Dual Chain StrategyDual Chain Strategy - Technical Overview

How It Works:

The Dual Chain Strategy is a unique approach to trading that utilizes Exponential Moving Averages (EMAs) across different timeframes, creating two distinct "chains" of trading signals. These chains can work independently or together, capturing both long-term trends and short-term price movements.

Chain 1 (Longer-Term Focus):

Entry Signal: The entry signal for Chain 1 is generated when the closing price crosses above the EMA calculated on a weekly timeframe. This suggests the start of a bullish trend and prompts a long position.

bullishChain1 = enableChain1 and ta.crossover(src1, entryEMA1)

Exit Signal: The exit signal is triggered when the closing price crosses below the EMA on a daily timeframe, indicating a potential bearish reversal.

exitLongChain1 = enableChain1 and ta.crossunder(src1, exitEMA1)

Parameters: Chain 1's EMA length is set to 10 periods by default, with the flexibility for user adjustment to match various trading scenarios.

Chain 2 (Shorter-Term Focus):

Entry Signal: Chain 2 generates an entry signal when the closing price crosses above the EMA on a 12-hour timeframe. This setup is designed to capture quicker, shorter-term movements.

bullishChain2 = enableChain2 and ta.crossover(src2, entryEMA2)

Exit Signal: The exit signal occurs when the closing price falls below the EMA on a 9-hour timeframe, indicating the end of the shorter-term trend.

exitLongChain2 = enableChain2 and ta.crossunder(src2, exitEMA2)

Parameters: Chain 2's EMA length is set to 9 periods by default, and can be customized to better align with specific market conditions or trading strategies.

Key Features:

Dual EMA Chains: The strategy's originality shines through its dual-chain configuration, allowing traders to monitor and react to both long-term and short-term market trends. This approach is particularly powerful as it combines the strengths of trend-following with the agility of momentum trading.

Timeframe Flexibility: Users can modify the timeframes for both chains, ensuring the strategy can be tailored to different market conditions and individual trading styles. This flexibility makes it versatile for various assets and trading environments.

Independent Trade Logic: Each chain operates independently, with its own set of entry and exit rules. This allows for simultaneous or separate execution of trades based on the signals from either or both chains, providing a robust trading system that can handle different market phases.

Backtesting Period: The strategy includes a configurable backtesting period, enabling thorough performance assessment over a historical range. This feature is crucial for understanding how the strategy would have performed under different market conditions.

time_cond = time >= startDate and time <= finishDate

What It Does:

The Dual Chain Strategy offers traders a distinctive trading tool that merges two separate EMA-based systems into one cohesive framework. By integrating both long-term and short-term perspectives, the strategy enhances the ability to adapt to changing market conditions. The originality of this script lies in its innovative dual-chain design, providing traders with a unique edge by allowing them to capitalize on both significant trends and smaller, faster price movements.

Whether you aim to capture extended market trends or take advantage of more immediate price action, the Dual Chain Strategy provides a comprehensive solution with a high degree of customization and strategic depth. Its flexibility and originality make it a valuable tool for traders seeking to refine their approach to market analysis and execution.

How to Use the Dual Chain Strategy

Step 1: Access the Strategy

Add the Script: Start by adding the Dual Chain Strategy to your TradingView chart. You can do this by searching for the script by name or using the link provided.

Select the Asset: Apply the strategy to your preferred trading pair or asset, such as #BTCUSD, to see how it performs.

Step 2: Configure the Settings

Enable/Disable Chains:

The strategy is designed with two independent chains. You can choose to enable or disable each chain depending on your trading style and the market conditions.

enableChain1 = input.bool(true, title='Enable Chain 1')

enableChain2 = input.bool(true, title='Enable Chain 2')

By default, both chains are enabled. If you prefer to focus only on longer-term trends, you might disable Chain 2, or vice versa if you prefer shorter-term trades.

Set EMA Lengths:

Adjust the EMA lengths for each chain to match your trading preferences.

Chain 1: The default EMA length is 10 periods. This chain uses a weekly timeframe for entry signals and a daily timeframe for exits.

len1 = input.int(10, minval=1, title='Length Chain 1 EMA', group="Chain 1")

Chain 2: The default EMA length is 9 periods. This chain uses a 12-hour timeframe for entries and a 9-hour timeframe for exits.

len2 = input.int(9, minval=1, title='Length Chain 2 EMA', group="Chain 2")

Customize Timeframes:

You can customize the timeframes used for entry and exit signals for both chains.

Chain 1:

Entry Timeframe: Weekly

Exit Timeframe: Daily

tf1_entry = input.timeframe("W", title='Chain 1 Entry Timeframe', group="Chain 1")

tf1_exit = input.timeframe("D", title='Chain 1 Exit Timeframe', group="Chain 1")

Chain 2:

Entry Timeframe: 12 Hours

Exit Timeframe: 9 Hours

tf2_entry = input.timeframe("720", title='Chain 2 Entry Timeframe (12H)', group="Chain 2")

tf2_exit = input.timeframe("540", title='Chain 2 Exit Timeframe (9H)', group="Chain 2")

Set the Backtesting Period:

Define the period over which you want to backtest the strategy. This allows you to see how the strategy would have performed historically.

startDate = input.time(timestamp('2015-07-27'), title="StartDate")

finishDate = input.time(timestamp('2026-01-01'), title="FinishDate")

Step 3: Analyze the Signals

Understand the Entry and Exit Signals:

Buy Signals: When the price crosses above the entry EMA, the strategy generates a buy signal.

bullishChain1 = enableChain1 and ta.crossover(src1, entryEMA1)

Sell Signals: When the price crosses below the exit EMA, the strategy generates a sell signal.

bearishChain2 = enableChain2 and ta.crossunder(src2, entryEMA2)

Review the Visual Indicators:

The strategy plots buy and sell signals on the chart with labels for easy identification:

BUY C1/C2 for buy signals from Chain 1 and Chain 2.

SELL C1/C2 for sell signals from Chain 1 and Chain 2.

This visual aid helps you quickly understand when and why trades are being executed.

Step 4: Optimize the Strategy

Backtest Results:

Review the strategy’s performance over the backtesting period. Look at key metrics like net profit, drawdown, and trade statistics to evaluate its effectiveness.

Adjust the EMA lengths, timeframes, and other settings to see how changes affect the strategy’s performance.

Customize for Live Trading:

Once satisfied with the backtest results, you can apply the strategy settings to live trading. Remember to continuously monitor and adjust as needed based on market conditions.

Step 5: Implement Risk Management

Use Realistic Position Sizing:

Keep your risk exposure per trade within a comfortable range, typically between 1-2% of your trading capital.

Set Alerts:

Set up alerts for buy and sell signals, so you don’t miss trading opportunities.

Paper Trade First:

Consider running the strategy in a paper trading account to understand its behavior in real market conditions before committing real capital.

This dual-layered approach offers a distinct advantage: it enables the strategy to adapt to varying market conditions by capturing both broad trends and immediate price action without one chain's activity impacting the other's decision-making process. The independence of these chains in executing transactions adds a level of sophistication and flexibility that is rarely seen in more conventional trading systems, making the Dual Chain Strategy not just unique, but a powerful tool for traders seeking to navigate complex market environments.

Educational

FXN - Week and Day Separator midnight open. A simple modification of the regular FXN day separator indicator. It starts the days at 12:00 of the time-zone you select as opposed to the regular 17:00 server time.

Summer 2020/2021The Pine Script indicator you are examining is designed to enhance your trading chart by visually demarcating specific seasonal periods known as summer for the years 2020 and 2021. This indicator achieves this by employing background shading to indicate these defined summer periods, providing traders with a visual reference to help in analyzing seasonal trends and making informed decisions.

The script operates with precision by defining two critical summer periods: one for the year 2020 and another for the year 2021. The summer period, in this context, is identified as the time span between June 21 and September 22 of each specified year. The script utilizes the Pine Script timestamp function to create exact date and time boundaries for these periods, marking June 21 as the start of summer and September 22 as the end of summer for each year.

In detail, the indicator sets up two distinct background colors to represent the summer periods of 2020 and 2021. Specifically, it employs a semi-transparent blue color to signify the summer period of 2020, and a semi-transparent green color to denote the summer period of 2021. This differentiation in colors allows for easy visual distinction between the two years on the chart.

