TASC 2025.07 Laguerre Filters█ OVERVIEW

This script implements the Laguerre filter and oscillator described by John F. Ehlers in the article "A Tool For Trend Trading, Laguerre Filters" from the July 2025 edition of TASC's Traders' Tips . The new Laguerre filter utilizes the UltimateSmoother filter in place of an exponential moving average (EMA) in its calculation, offering improved responsiveness and reduced lag.

█ CONCEPTS

As Ehlers explains in his article, the Laguerre filter is a form of transversal filter . A transversal filter calculates an output signal using a tapped delay line . It creates multiple delayed versions of an input signal, applies weight to each delay, and then calculates their sum to generate the filtered result.

The Laguerre filter's structure relies on Laguerre polynomials — solutions to a differential equation solved by Edmond Laguerre in the 1800s. When Ehlers analyzed the formula for these polynomials on discrete systems (e.g., financial time series), he found that the first term's expression corresponds to an EMA response, and all subsequent terms correspond to an all-pass response. In contrast to other filter types, an all-pass filter produces phase shift (i.e., delay) in an input signal's components without affecting its amplitude.

Ehlers observed that these characteristics of Laguerre polynomials make them suitable for use in a transversal filter structure, and thus the Laguerre filter was born. However, he notes that EMAs are not great filters in general. As such, to improve on the Laguerre filter's design, Ehlers modified it by replacing the EMA term with his UltimateSmoother filter. The resulting Laguerre filter has significantly reduced lag, achieving a tighter response to market fluctuations while maintaining smoothness. Ehlers suggests that traders can analyze crossings between the UltimateSmoother and this Laguerre filter, or those between two Laguerre filters of different order, for helpful buy and sell signals.

In addition to the Laguerre filter, Ehlers derived a smooth, low-lag oscillator based on the difference between the first and second terms in the modified filter structure, scaled by the root mean square (RMS). The resulting oscillator provides an alternative filtered representation of market data, which can help traders identify swing and mean-reversion signals.

█ USAGE

This indicator calculates both the Laguerre filter and the Laguerre oscillator described in Ehlers' article. It displays the Laguerre filter on the main chart pane and the oscillator in a separate pane.

Users can control the behavior of the filter and oscillator with the inputs in the "Settings/Inputs" tab:

The "Period" input defines the critical period of the UltimateSmoother used in the Laguerre filter and oscillator calculations. Its default value is 30.

The "Gamma" input determines the weighting behavior of the Laguerre filter and oscillator. It accepts a positive value between 0 and 1. Use a lower value for quicker responsiveness to market changes, and a higher value for trends. The default value is 0.5.

The "RMS length" input determines the length of the RMS calculation for oscillator normalization. The default value is 100 bars.

Ehlers

Ehlers Ultimate Bands (UBANDS)UBANDS: ULTIMATE BANDS

🔍 OVERVIEW AND PURPOSE

Ultimate Bands, developed by John F. Ehlers, are a volatility-based channel indicator designed to provide a responsive and smooth representation of price boundaries with significantly reduced lag compared to traditional Bollinger Bands. Bollinger Bands typically use a Simple Moving Average for the centerline and standard deviations from it to establish the bands, both of which can increase lag. Ultimate Bands address this by employing Ehlers' Ultrasmooth Filter for the central moving average. The bands are then plotted based on the volatility of price around this ultrasmooth centerline.

The primary purpose of Ultimate Bands is to offer traders a clearer view of potential support and resistance levels that react quickly to price changes while filtering out excessive noise, aiming for nearly zero lag in the indicator band.

🧩 CORE CONCEPTS

Ultrasmooth Centerline: Employs the Ehlers Ultrasmooth Filter as the basis (centerline) for the bands, aiming for minimal lag and enhanced smoothing.

Volatility-Adaptive Width: The distance between the upper and lower bands is determined by a measure of price deviation from the ultrasmooth centerline. This causes the bands to widen during volatile periods and contract during calm periods.

Dynamic Support/Resistance: The bands serve as dynamic levels of potential support (lower band) and resistance (upper band).

🧮 CALCULATION AND MATHEMATICAL FOUNDATION

Ehlers' Original Concept for Deviation:

John Ehlers describes the deviation calculation as: "The deviation at each data sample is the difference between Smooth and the Close at that data point. The Standard Deviation (SD) is computed as the square root of the average of the squares of the individual deviations."

This describes calculating the Root Mean Square (RMS) of the residuals:

Smooth = UltrasmoothFilter(Source, Length)

Residuals = Source - Smooth

SumOfSquaredResiduals = Sum(Residuals ^2) for i over Length

MeanOfSquaredResiduals = SumOfSquaredResiduals / Length

SD_Ehlers = SquareRoot(MeanOfSquaredResiduals) (This is the RMS of residuals)

Pine Script Implementation's Deviation:

The provided Pine Script implementation calculates the statistical standard deviation of the residuals:

Smooth = UltrasmoothFilter(Source, Length) (referred to as _ehusf in the script)

Residuals = Source - Smooth

Mean_Residuals = Average(Residuals, Length)

Variance_Residuals = Average((Residuals - Mean_Residuals)^2, Length)

SD_Pine = SquareRoot(Variance_Residuals) (This is the statistical standard deviation of residuals)

Band Calculation (Common to both approaches, using their respective SD):

UpperBand = Smooth + (NumSDs × SD)

LowerBand = Smooth - (NumSDs × SD)

🔍 Technical Note: The Pine Script implementation uses a statistical standard deviation of the residuals (differences between price and the smooth average). Ehlers' original text implies an RMS of these residuals. While both measure dispersion, they will yield slightly different values. The Ultrasmooth Filter itself is a key component, designed for responsiveness.

📈 INTERPRETATION DETAILS

Reduced Lag: The primary advantage is the significant reduction in lag compared to standard Bollinger Bands, allowing for quicker reaction to price changes.

Volatility Indication: Widening bands indicate increasing market volatility, while narrowing bands suggest decreasing volatility.

Overbought/Oversold Conditions (Use with caution):

• Price touching or exceeding the Upper Band may suggest overbought conditions.

• Price touching or falling below the Lower Band may suggest oversold conditions.

Trend Identification:

• Price consistently "walking the band" (moving along the upper or lower band) can indicate a strong trend.

• The Middle Band (Ultrasmooth Filter) acts as a dynamic support/resistance level and indicates the short-term trend direction.

Comparison to Ultimate Channel: Ehlers notes that the Ultimate Band indicator does not differ from the Ultimate Channel indicator in any major fashion.

🛠️ USE AND APPLICATION

Ultimate Bands can be used similarly to how Keltner Channels or Bollinger Bands are used for interpreting price action, with the main difference being the reduced lag.

Example Trading Strategy (from John F. Ehlers):

Hold a position in the direction of the Ultimate Smoother (the centerline).

Exit that position when the price "pops" outside the channel or band in the opposite direction of the trade.

This is described as a trend-following strategy with an automatic following stop.

⚠️ LIMITATIONS AND CONSIDERATIONS

Lag (Minimized but Present): While significantly reduced, some minimal lag inherent to averaging processes will still exist. Increasing the Length parameter for smoother bands will moderately increase this lag.

