit.

The background of the macro period is highlighted with a customizable color to visually distinguish the timeframe.

The horizontal line updates at each macro period, ensuring that the opening price for every macro session is accurately reflected on the chart.

This tool is useful for traders who want to track the behavior of price within key macro intervals and visually assess price movement and volatility during these periods.

Futures Globex Session(s)This indicator draws a box around the Globex Session for the various Futures markets. The box height defines the highs and lows of that session, and the width defines the timeframe of that session. The boxes are outlined green if price rose during that period, and red if price fell during that period. The default Globex Session is set for the Equity Index Futures and is set in the UTC-4 time zone (Eastern Time). In the settings you can adjust the session time and time zone of your Globex Session to reflect the trading times of that market. Below are the session times for various Futures markets set in time zone UTC-4.

Equity Indexes: 18:00 - 9:30

(ES, NQ, YM, RTY)

Treasuries: 18:00 - 8:20

(ZN, ZB)

Metals: 18:00 - 8:20

(GC)

Energies: 18:00 - 9:00

(CL, NG)

Agricultures: 20:00 - 9:30

(ZS, ZW)

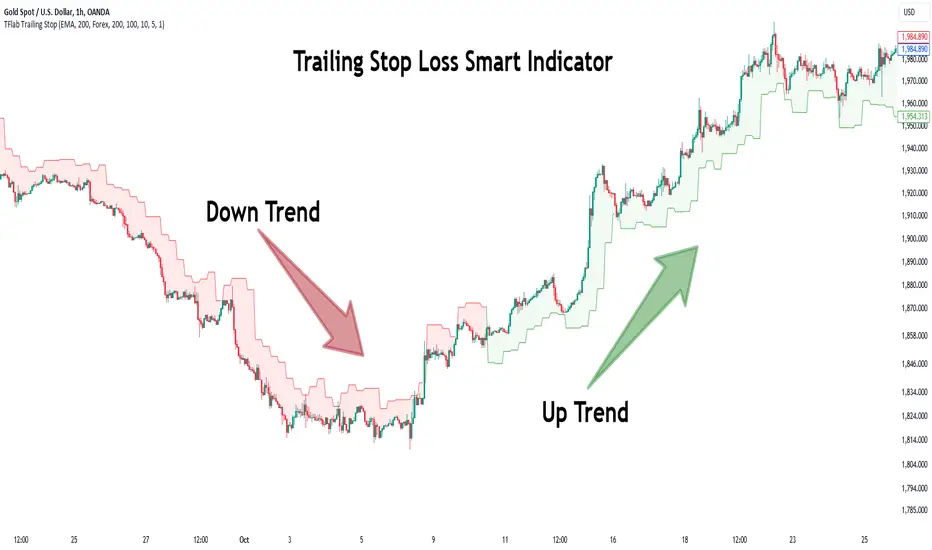

Trailing Stop Loss Smart [TradingFinder] Market Trend + CVD/EMA🔵 Introduction

Trailing Stop Loss (TSL) is one of the most powerful tools available. A Trailing Stop Loss is a modification of a typical stop order that adjusts dynamically based on market price movement. It can be set at a defined percentage or dollar amount away from the security's current market price, making it a flexible tool for locking in profits while minimizing risk. Unlike standard stop-loss orders, a Trailing Stop follows the market in the direction of the trade, protecting gains without requiring constant manual adjustments.

The Trailing Stop Loss Smart (TFlab Trailing Stop) indicator takes this concept even further by incorporating advanced metrics like Cumulative Volume Delta (CVD), volume dynamics, and Average True Range (ATR). This combination not only enhances risk management but also acts as a trend identifier, providing traders with a powerful tool to capitalize on both short-term and long-term price movements.

This indicator also supports various Order Types, allowing for flexible strategies that include a trailing stop/stop-loss combo to maximize winning trades while minimizing losses. The trailing stop limit is particularly useful for traders who want to set their stop at a precise level relative to the current market price, either by a percentage or a dollar amount. The Trailing Stop Loss Smart indicator can help ensure that traders do not exit too early during trends, while the stop-loss feature kicks in during reversals.

The advantages of using a Trailing Stop Loss are its ability to protect profits and reduce the emotional decision-making process in volatile markets. However, like all trading strategies, it has disadvantages, such as the risk of triggering too early during normal market fluctuations. By understanding how the Trailing Stop Loss Smart indicator integrates features like CVD, ATR, and volume analysis, traders can leverage its full potential while navigating these pros and cons.

With its unique ability to track market movements and trends using Cumulative Volume Delta, volume dynamics, and ATR-based trailing stops, this indicator offers a complete solution for traders looking to secure profits while minimizing downside risk. Whether you're employing a simple trailing stop or a trailing stop/stop-loss combo, this tool provides all the flexibility and precision needed to execute winning trades in various markets, including Forex, Crypto, and Stock.

🔵 How to Use

The Trailing Stop Loss Smart indicator integrates multiple advanced components to provide traders with superior risk management and trend identification.

Here’s how each part of the logic works :

🟣 Cumulative Volume Delta (CVD) Logic

The CVD tracks buying and selling pressure by calculating the difference between upward and downward price movements. When there’s more buying pressure, the CVD is positive, indicating a potential bullish trend. Conversely, more selling pressure results in a negative CVD, pointing to a bearish trend.