To achieve this visual effect, the script continuously evaluates the current bar's timestamp against the defined summer periods. If the current bar falls within the summer range of 2020, the background is shaded with the specified blue hue. Conversely, if the current bar is within the summer range of 2021, the background is shaded with the green hue. This approach ensures that the chart background reflects the specific summer periods accurately and distinctly.

By incorporating this indicator into your TradingView chart, you gain the ability to visually distinguish between different summer periods of consecutive years. This can be particularly useful for analyzing how market behavior or price movements vary during these specific times, facilitating better trend analysis and decision-making based on historical seasonal patterns.

Overall, this indicator serves as a practical tool for enhancing your chart's clarity and providing a seasonal context that can aid in the evaluation of trading strategies and historical market trends during the summer months of 2020 and 2021.

Valuation Tool V2Explanation:

Inputs:

equitySymbol: The symbol for the equity index (default is "SPY" for the S&P 500 ETF).

bondSymbol: The symbol for the bond market (default is "TLT" for the 20+ Year Treasury Bond ETF).

Fetch Data:

equityClose and bondClose retrieve the daily closing prices for the specified equity and bond symbols.

Relative Spread Calculation:

The relative spread is calculated by dividing the equity index's closing price by the bond market's closing price.

Thresholds:

The 50-period Simple Moving Average (SMA) of the relative spread is calculated.

Overvalued and undervalued thresholds are set at 10% above and below the SMA, respectively.

Normalized Spread:

The normalized spread is calculated to normalize the relative spread around its SMA, which helps in visualizing it as an oscillator.

Plotting:

The normalized spread is plotted as a blue line in the oscillator panel.

Overvalued and undervalued thresholds are plotted as dotted lines at 0.1 and -0.1, respectively.

The zero line is plotted as a solid orange line.

Background colors indicate overvalued (red) and undervalued (green) regions.

Signals:

Buy signals are plotted when the normalized spread crosses above the undervalued threshold (-0.1).

Sell signals are plotted when the normalized spread crosses below the overvalued threshold (0.1).

This script plots the relative spread as an oscillator, allowing you to see overvalued and undervalued conditions in a separate panel. You can further customize the look and feel based on your preferences and trading strategy.

TCLC(TraderChitra Learning Class)-Option ChainThis indicator plots the Option chain data of the following instruments and columns..

It plots 11 rows ,

5 Rows above the input strike price

1 Row for the input strike price

5 Rows below the input strike price

Instruments :

1. NIFTY

2. BANKNIFTY

3. FINNIFTY

4. MIDCPNifty

Columns :

1. StrikePrice

2.CMP

3.Volume

4.VWAP

5.Diff (Open-Close)

Traders need to change the expiry date to check the premium of the corresponding instruments...

There are few key things,

1. Rows in yellow are marked as ATM strike price

2. Cell values in red / green indicates the prices are trading above / below the VWAP

The prices are expected to be bullish when cmp trades above VWAP and we can gauge the trend

The column Volume provides the details in which strike price more traders are actively traded..

The far month contracts can also be changed in the settings and it helps the swing/positional traders

The Strike price can be modified to check the appropriate strikes

Partial Profit Calculator [TFO]This indicator was built to help calculate the outcome of trades that utilize multiple profit targets and/or multiple entries.

In its simplest form, we can have a single entry and a single profit target. As shown below in this long trade example, the indicator will draw risk and reward boxes (red and green, respectively) with several annotations. On the left-hand side, all entries will be displayed (in this case there is only one entry, "E1"). On the bottom, the "SL" label indicates the trade's stop loss placement. On the top, all target prices are displayed (in this case there is only one target, "TP1"). Lastly, on the right-hand side a label will display the total R that is to be expected from a winning trade, where R is one's unit of risk.

In the following example, we have two target prices - one at 18600 and one at 18700. You can input as many target prices as you'd like, separated by commas, i.e. "18600,18700" in this example. Make sure the values are separated by commas only, and not spaces, new lines, etc. As a result, we can see that the indicator draws where our profit targets would be with respect to our entry, E1. The indicator assumes that equal parts of the trade position are taken off at each target price. In this example on Nasdaq futures (NQ1!), since we have 2 target prices, this would be equivalent to assuming that we take exactly half the trade position off at TP1, and the remaining half of the position at TP2.

If we wanted to take more of the position off at a certain target, we could simply duplicate the target price. Here I set the target prices to "18600,18600,18700" to enforce that two thirds of the position be taken off at TP1 and TP2, while the remaining third gets taken off at TP3.

We can also show outcome annotations to describe how much R is generated from each possible trade outcome. Using the below chart as an example, the stop loss indicates a -1R loss. The total R from this trade criteria is 1.33 R, and each target price shows how much R is being generated if one were to take off an equal part of the position at said target prices. In this case, we would generate 0.17 R from taking one third of the position off at TP1, another 0.5 R from taking one third of the position off at TP2, and another 0.67 R from taking the remaining one third of the position off at TP3, all adding up to the total R indicated on the right-hand side label.

Using multiple entries works the same way as using multiple target prices, where the input should indicate each entry price separated by commas. In this example I've used "18550,18450" to achieve an average price of 18500, as indicated by the "E_avg" label that appears when more than one entry price is utilized. We can also opt to display risk as dollars instead of R values, where you can input your desired risk per trade, and all values are shown as dollar amounts instead of R multiples, as shown below with a risk per trade of $100.

This is meant to be an educational tool for trades that utilize multiple profit targets and/or entries. Hope you like it!

Custom Text DisplayThe "Custom Text Display" indicator allows users to display customizable text in a fixed position in the bottom-right corner of their chart. Each text entry can have its own color, which can be set in the indicator's settings. Follow these steps to set up and use the indicator effectively:

Adding the Indicator to Your Chart:

Apply the "Custom Text Display" indicator to your chart from the indicators list.

Configuring Text and Colors:

Open the settings for the indicator.

Enter the desired text for each of the five text fields labeled "Text 1", "Text 2", etc.

Choose a color for each text entry using the color pickers labeled "Color 1", "Color 2", etc.

Selecting the Active Text:

In the indicator settings, find the "Select Active Text" dropdown menu.

This menu offers six options: "0" (None), "1" (Text 1), "2" (Text 2), "3" (Text 3), "4" (Text 4), and "5" (Text 5).

Select the number corresponding to the text you want to activate. Only one text can be active at a time.

Viewing the Active Text on the Chart:

The selected active text will be displayed in the bottom-right corner of the chart with the corresponding background color.

If no text is selected (option "0"), no text will be displayed.

Volatility Adaptive Signal Tracker (VAST)The Adaptive Trend Following Buy/Sell Signals Pine Script is designed to help traders identify and capitalize on market trends using an adaptive trend-following strategy. This script focuses on generating reliable buy and sell signals by analyzing market trends and volatility. It simplifies the trading process by providing clear signals without plotting additional lines, making it easy to use and interpret.

Key Features:

Adaptive Trend Following:

The script employs an adaptive trend-following approach that leverages market volatility to generate buy and sell signals. This method is effective in both trending and volatile markets.

Inputs and Customization:

The script includes customizable parameters for the Simple Moving Average (SMA) length, the Average True Range (ATR) length, and the ATR multiplier. These inputs allow traders to adjust the sensitivity of the signals to match their trading style and market conditions.

Signal Generation:

Buy Signal: Generated when the closing price crosses above the upper adaptive band, indicating a potential upward trend.

Sell Signal: Generated when the closing price crosses below the lower adaptive band, indicating a potential downward trend.

Visual Signals:

The script uses plotshape to mark buy signals with green labels below the bars and sell signals with red labels above the bars. This clear visual representation helps traders quickly identify trading opportunities.

Alert Conditions:

The script sets up alert conditions for both buy and sell signals. Traders can use these alerts to receive notifications when a signal is generated, ensuring they do not miss any trading opportunities.

How It Works:

SMA Calculation: The script calculates the Simple Moving Average (SMA) over a specified period, which helps in identifying the general trend direction.

ATR Calculation: The Average True Range (ATR) is calculated to measure market volatility.