Parameter Sensitivity: The Length and StdDev Multiplier settings are key to tuning the indicator for different assets and timeframes.

False Signals: As with any band indicator, false signals can occur, particularly in choppy or non-trending markets.

Not a Standalone System: Best used in conjunction with other forms of analysis for confirmation.

Deviation Calculation Nuance: Be aware of the difference in deviation calculation (statistical standard deviation vs. RMS of residuals) if comparing directly to Ehlers' original concept as described.

📚 REFERENCES

Ehlers, J. F. (2024). Article/Publication where "Code Listing 2" for Ultimate Bands is featured. (Specific source to be identified if known, e.g., "Stocks & Commodities Magazine, Vol. XX, No. YY").

Ehlers, J. F. (General). Various publications on advanced filtering and cycle analysis. (e.g., "Rocket Science for Traders", "Cycle Analytics for Traders").

TASC 2025.06 Cybernetic Oscillator█ OVERVIEW

This script implements the Cybernetic Oscillator introduced by John F. Ehlers in his article "The Cybernetic Oscillator For More Flexibility, Making A Better Oscillator" from the June 2025 edition of the TASC Traders' Tips . It cascades two-pole highpass and lowpass filters, then scales the result by its root mean square (RMS) to create a flexible normalized oscillator that responds to a customizable frequency range for different trading styles.

█ CONCEPTS

Oscillators are indicators widely used by technical traders. These indicators swing above and below a center value, emphasizing cyclic movements within a frequency range. In his article, Ehlers explains that all oscillators share a common characteristic: their calculations involve computing differences . The reliance on differences is what causes these indicators to oscillate about a central point.

The difference between two data points in a series acts as a highpass filter — it allows high frequencies (short wavelengths) to pass through while significantly attenuating low frequencies (long wavelengths). Ehlers demonstrates that a simple difference calculation attenuates lower-frequency cycles at a rate of 6 dB per octave. However, the difference also significantly amplifies cycles near the shortest observable wavelength, making the result appear noisier than the original series. To mitigate the effects of noise in a differenced series, oscillators typically smooth the series with a lowpass filter, such as a moving average.

Ehlers highlights an underlying issue with smoothing differenced data to create oscillators. He postulates that market data statistically follows a pink spectrum , where the amplitudes of cyclic components in the data are approximately directly proportional to the underlying periods. Specifically, he suggests that cyclic amplitude increases by 6 dB per octave of wavelength.

Because some conventional oscillators, such as RSI, use differencing calculations that attenuate cycles by only 6 dB per octave, and market cycles increase in amplitude by 6 dB per octave, such calculations do not have a tangible net effect on larger wavelengths in the analyzed data. The influence of larger wavelengths can be especially problematic when using these oscillators for mean reversion or swing signals. For instance, an expected reversion to the mean might be erroneous because oscillator's mean might significantly deviate from its center over time.

To address the issues with conventional oscillator responses, Ehlers created a new indicator dubbed the Cybernetic Oscillator. It uses a simple combination of highpass and lowpass filters to emphasize a specific range of frequencies in the market data, then normalizes the result based on RMS. The process is as follows:

Apply a two-pole highpass filter to the data. This filter's critical period defines the longest wavelength in the oscillator's passband.

Apply a two-pole SuperSmoother (lowpass filter) to the highpass-filtered data. This filter's critical period defines the shortest wavelength in the passband.

Scale the resulting waveform by its RMS. If the filtered waveform follows a normal distribution, the scaled result represents amplitude in standard deviations.

The oscillator's two-pole filters attenuate cycles outside the desired frequency range by 12 dB per octave. This rate outweighs the apparent rate of amplitude increase for successively longer market cycles (6 dB per octave). Therefore, the Cybernetic Oscillator provides a more robust isolation of cyclic content than conventional oscillators. Best of all, traders can set the periods of the highpass and lowpass filters separately, enabling fine-tuning of the frequency range for different trading styles.

█ USAGE

The "Highpass period" input in the "Settings/Inputs" tab specifies the longest wavelength in the oscillator's passband, and the "Lowpass period" input defines the shortest wavelength. The oscillator becomes more responsive to rapid movements with a smaller lowpass period. Conversely, it becomes more sensitive to trends with a larger highpass period. Ehlers recommends setting the smallest period to a value above 8 to avoid aliasing. The highpass period must not be smaller than the lowpass period. Otherwise, it causes a runtime error.

The "RMS length" input determines the number of bars in the RMS calculation that the indicator uses to normalize the filtered result.

This indicator also features two distinct display styles, which users can toggle with the "Display style" input. With the "Trend" style enabled, the indicator plots the oscillator with one of two colors based on whether its value is above or below zero. With the "Threshold" style enabled, it plots the oscillator as a gray line and highlights overbought and oversold areas based on the user-specified threshold.

Below, we show two instances of the script with different settings on an equities chart. The first uses the "Threshold" style with default settings to pass cycles between 20 and 30 bars for mean reversion signals. The second uses a larger highpass period of 250 bars and the "Trend" style to visualize trends based on cycles spanning less than one year:

Ehlers Regime Dynamic CandlesCore Calculation Mechanism

The indicator uses advanced Ehlers signal processing techniques to identify market regimes and create dynamically colored candles that reflect market conditions.

Super Smoother Filter: Price data (open, high, low, close) is processed through an Ehlers Super Smoother Filter to reduce market noise while preserving important price movements. This creates a clearer signal for regime detection.

Autocorrelation Analysis: The core of regime detection uses autocorrelation functions at different lag periods:

Primary autocorrelation measures correlation between the current price and its previous value

Trending autocorrelation measures longer-term persistence in the data series

These values combined determine if the market is in a trending or choppy regime

(Image showing Ehlers custom candles vs default candlesticks)

Regime Strength Calculation:

-Raw signal from autocorrelation with user-defined threshold adjustment

-Adaptive scaling based on sensitivity parameter

-Optional volume validation that confirms signal strength using volume data

-Normalization to 0-1 range and smoothing for visual consistency

-Percentile ranking to provide contextually meaningful strength values

Fisher Transform: Applied to the smoothed price to identify statistical extremes, which helps adjust transparency levels during significant price movements.

Key Features & Components

Regime Detection: Identifies trending vs. choppy market conditions using Ehlers' autocorrelation techniques.

Dynamic Candle Coloring: Candles transition smoothly between three color states:

Bullish trending (typically green/teal)

Bearish trending (typically red/purple)

Choppy/neutral (typically blue/silver)

Volume Validation: Optional incorporation of volume data to confirm trend strength (stronger volume during trending periods increases confidence).

Adaptive Transparency: Candles become more opaque during statistically significant price movements based on Fisher Transform values.

Gradient Smoothing: Controls the visual transition between regime states for a more aesthetically pleasing appearance.

Customizable Colors and Style: Full control over all visual aspects including candle body/wick colors and transparency.

Configuration Options

Users can adjust the following parameters in the indicator settings:

Main Settings:

Cycle Length: Controls the lookback period for cycle detection. Lower values increase responsiveness but may introduce noise.

Gradient Smoothness: Determines how quickly colors transition when regime changes.

Trend Detection Threshold: Sets the autocorrelation strength required to classify a trend.

Trend Sensitivity: Scales regime strength calculation to produce a better distribution of values.

