ADX + Volume Strategy### Strategy Description: ADX and Volume-Based Trading Strategy

This strategy is designed to identify strong market trends using the **Average Directional Index (ADX)** and confirm trading signals with **Volume**. The idea behind the strategy is to enter trades only when the market shows a strong trend (as indicated by ADX) and when the price movement is supported by high trading volume. This combination helps filter out weaker signals and provides more reliable entries into positions.

### Key Indicators:

1. **ADX (Average Directional Index)**:

- **Purpose**: ADX is a technical indicator that measures the strength of a trend, regardless of its direction (up or down).

- **Usage**: The strategy uses ADX to determine whether the market is trending strongly. If ADX is above a certain threshold (default is 25), it indicates that a strong trend is present.

- **Directional Indicators**:

- **DI+ (Directional Indicator Plus)**: Indicates the strength of the upward price movement.

- **DI- (Directional Indicator Minus)**: Indicates the strength of the downward price movement.

- ADX does not indicate the direction of the trend but confirms that a trend exists. DI+ and DI- are used to determine the direction.

2. **Volume**:

- **Purpose**: Volume is a key indicator for confirming the strength of a price movement. High volume suggests that a large number of market participants are supporting the movement, making it more likely to continue.

- **Usage**: The strategy compares the current volume to the 20-period moving average of the volume. The trade signal is confirmed if the current volume is greater than the average volume by a specified **Volume Multiplier** (default multiplier is 1.5). This ensures that the trade is supported by strong market participation.

### Strategy Logic:

#### **Entry Conditions:**

1. **Long Position** (Buy):

- **ADX** is above the threshold (default is 25), indicating a strong trend.

- **DI+ > DI-**, signaling that the market is trending upward.

- The **current volume** is greater than the 20-period average volume multiplied by the **Volume Multiplier** (e.g., 1.5), indicating that the upward price movement is backed by sufficient market activity.

2. **Short Position** (Sell):

- **ADX** is above the threshold (default is 25), indicating a strong trend.

- **DI- > DI+**, signaling that the market is trending downward.

- The **current volume** is greater than the 20-period average volume multiplied by the **Volume Multiplier** (e.g., 1.5), indicating that the downward price movement is backed by strong selling activity.

#### **Exit Conditions**:

- Positions are closed when the opposite signal appears:

- **For long positions**: Close when the short conditions are met (ADX still above the threshold, DI- > DI+, and the volume condition holds).

- **For short positions**: Close when the long conditions are met (ADX still above the threshold, DI+ > DI-, and the volume condition holds).

### Parameters:

- **ADX Period**: The period used to calculate ADX (default is 14). This controls how sensitive the ADX is to price movements.

- **ADX Threshold**: The minimum ADX value required for the strategy to consider the market trend as strong (default is 25). Higher values focus on stronger trends.

- **Volume Multiplier**: This parameter adjusts how much higher the current volume needs to be compared to the 20-period moving average for the signal to be valid. A value of 1.5 means the current volume must be 50% higher than the average volume.

### Example Trade Flow:

1. **Long Trade Example**:

- ADX > 25, confirming a strong trend.

- DI+ > DI-, confirming that the trend direction is upward.

- The current volume is 50% higher than the 20-period average volume (multiplied by 1.5).

- **Action**: Enter a long position.

2. **Short Trade Example**:

- ADX > 25, confirming a strong trend.

- DI- > DI+, confirming that the trend direction is downward.

- The current volume is 50% higher than the 20-period average volume.

- **Action**: Enter a short position.

### Strengths of the Strategy:

- **Trend Filtering**: The strategy ensures that trades are only taken when the market is trending strongly (confirmed by ADX) and that the price movement is supported by high volume, reducing the likelihood of false signals.

- **Volume Confirmation**: Using volume as confirmation provides an additional layer of reliability, as volume spikes often accompany sustained price moves.

- **Dual Signal Confirmation**: Both trend strength (ADX) and volume conditions must be met for a trade, making the strategy more robust.

### Weaknesses of the Strategy:

- **Limited Effectiveness in Range-Bound Markets**: Since the strategy relies on strong trends, it may underperform in sideways or non-trending markets where ADX stays below the threshold.

- **Lagging Nature of ADX**: ADX is a lagging indicator, which means that it may confirm the trend after it has already begun, potentially leading to late entries.

- **Volume Requirement**: In low-volume markets, the volume multiplier condition may not be met often, leading to fewer trade opportunities.

### Customization:

- **Adjust the ADX Threshold**: You can raise the threshold if you want to focus only on very strong trends, or lower it to capture moderate trends.

- **Adjust the Volume Multiplier**: You can change the multiplier to be more or less strict. A higher multiplier (e.g., 2.0) will require a stronger volume spike to confirm the signal, while a lower multiplier (e.g., 1.2) will allow more trades with weaker volume confirmation.

### Summary:

This ADX and Volume strategy is ideal for traders who want to follow strong trends while ensuring that the trend is supported by high trading volume. By combining a trend strength filter (ADX) and volume confirmation, the strategy aims to increase the probability of entering profitable trades while reducing the number of false signals. However, it may underperform in range-bound markets or in markets with low volume.

Educational

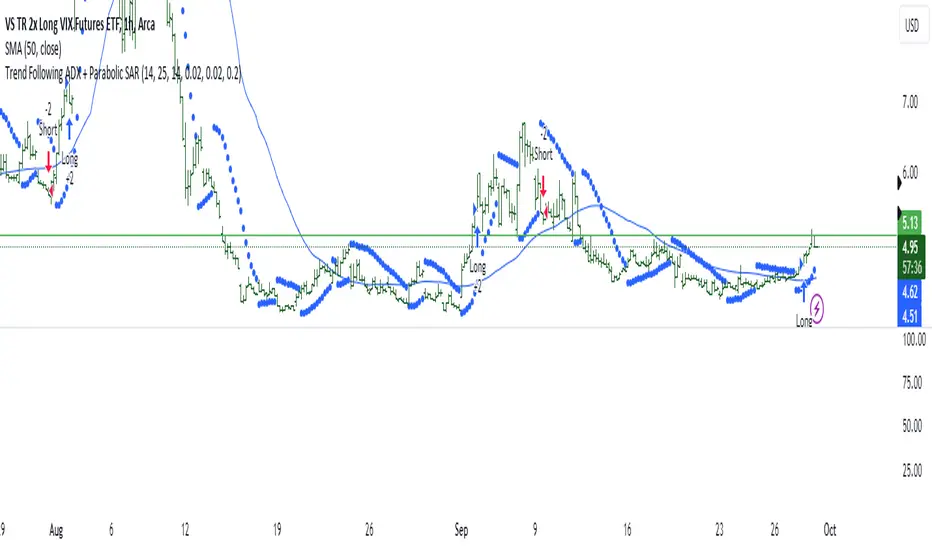

Trend Following ADX + Parabolic SAR### Strategy Description: Trend Following using **ADX** and **Parabolic SAR**

This strategy is designed to follow market trends using two popular indicators: **Average Directional Index (ADX)** and **Parabolic SAR**. The strategy attempts to enter trades when the market shows a strong trend (using ADX) and confirms the trend direction using the Parabolic SAR. Here's a breakdown:

### Key Indicators:

1. **ADX (Average Directional Index)**:

- **Purpose**: ADX measures the strength of a trend, regardless of direction.

- **Usage**: The strategy uses ADX to confirm that the market is trending. When ADX is above a certain threshold (e.g., 25), it indicates a strong trend.

- **Directional Indicators**:

- **DI+ (Directional Indicator Plus)**: Indicates upward movement strength.

- **DI- (Directional Indicator Minus)**: Indicates downward movement strength.