Adaptive Bands: Upper and lower adaptive bands are created by adding and subtracting a multiple of the ATR to the SMA, respectively.

Signal Logic: Buy signals are generated when the closing price crosses above the upper band, while sell signals are generated when the closing price crosses below the lower band.

Example Use Case:

A trader looking to capitalize on medium-term trends in the Nifty futures market can use this script to receive timely buy and sell signals. By customizing the SMA length and ATR parameters, the trader can fine-tune the script to match their trading strategy, ensuring they enter and exit trades at optimal points.

Benefits:

Simplicity: The script provides clear buy and sell signals without cluttering the chart with additional lines or indicators.

Adaptability: Customizable parameters allow traders to adapt the script to various market conditions and trading styles.

Alerts: Built-in alert conditions ensure traders receive timely notifications, helping them to act quickly on trading signals.

How to Use:

Open TradingView: Go to the TradingView website and log in.

Create a New Chart: Click on the “Chart” button to open a new chart.

Open the Pine Script Editor: Click on the “Pine Editor” tab at the bottom of the chart.

Create a New Script: Delete any default code in the Pine Script editor and paste the provided script.

Add to Chart: Click on the “Add to Chart” button to compile and add the script to your chart.

Save the Script: Click “Save” and name the script.

Set Alerts: Right-click on the chart, select “Add Alert,” and choose the appropriate condition to set alerts for buy and sell signals.

Moving Average Ratio [InvestorUnknown]Overview

The "Moving Average Ratio" (MAR) indicator is a versatile tool designed for valuation, mean-reversion, and long-term trend analysis. This indicator provides multiple display modes to cater to different analytical needs, allowing traders and investors to gain deeper insights into the market dynamics.

Features

1. Moving Average Ratio (MAR):

Calculates the ratio of the chosen source (close, open, ohlc4, hl2 …) to a longer-term moving average of choice (SMA, EMA, HMA, WMA, DEMA)

Useful for identifying overbought or oversold conditions, aiding in mean-reversion strategies and valuation of assets.

For some high beta asset classes, like cryptocurrencies, you might want to use logarithmic scale for the raw MAR, below you can see the visual difference of using Linear and Logarithmic scale on BTC

2. MAR Z-Score:

Computes the Z-Score of the MAR to standardize the ratio over chosen time period, making it easier to identify extreme values relative to the historical mean.

Helps in detecting significant deviations from the mean, which can indicate potential reversal points and buying/selling opportunities

3. MAR Trend Analysis:

Uses a combination of short-term (default 1, raw MAR) and long-term moving averages of the MAR to identify trend changes.

Provides a visual representation of bullish and bearish trends based on moving average crossings.

Using Logarithmic scale can improve the visuals for some asset classes.

4. MAR Momentum:

Measures the momentum of the MAR by calculating the difference over a specified period.

Useful for detecting changes in the market momentum and potential trend reversals.

5. MAR Rate of Change (ROC):

Calculates the rate of change of the MAR to assess the speed and direction of price movements.

Helps in identifying accelerating or decelerating trends.

MAR Momentum and Rate of Change are very similar, the only difference is that the Momentum is expressed in units of the MAR change and ROC is expressed as % change of MAR over chosen time period.

Customizable Settings

General Settings:

Display Mode: Select the display mode from MAR, MAR Z-Score, MAR Trend, MAR Momentum, or MAR ROC.

Color Bars: Option to color the bars based on the current display mode.

Wait for Bar Close: Toggle to wait for the bar to close before updating the MAR value.

MAR Settings:

Length: Period for the moving average calculation.

Source: Data source for the moving average calculation.

Moving Average Type: Select the type of moving average (SMA, EMA, WMA, HMA, DEMA).

Z-Score Settings:

Z-Score Length: Period for the Z-Score calculation.

Trend Analysis Settings:

Moving Average Type: Select the type of moving average for trend analysis (SMA, EMA).

Longer Moving Average: Period for the longer moving average.

Shorter Moving Average: Period for the shorter moving average.

Momentum Settings:

Momentum Length: Period for the momentum calculation.

Rate of Change Settings:

ROC Length: Period for the rate of change calculation.

Calculation and Plotting

Moving Average Ratio (MAR):

Calculates the ratio of the price to the selected moving average type and length.

Plots the MAR with a gradient color based on its Z-Score, aiding in visual identification of extreme values.

// Moving Average Ratio (MAR)

ma_main = switch ma_main_type

"SMA" => ta.sma(src, len)

"EMA" => ta.ema(src, len)

"WMA" => ta.wma(src, len)

"HMA" => ta.hma(src, len)

"DEMA" => ta.dema(src, len)

mar = (waitforclose ? src : src) / ma_main

z_col = color.from_gradient(z, -2.5, 2.5, color.green, color.red)

plot(disp_mode.mar ? mar : na, color = z_col, histbase = 1, style = plot.style_columns)

barcolor(color_bars ? (disp_mode.mar ? (z_col) : na) : na)

MAR Z-Score:

Computes the Z-Score of the MAR and plots it with a color gradient indicating the magnitude of deviation from the mean.

// MAR Z-Score

mean = ta.sma(math.log(mar), z_len)

stdev = ta.stdev(math.log(mar),z_len)

z = (math.log(mar) - mean) / stdev

plot(disp_mode.mar_z ? z : na, color = z_col, histbase = 0, style = plot.style_columns)

plot(disp_mode.mar_z ? 1 : na, color = color.new(color.red,70))

plot(disp_mode.mar_z ? 2 : na, color = color.new(color.red,50))

plot(disp_mode.mar_z ? 3 : na, color = color.new(color.red,30))

plot(disp_mode.mar_z ? -1 : na, color = color.new(color.green,70))

plot(disp_mode.mar_z ? -2 : na, color = color.new(color.green,50))

plot(disp_mode.mar_z ? -3 : na, color = color.new(color.green,30))

barcolor(color_bars ? (disp_mode.mar_z ? (z_col) : na) : na)

MAR Trend:

Plots the MAR along with its short-term and long-term moving averages.

Uses color changes to indicate bullish or bearish trends based on moving average crossings.

// MAR Trend - Moving Average Crossing

mar_ma_long = switch ma_trend_type

"SMA" => ta.sma(mar, len_trend_long)

"EMA" => ta.ema(mar, len_trend_long)

mar_ma_short = switch ma_trend_type

"SMA" => ta.sma(mar, len_trend_short)

"EMA" => ta.ema(mar, len_trend_short)

plot(disp_mode.mar_t ? mar : na, color = mar_ma_long < mar_ma_short ? color.new(color.green,50) : color.new(color.red,50), histbase = 1, style = plot.style_columns)

plot(disp_mode.mar_t ? mar_ma_long : na, color = mar_ma_long < mar_ma_short ? color.green : color.red, linewidth = 4)

plot(disp_mode.mar_t ? mar_ma_short : na, color = mar_ma_long < mar_ma_short ? color.green : color.red, linewidth = 2)

barcolor(color_bars ? (disp_mode.mar_t ? (mar_ma_long < mar_ma_short ? color.green : color.red) : na) : na)

MAR Momentum:

Plots the momentum of the MAR, coloring the bars to indicate increasing or decreasing momentum.

// MAR Momentum

mar_mom = mar - mar

// MAR Momentum

mom_col = mar_mom > 0 ? (mar_mom > mar_mom ? color.new(color.green,0): color.new(color.green,30)) : (mar_mom < mar_mom ? color.new(color.red,0): color.new(color.red,30))

plot(disp_mode.mar_m ? mar_mom : na, color = mom_col, histbase = 0, style = plot.style_columns)

MAR Rate of Change (ROC):

Plots the ROC of the MAR, using color changes to show the direction and strength of the rate of change.

// MAR Rate of Change

mar_roc = ta.roc(mar,len_roc)

// MAR ROC

roc_col = mar_roc > 0 ? (mar_roc > mar_roc ? color.new(color.green,0): color.new(color.green,30)) : (mar_roc < mar_roc ? color.new(color.red,0): color.new(color.red,30))

plot(disp_mode.mar_r ? mar_roc : na, color = roc_col, histbase = 0, style = plot.style_columns)

Summary:

This multi-purpose indicator provides a comprehensive toolset for various trading strategies, including valuation, mean-reversion, and trend analysis. By offering multiple display modes and customizable settings, it allows users to tailor the indicator to their specific analytical needs and market conditions.