Use Volume: Toggles whether volume data is used to validate trend strength.

Color Settings:

Trending Regime Colors: Separate color options for bullish and bearish candle bodies and wicks.

Choppy Regime Colors: Color options for candle bodies and wicks during sideways/neutral markets.

Style Settings:

Candle Border Options: Toggle borders and adjust their color and transparency.

Adaptive Transparency: Enable/disable dynamic transparency based on statistical significance.

Base Transparency: Set the baseline transparency level for all candles.

Interpretation Notes

Color Transitions: As the market shifts between regimes, candle colors gradually transition, providing visual cues about market structure changes.

Regime Strength: The intensity of colors indicates the strength of the detected regime:

Strong trending regimes show vibrant trending colors

Weak or mixed regimes display colors closer to the choppy/neutral color

Transitions between regimes show gradient colors

Transparency Changes: More opaque candles indicate statistically significant price movements, while more transparent candles suggest routine or less significant price action.

Volume Interaction: When volume validation is enabled, trending colors become more pronounced during high volume trends and subdued during low volume periods.

Disclaimer: These are custom candles that are significantly different from normal candlesticks.

Unlike traditional candlesticks that display raw price data, these candles:

• Use Ehlers signal processing to filter and smooth price data

• Dynamically change color based on detected market regimes

• Show statistical significance through transparency

• May appear delayed compared to standard candles due to the filtering process

Traditional trading strategies dependent on candlestick patterns will not work with these.

Risk Disclaimer

Trading involves significant risk. This indicator is provided for analytical purposes only and does not constitute financial advice. Past performance is not indicative of future results. Use sound risk management practices and never trade with capital you cannot afford to lose. The Ehlers Regime Dynamic Candles indicator should be used as part of a comprehensive trading approach, not as a standalone trading system.

Ehlers Adaptive RSIThe Ehlers Adaptive RSI improves on the traditional RSI by dynamically adjusting its period based on market conditions.

Problem with the Classic RSI:

The traditional Relative Strength Index (RSI) uses a fixed period (e.g., 14), making it slow to react in volatile markets and too sensitive in stable conditions.

How the Adaptive RSI Solves This:

Instead of a fixed period, this version automatically adapts based on market volatility using a combination of ATR (Average True Range) and EMA (Exponential Moving Average).

Key Benefits:

More Responsive – Quickly adapts to market shifts, reducing lag.

Less Noise – Filters out unnecessary fluctuations in stable trends.

Self-Adjusting – No need to manually change RSI settings for different market conditions.

Better Signal Accuracy – Helps detect real trend reversals without false alarms.

This script is for informational and educational purposes only. It does not constitute financial advice, and past performance does not guarantee future results. Use it at your own risk.

Hull Moving Average Adaptive RSI (Ehlers)Hull Moving Average Adaptive RSI (Ehlers)

The Hull Moving Average Adaptive RSI (Ehlers) is an enhanced trend-following indicator designed to provide a smooth and responsive view of price movement while incorporating an additional momentum-based analysis using the Adaptive RSI.

Principle and Advantages of the Hull Moving Average:

- The Hull Moving Average (HMA) is known for its ability to track price action with minimal lag while maintaining a smooth curve.

- Unlike traditional moving averages, the HMA significantly reduces noise and responds faster to market trends, making it highly effective for detecting trend direction and changes.

- It achieves this by applying a weighted moving average calculation that emphasizes recent price movements while smoothing out fluctuations.

Why the Adaptive RSI Was Added:

- The core HMA line remains the foundation of the indicator, but an additional analysis using the Adaptive RSI has been integrated to provide more meaningful insights into momentum shifts.

- The Adaptive RSI is a modified version of the traditional Relative Strength Index that dynamically adjusts its sensitivity based on market volatility.

- By incorporating the Adaptive RSI, the HMA visually represents whether momentum is strengthening or weakening, offering a complementary layer of analysis.

How the Adaptive RSI Influences the Indicator:

- High Adaptive RSI (above 65): The market may be overbought, or bullish momentum could be fading. The HMA turns shades of red, signaling a possible exhaustion phase or potential reversals.

- Neutral Adaptive RSI (around 50): The market is in a balanced state, meaning neither buyers nor sellers are in clear control. The HMA takes on grayish tones to indicate this consolidation.

- Low Adaptive RSI (below 35): The market may be oversold, or bearish momentum could be weakening. The HMA shifts to shades of blue, highlighting potential recovery zones or trend slowdowns.

Why This Combination is Powerful:

- While the HMA excels in tracking trends and reducing lag, it does not provide information about momentum strength on its own.

- The Adaptive RSI bridges this gap by adding a clear visual layer that helps traders assess whether a trend is likely to continue, consolidate, or reverse.

- This makes the indicator particularly useful for spotting trend exhaustion and confirming momentum shifts in real-time.

Best Use Cases:

- Works effectively on timeframes from 1 hour (1H) to 1 day (1D), making it suitable for swing trading and position trading.

- Particularly useful for trading indices (SPY), stocks, forex, and cryptocurrencies, where momentum shifts are frequent.

- Helps identify not just trend direction but also whether that trend is gaining or losing strength.

Recommended Complementary Indicators:

- Adaptive Trend Finder: Helps identify the dominant long-term trend.

- Williams Fractals Ultimate: Provides key reversal points to validate trend shifts.

- RVOL (Relative Volume): Confirms significant moves based on volume strength.

This enhanced HMA with Adaptive RSI provides a powerful, intuitive visual tool that makes trend analysis and momentum interpretation more effective and efficient.

This indicator is for educational and informational purposes only. It should not be considered financial advice or a guarantee of performance. Always conduct your own research and use proper risk management when trading. Past performance does not guarantee future results.

TASC 2025.04 The Ultimate Oscillator█ OVERVIEW

This script implements an alternative, refined version of the Ultimate Oscillator (UO) designed to reduce lag and enhance responsiveness in momentum indicators, as introduced by John F. Ehlers in his article "Less Lag In Momentum Indicators, The Ultimate Oscillator" from the April 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers states that indicators are essentially filters that remove unwanted noise (i.e., unnecessary information) from market data. Simply put, they process a series of data to place focus on specific information, providing a different perspective on price dynamics. Various filter types attenuate different periodic signals within the data. For instance, a lowpass filter allows only low-frequency signals, a highpass filter allows only high-frequency signals, and a bandpass filter allows signals within a specific frequency range .

Ehlers explains that the key to removing indicator lag is to combine filters of different types in such a way that the result preserves necessary, useful signals while minimizing delay (lag). His proposed UltimateOscillator aims to maintain responsiveness to a specific frequency range by measuring the difference between two highpass filters' outputs. The oscillator uses the following formula:

UO = (HP1 - HP2) / RMS

Where:

HP1 is the first highpass filter.

HP2 is another highpass filter that allows only shorter wavelengths than the critical period of HP1.

RMS is the root mean square of the highpass filter difference, used as a scaling factor to standardize the output.

The resulting oscillator is similar to a bandpass filter , because it emphasizes wavelengths between the critical periods of the two highpass filters. Ehlers' UO responds quickly to value changes in a series, providing a responsive view of momentum with little to no lag.