2. **Parabolic SAR**:

- **Purpose**: Parabolic SAR is a trend-following indicator used to identify potential reversals in the price direction.

- **Usage**: It provides specific price points above or below which the strategy confirms buy or sell signals.

### Strategy Logic:

#### **Entry Conditions**:

1. **Long Position** (Buy):

- **ADX** is above the threshold (default: 25), indicating a strong trend.

- **DI+ > DI-**, indicating the upward trend is stronger than the downward.

- The price is above the **Parabolic SAR** level, confirming the upward trend.

2. **Short Position** (Sell):

- **ADX** is above the threshold (default: 25), indicating a strong trend.

- **DI- > DI+**, indicating the downward trend is stronger than the upward.

- The price is below the **Parabolic SAR** level, confirming the downward trend.

#### **Exit Conditions**:

- Positions are closed when an opposite signal is detected.

- For example, if a long position is open and the conditions for a short position are met, the long position is closed, and a short position is opened.

### Parameters:

1. **ADX Period**: Defines the length of the period for the ADX calculation (default: 14).

2. **ADX Threshold**: The minimum value of ADX to confirm a strong trend (default: 25).

3. **Parabolic SAR Start**: The initial step for the SAR (default: 0.02).

4. **Parabolic SAR Increment**: The step increment for SAR (default: 0.02).

5. **Parabolic SAR Max**: The maximum step for SAR (default: 0.2).

### Example Trade Flow:

#### **Long Trade**:

1. ADX > 25, confirming a strong trend.

2. DI+ > DI-, indicating the market is trending upward.

3. The price is above the Parabolic SAR, confirming the upward direction.

4. **Action**: Enter a long (buy) position.

5. Exit the long position when a short signal is triggered (i.e., DI- > DI+, price below Parabolic SAR).

#### **Short Trade**:

1. ADX > 25, confirming a strong trend.

2. DI- > DI+, indicating the market is trending downward.

3. The price is below the Parabolic SAR, confirming the downward direction.

4. **Action**: Enter a short (sell) position.

5. Exit the short position when a long signal is triggered (i.e., DI+ > DI-, price above Parabolic SAR).

### Strengths of the Strategy:

- **Trend-Following**: It performs well in markets with strong trends, whether upward or downward.

- **Dual Confirmation**: The combination of ADX and Parabolic SAR reduces false signals by ensuring both trend strength and direction are considered before entering a trade.

### Weaknesses:

- **Range-Bound Markets**: This strategy may perform poorly in choppy, non-trending markets because both ADX and SAR are trend-following indicators.

- **Lagging Nature**: Since both ADX and SAR are lagging indicators, the strategy may enter trades after the trend has already started, potentially missing early profits.

### Customization:

- **ADX Threshold**: You can increase the threshold if you only want to trade in very strong trends, or lower it to capture more moderate trends.

- **SAR Parameters**: Adjusting the SAR `start`, `increment`, and `max` values will make the Parabolic SAR more or less sensitive to price changes.

### Summary:

This strategy combines the ADX and Parabolic SAR to take advantage of strong market trends. By confirming both trend strength (ADX) and trend direction (Parabolic SAR), it aims to enter high-probability trades in trending markets while minimizing false signals. However, it may struggle in sideways or non-trending markets.

For Educational purposes only !!!

Cypher Harmonic Pattern [TradingFinder] Cypher Pattern Detector🔵 Introduction

The Cypher Pattern is one of the most accurate and advanced harmonic patterns, introduced by Darren Oglesbee. The Cypher pattern, utilizing Fibonacci ratios and geometric price analysis, helps traders identify price reversal points with high precision. This pattern consists of five key points (X, A, B, C, and D), each playing an important role in determining entry and exit points in the financial markets.

The reversal point typically occurs in the XD region, with the Fibonacci ratio ranging between 0.768 and 0.886. This zone is referred to as the Potential Reversal Zone (PRZ), where traders anticipate price changes to occur.

The Cypher harmonic pattern is popular among professional traders due to its high accuracy in identifying market trends and reversal points. The pattern appears in two forms: bullish Cypher pattern and bearish Cypher pattern.

In the bullish Cypher pattern, after a price correction, the price moves upward, while in the bearish Cypher pattern, the price moves downward after a temporary increase. These patterns help traders use technical analysis to identify strong reversal points in the PRZ and execute more optimal trades.

Bullish Cypher Pattern :

Bearish Cypher Pattern :

🔵 How to Use

The Cypher pattern is one of the most complex and precise harmonic patterns, leveraging Fibonacci ratios to help traders identify price reversals. This pattern is comprised of five key points, each playing a critical role in determining entry and exit points.

The Cypher pattern appears in two main types :

Bullish Cypher pattern : This pattern appears as an M shape on the chart and indicates a trend reversal to the upside after a price correction. Traders can prepare for buying after identifying this pattern in technical analysis.

Bearish Cypher pattern : This pattern appears as a W shape and signals the start of a downtrend after a temporary price increase. Traders can use this pattern to enter short positions.

🟣 How to Identify the Cypher Pattern on a Chart

Identifying the Cypher pattern requires precision and the use of advanced technical analysis tools. The pattern consists of four main legs, each identified using Fibonacci ratios and geometric analysis.

To spot the Cypher pattern on a chart, first, identify the five key points : X, A, B, C, and D.

XA leg : The initial move from point X to A.

AB leg : The first correction after the XA move, where the price moves to point B.

BC leg : After the correction, the price moves upwards to point C.

CD leg : The final price move that reaches point D, where a price reversal is expected.

In a bullish Cypher pattern, point D indicates the start of a new uptrend, while in a bearish Cypher pattern, point D signals the beginning of a downtrend. Correctly identifying these points helps traders determine the best time to enter a trade.

🟣 How to Trade Using the Cypher Pattern

Once the Cypher pattern is identified on the chart, traders can use it to set entry and exit points. Point D is the key point for trade entry. In the bullish Cypher pattern, the trader can enter a long position after point D forms, while in the bearish Cypher pattern, point D serves as the ideal point for entering a short position.

🟣 Entering a Buy Trade with the Bullish Cypher Pattern

In a bullish Cypher pattern, traders wait for the price to reach point D, after which they can enter a buy position. At this point, the price is expected to start rising.

🟣 Entering a Sell Trade with the Bearish Cypher Pattern

In a bearish Cypher pattern, the trader enters a sell position at point D, expecting the price to move downward after reaching this point. For additional confirmation, traders can use technical indicators such as RSI or MACD.

🟣 Risk Management in Cypher Pattern Trades

Risk management is one of the most critical aspects of any trade, and this holds true for trading the Cypher pattern. Traders should always use stop-loss orders to prevent larger losses in case the pattern fails.

In the bullish Cypher pattern, the stop-loss is usually placed slightly below point D to exit the trade if the price continues to drop.

In the bearish Cypher pattern, the stop-loss is placed above point D to limit losses if the price rises unexpectedly.

🟣 Combining the Cypher Pattern with Other Technical Tools

The Cypher pattern is a powerful tool in technical analysis, but combining it with other methods such as price action and technical indicators can improve trading accuracy.

🟣 Combining with Price Action

Traders can use price action to confirm the Cypher pattern. Candlestick patterns like reversal candlesticks can provide additional confirmation for price reversals at point D.

🟣 Using Technical Indicators

Incorporating technical indicators such as RSI and MACD can also help traders receive stronger signals for entering trades based on the Cypher pattern. These indicators help identify overbought or oversold conditions, allowing traders to make more informed decisions.

🟣 Advantages and Disadvantages of the Cypher Pattern in Technical Analysis

Advantages :

High accuracy : The Cypher pattern, using Fibonacci ratios and geometric analysis, provides high precision in identifying reversal points.

