Phase CalculationPhase Calculation was authored by John F. Elders in the Stocks and Commodities Magazine 11/1996

This indicator will tell you if the stock is in a uptrend or downtrend. A phase number with a low number means it is in a uptrend and a phase number with a high number means it is in a downtrend.

Let me know if you want to see me write code for different indicators!

Ehler

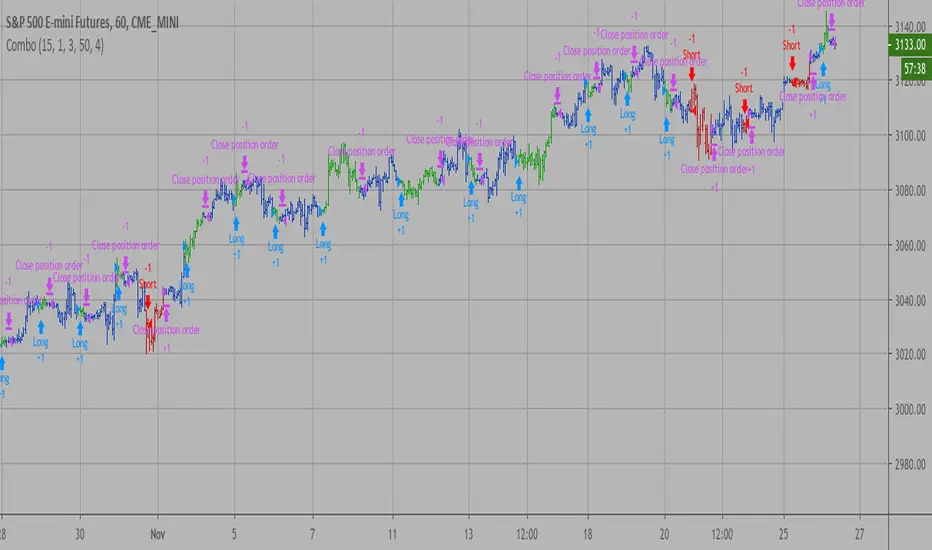

Combo Backtest 123 Reversal & D_ELI (Ehlers Leading Indicator) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Indicator plots a single

Daily DSP (Detrended Synthetic Price) and a Daily ELI (Ehlers Leading

Indicator) using intraday data.

Detrended Synthetic Price is a function that is in phase with the dominant

cycle of real price data. This one is computed by subtracting a 3 pole Butterworth

filter from a 2 Pole Butterworth filter. Ehlers Leading Indicator gives an advanced

indication of a cyclic turning point. It is computed by subtracting the simple

moving average of the detrended synthetic price from the detrended synthetic price.

Buy and Sell signals arise when the ELI indicator crosses over or under the detrended

synthetic price.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & D_ELI (Ehlers Leading Indicator) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Indicator plots a single

Daily DSP (Detrended Synthetic Price) and a Daily ELI (Ehlers Leading

Indicator) using intraday data.

Detrended Synthetic Price is a function that is in phase with the dominant

cycle of real price data. This one is computed by subtracting a 3 pole Butterworth

filter from a 2 Pole Butterworth filter. Ehlers Leading Indicator gives an advanced

indication of a cyclic turning point. It is computed by subtracting the simple

moving average of the detrended synthetic price from the detrended synthetic price.

Buy and Sell signals arise when the ELI indicator crosses over or under the detrended

synthetic price.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Detrended Synthetic Price V 2 This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Detrended Synthetic Price is a function that is in phase with the

dominant cycle of real price data. This DSP is computed by subtracting

a half-cycle exponential moving average (EMA) from the quarter cycle

exponential moving average.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & D_DSP (Detrended Synthetic Price) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Detrended Synthetic Price is a function that is in phase with the

dominant cycle of real price data. This DSP is computed by subtracting

a half-cycle exponential moving average (EMA) from the quarter cycle

exponential moving average.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & D_DSP (Detrended Synthetic Price) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Detrended Synthetic Price is a function that is in phase with the

dominant cycle of real price data. This DSP is computed by subtracting

a half-cycle exponential moving average (EMA) from the quarter cycle

exponential moving average.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

MTF IQ IFM Moving AverageMTF ready adaptive MA using Ehler's IQ IFM ( In Phase - Quadrature Instantaneous Frequency Measurement ).

Ehler's formula is a method of quantitatively measuring the length of a market cycle. In this case it is used to calculate the "optimal" adaptive EMA.