ArbitrageDashboardv3310824This indicator allows you to monitor the spread (difference in exchange rates) between two assets in real-time for up to 12 trading pairs simultaneously.

⚙️ How does the indicator work?

In the settings menu, you can select two trading pairs, such as BTCUSDT on Binance and BTCUSDT on Bybit. The script then fetches prices from both exchanges and compares them, calculating the percentage difference (spread). This process is repeated for all 12 trading pairs added in the settings. The script works only with the assets and exchanges available on TradingView.

⚡️ How to use it?

When the spread is negative, it means the asset's price on the first exchange is lower than on the second. By buying on the first exchange and selling on the second, you can make a profit (taking into account the exchange fees). When the spread is positive, the opposite is true. The buy prices and exchanges are shown in a green Buy row, while sell prices and exchanges are displayed in a red Sell row. If the spread is zero, prices are the same on both exchanges, and no arbitrage opportunity exists. For better accuracy, use the smallest timeframe available in your TradingView subscription, such as minute or second intervals.

🕒 Arbitrage Situation Counter

For each trading pair, the table below the Buy row shows the number of arbitrage situations within a specified timeframe. An arbitrage situation occurs when the spread exceeds the Signal Threshold Level set by the user. Each time this happens, the counter increases by one. It only counts situations that occurred within the selected timeframe, such as the past hour for a 1-hour period. You can track arbitrage situations for up to three different periods simultaneously, ranging from 5 minutes to 24 hours. This counter helps evaluate the potential for arbitrage in the selected trading pairs. If a pair shows only 1-2 arbitrage situations per hour, it might be better to look for another pair.

🔔 Setting Up Alerts

In the script settings, you can set the Spread Signal Threshold. When the spread reaches this level, the table for that asset will be highlighted. This threshold also acts as a signal for setting up alerts. To set alerts, go to the Alerts tab in the TradingView menu on the right, click "Create Alert", and select this indicator under "Condition". You can then name the alert and finish the setup by clicking "Create".

We, the authors, have long been involved in cryptocurrency arbitrage and created this script for our own trading, but you can use it for any assets and markets as you see fit.

We also offer lighter versions of the indicator that track the spread for one or three trading pairs. These versions also display the spread chart, which can be useful for historical analysis. If the full indicator is too resource-intensive for your device, try these lighter versions:

🧩 Arbitrage Spread v1 : 1 pair + 1 chart

🧩 Arbitrage Spread v2 : 3 pairs + 3 charts

If your hardware can handle it, you can use the 12-pair version as a dashboard and add one of the versions with a spread chart for a detailed view of one or three pairs.

--

Этот индикатор позволяет в реальном времени отслеживать изменение спреда (разницы в цене) между двумя активами для 12 торговых пар одновременно.

⚙️ Как работает индикатор?

В меню настроек индикатора пользователь выбирает две торговые пары, например BTCUSDT на бирже Binance и BTCUSDT на бирже Bybit. Скрипт получает цены с обеих бирж и сравнивает их, рассчитывая процентное отклонение (спред). Этот процесс выполняется для всех 12 торговых пар, указанных в настройках. Скрипт работает только с теми активами и биржами, которые доступны на TradingView.

⚡️ Как использовать?

Когда спред отрицательный, это означает, что цена на первый актив ниже, чем на второй. В таком случае можно купить актив на первой бирже и продать на второй, получив прибыль (не забывая учитывать биржевые комиссии). Когда спред положительный, ситуация обратная. Биржи и цены для покупки отображаются в зеленой строке Buy, а для продажи – в красной строке Sell. При нулевом спреде цены на обеих биржах одинаковы, и арбитражная ситуация отсутствует.

Для повышения точности индикатора используйте минимально доступный таймфрейм на TradingView – минутный или секундный.

🕒 Счетчик арбитражных ситуаций

По каждой торговой паре в таблице под строкой Buy отображается количество арбитражных ситуаций за определенный промежуток времени. Арбитражная ситуация возникает, когда спред превышает установленный пользователем сигнальный уровень (Signal Threshold Level). При каждом превышении этого уровня счетчик увеличивается на единицу. Счетчик учитывает арбитражные ситуации за определенный период, например, за последний час для 1-часового периода (1h). Можно отслеживать количество арбитражных ситуаций одновременно для трех временных периодов от 5 минут до суток.

Счетчик помогает оценить перспективность арбитража выбранных пар. Если за час на паре было всего 1-2 арбитражные ситуации, возможно, лучше поискать другую пару.

🔔 Настройка оповещений

В настройках скрипта можно задать пороговое значение спреда (Spread Signal Threshold). Когда спред достигнет этого уровня, таблица для данного актива будет подсвечена. Этот уровень также служит сигналом для настройки оповещений.

Для настройки оповещений откройте вкладку «Оповещения» в меню TradingView справа. Нажмите кнопку «Создать оповещение». В открывшемся окне в строке «Условие» выберите данный индикатор. Затем задайте название и завершите настройку, нажав кнопку «Создать».

Мы, авторы этого скрипта, давно занимаемся арбитражем криптовалют и создали его для себя, но вы можете использовать его для любых активов и на любых рынках по своему усмотрению.

У нас также есть более простая версия индикатора, которая отслеживает спред для одной или трех торговых пар. В этих версиях можно просматривать график самого спреда, что полезно для оценки его динамики. Если этот индикатор кажется вам или вашему устройству слишком тяжелым, вы можете воспользоваться облегченными версиями:

🧩 Arbitrage Spread v1 : 1 пара + 1 график

🧩 Arbitrage Spread v2 : 3 пары + 3 графика

Если ваше оборудование позволяет, вы можете добавить несколько индикаторов на экран. Например, использовать версию с 12 парами как дашборд, а одну из версий с графиком спреда для более детального анализа по одному или трем инструментам.

Portfolio Index Generator [By MUQWISHI]▋ INTRODUCTION:

The “Portfolio Index Generator” simplifies the process of building a custom portfolio management index, allowing investors to input a list of preferred holdings from global securities and customize the initial investment weight of each security. Furthermore, it includes an option for rebalancing by adjusting the weights of assets to maintain a desired level of asset allocation. The tool serves as a comprehensive approach for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investment. The output includes an index value, a table of holdings, and chart plotting, providing a deeper understanding of the portfolio's historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom portfolio index. I created this index and named it “My Portfolio Performance”, which comprises several global companies and crypto assets.

_______________________

▋ OUTPUTS:

The output can be divided into 4 sections:

1. Portfolio Index Title (Name & Value).

2. Portfolio Specifications.

3. Portfolio Holdings.

4. Portfolio Index Chart.

1. Portfolio Index Title, displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Portfolio Specifications, displays the essential information on portfolio performance, including the investment date range, initial capital, returns, assets, and equity.

3. Portfolio Holdings, a list of the holding securities inside a table that contains the ticker, average entry price, last price, return percentage of the portfolio's initial capital, and customized weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Index Chart, display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Style Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Equity or Return (%)}, and the plot type for the index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any indicator’s components.

Section(2): Performance Settings

(1) Calculation window period: from DateTime to DateTime.

(2) Initial Capital and specifying currency.

(3) Option to enable portfolio rebalancing in {Monthly, Quarterly, or Yearly} intervals.

Section(3): Portfolio Holdings

(1) Enable and count security in the investment portfolio.

(2) Initial weight of security. For example, if the initial capital is $100,000 and the weight of XYZ stock is 4%, the initial value of the shares would be $4,000.

(3) Select and add up to 30 symbols that interested in.

Please let me know if you have any questions.