Applicable in various markets : This pattern can be used in a wide range of financial markets, including forex, stocks, and cryptocurrencies.

Disadvantages :

Rarit y: The Cypher pattern appears less frequently on charts compared to other harmonic patterns.

Complexity : Accurately identifying this pattern requires significant experience, which may be challenging for novice traders.

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Forma t: If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

🔵 Conclusion

The Cypher harmonic pattern is one of the most powerful and accurate patterns used in technical analysis. Its high precision in identifying price reversal points, particularly within the Potential Reversal Zone (PRZ), has made it a popular tool among professional traders. The PRZ, located between the Fibonacci ratios of 0.768 and 0.886 in the XD region, offers traders a clear indication of where price reversals are likely to occur.

However, to use this pattern successfully, traders must employ proper risk management and combine it with supplementary tools like technical indicators and price action. By understanding how to utilize the PRZ, traders can enhance the accuracy of their trade entries and exits.

Ultimately, the Cypher pattern, when used in conjunction with the PRZ, helps traders make more precise decisions in the financial markets, leading to more successful and well-informed trades.

(Early Test) Weekly Seasonality with Dynamic Kelly Criterion# Enhancing Trading Strategies with the Weekly Seasonality Dynamic Kelly Criterion Indicator

Amidst this pursuit to chase price, a common pitfall emerges: an overemphasis on price movements without adequate attention to risk management, probabilistic analysis, and strategic position sizing. To address these challenges, I developed the **Weekly Seasonality with Dynamic Kelly Criterion Indicator**. It is designed to refocus traders on essential aspects of trading, such as risk management and probabilistic returns, thereby catering to both short-term swing traders and long-term investors aiming for tax-efficient positions.

## The Motivation Behind the Indicator

### Overemphasis on Price: A Common Trading Pitfall

Many traders concentrate heavily on price charts and technical indicators, often neglecting the underlying principles of risk management and probabilistic analysis. This overemphasis on price can lead to:

- **Overtrading:** Making frequent trades based solely on price movements without considering the associated risks.

- **Poor Risk Management:** Failing to set appropriate stop-loss levels or position sizes, increasing the potential for significant losses.

- **Emotional Trading:** Letting emotions drive trading decisions rather than objective analysis, which can result in impulsive and irrational trades.

### The Need for Balanced Focus

To achieve sustained trading success, it is crucial to balance price analysis with robust risk management and probabilistic strategies. Key areas of focus include:

1. **Risk Management:** Implementing strategies to protect capital, such as setting stop-loss orders and determining appropriate position sizes based on risk tolerance.

2. **Probabilistic Analysis:** Assessing the likelihood of various market outcomes to make informed trading decisions.

3. **Swing Trading Percent Returns:** Capitalizing on short- to medium-term price movements by buying assets below their average return and selling them above.

## Introducing the Weekly Seasonality with Dynamic Kelly Criterion Indicator

The **Weekly Seasonality with Dynamic Kelly Criterion Indicator** is designed to integrate these essential elements into a comprehensive tool that aids traders in making informed, risk-aware decisions. Below, we explore the key components and functionalities of this indicator.

### Key Components of the Indicator

1. **Average Return (%)**

- **Definition:** The mean percentage return for each week across multiple years.

- **Purpose:** Serves as a benchmark to identify weeks with above or below-average performance, guiding buy and sell decisions.

2. **Positive Percentage (%)**

- **Definition:** The proportion of weeks that yielded positive returns.

- **Purpose:** Indicates the consistency of positive returns, helping traders gauge the reliability of certain weeks for trading.

3. **Volatility (%)**

- **Definition:** The standard deviation of weekly returns.

- **Purpose:** Measures the variability of returns, providing insights into the risk associated with trading during specific weeks.

4. **Kelly Ratio**

- **Definition:** A mathematical formula used to determine the optimal size of a series of bets to maximize the logarithmic growth of capital.

- **Purpose:** Balances potential returns against risks, guiding traders on the appropriate position size to take.

5. **Adjusted Kelly Fraction**

- **Definition:** The Kelly Ratio adjusted based on user-defined risk tolerance and external factors like Federal Reserve (Fed) stance.

- **Purpose:** Personalizes the Kelly Criterion to align with individual risk preferences and market conditions, enhancing risk management.

6. **Position Size ($)**

- **Definition:** The calculated amount to invest based on the Adjusted Kelly Fraction.

- **Purpose:** Ensures that position sizes are aligned with risk management strategies, preventing overexposure to any single trade.

7. **Max Drawdown (%)**

- **Definition:** The maximum observed loss from a peak to a trough of a portfolio, before a new peak is attained.

- **Purpose:** Assesses the worst-case scenario for losses, crucial for understanding potential capital erosion.

### Functionality and Benefits

- **Weekly Data Aggregation:** Aggregates weekly returns across multiple years to provide a robust statistical foundation for decision-making.

- **Quarterly Filtering:** Allows users to filter weeks based on quarters, enabling seasonality analysis and tailored strategies aligned with specific timeframes.

- **Dynamic Risk Adjustment:** Incorporates the Dynamic Kelly Criterion to adjust position sizes in real-time based on changing risk profiles and market conditions.

- **User-Friendly Visualization:** Presents all essential metrics in an organized Summary Table, facilitating quick and informed decision-making.

## The Origin of the Kelly Criterion and Addressing Its Limitations

### Understanding the Kelly Criterion

The Kelly Criterion, developed by John L. Kelly Jr. in 1956, is a formula used to determine the optimal size of a series of bets to maximize the long-term growth of capital. The formula considers both the probability of winning and the payout ratio, balancing potential returns against the risk of loss.

**Kelly Formula:**

\

Where:

- \( b \) = the net odds received on the wager ("b to 1")

- \( p \) = probability of winning

- \( q \) = probability of losing ( \( q = 1 - p \) )

### The Risk of Ruin

While the Kelly Criterion is effective in optimizing growth, it carries inherent risks:

- **Overbetting:** If the input probabilities or payout ratios are misestimated, the Kelly Criterion can suggest overly aggressive position sizes, leading to significant losses.

- **Assumption of Constant Probabilities:** The criterion assumes that probabilities remain constant, which is rarely the case in dynamic markets.

- **Ignoring External Factors:** Traditional Kelly implementations do not account for external factors such as Federal Reserve rates, margin requirements, or market volatility, which can impact risk and returns.

### Addressing Traditional Limitations

Recognizing these limitations, the **Weekly Seasonality with Dynamic Kelly Criterion Indicator** introduces enhancements to the traditional Kelly approach:

- **Incorporation of Fed Stance:** Adjusts the Kelly Fraction based on the current stance of the Federal Reserve (neutral, dovish, or hawkish), reflecting broader economic conditions that influence market behavior.

- **Margin and Leverage Considerations:** Accounts for margin rates and leverage, ensuring that position sizes remain within manageable risk parameters.

- **Dynamic Adjustments:** Continuously updates position sizes based on real-time risk assessments and probabilistic analyses, mitigating the risk of ruin associated with static Kelly implementations.

## How the Indicator Aids Traders

### For Short-Term Swing Traders

Short-term swing traders thrive on capitalizing over weekly price movements. The indicator aids them by:

- **Identifying Favorable Weeks:** Highlights weeks with above-average returns and favorable volatility, guiding entry and exit points.

- **Optimal Position Sizing:** Utilizes the Adjusted Kelly Fraction to determine the optimal amount to invest, balancing potential returns with risk exposure.

- **Probabilistic Insights:** Provides metrics like Positive Percentage (%) and Kelly Ratio to assess the likelihood of favorable outcomes, enhancing decision-making.