█ USAGE

Ehlers' UltimateOscillator sets the critical periods of its highpass filters using two parameters: BandEdge and Bandwidth :

The BandEdge sets the critical period of the second highpass filter, which determines the shortest wavelengths in the response.

The Bandwidth is a multiple of the BandEdge used for the critical period of the first highpass filter, which determines the longest wavelengths in the response. Ehlers suggests that a Bandwidth value of 2 works well for most applications. However, traders can use any value above or equal to 1.4.

Users can customize these parameters with the "Bandwidth" and "BandEdge" inputs in the "Settings/Inputs" tab.

The script plots the UO calculated for the specified "Source" series in a separate pane, with a color based on the chart's foreground color. Positive UO values indicate upward momentum or trends, and negative UO values indicate the opposite.

Additionally, this indicator provides the option to display a "cloud" from 10 additional UO series with different settings for an aggregate view of momentum. The "Cloud" input offers four display choices: "Bandwidth", "BandEdge", "Bandwidth + BandEdge", or "None".

The "Bandwidth" option calculates oscillators with different Bandwidth values based on the main oscillator's setting. Likewise, the "BandEdge" option calculates oscillators with varying BandEdge values. The "Bandwidth + BandEdge" option calculates the extra oscillators with different values for both parameters.

When a user selects any of these options, the script plots the maximum and minimum oscillator values and fills their space with a color gradient. The fill color corresponds to the net sum of each UO's sign , indicating whether most of the UOs reflect positive or negative momentum. Green hues mean most oscillators are above zero, signifying stronger upward momentum. Red hues mean most are below zero, indicating stronger downward momentum.

[GYTS] Ultimate Smoother (3-poles + 2 poles)Ultimate Smoother (3-pole)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 Release of 3-Pole Ultimate Smoother

This indicator presents a new 3-pole version of John Ehlers' Ultimate Smoother (2024) . This results in an unconventional filter that exhibits effectively zero lag in practical trading applications, regardless of the set period. By using a 2-pole high-pass filter in its design, it responds to price direction changes on the same bar, while still allowing the user to control smoothness.

💮 What is the Ultimate Smoother?

The original Ultimate Smoother is a revolutionary filter designed by John Ehlers (2024) that smooths price data with virtually zero lag in the pass band. While conventional filters always introduce lag when removing market noise, the Ultimate Smoother maintains phase alignment at low frequencies while still providing excellent noise reduction.

💮 Mathematical Foundation

The Ultimate Smoother achieves its remarkable properties through a clever mathematical approach:

1. Instead of directly designing a low-pass filter (like traditional moving averages), it subtracts a high-pass filter from an all-pass filter (the original input data).

2. At very low frequencies, the high-pass filter contributes almost nothing, so the output closely matches the input in both amplitude and phase.

3. At higher frequencies, the high-pass filter's response increasingly matches the input data, resulting in cancellation through subtraction.

The 3-pole version extends this principle by using a higher-order high-pass filter, requiring additional coefficients and handling more terms in the numerator of the transfer function.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Period Parameter Behaviour

The period parameter in the 3-pole Ultimate Smoother works somewhat counterintuitively:

- Longer periods: Result in less smooth, but more responsive following of the price. The filter output more closely tracks the input data.

- Shorter periods: Produce smoother output but may exhibit overshooting (extrapolating price movement) for larger movements.

This is different from most filters where longer periods typically produce smoother outputs with more lag.

💮 When to Choose 3-Pole vs. 2-Pole

- Choose the 3-pole version when you need zero-lag but want to control the smoothness

- Choose the 2-pole version when you are okay with some lag with the benefit of more smoothness.

🌸 --------- ACKNOWLEDGEMENTS --------- 🌸

This indicator builds upon the pioneering work of John Ehlers, particularly from his article April 2024 edition of TASC's Traders' Tips . The original version is published on TradingView by @PineCodersTASC .

This 3-pole extension was developed by @GoemonYae . Feedback is highly appreciated!

Ehlers Stable Dominant Cycle Length [graylange]Stable Dominant Cycle Length – Adaptive Cycle Detection for Market Timing

This script calculates the dominant cycle length of the market using an improved version of John Ehlers' Hilbert Transform approach. Unlike traditional implementations, this version includes advanced smoothing techniques to reduce noise and prevent erratic spikes, making it more reliable for adaptive cycle-based strategies.

🔥 Key Features:

✅ Noise-Reduced Cycle Detection – Uses a Weighted Moving Average (WMA) detrending method instead of raw Hilbert Transform values to enhance stability.

✅ Adaptive Smoothing – Applies an Exponential Moving Average (EMA) to the instantaneous period, reducing excessive volatility in cycle length calculations.

✅ Phase Wrapping & Constraints – Clamps phase changes to prevent unrealistic cycle swings and division errors.

✅ Dynamic Cycle Adjustment – The dominant cycle length updates in real time, constrained within a reasonable range (6 to 50 bars) to avoid extreme peaks.

📌 How to Use It:

Identify Market Cycles – Use the dominant cycle length to determine optimal trend-following vs. mean-reversion strategies.

Enhance MESA Filters – Apply the detected cycle length to adjust Ehlers’ MESA Adaptive Moving Average (MAMA) dynamically.

Fine-Tune Alpha Settings – Reduce overfitting in cycle-based indicators by basing parameters on a stable dominant cycle estimate.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Ehlers Maclaurin Ultimate Smoother [CT]Ehlers Maclaurin Ultimate Smoother

Introduction

The Ehlers Maclaurin Ultimate Smoother is an innovative enhancement of the classic Ehlers SuperSmoother. By leveraging advanced Maclaurin series approximations, this indicator offers superior market analysis and signal generation.

The indicator combines Ehlers' Ultimate Smoother with Maclaurin series approximations to create a more efficient and accurate smoothing mechanism:

Input price data passes through the initial smoothing phase

Maclaurin series approximates trigonometric functions

Enhanced high-pass filter removes market noise

Final smoothing phase produces the output signal

Why the Maclaurin Approach?

The Maclaurin series is a special form of the Taylor series, centered around 0. It provides an efficient way to approximate complex functions using polynomial terms. In this indicator, we use the Maclaurin approach to improve the sine and cosine functions, resulting in:

Faster Calculations: By using polynomial approximations, we significantly reduce computational complexity.

Improved Stability: The approximation provides a more stable numerical basis for calculations.

Preservation of Precision: Despite the approximation, we maintain the precision needed for price smoothing.

Calculations

The indicator employs several key mathematical components:

Maclaurin Series Approximation:

sin(x) ≈ x - x³/3! + x⁵/5! - x⁷/7! + x⁹/9!

cos(x) ≈ 1 - x²/2! + x⁴/4! - x⁶/6! + x⁸/8!

Smoothing Algorithm:

Uses exponential smoothing with optimized coefficients

Implements high-pass filtering for noise reduction

Applies dynamic weighting based on market conditions

Mathematical Foundation

Utilizes Maclaurin series for trigonometric approximation

Implements Ehlers' smoothing principles

Incorporates advanced filtering techniques

Technical Advantages

Signal Processing:

Lag Reduction: Faster signal detection with less delay.

Noise Filtration: Effective elimination of high-frequency noise.

Precision Enhancement: Preservation of critical price movements.