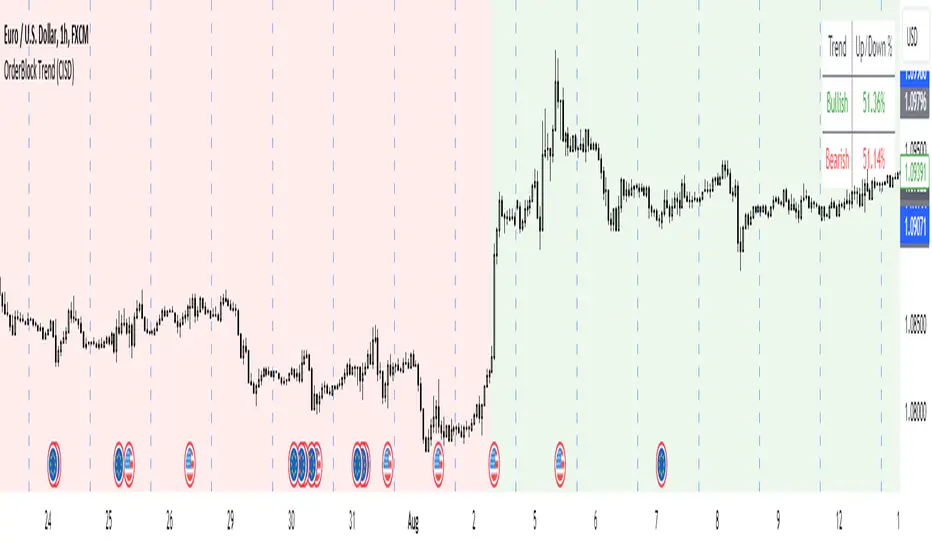

OrderBlock Trend (CISD)OrderBlock Trend (CISD) Indicator

Overview:

The "OrderBlock Trend (CISD)" AKA: change in state of delivery by ICT inner circle trader this indicator is designed to help traders identify and visualize market trends based on higher timeframe candle behavior. This script leverages the concept of order blocks, which are price levels where significant buying or selling activity has occurred, to signal potential trend reversals or continuations. By analyzing bullish and bearish order blocks on a higher timeframe, the indicator provides visual cues and statistical insights into the market's current trend dynamics.

Key Features:

Higher Timeframe Analysis: The indicator uses a higher timeframe (e.g., Daily) to assess the trend direction based on the open and close prices of candles. This approach helps in identifying more significant and reliable trend changes, filtering out noise from lower timeframes.

Bullish and Bearish Order Blocks: The script detects the first bullish or bearish candle on the selected higher timeframe and uses these candles as reference points (order blocks) to determine the trend direction. A bullish trend is indicated when the current price is above the last bearish order block's open price, and a bearish trend is indicated when the price is below the last bullish order block's open price.

Visual Trend Indication: The indicator visually represents the trend using background colors and plot shapes:

A green background and a square shape above the bars indicate a bullish trend.

A red background and a square shape above the bars indicate a bearish trend.

Candle Count and Statistics: The script keeps track of the number of up and down candles during bullish and bearish trends, providing percentages of up and down candles in each trend. This data is displayed in a table, giving traders a quick overview of market sentiment during each trend phase.

User Customization: The higher timeframe can be adjusted according to the trader's preference, allowing flexibility in trend analysis based on different time horizons.

Concepts and Calculations:

The "OrderBlock Trend (CISD)" indicator is based on the concept of order blocks, a key area where institutional traders are believed to place large orders, creating significant support or resistance levels. By identifying these blocks on a higher timeframe, the indicator aims to highlight potential trend reversals or continuations. The use of higher timeframe data helps filter out minor fluctuations and focus on more meaningful price movements.

The candle count and percentage calculations provide additional context, allowing traders to understand the proportion of bullish or bearish candles within each trend. This information can be useful for assessing the strength and consistency of a trend.

How to Use:

Select the Higher Timeframe: Choose the higher timeframe (e.g., Daily) that best suits your trading strategy. The default setting is "D" (Daily), but it can be adjusted to other timeframes as needed.

Interpret the Trend Signals:

A green background indicates a bullish trend, while a red background indicates a bearish trend. The corresponding square shapes above the bars reinforce these signals.

Use the information on the proportion of up and down candles during each trend to gauge the trend's strength and consistency.

Trading Decisions: The indicator can be used in conjunction with other technical analysis tools and indicators to make informed trading decisions. It is particularly useful for identifying trend reversals and potential entry or exit points based on the behavior of higher timeframe order blocks.

Customization and Optimization: Experiment with different higher timeframes and settings to optimize the indicator for your specific trading style and preferences.

Conclusion:

The "OrderBlock Trend (CISD)" indicator offers a comprehensive approach to trend analysis, combining the power of higher timeframe order blocks with clear visual cues and statistical insights. By understanding the underlying concepts and utilizing the provided features, traders can enhance their trend detection and decision-making processes in the markets.

Disclaimer:

This indicator is intended for educational purposes and should be used in conjunction with other analysis methods. Always perform your own research and risk management before making trading decisions.

Some known bugs when you switch to lower timeframe while using daily timeframe data it didn't use the daily candle close to establish the trend change but your current time frame If some of you know how to fix it that would be great if you help me to I would try my best to fix this in the future :) credit to ChatGPT 4o

Auto Fib GOLDEN TARGET Golden Target Auto Fib Indicator

Unlock the power of automatic Fibonacci analysis with the Golden Target Auto Fib Indicator. Designed for traders who want to effortlessly incorporate Fibonacci retracement levels into their strategy, this indicator dynamically calculates and plots key Fibonacci levels based on recent price action.

Key Features:

Automatic Fibonacci Levels: Automatically determines the critical Fibonacci retracement levels using the most recent high and low over a user-defined period.

Customizable Length: Adjust the period over which the Fibonacci levels are calculated to match your trading style and market conditions.

Dynamic Plotting: Fibonacci levels are plotted in real-time, reflecting current market conditions and potential support and resistance areas.

Color-Coded Levels: Distinguishes between different Fibonacci levels with distinct colors, making it easy to identify significant price points at a glance.

Target Labels (Optional): Optionally display labels next to the Fibonacci levels to help identify potential target zones and better visualize the key levels.

How It Works:

The Golden Target Auto Fib Indicator calculates Fibonacci retracement levels based on the highest high and lowest low over a specified length. The levels plotted include key Fibonacci ratios: 23.6%, 38.2%, 61.8%, and the 100% extension, providing valuable insights into potential support and resistance areas as well as price targets.

Usage:

Adjust Settings: Set the Length parameter to define the period over which Fibonacci levels are calculated.

Analyze Levels: Observe the plotted Fibonacci levels and their color-coded lines to identify potential price retracement zones and target areas.

Incorporate Into Strategy: Use these levels in conjunction with your trading strategy to make more informed decisions on entry and exit points.

Whether you're a day trader or a swing trader, the Golden Target Auto Fib Indicator simplifies Fibonacci analysis and integrates seamlessly into your TradingView charts, helping you make more precise trading decisions.

Get started today and enhance your technical analysis with the Golden Target Auto Fib Indicator!

Feel free to adjust the description according to the specific features or customization options of your indicator.

1000SATS and ORDI Market Cap RatioSure! Here is a detailed description and usage guide for your TradingView indicator:

### Indicator Description

**Title**: 1000SATS/ORDI Market Cap Ratio

**Description**: The "1000SATS/ORDI Market Cap Ratio" indicator calculates and visualizes the market capitalization ratio between 1000SATS and ORDI. This indicator allows traders and investors to analyze the relative market strength and valuation trends of 1000SATS compared to ORDI over time. By tracking this ratio, users can gain insights into market dynamics and potential trading opportunities between these two assets.

### Indicator Usage

**Purpose**:

- To compare the market capitalizations of 1000SATS and ORDI.

- To identify potential undervaluation or overvaluation of 1000SATS relative to ORDI.

- To assist in making informed trading and investment decisions based on market cap trends.

**How to Use**:

1. **Add the Indicator to Your Chart**:

- Open TradingView and navigate to your chart.

- Click on the "Indicators" button at the top of the chart.

- Select "Pine Editor" and paste the provided script.

- Click "Add to Chart" to apply the indicator.

2. **Interpret the Ratio**:

- The indicator will plot a line representing the ratio of the market capitalization of 1000SATS to ORDI.

- A rising ratio indicates that the market cap of 1000SATS is increasing relative to ORDI, suggesting stronger market performance or higher valuation of 1000SATS.

- A falling ratio indicates that the market cap of 1000SATS is decreasing relative to ORDI, suggesting weaker market performance or lower valuation of 1000SATS.