### For Long-Term Tax-Free Investors

This is effectively a drop-in replacement for DCA which uses fixed position size that doesn't change based on market conditions, as a result, it's like catching multiple falling knifes by the blade and smiling with blood on your hand... I don't know about you, but I'd rather juggle by the hilt and look like an actual professional...

Long-term investors, especially those seeking tax-free positions (e.g., through retirement accounts), benefit from:

- **Consistent Risk Management:** Ensures that position sizes are aligned with long-term capital preservation strategies.

- **Seasonality Analysis:** Allows for strategic positioning based on historical performance trends across different weeks and quarters.

- **Dynamic Adjustments:** Adapts to changing market conditions, maintaining optimal risk profiles over extended investment horizons.

### Developers

Please double check the logic and functionality because I think there are a few issue and I need to crowd source solutions and be responsible about the code I publish. If you have corrections, please DM me or leave a respectful comment.

I want to publish this by the end of the year and include other things like highlighting triple witching weeks, adding columns for volume % stats, VaR and CVaR, alpha, beta (to see the seasonal alpha and beta based off a benchmark ticker and risk free rate ticker and other little goodies.

Trend Following Moron TFM 10% System

Trend Following Moron TFM 10% System

The TFM 10% Market Timing System

The Trend Following Moron TFM 10% System is a powerful trading tool designed using Pine Script™, following the principles outlined by Dave S. Landry. This script helps traders identify optimal entry and exit points based on moving averages and market trends.

What the Script Does:

Visual representation of trend strength.

As long as it is trending in green band, trend is very strong and price is contained within 5% of the high.

As price drops to yellow band, strength is weakening and caution is advised. Price is between 5% to 10% away from52 week high.

As price drops in red band, it is to be avoided as trend is rolling over. Price is more than 10% way from 52 week high.

Moving Averages Calculation:

Users can choose between Simple Moving Average (SMA) and Exponential Moving Average (EMA) for daily, weekly, and monthly periods. The script calculates the moving averages to provide trend direction.

Trend Color Coding:

Moving averages are displayed in different colors based on market conditions: green indicates an uptrend, red for a downtrend, and gray for neutral conditions.

Highs Calculation:

The script calculates the 52-week and 12-month closing highs, which are crucial for identifying potential breakout points.

Level Definition:

Traders can set levels based on either Average True Range (ATR) or percentage changes from these highs, allowing for flexible risk management strategies.

Buy and Sell Conditions:

The script defines specific buy conditions: when the price is within 10% of the highest close and trading above the moving averages, and sell conditions: when the price falls below these thresholds.

Visual Indicators:

Buy and sell signals are visually represented on the chart with arrows, making it easy for traders to see potential trading opportunities at a glance.

Performance Labels:

The script includes performance labels that track the number of bars above or below the moving averages and the percentage change from the moving average, providing users with key metrics to evaluate their trades.

Interactive Table:

A table summarizing the buy and sell rules is displayed on the chart, ensuring that traders have quick access to the system’s trading logic.

Benefits of Using the TFM 10% System:

Streamlined Decision Making:

The script simplifies the trading process by clearly outlining buy and sell signals, making it accessible even for novice traders.

Customizable Parameters:

Users can tailor the script to their preferences by adjusting moving average types and lengths, ATR levels, and percentage thresholds. Bands are interchange able for ATR and Percent below 52 week high for volatility looks. But buy and sell are fixed in 10% threshold.

Risk Management:

By utilizing ATR and percentage levels, traders can effectively manage their risk, making the trading process more systematic.

Comprehensive Market Analysis:

The combination of multiple time frames (daily, weekly, monthly) allows for a well-rounded analysis of market trends, enhancing trading accuracy.

V20 with Prices- Ashish SinghV20 with Prices

The V20 with Prices strategy is a unique tool designed to assist traders in identifying potential buy and sell levels by analyzing continuous bullish price movements (green candles). This strategy tracks streaks of green candles and calculates key price levels based on the highest and lowest points during the streak. It highlights potential reversal points, giving traders insights into where they could consider buying or selling based on price movement thresholds.

Key Features:

Tracking Green Candle Streaks: The V20 with Prices strategy identifies sequences of continuous green candles and captures the lowest price and highest price within the streak, helping traders identify potential turning points in an uptrend.

Next Buy and Sell Levels: After a streak of green candles ends, the strategy highlights:

Next Buy at: The lowest price of the streak, indicating a potential re-entry point if the price revisits this level.

Next Sell at: The highest price of the streak, indicating a potential profit-taking point if the price reaches this level again.

Both of these price levels are displayed on the chart, and traders can choose whether to show these levels via customizable input settings.

Movement Percentage Highlight: The strategy calculates the percentage movement between the lowest and highest prices in the streak. If the movement exceeds the user-defined threshold (default is 20%), it highlights these candles with a green background, allowing traders to quickly identify significant price movements.

Customizable Price Display: Users can toggle the display of the Next Buy at and Next Sell at price levels through input settings, providing full control over what is shown on the chart.

How It Works:

Green Candle Tracking: The strategy identifies a streak of green candles where the close price is higher than the open price. During this streak, the lowest low and highest high are tracked.

Price Movement Threshold: If the movement between the lowest low and highest high exceeds the user-defined threshold, the candles are highlighted with a green background.

Key Levels: After a streak of green candles ends (when a red candle appears), the Next Buy at and Next Sell at levels are stored and displayed, giving traders clear reference points for future price action.

How to Use:

Movement Threshold: Customize the movement threshold to filter significant price moves. A higher threshold reduces sensitivity to small movements, while a lower threshold increases sensitivity.

Customizable Price Display: Toggle the display of key price levels to match your trading style.

Ideal Use Cases:

Trend-following: The strategy is perfect for traders looking to identify potential re-entry points during an uptrend or take-profit points as the price reaches new highs.

Retracement Trading: Traders can monitor the Next Buy at level to capitalize on price retracements after strong upward movements.

Important Notes:

Disclaimer: This strategy is for informational purposes only and is not intended as financial advice or a buy/sell recommendation. Traders should always perform their own analysis before making any trading decisions.

Non-Repainting: This strategy does not repaint, ensuring that all displayed levels are based on actual price action.

Open Source: The logic and source code are transparent, allowing traders to modify the strategy if needed.

ANN Trend PredictionThis trend indicator utilizes an artificial neural network (ANN) to predict the next market reversal within a certain range of previous candles. The larger the range of previous candles you set, the fewer reversals will be predicted, and trends will tend to last longer.

The ANN is trained on the BTCUSD 4-hour chart, so using it on other assets or timeframes may yield suboptimal results. It takes three input values: the closing price, the Stochastic RSI, and a Choppiness Indicator. Based on these inputs, the ANN categorizes the current candle as part of an uptrend, downtrend, or as undefined.

Compared to an EMA-based trend indicator, this ANN identifies reversals several candles earlier. It achieves this by detecting subtle patterns in the input values that typically appear before a market turnaround. These patterns are somewhat specific to that chosen asset and timeframe.

The results are displayed using rows of triangles that indicate the predicted price direction. The price levels of the triangles correspond to the closing price at the last reversal. The area between the triangle row and the price is colored green if the ANN correctly predicted the move, and red if it did not.

This indicator is designed to showcase the capabilities and potential of ANNs, and is not intended for actual trading use. The ANN can be trained on any other input values, assets and timeframes for several predictions tasks.

You can use the Predicted_Trend_Signal of this Indicator in any backtest indicator. In the Backtester just grap the Predicted_Trend_Signal. downtrend = 1, uptrend = -1, undefined = 0

Feel free to write me a comment.