Theoretically the length generated by Ehler's formula could be used in many indicators and it's been placed within it's own function so you should be able to simply copy/paste it. HOWEVER pine will not accept series variables for the length input used in built-in functions. You will have to manually code (or find) a version of your indicator that doesn't use the pine built in.

Options :

type : optionally add volume weighting

range : historical range used in IQ IFM

cycle length mult : method to create faster/slower MAs. eg 0.5 is half the length of a cycle and a faster EMA ie EMA10 vs EMA20

low sat fix : some cryptocurrencies with low satoshi values cause an issue with the calculation, if you get no/nonsensical lines, enable this. Shouldn't affect other instruments, but can be disabled just in case.

MTF options: run the calculation on an alternative timeframe

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

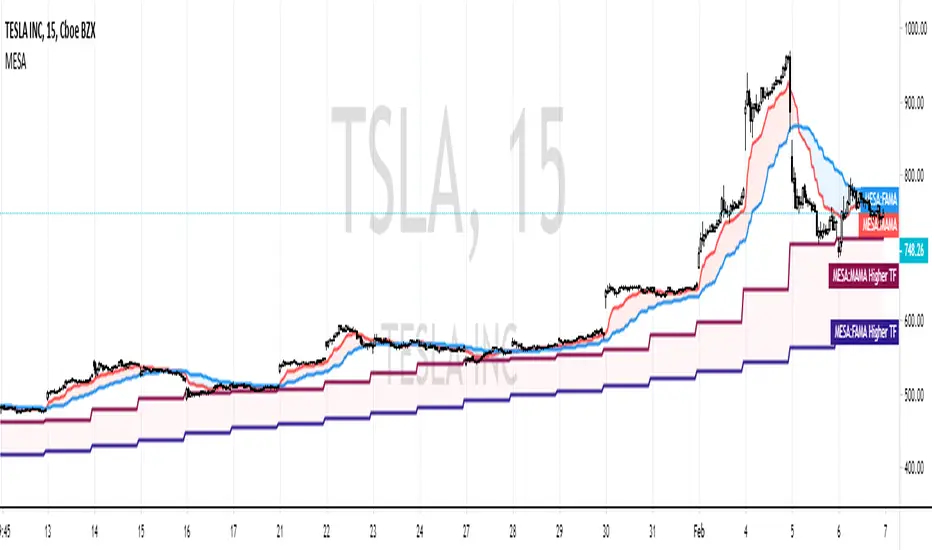

MESA Adaptive Moving AverageIntro

One of Ehlers most well-known indicators! I've seen many variations of this on TradingView, however, none seem to be true to the original released by Ehlers himself.

I've taken it upon myself to simply translate the MAMA into Pinescript, instead of re-writing like some others have done.

You can use it as a very effective & adaptive moving average with other signals or

as a standalone signal.

In the case that you're going to use it for signals and not simple technical trading (non-quantitative),

I've also added a threshold parameter to filter out weak signals.

My MAMA indicator is different from others in very simple ways - I don't use the nz() command, which sets all "Not a Number" values to 0. In others' scripts, you immediately load the indicator with several 0 values,

causing a slight lag in future calculations since this code is recursive (refers to previous values it generated).

In my version, I simply wait until the script has access to all the bar data it needs, instead of instantly performing calculations and

setting erroneous values to 0. In this case, we start with the correct values (or closer to correct).

If you want to compare this indicator the current most popular MAMA by LazyBear, you'll notice it often gives buy and sell crosses one bar earlier than theirs.

Setting Parameters

Source - the data series to perform calculations on. (Initially, Ehlers himself favored hl/2, but conceded that there isn't empirical benefit over close.)

Fast Limit - controls how quickly the MAMA will "ratchet up" fast price action. (Higher values are faster)

Slow Limit - controls how closely the FAMA will follow the MAMA. (Again, higher is faster. You typically want the FAMA to be slower though.)

Crossover Threshold - simple error thresholding to limit the number of weak trade signals. (Lower means lower tolerance)

Show Crosses? - show/hide the arrows at moving average crosses

Adaptive Bandpass Trigger OscillatorThis is based off of Ehler's Bandpass Filter system (link below slides 15-17). I then used Ehler's methods for finding the dominant cycle to automatically input the dominant cycle to the length. Essentially Ehler runs a band pass with a given period to detrend the price data and highlight a cycle with the given frequency(length). This represents the In phase cycle. Ehler then creates the trigger line by taking the one bar momentum of the In Phase line, multiplying by 2Pi and then using this to create a 60 degree leading signal. The triggers are crossovers of the In Phase and Lead lines. You can also use conservative signals by waiting for the In Phase line to trend in the direction of the trigger crossover as well.