3. **Analyze Trends**:

- Use the indicator to spot trends and potential reversal points in the market cap ratio.

- Combine the ratio analysis with other technical indicators and chart patterns to enhance your trading strategy.

4. **Set Alerts**:

- Set custom alerts on the ratio to notify you of significant changes or specific thresholds being reached, enabling timely decision-making.

**Example**:

- If the ratio is consistently rising, it may indicate a good opportunity to consider 1000SATS as a stronger investment relative to ORDI.

- Conversely, if the ratio is falling, it may be a signal to reevaluate the strength of 1000SATS compared to ORDI.

**Note**: Always conduct thorough analysis and consider other market factors before making trading decisions based on this indicator.

### Script

```pinescript

//@version=4

study("1000SATS and ORDI Market Cap Ratio", shorttitle="1000SATS/ORDI Ratio", overlay=true)

// Define the circulating supply for ORDI and 1000SATS

ORDI_supply = 21000000 // Circulating supply of ORDI

SATS_1000_supply = 2100000000000 // Circulating supply of 1000SATS

// Fetch the price data for ORDI

ordi_price = security("BINANCE:ORDIUSDT", timeframe.period, close)

// Fetch the price data for 1000SATS

sats_1000_price = security("BINANCE:1000SATSUSDT", timeframe.period, close)

// Calculate the market capitalizations

ordi_market_cap = ordi_price * ORDI_supply

sats_1000_market_cap = sats_1000_price * SATS_1000_supply

// Calculate the market cap ratio

ratio = sats_1000_market_cap / ordi_market_cap

// Plot the ratio

plot(ratio, title="1000SATS/ORDI Market Cap Ratio", color=color.blue, linewidth=2)

```

This description and usage guide should help users understand the purpose and functionality of your indicator, as well as how to effectively apply it in their trading activities on TradingView.

MultiTFlevels with Volume Display1. Overview

This indicator is intended for use on trading platforms like TradingView and provides the following features:

Volume Profile Analysis:

Shows cumulative volume delta (CVD) and displays buying and selling volumes.

Historical OHLC Levels:

Plots historical open, high, low, and close levels for various timeframes (e.g., daily, weekly, monthly).

Customizable Settings:

Allows users to toggle different elements and customize display options.

2. Inputs

Timeframe Display Toggles:

Users can choose to display OHLC levels from different timeframes such as previous month, week, day, 4H, 1H, 30M, 15M, and 5M.

CVD Display Toggle: Option to show or hide the Cumulative Volume Delta (CVD).

Line and Label Customization:

leftOffset and rightOffset: Define how far lines are extended left and right from the current bar.

colorMonth, colorWeek, etc.: Customize colors for different timeframe OHLC levels.

labelOffset and rightOffset: Control the positioning of volume labels.

3. Key Features

Cumulative Volume Delta (CVD)

Calculation:

Computes the cumulative volume delta by adding or subtracting the volume based on whether the close price is higher or lower than the open price.

Display:

Shows a label on the chart indicating the current CVD value and whether the market is leaning towards buying or selling.

Historical OHLC Levels

Data Retrieval:

Uses the request.security function to fetch OHLC data from different timeframes (e.g., monthly, weekly, daily).

Plotting:

Draws lines and labels on the chart to represent open, high, low, and close levels for each selected timeframe.

Buying and Selling Volumes

Calculation:

Calculates buying and selling volumes based on whether the close price is higher or lower than the open price.

Display:

Shows labels on the chart for buying and selling volumes.

4. Functions

getOHLC(timeframe)

Retrieves open, high, low, and close values from the specified timeframe.

plotOHLC(show, open, high, low, close, col, prefix)

Draws OHLC lines and labels on the chart for the given timeframe and color.

5. Usage

Chart Overlay: The indicator is overlaid on the main chart (i.e., it appears directly on the price chart).

Historical Analysis:

Useful for analyzing historical price levels and volume dynamics across different timeframes.

Volume Insights:

Helps traders understand the cumulative volume behavior and market sentiment through the CVD and volume labels.

In essence, this indicator provides a comprehensive view of historical price levels across multiple timeframes and the dynamics of market volume through CVD and volume labels. It can be particularly useful for traders looking to combine price action with volume analysis for a more in-depth market assessment.

Important Levels by Sandun Kolambage

### Pine Script Indicator: Important Levels by Sandun Kolambage

#### Description

Introducing our new pivot point and high/low indicator for TradingView! This indicator is designed to help traders identify key levels of support and resistance across different timeframes, from daily to yearly. By analyzing historical data and market trends, our indicator displays the most important pivot points and high/low levels, giving you a better understanding of market dynamics and potential trading opportunities.

Whether you're a day trader, swing trader, or long-term investor, our indicator can help you optimize your trading strategy and achieve your financial goals. Install our indicator on TradingView today and start taking advantage of these important levels!

#### Key Features

- **Daily, Weekly, Monthly, and Yearly Levels:** Automatically plots the open, high, low, and close prices for different timeframes to help traders identify significant levels.

- **Pivot Points:** Calculates and displays pivot points for weekly, monthly, and yearly timeframes, providing additional support and resistance levels.

- **Customizable Line Styles:** Offers options to customize the appearance of the lines (solid, dashed, or dotted) for better visualization.

- **Conditional Coloring:** Uses color coding to highlight the relationship between different timeframe closes, making it easy to spot important levels.

#### How It Works

1. **Daily, Weekly, Monthly, and Yearly Levels:**

- The indicator uses `request.security` to fetch and display open, high, low, and close prices for daily, weekly, monthly, and yearly timeframes.

- Lines are plotted at these key levels with colors indicating their relationship to closes of other timeframes.

2. **Pivot Points:**

- Pivot points are calculated using the formula \((High + Low + Close) / 3\).

- These pivot points are plotted on the chart and labeled clearly to indicate potential support and resistance areas.

3. **Customizable Line Styles:**

- Users can select from solid, dashed, or dotted lines to represent the key levels and pivot points for better clarity and personal preference.

4. **Conditional Coloring:**

- The indicator applies conditional coloring to the lines based on the comparison of current close prices across different timeframes. Yellow indicates lower closes, and red indicates higher closes, making it easy to identify important price levels quickly.

#### Usage Instructions

1. **Enable Key Levels:**

- Toggle the "Daily Weekly Monthly High/Low" option to display or hide the respective levels.

- Select your preferred line style (solid, dashed, dotted) for better visibility.

2. **Display Pivot Points:**

- Toggle the "Pivot" option to show or hide the weekly, monthly, and yearly pivot points on the chart.

3. **Interpret Color Coding:**

- Yellow lines indicate levels where the close price is lower compared to a specific timeframe close.

- Red lines indicate levels where the close price is higher compared to a specific timeframe close.

- Specific colors for yearly levels and pivots are used to distinguish them clearly on the chart.

By following these guidelines, traders can effectively use this indicator to identify critical price levels and make informed trading decisions.

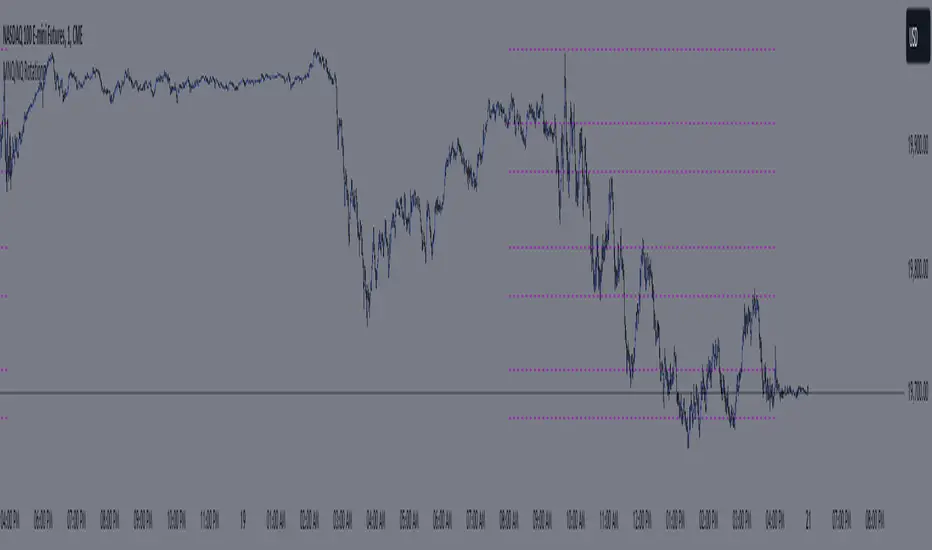

MNQ/NQ Rotations [Tiestobob]### Indicator Description: MNQ/NQ Rotations

TO BE USED ONLY ON THE CONTINOUS CONTRACTS NQ1! and MNQ1! It will not work on others or the forward contracts of these.