Consecutive Beta with Dynamic Support Resistance [TrendX_]The Consecutive Beta with Dynamic Support Resistance indicator is tailored to harness trend momentum, recognize top & bottom reversals, and leverage dynamic support and resistance levels. This indicator introduces a new approach by combining the concepts of beta, consecutive counting mechanisms, and the supertrend structure, making it a fresh tool for understanding market trends and patterns.

💎 KEY FEATURES

Candle’s Relative Valuation Using Beta: The core of the TrendX indicator lies in using beta to gauge volatility. Beta serves as a measure of how an asset moves relative to the broader market, helping traders understand whether the asset is more or less volatile in different market conditions.

Counting Techniques for Momentum & Reversals: By employing counting techniques to reach a significant threshold, the indicator can measure trend momentum and spot top/bottom reversals.

Dynamic Support & Resistance: This feature relies on consecutive beta counting to dynamically adapt support and resistance levels. These levels are key in predicting potential entry and exit points following the general trend direction.

⚙️ USAGES

Initial Start and Distance: Customize the initial start point and distance for better control over trading strategies. For instance, starting at 1 and using an even distance of 2 will yield odd consecutive counting series;

Phase 1 Completion for Reversal Strategies: This initial phase focuses on identifying short-term reversals;

Phase 2 Completion for Support/Resistance: A support level forms after completing two bullish phases, while a resistance level forms after completing two bearish phases. This structure helps in clarifying trend directions when breakout these key levels.

🔎 BREAKDOWN

Phase 1:

The indicator counts consecutive candles that show a higher Beta than in previous periods over a given length. The completion of countings only succeed when the whole series is uninterruptedly counted, or else countings will be canceled. This strict adherence to consecutive counts serves to ensure that only strong, sustained momentum is recognized and also helps filter out noise, weak signals and establish the initial direction catalyst, setting up for further trend analysis.

Phase 2:

After Phase 1 ends, the Phase 2 counting mechanism begins. This phase focuses on bottom reversals through consecutive higher beta candles, and top reversals by counting lower beta candles. At this stage, interuptions will not cancel the counting process. The ability to continue counting in Phase 2 allows for a broader perspective on market behavior. Even if individual candles do not consistently meet the criteria for consecutive counts, the cumulative effect of higher or lower beta readings over time provides valuable insights into market sentiment and trend direction.

Dynamic Support & Resistance:

After Phase 2 completion, if the average of high, low, and close surpasses both recent support and resistance levels from Phase 2, an uptrend is confirmed, which the support level is displayed. If it drops below these levels, a downtrend is indicated, where resistance is displayed instead of support. The result is displayed through a colored supertrend-line (teal for uptrend, red for downtrend).

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur. Therefore, one should always exercise caution and judgment when making decisions based on past performance.

Indicator Test with Conditions TableOverview: The "Indicator Test with Conditions Table" is a customizable trading strategy developed using Pine Script™ for the TradingView platform. It allows users to define complex entry conditions for both long and short positions based on various technical indicators and price levels.

Key Features:

Customizable Input Conditions:

Users can configure up to three input conditions for both long and short entries, each with its own logical operator (AND/OR) for combining conditions.

Input conditions can be based on:

Price Sources: Users can select any price data (e.g., close, open, high, low) for each condition.

Comparison Operators: Users can choose from a variety of operators, including:

Greater than (>)

Greater than or equal to (>=)

Less than (<)

Less than or equal to (<=)

Equal to (=)

Not equal to (!=)

Crossover (crossover)

Crossunder (crossunder)

Logical Operators:

The strategy provides options for combining conditions using logical operators (AND/OR) for greater flexibility in defining entry criteria.

Dynamic Condition Evaluation:

The strategy evaluates the defined conditions dynamically, checking whether they are enabled before proceeding with the comparison.

Users can toggle conditions on and off using boolean inputs, allowing for quick adjustments without modifying the code.

Visual Feedback:

A table is displayed on the chart, providing real-time status updates on the conditions and whether they are enabled. This enhances user experience by allowing easy monitoring of the strategy's logic.

Order Execution:

The strategy enters long or short positions based on the combined conditions' evaluations, automatically executing trades when the criteria are met.

How to Use:

Set Up Input Conditions:

Navigate to the strategy’s input settings to configure your desired price sources, operators, and logical combinations for long and short conditions.

Monitor Conditions:

Observe the condition table displayed at the bottom right of the chart to see which conditions are enabled and their current evaluations.

Adjust Strategy Parameters:

Modify the conditions, logical operators, and input sources as needed to optimize the strategy for different market scenarios or trading styles.

Execution:

Once the conditions are met, the strategy will automatically enter trades based on the defined logic.

Conclusion: The "Indicator Test with Conditions Table" strategy is a robust tool for traders looking to implement customized trading logic based on various market conditions. Its flexibility and real-time monitoring capabilities make it suitable for both novice and experienced traders.

Custom Text BoxThis is an indicator to have text anchored in any symbol or chart, keep your ules at sight so is easy for you to follow, have your Bias too.

GBP Index vs CAD Index Currency OscillatorGBP vs CAD Currency Oscillator

This custom oscillator compares the relative strength of GBP (British Pound) and CAD (Canadian Dollar) against a basket of other currencies to determine potential overbought and oversold conditions. The indicator is designed to help traders evaluate momentum shifts and identify possible trend reversals between these two currencies, not just the GBPCAD pair.

How it Works:

Currency Index Calculation:

The oscillator calculates the average percentage change in 7 key GBP pairs (GBPUSD, EURGBP, GBPJPY, GBPAUD, GBPNZD, GBPCAD, and GBPCHF).

Similarly, it calculates the average percentage change for 7 key CAD pairs (USDCAD, EURCAD, CADJPY, AUDCAD, NZDCAD, GBPCAD, and CADCHF).

Stochastic Oscillator:

The indicator calculates a 0-100 oscillator for both the GBP and CAD currency indices based on the highest high and lowest low over a user-defined lookback period (default is 14 anlthough 60 works great on 1m chart).

The oscillator is smoothed using a simple moving average (default smoothing period is 3) to reduce noise and improve visual clarity.

Overbought/Oversold Conditions:

Overbought: When both the GBP and CAD oscillators exceed 80, the background turns red, indicating potential overbought conditions.

Oversold: When both oscillators fall below 20, the background turns green, signaling possible oversold conditions.

Crossovers:

When the GBP oscillator crosses above the CAD oscillator, a green dot appears at the bottom of the chart, signaling potential GBP strength.

When the GBP oscillator crosses below the CAD oscillator, a red dot appears, signaling potential CAD strength.

How to Use:

Overbought/Oversold Conditions: Use the red and green background highlights to spot potential overbought or oversold market conditions, helping you identify possible turning points.

Customization Options:

Lookback Period: You can adjust the lookback period for the stochastic calculation, allowing for sensitivity tuning (default: 14).

Smoothing Period: Control the degree of smoothing applied to the oscillators (default: 3).

This oscillator is ideal for traders focused on trading GBP and CAD pairs, offering a comparative analysis that can assist in better decision-making based on relative currency strength.

New York Midnight Indicator█ OVERVIEW

This script provides a visual tool for traders to track the New York Midnight (NY Midnight), a significant time marker for those who rely on New York’s financial markets. The script calculates the exact moment of midnight in New York and places a vertical line on the chart at this time, helping traders identify when a new trading day begins according to the New York time zone. The indicator also marks the midnight point with a lime-colored downward triangle to enhance visibility on the chart. It is specifically useful for traders who want to synchronize their strategies with New York’s trading hours, especially in global markets.

The script is flexible, allowing traders to adjust the UTC offset to accommodate different time zones. This is critical for those trading in different regions but still using New York as the main time reference.