Adaptive Processing: Dynamic response to market volatility.

Visual Enhancements:

Smart color intensity mapping.

Real-time visualization of trend strength.

Adaptive opacity based on movement significance.

Implementation

Core Configuration:

Plot Type: Choose between the original and the Maclaurin enhanced version.

Length: Default set to 30, optimal for daily timeframes.

hpLength: Default set to 10 for enhanced noise reduction.

Advanced Parameters:

The indicator offers advanced control with:

Dual processing modes (Original/Maclaurin).

Dynamic color intensity system.

Customizable smoothing parameters.

Professional Analysis Tools:

Accurate trend reversal identification.

Advanced support/resistance detection.

Superior performance in volatile markets.

Technical Specifications

Maclaurin Series Implementation:

The indicator employs a 5-term Maclaurin series approximation for both sine and cosine, ensuring efficient and accurate computation.

Performance Metrics

Improved processing efficiency.

Reduced memory utilization.

Increased signal accuracy.

Licensing & Attribution

© 2024 Mupsje aka CasaTropical

Professional Credits

Original Ultimate and SuperSmoother concept: John F. Ehlers

Maclaurin enhancement: Casa Tropical (CT)

www.mathsisfun.com

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Ehlers Loops [BigBeluga]The Ehlers Loops indicator is based on the concepts developed by John F. Ehlers, which provide a visual representation of the relationship between price and volume dynamics. This tool helps traders predict future market movements by observing how price and volume data interact within four distinct quadrants of the loop, each representing different combinations of price and volume directions. The unique structure of this indicator provides insights into the strength and direction of market trends, offering a clearer perspective on price behavior relative to volume.

🔵 KEY FEATURES & USAGE

● Four Price-Volume Quadrants:

The Ehlers Loops chart consists of four quadrants:

+Price & +Volume (top-right) – Typically indicates a bullish continuation in the market.

-Price & +Volume (bottom-right) – Generally shows a bearish continuation.

+Price & -Volume (top-left) – Typically indicates an exhaustion of demand with a potential reversal.

-Price & -Volume (bottom-left) – Indicates exhaustion of supply and near trend reversal.

By watching how symbols move through these quadrants over time, traders can assess shifts in momentum and volume flow.

● Price and Volume Scaling in Standard Deviations:

Both price and volume data are individually filtered using HighPass and SuperSmoother filters, which transform them into band-limited signals with zero mean. This scaling allows traders to view data in terms of its deviation from the average, making it easier to spot abnormal movements or trends in both price and volume.

● Loops Trajectories with Tails:

The loops draw a trail of price and volume dynamics over time, allowing traders to observe historical price-volume interactions and predict future movements based on the curvature and direction of the rotation.

● Price & Volume Histograms:

On the right side of the chart, histograms for each symbol provide a summary of the most recent price and volume values. These histograms allow traders to easily compare the strength and direction of multiple assets and evaluate market conditions at a glance.

● Flexible Symbol Display & Customization:

Traders can select up to five different symbols to be displayed within the Ehlers Loops. The settings also allow customization of symbol size, colors, and visibility of the histograms. Additionally, traders can adjust the LPPeriod and HPPeriod to change the smoothness and lag of the loops, with a shorter LPPeriod offering more responsiveness and a longer HPPeriod emphasizing longer-term trends.

🔵 USAGE

🔵 SETTINGS

Low pass Period: default is 10 to

obtain minimum lag with just a little smoothing.

High pass Period: default is 125 (half of the year if Daily timeframe) to capture the longer term moves.

🔵 CONCLUSION

The Ehlers Loops indicator offers a visually rich and highly customizable way to observe price and volume dynamics across multiple assets. By using band-limited signals and scaling data into standard deviations, traders gain a powerful tool for identifying market trends and predicting future movements. Whether you're tracking short-term fluctuations or long-term trends, Ehlers Loops can help you stay ahead of the market by offering key insights into the relationship between price and volume.

TASC 2024.11 Ultimate Strength Index█ OVERVIEW

This script implements the Ultimate Strength Index (USI) indicator, introduced by John Ehlers in his article titled "Ultimate Strength Index (USI)" from the November 2024 edition of TASC's Traders' Tips . The USI is a modified version of Wilder's original Relative Strength Index (RSI) that incorporates Ehlers' UltimateSmoother lowpass filter to produce an output with significantly reduced lag.

█ CONCEPTS

Many technical indicators, including the RSI, lag due to their heavy reliance on historical data. John Ehlers reformulated the RSI to substantially reduce lag by applying his UltimateSmoother filter to upward movements ( strength up - SU ) and downward movements ( strength down - SD ) in the time series, replacing the standard process of smoothing changes with rolling moving averages (RMAs). Ehlers' recent works, covered in our recent script publications, have shown that the UltimateSmoother is an effective alternative to other classic averages, offering notably less lag in its response.

Ehlers also modified the RSI formula to produce an index that ranges from -1 to +1 instead of 0 to 100. As a result, the USI indicates bullish conditions when its value moves above 0 and bearish conditions when it falls below 0.

The USI retains many of the strengths of the traditional RSI while offering the advantage of reduced lag. It generally uses a larger lookback window than the conventional RSI to achieve similar behavior, making it suitable for trend trading with longer data lengths. When applied with shorter lengths, the USI's peaks and valleys tend to align closely with significant turning points in the time series, making it a potentially helpful tool for timing swing trades.

█ CALCULATIONS

The first step in the USI's calculation is determining each bar's strength up (SU) and strength down (SD) values. If the current bar's close exceeds the previous bar's, the calculation assigns the difference to SU. Otherwise, SU is zero. Likewise, if the current bar's close is below the previous bar's, it assigns the difference to SD. Otherwise, SD is zero.

Next, instead of the RSI's typical smoothing process, the USI's calculation applies the UltimateSmoother to the short-term average SU and SD values, reducing high-frequency chop in the series with low lag.

Finally, this formula determines the USI value:

USI = ( Ult (SU) − Ult (SD)) / ( Ult (SU) + Ult (SD)),

where Ult (SU) and Ult (SD) are the smoothed average strength up and strength down values.

Smooth Cloud [BigBeluga]This trend-following indicator, called Smooth Cloud, is built on top of a SuperSmoother Filter of John Ehlers with small modification.

It consists of three smoothed lines—Fast, Middle, and Slow—that together form a cloud. These lines are based on different periods, helping traders analyze market changes over different timeframes (fast, mid, and slow). The indicator offers a color-coded visual cloud to depict trend direction, along with a detailed dashboard that shows the positioning of the lines, whether they are rising or falling, and their price levels.

🔵 IDEA

The Smooth Cloud indicator is designed to help traders quickly assess the market trend by using three smoothed lines with varying periods. The lines represent fast, mid, and slow market changes, and their relative positioning provides a clear view of trend shifts. The dashboard gives a more granular view by showing if the lines are rising or falling individually, without comparing them to each other, providing insights into potential trend changes before they are fully formed. The color-coded cloud further enhances the visual experience by allowing traders to see trend direction at a glance, making it easier to spot major and minor shifts in the market.