#### Overview

The MNQ/NQ Rotations indicator is designed for traders of Nasdaq futures (MNQ and NQ) to visualize key price levels where typical market rotations occur. This indicator identifies and highlights the xxx.20 and xxx.80 levels based on empirical data and trading experience, allowing traders to recognize potential support and resistance points during trading sessions.

#### Key Features

- **Timeframe Selection**: The indicator allows users to specify a timeframe for identifying breakout candles, ensuring flexibility across different trading strategies.

- **Active Trading Range**: Users can define an active trading range, focusing the analysis on specific hours when the market is most active.

- **Visual Representation**: The indicator paints horizontal lines at key price levels (xxx.20 and xxx.80), extending them across a user-defined length to aid in visual analysis.

- **Customization**: Users can customize the color of the lines to match their charting preferences.

#### Inputs

- **Timeframe (`tf`)**: Defines the timeframe to select the breakout candle (default: 1 minute).

- **Active Trading Range (`session`)**: Specifies the time range for identifying breakout candles (default: 08:00-12:00).

- **Line Color (`line_color`)**: Allows customization of the line color (default: purple).

#### Logic

1. **Session Validation**: The indicator checks if the current bar falls within the specified active trading range.

2. **Price Point Calculation**: For each candle close, the indicator calculates the nearest xxx.20 and xxx.80 levels.

3. **Line Drawing**: Horizontal lines are drawn at these key levels, extending a specified length forward to highlight potential rotation points.

#### Use Cases

- **Support and Resistance Identification**: By highlighting the xxx.20 and xxx.80 levels, traders can easily spot areas where the market is likely to reverse or consolidate.

- **Breakout Trading**: Traders can use the indicator to identify breakout levels and set appropriate entry points.

- **Risk Management**: The visual cues provided by the indicator can help traders set more effective stop-loss and take-profit levels.

#### Example

A trader using a 1-minute timeframe with an active trading range from 08:00 to 12:00 will see horizontal lines painted at the nearest xxx.20 and xxx.80 levels for each candle close during this period. These lines serve as visual markers for typical rotation points, aiding in decision-making and trade planning.

#### Conclusion

The MNQ/NQ Rotations indicator is a powerful tool for traders looking to enhance their market analysis of Nasdaq futures. By focusing on empirically derived rotation levels, this indicator provides clear visual cues for identifying key price levels, supporting more informed trading decisions.

HTF TriangleHTF Triangle by ZeroHeroTrading aims at detecting ascending and descending triangles using higher time frame data, without repainting nor misalignment issues.

It addresses user requests for combining Ascending Triangle and Descending Triangle into one indicator.

Ascending triangles are defined by an horizontal upper trend line and a rising lower trend line. It is a chart pattern used in technical analysis to predict the continuation of an uptrend.

Descending triangles are defined by a falling upper trend line and an horizontal lower trend line. It is a chart pattern used in technical analysis to predict the continuation of a downtrend.

This indicator can be useful if you, like me, believe that higher time frames can offer a broader perspective and provide clearer signals, smoothing out market noise and showing longer-term trends.

You can change the indicator settings as you see fit to tighten or loosen the detection, and achieve the best results for your use case.

Features

It draws the detected ascending and descending triangles on the chart.

It supports alerting when a detection occurs.

It allows for selecting ascending and/or descending triangle detection.

It allows for setting the higher time frame to run the detection on.

It allows for setting the minimum number of consecutive valid higher time frame bars to fit the pattern criteria.

It allows for setting a high/low factor detection criteria to apply on higher time frame bars high/low as a proportion of the distance between the reference bar high/low and open/close.

It allows for turning on an adjustment of the triangle using highest/lowest values within valid higher time frame bars.

Settings

Ascending checkbox: Turns on/off ascending triangle detection. Default is on.

Descending checkbox: Turns on/off descending triangle detection. Default is on.

Higher Time Frame dropdown: Selects higher time frame to run the detection on. It must be higher than, and a multiple of, the chart's timeframe. Default is 5 minutes.

Valid Bars Minimum field: Sets minimum number of consecutive valid higher time frame bars to fit the pattern criteria. Default is 3. Minimum is 1.

High/Low Factor checkbox: Turns on/off high/low factor detection criteria. Default is on.

High/Low Factor field: Sets high/low factor to apply on higher time frame bars high/low as a proportion of the distance between the reference bar high/low and open/close. Default is 0. Minimum is 0. Maximum is 1.

Adjust Triangle checkbox: Turns on/off triangle adjustment using highest/lowest values within valid higher time frame bars. Default is on.

Detection Algorithm Notes

The detection algorithm recursively selects a higher time frame bar as reference. Then it looks at the consecutive higher time frame bars (as per the requested number of minimum valid bars) as follows:

Ascending Triangle

Low must be higher than previous bar.

Open/close max value must be lower than (or equal to) reference bar high.

When high/low factor criteria is turned on, high must be higher than (or equal to) reference bar open/close max value plus high/low factor proportion of the distance between reference bar high and open/close max value.

Descending Triangle

High must be lower than previous bar.

Open/close min value must be higher than (or equal to) reference bar low.

When high/low factor criteria is turned on, low must be lower than (or equal to) reference bar open/close min value minus high/low factor proportion of the distance between reference bar low and open/close min value.

VWAP with RSIVWAP with RSI Indicator

Overview

The VWAP with RSI Indicator is a powerful tool that combines the Volume Weighted Average Price (VWAP) with the Relative Strength Index (RSI) to provide traders with comprehensive insights into price trends, volume-weighted price levels, and market momentum. This dual-indicator setup enhances your trading strategy by offering a clearer understanding of the market conditions, potential entry and exit points, and trend reversals.

Key Features

VWAP (Volume Weighted Average Price):

Calculation: The VWAP is calculated using the high, low, and close prices, weighted by trading volume over a specified period.

Purpose: VWAP provides an average price that reflects the trading volume at different price levels, helping traders identify the true average price over a given period.

Visualization: The VWAP line is plotted in blue on the price chart, indicating the volume-weighted average price.

RSI (Relative Strength Index):

Calculation: RSI is based on the average gains and losses over a specified period (default is 14 periods) and ranges from 0 to 100.

Purpose: RSI measures the speed and change of price movements, identifying overbought or oversold conditions in the market.

Overbought/Oversold Levels:

Overbought: RSI above 70 (red line).

Oversold: RSI below 30 (green line).

Midline: RSI at 50 (gray dashed line).

Visualization: The RSI line changes color based on its value (purple for normal, red for overbought, green for oversold) and is plotted below the price chart.

Background Fill for RSI:

Overbought Area: Shaded red when RSI is above 70.

Oversold Area: Shaded green when RSI is below 30.

Bullish and Bearish Divergence Detection:

Bullish Divergence: Occurs when price forms a lower low, but RSI forms a higher low, indicating potential upward reversal.

Visualization: Bullish divergence points are marked with a green line and labeled "Bull."

Bearish Divergence: Occurs when price forms a higher high, but RSI forms a lower high, indicating potential downward reversal.

Visualization: Bearish divergence points are marked with a red line and labeled "Bear."

Alerts: Conditions for bullish and bearish divergences trigger alerts.

Settings

VWAP Settings:

hideonDWM: Option to hide VWAP on daily or higher timeframes.

src: Source for VWAP calculation (default is hlc3 - (high + low + close)/3).

offset: Offset for plotting the VWAP.