█ CONCEPTS

New York Midnight: For many traders, especially those following the Forex and US stock markets, midnight in New York signifies the start of a new trading day. This point is essential for technical analysis as it often aligns with daily opening ranges, trend shifts, and volume spikes.

UTC Offset: The script includes a user-input parameter (utcOffset) to adjust the calculated time for New York midnight, ensuring that it accounts for time zone differences. This allows it to be used effectively regardless of the user’s local time zone, offering flexibility to global traders.

█ METHODOLOGY

UTC Offset Adjustment: The script starts by asking the trader to input their UTC offset (e.g., UTC -5 for New York without daylight saving time). This offset is added to the current chart time to align it with New York’s local time.

Current Hour Calculation: Once the UTC offset is applied, the script calculates the New York Hour by taking the chart’s current hour and adjusting it with the offset. This ensures that the displayed hour matches New York’s local time, regardless of the trader's location.

Vertical Line at Midnight: When the current New York hour equals 00:00 (midnight), the script plots a black vertical line on the chart. This line serves as a visual reference for the exact moment when New York's trading day begins, allowing traders to align their strategies accordingly.

Downward Triangle Plot: In addition to the vertical line, the script also adds a lime-colored downward triangle at the same bar location to further highlight the midnight point. This is useful for traders who prefer shape markers to visualize significant time events.

█ HOW TO USE

Identifying Daily Resets: The script makes it easy for traders to track when New York’s trading day resets. This is especially useful in Forex markets, where daily cycles and time zone-based volatility play an important role in price movement and volume spikes.

Time Zone Flexibility: By adjusting the UTC offset parameter, traders across the globe can synchronize their charts with New York time. This is critical for international traders who want to execute trades based on New York market patterns but reside in different time zones.

Strategic Time Marking: The vertical line and shape markers at midnight allow traders to quickly see when a new trading day starts, helping them identify patterns like the daily range, key support/resistance levels, or even potential reversals around this time.

Session-Based Analysis: Traders who work with session-based strategies (e.g., trading the Asian, European, or US sessions) can use this marker to better time their entries or exits relative to the start of the New York session.

█ METHOD VARIANTS

This script can be modified or extended in various ways to better suit specific trading strategies:

Highlighting Other Session Starts: It could be adapted to plot lines for other key session starts (e.g., London open, Tokyo open).

Multiple Time Zones: For traders who monitor several markets, the script could be extended to display midnight markers for multiple time zones.

Custom Line Styles: Users could modify the line color, thickness, or style to better match their chart aesthetic or preferences.

3% Above and Below Previous Day Close (Stable)This indictor will mark intraday levels. Levels will be marked by calculating 3% up and 3% down from previous day close.

This indicator calculates 3% levels above and below the previous day's close. These levels can be used to track potential support or resistance levels throughout the trading day.

This script helps plot 3% above and below the previous day's close price. It allows you to toggle historical levels and can be useful for monitoring potential intraday price action around these key levels.

ADX Trend Strength Analyzer█ OVERVIEW

This script implements the Average Directional Index (ADX), a powerful tool used to measure the strength of market trends. It works alongside the Directional Movement Index (DMI), which breaks down the directional market pressure into bullish (+DI) and bearish (-DI) components. The purpose of the ADX is to indicate when the market is in a strong trend, without specifying the direction. This indicator can be especially useful for identifying market trends early and validating trading strategies based on trend-following systems.

The ADX component in this script is based on two key parameters:

ADX Smoothing Length (adxlen), which determines the degree of smoothing for the trend strength.

DI Length (dilen), which defines the look-back period for calculating the directional index values.

Additionally, a horizontal line is plotted at the 30 level, providing a widely used threshold that signifies when a trend is considered strong (above 30).

█ CONCEPTS

Directional Movement (DM): The core idea behind this indicator is the calculation of price movement in terms of bullish and bearish forces. By evaluating the change in highs and lows, the script distinguishes between bullish movement (+DM) and bearish movement (-DM). These values are normalized by dividing them by the True Range (TR), creating the +DI and -DI values.

True Range (TR): The True Range is calculated using the Average True Range (ATR) formula, and it serves to smooth out volatility, ensuring that short-term fluctuations don't distort the long-term trend signal.

ADX Calculation: The ADX is derived from the absolute difference between the +DI and -DI. By smoothing this difference and normalizing it, the ADX is able to measure the overall strength of the trend without regard to whether the market is moving up or down. A rising ADX indicates increasing trend strength, while a falling ADX signals weakening trends.

█ METHODOLOGY

Directional Movement Calculation: The script first determines the upward and downward price movement by comparing changes in the high and low prices. If the upward movement is greater than the downward movement, it registers a bullish signal and vice versa for bearish movement.

True Range Adjustment: The script then applies a smoothing function to normalize these movements by dividing them by the True Range (ATR). This ensures that the trend signal is based on relative, rather than absolute, price movements.

ADX Signal Generation: The final step is to calculate the ADX by applying the Relative Moving Average (RMA) to the difference between +DI and -DI. This produces the ADX value, which is plotted in red, making it easy to visualize shifts in market momentum.

Threshold Line: A blue horizontal line is plotted at 30, which serves as a key reference point. When the ADX is above this line, it indicates a strong trend, whether bullish or bearish.

█ HOW TO USE

Trend Strength: Traders typically use the 30 level as a critical threshold. When the ADX is above 30, it signifies a strong trend, making it a favorable environment for trend-following strategies. Conversely, ADX values below 30 suggest a weak or non-trending market.

+DI and -DI Relationship: The indicator also provides insight into whether the trend is bullish or bearish. When +DI is greater than -DI, the market is considered bullish. When -DI is greater than +DI, the market is considered bearish. While this script focuses on the ADX value itself, the underlying +DI and -DI help interpret the trend direction.

Market Conditions: This indicator is effective in trending markets, but not ideal for choppy or sideways conditions. Traders can use it to determine the best entry and exit points when trends are strong, or to avoid trading in periods of low volatility.

Combining with Other Indicators: The ADX is commonly used in conjunction with oscillators like RSI or moving averages, to confirm the trend strength and avoid false signals.

█ METHOD VARIANTS

This script applies the standard approach for calculating the ADX, but could be adapted with the following variants:

Different Timeframes: The script could be modified to calculate ADX values across higher or lower timeframes, depending on the trader's strategy.

Custom Thresholds: Instead of using the default 30 threshold, traders could adjust the horizontal line to suit their own risk tolerance or market conditions.

Candle Low Offset [QuadzCrypto]==== Candle Low Offset Indicator ====

==== Overview ====

The "Candle Low Offset" indicator offers a method for tracking a price point that sit below the low of each candle by a percentage offset.

It was originally intended to provide a price point with flexibility for setting a stop loss below the entry candle low, however, it could be used for other applications.

==== Definitions ====

- Offset Percentage: The % below the low you wish the trend line to follow configurable to 0.01 increments

==== Plots ====

- Offset: Plots a trend line below the candle lows

==== Style ====

- Offset: Allows users to configure the colour and thickness of the offset plot line

==== Application ====

This has been coded to be used with the Max StopLoss function on the Krown Quant SKX indicator to provide an alternative stop loss location on the entry candle.

==== Disclaimer ====

This indicator is for educational purposes only and should not be construed as financial advice. Trading involves risk, and you should consult with a qualified financial advisor before making any trading decisions.

Custom Pattern DetectionOverview

Chart Patterns is a major tool for many traders. Pattern formation at specific location on the chart is used for investment/trading decisions.

This indicator is designed in a way to allow investors/traders to define patterns of their choice based on certain input parameters and then detect defined pattern on the chart.

Investors/traders can use their own creativity to create and detect patterns.