🔵 KEY FEATURES & USAGE

◉ Three Smoothed Lines (Fast, Mid, Slow):

The indicator consists of three smoothed lines, each representing a different periods. The Fast line reacts more quickly to price changes, while the Slow line reacts more slowly, allowing traders to capture both short-term and long-term trend information. The lines are based on different lengths, and their positioning relative to each other helps determine market direction.

◉ Color-Coded Cloud:

The cloud formed between the lines is color-coded to indicate trend direction. When the Fast line is above the Slow line, it signals an upward trend, and the cloud is green. When the Fast line is below the Slow line, the cloud turns red, indicating a downward trend. This color coding makes it easy to spot the overall trend direction visually without having to analyze the lines in detail.

◉ Dashboard for Line Positioning and Trend Direction:

A dashboard in the top right corner of the chart shows the positioning of the Fast, Middle, and Slow lines relative to each other. It displays arrows for each line to indicate whether the line is above or below the other lines. For exae determines its trend direction based on its position to mid line — if it's above, an upward arrow is displayed, and if it's below mid line, a downward arrow is shown.mple, if the Fast line is above the Slow line, the dashboard shows an upward arrow for the Fast line. The Slow lin

Up trend:

Up trend shift:

Down trend shift:

Down Trend:

◉ Rising and Falling Detection:

The dashboard also tracks whether the lines are rising or falling based solely on their own values. If a line rises or falls consistently over three bars, the dashboard shows an upward or downward arrow under the "Rising or Falling" section. This feature provides additional insight into the market's momentum, allowing traders to spot potential trend reversals more quickly.

◉ Price Levels for Fast, Middle, and Slow Lines:

The dashboard includes the price levels for the Fast, Middle, and Slow lines, displayed at the bottom. These levels give traders a quick reference for where the lines are currently positioned relative to the price, adding further context to the trend information displayed.

◉ Fast Signals:

The fast signals are diplayed when fast line crosses slow line. Gree arrows up shows fast line crossed over slow and when arrow down fast line crossed under slow one.

🔵 CUSTOMIZATION

Length Input: You can adjust the length parameter, which affects the smoothing period for the lines. A shorter length makes the lines react more quickly to price changes, while a longer length provides a smoother, more gradual response.

Source Input: The indicator uses the hl2 source (the average of the high and low prices), but you can change this to another source to better suit your trading strategy.

Signals Type: Select between "Fast" and "Slow". Fast signals - is interaction of fast and slow lines. Slow signals is interaction of mid and slow lines

Related script:

Ehlers Band-Pass FilterHeyo,

This indicator is an original translation from Ehlers' book "Cycle Analytics for Traders Advanced".

First, I describe the indicator as usual and later you can find a very insightful quote of the book.

Key Features

Signal Line: Represents the output of the band-pass filter, highlighting the dominant cycle in the data.

Trigger Line: A leading indicator derived from the signal line, providing early signals for potential market reversals.

Dominant Cycle: Measures the dominant cycle period by counting the number of bars between zero crossings of the band-pass filter output.

Calculation:

The band-pass filter is implemented using a combination of high-pass and low-pass filters.

The filter's parameters, such as period and bandwidth, can be adjusted to tune the filter to specific market cycles.

The signal line is normalized using an Automatic Gain Control (AGC) to provide consistent amplitude regardless of price swings.

The trigger line is derived by applying a high-pass filter to the signal line, creating a leading

waveform.

Usage

The indicator is effective in identifying peaks and valleys in the market data.

It works best in cyclic market conditions and may produce false signals during trending periods.

The dominant cycle measurement helps traders understand the prevailing market cycle length, aiding in better decision-making.

Quoted from the Book

Band-Pass Filters

“A little of the data narrowly passed,” said Tom broadly.

Perhaps the least appreciated and most underutilized filter in technical analysis is the band-pass filter. The band-pass filter simultaneously diminishes the amplitude at low frequencies, qualifying it as a detrender, and diminishes the amplitude at high frequencies, qualifying it as a data smoother.

It passes only those frequency components from input to output in which the trader is interested. The filtering produced by a band-pass filter is superior because the rejection in the stop bands is related to its bandwidth. The degree of rejection of undesired frequency components is called selectivity. The band-stop filter is the dual of the band-pass filter. It rejects a band of frequency components as a notch at the output and passes all other frequency components virtually unattenuated. Since the bandwidth of the deep rejection in the notch is relatively narrow and since the spectrum of market cycles is relatively broad due to systemic noise, the band-stop filter has little application in trading.

Measuring the Cycle Period

The band-pass filter can be used as a relatively simple measurement of the dominant cycle.

A cycle is complete when the waveform crosses zero two times from the last zero crossing. Therefore, each successive zero crossing of the indicator marks a half cycle period. We can establish the dominant cycle period as twice the spacing between successive zero crossings.

When we measure the dominant cycle period this way, it is best to widen the pass band of the band-pass filter to avoid distorting the measurement simply due to the selectivity of the filter. Using an input bandwidth of 0.7 produces an octave-wide pass band. For example, if the center period of the filter is 20 and the relative bandwidth is 0.7, the bandwidth is 14. That means the pass band of the filter extends from 13-bar periods to 27-bar periods.

That is, roughly an octave exists because the longest period is twice the shortest period of the pass band. It is imperative that a high-pass filter is tuned one octave below the half-bandwidth edge of the band-pass filter to ensure a nominal zero mean of the filtered output. Without a zero mean, the zero crossings can have a substantial error.

Since the measurement of the dominant cycle can vary dramatically from zero crossing to zero

crossing, the code limits the change between measurements to be no more than 25 percent.

While measuring the changing dominant cycle period via zero crossings of the band-pass waveform is easy, it is not necessarily the most accurate method.

Best regards,

simwai

Good Luck with your trading! 🙌

TASC 2024.09 Precision Trend Analysis█ OVERVIEW

This script introduces an approach for detecting and confirming trends in price series based on digital signal processing principles, as presented by John Ehlers in the "Precision Trend Analysis" article from the September 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

Traditional trend-following indicators, such as moving averages , are lowpass filters that pass low-frequency components in a series and remove high-frequency components. Because lowpass filters preserve lengthy cycles in the data while attenuating shorter cycles, such filters have unavoidable lag that impacts the timeliness of trading signals.

In his article, John Ehlers presents an alternative approach that combines two highpass filters with different lengths to remove undesired high-frequency content via cancellation . Highpass filters have nearly zero lag. As such, the resulting trend indicator from this approach is very responsive to changes in the price series, with peaks and valleys that closely align with those of the price data. The indicator signifies an uptrend when its value is positive (i.e., above the balance point) and a downtrend when it is negative.

Subsequently, John Ehlers demonstrates that one can use the trend indicator's rate of change (ROC) to determine the onset of new trend movements. The ROC is zero at peaks and valleys in the trend indicator. Therefore, when the ROC crosses above zero, it signifies the onset or continuation of an uptrend. Likewise, the ROC crossing below zero indicates the onset or continuation of a downtrend. Note, however, that because the ROC does not preserve lower-frequency information, it can produce whipsaw trading signals in sideways or continuously trending price series.