RSI Settings:

rsiLengthInput: Period length for RSI calculation (default is 14).

rsiSourceInput: Source for RSI calculation (default is close price).

maTypeInput: Type of moving average applied to RSI (options: SMA, EMA).

maLengthInput: Length of the moving average applied to RSI.

How to Use

Trend Identification: Use VWAP to identify the average price level and market trend. If the price is above VWAP, it suggests an uptrend, and if below, it suggests a downtrend.

Overbought/Oversold Conditions: Use RSI to identify potential reversal points. RSI above 70 indicates overbought conditions, and below 30 indicates oversold conditions.

Divergence: Look for bullish or bearish divergences between price and RSI to anticipate potential trend reversals.

Conclusion

By combining VWAP and RSI, this indicator provides a robust framework for analyzing market conditions, identifying trends, and making more informed trading decisions. Enhance your trading strategy today with the VWAP with RSI Indicator!

Global Market Cap of all measuable assets# Comprehensive Global Market Cap Overview

This indicator provides a dynamic, real-time estimate of the total global market value across multiple asset classes and economic sectors. It aims to give traders and analysts a broad perspective on the state of global markets and wealth.

## Features:

- Real-time data for major market segments including stocks, bonds, real estate, cryptocurrencies, and commodities

- Estimates for hard-to-quantify sectors like derivatives, private equity, and OTC markets

- Includes often-overlooked categories such as cash deposits, insurance markets, and natural resources

- Static estimates for art/collectibles and intellectual property

- Total global value calculation and breakdown by category

- Easy-to-read table display of all categories

## Categories Tracked:

1. Global Stock Market

2. Global Bond Market

3. Real Estate

4. Cryptocurrencies

5. Commodities

6. Derivatives Market

7. Private Equity and Venture Capital

8. Cash and Bank Deposits

9. Insurance Markets

10. Sovereign Wealth Funds

11. OTC Markets

12. Natural Resources

13. Art and Collectibles

14. Intellectual Property

## Data Sources:

- Uses popular ETFs and indices as proxies for global markets where possible

- Incorporates data from specific company stocks to represent certain markets (e.g., CME for derivatives, OTCM for OTC markets)

- Utilizes FRED data for bank deposits

- Includes static estimates for categories without reliable real-time data sources

## Notes:

- All values are approximate and should be used for general perspective rather than precise financial analysis

- Some categories use scaled proxy data, which may not perfectly represent global totals

- Static estimates are used where real-time data is unavailable and should be updated periodically

- The total global value includes human capital but this is not displayed in the table due to its speculative nature

This indicator is designed to provide a comprehensive overview of global market value, going beyond traditional market capitalization metrics. It's ideal for traders, researchers, and anyone interested in gaining a broader understanding of global wealth distribution across various sectors.

Please note that due to the complexity of global markets and limitations in data availability, all figures should be considered estimates and used as part of a broader analysis rather than as definitive values.

CofG Oscillator w/ Added Normalizations/TransformationsThis indicator is a unique study in normalization/transformation techniques, which are applied to the CG (center of gravity) Oscillator, a popular oscillator made by John Ehlers.

The idea to transform the data from this oscillator originated from observing the original indicator, which exhibited numerous whips. Curious about the potential outcomes, I began experimenting with various normalization/transformation methods and discovered a plethora of interesting results.

The indicator offers 10 different types of normalization/transformation, each with its own set of benefits and drawbacks. My personal favorites are the Quantile Transformation , which converts the dataset into one that is mostly normally distributed, and the Z-Score , which I have found tends to provide better signaling than the original indicator.

I've also included the option of showing the mean, median, and mode of the data over the period specified by the transformation period. Using this will allow you to gather additional insights into how these transformations effect the distribution of the data series.

I've also included some notes on what each transformation does, how it is useful, where it fails, and what I've found to be the best inputs for it (though I'd encourage you to play around with it yourself).

Types of Normalization/Transformation:

1. Z-Score

Overview: Standardizes the data by subtracting the mean and dividing by the standard deviation.

Benefits: Centers the data around 0 with a standard deviation of 1, reducing the impact of outliers.

Disadvantages: Works best on data that is normally distributed

Notes: Best used with a mid-longer transformation period.

2. Min-Max

Overview: Scales the data to fit within a specified range, typically 0 to 1.

Benefits: Simple and fast to compute, preserves the relationships among data points.

Disadvantages: Sensitive to outliers, which can skew the normalization.

Notes: Best used with mid-longer transformation period.

3. Decimal Scaling

Overview: Normalizes data by moving the decimal point of values.

Benefits: Simple and straightforward, useful for data with varying scales.

Disadvantages: Not commonly used, less intuitive, less advantageous.

Notes: Best used with a mid-longer transformation period.

4. Mean Normalization

Overview: Subtracts the mean and divides by the range (max - min).

Benefits: Centers data around 0, making it easier to compare different datasets.

Disadvantages: Can be affected by outliers, which influence the range.

Notes: Best used with a mid-longer transformation period.

5. Log Transformation

Overview: Applies the logarithm function to compress the data range.

Benefits: Reduces skewness, making the data more normally distributed.

Disadvantages: Only applicable to positive data, breaks on zero and negative values.

Notes: Works with varied transformation period.

6. Max Abs Scaler

Overview: Scales each feature by its maximum absolute value.

Benefits: Retains sparsity and is robust to large outliers.

Disadvantages: Only shifts data to the range , which might not always be desirable.

Notes: Best used with a mid-longer transformation period.

7. Robust Scaler

Overview: Uses the median and the interquartile range for scaling.

Benefits: Robust to outliers, does not shift data as much as other methods.

Disadvantages: May not perform well with small datasets.

Notes: Best used with a longer transformation period.

8. Feature Scaling to Unit Norm

Overview: Scales data such that the norm (magnitude) of each feature is 1.

Benefits: Useful for models that rely on the magnitude of feature vectors.

Disadvantages: Sensitive to outliers, which can disproportionately affect the norm. Not normally used in this context, though it provides some interesting transformations.

Notes: Best used with a shorter transformation period.

9. Logistic Function

Overview: Applies the logistic function to squash data into the range .

Benefits: Smoothly compresses extreme values, handling skewed distributions well.

Disadvantages: May not preserve the relative distances between data points as effectively.

Notes: Best used with a shorter transformation period. This feature is actually two layered, we first put it through the mean normalization to ensure that it's generally centered around 0.

10. Quantile Transformation

Overview: Maps data to a uniform or normal distribution using quantiles.

Benefits: Makes data follow a specified distribution, useful for non-linear scaling.

Disadvantages: Can distort relationships between features, computationally expensive.

Notes: Best used with a very long transformation period.

Conclusion

Feel free to explore these normalization/transformation techniques to see how they impact the performance of the CG Oscillator. Each method offers unique insights and benefits, making this study a valuable tool for traders, especially those with a passion for data analysis.

9:30 Opening Price MarkerIndicator Name: 9:30 Opening Price Marker

Description:

The "9:30 Opening Price Marker" is a custom indicator for TradingView that highlights the opening price at 9:30 AM in the UTC-4 time zone (Eastern Daylight Time) on the chart. It helps traders and analysts easily identify and track the price level at which the market opens each day.

Features:

Timezone Conversion: The indicator converts the current time to the UTC-4 timezone (Eastern Daylight Time) to accurately determine the 9:30 AM opening price.

Visual Marker: It visually marks the opening price with a dotted line on the chart, making it prominent for quick reference.

Label: Additionally, it includes a label next to the opening price line, indicating "9:30 Opening Price", enhancing clarity and usability.

Overlay: The indicator is designed to overlay on the price chart, ensuring it doesn't clutter other technical analysis tools or indicators.

Usage:

Day-to-Day Analysis: Traders can use this indicator to quickly gauge market sentiment at the daily opening, which can influence intraday trading strategies.

Reference Point: Acts as a reference point for identifying price movements and potential trading opportunities relative to the day's opening price.

Time-Specific Insights: Provides insights into price action immediately following the market open, aiding in decision-making based on early trading activity.

Installation: Copy the provided Pine Script code into TradingView's Pine Editor, save the script as an indicator, and apply it to your chart.

Disclaimer : This indicator is intended for informational purposes only and should not be solely relied upon for trading decisions. Always consider multiple sources of information and perform thorough analysis before executing trades.