Delta represents how much to influence the oscillator by the price (Delta 0 is a perfect wave)

Alpha represents how quickly to adapt between the dominant cycle changes in the price.

Thanks to LazyBear for implementing Ehler's original adaptive code, which I used for this system

Thanks to HPotter for the BandPass Filter code, which I used as a base for implementing the rest of the system

www.mesasoftware.com

Ehler Bandpass Trigger OscillatorThis is based off of Ehler's Bandpass Filter system (link below slides 15-17). Essentially Ehler runs a band pass with a given period to detrend the price data and highlight a cycle with the given frequency(length). This represents the In phase cycle. Ehler then creates the trigger line by taking the one bar momentum of the In Phase line, multiplying by 2Pi and then using this to create a 60 degree leading signal. The triggers are crossovers of the In Phase and Lead lines. You can also use conservative signals by waiting for the In Phase line to trend in the direction of the trigger crossover as well.

Length represent the cycle period you want to highlight.

Delta represents how much to influence the oscillator by the price (Delta 0 is a perfect wave)

Thanks to HPotter for the BandPass Filter code, which I used as a base for implementing the rest of the system

www.mesasoftware.com

Recursive Median Oscillator & Fisher Transforms RibbonThis is a composite indicator made up of:

- modifided (rescaled) version of evergets version of recursive median oscillator.

- 1996anoojpatels Futur modification of Ehlers Fisher Transform Ribbons Indicator

I think Ehlers attempts to minimise latency in indicators are extremely valuable and some of my most use trading tools. Thanks to all the authors whose iterations keep moving these indicators toward perfection. Here is my contribution.

Ehlers FilterThis is the Adaptive Ehlers Filter.

I had to unroll the for loops and array because TV is missing crucial data structures and data conversions (Arrays and series to integer conversion for values).

I'm in the process of releasing some scripts. This is a very old script I had. This contains volatility ranges and can be used as trading signals. You can also see how the EF moves up or down, the direction, when price is sideways, and use price breaks up and down as signals from the line.

Have fun, because I didn't making this script hahaha

NOTE : There is an issue with the script where at certain time frames it positions itself below or above. I think its due to calculations. If anyone knows the fix before I get the chance to take a look at it, please let me know.

books.google.com

Multi OscillatorAn oscillator toolbox. Highly configurable.

Three oscillators can be selected to show the momentum of:

price

flow -> the change in price

volume

money -> (volume * flow)

See the comments at the beginning of the script for a complete description.

--------------------------------

As my interest in oscillators increased, I was baffled by the vast jungle of available options. Over time, I did my best to distill the essence of what each indicator offered: RSI, Stoch RSI, CMF, OBV, MFI, MACD, VPT, Accum/Dist Index, Ehler's roofing...

Standing on the shoulders of giants, this indicator is a humble re-synthesis of all these indicators. The "value add" is in the organization, which facilitates the cohesive processing of different oscillators in one plot.

In this script, an oscillator is composed in stages:

Construct signal -> Remove noise -> Compose Oscillation -> Normalize -> Smooth -> Shape

where each stage is configurable.

There is a lot of flexibility, but once defined, each source (price, flow, volume, money) is constructed in the same way. This facilitates a degree of cohesion that is hard for my brain to render otherwise.

While I find the default settings valuable in my trading, there are so many ways to experiment. Find out what works for you! Share comments of new configurations... as we all learn!

Fisher Transform Ribbons Indicator V1.0Utilizing the Fisher Transform by Ehlers with different lengths based on multipliers will allow you to notice movements in price and understand whether the shift was a correctional wave, or part of the overall trend.

To learn about Fisher Transform , check out the Fisher Transform documentation: www.mesasoftware.com

Fisher has plenty of functionalities. Ribbons provides you with a view of consistency in price action. If all ribbons flip, generally this is a strong signal that the trend is changing. Fisher is extremely punctual (minimum input lag) and robust (doesn't miss movement). Look for everything, including divergences, trends, and Oversold, Overbought points.

Changing length will further provide you more sensitivity in overselling and buying, while numbing chop.

Enjoy!

And for a single Fisher, check out HPotter's Fisher Transform or LazyBear's implementation of the inverse of the Fisher, which has many other interesting properties