This script implements both the trend indicator and its ROC along with the following on-chart signals:

• Green and red arrows that indicate the possible onset or continuation of an uptrend and downtrend, respectively

• Bar and plot colors that signify the sign (direction) of the trend indicator

█ CALCULATIONS

The math behind the trend indicator comes from digital filter design principles. The first step applies a digital highpass filter that attenuates long cycles with periods above the user-specified critical period. The default value is 250 bars, representing roughly one year for instruments such as stocks on the daily timeframe. The next step applies a highpass filter with a shorter period (40 bars by default). The difference between these filters determines the trend indicator, which preserves cyclic components between 40 and 250 bars by default while attenuating and eliminating others. The ROC represents the scaled one-bar difference in the trend indicator.

ICT Balanced Price Range [TradingFinder] BPR | FVG + IFVG🔵 Introduction

The ICT Balanced Price Range (BPR) indicator is a valuable tool that helps traders identify key areas on price charts where a balance between buyers and sellers is established. These zones can serve as critical points for potential price reversals or continuations.

🟣 Bullish Balanced Price Range

A Bullish BPR forms when a buying pressure zone (Bullish FVG) overlaps with a Bullish Inversion FVG. This overlap indicates a high probability of price moving upwards, making it a crucial area for traders to consider.

🟣 Bearish Balanced Price Range

Similarly, a Bearish BPR is created when a selling pressure zone (Bearish FVG) overlaps with a Bearish Inversion FVG. This zone is often seen as a key area where the price is likely to move downward.

🔵 How to Use

🟣 Identifying the Balanced Price Range (BPR)

To identify the Balanced Price Range (BPR), you must first locate two Fair Value Gaps (FVGs) on the price chart. One FVG should be on the sell side, and the other on the buy side. When these two FVGs horizontally oppose each other, the area where they overlap is recognized as the Balanced Price Range (BPR).

This BPR zone is highly sensitive to price movements due to the combination of two FVGs, often leading to strong market reactions. As the price approaches this area, the likelihood of a significant market move increases, making it a prime target for professional traders.

🟣 Bullish Balanced Price Range (Bullish BPR)

To effectively trade using a Bullish BPR, begin by identifying a bullish market structure and searching for bullish Price Delivery Arrays (PD Arrays). Once the market structure shifts to bullish in a lower time frame, locate a Bullish FVG within the Discount Zone that overlaps with a Bearish FVG.

Mark this overlapping zone and wait for the price to test it before executing a buy trade. Alternatively, you can set a Buy Limit order with a stop loss below the recent swing low and target profits based on higher time frame liquidity draws.

🟣 Bearish Balanced Price Range (Bearish BPR)

For bearish trades, start by identifying a bearish market structure and look for bearish PD Arrays. After the market structure shifts to bearish in a lower time frame, identify a Bearish FVG within the Discount Zone that overlaps with a Bullish FVG. Mark this overlapping zone and execute a sell trade when the price tests it.

You can also use a Sell Limit order with a stop loss above the recent swing high and target profits according to higher time frame liquidity draws.

🔵 Settings

🟣 Global Settings

Show All Inversion FVG & IFVG : If disabled, only the most recent FVG & IFVG will be displayed.

FVG & IFVG Validity Period (Bar) : Determines the maximum duration (in number of candles) that the FVG and IFVG remain valid.

Switching Colors Theme Mode : Includes three modes: "Off", "Light", and "Dark". "Light" mode adjusts colors for light mode use, "Dark" mode adjusts colors for dark mode use, and "Off" disables color adjustments.

🟣 Display Settings

Show Bullish BPR : Toggles the display of demand-related boxes.

Show Bearish BPR : Toggles the display of supply-related boxes.

Mitigation Level BPR : Options include "Proximal", "Distal", or "50 % OB" modes, which you can choose based on your needs. The "50 % OB" line is the midpoint between distal and proximal.

Show Bullish IFVG : Toggles the display of demand-related boxes.

Show Bearish IFV G: Toggles the display of supply-related boxes.

Mitigation Level FVG and IFVG : Options include "Proximal", "Distal", or "50 % OB" modes, which you can choose based on your needs. The "50 % OB" line is the midpoint between distal and proximal.

🟣 Logic Settings

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter : Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filter : Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter : Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filte r: Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

🟣 Alert Settings

Alert Inversion FVG Mitigation : Enables alerts for Inversion FVG mitigation.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

Display More Info : Provides additional details in alert messages, including price range, date, hour, and minute. Set to 'Off' to exclude this information.

🔵 Conclusion

The ICT Balanced Price Range is a powerful and reliable tool for identifying key points on price charts. This strategy can be applied across various time frames and serves as a complementary tool alongside other indicators and technical analysis methods.

The most crucial aspect of utilizing this strategy effectively is correctly identifying FVGs and their overlapping areas, which comes with practice and experience.

Inversion Fair Value Gaps [TradingFinder] IFVG ICT Signal| Alert🔵 Introduction

🟣 Inversion Fair Value Gap (IFVG)

An ICT Inversion Fair Value Gap, or reverse FVG, occurs when a fair value gap fails to hold its price, resulting in the price moving beyond and breaking the gap. This situation marks the initial change in price momentum.

Generally, prices respect fair value gaps and continue in their trend direction. However, when a fair value gap is breached, it transforms into an inversion fair value gap, signaling a potential short-term reversal or a subsequent change in direction.

🔵 How to Use

🟣 Identifying an Inversion Fair Value Gap

To spot an IFVG, you must first identify a fair value gap.

Inversion fair value gaps can be categorized into two types :

🟣 Bullish Inversion Fair Value Gap

A bullish IFVG occurs when a bearish fair value gap is invalidated by the price closing above it.

Steps to identify it :

Identify a bearish fair value gap.

When the price closes above this gap, it becomes a bullish inversion fair value gap.

This gap acts as a support level, pushing the price upwards and indicating a shift in momentum from sellers to buyers.

🟣 Bearish Inversion Fair Value Gap

A bearish IFVG happens when a bullish fair value gap fails, with the price closing below it.

Steps to identify it :

Identify a bullish fair value gap.

When the price closes below this gap, it becomes a bearish inversion fair value gap.

This gap acts as a resistance level, pushing the price downwards and indicating a shift in momentum from buyers to sellers.

🔵 Settings

🟣 Global Settings

Show All Inversion FVG: If disabled, only the most recent FVG will be displayed.

IFVG Validity Period (Bar): Determines the maximum duration (in number of candles) that the FVG and IFVG remain valid.Switching Colors Theme Mode: Includes three modes: "Off", "Light", and "Dark". "Light" mode adjusts colors for light mode use, "Dark" mode adjusts colors for dark mode use, and "Off" disables color adjustments.

🟣 Logic Settings

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter : Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filte r: Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter : Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filter : Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

Mitigation Level FVG and IFVG : Options include "Proximal", "Distal", or "50 % OB" modes, which you can choose based on your needs. The "50 % OB" line is the midpoint between distal and proximal.

🟣 Display Settings

Show Bullish IFVG : Toggles the display of demand-related boxes.

Show Bearish IFVG : Toggles the display of supply-related boxes.

🟣 Alert Settings

Alert Inversion FVG Mitigation : Enables alerts for Inversion FVG mitigation.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

Display More Info : Provides additional details in alert messages, including price range, date, hour, and minute. Set to 'Off' to exclude this information.