CVD Trend Detection : The indicator determines whether the market is in a bullish or bearish phase by comparing the CVD to its moving average. A bullish trend is confirmed when the CVD is above its moving average and the price is closing higher.

A bearish trend occurs when the CVD is below its moving average and the price is closing lower. This trend detection is critical for determining whether the trailing stop should be placed below the price (bullish) or above it (bearish).

🟣 Volume Dynamics

Volume is a key factor in identifying market strength. The Trailing Stop Loss Smart indicator pulls volume data based on the market selected (Forex, Crypto, or Stock) and adjusts the trailing stop based on whether the market is experiencing high volume or low volume.

High Volume : When the current volume exceeds the average volume, the market is in a high-volume state. During these conditions, the trailing stop is placed closer to the price, as high volume often indicates strong trends with less chance of reversals.

Low Volume : In low-volume conditions, the trailing stop gives the market more room to breathe by placing the stop further away from the price. This prevents premature stop-outs in periods of reduced market activity.

🟣 ATR-Based Trailing Stop

The Average True Range (ATR) is used to measure market volatility. The Trailing Stop Loss Smart uses the ATR to dynamically adjust the stop-loss distance.

Bullish Market : When a bullish trend is detected, the trailing stop is placed below the lowest price of the recent bars (determined by the Bar Back parameter), and adjusted by the ATR Multiplier. This allows for tighter protection during strong bullish trends.

Bearish Market : When the market is bearish, the trailing stop is placed above the highest price of recent bars, also adjusted by the ATR Multiplier. This ensures that short positions are safeguarded against sudden reversals.

🟣 Dynamic Stop-Loss Updates

The trailing stop is updated every few bars (according to the Refiner parameter), ensuring it remains relevant to the most recent price action and volume changes. This dynamic feature ensures the stop-loss adapts to both trending and volatile market conditions, without requiring manual intervention.

High Volume with Trends : In periods of high volume and a confirmed trend, the stop-loss is positioned tightly to lock in profits while minimizing the risk of reversal.

Low Volume with Trends : In low-volume conditions, the stop-loss is placed further from the price, allowing the market to move freely without triggering premature exits.

🟣 Visual Representation

The indicator visually represents the trailing stop on the chart, with green lines indicating bullish trends and red lines for bearish trends. This visual aid helps traders quickly assess the state of the market and the position of their trailing stop in real-time.

🔵 Settings

The Trailing Stop Loss Smart indicator offers several customizable settings to suit various trading strategies. Understanding these inputs is key to optimizing the tool for your specific trading style.

🟣 General Settings

Cumulative Mode : This controls how the CVD is calculated.

You can choose between :

EMA : Exponential Moving Average smoothing.

Periodic : Sums the delta over a fixed period.

CVD Period : Defines the look-back period for CVD calculation. A longer period smooths the data, making it less sensitive to short-term fluctuations.

Ultra Data : This Boolean input aggregates volume across multiple exchanges for a more comprehensive view of market activity.

Market Ultra Data : Select between Forex, Crypto, and Stock to ensure the indicator pulls accurate volume data for your market.

🟣 Logical Settings

Moving Average CVD Period : Defines the period for the moving average of the CVD. A longer period smooths the trend, reducing noise.

Moving Average Volume Period : Sets the period for the moving average used to distinguish between high and low volume conditions.

Level Finder Bar Back : Determines how many bars to look back when identifying the highest or lowest price for trailing stop placement.

Levels update per candles : Sets how often (in bars) the trailing stop should be updated to remain in sync with market movements.

ATR On : Toggles the use of ATR to adjust the trailing stop based on volatility.

ATR Multiplie r: Defines how far the stop is placed from the price based on the ATR. A larger multiplier increases the stop distance, reducing the likelihood of getting stopped out during market fluctuations.

ATR Multiplier Adjusts the distance of the trailing stop based on the ATR. A higher multiplier places the stop further from the price, providing more breathing room in volatile markets.

🔵 Conclusion

The Trailing Stop Loss Smart indicator is a comprehensive tool for traders looking to manage risk while identifying market trends. By incorporating Cumulative Volume Delta (CVD) to detect buying and selling pressure, volume dynamics to gauge market activity, and ATR to adjust for volatility, this indicator ensures that stop-loss levels are both adaptive and protective.

Whether you’re trading in Forex, Crypto, or Stock markets, the Trailing Stop Loss Smart allows you to capitalize on trends while dynamically adjusting to changing market conditions. Its ability to distinguish between high-volume and low-volume periods ensures that you’re not stopped out prematurely during periods of consolidation or market hesitation.

By providing real-time visual feedback, dynamic adjustments, and trend identification, this indicator serves as a vital tool for traders aiming to maximize profits while minimizing risk. Its versatility and adaptability make it an essential part of any trader’s toolkit, helping you stay ahead in fast-moving markets while safeguarding your positions.

Abdozo - Highlight First DaysAbdozo - Highlight First Days Indicator

This Pine Script indicator helps traders easily identify key timeframes by highlighting the first trading day of the week and the first day of the month. It provides visual markers directly on your chart, helping you stay aware of potential market trends and turning points.

Features:

- Highlight First Day of the Week (Monday): Automatically marks Mondays to help you track weekly market cycles.

- Highlight First Day of the Month: Spot the start of each month with ease to analyze monthly performance and trends.