This indicator works in 2 modes

Create Pattern: One can define a pattern and verify sample pattern formation visually

Detect Pattern: Detect and mark patterns on the chart

Settings

Create Custom Pattern:

Show Custom Pattern – This will mark the pattern lines on the chart so that one can verify how pattern appears based on the input’s parameters provided for lines XA, AB, BC, CD, DE, EF

Offset – Used while pattern creation. Offset is horizonal distance between 2 lines.

XA Points – Used to draw XA line when sample pattern is drawn. XA points can be a negative or position number.

XA line is drawn based on Offset and XA Points. E.g. Offset = 5 and XA Points = -20. In this line would be drawn from last candle high to high – 20 (these are y1 and y2 points of a line). While drawing line distance of 5 candles would be placed between 2 line points (these are x1 and x2 points of a line). In XA line X forms start point and A forms end point of the line.

Line AB – Line AB is drawn from point X. To derive the end point of AB, average Fib% is derived based on From Fib% and To Fib% parameters. Finally end point is derived by applying Fib Retracement on Line XA based on average Fib%.

Line AB to Line EF – These points are derived as explained in Line AB.

The indicator can be used to define/create patterns up to 6 legs/lines. The line would be named as XA -> AB -> BC -> CD -> DE -> EF.

If one wish to create pattern consisting 3 legs then it can be achieved by unchecking/deselecting Line CD, DE and EF or by checking only Line AB and BC.

Based on the parameters above indicator draws a sample pattern after last candle/bar on the chart. Sample pattern helps to visually see how pattern will appear on the chart.

Pattern Identification

Indicator derive the swing high/low points based on the Pivot lookback and use as reference points while detecting patterns.

Use of From Fib% and To Fib% - While detecting pattern, retracement price points are derived for From Fib% and To Fib%. Price points between from Fib% and To Fib% are treated as valid retracement points.

How to configure and use indicator for detecting patterns

Sample Pattern 1

Sample Pattern 2

Sample Pattern 3

Sample Pattern 4

Supply Demand by WowTradingInfoThis indicator identifies supply and demand zones based on price action, which is a crucial concept for technical analysis. Supply zones represent areas where the price has historically shown selling pressure, while demand zones show areas with strong buying interest.

Explanation:

Rally-Base-Rally (RBR):

A rally is defined as a price movement where the percentage increase between the current high and the previous low.

A base is defined as a period of consolidation where price stays within a narrow range, with low volatility.

A RBR pattern is detected when a rally occurs, followed by a base, and then another rally.

Drop-Base-Drop (DBD):

A drop is identified when the price decrease between the current low and the previous high.

A DBD pattern is detected when a drop occurs, followed by a base, and then another drop.

Zone Marking:

RBR Zones are drawn with repaint the candles color as yellow (where buyers are likely to step in).

DBD Zones are drawn with repaint the candles color as pink (where sellers are likely to step in).

Example Use Case:

Rally-Base-Rally: When you see a yellow zone, it suggests that price rallied, consolidated, and is likely to rally again. It can be used as a potential demand zone.

Drop-Base-Drop: pink zones indicate that price dropped, consolidated, and may drop again. It can be used as a potential supply zone.

This script will help you automatically detect and visualize RBR and DBD patterns on your TradingView chart. These zones can provide valuable insights into areas where price may react due to past buying or selling pressure.

Elite By Ashu4750Inside Bar Detection:

The script identifies inside bars, which are candles where the high is lower and the low is higher than the previous bar. It tracks the high and low of the mother candle (the candle preceding the inside bars) and plots the ranges on the chart using lines and labels.

Exponential Moving Averages (EMA):

Three EMAs are calculated and plotted (with default periods of 9, 21, and 50). This is a classic trend-following technique used to smooth price data and identify the direction of the market.

Bollinger Bands (BB):

The script includes a Bollinger Band calculation using the simple moving average (SMA) with a standard deviation multiplier. The bands help visualize volatility and potential overbought or oversold conditions.

The user can configure settings like the length of the SMA and the multiplier for the upper and lower bands.

Volume Weighted Average Price (VWAP):

The VWAP is plotted on the chart and reset based on user-defined timeframes (e.g., session, week, month). VWAP is a popular indicator for institutional trading, as it shows the average price weighted by volume and can act as support or resistance.

Crossover Signals (Buy/Sell):

A combination of crossovers between VWAP, EMAs, and Bollinger Bands triggers buy and sell signals. Specifically:

Buy signal is generated when VWAP crosses over the 9 EMA, the close crosses over the Bollinger Band line, and VWAP crosses over the Bollinger Band.

Sell signal is triggered when VWAP crosses under the 9 EMA, and similar conditions exist for the other indicators.

These signals are plotted with a green "Buy" or red "Sell" marker below the bars, and alerts are set up for both buying and selling.

Additional Bollinger Band Configuration:

The script provides more flexibility in Bollinger Bands by allowing the user to select between SMA, EMA, or SMMA for the moving average.

The user can also choose the standard deviation multiplier and whether to display the bands.

Alerts:

Buy and sell conditions are linked to alert conditions, allowing the user to be notified when a signal is triggered, based on the defined crossover logic.

Technical Breakdown:

Inside Bar Logic: Tracks inside bars and plots lines representing the high and low of the mother candle. The line and label functions are used to draw these on the chart, which provides a visual representation of the range.

EMA and VWAP Crossovers:

The 9, 21, and 50-period EMAs are calculated and used in crossover logic with VWAP. Crossovers between VWAP and EMAs are a common method for identifying potential trend changes.

Bollinger Bands:

The Bollinger Band component allows for volatility analysis by calculating the upper and lower bands based on the moving average's standard deviation.

Alert System:

Alerts are set for crossover signals, allowing for real-time notifications of potential buy and sell opportunities.

Visualization:

The script plots the EMAs, VWAP, and Bollinger Bands on the price chart. It highlights inside bar patterns and displays buy/sell markers on the chart when the specified conditions are met. These visual cues make it easier to follow the market’s movements and spot trading opportunities.

Customizability:

The script is highly customizable with inputs for:

EMA periods.

VWAP settings.

Bollinger Band parameters (moving average type, length, standard deviation).

Candle color options for inside bars.

In this traders looking for multiple indicators to analyze market trends, volatility, and price action.

Shifted Symbol Overlay with OffsetThe Shifted Symbol Overlay Indicator is a custom TradingView indicator designed to overlay the price data of one stock or asset over another, allowing for direct visual comparison. This is particularly useful for comparing the performance of two assets over different time periods. The indicator enables you to shift the data from one asset either forward or backward in time, making it easier to compare historical data from one stock with more recent data from another. The indicator supports shifting both to the right (future periods) and to the left (earlier periods), helping traders and analysts explore correlations or divergences between two financial instruments.

The indicator also includes a normalization option that adjusts the scale of the two assets, so you can compare them even if they have vastly different price levels. This is useful when you're interested in relative performance rather than the absolute price values.

Cumulative Volume Delta Divergence [TradingFinder] Periodic EMA🔵 Introduction

The Cumulative Volume Delta (CVD) is a powerful tool in technical analysis that is derived from market volume or trading activity. The Cumulative Volume Delta Divergence Detector Indicator helps traders identify Cumulative Volume Delta Divergences (CVD Divergence), which can provide reliable trading signals.

These divergences, such as bullish and bearish CVD divergences, act as key indicators of potential trend reversals in financial markets. By analyzing CVD divergences, traders can gain insights into the strength of buying and selling pressure and make more informed predictions about price trends.

The CVD indicator is particularly effective for traders who engage in day trading and scalping, as it helps identify price reversal points by analyzing volume and price behavior.

Using the CVD indicator in combination with other technical tools such as support and resistance levels and candlestick patterns allows for a more accurate market analysis.