Order Blocks & Breaker Blocks [TradingFinder] Signals + Alerts🔵 Introduction

Order Block and Breaker Block, are powerful tools in technical analysis. By understanding these concepts, traders can enhance their ability to predict potential price reversals and continuations, leading to more effective trading strategies.

Using historical price action, volume analysis, and candlestick patterns, traders can identify key areas where institutional activities influence market movements.

🟣 Demand Order Block and Supply Breaker Block

Demand Order Block : A Demand Order Block is formed when the price succeeds in breaking the previous high pivot.

Supply Breaker Block : A Supply Breaker Block is formed when the price succeeds in breaking the Demand Order Block. As a result, the Order Block changes its role and turns from the role of price support to resistance.

🟣 Supply Order Block and Demand Breaker Block

Supply Order Block : A Supply Order Block is formed when the price succeeds in breaking the previous low pivot.

Demand Breaker Block : A Demand Breaker Block is formed when the price succeeds in breaking the Supply Order Block. As a result, the Order Block changes its role and turns from the role of price resistance to support.

🔵 How to Use

🟣 Order Blocks (Supply and Demand)

Order blocks are zones where the likelihood of a price reversal is higher. In demand zones, buying opportunities arise, while in supply zones, selling opportunities can be explored.

The "Refinement" feature allows you to adjust the width of the order block to fit your trading strategy. There are two modes in the "Order Block Refine" feature: "Aggressive" and "Defensive." The primary difference between these modes is the width of the order block.

For risk-averse traders, the "Defensive" mode is ideal as it offers a lower loss limit and a higher reward-to-risk ratio.

Conversely, for traders who are willing to take more risks, the "Aggressive" mode is more suitable. This mode, with its wider order block width, caters to those who prefer entering trades at higher prices.

🟣 Breaker Blocks (Supply and Demand)

Trading based on breaker blocks is the same as order blocks and the price in these zones is likely to be reversed.

🔵 Setting

🟣 Global Setting

Pivot Period of Order Blocks Detector : Enter the desired pivot period to identify the Order Block.

Order Block Validity Period (Bar) : You can specify the maximum time the Order Block remains valid based on the number of candles from the origin.

Mitigation Level Order Block : Determining the basic level of a Order Block. When the price hits the basic level, the Order Block due to mitigation.

Mitigation Level Breaker Block : Determining the basic level of a Breaker Block. When the price hits the basic level, the Breaker Block due to mitigation.

Switching Colors Theme Mode : Three modes "Off", "Light" and "Dark" are included in this parameter. "Light" mode is for color adjustment for use in "Light Mode".

"Dark" mode is for color adjustment for use in "Dark Mode" and "Off" mode turns off the color adjustment function and the input color to the function is the same as the output color.

🟣 Order Block Display

Show All Order Block : If it is turned off, only the last Order Block will be displayed.

Demand Main Order Block : Show or not show and specify color.

Demand Sub (Propulsion & BoS Origin) Order Block : Show or not show and specify color.

Supply Main Order Block : Show or not show and specify color.

Supply Sub (Propulsion & BoS Origin) Order Block : Show or not show and specify color.

🟣 Breaker Block Display

Show All Breaker Block : If it is turned off, only the last Breaker Block will be displayed.

Demand Main Breaker Block : Show or not show and specify color.

Demand Sub (Propulsion & BoS Origin) Breaker Block : Show or not show and specify color.

Supply Main Breaker Block : Show or not show and specify color.

Supply Sub (Propulsion & BoS Origin) Breaker Block : Show or not show and specify color.

🟣 Order Block Refinement

Refine Order Blocks : Enable or disable the refinement feature. Mode selection.

🟣 Alert

Alert Name : The name of the alert you receive.

Alert Demand OB Mitigation :

On / Off

Alert Demand BB Mitigation :

On / Off

Alert Supply OB Mitigation :

On / Off

Alert Supply BB Mitigation :

On / Off

Message Frequency :

This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone :

The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

Display More Info :

Displays information about the price range of the order blocks (Zone Price) and the date, hour, and minute under "Display More Info".

If you do not want this information to appear in the received message along with the alert, you should set it to "Off".

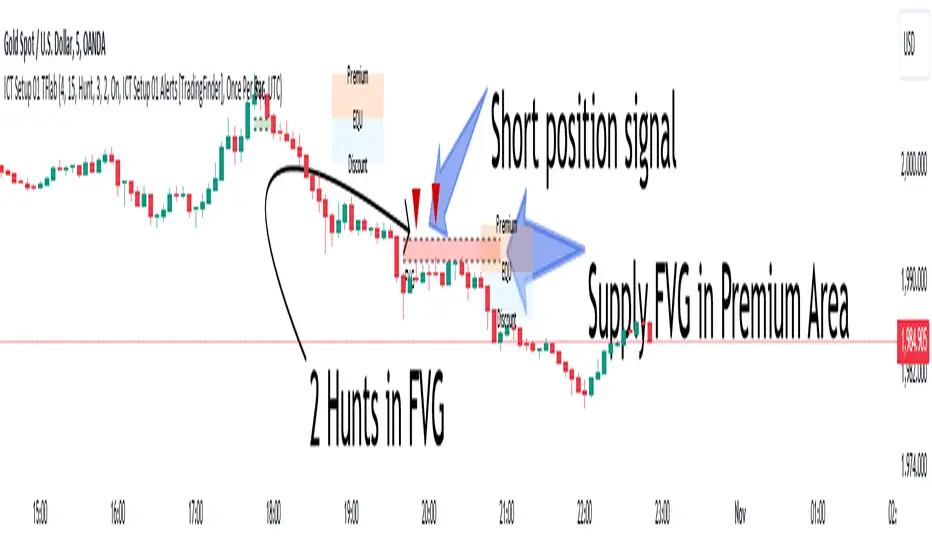

ICT Setup 01 [TradingFinder] FVG + Liquidity Sweeps/Hunt Alerts🔵 Introduction

The ICT (Inner Circle Trader) style of trading involves analyzing the behavior of market participants and market makers to identify areas where fake buy and sell activities occur. This trading style helps retail traders align with market maker behavior and avoid falling into market traps.

A key aspect of the ICT strategy is focusing on liquidity hunts. This involves searching for trading opportunities in areas of the market with low liquidity or where other traders have little activity. The ICT method leverages market inefficiencies and weaknesses, allowing traders to profit from small price movements that might go unnoticed by others.

In "ICT Setup 01," our focus is on these liquidity areas and stop hunts that form in Fair Value Gaps (FVGs). Trading within FVGs, combined with confirmations from "Hunts" and "Sweeps," can enhance trader performance.

🔵 How to Use

The presence of Fair Value Gaps (FVGs) in the market indicates rapid, powerful movements likely caused by the influx of smart money. When the price returns to these levels, a market reaction is expected.

Combining this with the complex and deceptive behavior of smart money—such as "Liquidity Sweeps" and "Stop Hunts"—forms an ICT-based price action setup that we expect to perform well.

Components of "ICT Setup 01" :

● Fair Value Gap (FVG)

● Premium and Discount

● Hunts / Sweeps

Whenever the price returns to an FVG area and reacts in such a way that only the wicks of the candles remain in the area and the candle bodies are outside the FVG, the first condition for creating the setup is met.