🔵 How to Use

Divergences are one of the most important technical analysis signals that indicate the current strength of a price move may not be sustainable.

Cumulative Volume Delta Divergence helps traders identify potential trading opportunities that may not be visible on the price chart alone.

This type of divergence examines the relationship between buying and selling volume and price, enabling traders to better understand price trends.

🟣 Bullish CVD Divergence

A bullish CVD divergence occurs when the price makes a lower low, but the CVD indicator shows a higher low. This indicates increasing buying pressure in the market, even though the price is declining. In other words, despite the price dropping, buyers are gradually gaining strength, which could signal a price reversal and the start of a bullish trend.

How to use this signal : In this scenario, traders looking to go long can use this signal as a favorable opportunity to enter the market. After a bullish divergence, the market typically tends to move upward.

To reduce risk, traders can wait for further confirmation from the price chart. For example, if the price breaks through the previous high after the divergence or breaks a resistance level, this could be a more reliable signal for entering the market.

🟣 Bearish CVD Divergence

A bearish CVD divergence is the opposite of a bullish divergence. In this type of divergence, the price makes a higher high, but the CVD indicator shows a lower high. This indicates decreasing buying pressure and weakening momentum in the current bullish trend. A bearish divergence often serves as a warning of a potential market reversal to the downside.

How to use this signal : Traders can use this divergence as an opportunity to exit long positions or enter short positions. When the CVD indicator makes a lower high compared to the price, it signals weakness in buyer strength.

If traders receive further confirmation from the price chart, such as a break of key support levels or an increase in selling volume, this can serve as a stronger signal for the beginning of a bearish trend.

🟣 How to Build a Trading Strategy with Cumulative Volume Delta Divergence

Using CVD divergence alone may not be sufficient. Traders should combine this tool with other technical analysis techniques and indicators to have more confidence in their decisions. For example, when observing a CVD divergence, traders can also analyze volume, trend lines, or candlestick patterns to get a more accurate market analysis.

Additionally, risk management should always be a priority. Using stop-loss orders and properly sizing trades can help traders minimize their losses if they make a mistake.

🔵 Setting

Divergence Fractal Period : Determines the period of swings. The minimum and default value is 2.

CVD Period : You can set the period of " Periodic " and " EMA " modes.

Cumulative Mode : It has three modes "Periodic" and "EMA". In "Periodic" mode, it accumulates the volume periodically and in "EMA" mode, it calculates the moving average of the volume.

Market Ultra Data : If you turn on this feature, 26 large brokers will be included in the calculation of the trading volume. The advantage of this capability is to have more reliable volume data. You should be careful to specify the market you are in, FOREX brokers and Crypto brokers are different.

🔵 Conclusion

The Cumulative Volume Delta (CVD) indicator is a powerful tool in technical analysis, helping traders better identify price trends and make more accurate market predictions. By identifying CVD divergences, traders can anticipate price reversals and time their market entries and exits accordingly.

Bullish and bearish CVD divergences each provide valuable signals that can help traders identify the best entry and exit points in the market. A bullish CVD divergence signals strength in buying that will likely lead to a price increase, while a bearish CVD divergence indicates weakness in the bullish trend and the potential for the beginning of a bearish trend.

Overall, combining CVD with other technical analysis tools and employing risk management strategies can help traders make better trading decisions and capitalize on available market opportunities.

Nifty Dashboard//@version=5

//Author @GODvMarkets

indicator("GOD NSE Nifty Dashboard", "Nifty Dashboard")

i_timeframe = input.timeframe("D", "Timeframe")

// if not timeframe.isdaily

// runtime.error("Please switch timeframe to Daily")

i_text_size = input.string(size.auto, "Text Size", )

//-----------------------Functions-----------------------------------------------------

f_oi_buildup(price_chg_, oi_chg_) =>

switch

price_chg_ > 0 and oi_chg_ > 0 =>

price_chg_ > 0 and oi_chg_ < 0 =>

price_chg_ < 0 and oi_chg_ > 0 =>

price_chg_ < 0 and oi_chg_ < 0 =>

=>

f_color(val_) => val_ > 0 ? color.green : val_ < 0 ? color.red : color.gray

f_bg_color(val_) => val_ > 0 ? color.new(color.green,80) : val_ < 0 ? color.new(color.red,80) : color.new(color.black,80)

f_bg_color_price(val_) =>

fg_color_ = f_color(val_)

abs_val_ = math.abs(val_)

transp_ = switch

abs_val_ > .03 => 40

abs_val_ > .02 => 50

abs_val_ > .01 => 60

=> 80

color.new(fg_color_, transp_)

f_bg_color_oi(val_) =>

fg_color_ = f_color(val_)

abs_val_ = math.abs(val_)

transp_ = switch

abs_val_ > .10 => 40

abs_val_ > .05 => 50

abs_val_ > .025 => 60

=> 80

color.new(fg_color_, transp_)

f_day_of_week(time_=time) =>

switch dayofweek(time_)

1 => "Sun"

2 => "Mon"

3 => "Tue"

4 => "Wed"

5 => "Thu"

6 => "Fri"

7 => "Sat"

//-------------------------------------------------------------------------------------

var table table_ = table.new(position.middle_center, 22, 20, border_width = 1)

var cols_ = 0

var text_color_ = color.white

var bg_color_ = color.rgb(1, 5, 19)

f_symbol(idx_, symbol_) =>

symbol_nse_ = "NSE" + ":" + symbol_

fut_cur_ = "NSE" + ":" + symbol_ + "1!"

fut_next_ = "NSE" + ":" + symbol_ + "2!"

= request.security(symbol_nse_, i_timeframe, [close, close-close , close/close -1, volume], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_cur_, i_timeframe, , ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_next_, i_timeframe, , ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_cur_ + "_OI", i_timeframe, [close, close-close ], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_next_ + "_OI", i_timeframe, [close, close-close ], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

stk_vol_ = stk_vol_nse_

fut_vol_ = fut_cur_vol_ + fut_next_vol_

fut_oi_ = fut_cur_oi_ + fut_next_oi_

fut_oi_chg_ = fut_cur_oi_chg_ + fut_next_oi_chg_

fut_oi_chg_pct_ = fut_oi_chg_ / fut_oi_

fut_stk_vol_x_ = fut_vol_ / stk_vol_

fut_vol_oi_action_ = fut_vol_ / math.abs(fut_oi_chg_)

= f_oi_buildup(chg_pct_, fut_oi_chg_pct_)

close_color_ = fut_cur_close_ > fut_vwap_ ? color.green : fut_cur_close_ < fut_vwap_ ? color.red : text_color_

if barstate.isfirst

row_ = 0, col_ = 0

table.cell(table_, col_, row_, "Symbol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Close", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "VWAP", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Pts", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Stk Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Fut Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Fut/Stk Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Cur", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Next", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Cur Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Next Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI ", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Vol/OI Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI Chg%", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Pr.Chg%", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Buildup", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

cell_color_ = color.white

cell_bg_color_ = color.rgb(1, 7, 24)

if barstate.islast

row_ = idx_, col_ = 0

table.cell(table_, col_, row_, str.format("{0}", symbol_), text_color = f_color(chg_pct_), bgcolor = f_bg_color_price(chg_pct_), text_size = i_text_size, text_halign = text.align_left), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#.00}", fut_cur_close_), text_color = close_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#.00}", fut_vwap_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00}", chg_pts_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", stk_vol_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_vol_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00}", fut_stk_vol_x_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_cur_oi_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_next_oi_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_cur_oi_chg_), text_color = f_color(fut_cur_oi_chg_), bgcolor = f_bg_color(fut_cur_oi_chg_), text_size = i_text_size, text_halign = text.align_right), col_ += 1